supporting the emissions saving benefits of using lpg … · supporting the emissions saving...

TRANSCRIPT

Supporting the emissions saving benefits of using

LPG in transport

Authors:

Alastair Hope-Morley

Celine Cluzel

Element Energy

7 August 2015

2

Key findings – using LPG in transport can bring AQ benefits but a policy framework must be put in place to attract LPG car supply

• With a refuelling infrastructure in place nationally and a relatively low price premium, LPG cars could be an option additional to cleaner technologies that are not yet as mature, have higher upfront costs and/or cannot meet the needs of some drivers (such as driving range, access to infrastructure)

• Leveraging the LPG infrastructure in place in Air Quality Management Areas would be of particular interest, as these are typically dense cities where installing new infrastructure such as charge points and hydrogen stations will be challenging on the basis of land constraints. While the infrastructure needed to support Zero Emission vehicles will grow, LPG cars could help improve air quality in the short term as well as provide an extra choice to meet consumers’ driving needs and preferences

• Taking into account consumer purchase behaviour, car uptake modelling suggests sales could reach over 100,000 p.a. by late 2020s, assuming car OEMs bring factory-fitted LPG models to the UK and make a concerted effort to raise consumers awareness of the LPG option. While in the model this level of sales is reached without a grant, a strong sign of commitment from the government will be needed to make OEMs confident it is worth bringing LPG vehicles to the UK

• In France, a notable increase in LPG car supply was observed when a purchase grant was set up, but other policy tools might be more adequate/as effective. In Germany, a long term fuel tax differential has attracted good supply (67 LPG models for sale as of 2015)

• Furthermore, cities might consider local support actions. As an example, both Birmingham City and Reading Councils are currently using the DfT Clean Vehicle Technology Fund to retrofit old diesel taxis with LPG technology, as part of their effort to improve air quality in their city centres

LPG role in the Air Quality challenge

LPG sales prospects

Attracting supply to the UK

3

Despite many UK cities facing an Air Quality challenge, the use of LPG in transport – a clean burning fuel – seems to have been overlooked

Map from http://uk-air.defra.gov.uk/aqma/maps Ordnance Survey data © Crown copyright and database right 2014

1 – Atlantic Consulting: A comparative Environmental Impact Assessment of car-and-van fuels, 2014

Blue zones show the AQMAs where NO2 and/or PM limits are exceeded (either annual or 1h/24h mean)

• There are many areas in the UK where the recommended limits for NO2 and/or Particulate Matter (PM) are exceeded, with transport being one of the main source of emissions. Such areas are declared Air Quality Management Areas (AQMAs)

• The largest ones are typically in the largest conurbations, e.g. Greater London, West Midlands (in particular Birmingham, Coventry and the Black Country), Manchester, Glasgow

• Running a vehicle on LPG instead of gasoline or diesel has considerable AQ benefits (as well as some CO2 benefit on a Well To Wheel basis)1 but the UK LPG car market is limited, despite a fully functioning network of public LPG refuelling points (including in aforementioned AQMAs)

• The case of France suggests the main limitation to the UK market is the supply of OEM vehicles (LPG-ready as opposed to post-sales conversion)

• This assumption was tested by estimating the level of sales LPG cars could reach if supply was in place, through a car uptake modelling tool that accounts for UK car buyer behaviour and preferences

• The results suggest sales could reach well over 10,000 units per year and the corresponding AQ benefits were quantified in a separate analysis

• Lastly, observations are made on how the UK could put the framework in place to capture these AQ benefits, in parallel to the current support for Zero Emission vehicles such as electric vehicles

