support mechanisms for cofiring secondary fuels mechanisms... · nrel national renewable energy...

TRANSCRIPT

Support mechanisms forcofiring secondary fuels

Nigel S Dong

CCC/211 ISBN 978-92-9029-531-0

December 2012

copyright © IEA Clean Coal Centre

Abstract

This report discusses the enabling and supporting mechanisms for coal/biomass cofiring in selectedcountries that have either considerable operational experience or potential in this technology. Itinvestigates Europe, the USA, Australia and China as case studies and discusses the main supportingincentives adopted in consideration of the specific characteristics of renewable energy markets and thegovernment’s position in clean energy and climate change in each of these countries. As such, thisreport provides not only a policy overview but also a collation of the measures adopted by thepolicymakers in each country to promote cofiring biomass in coal-fired power stations.

Acronyms and abbreviations

2 IEA CLEAN COAL CENTRE

AEEG Authority for Electricity and Gasc Euro cent¢ US centCCL Climate Change LevyCRS Center for Resource Solutions (USA)CDM Clean Development MechanismCFB circulating fluidised bedCHP combined heat and powerDECC Department of Energy and Climate Change (UK)EU ETS European Union Emission Trading SystemEEG Erneuerbare Energien GesetzFYP Five-Year Plan (China)GHG greenhouse gasGSE Gestore Servizi EnergeticiIRR internal rate of returnITC investment tax creditLGC Large-scale Generation CertificateMSW municipal solid wasteMtoe million tonnes of oil equivalentMYPP Multi-Year Programme PlanNREL National Renewable Energy LaboratoryPCC pulverised coal combustionPCT production tax creditpf pulverised fuelPURPA Public Utility Regulatory Policies ActREC Renewable Energy CertificateR&D research and developmentRD&D research, development and demonstrationRPS Renewable Portfolio StandardRO Renewable ObligationROC Renewable Obligation CertificateSDE Stimulering Duurzame EnergieSTC Small-scale Technology CertificateUS DOE Department of Energy (USA)

Contents

3Support mechanisms for cofiring secondary fuels

Acronyms and abbreviations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Contents. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

2 European Union . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 72.1 EU’s position on biomass energy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 72.2 Biomass resources and utilisation in Europe . . . . . . . . . . . . . . . . . . . . . . . . . . . . 72.3 Biomass cofiring in Europe . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 82.4 Support mechanisms for biomass cofiring in Europe . . . . . . . . . . . . . . . . . . . . . 8

2.4.1 Austria. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 92.4.2 Belgium. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 92.4.3 Denmark . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 102.4. 4 Finland . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 112.4.5 Germany . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 112.4.6 Italy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 122.4.7 The Netherlands . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 132.4.8 Sweden . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 132.4.9 United Kingdom . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

2.5 Summary & comments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

3 USA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 203.1 US energy and climate policies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 203.2 Biopower and biomass cofiring . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 213.3 US supporting mechanisms for biomass cofiring. . . . . . . . . . . . . . . . . . . . . . . . 21

3.3.1 PURPA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 213.3.2 Renewable Portfolio Standard . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 223.3.3 Voluntary green pricing programme. . . . . . . . . . . . . . . . . . . . . . . . . . . . 223.3.4 Renewable Energy Credit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 243.3.5 GHG offsets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 253.3.6 Biomass cofiring R&D initiative . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

3.4 Tax incentives ineligible for biomass cofiring with coal . . . . . . . . . . . . . . . . . . 263.5 Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

4 Australia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 284.1 Bioenergy in Australia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 284.2 Biomass resources in Australia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 294.3 Cofiring in Australia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 314.4 Enabling policy incentives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 324.5 Barriers to cofiring biomass in Australian coal-fired power stations . . . . . . . . . 334.6 Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

5 China. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 365.1 Coal dominance in China . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 365.2 China’s position in biomass power . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

5.2.1 Five-Year Plans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 375.2.2 Renewable Energy Law . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 385.2.3 Current status of biomass power . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

5.3 Biomass fuel resources . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 395.4 Coal-fired power generation in China . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 395.5 Market potential of biomass cofiring in China. . . . . . . . . . . . . . . . . . . . . . . . . . 415.6 Barriers to uptake of biomass cofiring . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 425.7 Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

6 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45

7 Reference . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

4 IEA CLEAN COAL CENTRE

1 Introduction

5Support mechanisms for cofiring secondary fuels

Worldwide, biomass, including ‘degradable’ wastes, are currently the largest sources of renewableenergy. The world’s total primary consumption of biomass reached 1225 million tonnes of oilequivalent (Mtoe) in 2008, and is expected to increase to nearly 2000 Mtoe in 2035 (WEO, 2010). Thesignificant increase is mainly driven by the perception that biomass is a ‘CO2-neutral’ energy resourceand its use produces only a small amount of net CO2 emissions resulting mainly from its growing andharvesting. Currently, more than 60% of biomass is used for traditional domestic cooking and heating,whilst new applications in more efficient modern processes are being developed notably in OECDcountries. Among those new applications, the largest market is industry where biomass is used toproduce steam and heat. The second largest market is power generation, followed by utilisation inproduction of liquid transport fuels. Looking to the future, the bulk of the increase in biomass demandbetween 2008 and 2035 is expected to come from the electric power sector and the transportationsector. The electric power sector, in particular, is expected to surpass other industries as the largestsource of demand for biomass (WEO, 2010).

Power generation using biomass is undertaken widely in two types of power plants: dedicated biomasspower plants (biomass as the only fuel) and existing power plants that combust both coal and biomass.Dedicated biomass power plants are based either on grate firing or fluidised bed combustion, hence theplant capacity is generally not very large. Firing biomass alone gives rise to issues in relation to biomasssupply and power plant performance such as reduction in efficiency and availability. Some of these issuescan be solved effectively if the biomass is cofired with coal in a larger-sized power plant. Currently, thetypical conversion efficiency for a dedicated biomass-fired power plant is 25% (HHV) (van Loo andKoppejan, 2008). In contrast, conventional subcritical pulverised coal fired power plants have a thermalefficiency in the range 33–39% (HHV) in OECD countries, while new state-of-the-art power plants boastat least 43% (HHV) (Nalbandian, 2008). Moreover, numerous cofiring trials have shown that the coal-fired power plant efficiency is not compromised when the cofired biomass fuel represents a modest shareof total energy input. As such, biomass/coal cofiring represents a more efficient use of biomass for powergeneration. At modest cofiring levels, the combustion of biomass does not lead to significant problems ofalkali-related high-temperature corrosion, slagging and fouling, which could severely affect the operationof dedicated biomass power plants (Fernando, 2005). Furthermore, biomass cofiring with coal requiresrelatively simple modification to power plants, so the capital costs are lower than those needed toconstruct a new dedicated plant (about 123–1235 US$/kW compared to 1975–3085 US$/kW for biomass-only) (IEA, 2008). Cofiring also offers the flexibility to cope with a temporary loss of biomass supply orshort-term biomass price volatility by increasing the share of coal in the fuel mix. Furthermore, cofiringcan reduce the pollutant emissions from coal-fired power plants; research has shown that, with cofiring, acoal plant’s SO2 and CO2 emissions can be reduced and its NOx emissions could also be reduceddepending on the biomass fuel used (Fernando, 2005).

