supplementary chapter recording transactions in...

TRANSCRIPT

May 1995

SUPPLEMENTARY CHAPTER

RECORDING TRANSACTIONS IN A JOB COSTING SYSTEM

CONTENTS

1. INTRODUCTION.......................................................................................................... 1

1.1. THE ACCOUNTING EQUATION........................................................................................ 11.2. REPORTING PROFIT..................................................................................................... 31.3. THE MATCHING, OR ACCRUALS, CONCEPT ....................................................................... 31.4. THE PRUDENCE CONCEPT............................................................................................. 41.5. FINANCIAL STATEMENTS ............................................................................................. 41.6. DOUBLE ENTRY BOOKKEEPING: RECORDING IN LEDGER ACCOUNTS....................................... 5

2. MANAGEMENT ACCOUNTING COSTS AND REVENUES IN LEDGER ACCOUNTS...... 7

3. THE FLOW OF ENTRIES IN A JOB COSTING SYSTEM................................................ 9

3.1. MATERIALS INVENTORY .............................................................................................. 93.2. WAGES .................................................................................................................... 93.3. PRODUCTION OVERHEADS............................................................................................ 93.4. COMPLETION OF WORK-IN-PROGRESS............................................................................ 103.5. ADMINISTRATION AND SELLING .................................................................................. 103.6. REVENUE ............................................................................................................... 10

4. RECORDING TRANSACTIONS FOR A JOB COSTING SYSTEM ................................. 10

4.1. ACQUISITION OF INVENTORY: DIRECT MATERIALS ......................................................... 114.2. ACQUISITION OF INVENTORY: INDIRECT MATERIALS....................................................... 114.3. RETURN OF INVENTORY TO SUPPLIER............................................................................ 114.4. CONVERTING RAW MATERIALS INTO WORK-IN-PROGRESS: DIRECT MATERIALS..................... 114.5. TREATMENT OF INDIRECT MATERIALS .......................................................................... 124.6. PAYING THE WAGES.................................................................................................. 124.7. PAYMENT FOR PRODUCTION OVERHEAD COSTS............................................................... 124.8. RECORDING INDIRECT LABOUR AS A PRODUCTION OVERHEAD COST .................................... 134.9. COMPLETING THE WORK-IN-PROGRESS ACCOUNT: DIRECT LABOUR.................................... 134.10. TAKING PRODUCTION OVERHEADS TO THE WORK-IN-PROGRESS ACCOUNT........................... 134.11. TRANSFERRING WORK-IN-PROGRESS TO FINISHED GOODS................................................ 144.12. SALE OF GOODS...................................................................................................... 14

5. THE USE OF CONTROL ACCOUNTS AND INTEGRATION WITH THE FINANCIALACCOUNTS ................................................................................................................... 16

6. PRACTICAL EXAMPLE OF THE USE OF CONTROL ACCOUNTS (TOTAL ACCOUNTS)...................................................................................................................................... 16

6.1. ACQUISITION OF INVENTORY: DIRECT AND INDIRECT MATERIALS (FIGURE 9)...................... 186.2. WAGES: DIRECT AND INDIRECT COSTS (FIGURE 10)......................................................... 216.3. PRODUCTION OVERHEAD (FIGURE 11)........................................................................... 236.4. WORK-IN- PROGRESS (FIGURE 12)................................................................................ 266.5. FINISHED GOODS INVENTORY (FIGURE 13)..................................................................... 27

7. ILLUSTRATION OF CONTRACT ACCOUNTING........................................................ 28

8. SUMMARY: ACCOUNTING RECORDS IN A JOB COSTING SYSTEM......................... 34

masuppl.doc 02/10/02 1

SUPPLEMENTARY CHAPTER

RECORDING TRANSACTIONS IN A JOB COSTING SYSTEM

LEARNING OBJECTIVES:

This chapter is supplementary to Chapter 19 of the combined text book (or Chapter2 of the stand-alone Management Accounting: An Introduction. After studying thischapter you should be able to:

1. Prepare ledger accounts to record transactions contributing to work-in-progressand finished goods for a job costing system

2. Understand and prepare control accounts and supporting records

3. Prepare a contract ledger account

1. Introduction

In chapter 19 the elements of a job costing system (direct materials, direct labour andproduction overheads) were explained. This chapter shows how the bookkeepingsystem may be used to record transactions in respect of direct materials, direct labourand production overheads and to show how these contribute to the recording of work-in-progress, finished goods and cost of goods sold.

Chapter 2 of the Financial Accounting section of the combined text book containsseveral variations of the balance sheet equation. The rules of bookkeeping areexplained in the supplement to that chapter. If you have read that chapter or you havea similar working knowledge of the accounting equation and basic principles ofaccounting statements, you can proceed directly to section 2 of this paper.

If you have not studied the Financial Accounting section of the combined text bookand who are meeting accounting for the first time, you should read the rest of thissection. In 1.1 you will find the accounting equation, extended to a profit equation in1.2. The matching concept is described in 1.3 and the prudence concept in section1.4. The main financial statements are described in 1.5, followed by the rules ofbookkeeping in 1.6.

1.1. The accounting equation

Those who manage a business need a full understanding and knowledge of theresources available to the business and the obligations of the business to those outsideit. They will also have to be confident that the business has an adequate flow of cashto support the continuation of the business. Accounting has traditionally applied theterm assets to the resources available to the business and has applied the termliabilities to the obligations of the business to persons other than the owner.

masuppl.doc 02/10/02 2

The owners of the business have a claim to the resources of the business after all otherobligations have been satisfied. This is called the ownership interest or the equityinterest. From time to time the managers of a business must show the owners how theoperation of the business is increasing or decreasing the ownership interest. A textbook on financial reporting will contain a substantial section on accounting aspects ofthe ownership interest. A text book on management accounting concentrates on themanagement of the assets and liabilities. Assets and liabilities are reported in afinancial statement called a balance sheet. The balance sheet is a statement of thefinancial position of the entity at a particular point in time. It may be described by avery simple equation.

Assets minus Liabilities equal Ownership interest

The ownership interest is the residual claim after liabilities to third parties have beensatisfied. The equation expressed in this form emphasises that residual aspect.

Another way of thinking about an equation is to imagine a see-saw on which twocontainers are balanced. In one container are the assets minus liabilities. In the otheris the ownership claim.

A - L Own

If anything happens to disturb the assets then the see-saw will fall out of balanceunless some matching disturbance is applied to the ownership interest. If anythinghappens to disturb the liabilities then the see-saw will fall out of balance unless somematching disturbance is applied to the ownership interest. If a disturbance applied toan asset is applied equally to a liability then the see-saw will remain in balance.

The ownership interest will increase if assets grow (provided liabilities do not growfaster). Achieving that growth is an essential skill of management. The ownershipinterest will increase if capital (cash or other assets) is contributed by the owner and itwill decrease if capital is withdrawn by the owner. Those actions of the owner are notin the control of management. Consequently this book concentrates on the activitiesof making use of assets and controlling liabilities. The words revenue and expenseare used to describe the results of actions which increase or decrease the ownershipinterest through the management of assets and liabilities

Change inownership interest

equalsCapital contributed/withdrawn by the ownerplus revenueminus expenses

masuppl.doc 02/10/02 3

The difference between revenue and expenses is more familiarly known as profit. Soa further subdivision of the basic equation is:

Profit equals revenue minus expenses

1.2. Reporting profit

An expense is caused by a transaction or event arising during the operations of thebusiness which causes a decrease in the ownership interest. It could be due to anoutflow or depletion of assets such as cash, trading stock, or fixed assets. It could bedue to a liability being incurred without a matching asset being acquired.

Revenue is created by a transaction or event arising during the operations of thebusiness which causes an increase in the ownership interest. It could be due to anincrease in cash or debtors, received in exchange for goods or services. Depending onthe nature of the business, revenue may be described as sales, turnover, fees,commission, royalties or rent.

