support staff pension presentation

DESCRIPTION

November 2011 versionTRANSCRIPT

Local Government Local Government Pension Scheme Pension Scheme

UpdateUpdate

The Scope of the Hutton The Scope of the Hutton Report – Schemes coveredReport – Schemes covered Local Government Pension Scheme Teachers’ Pension Scheme NHS Pension Scheme Civil Service Pension Scheme Armed Forces Pension Scheme Police Pension Scheme Firefighters’ Pension Scheme UK Atomic Energy Authority Pension

Scheme

Public Sector Schemes Public Sector Schemes Comparison Comparison

SchemeScheme ContributionContribution Employer Cont.Employer Cont. Normal Normal Pension Pension

AgeAge

Average Average Pension Pension

PolicePolice 9.5% - 11%9.5% - 11% 24.2%24.2% 5555 £14,000£14,000

FirefightersFirefighters 8.5% - 11%8.5% - 11% 14.2% - 26.5%14.2% - 26.5% 55 or 6055 or 60 £12,000£12,000

Teachers 6.4%6.4% 14.1%14.1% 60 or 6560 or 65 £10,000£10,000

Armed Armed ForcesForces

0%0% 29.4%29.4% 5555 £8,693£8,693

NHSNHS 5% - 8.5%5% - 8.5% 14%14% 60 or 6560 or 65 £7,000£7,000

Civil ServiceCivil Service 1.5% - 3.5%1.5% - 3.5% 3% - 18.9%3% - 18.9% 60 60 oror 65 65 £6,200£6,200

Local Local GovernmentGovernment

5.5% - 7.5%5.5% - 7.5% 13.20% (avge.)13.20% (avge.) 6565 £4,044£4,044

Why is Change Needed? Why is Change Needed?

Current system is seen to be unfair Life expectancy has increased Increased cost to taxpayer –

unfunded schemes Final salary schemes do not reflect

true pay / contribution history Change is needed to retain high

quality defined benefit schemes

Hutton’s RecommendationsHutton’s Recommendations

No change from a defined benefit basis, but…

Move from a final salary arrangement to one based on career average earnings

Raise the normal retirement age Uniformed service retirement age to

increase to 60 Increased employee contribution Cap on employer contribution accrued rights should be protected Implementation by 2015

The Government’s Response The Government’s Response to the Hutton Reportto the Hutton Report Introduction of career average scheme for

new service Final salary basis protected for old service Increased retirement age for new service

with a link to State pension age Retention of existing retirement age for old

service Increased employee contribution at around

3% more No increase in contributions for those

earning less than £15,000 pa Increase in contributions pegged to 1.5%

for those earning £15,000 - £18,000 pa

Some Frequently Some Frequently Asked Questions…Asked Questions…

Will I Have to Pay More?Will I Have to Pay More?

Increased contributions are possible

LGPS contribution rates were reviewed in 2008

Funded nature of LGPS means that other changes will be implemented instead

Risk of opt-outs – Hutton has Risk of opt-outs – Hutton has said this needs to be avoided said this needs to be avoided

