sustainable economic development and ict sector programme ... · sustainable economic development...

TRANSCRIPT

Sustainable Economic Development in TCc - Private Sector Development Strategy 2011 - 2015

Page | 1

The European Union’s Programme for the Turkish Cypriot Community

Sustainable Economic Development and ICT Sector Programme in the northern part of Cyprus

EuropeAid/127043/C/SER/CY

Cyprus - northern part

Private Sector Development Strategy 2011-2015

This project is funded by the European Union

This project is implemented by DIADIKASIA Business Consultants S.A.

Consortium

The European Union’s Programme for the Turkish Cypriot Community

Sustainable Economic Development in TCc - Private Sector Development Strategy 2011 - 2015

Page | 2

Table of Contents

Chapter 1. Methodological Approach ................................................................. 6

Chapter 2. Socio-Economic analysis of Northern Cyprus current situation ........... 9

2.1. Country Information ........................................................................................ 9

2.1.1. Geography ............................................................................................................ 9 2.1.2. Climate ................................................................................................................10 2.1.3. Demographic characteristics ..............................................................................10 2.1.4. Education ............................................................................................................12 2.1.5. Labour force and employment ............................................................................13 2.1.6. Physical and social infrastructure .......................................................................16

2.2. Macro-economic background ......................................................................... 18

2.3. Private Sector - Business environment ............................................................ 20

2.3.1. Identification of key sectors ................................................................................20 2.3.2. Identification of SMEs .........................................................................................30

2.4. Telecommunications& ICT sector.................................................................... 33

2.5. Financial sector .............................................................................................. 37

2.5.1. Fiscal policy .........................................................................................................37 2.5.2. Banking sector ....................................................................................................37 2.5.3. Tax System ..........................................................................................................38 2.5.4. Business environment regulatory framework .....................................................39

2.6. Investment climate ........................................................................................ 42

2.6.1. Incentives for Investors .......................................................................................42

2.7. Overview of current approaches to Private Sector Development ..................... 46

2.7.1. Current national strategy / programmes towards Private Sector Development46 2.7.2. Turkish Cypriot Community Administration priorities towards private sector

development .......................................................................................................47

Chapter 3. Key Points of socioeconomic analysis- SWOT Analysis ...................... 48

Chapter 4. Identification of major barriers to Private Sector Development ........ 50

Chapter 5. Private Sector Development Strategy .............................................. 52

5.1. Vision and Strategy ........................................................................................ 52

5.2. Strategic Objectives ....................................................................................... 53

5.3. Thematic Priorities & Interventions ................................................................ 59

Chapter 6. Action Plan ...................................................................................... 61

6.1. Proposed actions under the 1st Priority: “Competitive TCc economy” .............. 62

6.2. Proposed actions under the 2nd Priority: “Institutional framework” ................. 65

6.3. Proposed actions under the 3rd Priority: “Knowledge society and innovation” . 68

6.4. Proposed actions under the 4th Priority: “Employment and Social Cohesion” ... 70

6.5. Proposed actions under the 5th Priority: “Attractiveness of TCc as an area to invest, work and live in” ............................................................................. 71

Chapter 7. Strategy Monitoring Mechanism ...................................................... 73

Sustainable Economic Development in TCc - Private Sector Development Strategy 2011 - 2015

Page | 3

List of Tables Table 1 Population Basic Indicators (2002-2008) ............................................................... 10 Table 2 Distribution of Population by Districts and Sub-Districts according to the Results

of the 2006 Population Census .............................................................................. 10 Table 3 Household Population, Number and Size (2006 Census) ...................................... 11 Table 4 Distribution of Population by Sex and Age (2008) ................................................. 12 Table 5 Number of students pursuing in Higher Education (2008-2009) ........................... 13 Table 6 Expected enrolments (number of students) .......................................................... 13 Table 7 Household Labour force Survey - Main Indicators (2009) ..................................... 13 Table 8 Employment According to Household Labour Force Survey 2008* ...................... 14 Table 9 Household Labour force Survey – Employed level of education (2009) ................ 15 Table 10 Number of beds and health personnel in TCc for 2008 ........................................ 16 Table 11 Basic macroeconomic indicators of the TCc economy (2002-2008) ...................... 18 Table 12 Sectoral Distribution of Gross Domestic Product .................................................. 20 Table 13 Sectoral Distribution of Fixed Capital Investments ................................................ 22 Table 14 Credits - Sectoral (Total) (31 -03-2010).................................................................. 22 Table 15 Production of main agricultural products (2008) .................................................. 23 Table 16 Number of livestock and main animal products (2008) ........................................ 24 Table 17 Number of accommodation establishments by regions and categories ............... 25 Table 18 Number of arrivals and departures to and from TCc by nationality for 2009 ....... 26 Table 19 Number of Tourists and bed nights in tourist accommodation establishments by

district for 2009 ...................................................................................................... 26 Table 20 Number of tourism establishments and number of employees working in the

tourism sector for 2009 ......................................................................................... 27 Table 21 Size of the Company and Region (or percentage of each size of the company in

the Region) ............................................................................................................. 31 Table 22 Balance of State Budget as a share in GNP ............................................................ 37 Table 23 Justification of the proposed strategic objectives based on the findings of the

SWOT analysis ........................................................................................................ 54 Table 24 Justification of the proposed strategic objectives based on the key barriers to

private sector development growth ...................................................................... 58

List of Figures

Figure 1 Methodology for drafting the Private Sector Development Strategy .................... 6 Figure 2 TCc Distribution of population among districts .................................................... 11 Figure 3 Distribution of TCc urban and rural population .................................................... 11 Figure 4 Distribution of urban and rural population among districts ................................. 11 Figure 5 TCc imports and exports by countries (in Million US $) for the period 2002-2008

............................................................................................................................... 19 Figure 6 Allocation of TCc’s imports and exports according to the countries (2008)......... 19 Figure 7 Number of arrivals and departures to and from TCc by nationality for 2009 ...... 26 Figure 8 Percentage (%) of Tourists by district for 2009..................................................... 27 Figure 9 Size of the business entity (company) according to the number of employees ... 31 Figure 10 Turkish Cypriot Community compared to global good practice economy as well as

selected economies ............................................................................................... 41

Sustainable Economic Development in TCc - Private Sector Development Strategy 2011 - 2015

Page | 4

List of Abbreviations

2G Second Generation

3D Three Dimensional

3G Third Generation

ADSL Asynchronous Digital subscriber Line

ATM Automated Teller Machine – Asynchronous Transfer Mode

B2B Business to Business

CDMA Code Divided Multiple Access

CNC Computer Numerical Control

EC European Commission

ECDL European Computer Driving License

EFT Electronic Fund Transfer

EMU East Mediterranean University

EU European Union

EUROSTAT Statistical Office of the European Union

F/O Fibre Optic

GDP Growth Domestic Product

GIS Geographical Information System

GSM Global System for Mobile

HACCP Hazard Analysis Critical Control Point

ICT Information and Communication Technologies

ISDN Integrated Services Digital Network

ISO International Organization for Standardization

ISP Internet Service Provider

KAMUNET Public Network Committee

KOBIGEM SME Development Centre (Kobi Gelistirme Merkezi)

KTEZO Chamber of Craftsment and Artisians (Kıbrıs Türk Esnaf Zanaatkarlar Odası)

KTTO Chamber of Commerce (Kıbrıs Türk Ticaret Odası)

KTSO Chamber of Industry (Kıbrıs Türk Sanayi Odası)

NACE Nomenclature générale des Activités économiques dans les Communautés Européennes

NGN Next Generation Network

NGO Non Governmental Organisation

PDH Plesiosynchronous Digital Hierarchy

POS Point of Sale

Sustainable Economic Development in TCc - Private Sector Development Strategy 2011 - 2015

Page | 5

PSDS Sustainable Economic Development in TCc - Private Sector Development Strategy

R&D Research and Development

SBA Small Business Act

SDH Synchronized Digital Hieracrchy

SME Small and Medium Sized Enterprise

SPO State Planning Office

SWOT Strengths, Weaknesses, Opportunities and Threats

TCc Turkish Cypriot community

TDM Time Division Multiplexing

US United States

USD United State Dollars

YAGA Investment Development Agency (Yatırm Geliştirme Ajansı)

VET Vocational Education and Training

Sustainable Economic Development in TCc - Private Sector Development Strategy 2011 - 2015

Page | 6

Chapter 1. Methodological Approach

The methodology applied for drafting the private sector development strategy of the Northern part of Cyprus, is depicted in the following figure:

Figure 1 Methodology for drafting the Private Sector Development Strategy

Private Sector Development Strategy

Identification of barriers

and needs

VISION /

STRATEGY

Actions

Objectives

STRENGTHS

.

WEAKNESSES

OPPORTUNITIES THREATS

SWOT ANALYSIS

Priorities /

Interventions

More analytically the tasks foreseen in the framework of the selected PSDS’ methodology include the following:

Task 1 - Analysis of current situation: During this task data collection and analysis for the northern part of the island in terms of its basic characteristics, such as physical, geographical, demographical, as well as its general socio economic context, such as basic economic drivers, productivity and growth; the labour market including the structure of employment, unemployment and skills levels, as well as the share of the three sectors (agriculture, industry and services) in its economy, will take place. The sources of information that will be used for drafting the baseline analysis include:

Statistics from various stakeholders (e.g. Eurostat, local statistics services, YAGA, State Planning Organization, etc)

Other related project reports

Previous Studies and reports

Task 2 - SWOT analysis: Having completed the baseline analysis of the current situation the next step refers to the deployment of a strategic SWOT analysis, namely establishing the TCc current position in the light of its strengths, weaknesses, opportunities and threats.