Definition

Revenue is created by a transaction or event arising during the ordinary activities ofthe business which causes an increase in the ownership interest

An expense is caused by a transaction or event arising during the ordinary activities ofthe business which causes a decrease in the ownership interest

In management accounting it is common to use the word cost rather than expense,which is more commonly encountered in financial accounting. For the purposes ofthis book the word cost may be taken as equivalent to expense. Financial accountingtakes a broad view in deciding the categories of expense (e.g. selling expense,administrative expense). Management accounting delves much deeper into thevarious types of cost (e.g. selling expense is subdivided into costs of commission paidto sales staff, costs of travel in selling goods, costs of paperwork in recording ordersand sales, and costs of goods or services rejected by customers).

1.3. The matching, or accruals, concept

One very important aspect of accounting practice is that it is based on the idea thatcosts of any period should be matched against the sales which have been earnedthrough incurring those costs. When a product is manufactured using electricity, thecost measured should include the cost of electricity used for that item. However, the

masuppl.doc 02/10/02 4

electricity may not be paid for until some time later. So the amount of cash paid atone point in time will relate to the use of electricity in an earlier period.

The matching concept of accounting (also called the accruals concept) requires themanagement of a business to estimate the cost of resources used during a period inproducing the goods or services of the period. Returning to the electricity example,management would be expected to keep records of electricity consumed and toestimate the costs from that information. That cost would appear in a profit and lossaccount, matching the sales created during the period. The cash payment made to theelectricity supplier would be reported separately in a cash flow statement.

1.4. The prudence concept

The preparers of financial statements have to contend with uncertainty surroundingmany events and circumstances. The existence of uncertainties is recognised by thedisclosure of their nature and extent and by the exercise of prudence in thepreparation of the financial statements. Prudence means that there will be a degree ofcaution in the exercise of the judgments needed in making estimates. In particularthere will be a wish to ensure that income or assets are not overstated and thatexpenses or liabilities are not understated. The need for prudence should not,however, be regarded as justification for deliberate understatement of assets revenueand deliberate overstatement of liabilities and expenses. That would lead to asituation which was not reliable. Take as an example the costs of repair work lastingover more than one accounting period. It might be argued as prudent to report all therepair cost in the first period but that would give a wrong impression of the cost ofrepairs if the activity is in fact spread over the two periods. One example of theapplication of prudence in this text is the reporting of profit on a partly-completedcontract. A portion of profit is reported in order to reflect the economic activity of theperiod and to apply the matching concept, but some portion of profit is kept back untila later period as a prudent precaution against unforseen events.

1.5. Financial statements

The various financial statements produced by enterprises for the owners and otherexternal users are derived from the accounting equation. There is a view that thereare three purposes of external financial reporting, in producing information about thefinancial position, performance and financial adaptability of the enterprise. The threemost familiar primary financial statements, and their respective purposes, are:

Primary financial statement forexternal users

Purpose is to report Main contents

Balance sheet financial position assets, liabilities,ownership interest

masuppl.doc 02/10/02 5

Profit and loss account performance revenue (also calledturnover or sales)expenses (also calledcosts), profit for period

Cash flow statements financial adaptabilityand ability to meetneed for cash

cash flow in and cashflow out, cash positionat end of period

These are the financial statements produced by management when reporting to theexternal users of accounting information. Management uses similar financialstatements for internal purposes but designed to provide much more information.This text book will show examples in the subsequent chapters. If you have studiedfinancial accounting previously, you will find that management accounting reportslook quite different because they are produced for different purposes. Those differentpurposes relate to the variety of functions which management carries out. Thesefunctions are described in chapter 16 (chapter 1).

1.6. Double entry bookkeeping: recording in ledger accounts

The double entry system of bookkeeping records business transactions in ledgeraccounts. It makes use of the fact that there are two aspects to every transaction whenanalysed in terms of the accounting equation.

A ledger account accumulates the increases and reductions in either a category ofbusiness activities such as sales or in dealings with individual customers andsuppliers.

Ledger accounts may be subdivided. Sales could be subdivided into home sales andexport sales. Separate ledger accounts might be kept for each type of fixed asset, e.g.buildings and machinery. The ledger account for machinery might be subdivided asoffice machinery and production machinery.

Ledger accounts for rent, business rates and property insurance might be keptseparately or the business might instead choose to keep one ledger account to recordtransactions in all of these items, giving them the collective name administrativeexpenses. The decision would depend on the number of transactions in an accountingperiod and on whether it was useful to have separate records.

The managers of the business have discretion to combine or subdivide ledgeraccounts to suit the information requirements of the business concerned.

Before entries are made in ledger accounts, the double entry system of bookkeepingassigns to each aspect of a business transaction a debit or a credit notation, based onthe analysis of the transaction using the accounting equation.

masuppl.doc 02/10/02 6

In its simplest form the accounting equation is stated as:

Assets minus Liabilities equal Ownership interest

To derive the debit and credit rules it is preferable to rearrange the equation so there isno minus sign.

Assets equal Liabilities plus Ownership interest

There are three elements to the equation and each one of these elements may eitherincrease or decrease as a result of a transaction or event. The six possibilities are setout in Figure 1.

Figure 1 Combinations of increases and decreases of the main elements oftransactions

Left-hand side of the equationAssets Increase DecreaseRight-hand side of the equationLiabilities Decrease IncreaseOwnership interest Decrease Increase

The double entry bookkeeping system uses this classification (which preserves thesymmetry of the equation) to distinguish debit and credit entries as shown in Figure 2.

Figure 2 Rules of debit and credit for ledger entries, basic accounting equation

DEBITENTRIES IN ALEDGERACCOUNT

CREDITENTRIES IN ALEDGERACCOUNT

Left-hand side of the equationAsset Increase DecreaseRight-hand side of the equationLiability Decrease IncreaseOwnership interest Decrease Increase

It was shown in the main body of the chapter that the ownership interest may beincreased by:

Earning revenueNew capital contributed by the owner

masuppl.doc 02/10/02 7

and the ownership interest may be decreased by:

Incurring expensesCapital withdrawn by the owner.

So the 'ownership interest' section of Figure 2 may be expanded as shown Figure 3.

Figure 3 Rules of debit and credit for ledger entries, distinguishing differentaspects of ownership interest

DEBITENTRIES INA LEDGERACCOUNT

CREDITENTRIES IN ALEDGERACCOUNT

Left-hand side of the equationAsset Increase DecreaseRight-hand side of the equationLiability Decrease IncreaseOwnership interest Expense Revenue

Capitalwithdrawn

Capitalcontributed

That is all you ever have to know about the rules of bookkeeping. All the rest can bereasoned from this table. For any transaction there will be two aspects. (If you findthere are more than two, the transaction needs breaking down into simpler steps). Foreach aspect there will be a ledger account. Taking each aspect in turn you askyourself:

“Is this an asset, a liability, or an aspect of the ownership interest?

Then you ask yourself

“Is it an increase or a decrease?”

2. Management accounting costs and revenues in ledger accounts

We know that in financial accounting the following rules apply for debit and creditentries in the ledger account:

Type of account Debit entries Credit entriesExpense account Increase in expense Decrease in expenseRevenue account Decrease in revenue Increase in revenue

masuppl.doc 02/10/02 8

In management accounting the term "cost" is used more frequently than "expense",which is mainly found in financial accounting. Another difference is that, inmanagement accounting, costs tend to move from one ledger account to another in amanner which reflects the physical activity of the enterprise. Financial accounting, onthe other hand, is concerned more with the nature of the expense. In this chapter youwill see a more intricate flow of costs before they reach the profit and loss accountwhich is intended to meet the needs of management accounting. Changing the namefrom "expense" to "cost", and allowing for the flow of costs around the ledger. Figure4 provides a useful summary of the basic approach to recording cost transactions. Incost accounting records there are frequently transfers to and from ledger accounts,reflecting the flow of costs through the accounting system.

Figure 4 Debit and credit entries for transactions in a ledger account for costs.