Air Quality Management Areas BACKGROUND AND REPORT SUMMARY

4

PowerShift program

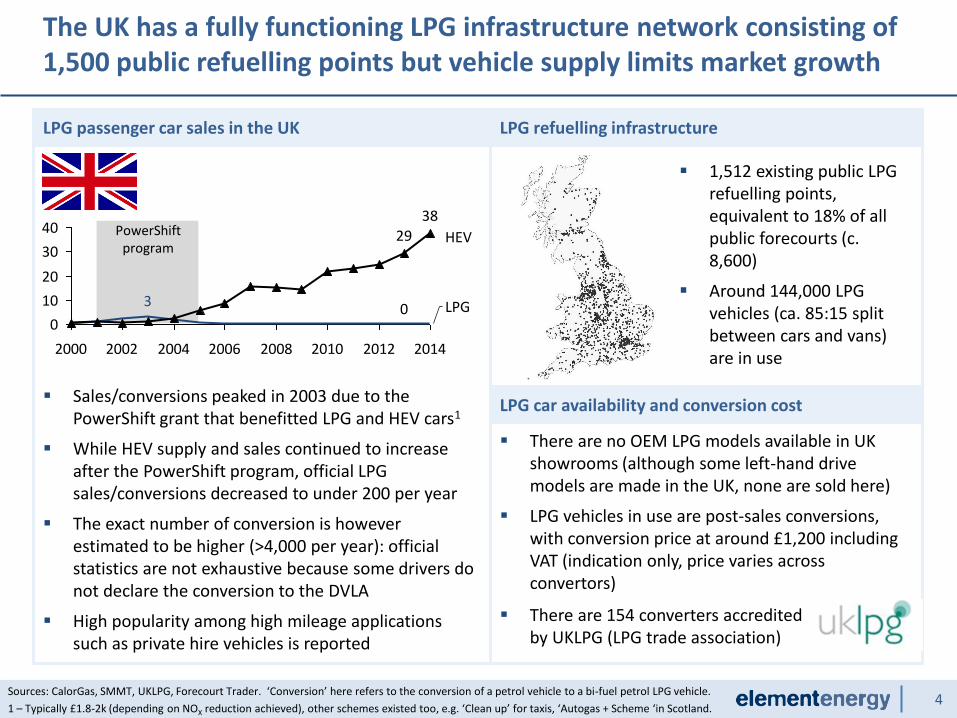

The UK has a fully functioning LPG infrastructure network consisting of 1,500 public refuelling points but vehicle supply limits market growth

LPG passenger car sales in the UK

Sources: CalorGas, SMMT, UKLPG, Forecourt Trader. ‘Conversion’ here refers to the conversion of a petrol vehicle to a bi-fuel petrol LPG vehicle.

1 – Typically £1.8-2k (depending on NOX reduction achieved), other schemes existed too, e.g. ‘Clean up’ for taxis, ‘Autogas + Scheme ‘in Scotland.

Sales/conversions peaked in 2003 due to the PowerShift grant that benefitted LPG and HEV cars1

While HEV supply and sales continued to increase after the PowerShift program, official LPG sales/conversions decreased to under 200 per year

The exact number of conversion is however estimated to be higher (>4,000 per year): official statistics are not exhaustive because some drivers do not declare the conversion to the DVLA

High popularity among high mileage applications such as private hire vehicles is reported

LPG refuelling infrastructure

LPG car availability and conversion cost

There are no OEM LPG models available in UK showrooms (although some left-hand drive models are made in the UK, none are sold here)

LPG vehicles in use are post-sales conversions, with conversion price at around £1,200 including VAT (indication only, price varies across convertors)

1,512 existing public LPG refuelling points, equivalent to 18% of all public forecourts (c. 8,600)

Around 144,000 LPG vehicles (ca. 85:15 split between cars and vans) are in use

2000 2002 2004 2006 2008 2010 2012 2014

40

20

30

0

10

29 HEV

38

LPG 0 3

There are 154 converters accredited by UKLPG (LPG trade association)

5

Bonus system starts:

CASE STUDY: In France, good OEM vehicle supply, appropriate incentives and a national infrastructure enabled LPG car sales to reach 76k p.a.

LPG passenger car sales in France, thousands

Sources: Fichier Central des Sinistres Automobiles, Sous-direction des statistiques de l'énergie, Comité Français du Butane et du Propane HEV = Hybrid Electric Vehicle 1- Comparing MJ/100km figures for cars offered in both petrol and LPG versions (24MJ/L for LPG, 36MJ/L for gasoline)

LPG car sales in France increased by c. 850% from 2008-2009 and peaked at c. 76k p.a. in 2010

Ramp-up largely driven by an attractive tax rebate

After three years the incentive was withdrawn and vehicles sales returned to pre-subsidy levels

This illustrates that with the right price proposition and OEM supply, LPG car sales can reach over 70,000 p.a., even in a market largely skewed towards diesel powertrains

LPG refuelling infrastructure

1,867 existing public LPG refuelling points, representing 13% of all public forecourts (c. 13,800)

An estimated 260,000 LPG vehicles are in use in France today

LPG car availability and capital cost premium

At least 9 OEMs offer LPG bi-fuel cars across a broad range of vehicle segments

Relative to similar petrol vehicles, LPG cars have an average capex premium of €1,700, and are 14% more energy efficient (based on NEDC data1)

Increasing vehicle segment size

Fiat Punto Opel Mokka Opel Meriva Renault Clio

Increase supply of series LPG vehicles and low cost models

€2,000 for HEVs and LPG cars

<135g/km

€2,000 for HEVs <110g/km

2012 2013

80

2014 2004 2005 2006

60

0

20

2010 2011 2008 2009

40

2007

47

LPG

76

12 HEV

3

25

3

6

The evaluation of the potential LPG market benefitted from an existing uptake modelling tool that accounts for UK car buyers’ behaviour