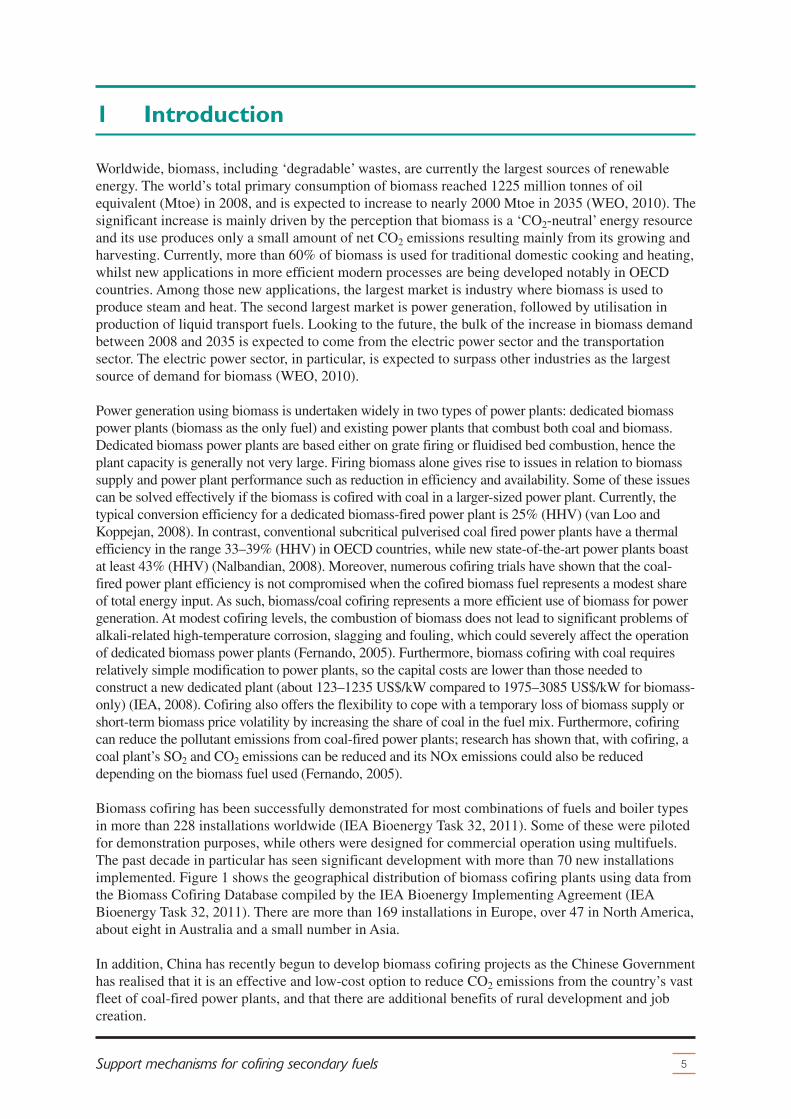

Biomass cofiring has been successfully demonstrated for most combinations of fuels and boiler typesin more than 228 installations worldwide (IEA Bioenergy Task 32, 2011). Some of these were pilotedfor demonstration purposes, while others were designed for commercial operation using multifuels.The past decade in particular has seen significant development with more than 70 new installationsimplemented. Figure 1 shows the geographical distribution of biomass cofiring plants using data fromthe Biomass Cofiring Database compiled by the IEA Bioenergy Implementing Agreement (IEABioenergy Task 32, 2011). There are more than 169 installations in Europe, over 47 in North America,about eight in Australia and a small number in Asia.

In addition, China has recently begun to develop biomass cofiring projects as the Chinese Governmenthas realised that it is an effective and low-cost option to reduce CO2 emissions from the country’s vastfleet of coal-fired power plants, and that there are additional benefits of rural development and jobcreation.

Typical power stations where cofiring isapplied are in the range from approximately50 MWe (a few units are between 5 MWe and50 MWe) to 700 MWe (IEA Bioenergy Task32, 2011). The majority are of pulverised coalcombustion (PCC) type with various firingmodes; bubbling and circulating fluidised bedboilers, cyclone boilers and stoker boilers arealso used. The proportion of biomass rangesfrom 1% to 20% on an energy input basis.Tests have been performed with everycommercially significant fuel type (lignite,subbituminous coal, bituminous coal, andopportunity fuels such as petroleum coke), andwith every major category of biomass(herbaceous and woody fuel types, residuesand energy crops). Experience with biomasscofiring in PCC boilers has demonstrated thatcofiring woody biomass resulted in a modestdecrease in boiler efficiency but no loss ofboiler capacity (Al-Mansour and Zuwala,2010). There are three basic cofiring concepts:direct cofiring (the majority of currentinstallations), indirect cofiring (limitedexperience) and parallel cofiring (littleexperience). All these concepts have alreadybeen implemented either on a demonstration ora fully commercial basis, and each with itsown particular merits and disadvantages.Technical details of these concepts can befound in previous IEA CCC reports (Davidson,1999; Fernando, 2002, 2005).

Differing from previous IEA CCC reports thatinvestigate the technological perspectives ofcofiring, this report focuses on the

supporting/enabling mechanisms for adopting biomass/coal cofiring as an initial, easy option forutilising biomass for power generation. It takes Europe, the USA, Australia and China as case-studyregions and investigates the main supporting incentives they have adopted in consideration of thespecific characteristics of renewable energy markets and the government’s position in clean energyand climate change in each of these regions.

6 IEA CLEAN COAL CENTRE

Introduction

Indonesia

Taiwan

Thailand

Australia

Austria

Belgium

Denmark

Finland

Germany

Italy

Netherlands

Norway

Spain

Sweden

UK

Canada

USA

211 85 1

9

78

27

67

12

15

18

7

40

Figure 1 The distribution of biomass cofiringinstallations worldwide (based on thedata extracted from the IEA BioenergyTask 32 – Biomass Cofiring Database)

2 European Union

7Support mechanisms for cofiring secondary fuels

This chapter first gives a brief review of the role of biomass in Europe’s energy strategy, biomassresources, biomass utilisation and technology status of biomass cofiring in Europe. A detaileddiscussion is then made on the incentives that main European countries adopt to support thedevelopment of biomass cofiring.

2.1 EU’s position on biomass energy

The European Union set a clear climate and energy agenda through its climate and energy legislativepackage adopted in 2009. This agenda mandates the EU to meet the following targets for 2020:greenhouse gas (GHG) emissions reduced by 20% below 1990 levels, or possibly by 30% if therewould be a clear global post-Kyoto commitment; 20% of the final energy consumption coming fromrenewable energy; primary energy consumption reduced by 20% below the ‘business-as-usual’projection for 2020. With a share in the range of 61–70% of EU-27 nations’ renewable energy mixsince 1990, biomass will be the most important renewable energy source to meet the EU’s 2020targets (AEBIOM, 2011). The concerns about climate change and dependency on fossil fuel importsare major drivers for promoting biomass energy in Europe; there are also expectations that promotionof biomass energy will stimulate rural development and create more jobs. The European BiomassAssociation projects that the gross inland consumption of biomass will more than double to 220 Mtoeby 2020 (AEBIOM, 2011).

2.2 Biomass resources and utilisation in Europe

In Europe, biomass comes mainly from three sources: agriculture, forestry and wastes. The forestryindustry is currently the largest source of biomass and will likely remain so at least over the nextdecade. Biomass wastes, such as degradable municipal solid waste (MSW) and sewage sludge/gas,have traditionally been the second most important supply. Energy recovery from wastes byincineration is practised intensively in Germany, France, Belgium, the Netherlands and NorthernEuropean countries such as Denmark and Sweden. Sweden has even gone as far as to set up wasteimport sectors. Agricultural byproducts may also become an important source of supply in the comingyears, but their production costs are higher. Energy crops have emerged and developed rapidly inrecent years in some regions. Energy crops are used primarily for production of liquid biofuels orbiogas; Germany is currently the largest producer of methanised biogas in Europe. Energy crops areexpected to supply a significant portion of the additional demand for bioenergy in 2020. In addition,biomass imports are expected to increase considerably, from 2 Mtoe in 2007 to around 20 Mtoe in2020, both in the form of transport biofuels (ethanol and biodiesel) and solid biomass (pellets andwood chips) (AEBIOM, 2011).

Currently, the majority (79%) of biomass is used for heat production with more than two thirdsproduced in combined heat and power (CHP) plants. Biomass-derived heat has a significant share ofthe heating markets in Denmark, Estonia, Finland, France, Germany, Italy, Latvia, Lithuania andSweden (EurObserv’ER, 2010a). Households are the biggest consumer of biomass-derived heat,followed by the industry and service sectors. The electric power sector is the second largest consumerof biomass. Biomass-based electricity accounted for 16–20% of total renewable electricity generatedin the EU during 2005-08. However, this represented only a small share of EU’s gross electricityproduction, in the range of 2–3% (AEBIOM, 2011; EurObserv’ER, 2010a).

2.3 Biomass cofiring in Europe

In Europe, there is great interest in cofiring biomass with coal in existing coal-fired boilers, andextensive experience has been gained. It is perceived by governments and industries as aneconomically sound short- and medium-term option for increasing renewable energy production whilereducing conventional pollutants and GHG emissions. A relatively modest capital investment,typically up to 50–300 US$/kW of biomass capacity, is needed to implement biomass cofiring as suchsystems can capitalise on the large investment and infrastructure associated with existing coal-basedpower systems. Power plant operating costs are, in most cases, higher for biomass than for coal, due

to the higher delivered cost of fuel,particularly if energy crops are used. Evenwhen the biomass is nominally free at thepoint of production, the costs associated withcollection, transportation, preparation, and on-site handling can increase the cost per unit ofenergy input to a point where it rivals, andoften exceeds, the cost of coal. Compared toalternative renewable energy sources, however,biomass cofiring is normally significantlycheaper, and cofiring has the advantage that itcan be implemented relatively quickly.