Type of account Debit entries Credit entries

Cost accountIncrease in cost Decrease in cost

Transfer of cost fromanother cost account

Transfer of cost toanother cost account

This chapter explains first of all the relationships among various ledger accounts in ajob costing system. Figure 5 contains the basic requirements to build up a minimumset of ledger accounts, sufficient for management accounting purposes but not over-elaborate. The application of this simple system is illustrated in a practical example(figures 6 and 7). The need for control accounts and subsidiary records is thenexplained and a further practical example is presented which elaborates on the firstexample, showing the use of control accounts. Finally a contract account, as a veryspecific form of job costing, is explained and illustrated.

There are no new principles involved in creating ledger accounts to record costtransactions for management accounting purposes. However, there is a need for muchmore detailed analysis of transactions and so there is a need for more ledger accountsthan were shown in the financial accounting section of this book.

There is an important question in how to keep track of both the financial accountingand the management accounting information in the ledger system. Some smallbusinesses may prefer to keep their financial accounting ledger separately from thecost accounting records and have two separate sets of ledger accounts for the purpose.However, most larger businesses, especially where a computer is in use, will integratethe cost accounting ledger accounts with the financial accounting records. Thischapter will concentrate on the integrated approach.

The choice of headings used in ledger accounts for financial accounting purposes is tosome extent constrained by the legislative regulations applied to external financialreporting. Those constraints are not present in management accounting so there are

masuppl.doc 02/10/02 9

opportunities to choose the number and type of ledger accounts which best serve themanagement needs.

3. The flow of entries in a job costing system

This description follows transactions through Figure 5 by reference to the letters usedto label each ledger account. The diagram is based on a situation where materials areacquired on credit whilst wages are paid in cash. It also assumes that all overheadsare paid for in cash. For completeness, it also shows the recording of revenue in theprofit and loss account.

Figure 5 Insert here

which is on a separate file called MAFIG2.DOC]

3.1. Materials inventory

When inventory is acquired an asset is created, shown by a debit entry in theinventory account (a). In this instance the inventory has been purchased on creditterms, shown by a credit entry in the account for trade creditors (a).

When direct materials are issued to production, they cease to be part of the asset ofinventory and are transferred to the asset of work-in-progress (d). Some of thematerials acquired may be indirect materials (e), which are transferred to theproduction overhead account (e). All production overhead costs are collectedtogether before being transferred to work-in-progress using a suitable overhead costrate.

3.2. Wages

In the situation where the wages are paid immediately from the bank account, anexpense is incurred, so there is a debit entry in the wages account (b). The asset ofcash is reduced, recorded as a credit entry (b).

The wages are then subdivided for cost accounting purposes into direct labour andindirect labour. The direct labour (f) is transferred to the work-in-progress accountwhile the indirect labour(g) is transferred to the production overhead account.Detailed job cost records show the amount of direct labour time spent on each job.

3.3. Production overheads

Production overhead costs incurred as a result of cash payments are debited as costsin the production overhead account (c). There they join the production overhead coststransferred from other ledger accounts (e) and (g). Detailed job cost records willshow the amount of time that employees have worked on the job, causing overhead

masuppl.doc 02/10/02 10

costs to be incurred. This information will be sufficient to authorise transfers fromthe production overhead account to the work-in-progress account (h). All productionoverheads (h) are then transferred to the work-in-progress account so that work-inprogress now contains the prime cost (direct materials and direct labour) and all theproduction overhead costs.

3.4. Completion of work-in-progress

When work-in-progress is completed it becomes another asset, finished goods. Thecompleted work-in-progress (j) is transferred to finished goods. When the finishedgoods are sold they are transferred to the cost of sales account (k) and from there tothe profit and loss account (l) which is produced for management accountingpurposes.

3.5. Administration and selling

There are other overhead costs incurred, such as administration and selling costs,which are not part of the production cost. They are credited in the cash account (m),showing a reduction in the asset of cash, and are debited as expenses in a separateaccount for administration and selling overheads. From there these administrationand selling overhead costs are transferred to profit and loss account (n).

3.6. Revenue

Revenue is created for the enterprise by selling goods on credit. The increase inrevenue is credited in the sales account (o) while the increase in the asset of debtors isrecorded as a debit in the debtors' control account (o). Finally the revenue istransferred from the sales account to the profit and loss account (p).

4. Recording transactions for a job costing system

The general scheme outlined in Figure 5 may now be applied to a practical example,the transactions for which are set out in Figure 6. These transactions relate to workundertaken by Specialprint, a company which prints novelty stationery to be sold to achain of retail stores. The company has only one customer for this novelty stationery.

Figure 6 Specialprint - Transactions to be recorded for the month of June

1 June Bought 60 rolls of paper on credit from supplier, invoiced pricebeing £180,000.

1 June Bought inks, glue and dyes, cost £25,000 paid in cash.2 June Returned to supplier one roll, damaged in transit, £2,500.3 June Rolls of paper issued to printing department, cost £120,000.4 June Issued half of inks, glues and dyes to printing department, £12,500.14 June Paid printing employees' wages £8,000.14 June Paid maintenance wages £250.

masuppl.doc 02/10/02 11

16 June Paid rent, rates and electricity in respect of printing, £14,000, incash.

28 June Paid printing employees' wages £8,000.28 June Paid maintenance wages £250.30 June Transferred printed stationery to finished goods inventory, valued at

cost of £160,000.30 June Sold stationery to customer on credit, cost of goods sold being

£152,000.

Each transaction is now analysed to determine the relevant journal entry. A briefexplanation is provided for each entry. The resulting ledger accounts are presented inFigure 7.

4.1. Acquisition of inventory: Direct materials

In purchasing the rolls of paper, the business acquires an asset, shown by a debit entryin the ledger account for materials inventory. In taking credit from the supplier itincurs a liability, shown by a credit entry in the ledger account for a trade creditor.

1 June Materials inventory Dr £180,000Trade creditor Cr £180,000

4.2. Acquisition of inventory: Indirect materials

In purchasing the inks, glue and dyes, the business acquires a further asset, shown bya debit entry in the ledger account for materials inventory. In exchange, the asset ofcash has diminished, shown by a credit entry in the cash account.

1 June Materials inventory Dr £25,000Cash Cr £25,000

4.3. Return of inventory to supplier

Returning the damaged roll of paper reduces the asset of materials inventory, shownby a credit entry, and reduces the liability to the trade creditor, shown by a debit entry.

2 June Trade creditor Dr £2,500Materials inventory Cr £2,500

4.4. Converting raw materials into work-in-progress: Direct materials

When the rolls of paper are issued from the stores to the printing department, theybecome a part of the work-in-progress of that department. Since this work-in-progress is expected to bring a benefit to the enterprise in the form of cash flows fromsales when it is eventually finished and sold, it meets the definition of an asset. The

masuppl.doc 02/10/02 12

increase in the asset of work-in-progress is shown by a debit entry, while the decreasein the inventory of materials is shown by a credit entry.

3 June Work-in-progress Dr £120,000Materials inventory Cr £120,000

4.5. Treatment of indirect materials

Inks, glue and dyes are indirect materials. The ledger recording for indirect materialsdiffers from that used for direct materials. The indirect cost is transferred to theproduction overhead account, to be accumulated with other indirect costs and latertransferred to work-in-progress as a global figure for production overhead. In thiscase only half of the indirect materials have been issued (£12,500), the rest remainingin inventory.

4 June Production overhead Dr £12,500Materials inventory Cr £12,500

4.6. Paying the wages

There are two amounts of direct labour costs paid during the period in respect of theprinting employees, and two amounts of indirect wages in respect of maintenance.For each amount the wages account is debited (because an expense has occurred) andthe cash account is credited because the asset of cash has decreased. At this point nodistinction is made between direct and indirect labour because they all form part ofthe total labour cost. That information is required for other purposes (such as theexternal financial reporting).

It will only be after analysis of the labour records for the period that an accuratesubdivision into direct and indirect costs may be made. Although it is assumed herethat all wages of printing employees are direct costs, it could be that enforced idletime through equipment failure would create an indirect cost. (For simplification inthis example, income taxes and employer's costs in relation to employees areomitted.)