SWOT analysis is a tool for assessing and communicating the current position of a particular reform option in terms of its internal Strengths and Weakness and the external Opportunities and Threats it faces. It provides a clear basis on which to develop a picture of the changes needed to build on strengths, minimise weaknesses, and take advantage of

Sustainable Economic Development in TCc - Private Sector Development Strategy 2011 - 2015

Page | 7

opportunities and deal with threats Moreover SWOT-Analysis involves specifying the objective of the project and identifying the internal and external factors that are favourable and unfavourable to achieving that objective. The objective of the SWOT is to determine to what degree the actual strategy is suitable and appropriate to meet the challenges and changes in the current environment. The value of the SWOT analysis lies mainly in the fact that it constitutes a self assessment for the private sector development strategy implementation in the northern part of the island.

Task 3 – Identification of barriers and needs: The completion of the above mentioned SWOT analysis will lead to the definition of the barriers and local needs of the TCc, in terms of promoting private sector development and increasing the competitiveness of the TCc economy. Emphasis will be given in the rational determination of TCc’s existing barriers and needs, as well as in setting them in order of precedence (hierarchy of needs) since they will be the base for the private sector development strategy approach in the next task.

Task 4 – Strategic planning: This task includes the process of defining the TCc private sector development strategy, or direction, and making decisions on allocating its resources to pursue this strategy, including its capital and people. Strategic planning is a very important activity, which ends with objectives and a roadmap of priorities to achieve those objectives. In this framework, a specific vision - strategy for developing the private sector of the northern part of the island will be formed, in terms of improving the private sector’s competitiveness.

More analytically the Vision defines where the TCc wants to be in the future. It reflects the optimistic view of the community’s future. The vision statement must be SMART, namely

Specific

Measurable

Achievable Relevant

Time bound

At the same time the Strategy defines the way to implement this vision and make it true. Then this strategy will be specialized in particular Objectives, which in fact aim at addressing the specific intervention areas of the TCc private sector. Objectives, in fact, constitute the specific, time bound statements of intended future results.

These objectives will be translated into thematic priorities and intervention areas aiming at covering the identified local needs, so that the foreseen increase of competitiveness will be accomplished. Finally, the above mentioned intervention areas will be specified into specific

Sustainable Economic Development in TCc - Private Sector Development Strategy 2011 - 2015

Page | 8

actions that will be carried out by the local authorities and stakeholders in order to address the particular needs of the TCc, in terms of Private Sector Development and SMEs competitiveness improvement and entrepreneurship promotion.

Sustainable Economic Development in TCc - Private Sector Development Strategy 2011 - 2015

Page | 9

Chapter 2. Socio-Economic analysis of Northern Cyprus current situation

2.1. Country Information

2.1.1. Geography

Cyprus is situated in the Eastern Mediterranean Sea, at the hub of three continents where the trade routes intersect. It is the third largest island in the Mediterranean Sea after Sicily and the Sardinia. The total area of the island covers 9,251 square kms.

Northern Cyprus (Turkish: Kuzey Kıbrıs) is a de facto state located in the northern portion of the island of Cyprus.

The area of the Turkish Cypriot community is 3,242 square kms. The nearest neighbouring country is Turkey which lies at a distance of 65 kms to the north.

The northern part of Cyprus is a region divided into five districts as shown in the map above:

Nicosia (Lefkoşa)

Famagusta (Mağusa)

Kyrenia (Girne)

Morphou (Güzelyurt)

Trikomo (İskele)

The capital Nicosia is the largest city of the TCc. The other major towns are Famagusta and Kyrenia which are located on the coast.

The official language is Turkish but English is widely spoken and understood in official and commercial circles.

The religion is Islam, with Muslims making up 99% of the population.

Sustainable Economic Development in TCc - Private Sector Development Strategy 2011 - 2015

Page | 10

2.1.2. Climate

The northern part of Cyprus has a typical Mediterranean climate with about 300 days of sunshine per year. It enjoys dry, warm summers and mild winters. The bulk of the rain falls during the period from November to March. The coldest month is January having minimum and maximum mean temperatures of 6 oC and 16oC respectively. In the hottest month August the corresponding minimum and maximum mean temperatures are 21oC and 35oC.

2.1.3. Demographic characteristics

According to the final results of the Census of Population and Housing Unit, which was held on 30 April 2006, the de-facto population of TCc is 256,644. The population density is 79.16 persons per square km.

In the following table information about population development, population increase rate (%) and population density are shown regarding the period 2003-2008, according to the SPO statistics. It is pointed out that for numbers related to the years after 2006 are projections based on the General Population and Housing Unit Census.

Table 1 Population Basic Indicators (2002-2008)

Indicator 2002 2003 2004 2005 2006 2007 2008

Population 213,491 215,790 218,066 220,289 257,513 11 268,011 274,436

Population Increase Rate (%) 1.1 1.1 1.1 1.0 16.9 4.1 2.4

Population Density 65.9 66.6 67.3 68.0 79.4 82.7 84.7

Crude Birth Rate (Per Thousand) 15.0 15.0 16.0 16.0 14.9 15.0 15.4

Crude Death Rate (Per Thousand)8.0 8.0 8.0 7.0 6.7 6.8 6.8

Natural Increase Rate (%) 0.7 0.7 0.8 0.9 0.8 0.9 0.9

Infant Mortality Rate (Per

Thousand Live Birth)10.0 10.0 10.0 9.0 15.8 15.0 14.3

Total Fertil ity Rate 1.8 1.8 1.9 1.9 1.8 1.8 1.8

Life Expectancy at Birth (Year)4

Male 71.0 71.0 71.0 71.0 71.4 71.5 71.7

Female 75.6 75.6 75.6 75.6 76.0 76.2 76.4

* Since 2006 mid-year de-jure population projections based on the General Population and Housing Unit Census are indicated, Source: State Planning Organization

Table 2 Distribution of Population by Districts and Sub-Districts according to the Results of the 2006 Population Census

District Total Urban Rural

Total 256,644 146,831 109,813

Nicosia 84,776 56,052 28,724

Famagusta 63,603 39,231 24,372

Kyrenia 57,902 24,876 33,026

Morfou 29,264 19,923 9,341

Trikomo 21,099 6,749 14,350 Source: State Planning Organization

Sustainable Economic Development in TCc - Private Sector Development Strategy 2011 - 2015

Page | 11

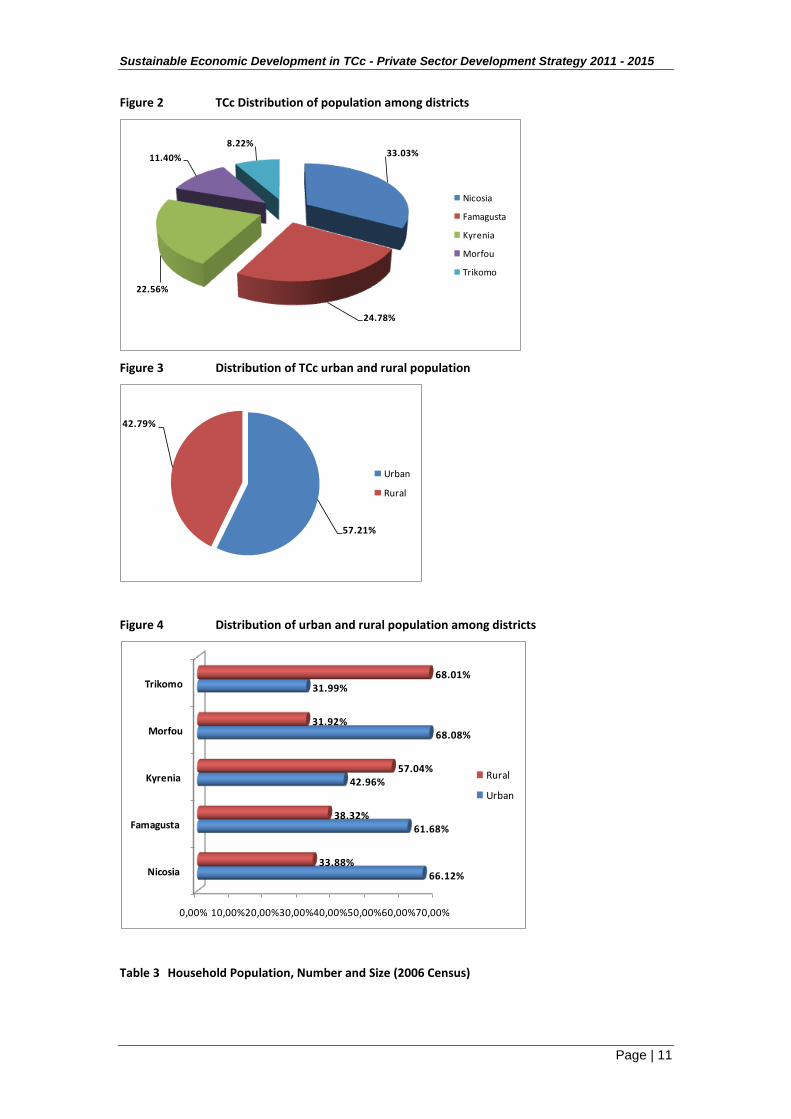

Figure 2 TCc Distribution of population among districts

33.03%

24.78%

22.56%

11.40%

8.22%

Nicosia

Famagusta

Kyrenia

Morfou

Trikomo

Figure 3 Distribution of TCc urban and rural population

57.21%

42.79%

Urban

Rural

Figure 4 Distribution of urban and rural population among districts

0,00% 10,00%20,00%30,00%40,00%50,00%60,00%70,00%

Nicosia

Famagusta

Kyrenia

Morfou

Trikomo

66.12%

61.68%

42.96%

68.08%

31.99%

33.88%

38.32%

57.04%

31.92%

68.01%

Rural

Urban

Table 3 Household Population, Number and Size (2006 Census)