Europe is presently the world’s leader inbiomass cofiring implementation withexperience gained from more than169 installations (IEA Bioenergy Task 32,2011). As shown in Figure 2, theseinstallations, either as pilot tests or incommercial operation, are spread over elevencountries and are discussed briefly as follows.Most of the information is extracted from theIEA Bioenergy Task 32 – cofiring database,which was last updated in 2009.

2.4 Support mechanisms forbiomass cofiring inEurope

The current European policy and legislationenvironment is highly conducive to biomass

energy. The European Commission, through its overarching renewable energy policy – the EuropeanRenewable Energy Directive (2009/28/EC), demanded that each member state submit a nationalrenewable energy action plan in 2010. These plans, drawn up in view of Article 4 of the Directive,mandated the member states to present a renewable energy sector development programme to achievetheir respective contributions to EU targets: 20% of the final energy consumption coming fromrenewables and a mandatory 10% minimum target for the share of biofuel in transport fuelconsumption by 2020. The Directive also requires governments to design support mechanisms toachieve the targets cost-effectively and to establish the sustainability criteria.

Another EU-wide policy relating to biomass is the Combined Heat and Power Directive (2004/8/EC),which entered into force in February 2004. Combined Heat and Power (CHP) is an important avenuefor utilising biomass in Europe. This Directive requires member states to report the status of CHP

8 IEA CLEAN COAL CENTRE

European Union

Austria

Belgium

Denmark

Finland

Germany

Italy

Netherlands

Norway

Spain

Sweden

UK

5 1 9

78

27

7

612

15

18

Figure 2 The distribution of biomass cofiringplants in Europe (based on data fromthe IEA Bioenergy Task 32 – CofiringDatabase)

development, to remove barriers and create promotional measures, and to track the progress of highefficiency co-generation in energy markets.

The EU Emissions Trading System (EU ETS) also has a profound and widely-ranging impact on thedevelopment of renewable energy. A survey, participated in by 23 large European electric utilities,clearly illustrated the effect of ETS on decisions to implement biomass cofiring (New Energy Finance,2009). It was believed that a solid carbon price may promote the uptake of biomass cofiring anddedicated biomass generation. Nevertheless, respondents to the survey recognised that the carbonprice was only one factor amongst many when considering new investment in biomass cofiring.Renewable subsidies and fuel prices were often quoted as stronger determinants than carbon price inthe decision making.

In addition to the above EU-wide energy policies, each member state has designed its own incentivesand mechanisms to support uptake of biomass cofiring, which are discussed as follows.

2.4.1 Austria

Cofiring in Austria only takes place in industries where biomass fuels are available as residues, forexample in the pulp and paper industry (Cremers, 2009). The Austrian utility company VERBUNDcommercially cofired wood chips and bark (3% net calorific value) at its 284 MWth grate-firedSt Andrä power plant from 1995 to 2004, but the plant is now closed. VERBUND is still cofiring bark,wood chips and sawdust (accounting for 10 MW heat input) in the 330 MWth pulverised fuel (pf)Biococomb plant that burns polish hard coal. Biomass cofiring in circulating fluidised bed (CFB) andbubbling fluidised bed (BFB) combustion systems is applied commercially in several CHP plants inthe pulp and paper industry. A wide range of biomass fuels are used, including bark, wood residues,black liquor and sewage sludge.

Austria currently focuses on decentralised dedicated biomass application, while cofiring is not afavoured technology choice. The country’s main support mechanism is the renewable feed-in tariffs ,which are adjusted annually by law. The yearly budget is pre-allocated to different types of renewableenergy (30% to biomass, 30% to biogas, 30% to wind and 10% to photovoltaic and other renewableenergy sources). Within these categories, funds will be given on a ‘first come first served’ basis.However, the feed-in tariff is considered to be low for electricity from biomass cofiring plants, whichfor the use of untreated biomass (such as forest wood chips) amounts to 6.28 c/kWh of electricity. Thetariffs decrease by 25% in case of using saw mills byproducts and by 40% when demolition wood isused. Compared to the market price for base load electricity (around 4.80 c/kWh), it is clear that onlythe tariff for cofiring forest wood chips is usually higher than the market price of baseload electricityand that cofiring other biomass fuels would be hardly beneficial. Thus the support regime would haveto be changed appropriately if it was to attract interests in cofiring a variety of biomass fuels. There isalso an array of additional federal incentives for renewable heat, which consist mainly of investmentsubsidies.

2.4.2 Belgium

In Belgium, utilising biomass (including cofiring) to produce electricity took off after 2001 when thegovernment implemented the Green Certificate scheme (Cremers, 2009). At the end of 2007,Electrabel had renewable energy capacity of 402.7 MWe, of which biomass accounted for 78% (or314 MWe). Small-scale co-generation (CHP) units and biogas production from waste are responsiblefor a total of around 10 MWe. The remaining 300 MWe is produced by five power plants: the 100%wood pellets-fired Electrabel’s Les Awirs has an electricity output of 80 MWe with fuel demand of~1000 t/d; the four other power plants, including Ruien, Langrlo, Rodenhuize and Mol, cofire woodand olive residues.

9Support mechanisms for cofiring secondary fuels

European Union

Belgium has two sets of measures to support renewable electricity. The first measure is to setObligatory Targets for all electricity suppliers to supply a specific proportion of renewable electricity,for which the government guarantees minimum prices or ‘fall back prices’. Additionally, a greencertificate is attached to a unit of renewable electricity produced. In the country’s three regions(Wallonia, Flanders and Brussels-Capital), separate markets for green certificates have been created.In the Wallonia region, the Commission Wallonne pour l’Energie registered an average price of90 €/MWh per certificate during the first three months of 2006. In the Flanders, the average price wasaround 110 €/MWh per certificate during the first half of 2006. However, it is presently morebeneficial (financially) to pay penalties than to use the certificates due to the low penalty rates that areexpected to increase over time. Little trading of the green certificates has taken place so far. The otherset of measures is investment support for renewable energy projects. For example, renewable heatproduction is being supported by investment incentives in all three regions. The maximum level ofsupport is as high as 15% in the Wallonia region and 20% in the other two regions.

2.4.3 Denmark

Biomass has been used for electricity production in different sectors in Denmark since the 1980s(Cremers, 2009). The technologies used can be broadly divided into the following four categories:cofiring wood or straw in medium- to large-scale power plants, dedicated biomass-fired CHP plants(smaller boilers), dedicated biomass-fired boilers coupled to the steam cycle of a larger coal-firedpower plant, and pilot or demonstration plants for dedicated biomass utilisation at small scale (forexample, gasification and Stirling engines). Denmark has extensive experience in cofiring straw atvery high ratios in different combustion systems including grate-fired, one CFB drum type and fourpf-type units. Some plants, such as DONG Energy’s grate-fired Herningvœrket plant, Grenaa CFBco-generation plant, and Avedøre No 2 (pf boiler), operate in reverse cofiring mode, such that thebiomass accounts for 50–70% of total heat output. The secondary fuels may include coal, natural gasand fuel oil. Notably, the 365 MWe Avedøre No 2 unit features an ultra-supercritical boiler, whichfires wood pellets only up to 70% load and natural gas is used as supplementary fuel from 70% to100% load. An additional dedicated straw-fired boiler is installed, which accounts for 10% of thisunit’s total fuel consumption (or ~150 kt/y of straw). Another noteworthy cofiring plant is Vattenfall’sAmager No 1 (250 MWth), which can operate on either 100% pulverised coal or 100% wood pellets,using the same fuel feeding lines (not simultaneously, and only 90% capacity can be achieved instraw-only operation). Those cofiring plants have demonstrated great fuel flexibility. Extensive testsusing straw have clearly shown the limitations of the direct cofiring method.

The driving force behind biomass-based electricity development in Denmark has been a specificscheme set up by parliament (Folketinget) in the early 1990s. This scheme requires power plants touse a certain amount (1.4 Mt) of biomass annually. In 2008 the required proportion was increased byan additional 0.7 Mt/y as a result of a political agreement that lifted the legislative ban on increasedcoal use for power generation. More recently, a new supporting regime has been instigated, which setsan electricity price when using biomass for electricity generation at 150 DKK/MWh on top of thenormal spot electricity price (the hourly market price as set up by Nordpool) (Tørslev, 2012). AllDONG Energy plants have or will shortly convert to the new supporting regime.