LGPS – current ratesLGPS – current rates

FTE PayFTE Pay Contribution rateContribution rate

Up to £12,901 5.5%

£12,901 to £15,101 5.8%

£15,101 to £19,401 5.9%

£19,401 to £32,401 6.5%

£32,401 to £43,301 6.8%

£43,301 to £81,101 7.2%

Over £81,101 7.5%

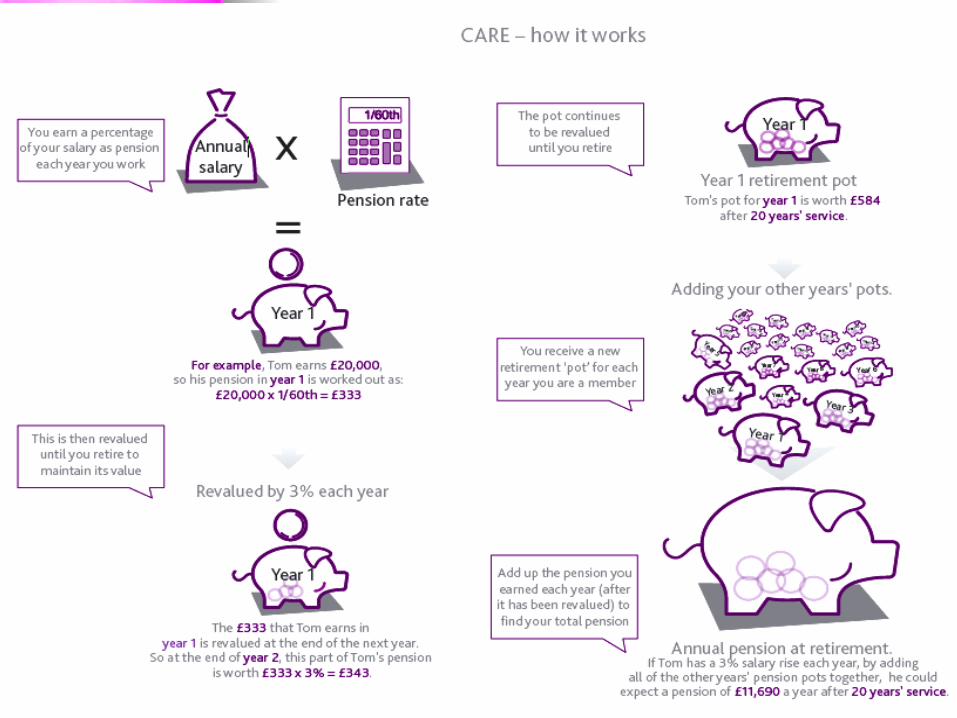

How Does a Career Average How Does a Career Average Scheme Work?Scheme Work? Each year is calculated

individually CPI adjustment made to each

year’s benefits Earlier years’ values have more

increases applied to bring them up to date

At retirement, all the revalued individual years are added together

Career Average Schemes – Better Career Average Schemes – Better or Worse than Final Salary? or Worse than Final Salary?

Less generous for employees who have rapid pay progression, particularly in their later years

Similar benefits for those with steady pay growth

Career average method is still a “defined benefit” arrangement

Remember: service to date of change will still be based on final pay

……the “Steady Eddie”the “Steady Eddie”

Years

Pay

……the “High Flyer”the “High Flyer”

Years

Pay

Will I Have to Work Until Age Will I Have to Work Until Age 65? 65? Remember – your benefits built up

to the date of any change will have the same retirement date and calculation as before

New service worked after the date of change may have a later payment date for full benefits

Most employees already have a retirement age of 65 in the LGPS

85 year rule protections will remain

But Didn’t the LGPS Change a Few But Didn’t the LGPS Change a Few Years Ago?Years Ago?

Yes, changes were made to:-Removal of the 85 year ruleBanded employee contributionsChange from 80th’s to 60th’s

Change from RPI to CPI will help reduce scheme costs

Further changes are still needed

Should I Opt Out?Should I Opt Out?

Personal decision occupational pension schemes

are extremely valuable Employer contribution Tax and NI savings Think very carefully before

opting out – independent advice

Remember…Remember…

Nothing has been decided yet Further consultation is planned later this

year

What You Get NowWhat You Get Now

An index-linked pension linked to pay and service

Tax free lump sum in most cases A range of retirement options

voluntary retirement age from 60 in most cases Early retirement from 55

A range of dependants’ cover including death in service lump sum of 3 x pay

Enhanced benefits if you have to leave work because of permanent ill health

The facility to top up your benefits

Get in Touch…Get in Touch… By ‘phone:-

0121 675 7070 By e-mail:-

[email protected] By post:-

Pensions TeamPO Box 14345BirminghamB2 2HZ

On the web:- www.wmpfonline.com