Sustainable Economic Development in TCc - Private Sector Development Strategy 2011 - 2015

Page | 12

District

Total

number of Urban Rural

Total 71,376 55,335 16,041

Nicosia 22,869 20,173 2,696

Famagusta 18,363 13,187 5,176

Kyernia 15,893 14,473 1,420

Morphou 8,509 5,361 3,148

Trikomo 5,742 2,141 3,601 Source: State Planning Organization

As far as the life expectancy at birth rate is concerned in 2008 the relative number was 71,7 years for male and 76,4 years for female, while the natural population increase rate seems to be steady over the last 10 years (1999- 2008) in the levels of 0,9%.

In the following table the distribution of TCc Population by Sex and Age is depicted. More than half of the population (54.57%) is male, while the majority of the total TCc population is between 20 and 44 years of old (48%).

Table 4 Distribution of Population by Sex and Age (2008)

Age Total Male Female

Total 279,064 152,295 126,769

0-4 17,391 8,902 8,489

5-9 15,752 8,062 7,691

10-14 16,346 8,443 7,691

15-19 24,745 13,713 11,032

20-24 39,991 24,396 15,595

25-29 29,573 17,579 11,994

30-34 25,663 14,553 11,110

35-39 19,912 11,066 8,846

40-44 17,996 9,870 8,126

45-49 16,707 8,841 7,866

50-54 14,288 7,445 6,843

55-59 11,888 6,173 5,715

60-64 9,359 4,633 4,726

65-69 6,943 3,288 3,655

70-74 5,258 2,31 2,948

75+ 7,251 3,021 4,23

Total 100.0 100.0 100.0 Source: State Planning Organization

2.1.4. Education

The education system in the TCc consists of pre-school education, primary education, secondary education and higher education. More analytically:

Pre-school education is provided by kindergartens for children between the ages of 5 and 6

Primary education is provided by elementary schools and designed for the 7-11 age group, it lasts for 5 years and is free of charge and compulsory

Secondary education is provided at 2 stages: First stage is lasting for three years, is intended for children in the 12-14 age group and is free of charge and compulsory. Second stage is designed for the 15-18 age group and has a 4 year programme of instruction.

Higher education is provided by the 6 Universities that operate in the northern part of Cyprus

Sustainable Economic Development in TCc - Private Sector Development Strategy 2011 - 2015

Page | 13

The education level in the TCc is high and the education sector is one of the biggest sectors of the TCc economy.

In particular, the existing Universities have a great number of students. There are 6, 2 semi-public and 4 private, universities operating in the region. The approximate number of students is as follows:

Table 5 Number of students pursuing in Higher Education (2008-2009)

University name Number of

Students

Eastern Mediterranean University 13,255

Girne/ Kyrenia American University 4,936

Near East University 14,270

European University of Nicosia 3,529

Cyprus International University 4,348

Middle East Technical University, Northern Cyprus Campus1,243

Total number of students 41,581 * Data for 2008-2009 academic semester Source: Universities, State Planning Organization

The following table shows expected number of students in the next few years. (Note: One of the new universities will have online-higher education).

Table 6 Expected enrolments (number of students)

2010-2011 2015-2016

Eastern Mediterranean University 17,000 20,000

Girne/ Kyrenia American University 10,000 13,000

Near East University 15,000 15,000

European University of Nicosia 5,000 7,000

Cyprus International University 5,000 6,000

Middle East Technical University, Northern Cyprus Campus3,000 6,000

Total number of students 55,000 67,000

Expected enrolments

(number of students)University name

Source: YAGA – TCc Investment Development Agency

2.1.5. Labour force and employment

With reference to the Labour Market, TCc’ labour force consists of about 104,491 people

- 91,550 or 87.6% employed and

- 12,941 or 12.4% of which are not employed

according to 2009 Household Labour force Survey. The majority of the employed labour force is engaged in the services sector (46%) followed by the public sector (30.2%), construction (10%), industry (9%) and agriculture (4.8%).

The following table shows the main indicators for the Household Labour Force as per a Survey of 2009 by the State Planning Office:

Table 7 Household Labour force Survey - Main Indicators (2009)

Sustainable Economic Development in TCc - Private Sector Development Strategy 2011 - 2015

Page | 14

Indicators Total Nicosia Famagusta Kyrenia Morfou Trikomo

Non-corporate* Civilian Population age 15 or Over 209,310 70,586 50,589 49,473 22,355 16,307

Workforce 104,491 38,099 22,865 25,943 10,590 6,992

Employed 91,550 33,797 20,037 22,747 9,063 5,905

Unemployed 12,941 4,302 2,828 3,196 1,527 1,087

Rate of Inclusion in Workforce (%) 49.9% 54.0% 45.2% 52.4% 47.4% 42.9%

Employment Rate (%) 43.7% 47.9% 39.6% 46.0% 40.5% 36.2%

Unemployment Rate (%) 12.4% 11.3% 12.4% 12.3% 14.4% 15.5%

Unemployment Rate in Young Population ** 31.4% 31.5% 31.5% 28.5% 27.1% 43.9%

* Non-corporate civilian population: excludes those living in schools, dormitories, hotels, nurseries, rehabilitation centres, hospitals, penitentiaries, barracks and other army accommodations. ** Population between 15 -24 Source: State Planning Organization

Table 8 Employment According to Household Labour Force Survey 2008*

Sectors 2004 % 2005 % 2006 % 2007 % 2008 %

1. Agriculture, Forestry, Hunting, Fishing

7,278,00 8.4 4,681,00 5.5 4,378.00 4.8 3,170.00 3.5 3,171.00 3.5

2. Mining. Quarrying 114.00 0.1 144.00 0.2 113.00 0.1 115.00 0.1 113.00 0.1

3. Manufacturing 9,490.00 10.9 8,440.00 9.9 8,006.00 8.7 7,679.00 8.5 7,171.00 7.9

4. Electricity. Gas. Water 607.00 0.7 641.00 0.7 644.00 0.7 1,103.00 1.2 860.00 0.9

5. Construction. Public Works

8,079.00 9.3 8,375.00 9.8 9,590.00 10.4 9,664.00 10.8 10,491.00 11.5

6. Wholesale-Retail Trade 14,130.00 16.3 14,563.00 17.0 16,757.00 18.3 17,340.00 19.3 16,123.00 17.7

7. Restaurants. Hotels 5,039.00 5.8 4,942.00 5.8 5,755.00 6.3 5,493.00 6.1 5,941.00 6.5

8. Transport. Communication. Storage

5,289.00 6.1 5,378.00 6.3 5,250.00 5.7 5,017.00 5.6 6,082.00 6.7

9. Financial Institutions 3,403.00 3.9 3,044.00 3.5 3,541.00 3.9 3,142.00 3.5 3,638.00 4.0

10. Property Renting 3,595.00 4.1 4,261.00 5.0 3,319.00 3.6 4,120.00 4.6 3,004.00 3.3

11. Public Administration 13,309.00 15.3 14,346.00 16.8 14,969.00 16.3 14,344.00 16.0 14,854.00 16.3

12. Educational Services 8,576.00 9.9 9,120.00 10.6 9,743.00 10.6 9,479.00 10.6 9,715.00 10.6

13. Health Services 2,545.00 2.9 2,470.00 2.9 2,931.00 3.2 3,013.00 3.4 2,907.00 3.2

14. Other Community Services

5,460.00 6.3 5,178.00 6.0 6,821.00 7.4 6,108.00 6.8 7,151.00 7.8

Total 86,914.00 100.0 85,583.00 100.0 91,817.00 100.0 89,787.00 100.0 91,221.00 100.0

* Sectoral figures may not add up to the general total due to rounding. Source: State Planning Organization

According to the above figure the 17.7% of TCc employers work in Wholesale and retail trade; 16.3% work in Public Administration, 11.5% work in Construction and Public works, while on the other hand the lowest rates are presented in mining and quarrying and electricity gas and water activities (0.1% and 0.9% respectively).

The following table presents data on the level of education of the employed people of the TCc (labour force according to 2009 Household Labour force Survey).