Most power plants in Denmark are CHP plants. Biomass for heat production from central powerplants are exempted from energy tax. The normal energy tax for fossil fuels used for heat productionis approximately 60 DKK/GJ and regulated yearly with a price index (Tørslev, 2012). The realadvantage of using biomass in Denmark, is to use it in CHP plants; biomass used only for electricityproduction is seldom a viable option.

10 IEA CLEAN COAL CENTRE

European Union

2.4. 4 Finland

Finland has seen its bioenergy market develop from small-sized local utilisation of wood fuels tolarger-scale CHP production over the past several decades. It has significant experience in efficientuse of biomass for energy production in municipalities and at pulp and paper mills. Of the variousindustrial sectors, the paper and board making factories are the largest source of demand for heatgenerated by CHP and cofiring. Wood is the major biomass fuel, while peat, deemed as a biomass fuelin Finland, is an important indigenous fuel, covering ~10% of Finland’s energy consumption. The useof agricultural byproducts, waste and energy crops for energy production is limited in Finland. Inaddition to wood fuels, other cofired fuels include sludge, fuel oil, methanol, recovered fuel pellets,refuse-derived fuels, and, in some cases, biogas.

Finland has the largest number (>78) of biomass cofiring installations in the world, almost all ofwhich are in CHP plants and adopt direct cofiring. A noteworthy exception is the 514 MW Kymijärvipower plant in Lahti, owned by Lahti Energia Oy, which uses parallel cofiring (that is firing thebiomass in a separate combustor and routing the steam produced to the main steam where it isupgraded to higher conditions). Conventional stoker- or grate-fired boilers are still competitive whenthe boiler capacity is under 20 MWe and can cofire 20–95% of biomass, while larger-sized plants usethe fluidised bed combustion (FBC) technology with cofiring rates in the range of 20–90% (Fernando,2005). In Finland, approximately three-quarters of the cofiring installations adopt bubbling FBCboilers (Cremers, 2009). Alholmens Kraft in Pietarsaari is the world’s largest biomass cofired powerplant with a boiler steam capacity of 550 MWth. Started up in 2001, it uses 45% peat, 10% forestresidue, 35% industrial wood and bark residues and 10% heavy fuel oil or coal (Kärki, 2009). Theoverall thermal efficiency of large-scale CHP plants is in the range of 85–90%. Thus Finnish energyproduction has high overall efficiency due to widespread use of CHP production.

Finland has taken the following measures to encourage the use of biomass in electricity generation:� tax breaks: electricity from renewable energy sources has been made exempt from the energy tax

paid by end users;� discretionary investment subsidies: new investments are eligible for subsidies up to 30%;� guaranteed access to grid for all renewable electricity users pursuant to the Electricity Market

Act – 386/1995.

Taxes imposed on heat are calculated on the basis of the net carbon emissions of the input fuels andare zero for renewable energy sources. Further support to heat production from biomass takes theform of direct investment assistance.

In 2010, a feed-in tariff scheme was introduced to promote electricity generation using gas frombiogas reactors (the other beneficiary technology is wind energy, while solid biomass is excluded). Itwas anticipated that about 60 biogas plants with combined capacity of 19 MW would participate inthis scheme. The tariff is the difference between the target price (83.5 €/MWh for biogas-basedelectricity, and 133.5 €/MWh in CHP generation) and the spot market electricity price (Kiviluoma,2010). The tariff is paid for 12 years. With the proposed tariff level, using biowastes and manure couldbe affordable for power plants if they receive subsidies from waste utilisation; in contrast, farm-sizebiogas plants are not economic.

2.4.5 Germany

The IEA Bioenergy Task 32 cofiring database shows that Germany has at least 26 cofiringinstallations, while the European Biomass Industry Association (EUBIA) recorded 32 cofiringinstallations (EUBIA, 2011). The individual capacity of these cofiring installations ranges from75 MWe to 350 MWe. The majority of the installations are of PCC type, while fluidised bed boilersare used in a few other installations. Sewage sludge is the most common (in 17 installations) biomass

11Support mechanisms for cofiring secondary fuels

European Union

fuel to be cofired; other biomass fuels include recycled materials, wood chips, straw and variouswastes. Despite no data available on the percentage of biomass cofired with coal, the cofiring rate isexpected to be modest, at least, for sewage sludge-cofired plants.

In Germany, feed-in tariffs are the most important incentive for promoting electricity from renewableenergy sources, and are among the highest in Europe. In 2004, the German Government introducedthe first feed-in tariff scheme, under the Erneuerbare Energien Gesetz (EEG) law. The scheme appliesto solar, wind, hydro, biomass and landfill/sewage gas generated electricity. The principle behind thisscheme is a 20-year contract for a flat rate electricity price. The feed-in tariff for biomass-basedelectricity is in the range 0.08–0.12 €/kWh in Germany. The large subsidised loans available throughDeutsche Ausgleichesbank’s Environment and Energy Efficiency Programme are other key incentives.In addition, the Heat & Power Act (KWKG) regulates the financing of CHP plants and heat supplynetworks into which heat from CHP plants is fed. A Market Incentive Programme provides investmentsubsidies for heat production from small-scale CHP plants (up to 50 kW). An Energy Tax Actprovides tax exemption for products used in CHP production if the CHP plant has a monthly or annualefficiency of no less than 70%. Biomass material that is used in a CHP plant or combustedimmediately after production is also exempt from tax.

2.4.6 Italy

Italy has seven cofiring plants with four in its northern areas and three on the island of Sardinia.Except for ENEL’s Sulcis No 2 in Sardinia, which was retrofitted with an Alstom CFB boiler(790 MWth + 340 MWe) in 2006, the other six installations are all based on PCC technology withoutput capacity in the range 165–340 MWe. The cofiring rate has reached 16% (on a heat input basis)at the Sulcis No 2 CFB plant, whilst the other plants cofire biomass at lower rates. Wood chips are themain cofiring biomass fuel; for example, the Sulcis No 2 plant cofires wood chips from local sourcesfor which a separate handling and feeding system was added.

Italy has adopted the following measures to promote renewable electricity (EREC, 2009):� priority access to the electricity grid for electricity from renewable power and CHP plants;� an obligation for large electricity generators and importers (more than 100 GWh/y) to supply a

mandatory proportion of renewable electricity. Starting from 2007 at 3.05%, the prescribedproportion will increase annually by 0.75% to 2012 (for example, the 2011 share was 6.80%).The post-2012 increase rate will be determined by the Italian Government. The governmentimposes sanctions in case of non-compliance, but in reality enforcement of this obligation isconsidered difficult because of ambiguity in the legislation;

� tradeable green certificates – each green certificate represents the production of 1 MWh ofenergy from renewable sources, and is issued for 15 years to producers based both on the outputand the type of renewable sources used. Issuing and trading of green certificates are overseen byGestore Servizi Energetici (GSE), the state energy administration agency. The Budget Law 2008stipulated that the value of each green certificate was equal to the difference between €180 andthe annual average price of electricity defined each year by the Italian Authority for Electricityand Gas (AEEG). GSE, as the last resort buyer, can retire unsold green certificates at the meanprice of the previous three years;

� feed-in tariff – the Italian Government introduced a feed-in tariff scheme in 2007, initially only to>1 kW photovoltaic projects. When the Budget Law 2008 amended many parts of the greencertificate scheme, it also introduced a new tariff for small-sized renewable projects (<1 MW) thatwere revamped or commissioned after 1 January 2008. The capacity provision suggests thatbiomass cofiring projects might not be eligible for this tariff as most cofiring takes place inlarge-sized boilers.

An amendment to the Budget Law 2008, introduced by Legislative Decree 28 in March 2011, revisesthe Italian system of incentives for renewable electricity. This renewable Decree introduces a new

12 IEA CLEAN COAL CENTRE

European Union

incentive system to renewable plant that will begin operation after 31 December 2012. The systemwill be adopted in late 2011, and comprise feed-in tariffs for all types of renewable energy sources. Itis expressly provided that new tariffs will be revised two years after they come into force and everythree years thereafter in order to give greater stability and reliability to the Italian renewable energymarket. On the other hand, all plants operational before 31 December 2012 will still comply with thecurrent incentive schemes. Nevertheless, under the amendment, GSE will retire the unsold greencertificate at a lower price, 78% of the mean price of green certificate over the previous three years,until 2015. The green certificate incentive will be replaced by the new tariff scheme after 2015.

