sustainability reporting & disclosure: form follows function · independent 501(c)3 non- profit...

TRANSCRIPT

© 2015 SASB™

Sustainability Reporting & Disclosure: Form Follows Function

Doug Park, JD, PhDDirector of Legal Policy and [email protected]

Moderator:Nicolai LundyEducation [email protected]

November 17, 2015

2 11/17/2015 © 2015

Source: SASB

The SASB MissionImproved non-financial disclosure results in enhanced market efficiency

The mission of SASB is to develop and disseminate sustainability accounting standards that help public corporations disclose material, decision-useful information to investors.

That mission is accomplished through a rigorous process that includes evidence-based research and broad, balanced stakeholder participation.

Facts about SASB

Independent 501(c)3 non-profit

American National Standards Institute (ANSI) accredited standards developer

Developing industry-specific standards for 10 sectors and 80+ industries

Guided by the U.S. Supreme Court’s definition of materiality, SASB prioritizes topics of disclosure and standardizes the form of disclosure

Robert H. HerzFormer Chairman –FASB

Dan Hanson, CFAPartner and Director of U.S. Equities – JarislowskyFraser USA

Strong LeadershipInformed by experience, credibility, character, commitment, and vision

3

Mary Schapiro – Vice ChairPromontory Advisory Board Vice ChairFormer Chairman – SEC

Jack EhnesCEO – CalSTRS

Steven O. Gunders, CPA, MBAPartner – Deloitte & Touche LLP (Retired)

Erika KarpCEO – Cornerstone Capital Inc.

Suz Mac CormacPartner – Morrison & FoersterLLP

Shawn LytlePresident – Delaware Management Holdings, Inc.

Michael R. Bloomberg – ChairPhilanthropist, Founder of Bloomberg LP, and the 108th Mayor of New York City

Clara Miller President – The F.B. Heron Foundation

Catherine OdelboExecutive Vice President, Corporate Strategy and Partnerships –Morningstar Inc.

Aulana PetersFormer Commissioner – SEC

Bob Eccles, PhDProfessor of Management Practice –Harvard Business School Edward D. White

Managing Partner – FahrLLC

Elisse WalterFormer Chairman – SEC

Kevin ParkerCEO – SICM

Jean Rogers, PhD, PEChief Executive Officer & Founder – SASB(Ex-officio)

Curtis RavenelGlobal Head, Sustainability Initiatives – Bloomberg LP

11/17/2015 © 2015 SASB™

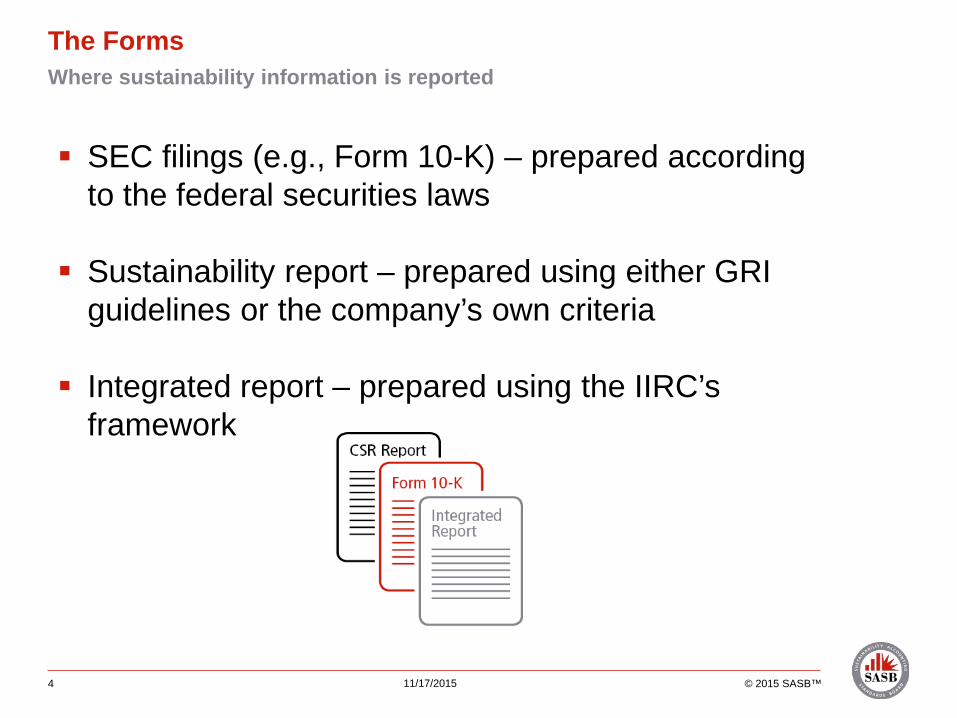

The FormsWhere sustainability information is reported

4 11/17/2015 © 2015 SASB™

SEC filings (e.g., Form 10-K) – prepared according to the federal securities laws