14 June Wages Dr £8,000Cash Cr £8,000

14 June Wages Dr £250Cash Cr £250

28 June Wages Dr £8,000Cash Cr £8,000

28 June Wages Dr £250Cash Cr £250

4.7. Payment for production overhead costs

masuppl.doc 02/10/02 13

Rent, rates and electricity costs paid from cash in respect of printing are productionoverhead costs. They are debited to the cost of production overhead. There is a creditentry in the cash account in this case. (Overhead costs are also often incurred oncredit terms.)

16 June Production overhead Dr £14,000Cash Cr £14,000

4.8. Recording indirect labour as a production overhead cost

The indirect labour cost is treated similarly to the indirect materials. At the end of themonth the cost is transferred from wages to production overhead so that all overheadcosts are accumulated together.

30 June Production overhead Dr £500Wages Cr £500

4.9. Completing the work-in-progress account: Direct labour

The direct labour cost amounts to £16,000 and forms part of the prime cost of work-in-progress. At the end of the month a debit entry is made in the work-in-progressaccount because the direct labour cost is adding to the value of the asset of work-in-progress. A credit entry is made in the wages account because the cost previouslyrecorded there is now being transferred elsewhere.

30 June Work-in-progress Dr £16,000Labour cost Cr £16,000

In a computerised accounting system the transfer to the work-in-progress accountwould follow immediately on the payment of wages, so that there would be a debitentry in the wages account recording the cost, and a credit entry transferring it towork-in-progress, both on the same date. In a manual system, more of the transferentries may be left until the end of the month, when management reports are beingprepared.

4.10. Taking production overheads to the work-in-progress account

It may be seen from figure 4 that there is now a total of £27,000 debited to theproduction overhead ledger account. At the end of the month it is all transferred tothe work-in-progress account by a credit entry in the production overhead account(reducing the expense recorded there) and debiting the work-in-progress account(adding to the value of the asset).

30 June Work-in-progress Dr £27,000Production overhead Cr £27,000

masuppl.doc 02/10/02 14

This transfer will enable the value of work-in-progress to be shown at full cost at theend of the month.

4.11. Transferring work-in-progress to finished goods

As the asset of work-in-progress is completed, it changes into another asset, theinventory of finished goods. A credit entry removes the asset from work-in-progressand a debit entry records its new existence as the asset of finished goods.

30 June Finished goods inventory Dr £160,000Work-in-progress Cr £160,000

4.12. Sale of goods

When a sale is made to a customer, the asset of finished goods inventory istransformed into the expense of cost of goods sold. The expense is recorded bymaking a debit entry in the cost of goods sold account. The reduction in the asset isshown by a credit entry in the finished goods inventory account. Any balanceremaining on the finished goods inventory account represents unsold goods.

30 June Cost of goods sold Dr £152,000Finished goods inventory Cr £152,000

masuppl.doc 02/10/02 15

Figure 7 Specialprint - Ledger account entries

L1 Cash accountRef Debit Credit Balance

L £ £ £1 June Materials 3 25,000 25,00014 June Wages 4 8,000 33,00014 June Wages 4 250 33,25016 June Rent, Rates, etc 5 14,000 47,25028 June Wages 4 8,000 55,25028 June Wages 4 250 55,500

L2 Trade creditorRef Debit Credit Balance

L £ £ £1 June Materials 3 180,000 180,0002 June Materials returned 3 2,500 177,500

L3 Materials inventoryRef Debit Credit Balance

L £ £ £1 June Trade creditor, (paper rolls) 2 180,000 180,0001 June Cash (inks, glue, dyes) 1 25,000 205,0002 June Returned to supplier 2 2,500 202,5003 June Work-in-progress 6 120,000 82,5004 June Production overhead 5 12,500 70,000

L4 WagesRef Debit Credit Balance

L £ £ £14 June Cash 1 8,000 8,00014 June Cash 1 250 8,25028 June Cash 1 8,000 16,25028 June Cash 1 250 16,50030 June Production overhead 5 500 16,00030 June Work-in-progress 6 16,000 nil

L5 Production overheadRef Debit Credit Balance

L £ £ £4 June Materials inventory 3 12,500 12,50016 June Cash 1 14,000 26,50030 June Wages 4 500 27,00030 June Work-in-progress 6 27,000 nil

L6 Work-in-progressRef Debit Credit Balance

L £ £ £3 June Direct materials 3 120,000 120,00030 June Direct labour 4 16,000 136,00030 June Production overhead 5 27,000 163,000

masuppl.doc 02/10/02 16

30 June Finished goods 7 160,000 3,000

L7 Finished goods inventoryRef Debit Credit Balance

L £ £ £30 June Work-in-progress 7 160,000 160,00030 June Cost of goods sold 8 152,000 8,000

L8 Cost of goods soldRef Debit Credit Balance

L £ £ £30 June Finished goods 7 152,000 152,000

5. The use of control accounts and integration with the financial accounts

Figure 7 has shown the recording of a set of transactions in ledger accounts whichfollow the diagram outlined in Figure 5. Although it shows the basic rules ofbookkeeping applied to a set of transactions, it is not sufficiently detailed to be ofpractical use in management accounting. The company will need to have separateinformation about the different types of novelty stationery produced, the differenttypes of materials used in manufacture, the various labour resources used and therange of production overhead costs applied.

Where a business is complex and has large numbers of transactions, those transactionsare collected together in what are called 'control accounts' (also called 'total accounts'because they control the total transactions of the type being recorded). Secondaryrecords are available to show the detailed analysis of those control accounts.

It is this device of 'control accounts' which allows the management accounting recordsto be integrated with the financial accounting records. The main ledger contains thecontrol accounts, while the detailed information is recorded outside the main ledger.The control accounts are sufficiently aggregated to be of use for financial accountingpurposes where only the total costs of each main category are required.

The next section of this chapter explains the progress of costs through the controlaccounts in the main ledger until they reach the profit and loss account. It illustratesthe use of control accounts and subsidiary records by expanding on the examplecontained in Figure 6.

You will find that the accounts shown in diagram form in Figure 5 and in the practicalexample of Figure 7 will become the control ('total') accounts and that new, moredetailed, subsidiary records will be provided to support these control accounts.

6. Practical example of the use of control accounts (total accounts)

masuppl.doc 02/10/02 17

The use of control accounts and subsidiary records may be illustrated by returning tothe transactions of Figure 6 and the ledger accounts of Figure 7. Those ledgeraccounts are all control accounts (total accounts) because the total amount of eachtransaction was entered without any analysis into more detailed elements. Considernow the additional information contained in Figure 8, which will be used to preparethe subsidiary records supporting the control accounts.

In Figure 8 various symbols appear in the second column. These symbols are used inthe ledger accounts of figures 9 to 12 as an aid to identifying how the subsidiaryrecords match up to the items in the control accounts.

masuppl.doc 02/10/02 18

Figure 8 Additional information relating to the transactions set out in Figure 6.

1 June � The rolls of paper acquired consisted of two different grades. 40 rollswere of medium grade paper at a total cost of £100,000 and 20 rolls wereof high grade at a total cost of £80,000.

1 June ♣ The inks cost £9,000 while the glue cost £12,000 and the dyes £4,000.2 June ⊗ The roll of paper returned was of medium grade.3 June † 20 high grade rolls were issued, together with 16 medium grade rolls.

There were three separate jobs: references 601, 602 and 603. The highgrade rolls were all for job 601 (note paper); 12 medium grade rolls werefor job 602 (envelopes) and the remaining 4 medium grade rolls were forjob 603 (menu cards).

4 June ø Exactly half of each item of inks, glue and dyes was issued, for useacross all three jobs.

14 June ψ Wages were paid to 10 printing employees, each earning the sameamount.

14 June λ Maintenance wages were paid to one part-time maintenance officer.16 June ‡ Payment for rent was £8,000, rates £4,000 and electricity £2,000.28 June ϖ Wages were paid to the same 10 employees as on 14 June.28 June ϕ Maintenance wages were paid to the same maintenance officer as on 14

June.30 June ♥ Employee records show that

5 printing employees worked all month on job 601,3 printing employees worked on job 602 and2 printing employees worked on job 603.