2.4.7 The Netherlands

The Netherlands has more than 16 years of experience in cofiring. The driver was been the need toreduce landfill of ~240,000 t of waste and demolition wood. The first cofiring operation was in 1995at the Gelderland power station in Nijmegen where ~60,000 t of demolition wood was cofired.Nowadays cofiring is a common practice in the country; its seven coal-fired units (capacity403–602 MWe) in five different power stations have experience in cofiring biomass. These unitscomprise tangentially-fired or opposed wall-fired pf boilers. Cofiring rates up to 15 th% are commonand higher rates have also been achieved, for example, in Unit 9 of Essent’s Amer Centrale plant(27 th% direct cofiring and 5 th% indirect cofiring). Cofired fuels have included wood pellets, wasteand demolition wood, paper sludge, compost residues, bio-oils, meat and bone meal, cocoa shells andfibres. Biomass feedstock is generally milled separately and then injected either in the coal lines or inseparate feed lines. There have also been trials of co-milling the biomass with coal at relatively lowpercentages (up to 5 th%). Ashes from cofired boilers are regularly utilised in building and civilengineering industries. The ashes are fully accepted by the market due to stringent quality criteria andgood public relations.

Widespread adoption of biomass cofiring had been attributed to the Dutch MEP (Milieukwaliteit vande Elektriciteitsproductie – environmental quality of power production) subsidy scheme 2003-07.MEP was a subsidy paid to domestic producers of grid-connected electricity from renewable sourcesand CHP plants. The subsidy took the form of a fixed premium paid on top of the wholesale price ofelectricity. The premium was paid to installations established after 1 January 1996 for a maximum often years, except for CHP. It was financed through a levy on all connections to the electricity grid,which was entirely compensated by means of a reduction in the ecotax on fossil energy consumption.MEP differentiated between various types of renewable energy technologies. It did not allow forcofiring bio-oil and significantly lowered the subsidies for cofiring certain types of contaminated solidbiomass fuels. As a result, the electricity output from cofiring biomass declined considerably in 2007,interrupting the upward trend during 2000-06.

MEP was suspended and subsequently succeeded by the SDE (stimulering duurzame energie – the aidscheme for renewable energy and CHP production) in 2008. The financing mechanism also changedfrom the levy to national budgeting. Despite being included in MEP, biomass/coal cofiring is noteligible for SDE. MEP, however, still holds for cofiring power stations covered by the pre-2009 MEPscheme, and therefore relates to the existing cofiring plants, except for the Hemweg 8 power station.The MEP subsidies were determined for the last time in 2007: 6.5 c/kWh for cofiring wood pellets,3.8 c/kWh for agro-residues, and 3.8 c/kWh for mixed biomass feedstock (Cremers, 2009).

2.4.8 Sweden

Although biomass/coal cofiring was extensively operated in the 1980s, the use of coal for heat andpower production is now very limited in Sweden. Of the total amount of coal used, only about onethird is used in CHP plants. This is mainly due to the carbon tax on heat production introduced in1991. Electricity generation with the bulk fuel being biomass is exempt from the carbon tax, which is

13Support mechanisms for cofiring secondary fuels

European Union

the dominant form of cofiring operation in 15 CHP plants at present. Two of these 15 plants employgrate-fired boilers, whereas ten plants at the paper and pulp mills use FBC boilers (seven CFB andthree BFB) with capacity less than 120 MWth. The other three plants cofire wood pellets, olive wasteand peat in PCC boilers of capacity in the range of 180–320 MWe. The cofiring rates at these plantsare not indicated in the cofiring Database (IEA Bioenergy Tasks 32, 2011).

Sweden has ambitious targets (49% by 2020) for electricity generation from renewable sources. Theprimary stimulating means of achieving this goal is the tradeable green certificate scheme introducedin 2003. The scheme mandates electricity suppliers to purchase green certificates to cover a certainproportion of their sales (renewable quota), which is set annually by the Swedish Parliament. Theinitial quota was set at 7.4% in 2003, increasing to 17.9% in 2012, and then decreasing to 4.2% in2030. In 2006, a new bill was proposed aiming to raise the renewable energy output to 17 TWh by2016 and to extend the green certificate scheme to 2030. The Norwegian and Swedish Governmentssigned an agreement in September 2009 to establish a common green certificate market which runsfrom 2012 until 2020. In this common market, more capital is expected to flow into biomass energyprojects in Sweden where the associated costs are lower, whilst Norway will attract more investmentin wind energy projects considering its climate and cost advantages. Norway is rich in hydro energyresources and has great potential for wind energy; however, cofiring with coal is rarely used becausethe country has little coal-fired capacity.

In Sweden, taxation on fossil fuels and carbon dioxide supports renewable energy in an indirect way.This is because most cofiring fuels, such as biomass, solid wastes and peat, are exempt from tax onenergy production. Main fuels used for electricity production, including coal, are also exempt fromenergy and CO2 taxes, though they are liable for NOx levy and sulphur tax.

2.4.9 United Kingdom

In the UK, 18 coal-fired power plants have had either trial or commercial operating experience incofiring biomass for various periods of time. All these power plants use large PCC boilers, except fortwo CFB boilers that belong to Caledonian Paper Plc in Scotland and Scottish and Southern Energy atSlough. Except for EDF Energy’s Cottam plant and the West Burton plant which adopt the indirectcofiring concept, all undertake direct cofiring. All but one have cofired with less than about 6 th% ofbiomass fuels; the exception is Drax power station located near Selby, Yorkshire. This 4000 MWepower station now has the capacity of generating 500 MWe from biomass, which corresponds to acofiring rate of 12.5 th%; a 50 th% cofiring rate was also successfully trialled in one unit. Theprincipal fuels are wood pellets and imported food processing residues, while biogenic liquids andenergy crops are also used. It is expected that in the long run the bulk of cofired biomass will beimported with indigenous biomass accounting for just 10% (ARUP, 2011).

The supporting mechanisms provided by the UK Government fall into two broad categories:1) those embedded in energy policies that promote production and use of biomass;2) those that have a bearing on the use of biomass energy systems.

The former category of mechanisms concerns how biomass can contribute to the power and heatneeds of the country, while the latter control how and where biomass derived fuels and conversiontechnologies can be used.

Cost effective collection and delivery of biomass are essential to the success of a cofiring project. Arange of schemes is now available in the UK for supporting production and supply of biomass fuels,see Table 1. These schemes may be available only in certain regions and to certain entities.

Introduced in 2001, the Climate Change Levy (CCL) is a tax imposed on the use of taxable energycommodities including lignite, coal, electricity, gas and LPG, but not oil. The levy is charged at a

14 IEA CLEAN COAL CENTRE

European Union

specific rate per nominal unit of energy; the rate varies across four categories of taxable commoditiesand is based on their energy content. All revenue raised through CCL is recycled back to businessthrough a 0.3% cut in employers’ national insurance contributions and support for energy efficiencyand low carbon initiatives (for example the Carbon Trust). The aim of the CCL is to encouragebusiness to become more energy efficient and reduce their greenhouse gas emissions. As an importantcomponent of CCL, exemption is given to electricity generated from new renewables or the fuel input

15Support mechanisms for cofiring secondary fuels

European Union

Table 1 Current schemes for supporting biomass fuels production and the supply chains(Biomass Energy Centre, 2011)

Scheme Notes

Availability

BusinessNon-for-profit

Publicsector

Privateindividuals

Energy CropsScheme

It offers grants to farmers in England forestablishing miscanthus and shortrotation coppice for their own energyuse or to supply power station; the rateof grant paid is 50% of all eligible costsincurred.

Yes Yes Yes Yes

ForestryCommissionGrants

A portfolio of grants managed by theForestry Commission. Aims to helppromote the stewardship of existingwoodlands, the creation of newwoodlands, and increase benefits to thepublic. The schemes vary in the fourregions across the UK.

Yes Yes Yes Yes

East MidlandsForestryMicro-enterpriseGrant

Grants of £2500–25,000 will beavailable towards buying new machineryor equipment, building handing orstorage facilities or installing woodfuelsystems.

Yes No No No

RuralDevelopmentProgramme

It is a significant sum of Europeanfunding for the development of ruralareas. Funding is available for a widerange of activities including thedevelopment and diversification ofland-based businesses and theinstallation of biomass boilers.