Sustainable Economic Development in TCc - Private Sector Development Strategy 2011 - 2015

Page | 15

Table 9 Household Labour force Survey – Employed level of education (2009)

Education Level

Sector No education Primary School

Technical Primary School

Junior high school or

other equivalent

General high school

Technical High school

University, college

Master, Doctorate

1. Agriculture, Forestry, Hunting, Fishing

512 2,282 0 435 600 384 198 22

2. Mining, Quarrying 0 41 0 65 0 0 0 0

3. Manufacturing 229 3,650 0 937 1,018 654 773 52

4. Electricity, Gas, Water 0 293 0 156 197 203 84 18

5. Construction, Public Works 401 4,348 0 1,392 981 708 1,238 137

6. Wholesale-Retail Trade 284 4,674 35 2,013 4,315 1,795 2,329 164

7. Restaurants, Hotels 46 1,335 0 453 1,133 638 1,139 129 8. Transport, Communication, Storage

279 2,164 0 1,712 1,780 560 741 80

9. Financial Institutions 0 182 0 223 1,113 651 1,269 340

10. Property Renting 153 823 0 359 1,010 209 1,491 135

11. Public Administration 220 2,376 0 1,316 5,036 1,909 4,114 447

12. Educational Services 56 1,177 0 511 639 615 5,264 1,921 13. Health services and other social service activities

32 381 0 202 392 467 979 82

14. Other Community Services

128 1,184 0 916 1,623 587 1,121 100

Total 2,339 24,909 35 10,689 19,837 9,378 20,738 3,626

% of education level as per total employed people

2.55% 27.21% 0.04% 11.68% 21.67% 10.24% 22.65% 3.96%

Number of employees working in a firm

Level of education

No education Primary School

Technical Primary School

Junior high school or

other equivalent

General high school

Technical High school

University, college

Master, Doctorate

Total

1 - 10 employees 1,328 12,632 0 4,988 7,022 3,022 5,756 565 35,314

11 - 19 employees 440 3,595 0 1,894 2,431 1,448 2,889 350 13,046

20 - 49 employees 129 3,156 35 1,185 2,475 1,291 3,280 411 11,962

more than 50 employees 441 5,526 0 2,621 7,909 3,618 8,813 2,299 31,227

TOTAL 2,339 24,909 35 10,689 19,837 9,378 20,738 3,626 91,550

* Sectoral figures may not add up to the general total due to rounding. Source: State Planning Organization

The above data shows that there is a very satisfying and favourable picture regarding the active labour force education level, since the 22.65% of the employed have a university degree while the 43.6 % have a high school certificate.

Guidance in the Employment Sector

In the northern part of the island, body in charge of labour and social security has four major departments, one of which is Employment Services (ES). The ES has five branches located in Nicosia, Kyrenia, Morphou, Famagusta and Trikomo. The ES is providing the employers and employees/job seekers with a variety of services, e.g., including work permits, job matching, inspections and very limited active labour market programmes.

There is, however, no career counselling service being provided to the employed and unemployed people.

Since economic conditions are changing rapidly at local and international level, there is need to reorganize and restructure this department, in order to adjust to the new environment, by utilising new methods and modern information technology based techniques that will contribute to the provision of efficient career guidance and counselling services to all potential employers and employees.

Education Initiatives

The education level in the northern part of the island is high. In this framework the public authority regarding Education, Sports and Youth has planned and working on the

Sustainable Economic Development in TCc - Private Sector Development Strategy 2011 - 2015

Page | 16

development of technical high schools and training centres, to support the labour market with educated and skilled technical staff. Furthermore the other public authorities of the TCc are supporting this kind of projects, by collaborating with NGOs (Chambers and Educational Centres) to create a better working environment.

Additionally, there is a variety of training centres offering formal and informal training to the unemployed, employed, men and women. In the northern part there are six universities, most of which have a “Continuing Education Centre.” The centres offer a variety of courses and training programmes to individual and institutional clients. There is, however, lack of information system through which people get informed about the variety of learning opportunities. Within this context, career counselling services would increase the access to lifelong learning facilities and to the labour market.

2.1.6. Physical and social infrastructure

This section includes brief information on the physical and social infrastructure and services in the northern part of the island. Public Services in the TCc include such spheres as healthcare, education, public transportation, fire and police services, electricity and gas, water services, waste management. Being a government-funded sector, public services are provided by state institutions for free (such as hospitals, schools, police department), thus guaranteed to be available for all the citizens regardless their social position or income. In this framework the following are mentioned:

As far as health services are concerned, the following table demonstrates some basic data regarding hospitals and medical facilities in the northern part of the island.

Table 10 Number of beds and health personnel in TCc for 2008

1. Number of Beds Public 971

Private 240

Total 1,211

2. Specialist Public 228

Private 256

Total 484

3. Practitioner Public 23

Private 50

Total 73

4. Dentist Public 21

Private 119

Total 140

5. Pharmacist Public 17

Private 159

Total 176

6. Nurse Public 663

7. Mid - Wife Public 10 Source: Ministry of Health, State Planning Organization

The structure of the health service is represented by hospital services; and primary care (dentists, opticians and pharmacists generally provide services as independent contractors). Hospitals are the major health care facilities in the TCc. There are general hospitals and medical facilities in all the towns (about 8 main hospitals exist). They provide with large numbers of beds for intensive care and long-term care as well as specialized facilities for surgery, childbirth, bioassay laboratories, etc. Private medical services are represented by clinics run by a private partnership of physicians. Clinics generally provide only outpatient services. Health centres provide services for ambulatory patients (as opposed to inpatients treated in a hospital). Some centres accept people with injuries or illnesses, which are not

Sustainable Economic Development in TCc - Private Sector Development Strategy 2011 - 2015

Page | 17

serious enough for a visit to an emergency room. In these cases patients are examined by medical professionals. If patients need to be examined by a specialist, they are referred to hospitals or private physicians.

In this framework it has to be noted that as far as private health centres are concerned, over the last few years the level of their services has been upgraded and they are operating according to international quality standards.

There is a private transport system of buses and mini buses in TCc operating within and between towns during the day. Since 1974, rail transport in the northern part of the island is inactive. A national railway company has never been founded, and old rail stations are abandoned. Regarding air transportation there is one airport operating in the northern part of the island (Ercan airport). Furthermore there are two seaports in Famagusta and Kyrenia operating at the moment.

With regard to the TCc cultural and historical heritage there are lots of castles, museums, monasteries that a visitor can go to and learn about the island's life and history. In particular there are about 30 museums operating in the northern part (6 in Nicosia, 11 in Famagusta , 9 in Kyrenia and 4 in Morphou).

Lastly as far as the water resources are concerned, it is pointed out that in July 2010 a protocol was signed between the TCc and Turkey to deliver 75 million cubic meter of water from Turkey to Cyprus every year. The project will be completed in 4 years and it planned start implementing the project (laying down its foundation) this autumn.

From a submarine barrage in the area of Mersin a system of pipeline will be built between Cyprus to Turkey to bring water, not only for the northern part of the island but for the entire island of Cyprus.

The project will be completed in three phases; the first phase is related to a tender contract of the submarine barrage in Mersin. The total cost of the project is 450 million dollars and this cost will be covered by Turkish budget.

Sustainable Economic Development in TCc - Private Sector Development Strategy 2011 - 2015

Page | 18

2.2. Macro-economic background

During the last decade Northern Cyprus experienced a constant economic development and the real growth rate in the period 2000 - 2006 was increased from -0.6% to 13.2%, while for the years 2007 & 2008 it was considerable decreased to 1.5% and -3.4% respectively.

In 2004 the growth indicator of Northern Cyprus rose to 15.4 %. At the same time, the effort of reduction of inflation had as result a decrease from the 76.8 % in 2001 in the 2.7% in 2005 and 14.5% in 2008. It is pointed out that the inflation increase during the years 2006-2008 was mainly based on the relevant inflation increase of the Turkish economy.

The TCc applies a free market economy approach. Turkish Lira is the official currency used in the area where the stability of the macro economy has had positive progresses in the recent years.

Below are presented some macroeconomic indicators which can offer an overall picture on the status of the TCc economy.

Table 11 Basic macroeconomic indicators of the TCc economy (2002-2008)

Indicator 2002 2003 2004 2005 2006 2007 2008

GNP (Million $) 941,4 1,283.7 1,765.2 2,327.8 2,845.2 3,598.8 3.995,6

Real Growth Rate (%) 6.9 11.4 15.4 13.5 13.2 1.5 -3.4

GNP Per Capita (Current Prices TL/YTL)1 6,645,260,285 8,837,624,376 11,560 14,271 17,063 19,165 20,739

GNP Per Capita ($) 4,409 5,949 8,095 10,567 11,837 14,765 16,158

Inflation Rate (%) 24.5 12.6 11.6 2.7 19.2 9.4 14.5

Budget Deficit (Million $)2 225.1 176.9 104.2 185.3 287.3 221.2 369.6

Bank Deposits (Million $)3 1,153.5 1,785.9 2,355.8 2,707.4 3.330,4 4.239,2 3.678,6

Foreign Exchange Reserves (Million $) 941.6 1,222.6 1,544.6 1,597.6 2,030.9 2,072.1 1,802.6

Export (Million $) 45.4 50.8 62.0 68.1 68.1 83.7 83.7

Import (Million $) 309.6 477.8 853.1 1,255.5 1,376.2 1,539.2 1,680.7

Foreign Trade Balance (Million $) -264.2 -427.0 -791.1 -1,187.4 -1,308.1 -1,455.5 -1,597.0

Export / Import(%) 14.7 10.6 7.3 5.4 4.9 5.4 5.0

1 Indicated as New Turkish Lira from 2005. 2 Indicates the fiscal balance in the balance of state budget table 3 Includes Turkish Lira and foreign currency deposits Source: State Planning Organization

According to the data demonstrated in the previous table, until 2007, TCc presented an increased growth rate, which in 2008 decreased following the trends of the European Union, regarding real GDP growth rate1 indicator. Despite its small size of economy, TCc has one of the highest growth rates among European Union countries, which constitutes a potential advantage for business development.