30 June ξ It is company policy to allocate production overheads in proportion tolabour costs of each job.

30 June # Transferred to finished goods an amount of £160,000, in respect of jobs601 and 602, which were completed, together with the major part of job603. There remained some unfinished work-in-progress on one sectionof job 603, valued at £3,000.Separate finished goods records are maintained for note paper, envelopesand menu cards.

30 June ≈ The customer took delivery of all note paper and all envelopes but tookonly £7,600 of menu cards, leaving the rest to await completion of thefurther items still in progress.

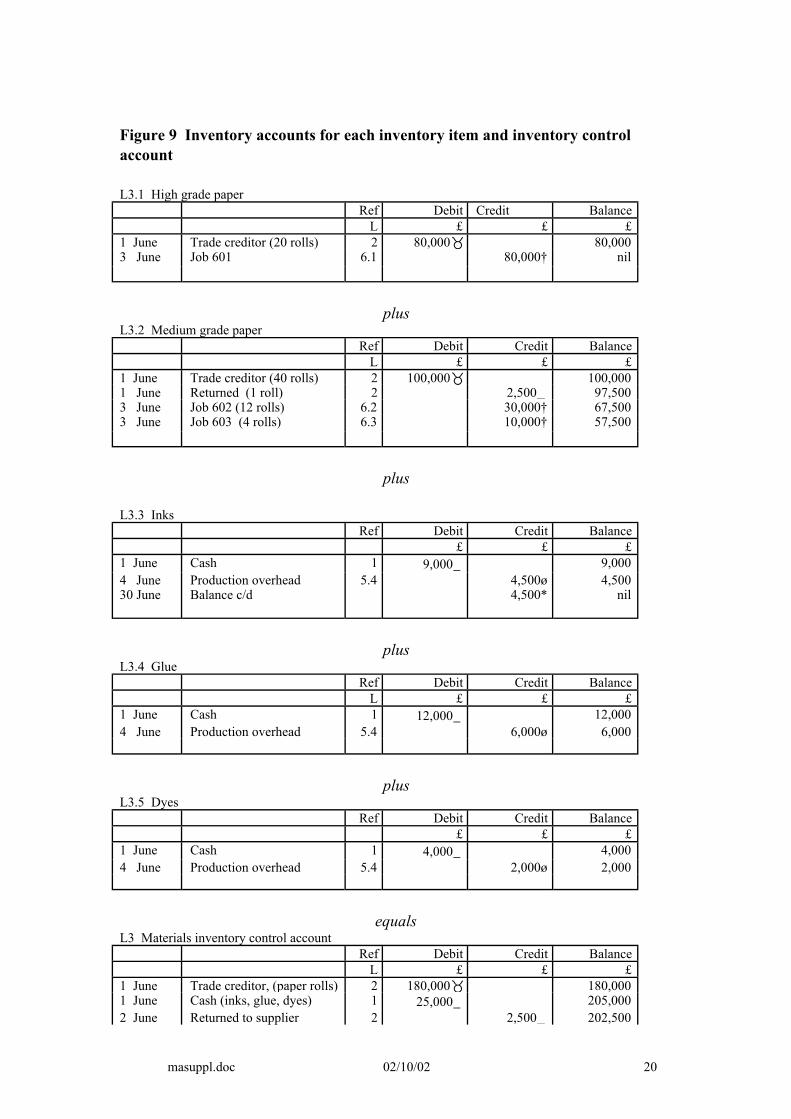

6.1. Acquisition of inventory: Direct and indirect materials (Figure 9)

For accurate control of stores it would be necessary to maintain a separate storesledger record for each type of material held. Five different types of material arementioned in Figure 8 and so five separate ledger accounts are shown in Figure 9.The separate debits and credits in each ledger account may be seen to equal the totalentries in the main ledger account for materials inventory, reproduced here from

masuppl.doc 02/10/02 19

Figure 7, and now renamed as the materials inventory control account (or totalaccount). Symbols to the right of each monetary amount show the items which,added together, are equal to the corresponding total in the control account.

masuppl.doc 02/10/02 20

Figure 9 Inventory accounts for each inventory item and inventory controlaccount

L3.1 High grade paperRef Debit Credit Balance

L £ £ £1 June Trade creditor (20 rolls) 2 80,000� 80,0003 June Job 601 6.1 80,000† nil

plusL3.2 Medium grade paper

Ref Debit Credit BalanceL £ £ £

1 June Trade creditor (40 rolls) 2 100,000� 100,0001 June Returned (1 roll) 2 2,500_ 97,5003 June Job 602 (12 rolls) 6.2 30,000† 67,5003 June Job 603 (4 rolls) 6.3 10,000† 57,500

plus

L3.3 InksRef Debit Credit Balance

£ £ £1 June Cash 1 9,000_ 9,0004 June Production overhead 5.4 4,500ø 4,50030 June Balance c/d 4,500* nil

plusL3.4 Glue

Ref Debit Credit BalanceL £ £ £

1 June Cash 1 12,000_ 12,0004 June Production overhead 5.4 6,000ø 6,000

plusL3.5 Dyes

Ref Debit Credit Balance£ £ £

1 June Cash 1 4,000_ 4,0004 June Production overhead 5.4 2,000ø 2,000

equalsL3 Materials inventory control account

Ref Debit Credit BalanceL £ £ £

1 June Trade creditor, (paper rolls) 2 180,000� 180,0001 June Cash (inks, glue, dyes) 1 25,000_ 205,0002 June Returned to supplier 2 2,500_ 202,500

masuppl.doc 02/10/02 21

3 June Work-in-progress 6 120,000† 82,5004 June Production overhead 5 12,500ø 70,000

6.2. Wages: Direct and indirect costs (Figure 10)

The wages account shown in Figure 7 becomes the wages control account which willbe supported by records for 10 individual employees, each debited with £800 on 14June and £800 on 28 June. There will be a separate employee record for themaintenance officer, debited with £250 on 14 June and £250 on 28 June. Transfersfrom the employee records will be to the various jobs on which each employee hasworked.

There will be ten separate employee records. Employees 1 to 5 work on job 601 sothe direct cost of their labour (£8,000) is transferred to job 601 at the end of themonth. Employees 6 to 8 work on job 602 so the direct cost of their labour (£4,800)is transferred to job 602 at the end of the month. Employees 9 and 10 work on job603 and the direct cost of their labour (£3,200) is transferred to job 603 at the end ofthe month.

The transfer from the maintenance officer's record will be to a record which collectsall indirect labour costs (which might include printing employee costs if they hadunproductive time on their time-sheets. That indirect labour record is one of thesubsidiary records supporting the production overhead control account.

The total of all the entries in each of the individual employee records equals the totalshown in the wages account of Figure 7, now renamed as the wages control account.

masuppl.doc 02/10/02 22

Figure 10 Wages accounts for each employee and wages control account

L4.1 Printing employee number 1Ref Debit Credit Balance

L £ £ £14 June Cash 1 800_ 1,60028 June Cash 1 800_ 1,60030 June Job 601 6.1 1,600_ nil

L4.2 Printing employee number 2Ref Debit Credit Balance

L £ £ £14 June Cash 1 800_ 1,60028 June Cash 1 800_ 1,60030 June Job 601 6.1 1,600_ nil

L4.3 Printing employee number 3Ref Debit Credit Balance

L £ £ £14 June Cash 1 800_ 1,60028 June Cash 1 800_ 1,60030 June Job 601 6.1 1,600_ nil

L4.4 Printing employee number 4Ref Debit Credit Balance

L £ £ £14 June Cash 1 800_ 1,60028 June Cash 1 800_ 1,60030 June Job 601 6.1 1,600_ nil

L4.5 Printing employee number 5Ref Debit Credit Balance

L £ £ £14 June Cash 1 800_ 1,60028 June Cash 1 800_ 1,60030 June Job 601 6.1 1,600_ nil

L4.6 Printing employee number 6Ref Debit Credit Balance

L £ £ £14 June Cash 1 800_ 1,60028 June Cash 1 800_ 1,60030 June Job 602 6.2 1,600_ nil