Yes Yes

Single PaymentScheme

A EU support scheme for agricultureFlat rate payments based on the totalfarm size rather than specific cropareas.

Yes Yes Yes

Woodfuel EastStrategicInvestmentSupportProgramme

A strategic investment supportprogramme from WoodFuel Estate tosupport woodchip production, dryingand storage for producing woodfuel;awarded through the European RuralDevelopment Programme and subjectedto the eligibility criteria of thatprogramme.

Yes Yes

Waste &ResourcesActionProgramme

Capital grants to small and mediumenterprises to help promote therecycling of a number of materialsincluding food waste processing.

Yes

to ‘good quality’ combined heat and power (the quality has to be verified by the CHP QualityAssurance Programme). Agriculture and forestry wastes, energy crops and landfill gas are eligible forthe exemption. Municipal and industrial wastes can be regarded as a renewable source eligible forCCL exemption provided that fossil fuel does not make up 90% or more of its energy content. Theexemption works on an ‘equivalent amount’ basis to take into account the practicalities of distribution.Auditing is required to ensure that exemption must be matched by purchases of electricity fromrenewable sources. As part of the auditing system, Renewable Levy Exemption Certificates(Renewable LECs) are issued to demonstrate that a quantity of electricity supplied to the finalconsumer ‘matches’ that generated from renewable sources. The Office of the Gas and ElectricityMarkets (Ofgem) and the Northern Ireland Authority for Utility Regulation (NIAUR) are responsiblefor administering, issuing, transferring and allocation of renewable LECs. NIAUR covers NorthernIreland and the Republic of Ireland, while Ofgem manages CCL exemption elsewhere.

Renewable Obligation (RO) is the UK Government’s main subsidy scheme for renewable electricity.RO requires all licensed electricity suppliers to source a proportion of their electricity from eligiblerenewable sources, including both dedicated biomass and biomass cofiring generation. It wasintroduced in England and Wales and in a different form in Scotland in April 2002, and then inNorthern Ireland in April 2005. The proportion of renewable electricity is required to increase year onyear, being 11.1% for 2010-11 and rising to 15.4% by 2015-16 (Ofgem, 2010). Since its introduction,RO has succeeded in more than tripling the level of renewable electricity generation in the UK from1.8% to 6.64%, and is currently worth around £1.4 billion per year in support to the renewableelectricity sector (DECC, 2010). As reflected in its Spending Review of 20 October 2010, the UKGovernment intends to continue the RO, extending its current end date of 2027 to 2037 for newprojects, in order to provide greater long-term certainty for investors. However, RO will be replaced in2017 by a system of contracts for electricity generation.

Since its introduction, the RO has been subject to various revisions and improvements. The mostimportant change, made in April 2009 established tiered support depending on technologies used,their costs and potential for large-scale deployment. Such banding provided a greater incentive toprojects that may hold a potential for large-scale generation, but are geographically farther fromsources of demand. The Department of Energy and Climate Change (DECC) is currently consultingon proposals for new levels of banded support during 2013-17. The new bands will come into effecton 1 April 2013 (1 April 2014 for offshore wind), subject to Parliamentary and State Aids approval.Similarly, the Scottish Government also published its consultation paper on changes to the RenewableObligation (Scotland) Order, while a separate consultation on banding changes to the Northern IrelandRO was published by its Department of Trade, Enterprise and Investment.

To demonstrate compliance with the RO, electricity suppliers are given Renewable ObligationCertificates (ROC) issued by Ofgem. Article 12(4) of the Renewable Obligation Order 2009 requiresthe Secretary of State to publish the number of ROC a designated electricity supplier is required toproduce in respect to each megawatt hour of electricity it supplies to customers in England and Walesduring an obligation period in order to discharge its renewable obligation for that period. For 2011-12,DECC sets the obligation level of 0.124 ROC/MWh, which will increase to 0.158 ROC/MWh nextyear. If an electricity supplier has not been able to cover its obligation, it may either buy more ROCsfrom others that have a surplus or pay a buy-out price (£36.99 per ROC in 2010-11) (Ofgem, 2010).Ofgem updates the buy-out price annually to reflect changes in the Retail Prices Index. Thus the ROCgives added value to producers of renewable electricity. Prior to the introduction of banding, one ROCwas issued to producers for each megawatt-hour of renewable electricity generated. Currently, newgenerators joining the RO receive different numbers of ROC, as shown in Table 2.

There is a provision of ‘mutualisation ceiling’ in the Renewable Obligation. It comes into effect whenan electricity supplier is unable to obtain sufficient funds to meet its renewable obligation. All othersuppliers, who have met their obligation, are then required to make additional payments to make upthe shortfall, up to the level of the’ mutualisation ceiling’, which is the maximum total amount they

16 IEA CLEAN COAL CENTRE

European Union

would have to pay. Mutualisation payment is in proportion to each suppliers’ obligation comparedwith the total obligation. For 2010-11, the ceiling is £222,805,333.33 in England and Wales, and£22,280,533.33 in Scotland. It is normally adjusted by Ofgem each year to reflect changes in theRetail Prices Index.

Cofiring is eligible for the RO, and its role in the RO has been reviewed on a number of occasions. Acap is placed on the extent to which cofiring ROCs can be used by a licensed electricity supplier.When the RO was introduced in 2002, the cap was set at 25% with requirement of at least 75% of thebiomass being energy crops. These rules were reviewed in 2004 in light of an increasingly apparentinsufficient supply of energy crops, and a number of changes were made as follows:� the date for cofiring to be phased out of the RO was postponed until 2016;� the energy crops share requirement was relaxed;� the overall cap was reduced to 10% from 2006 to 2010 and increased to 12.5% in April 2010

(Oxera, 2009).

The initial reduction in cap (25% down to 10%) was believed to be necessary in order to mitigate therisk that the potential volatility of cofiring volumes has on ROC prices. In a DECC-commissionedstudy, it was found that the level of cap, once beyond a certain level, has little effect on total cofiringdeployment and hence ROC prices. This is because technical constraints become more important infurther increase of cofiring capacity (Oxera, 2009). In the consultation paper on ROCs banding for2013-17, DECC is proposing to increase support for biomass cofiring. Coal-fired power stations thatburn more than 15% biomass will get 1 ROC/MWh support, double what they receive at present.DECC has also created a new ROC band to support converting coal-fired capacity to 100%biomass-fired capacity. In contrast, the Scottish Government does not increase its support for cofiringdue largely to concerns that the increasing demand from cofiring installations may constrain suppliesof biomass fuels for industrial heat production.

Despite these supports from the government, cofiring may be constrained by the extent to which theexisting coal-fired power generation continues to operate in the future. The Large Combustion PlantDirective (LCPD) has already forced seven UK coal-fired power stations to opt out of operation byend of 2015. Opt-in coal generation units fitted with FGD will need to comply with the IndustrialEmissions Directive (IED) from 2016. It is unlikely that all these plants will invest in expensive

17Support mechanisms for cofiring secondary fuels

European Union

Table 2 The current banding of ROCs for biomass firing and cofiring generation(DECC, 2009)

Generation type

Amount of electricity stated ineach ROC, MWh

Relevantproportion*

Remainder

Cofiring of biomass with CHP (burnt in separate boilers or engines) 1 2

Cofiring of energy crops with CHP (burnt in separate boilers or engines) 2/3 1

Dedicated biomass/energy crops with CHP 1/2 2/3

Cofiring of biomass 2

Cofiring of energy crops 2

Standard gasification 2

Dedicated biomass 2/3

Dedicated energy crops 1/2

* The relevant proportion, in relation to electricity generated by a qualifying combined heat and power (CHP) plant, is theproportion which the qualifying power output of that station bears to its total power output

selective catalytic reduction (SCR) to meet more stringent NOx emission standards. Instead, mostmay probably make use of either the delayed options for compliance by 2020 or the IED opt-outprovisions that allow continued but limited operation until 2023 before closure. Therefore, no morethan a few of the existing coal generation units or perhaps none will remain in service by 2030. Inaddition, the load factor of the remaining coal generation is also expected to reduce beyond 2015. Forthose units that do retrofit with SCR, biomass cofiring may also be constrained or ceased as thecombustion products associated with biomass may damage the SCR catalytic membranes.