Sustainability report – prepared using either GRI guidelines or the company’s own criteria

Integrated report – prepared using the IIRC’s framework

Consensus-driven

Cost-effective

Evidence-based

Industry-specific

What Is Different About SASB?The ‘alphabet soup’ of the sustainability reporting landscape can be confusing

5 11/17/2015 © 2015 SASB™

Decision-useful

Sustainable Industry Classification SystemSICS™ industries are grouped by resource intensity and sustainability impacts

11/17/2015 © 2015 SASB™6

Health Care Biotechnology Pharmaceuticals Medical Equipment & Supplies Health Care Delivery Health Care Distributors Managed Care

Technology & Communications Electronic Manufacturing Services &

Original Design Manufacturing Software & IT Services Hardware Semiconductors Telecommunications Internet Media & Services

Renewable Resources & Alternative Energy Biofuels Solar Energy Wind Energy Fuel Cells & Industrial Batteries Forestry & Paper

Transportation Automobiles Auto Parts Car Rental & Leasing Airlines Air Freight & Logistics Marine Transportation Rail Transportation Road Transportation

Non-Renewable Resources Oil & Gas – Exploration &

Production Oil & Gas – Midstream Oil & Gas – Refining & Marketing Oil & Gas – Services Coal Operations Iron & Steel Producers Metals & Mining Construction Materials

Infrastructure Electric Utilities Gas Utilities Water Utilities Waste Management Engineering & Construction Services Home Builders Real Estate Owners, Developers &

Investment Trusts Real Estate Services

Services Education Professional Services Hotels & Lodging Casinos & Gaming Restaurants Leisure Facilities Cruise Lines Advertising & Marketing Media Production & Distribution Cable & Satellite

Resource Transformation Chemicals Aerospace & Defense Electrical & Electronic Equipment Industrial Machinery & Goods Containers & Packaging

Financials Commercial Banks Investment Banking & Brokerage Asset Management & Custody

Activities Consumer Finance Mortgage Finance Security & Commodity Exchanges Insurance

Consumption Agricultural Products Meat, Poultry & Dairy Processed Foods Non-Alcoholic Beverages Alcoholic Beverages Tobacco Household & Personal Products Multiline and Specialty Retailers &

Distributors Food Retailers & Distributors Drug Retailers & Convenience Stores E-Commerce Apparel, Accessories & Footwear Building Products & Furnishings Appliance Manufacturing Toys & Sporting Goods

Reporting AlignmentSASB is separate from, but complementary to, a variety of reporting initiatives

7

SASB GRI IIRC FASB

Type of guidance

Scale

Standards Guidance Framework Standards

U.S. U.S.InternationalInternational

Target disclosure

Subject Non-financial Non-financial Non-financial Financial

Mandatory SEC filings

Voluntary report

Voluntary report

Mandatory SEC filings

Investors Investors InvestorsAll stakeholders

Target audience

GRI IIRCU.S. Supreme Court case law

U.S. Supreme Court case law

Definition of materiality

Scope Industry-specific

General General General

11/17/2015 © 2015 SASB™

8 11/17/2015 © 2015

Source: SASB

Robust StandardsBuilt to deliver high-quality data, SASB standards contain more than just metrics

SASB Standard

Disclosure topics

Technical protocol

Accounting metrics

No New Regulation RequiredSASB standards rest on existing regulation and support disclosure in the MD&A

9

Federal securities laws require companies to:

Disclose material information as appropriate in SEC filings such as the Form 10-K/20-F, 10-Q, and 8-K.

Disclose management’s view on known trends, events, and uncertainties that are reasonably likely to have a material impact on results of operations and financial condition.

Form 10-K (MD&A)