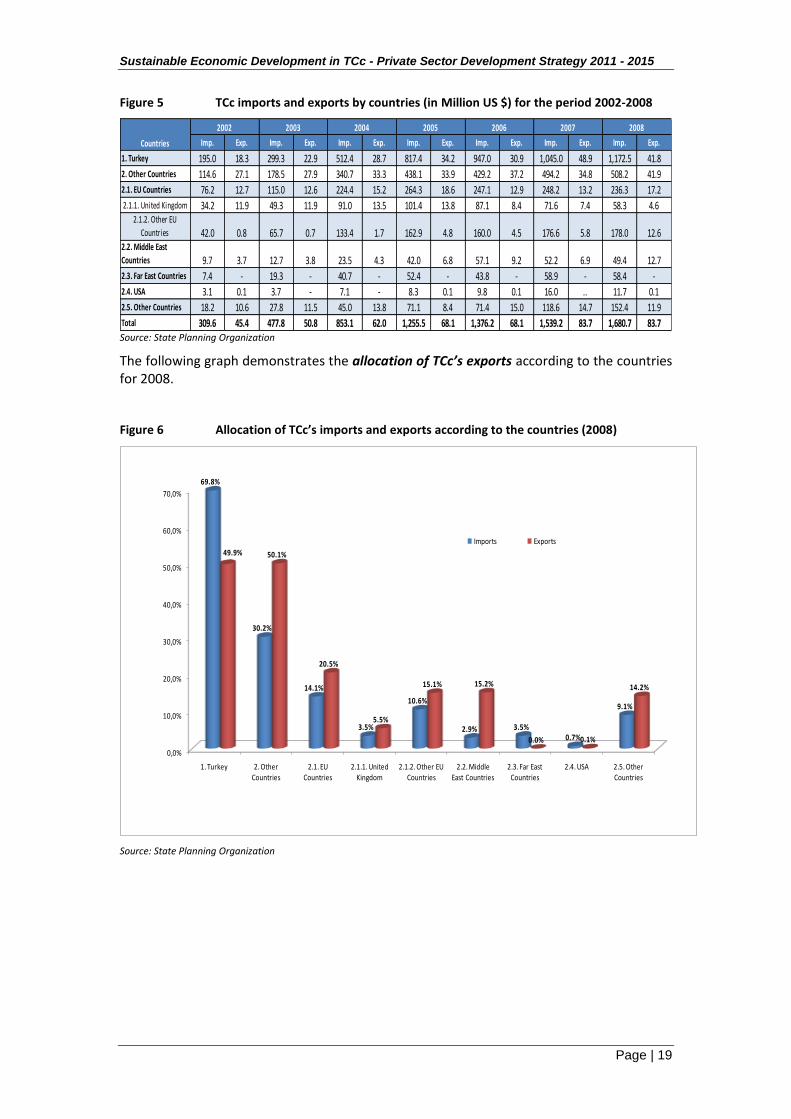

As far as imports and exports are concerned the following table shows their composition per country.

The data presented reflects that TCc products are mainly exported in Turkey and east countries, while the export rates in EU countries are rather low.

1 Reference:

http://epp.eurostat.ec.europa.eu/tgm/table.do?tab=table&init=1&language=en&pcode=tsieb020&plugin=1

Sustainable Economic Development in TCc - Private Sector Development Strategy 2011 - 2015

Page | 19

Figure 5 TCc imports and exports by countries (in Million US $) for the period 2002-2008

Imp. Exp. Imp. Exp. Imp. Exp. Imp. Exp. Imp. Exp. Imp. Exp. Imp. Exp.

1. Turkey 195.0 18.3 299.3 22.9 512.4 28.7 817.4 34.2 947.0 30.9 1,045.0 48.9 1,172.5 41.8

2. Other Countries 114.6 27.1 178.5 27.9 340.7 33.3 438.1 33.9 429.2 37.2 494.2 34.8 508.2 41.9

2.1. EU Countries 76.2 12.7 115.0 12.6 224.4 15.2 264.3 18.6 247.1 12.9 248.2 13.2 236.3 17.2

2.1.1. United Kingdom 34.2 11.9 49.3 11.9 91.0 13.5 101.4 13.8 87.1 8.4 71.6 7.4 58.3 4.62.1.2. Other EU

Countries 42.0 0.8 65.7 0.7 133.4 1.7 162.9 4.8 160.0 4.5 176.6 5.8 178.0 12.62.2. Middle East

Countries 9.7 3.7 12.7 3.8 23.5 4.3 42.0 6.8 57.1 9.2 52.2 6.9 49.4 12.7

2.3. Far East Countries 7.4 - 19.3 - 40.7 - 52.4 - 43.8 - 58.9 - 58.4 -

2.4. USA 3.1 0.1 3.7 - 7.1 - 8.3 0.1 9.8 0.1 16.0 .. 11.7 0.1

2.5. Other Countries 18.2 10.6 27.8 11.5 45.0 13.8 71.1 8.4 71.4 15.0 118.6 14.7 152.4 11.9

Total 309.6 45.4 477.8 50.8 853.1 62.0 1,255.5 68.1 1,376.2 68.1 1,539.2 83.7 1,680.7 83.7

2007 2008

Countries

2002 2003 2004 2005 2006

Source: State Planning Organization

The following graph demonstrates the allocation of TCc’s exports according to the countries for 2008.

Figure 6 Allocation of TCc’s imports and exports according to the countries (2008)

0,0%

10,0%

20,0%

30,0%

40,0%

50,0%

60,0%

70,0%

1. Turkey 2. Other Countries

2.1. EU Countries

2.1.1. United Kingdom

2.1.2. Other EU Countries

2.2. Middle East Countries

2.3. Far East Countries

2.4. USA 2.5. Other Countries

69.8%

30.2%

14.1%

3.5%

10.6%

2.9% 3.5%0.7%

9.1%

49.9% 50.1%

20.5%

5.5%

15.1% 15.2%

0.0% 0.1%

14.2%

Imports Exports

Source: State Planning Organization

Sustainable Economic Development in TCc - Private Sector Development Strategy 2011 - 2015

Page | 20

2.3. Private Sector - Business environment

2.3.1. Identification of key sectors

The economy of Turkish Cypriot community is dominated by the services sector (77.1% of GDP in 2008), which includes Trade-Tourism, Transport-Communication, Financial Institutions, Ownership of Dwellings, Business and Personal Services, Public Services and Import Duties. Industry (light manufacturing & construction) contributes 17.8% of GDP and agriculture 5.1%. [Source: SPO]. Sectors in TCc have gone through a number of significant changes in the last few years.

Over the last 30 years, the structure of the economy has shifted from agriculture to tourism, construction and industry. Like other small island economies, the economic structure is less diverse and the service sector is the back bone of the economy. The following tables present the sectoral development in gross national product in the TCc.

Table 12 Sectoral Distribution of Gross Domestic Product

(current Prices, % )

Sectors 2002 2003 2004 2005 2006 2007 2008

1. Agriculture 8.9 9.4 9.1 7.0 6.3 6.3 5.1

1.1. Crop Production 5.4 5.8 5.5 3.7 3.2 3.5 2.7

1.2. Livestock Production 3.1 3.3 3.1 2.8 2.7 2.4 2.1

1.3. Forestry .. .. .. .. .. .. ..

1.4. Fishing 0.4 0.3 0.4 0.4 0.3 0.3 0.3

2. Industry 11.2 10.2 9.4 9.2 9.5 9.4 10.7

2.1. Quarrying 0.6 0.6 0.5 0.6 1.0 1.1 0.8

2.2. Manufacturing 5.3 5.2 4.8 4.8 4.5 4.4 4.0

2.3. Electricity - Water 5.4 4.4 4.0 3.8 3.9 3.9 5.9

3. Construction 4.4 5.0 4.3 5.4 7.9 7.9 7.1

4. Trade-Tourism 15.3 16.0 15.9 17.6 15.5 13.7 14.2

4.1. Wholesale and Retail Trade

9.5 9.6 10.8 12.1 11.4 9.5 9.7

4.2. Hotels and Restaurants 5.8 6.4 5.2 5.6 4.1 4.2 4.5

5. Transport-Communication 13.2 11.8 10.5 10.7 11.0 11.6 12.1

6. Financial Institutions 6.4 6.1 7.6 6.4 6.5 6.7 7.0

7. Ownership of Dwellings 2.9 2.7 2.5 2.3 3.0 3.1 3.5

8. Business and Personal Services

9.9 8.1 9.2 10.0 11.1 10.7 10.3

9. Public Services 19.7 21.6 20.8 20.5 20.3 21.8 21.7

10. Import Duties 8.1 9.1 10.7 11.0 9.1 8.8 8.2

GDP 100.0 100.0 100.0 100.0 100.0 100.0 100.0

Sustainable Economic Development in TCc - Private Sector Development Strategy 2011 - 2015