Source: Element Energy 1 - Quantitative survey of consumer attitudes to plug-in vehicles, Element Energy for DfT, 2015 (pending publication) – Survey on 2,000 new car buyers conducted in February 2015

Understanding and modelling car buyers’ behaviour

Many parameters influence a car purchase decision, ranging from cost factors (upfront and running costs), practical (e.g. car size, access to recharging/refuelling), personal preferences (e.g. brand, fuel type). In the case of alternative fuel vehicles, access to information/awareness and low level of supply are also factors that can impact sales

Sales of alternative fuel vehicles – which are quite often more cost effective than petrol/diesel versions over their ownership period – illustrate the fact that cost is not the only choice factor and/or that future savings are discounted i.e. that a lower upfront cost is preferred

The way that UK car buyers weigh up capital & running costs and other parameters has been researched through qualitative and quantitative surveys, the most recent having been conducted in early 2015 for the Department of Transport1

Car upfront cost Running cost (fuel, taxes, insurance

and maintenance) Brand supply penalty

Access to recharging (for EVs) or to station (for LPG and H2 vehicles)

Bias for/against a given technology

These findings have been integrated in the car uptake model currently used by DfT, originally developed by Element Energy for the Energy Technologies Institute and DfT

This model was used to estimate the level of LPG car sales for a case where OEMs bring LPG cars to the UK

A price premium of £1,500 over petrol models was assumed for LPG cars (based on observed average premium in European markets). A ‘brand supply penalty’ (of £1,285)1, decaying after 5 years, was also added to LPG cars, to represent the fact that even if supply was kick-started in the UK, it’s unlikely the full range of brands would be on offer

Parameters of the choice model

7

We have updated the consumer choice model to include factors governing LPG car buyers’ decisions (e.g. capital and running costs, refuelling sites)

1 Represented in the model with a decrease in the ‘negative bias’ that most consumers hold against new technologies. In the case of LPG, the £ penalty represented by that bias decreases to c.£3k by 2030 in Scenario 2 (from c.£5k in 2015)

Model outputs

The model was run to simulate a concerted effort from OEMs to bring LPG vehicles to market in the UK, and consumer uptake of LPG cars between 2016-2030 was estimated

Two scenarios were considered:

1. Supply of LPG cars is in place but consumer awareness & acceptance of LPG cars stay limited (LOW CASE)

2. Supply of LPG car increases, and consumer awareness & acceptance of LPG cars increases with sales1 (HIGH CASE)

Modelling results show that, in Scenario 1, LPG car sales increase to c. 14k per year by 2020 and remain broadly constant thereafter. This is effectively an established ‘niche market’

In Scenario 2, sales reach c. 29k by 2020 and continue increasing, exceeding the 100,000 mark by the late 2020s

As a point of comparison, under these scenarios, sales of plug-in vehicles exceed 500,000 by the late 2020s, making LPG cars a complementary technology rather than a replacement or competitor

1814

9

29

9

140

2020 2030 2016

LOW CASE HIGH CASE

Annual sales of LPG cars, thousands

Model results under two scenarios. Based on existing LPG public infrastructure, £1,500 price premium for LPG cars, supply penalty to 2020 and baseline inputs.

8

A report prepared by Atlantic Consulting quantified the emission savings and corresponding AQ damage reduction from LPG car uptake

OUTPUTS

Several outputs were produced in the Atlantic Consulting analysis regarding the LPG substitution cases:

Reduction in CO2 emissions, in tonnes

Reduction in pollutants (including NOx, PM10, PM2.5) in tonnes

The corresponding health impact of these reductions, in avoided DALYs (disability adjusted life years, i.e. person-years of life lost to ill health or death which are caused by the pollutant)

The avoided health-care costs brought by the reduction in DALYs

The alternative cost of emission reductions (i.e. if not brought by LPG cars)

These results have been combined with the modelled LPG car sales (LOW and HIGH cases), presented next

Sources: UK air-emissions impact of introducing 40,000 LPG cars per year during 2016-2029, Atlantic Consulting, 2015; Element Energy

Atlantic Consulting analysed the emission savings LPG cars would bring, for 4 reference cases:

OLD DIESEL: LPG cars substitute old diesel cars

NEW DIESEL: LPG cars substitute new diesel cars (EURO 6)

PETROL & DIESEL: LPG cars substitute a mix of new petrol & diesel cars (50/50)

DIESEL REAL WORLD: LPG cars substitute new diesel cars (EURO 6), taking into account

research findings that show that, in ‘real world’ driving conditions, diesel cars emit 7.5 times

more NOx than the EURO 6 limit

REFERENCE CASES FOR EVALUATING THE SAVINGS BROUGHT BY LPG CARS

9

LPG cars could deliver substantial emissions savings, even in a low uptake case, bringing annual health case savings of £8-£30m by 2029

Savings cumulate to £53million (LOW case) and £151million (HIGH case) over the 2016-2029 period

Numbers on graphs are the average value. Ranges arise from the 4 reference cases (see previous slides for definition) – for health impact, only average values are plotted. LOW and HIGH uptake scenarios were derived from uptake modelling, see slides 5-6. Values shown are undiscounted.