L4.7 Printing employee number 7Ref Debit Credit Balance

L £ £ £14 June Cash 1 800_ 1,600

masuppl.doc 02/10/02 23

28 June Cash 1 800_ 1,60030 June Job 602 6.2 1,600_ nil

L4.8 Printing employee number 8Ref Debit Credit Balance

L £ £ £14 June Cash 1 800_ 1,60028 June Cash 1 800_ 1,60030 June Job 602 6.2 1,600_ nil

L4.9 Printing employee number 9Ref Debit Credit Balance

L £ £ £14 June Cash 1 800_ 1,60028 June Cash 1 800_ 1,60030 June Job 603 6.3 1,600_ nil

L4.10 Printing employee number 10Ref Debit Credit Balance

£ £ £14 June Cash 1 800_ 1,60028 June Cash 1 800_ 1,60030 June Job 603 6.3 1,600_ nil

L4.11 Maintenance officerRef Debit Credit Balance

L £ £ £14 June Cash 1 250_ 25028 June Cash 1 250 _ 50030 June Indirect labour 5.5 500_ nil

L4 Wages control accountRef Debit Credit Balance

L £ £ £14 June Cash 1 8,000_ 8,000

14 June Cash 1 250_ 8,25028 June Cash 1 8,000_ 16,25028 June Cash 1 250_ 16,50030 June Work-in-progress 6 16,000_ 50030 June Production overhead 5 500_ nil

6.3. Production overhead (Figure 11)

The production overhead control account will be supported by one subsidiary recordfor each type of overhead cost. The payments on 16 June relate to rent, rates andelectricity, each of which will require a separate record. Additionally there are

masuppl.doc 02/10/02 24

overheads of indirect materials and indirect labour created by transfers from otherrecords.

We are told in Figure 8 that production overheads are allocated in proportion to thedirect labour costs of each job. The total direct labour cost for the period is £16,000and so for each item of production overhead the overhead cost rate must be calculatedas:

overhead cost rate (in £ per £ of direct labour) = overhead tcos

16 000,

For indirect material the calculations are slightly more complex. The total indirectmaterial cost transferred to production overhead is £12,500. The overhead cost rate istherefore calculated as:

£ ,

£ ,

12 500

16 000 = 78.125 pence per £ of direct labour

This rate is then applied to the amounts of direct labour already charged to each job(which was £8,000 for job 601, £4,800 for job 602 and £3,200 for job 603). Theresulting amounts are transferred from the indirect materials account to the relevantjob records.

For indirect labour the only item is the cost of the maintenance officer.

Adding together all these subsidiary records gives amounts equal to the totals in theproduction overhead control account. In the ledger accounts different symbols areshown to the right-hand side of each monetary amount as an indication of the itemswhich add to give the respective totals.

masuppl.doc 02/10/02 25

Figure 11 Production overhead accounts for each cost item, and productionoverhead control account

L5.1 Production overhead: RentOverhead cost rate = 25p per £ of direct labour

Ref Debit Credit BalanceL £ £ £

16 June Cash 1 8,000‡ 8,00030 June Job 601 6.1 4,000_ 4,000

Job 602 6.2 2,400_ 1,600Job 603 6.3 1,600_ nil

L5.2 Production overhead: RatesOverhead cost rate = 50p per £ of direct labour

Ref Debit Credit BalanceL £ £ £

16 June Cash 1 4,000‡ 4,00030 June Job 601 6.1 2,000_ 2,000

Job 602 6.2 1,200_ 800Job 603 6.3 800_ nil

L5.3 Production overhead: ElectricityOverhead cost rate = 12.5p per £ of direct labour

Ref Debit Credit BalanceL £ £ £

16 June Cash 1 2,000‡ 2,00030 June Job 601 6.1 1,000_ 1,000

Job 602 6.2 600_ 400Job 603 6.3 400_ nil

L5.4 Production overhead: Indirect materialOverhead cost rate =78.125p per £ of direct labour

Ref Debit Credit BalanceL £ £ £

4 June Ink 3.3 4,500ø 4,500Glue 3.4 6,000ø 10,500Dyes 3.5 2,000ø 12,500

30 June Job 601 6.1 6,250_ 6,250Job 602 6.2 3,750_ 2,500Job 603 6.3 2,500_ nil

L5.5 Production overhead: Indirect labourOverhead cost rate =3.125p per £ of direct labour

Ref Debit Credit BalanceL £ £ £

30 June Maintenance officer 4.11 500_ 500Job 601 6.1 250_ 250Job 602 6.2 150_ 100Job 603 6.3 100 _ nil

L5 Production overhead control account

masuppl.doc 02/10/02 26

Ref Debit Credit BalanceL £ £ £

4 June Materials inventory 3 12,500ø 12,50016 June Cash 1 14,000‡ 26,50030 June Wages 4 500_ 27,00030 June Work-in-progress 6 27,000_ nil

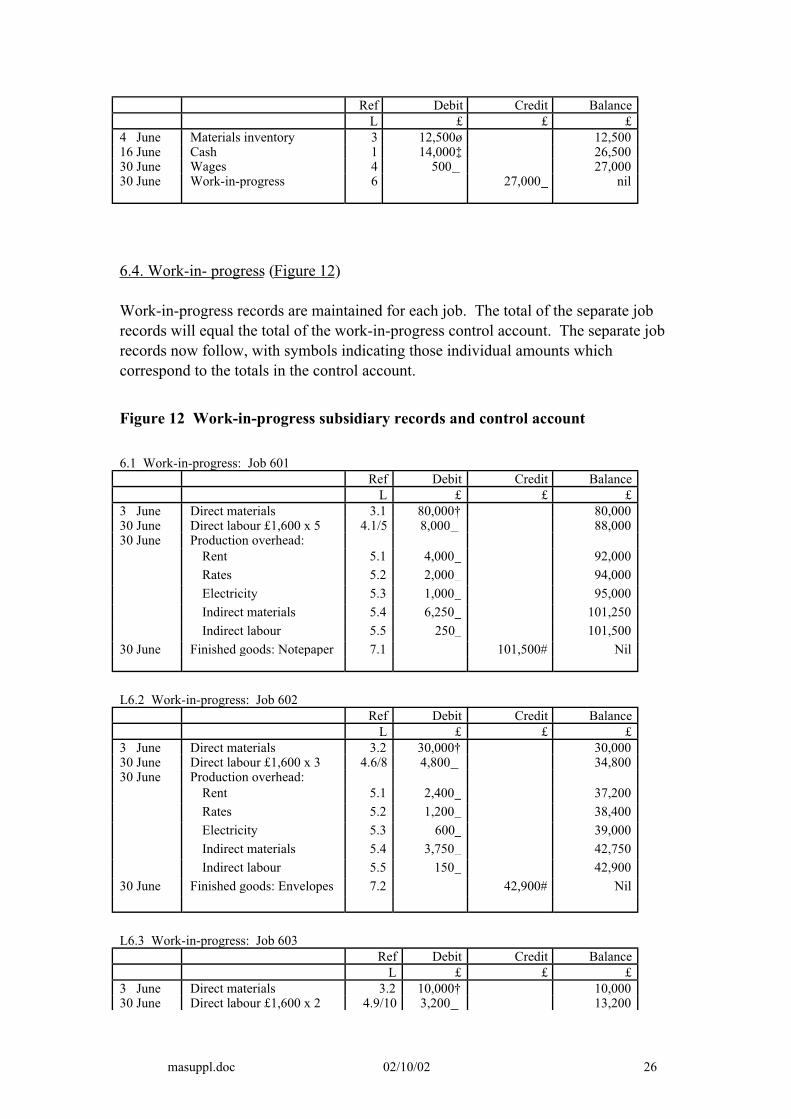

6.4. Work-in- progress (Figure 12)

Work-in-progress records are maintained for each job. The total of the separate jobrecords will equal the total of the work-in-progress control account. The separate jobrecords now follow, with symbols indicating those individual amounts whichcorrespond to the totals in the control account.