Page | 21

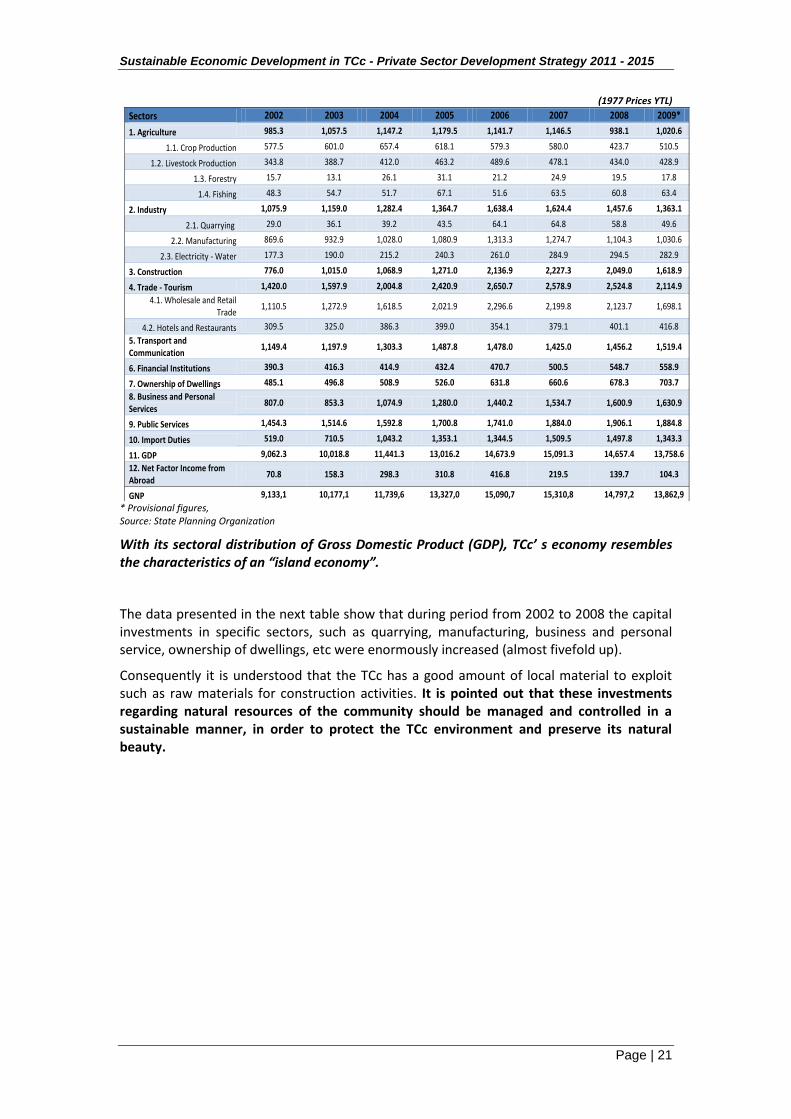

(1977 Prices YTL)

Sectors 2002 2003 2004 2005 2006 2007 2008 2009*

1. Agriculture 985.3 1,057.5 1,147.2 1,179.5 1,141.7 1,146.5 938.1 1,020.6

1.1. Crop Production 577.5 601.0 657.4 618.1 579.3 580.0 423.7 510.5

1.2. Livestock Production 343.8 388.7 412.0 463.2 489.6 478.1 434.0 428.9

1.3. Forestry 15.7 13.1 26.1 31.1 21.2 24.9 19.5 17.8

1.4. Fishing 48.3 54.7 51.7 67.1 51.6 63.5 60.8 63.4

2. Industry 1,075.9 1,159.0 1,282.4 1,364.7 1,638.4 1,624.4 1,457.6 1,363.1

2.1. Quarrying 29.0 36.1 39.2 43.5 64.1 64.8 58.8 49.6

2.2. Manufacturing 869.6 932.9 1,028.0 1,080.9 1,313.3 1,274.7 1,104.3 1,030.6

2.3. Electricity - Water 177.3 190.0 215.2 240.3 261.0 284.9 294.5 282.9

3. Construction 776.0 1,015.0 1,068.9 1,271.0 2,136.9 2,227.3 2,049.0 1,618.9

4. Trade - Tourism 1,420.0 1,597.9 2,004.8 2,420.9 2,650.7 2,578.9 2,524.8 2,114.9

4.1. Wholesale and Retail Trade

1,110.5 1,272.9 1,618.5 2,021.9 2,296.6 2,199.8 2,123.7 1,698.1

4.2. Hotels and Restaurants 309.5 325.0 386.3 399.0 354.1 379.1 401.1 416.8

5. Transport and Communication

1,149.4 1,197.9 1,303.3 1,487.8 1,478.0 1,425.0 1,456.2 1,519.4

6. Financial Institutions 390.3 416.3 414.9 432.4 470.7 500.5 548.7 558.9

7. Ownership of Dwellings 485.1 496.8 508.9 526.0 631.8 660.6 678.3 703.7

8. Business and Personal Services

807.0 853.3 1,074.9 1,280.0 1,440.2 1,534.7 1,600.9 1,630.9

9. Public Services 1,454.3 1,514.6 1,592.8 1,700.8 1,741.0 1,884.0 1,906.1 1,884.8

10. Import Duties 519.0 710.5 1,043.2 1,353.1 1,344.5 1,509.5 1,497.8 1,343.3

11. GDP 9,062.3 10,018.8 11,441.3 13,016.2 14,673.9 15,091.3 14,657.4 13,758.6

12. Net Factor Income from Abroad

70.8 158.3 298.3 310.8 416.8 219.5 139.7 104.3

GNP 9,133,1 10,177,1 11,739,6 13,327,0 15,090,7 15,310,8 14,797,2 13,862,9 * Provisional figures, Source: State Planning Organization

With its sectoral distribution of Gross Domestic Product (GDP), TCc’ s economy resembles the characteristics of an “island economy”.

The data presented in the next table show that during period from 2002 to 2008 the capital investments in specific sectors, such as quarrying, manufacturing, business and personal service, ownership of dwellings, etc were enormously increased (almost fivefold up).

Consequently it is understood that the TCc has a good amount of local material to exploit such as raw materials for construction activities. It is pointed out that these investments regarding natural resources of the community should be managed and controlled in a sustainable manner, in order to protect the TCc environment and preserve its natural beauty.

Sustainable Economic Development in TCc - Private Sector Development Strategy 2011 - 2015

Page | 22

Table 13 Sectoral Distribution of Fixed Capital Investments

(Current Prices YTL)

Sectors 2002 2003 2004 2005 2006 2007 2008

1. Agriculture 15,876,418.2 19,505,376.0 25,067,329.5 30,288,995.7 37,031,696.5 25,096,397.8 33,118,594.9

2. Industry 22,529,433.0 40,640,073.2 70,693,090.7 84,573,998.0 154,480,514.6 188,370,607.1 199,708,263.8

2.1. Quarrying 240,120.0 581,744.8 730,071.1 1,210,690.9 1,494,338.6 1,716,774.9 1,708,417.6

2.2. Manufacturing 14,629,250.3 26,897,248.7 55,959,681.7 59,725,765.6 66,640,455.5 69,492,101.5 68,504,697.8

2.3. Electricity - Water 7,660,062.7 13,161,07.,7 14,003,337.9 23,637,541.5 86,345,720.5 117,161,730.7 129,495,148.4

3. Construction 4,327,423.0 8,909,608.5 21,259,857.0 43,258,675.4 34,687,310.1 20,913,624.0 14,016,685.2

4. Trade-Tourism 19,239,532.6 35,370,682.2 55,650,643.9 68,847,433.3 90,649,789.0 101,226,532.6 82,215,951.7

4.1. Trade 8,838,60.5 14,210,973.8 25,636,774.0 31,365,312.0 35,800,632.3 50,075,646.0 42,451,755.2

4.2. Tourism 10,400,923.1 21,159,708.4 30,013,869.9 37,482,121.3 54,849,156.7 51,150,886.6 39,764,196.6

5. Transport-Communication 29,705,307.4 44,707,365.5 63,636,784.3 86,087,316.9 125,687,146.5 71,995,694.2 97,322,396.4

6. Financial Institutions 1,371,729.5 1,953,076.3 7,523,937.0 9,103,826.6 10,069,587.4 11,418,664.9 14,893,304.4

7. Ownership of Dwellings 66,347,993.9 91,113,091.2 121,390,563.7 204,215,564.9 353,405,768.1 466,969,956.7 480,192,774.8

8. Business and Personal Services

7,999,201.9 12,718,481.6 22,014,944.9 25,959,956.5 49,092,282.6 88,371,762.0 78,727,130.8

9. Public Services 31,834,567.3 51,285,602.2 79,363,510.0 93,124,289.1 111,555,220.1 89,918,968.8 62,507,292.3

9.1. Health 1,298,629.4 5,313,311.2 3,884,086.9 4,354,195.6 17,287,059.8 31,222,881.6 9,153,660.3

9.2. Education 15,117,50.0 23,454,844.6 41,220,862.1 54,362,203.5 51,152,845.3 10,076,850.3 9,135,207.9

9.3. Other 15,418,429.9 22,517,446.4 34,258,561.0 34,407,890.0 43,115,315.0 48,619,236.9 44,218,424.1

Total 199,231,606,8 306,203,356.7 466,600,661.0 645,460,056.4 966,659,314.9 1,064,282,208.1 1,062,702,394.2

Source: State Planning Organization

The following table presents data regarding the total credits allocated by the TCc Central Bank to SMEs among the various sectors.