219

55

HIGH LPG UPTAKE LOW LPG UPTAKE

Annual reduction in CO2 emissions, ‘000 tonnes

587

LOW LPG UPTAKE HIGH LPG UPTAKE

2,258

Annual reduction in NOx emissions, tonnes

65

256

LOW LPG UPTAKE HIGH LPG UPTAKE

Annual reduction in PM10 emissions, tonnes

The real-world emissions of EURO 6 diesel car create a large interval of results

EMISSION SAVINGS BROUGHT BY LPG CARS BY 2029 CORRESPONDING HEALTH IMPACT ABATEMENT

327

82

HIGH LPG UPTAKE LOW LPG UPTAKE

Annual DALYs reduction by 2029 (Disability adjusted life years)

31

8

HIGH LPG UPTAKE LOW LPG UPTAKE

Corresponding annual savings in health care in 2029, £m

10

Closing remarks and suggested next steps to capture the emissions savings that LPG could bring to UK cities

• With a refuelling infrastructure in place nationally and a relatively low price premium, LPG cars could be an option additional to cleaner technologies that are not yet as mature, have higher upfront costs and/or cannot meet the needs of some drivers (such as driving range, access to infrastructure)

• Leveraging the LPG infrastructure in place in Air Quality Management Areas would be of particular interest, as these are typically dense cities where installing new infrastructure such as charge points and hydrogen stations will be challenging on the basis of land constraints. While the infrastructure needed to support Zero Emission vehicles will grow, LPG cars could help improve air quality in the short term as well as provide an extra choice to meet consumers’ driving needs and preferences

• Taking into account consumer purchase behaviour, car uptake modelling suggests sales could reach over 100,000 p.a. by late 2020s, assuming car OEMs bring factory-fitted LPG models to the UK and make a concerted effort to raise consumers awareness of the LPG option. While in the model this level of sales is reached without a grant, a strong sign of commitment from the government will be needed to make OEMs confident it is worth bringing LPG vehicles

• In France, a notable increase in LPG car supply was observed when a purchase grant was set up, but other policy tools might be more adequate/as effective. In Germany, a long term fuel tax differential has attracted good supply (67 LPG models for sale as of 2015). Furthermore, cities might consider local support actions. As an example, both Birmingham City and Reading Councils are currently using the DfT Clean Vehicle Technology Fund to retrofit old diesel taxis with LPG technology, as part of their effort to improve air quality

• Understanding under what conditions the UK would become an interesting LPG market for car OEMs is the next step to fully appraise the prospect of LPG in transport. This could be investigated through in depth consultation with the key OEMs (e.g. VW, Renault, Vauxhall, Fiat, Hyundai, Ford, Dacia) that are currently marketing a wide range of LPG cars across Europe

LPG role in the AQ challenge

LPG sales prospects

Next steps

11

Appendix

12

Acronyms

AQ Air Quality

AQMA Air Quality Management Area

DALY Disability Adjusted Life Years

DEFRA Department for Environment, Food & Rural Affairs

DfT Department for Transport

DVLA Driver and Vehicle Licensing Agency

ETI Energy Technologies Institute

EV Electric Vehicle

HEV Hybrid Electric Vehicle

LPG Liquefied petroleum gas

NEDC New European Driving Cycle

NO2 Nitrogen dioxide

NOx Nitrogen oxides

OEM Original Equipment Manufacturer

PM Particulate Matter

SMMT Society of Motor Manufacturers & Traders

UK United Kingdom

13

The LPG refuelling network covers the main Air Quality Management Areas

Source: map and station data from CalorGas, location of AQMAs from DEFRA (map shown on slide 2)

1

2

3

4

1

2

3

Glasgow – over 15 public LPG retail points

Manchester and Liverpool City Region – over 60 public LPG retail points

Birmingham - 21 public LPG retail points (16% of forecourt coverage)

4 Greater London - 70 public LPG retail points (12% of forecourt coverage)

Example coverage in cities with AQMAs Public LPG refuelling points