Moreover, the role of coal in the UK future energy mix may be undermined considerably as a result ofgovernment’s recent Energy Market Reform. A Carbon Price Floor, announced in Budget 2011, willbe put in place as a key element of the reform package. Although this provides a stronger incentive toinvest in low-carbon generation, it makes coal-fired generation more expensive. The reform packagealso sets an Emission Performance Standard of 450 gCO2/kWh, which makes it actually impossible tobuild new coal-fired power stations without carbon capture and storage (CCS).

The Reform also introduces a new long-term feed-in tariff with contacts for difference. This providesstable financial incentives to invest in all forms of low carbon electricity generation. However, itsimplication for biomass cofiring is not clear at this stage as many details remain to be finalised by thegovernment.

2.5 Summary & comments

With more than 169 installations, Europe leads the world in deploying biomass cofiring technologieswith the main objective of promoting the use of renewable energy in line with EU’s energy andenvironmental targets. Cofiring is considered a cost-effective near- or medium-term option forreducing greenhouse gas emissions from existing coal-fired power or CHP plants.

Coal-fired power plants that cofire biomass are mainly located in Finland, Germany, the UK, Sweden,Denmark, Italy and the Netherlands (in descending order in terms of number of installations). Thetypical configuration applied in Finland is a fluidised bed combustion installation in the range of20–310 MW where different biomass wastes from the wood industry are directly cofired with a widerange of fuels. Fuel flexibility is a key requirement for the Finnish cofiring installations. One reasonfor this is the sparse population which makes specialised mass burning installations uneconomic. TheGerman cofiring installations are mainly of PCC type, while a few installations are on fluidised bedfurnaces. Sewage sludge is the most common biomass fuel for cofiring, whilst wood chips, straw andrecycled/refuse fuels are also cofired on some installations. In the UK, direct cofiring is undertaken in18 large coal-fired generation units. The principal fuels are wood pellets and imported food processingresidues, though some liquid biomass fuels and energy crops are also burned in some plants. InSweden, there are a large number of grate-fired boilers in the range of 1–20 MW operated for districtheating with frequent opportunities for cofiring different types of residues. In the paper and pulpindustries, there are both fluidised bed and grate furnaces that burn mixtures of bark, sludge, woodresidues, oil and some coal. Denmark has intensive experience in cofiring straw at very high ratios indifferent combustion configurations. There, the cofiring installations have demonstrated great fuelflexibility and extensive tests have also shown the limitation of the direct cofiring concept. In Italy,there are six cofiring installations on PCC boilers with capacities of 165–240 MWe and oneinstallation on a CFB boiler. Wood chips are the main biomass fuel for cofiring. Direct cofiring iscommon practice in the Netherlands with all its seven cofired units undertaking cofiring. Cofiringrates up to 15% (heat) are common and higher cofiring rates have been achieved. Wood pellets,demolition wood, paper sludge, meat and bone meal and other wastes are used as cofiring fuels.

The European countries have adopted a broad range of mechanisms to support biomass cofiring. Somemechanisms create disincentives for fossil fuels by taxing them or by making greenhouse gasesemissions expensive. Carbon tax and tax exemption for biomass fuels fall into this category.

18 IEA CLEAN COAL CENTRE

European Union

Alternatively, others aim to ensure viable markets for electricity or heat produced from biomass, suchas a feed-in tariff for renewable electricity or an obligation for electricity suppliers to include a certainlevel of renewable electricity into their supply portfolio. Still other policies and incentives focus oninvestment support and cost reduction of biomass-based power generation projects. Such diversifiedsupport mechanisms allow the governments to support biomass cofiring in a cost-effective manner.Nevertheless, a trend seems to emerge that most governments are increasingly in favour of feed-intariffs, which pass on the cost of support directly to end users of electricity.

19Support mechanisms for cofiring secondary fuels

European Union

3 USA

20 IEA CLEAN COAL CENTRE

Biomass has been used in many ways in the USA for energy production. This includes co-generationof steam and electricity in the industrial sector, power generation in the electricity sector, spaceheating in residential and commercial buildings, and transformation into liquid transport fuels.Biomass has played a relatively small role in terms of the overall US electricity generation. However,as the US political landscape for renewable energy and climate change has improved in recent years,biomass-based electricity generation (or biopower) is expected to increase significantly. This chapteranalyses the regulations, financial incentives and R&D initiatives that the USA has adopted forpromoting biopower and particularly biomass cofiring.

3.1 US energy and climate policies

The USA is heavily reliant on fossil fuels for energy supply. In 2009, petroleum, coal and natural gascomprised 83% of the nation’s total energy supply; the remaining portion came from nuclear (9%) andrenewables (8%) (EPA, 2011). Despite active promotion of energy efficiency and renewable energy,fossil fuels are still expected to provide 78% of US energy use in 2035 (EIA, 2011). Such a heavyreliance on fossil fuels has given rise to increasing concerns over energy security and environmentalimpact. Furthermore, the USA is currently the second largest emitter of GHG, accounting for almost20% of the world total. While climate change policy is unsettled in the USA (the nation has neitherratified nor withdrawn from the Kyoto Protocol), it has formally submitted its proposed GHGemissions target for 2020 to the UN under the Copenhagen Accord in 2010. It has pledged its goal toreduce GHG emissions by 17% by 2020 relative to 2005, although its target was dependent ondomestic climate legislation being passed (UNFCCC, 2012).

To meet these energy and climate challenges, the US Government has created an array of energypolicies that provide motives for a specific course of action regarding the use of energy. The EnergyPolicy Act of 2005, the Energy Independence and Security Act of 2007, and the Emergency EconomicStabilisation Act of 2008 each promote energy efficiency improvements and encourage developmentof renewable energy resources. The American Recovery and Reinvestment Act of 2009 includes morethan US$70 billion in direct spending and tax credits for clean energy and associated transportationprogrammes. In the 2011 State of the Union address, the Obama administration called for a cleanenergy standard that would set a goal of generating 80% of the country’s electricity from clean energysources by 2035. The Senate Energy and Natural Resources Committee has issued a white paper forcomment on this proposal.

The USA has also made progress in relation to policy and regulation development for climate change,particularly at the regional and the state level. A federal-level climate legislation has beenunsuccessful, though a small number of bills have been introduced in 2009-10. Nevertheless, theEnvironmental Protection Agency (EPA) now has the capacity to regulate GHG emissions fromstationary emitting sources, including power plants, refineries, and cement production facilities,following the Supreme Court’s rule in April 2007 that GHG is an pollutant under the Clean Air Act.EPA now requires permits under the New Source Prevention of Significant Deterioration (PSD) andthe Title V Operation for new industrial facilities that emit GHG in excess of 100,000 tCO2/y andexisting facilities where modification leads to an increase in emissions by at least 75,000 t/y. On23 December 2010, The EPA issued a proposed schedule for establishing GHG standards under theClean Air Act for fossil fuel fired power plants and petroleum refineries. This schedule provides ameasured and sensible path forward, which will allow the agency to address pollution from sourcesthat make up nearly 40% of the nation’s GHG emissions (EPA, 2011). These GHG standards areexpected to cover only new power plants. It is not clear when the more important guidelines forexisting plants will be issued.

At the regional level, nine Northeastern US states are involved in the Regional Greenhouse GasInitiative, a state level emissions cap-and-trade programme aiming for 10% reduction of CO2emissions from the power sector. Also, 1055 cities have joined the US Conference of Mayors’ ClimateProtection Agreement, vowing to reduce their CO2 emissions below 1990 levels, in line with theKyoto Protocol (CPC, 2011). At the state level, California began to implement its comprehensivestatewide climate programme, which combines targeted measures to achieve emission reductions inparticular sectors with a broad multi-sector GHG cap-and-trade programme. The regulationsgoverning the cap-and-trade programme were finalised in 2011, setting the stage for the system tocome into operation in 2013. As part of the Western Climate Initiative, California is looking to link itsprogramme with that in Québec also starting in 2013 and with programmes in Ontario and BritishColumbia once those are established (Kennedy, 2011).

3.2 Biopower and biomass cofiring

Electricity generation is the largest source of energy demand and consequently the largest sectorcontributor to GHG emissions. In 2009, coal and natural gas provided 44.6% and 23.3% of the total netelectricity generation, while conventional hydropower and non-hydro renewable sources accounted for9.6% and 3.6% respectively (EPA, 2011). The electricity consumption is projected to grow by 30%through 2035, though the rate of growth has slowed. The projected electricity generation gradually shiftsto low-carbon options; in particular, non-hydro renewable energy is projected to grow nearly three-fold.The increase in non-hydro renewable energy is due to considerable development of wind energy andbiopower, and to a less extent to other forms of renewables such as geothermal, solar and wastes.