Table 14 Credits - Sectoral (Total) (31 -03-2010)

Sector Credits (TRY) %

Public Enterprises and Institutions 1.342.308.906,78 33,46%

Agriculture 24.514.640,91 0,61%

Mining and Quarrying 40.907,88 0,00%

Manufacturing 6.634.990,23 0,17%

Transport and Communication 6.243.986,62 0,16%

Foreign and Domestic Trade 616.853.578,39 15,37%

Export 5.352.603,09 0,13%

Tourism 4.368.522,13 0,11%

Building and Construction 86.499.362,17 2,16%

Small Businesses and Craftsman 28.915.674,30 0,72%

Personal and Professional Credits and Others 1.890.519.685,80 47,12%

Bills Discounted 0,00 0,00%

TOTAL 4.012.252.858,30 100% NOTES: (1) Figures are prepared on a declaration basis from transitional bank balance-sheets, reported to the Central Bank of the TCc (2) Figures exclude Saving Deposits Insurance Fund (SDIF) banks Source: Central Bank of TCc

Based on these data it is understood that most credits are granted to the public sector (33.46%) while the rest of them are personal and professional credits (47.12%). Yet it has to be considered that most of these personal and professional credits are utilised for business activities, since there is lack in the regulatory framework, regarding the issue of getting credits for business investments.

2.3.1.1 Agriculture

Sustainable Economic Development in TCc - Private Sector Development Strategy 2011 - 2015

Page | 23

The agriculture sector was once the backbone of the TCc economy in 1980’s. Although its share in the economy has undergone a declining trend and decreased from 20.9% in 2005 to 6.4% in 2009, it still plays an important role in supplying vital input for the Tourism and niche Agrifood, which is perceived to be one of the primary sectors in the northern part of the island.

From the total area of 330,384 hectares of land cover in the northern part of the island 56.71% is covered by agricultural areas, 19.50% is covered by forests, 4.95% is covered by grazing land,10.69% is covered by towns, villages, rivers and lakes and 8.15% is covered by unused land {Source: SPO}.

The main agricultural products in the northern part include cereals, pulses, industrial crops, oil seeds, tuber crops, fodder crops, leafly or edible stem vegetables, fruit bearing vegetables, leguminous vegetables, root, bulb and tuberous vegetables, other vegetables, nuts, pome fruits, stone fruits, grape and grape like fruits and of course citrus fruit.

The following table presents the production in tons of the main agricultural products, regarding year 2008 {Source: SPO} and it understood that citrus and fresh vegetables constitute the main TCc production (53.7% and 28.1% respectively), followed by cereals and fruit and vineyard.

Table 15 Production of main agricultural products (2008)

Main Products

Production in

tons

% of total

production

Cereals 17,834 8.0%

Fodder crops 6,601 3.0%

Leguminous vegetables 3,178 1.4%

Fresh vegetables 62,846 28.1%

Fruit and vineyard 12,906 5.8%

Citrus 119,965 53.7%

Total 223,330 100.0%

Source: State Planning Organization

It is pointed out, according to SPO, that the export share of Citrus, which is one of the important export products reduced to 28.1% in 2006 from 35.1% in 2003. In other words, in four year period export of citrus fruits increased by 2.8%, while halloumi and cheese by 27.5% and 29.8% respectively, citrus concentrates increased by 28.9%, within the annual average growth rate of total export as 10.6 %.

As far as the livestock production is concerned, the following table includes basic indicators regarding number of livestock and main animal products of the TCc for 2008.

Sustainable Economic Development in TCc - Private Sector Development Strategy 2011 - 2015

Page | 24

Table 16 Number of livestock and main animal products (2008)

Sheep 230,992

Goat 58,918

Cattle 49,361

Broiler commercial type 6,503,376

Layer commercial type 109,978

Parent stock 68,897

Beehive 13,910

Total 7,035,432

Number of Livestock

Milk 109,626

Sheep goat 13,133

Cow 96,493

Poultry meat 9,810

Commercial eggs (in

dozens) 1,987,755

Muttons 3,627

Goat meat 738

Beef 4,066

Wool 272

Animal Products (in tons)

Source: State Planning Organization

Regarding the existing equipment and machinery used in agriculture activities, it is mentioned {Source: SPO} that their number has been increased over the last five years and it is considered almost adequate, while most of it is old fashioned and has been purchased many years ago.

Moreover in the TCc forestry products are also produced; in 2008 the production of fire wood reached 1.635 sterling pounds, which compared to previous years (2003) presented a decrease rate of about 45%.

2.3.1.2 Industry and manufacturing

The manufacturing sector contributes with 10% to the economy in 2009 {Source: YAGA}. Food and beverages, textile, furniture and processed agricultural products are the main sub sectors of the manufacturing.

Manufacturing contributes with 10 % to the GDP and 9.1% to total employment in 2009. Also the Construction sector has 6.5% share and contributes 10.1% to total employment.

Construction sector showed a boom in the TCc economy during 2005-2007, and it was accelerated by showing 8.7% of reel growth on average during the last 5 years. According to the SPO, the construction sector has an influence on 27 sub-sectors in the economy, this is why, its impact in the economy is very broad.

The average annual growth rate of manufacturing sector is 1.2% in the last five years including 2009. Manufacturing sector has 50.3% share of the total exports earnings in 2009, where processed agri-business products has 71.6% share.

Industrial zones intend to provide ready infrastructure for investment, particularly for SMEs. These zones formed by supplying the land parcels whose borders are registered and provided, with the necessary infrastructure services and other necessary facilities. Main purposes of these zones are to group all newly developed businesses together and to encourage SMEs to develop their activity in healthier working conditions.

Available industrial zones in TCc are;

Nicosia Industrial Zone

Famagusta Small Industrial Zone

Famagusta Industrial Zone

Agios Georgios (Karaoğlanoğlu) Industrial Zone

Sustainable Economic Development in TCc - Private Sector Development Strategy 2011 - 2015

Page | 25

Mia Milia (Haspolat) Industrial Zone

Gerolakkos (Alayköy) Industrial Zone

Rental time period is maximum 33 years (but may be extend twice more) and the rental price is low compared with similar conditions in other locations. As another advantage it is to mention that the renters in the industrial areas may register with the Land Registration Office and hand over or mortgage the buildings that they have inside the area during their rentals.

2.3.1.3 Services

Among the service sector, tourism and higher education are the leading sectors. Net revenues from tourism and higher education sectors are the two main sources of revenue and a major component of the current accounts in balance of payments. More analytically:

Tourism

Tourism is one of the leading growth sectors in TCc and the government places a high priority to the development of this sector.

Annual visitor numbers reached 809 thousand in 2008 and net tourism revenues is 434 million USD in 2009. In 2009 800 thousand tourists visited the country and net tourism revenues were reached to 450 million USD. In line with increasing visitor arrivals, TCc offers a wide range of accommodation from 5 star luxury hotels to holiday villages and a wide range of special tourism products such as bird watching, golfing, turtle watching, diving, historical site visit, eco/agro-tourism with more than 15.7 thousand bed capacity. According to the 2009 statistical yearbook of tourism there are approximately 134 facilities for tourist accommodation, the majority of which is located in Kyrenia (95 accommodation establishments) with the following distribution by regions and categories:

Table 17 Number of accommodation establishments by regions and categories

Tourism accomodation

establishments Total Nicosia Famagusta Kyrenia Morfou Trikomo

5 star hotel 12 1 1 9 1,0

4 star hotel 6 6

3 star hotel 16 2 1 12 1

2 star hotel 19 2 12 2 3

1 star hotel 19 1 13 1 4

special class hotel 1 1

boutique hotel 1 1

II. Class holiday village 6 5 1

touristic bungalow 32 2 28 2

apart hotel 6 1 4 1

traditional house 1 1

other accommodation establishment 15 1 1 4 9

Total 134 4 9 95 3 23 Source: 2009 statistical yearbook of tourism, Ministry of Tourism, Environment and Culture

The following tables and figures present data on the number of arrivals and departures to and from TCc by nationality (the majority is from Turkey):

Sustainable Economic Development in TCc - Private Sector Development Strategy 2011 - 2015

Page | 26

Table 18 Number of arrivals and departures to and from TCc by nationality for 2009

Nationality Arrivals Departures Total %

Turkey 638,700 637,186 1,275,886 63.42%

United Kingdom 61,558 62,133 123,691 6.15%

Germany 7,250 8,554 15,804 0.79%

Iran 6,913 6,522 13,435 0.67%

Russia 6,690 6,501 13,191 0.66%

Italy 2,653 2,176 4,829 0.24%

Other 76,612 76,508 153,120 7.61%

Tutkish Cypriot 205,219 206,517 411,736 20.47%

Total 1,005,595 1,006,097

Source: 2009 statistical yearbook of tourism, Ministry of Tourism, Environment and Culture

Figure 7 Number of arrivals and departures to and from TCc by nationality for 2009

63.42%6.15%

0.79%

0.67%

0.66%

0.24%

7.61%

20.47%

Turkey

United Kingdom

Germany

Iran

Russia

Italy

Other

Tutkish Cypriot

Source: 2009 statistical yearbook of tourism, Ministry of Tourism, Environment and Culture

Table 19 Number of Tourists and bed nights in tourist accommodation establishments by district for 2009

District

Number of

Tourists

Number of

Bednights

% of tourists

per district

Nicosia 17,945 41,968 3.78%

Famagusta 42,320 144,607 8.91%

Kyernia 361,100 1,277,318 76.01%

Morphou 584 1,056 0.12%

Trikomo 53,101 170,617 11.18%

Total 475,050 1,635,566 100.0% Source: 2009 statistical yearbook of tourism, Ministry of Tourism, Environment and Culture

Sustainable Economic Development in TCc - Private Sector Development Strategy 2011 - 2015

Page | 27

Figure 8 Percentage (%) of Tourists by district for 2009

3.78%

8.91%

76.01%

0.12%

11.18%

Nicosia

Famagusta

Kyernia

Morphou

Trikomo

Source: 2009 statistical yearbook of tourism, Ministry of Tourism, Environment and Culture

According to the same statistical yearbook, the number of tourists staying in tourist accommodation establishments reached 474,600 in 2009, with an average length of stay of 3.4 days.