Figure 12 Work-in-progress subsidiary records and control account

6.1 Work-in-progress: Job 601Ref Debit Credit Balance

L £ £ £3 June Direct materials 3.1 80,000† 80,00030 June Direct labour £1,600 x 5 4.1/5 8,000_ 88,00030 June Production overhead:

Rent 5.1 4,000_ 92,000Rates 5.2 2,000_ 94,000Electricity 5.3 1,000_ 95,000Indirect materials 5.4 6,250_ 101,250Indirect labour 5.5 250_ 101,500

30 June Finished goods: Notepaper 7.1 101,500# Nil

L6.2 Work-in-progress: Job 602Ref Debit Credit Balance

L £ £ £3 June Direct materials 3.2 30,000† 30,00030 June Direct labour £1,600 x 3 4.6/8 4,800_ 34,80030 June Production overhead:

Rent 5.1 2,400_ 37,200Rates 5.2 1,200_ 38,400Electricity 5.3 600_ 39,000Indirect materials 5.4 3,750_ 42,750Indirect labour 5.5 150_ 42,900

30 June Finished goods: Envelopes 7.2 42,900# Nil

L6.3 Work-in-progress: Job 603Ref Debit Credit Balance

L £ £ £3 June Direct materials 3.2 10,000† 10,00030 June Direct labour £1,600 x 2 4.9/10 3,200_ 13,200

masuppl.doc 02/10/02 27

30 June Production overhead:Rent 5.1 1,600_ 14,800Rates 5.2 800_ 15,600Electricity 5.3 400_ 16,000Indirect materials 5.4 2,500_ 18,500Indirect labour 5.5 100_ 18,600

30 June Finished goods: Menus 7.3 15,600# 3,000

L6 Work-in-progress control accountRef Debit Credit Balance

L £ £ £3 June Direct materials 3 120,000† 120,00030 June Direct labour 5 16,000_ 136,00030 June Production overhead 6 27,000_ 163,00030 June Finished goods 7 160,000# 3,000

6.5. Finished goods inventory (Figure 13)

There must be a separate record for each line of finished goods, �the total of which isrepresented by the control account for finished goods. In this example there are threecategories of finished goods, namely notepaper (produced by job 601), envelopes(produced by job 602) and menu cards (produced by job 603).

There will be three different records for finished goods, which may be notepaper,envelopes or menu cards. The total of the three separate records is £160,000 whichequals the amount shown by the control account.

Figure 13 Finished goods subsidiary records and control account

L7.1 Finished goods inventory: NotepaperRef Debit Credit Balance

L £ £ £30 June Job 601 6.1 101,500# 101,50030 June Cost of goods sold 8.1 101,500_ nil

L7.2 Finished goods inventory: EnvelopesRef Debit Credit Balance

L £ £ £30 June Job 602 6.2 42,900# 42,90030 June Cost of goods sold 8.2 42,900_ nil

L7.3 Finished goods inventory: Menu cardsRef Debit Credit Balance

L £ £ £30 June Job 603 6.3 15,600# 15,60030 June Cost of goods sold 8.3 7,600_ 8,000

masuppl.doc 02/10/02 28

L7 Finished goods inventory control accountRef Debit Credit Balance

L £ £ £30 June Work-in-progress 6 160,000# 160,00030 June Cost of goods sold 8 152,000_ 8,000

Finally, the sale of goods to the customer is recognised by a transfer from the finishedgoods inventory to the Cost of goods sold account. In order to analyse each productline separately, there will be separate cost of goods sold accounts for each item (L8.1notepaper, L8.2 envelopes and L8.4 menu cards) and a cost of goods control accountto record the total amount (these are not illustrated here but resemble L8 shownearlier).

7. Illustration of contract accounting

[This section repeats sections 19.5 of the text book, showing the bookkeeping entries.Read section 19.4 again before starting on this bookkeeping section.]

The following pages set out the method of recording the transactions on a contractwhich lasts fifteen months in total and straddles two accounting periods. Figures 14and 15 deal with Year 1, while figures 16 and 17 deal with Year 2. The overall profiton the contract is presented in figure 18 and explained in terms of the profit reportedin the two separate reporting periods.

masuppl.doc 02/10/02 29

Figure 14 Office Builders Ltd: Contract for Western Office Complex

Office Builders Ltd undertook a contract to build the Western Office Complex for afixed price of £390,000 during the period from May Year 1 to July Year 2. Thistable sets out transactions up to the company's year end in December, Year 1.

Transactions during Year 1: £000's

May Materials purchased and delivered to site 87May Equipment delivered to site 11July Architect's fee 6June- Dec Materials issued from store 51May- Dec Wages paid on site 65Sept Payment to subcontractors 8May- Dec Direct costs 25Dec Head office charges 7

At the end of Year 1Dec Value of equipment remaining on site 7Dec Value of material remaining on site 32Dec Sales value of work certified 240Dec Amount due to subcontractors 5Dec Direct costs incurred but not yet paid 8

In respect of materials, £87,000 was purchased and £51,000 recorded as being issued.It might be expected that would leave £36,000 to be carried forward in store. Butonly £32,000 of materials were found at the end of the year, implying that £,4000-worth of materials has either been scrapped, because of some defect, or been removedwithout authority. In practice this would probably lead to an investigation of thecontrol system to discover why some materials have apparently disappeared. Theledger account entries do not show the detail of materials issued, but instead assumethat any material not contained in the physical check at the end of the year must havebeen used on the contract.

The equipment delivered to the site had a cost of £11,000 and an estimated value of£7,000 remaining at the end of the year. Depreciation is therefore £4,000.

The cost of work certified is the total of the costs incurred to date on that portion ofthe work approved by the architect. In this case the work has been certified at the endof the accounting year so there is no problem in deciding which costs to treat as costof goods sold and which to carry forward. If the work had been certified before theend of the financial year, any subsequent costs would also need to be carried forwardto be matched against future estimated sales value of work done.

masuppl.doc 02/10/02 30

An architect's fee would be quite common on contract work of this type. Provided thefee is specific to the project, it forms a direct cost which must be included in thecontract account.

All further expenditure of the period, such as wages, other direct costs and paymentsto subcontractors, are debited to the contract because they are, or will become, costsof the contract. At the end of the accounting period a count is taken of everythingremaining unused on the site and this count forms the basis for determining howmuch of the 'expense' should be carried forward as an asset for the next period.

Any costs not carried to the next period will become part of the cost of goods sold, tobe compared with the value of work certified in determining the profit for the period.Those managing an enterprise prudently might decide to hold in suspense some of theprofit calculated in the early stages of a project, as a precaution against unforeseenproblems later. Various formulae are in use for calculating this 'prudent amount' butthis example will take a 'rule of thumb' approach in suggesting that taking credit fortwo thirds of the profit calculated might be a reasonably prudent approach.

The transactions of Figure 14 are recorded in the ledger accounts of Figure 15,showing how the debit and credit entries appear in the contract account. There will,naturally be other ledger accounts, such as cash, creditors and the profit and lossaccount, where the other half of the journal entry may be found.

Figure 15 Office Builders Ltd: Transactions for Year 1 of Western OfficeComplex

Contract account

Current transactions section (Compare Exhibit 19.7 of Chapter 19)Ref Debit Credit Balance

£000’s £000’s £000’sMay Materials purchased 87 87May Equipment at cost 11 98May Architect's fee 6 104May-Dec Wages paid 65 169Sept Subcontractors 8 177May-Dec Direct costs 25 202Dec Head office charges 7 209Dec Due to subcontractor c/d 5 214Dec Direct costs incurred c/d 8 222Dec Materials on site c/d 32 190

Equipment on site c/d 7 183

The balance of £183,000 represents the cost of work certified for Year 1.

Profit and loss section (Compare Exhibit 19.8 of Chapter 19)Ref Debit Credit Balance

£000’s £000’s £000’s

masuppl.doc 02/10/02 31

Year 1Dec Cost of work certified b/d 183 183Dec Profit and loss account 38 221Dec Value of work certified 240 (19)

The credit balance of £19,000 is the portion of profit not reported in this period.