11/17/2015 © 2015 SASB™

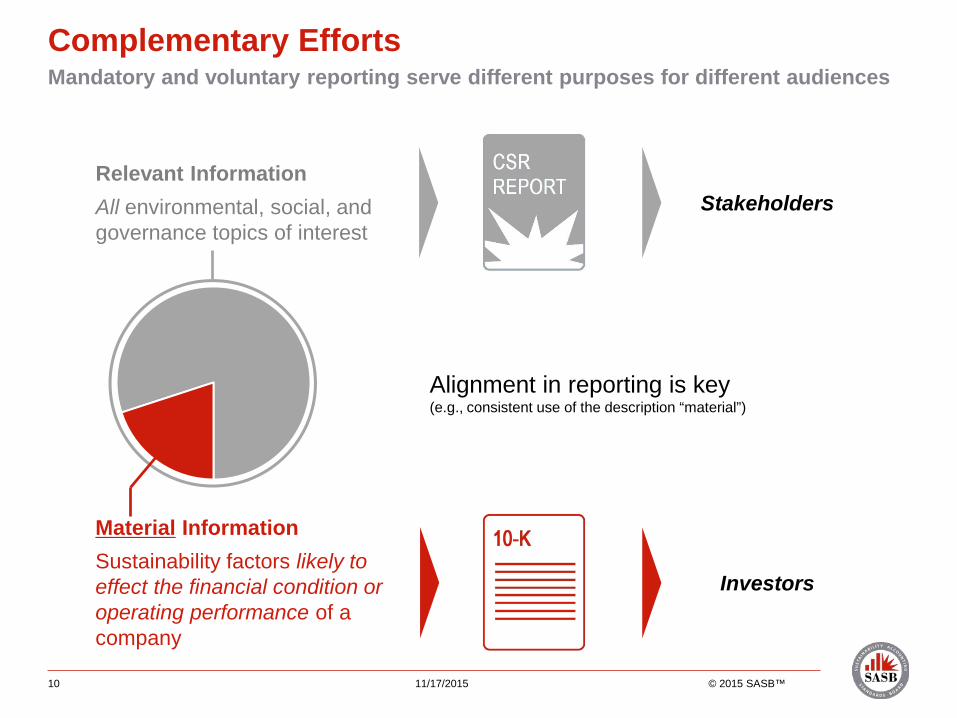

Complementary EffortsMandatory and voluntary reporting serve different purposes for different audiences

10 11/17/2015 © 2015 SASB™

Material InformationSustainability factors likely to effect the financial condition or operating performance of a company

Relevant Information All environmental, social, and governance topics of interest

Investors

Stakeholders

Alignment in reporting is key (e.g., consistent use of the description “material”)

Relationship To The Legal And Regulatory StructureOf each form

11 11/17/2015 © 2015 SASB™

SEC Filings Sustainability Report

Integrated Report

Required Not Required Not Required

Disclosure obligations in federal securities laws

No direct relationship, but potential legal implications

No direct relationship, but potential legal implications

Materiality as underlying disclosure principle

Different standard governs reporting

Different standard governs reporting

Disclosure AnalysisAn analysis by channel

12 11/17/2015 © 2015 SASB™

Consistency and Cost-EffectivenessConsistent reporting across channels improves efficiency and reduces legal risk

11/17/2015 © 2015 SASB™13

Product Design for Use-phase Efficiency“Our growth efforts focus on developing environmentally compatible and sustainable solutions that can effectively increase farmers’ yields and provide cost-effective alternatives to chemistries which may be prone to resistance.”

“Sustainable Product Sales: In 2014, we had a 17.5% increase in sales of sustainable products. A “sustainable product” is one that impacts one or more of the global challenges.” (i.e. scarce resources, climate change, environmental consciousness, food & health expectations, and land competition).

FY 2014 FORM 10K 2014 SUSTAINABILITY REPORT

Health, Safety, & Emergency Management“[The company] has steadily improved our recordable incident rate for the last five years. However, in 2014 our recordable incident rate did not decrease. We are taking specific actions to understand how we can continue to drive safety performance in all parts of our company.”

“Although we take precautions to enhance the safety of our operations and minimize the risk of disruptions, our operations are subject to hazards inherent in chemical manufacturing and the related storage and transportation of raw materials, products and wastes.” (…) “Some of these hazards may cause severe damage to or destruction of property and equipment or personal injury and loss of life and may result in suspension of operations or the shutdown of affected facilities.”

2014 2013 2012

Total Recordable Incident Rate (TRIR) 0.51 0.41 0.59

Process Safety Incidents (Tier 1 & 2) 0 0 0

RT0101-14: Revenue from products designed for use-phase resource efficiency

RT0101-20: Total Recordable Injury Rate for (a) direct employees and (b) contract employees

RT0101-17: Process Safety Incidents Count (PSIC), Process Safety Total Incident Rate (PSTIR)

SASB METRIC(S)

Learn MoreIncrease your understanding of the link between sustainability and corporate value

11/17/2015 © 2015 SASB™

14

Fundamentals of Sustainability Accounting CredentialThe world’s first credential in sustainability accounting

How industry-specific sustainability information can inform corporate strategies or investor decisions

How to evaluate corporate performance on sustainability factors

The context for materiality and sustainability

How to identify the sustainability factors impacting financial performance

FSA.sasb.org/prep for curriculum, free resources, and registration

Level I: Principles Level II: Application (2016)

Helping CompaniesSASB’s Implementation Guide helps companies focus—and report—on what matters

11/17/2015 © 2015 SASB™15

SASB Implementation Guide for Companies

Select sustainability topics Assess current state of disclosure and

management Embed SASB standards into financial

reporting and management processes Support disclosure and management with

internal control Present information for disclosure

◄

Q&A

Doug Park

Learn More:

(Now) FSA Credential – http://fsa.sasb.org

(Now) Standards Navigator – http://navigator.sasb.org

(Next Month) Implementation Guide

16 11/17/2015 © 2015 SASB™