As of 2009, there was 10.8 GW of biopower capacity in the country, representing 1.4% of total USelectricity generation capacity and 33.9% of total US non-hydro renewable power generation capacity(Levine, 2011). Woody biomass provided 0.9% of total US electric power generation, and 73% of thiswent to industrial CHP applications. The remaining biopower was mostly based on the use of biogenicmunicipal wastes, landfill gas and municipal sewage sludge. Dedicated biomass plants dominatedwoody biomass based power generation, generating 8.41 billion kWh of electricity in 2007, whilecofiring plants generated only 1.97 billion kWh (EIA, 2009). There have been over 40 commercialcofiring demonstrations, most of which are on old and small-sized (<200 MWth) power plants (IEABioenergy Task 32, 2011). A broad combination of fuels, such as residues, energy crops, herbaceousand woody biomass have been cofired in PCC, stoker and cyclone boilers. The proportion of biomasshas ranged from 1% to 20% by weight. Large-scale cofiring projects are under consideration byutilities as a means to comply with the Renewable Portfolio Standard (RPS). However, manyrepowering and cofiring projects are now put on hold as utilities are still concerned about technical,economic and regulatory risks. EIA projected that electricity generation from cofiring power plantswill increase by 17.4% annually to 78.17 billion kWh of electricity in 2030 (EIA, 2009). Such anincrease is the result of a variety of regulatory and financial incentives, which will be discussed brieflyin the following section.

3.3 US supporting mechanisms for biomass cofiring

There have been regulatory and tax incentives to promote the development of biomass and otherforms of renewable energy since the late 1970s.

3.3.1 PURPA

The Public Utility Regulatory Policies Act (PURPA), instigated in 1978, was to promote greater use ofindigenous renewable energy by forcing then regulated natural monopoly electric utilities to buypower from more environmentally friendly generation sources. This act became the basic legislation

21Support mechanisms for cofiring secondary fuels

USA

that enables renewable energy providers to gain a toehold in the market and exempts developers ofrenewable energy projects from numerous State and Federal regulatory regimes. However, PURPA’ssignificance is reducing because many of the contracts made under it during the 1980s are expiring.Electric deregulation and creation of a vast energy market easily accessible by utilities also promptedthe State regulatory agencies to stop forcing utilities to give contracts to developers of non-utilityprojects. In February 2005, an amendment was introduced to PURPA calling for an RPS.

3.3.2 Renewable Portfolio Standard

RPS requires end-use electricity providers to procure a proportion of their electricity supply fromqualifying renewable resources. As of July 2009, 29 states and the District of Columbia havemandatory RPS regimes, while five additional states and Guam have non-binding renewable portfoliogoals. Different states have different RPS targets; for example, in California, the RPS law requires33% of renewable by 2020, whereas New York has a 24% requirement by 2013. Whether biomasscofiring with fossil fuels qualifies under such a regime varies from state to state. A number of stateshave explicitly defined cofiring as a qualifying resource, while others have excluded it outright, likelybecause of its dependency on coal facilities. Also, in some states, the governing state commissionwould have to determine whether cofiring constitutes a renewable resource on a case-by-case basis.Although RPS rules might be specific to each state, it is true that these standards typically attach realfinancial value to electricity produced from renewable resources. RPS policies can incorporate amarket-based mechanism, the tradeable Renewable Energy Credits (see Section 2.3.4 for details), forRPS compliance so as to provide for contracting flexibility, to lower compliance costs and to simplifyverification.

The US Congress has considered a federal RPS (also known as renewable electricity standard or RES)since 1997-99: the Senate has passed legislation three times, and the Representative House once. Mostrecently, three congressmen have proposed new legislation calling for a national RPS in the lastcongress session, the main provisions of which are listed in Table 3. However, both houses have notacted in unison to pass any legislation so far. While many in Congress support a national RPS becauseof its perceived benefits for resource diversity, price stability, and environmental quality, others areconcerned that it could lead to higher consumer costs and differential regional impacts.

A study by the US National Renewable Energy Laboratory (NREL) analysed the possible impacts ofthe above three legislation proposals on the US electricity sector (Sullivan and others, 2009). TheMarkey scenario was the most straightforward because it had no efficiency component. Under thisscenario, renewables generation, including biomass cofiring with coal, largely displaced coal-firedpower, while natural gas capacity and generation remained constant from the reference scenario (thatis no legislation implemented). The study also showed that an efficiency allowance tended to reducethe overall electricity demand, so that with a less aggressive renewable standard, not only renewablebut also coal and gas generation are likely to decline compared to the reference case. Nevertheless, thebiomass cofiring generation increased in spite of a demand reduction, probably due to its costeffectiveness as a renewable generation source.

3.3.3 Voluntary green pricing programme

In 2009, state RPS policies collectively called for utilities to procure about 29.5 billion kWh of newrenewable power generation, compared to about 30 billion kWh sold to the voluntary green powermarkets. Voluntary consumer decisions to buy electricity from renewable energy sources thusrepresent another important support mechanism for renewable power development. Since the early1990s, US utilities have begun offering green power options to their customers. These programmes,termed ‘green pricing’, allow customers to purchase some portion of their power supply fromrenewable generation sources, generally at a higher price (with a premium), so as to contribute funds

22 IEA CLEAN COAL CENTRE

USA

for the utility to invest in renewable energy development. Customers can either purchase green powerfor a certain percentage of their electricity use or in discrete amounts or blocks at a fixed price. Mostutilities offer block products but may also allow customers to buy green power for their entire monthlyelectricity use. Utilities that offer percentage-of-use products generally allow residential customers toelect to purchase 25%, 50%, or 100% of their electricity use as renewable energy, while a few offerfractions as small as 10%. Large business users can often purchase green power for some fraction oftheir electricity use as well. The US DOE’s National Renewable Energy Laboratory (NREL)estimated that approximately 1.4 million US electricity customers nationwide purchased green powerproducts in 2009 through regulated utility companies from competitive green power markets, or in theform of RECs (NREL, 2009). RECs may come from nationwide renewable energy sources and besold nationally; alternatively, RECs may be subject to locality requirement – that is they are suppliedfrom renewable energy sources in a particularly region and marketed as such to local customers.

A detailed illustration of utilities’ green pricing programmes by state can be found on the website ofUS DOE’s Office of Energy Efficiency and Renewable Energy. In 2009, approximately 860 utilities in41 states are now offering green pricing programmes. The types of renewable power include wind, PV,landfill gas, hydro, geothermal, biomass and other various local renewable projects. However, biomasscofiring with coal is covered by just two utilities as shown in Table 4.

In 2009, the price of green power for residential customers ranged from –0.17 ¢/kWh to 10.00 ¢/kWhabove standard electricity rates with an average premium of 1.75 ¢/kWh (NREL, 2009). Thesepremiums have been adjusted to account for any fuel-cost exemptions granted to participants of thegreen pricing programme. Since 2000, the average premium has dropped to a compound annual rateof 7% (NREL, 2009). Some of this reduction can be attributed to lower market costs for renewableenergy suppliers or increased competitiveness over conventional generation sources. Thiscompetitiveness as well as regional demand for state RPSs will affect the price premium in comingyears.

23Support mechanisms for cofiring secondary fuels

USA

Table 3 The main provisions of three recent RES bills

Provisions Jeff Bingaman Edward Markey Henry Waxman

RPS target4% by 2011, 20% by2021 through 2039

6% by 2012, 25% by2025 through 2040

Same as Markey

Covered entitiesAll suppliers sellingmore than 4 millionMWh except in Hawaii

All suppliers sellingmore than 1 millionMWh

Same as Markey

‘Exisiting’ versus ‘New’renewables

RECs for existingrenewables (before1 January 2006) cannotbe traded

No differentiation No differentiation

Energy efficiencyallowed

Yes; can be used toaccount for up to 25% oftarget each year

No; Markey proposes anindependent scheme forenergy efficiency

Yes; states may petitionto reduce annualobligation by up to 20%if utilities comply withthe separate energyefficiency scheme

REC multiplier

2 federal RECs per kWhfor projects on triballands; 3 RECs per kWhfor distributed generationat customer sites with1 MW limit

3 federal RECs per kWhfrom distributedgeneration sources(non-combustionprojects at or nearcustomer sites, up to2 MW)

Same as Markey

3.3.4 Renewable Energy Credit