Balances brought forward sectionRef Debit Credit Balance

£ £ £Jan Equipment on site b/d 7 7

Material on site b/d 32 39Jan Due to subcontractor b/d 5 34Jan Due for direct costs b/d 8 26Jan Contract profit suspense b/d 19 5

In the profit and loss section for Year 1, Office Builders Ltd has shown the total profitof £57,000 in two components. Two thirds of this amount, £38,000, will be reportedin the profit and loss account for Year 1. One third of the amount, £19,000, will beheld in suspense to be carried forward to Year 2 in the ledger account and awaitrecognition there.

In the 'balance brought forward' section, two assets and two liabilities are also broughtforward. Equipment on site and material on site represent the items remaining in agood state for use in Year 2. There are liabilities to the subcontractor (£5,000) and topay for direct costs (£8,000), which must be settled early in Year 2.

To show the complete picture on the contract it is necessary to consider Year 2 also.Figure 16 sets out the transactions undertaken during Year 2.

masuppl.doc 02/10/02 32

Figure 16 Office Builders Ltd: Transactions of Western Office Complex forYear 2 (see Exhibit 19.9 of Chapter 19)

Transactions during Year 2:Jan Paid subcontractor amount due 5Jan Paid direct costs due at end of Year 1 8Feb Materials purchased and delivered to site 24June- Dec Materials issued from store 56May- Dec Wages paid on site 31Sept Payment to subcontractors 17May- Dec Direct costs 15Dec Head office charges 7At the end of Year 2Dec Value of equipment remaining on site nilDec Value of material remaining on site nilDec Sales value of work certified 150Dec Direct costs incurred but not yet paid 8

In Figure 17 are set out the ledger accounts for Year 2 of the contract to build theWestern Office Complex. The liabilities to pay for subcontractors and for direct costsare met by payment in January.

The profit in suspense (£19,000) which was brought down with other balances at thestart of Year 2 is taken to the profit and loss section of the contract account. Theprofit for Year 2 is equal to £9,000 (£150,000 value of work certified minus £141,000costs incurred for the period), but adding on the profit in suspense gives an overallprofit of £28,000 reported in Year 2. With the benefit of hindsight it probably was awise precaution to hold some of the Year 1 profit back from the reported profit and itwould appear possible that some of the costs incurred in Year 1 were providing abenefit to the work of Year 2.

At the end of Year 2 all profit can be reported since the outcome is certain. Inpractice there will be a further period during which the builder has responsibility toput right any defects. It could therefore be prudent to make provision again forpossible losses on repairs needed before the hand-over date, but that has not beendone in this illustration.

Although the profit is completed, the ledger account is kept open because there is stilla payment due to a subcontractor. Once that payment is made, the bookkeepingrecords for this contract may be terminated.

masuppl.doc 02/10/02 33

Figure 17 Office Builders Ltd: Transactions of Western Office Complex forYear 2 (see Exhibit 19.10 of Chapter 19).

Ref Debit Credit Balance£ £ £

Year 2Jan Equipment on site b/d 7 7Jan Material on site b/d 32 39Jan Due to subcontractor b/d 5 34Jan Due for direct costs b/d 8 26Jan Paid subcontractor 5 31

Jan Paid direct costs 8 39

Jan- July Materials purchased 24 63

Jan- July Wages paid 31 94

Mar Subcontractors 17 111

Jan-July Direct costs paid 15 126

July Head office charges 7 133

July Direct costs creditors c/d 8 141

July Cost of work certified c/d 141 nil

Profit and loss section (see Exhibit 19.11 Chapter 19)Ref Debit Credit Balance

£ £ £Jan Contract profit suspense

b/d19 19

July Sales value of workcertified

150 169

Dec Cost of work certified b/d 141 28Dec Profit and loss account 28 nil

masuppl.doc 02/10/02 34

Figures 14 to 17 have set out quite detailed illustrations of the recording of contractprofit and loss account. If ledger accounts are not required, this procedure may beregarded as a rather tedious process and it may be more convenient to move directlyto an overall statement of profit, as follows:

Figure 18 Statement of total contract profit (see Exhibit 19.12 of Chapter 19).

£000's £000'sContract price 390Direct costs Materials (87 + 24) 111 Labour (65 + 31) 96 Direct costs (25 + 8 + 15) 48 Payments to subcontractors (8 + 5 +17 + 8) 38 Depreciation of equipment 11 Architect's fee 6

310Indirect costs Head office charges (7 + 7) 14

324Total contract profit (reported as £38,000 in Year 1 and£28,000 in Year 2) 66

8. Summary: Accounting records in a job costing system

This chapter has set out, in a simplified manner, the use of debit and creditbookkeeping for recording the transactions of a business. It has shown how anintegrated system may serve the needs of both financial accounting and managementaccounting. The importance of control accounts has also been illustrated and.although a computerised system was not described, you should be able to imagine thetypes of accounts code systems which would be required to analyse the individualrecords. Finally the chapter considered contract accounts, which are a specific type ofjob costing record.

SELF-TESTING ON THE CHAPTER

1. An expense of £150 in respect of a gas account is paid in cash. What are thebookkeeping entries in the ledger?

2. How does a cost account relate to an expense account?

masuppl.doc 02/10/02 35

3. Why is there no definitive list of ledger account headings for managementaccounting purposes?

4. What is the purpose of the work-in-progress account and what types of entrieswould you expect to see there?

5. Why is the use of control accounts essential in both management accountingand financial accounting?

6. What is the purpose of a contract account and what types of entries would youexpect to see there?

7. The following list of transactions for a month is extracted from a trial balance.In which ledger accounts these figures be found?

£Purchases of raw materials 45,000Wages paid to production employees 16,000Salary of personnel manager 2,000Sales 65,000Heat and light expense paid 6,500

8. In a job costing system, the production department orders 16 components fromstore at a cost of £3 each, to be used on job 59. Explain how this transactionwill be recorded in a system where control accounts are in operation.

9. In a job costing system, an employee (A Jones) receives a weekly wage of£600. In week 29 this employee's time has been spent two-thirds on job 61and one-third on job 62. Explain how this transaction will be recorded in asystem where control accounts are in operation.

10. On 16 June, job 94 is finished at a total cost of £3,500. The job consisted ofprinting brochures for a supermarket advertising campaign. Explain how thistransaction will be recorded in a system where control accounts are inoperation and the printing of brochures is one of three production activities inthe business, all of which contribute to the inventory of finished goods.

11. The following transactions relate to a dairy, converting milk to cheese, for themonth of May. Prepare ledger accounts which record the transactions.

1 May Bought 600 drums of milk from supplier, invoiced price being£90,000

1 May Bought cartons, cost £6,000 paid in cash2 May Returned to supplier one drum damaged in transit, £1503 May 500 drums of milk issued to cheesemaking department, cost

£75,000

masuppl.doc 02/10/02 36

4 May Issued two thirds of cartons to cheesemaking department, £4,00014 May Paid cheesemakers' £3,00014 May Paid wages for cleaning and hygiene £60016 May Paid rent, rates and electricity in respect of printing, £8,000, in cash28 May Paid cheesemakers' wages £3,00028 May Paid wages for cleaning and hygiene £60030 May Transferred all production of cheese in cartons to finished goods

inventory. No work-in-progress at end of month.

Required

Prepare ledger accounts which record these transactions.

12.Bridge Builders Ltd undertook a contract to build a pedestrian footbridge for afixed price of £400,000 during the period from May Year 1 to July Year 2.This table sets out transactions up to the company's year end in December,Year 1.

Transactions during Year 1: £000's

May Materials purchased and delivered to site 91May Equipment delivered to site 14July Architect's fee 7June- Dec Materials issued from store 73May- Dec Wages paid on site 71Sept Payment to subcontractors 10May- Dec Direct costs 22Dec Head office charges 6

At the end of Year 1Dec Value of equipment remaining on site 9Dec Value of material remaining on site 15Dec Sales value of work certified 280Dec Amount due to subcontractors 3Dec Direct costs incurred but not yet paid 3

Required:

Prepare the contract ledger account for Year 1.