Table 20 Number of tourism establishments and number of employees working in the tourism sector for 2009

Type pf establishment Number of establishmentsNumber of

employees

Tourist accomodation 119 3,321

Other accomodation 15 43

Tourism & Travel agencies 144 340

Casinos 25 3,567

Tourist restaurants 360 1,953

Total 663 9,224 Source: 2009 statistical yearbook of tourism, Ministry of Tourism, Environment and Culture

From year to year, the northern part of the island has become an interesting destination for tourists hence it becomes a lucrative place where it worth to invest.

Sustainable Economic Development in TCc - Private Sector Development Strategy 2011 - 2015

Page | 28

Trade

The approved Green Line Regulation and Financial Aid Regulation of the EU for the Turkish Cypriot Community, and currently discussed Direct Trade Regulation, are the outcome of the understanding that the private sector in the northern part of the country needs special and well designed contributory programmes in order to develop and reach the EU’s standards under the given political circumstances. The aim of the regulations, especially the Direct Trade Regulation is to contribute to the development of the private sector and thus of SMEs through foreign trade. Similar programmes of the US through USAID also acknowledge the same understanding and aim at the development of the private sector and thus of SMEs in the northern part of Cyprus.

Considering that Turkish Cypriot SMEs have faced several economic and political fluctuations since 1963, the mentioned rationale behind these activities is important in providing a new level of international approach to Turkish Cypriot SMEs in the northern part of Cyprus.

The Green Line Regulation regulates the movement of persons and commercial products over the Green Line from the northern to the southern part of Cyprus. Looking to the performance of the Green Line Regulation (Report of the European Commission on the implementation of the Regulation, 2008) the total volume of trade as mentioned by the Turkish Cypriot Chamber of Commerce amounts to 8,575,190 Euro in the reporting period, where the breakdown is as follows:

vegetables 40%

wooden products/furniture 9%

building stones /articles of stone 12.5%

plastic products 9%

raw metal 12.5%

others 17%

The above mentioned value means a volume of approximately 714,000 euro monthly trade and this is considerably low. Considering the low performance on Green Line trade, EU Commission has proposed the Direct Trade Regulation just after the referenda on 26 April 2004. But this regulation is still in the negotiation process between the parties. Direct Trade Regulation (European Commission, COM 466, 2004) sets out reference to the statement made by UN Secretary General to UN Security Council which explains that “members can give a strong lead to all States to cooperate both bilaterally and in international bodies to eliminate unnecessary restrictions and barriers that have the effect of isolating Turkish Cypriots and impeding their development”.

The Direct Trade Regulation aims that goods which are wholly obtained and/or substantially improved in the northern part of Cyprus may be released for free circulation into the customs territory of the European Community with exemption from customs duties and charges having equivalent effect. This, of course, may bring additional impetus on exports from the northern part of Cyprus considering that almost half of the exports from this part of the island is already made to European countries (DPO, 2007) and, upon adoption and realisation of the Regulation, it may have positive impact on the development of the private sector as well as on the exporting SMEs from the northern part of Cyprus.

While some of the barriers on exports are related to unresolved political issues, considering the ongoing commercial relations with the other European and non-European countries, the foreign trade activities might be improved considerably by implementing comprehensive and targeted reforms in the foreign trade legislation and in relevant practices.

Sustainable Economic Development in TCc - Private Sector Development Strategy 2011 - 2015

Page | 29

Public Sector

According to the "Study on sustainability and sources of economic growth in the northern part of Cyprus" carried out by World Bank in 2006, the public sector has played a leading role in the economy of the northern part of Cyprus for three decades, supported by generous aid flows from Turkey.

Public enterprises have provided basic infrastructure, supplied financial services, marketed agricultural goods, and produced consumer products. Foreign trade has been controlled by taxes, licenses, and quotas. Public loans and subsidies have been handed out to firms and farms to promote investment and stabilize output. And the public sector has been the employer of last resort.

Public involvement in the economy was seen as necessary, given the uncertain political situation and considering the need to provide the TCc with jobs and economic stability; and according to the records, the public initiatives leaded also to a certain growth.

The cost of heavy public involvement in the economy, however, has become increasingly evident over the years. The public sector has grown to be too big, overstaffed, and inefficient and many areas of the private sector have become uncompetitive.

Sustainable Economic Development in TCc - Private Sector Development Strategy 2011 - 2015

Page | 30

2.3.2. Identification of SMEs

According to the information obtained during August 2010 till October 2010, it has been understood that the data regarding the precise number of enterprises as well as the standard set for official registration are not updated.

SMEs are registered either to more than one chamber, since they have more than one activity (i.e. most SMEs practice both industrial and commercial activities). Three chambers are operating in the region, where SMEs can be registered; name and number of registered Companies per chamber is as follows:

Institution No. of

Companies*

Turkish Cypriot Chamber of Commerce +3,500

Cyprus Turkish Chamber of Industry +530

Cyprus Turkish Chamber of Shopkeepers and Artisans +7,300

* Number of members, August 2010. [Source: KTTO, KTSO, KTEZO]

In the tourism sector, the internal market for private sector activity in the northern part of Cyprus is quite small and the size distribution of enterprises is highly skewed towards micro and small firms.

According to the Technical Report on the Labour Market Survey held in October 2009 –February 2010, under the EU project Technical Assistance to support the development and promotion of VET systems, lifelong learning and active labour market measures in the northern part of Cyprus,

- 91.6% of all enterprises are categorized as micro (0 to 9 employees),

- 7% are small (10 to 49 employees)

- 1.2% are medium (50 – 249 employees) and

- 0.2 % are large (more than 250 employees)

Sustainable Economic Development in TCc - Private Sector Development Strategy 2011 - 2015

Page | 31

Figure 9 Size of the business entity (company) according to the number of employees

Source: Technical Report on the Labour Market Survey held in October 2009 –February 2010, under the EU project Technical

Assistance to support the development and promotion of VET systems, lifelong learning and active labour market measures in the northern part of Cyprus

It is pointed out that the distribution of the enterprises per TCc region is as follows:

Table 21 Size of the Company and Region (or percentage of each size of the company in the Region)

Enterprise category Nicosia Famagusta Kyrenia Morfou Trikomo

Micro (0-9 employees) 62.5% 100/% 100.0% 84.1% 100.0%

Small (10-49 employees) 37.5% 12.7%

Medium (50-249 employees) 3.2%

Large (+250 employees) Source: Technical Report on the Labour Market Survey held in October 2009 –February 2010, under the EU project Technical

Assistance to support the development and promotion of VET systems, lifelong learning and active labour market measures in the northern part of Cyprus

According to a Survey conducted by the Chamber of Industry in October 2009, 70% of the industrial facilities work 50% under their production capacity. Only 5.9% of the industrial facilities are working over 75% of their production capacity additionally, 23.5% of the industrial facilities are working 25% under their production.

Another important finding from the survey is that 61.7% of the companies participating the survey believe that their production capacity usage has decreased in the first half of 2009 [Cyprus Turkish Chamber of Industry – Expectations and Appearance of the Industry in Northern Cyprus, 2009].

Although there are not enough data on the SME s performance level, yet recent studies and reports2 show that the major problems that TCc entrepreneurs and SMEs face are relative to the following issues:

The TCc market is small and trade restrictions and difficulties with Green Line trade hamper exports access to global markets. As a result, firms have small-scale plants and operate these plants at relatively low levels of capacity utilization.

2 According to the "Study on sustainability and sources of economic growth in the northern part of Cyprus" carried out

by World Bank in 2006

Sustainable Economic Development in TCc - Private Sector Development Strategy 2011 - 2015

Page | 32

Machinery in use in many companies in infrastructure and industry activities is older than the ones of competitors and the value of the new investments and technical upgrading is low.

Transportation costs are relatively high, because of

the need to tranship through Turkey due to trade restrictions,

small-volume imports and exports cost more to transport, and

relatively less efficient internal transport services

These increase the costs of key intermediate inputs and exporting. Port handling and other trade support services are also relatively less efficient and higher cost in the northern part of Cyprus than in competitor countries.

Infrastructure costs are higher (also utility rates are not full cost recovery rates) and quality of services lower than competitors, especially in the areas of water and electricity. Power outages are frequent and water shortages common. Many firms must run their own generators or operate their own water systems to produce, which adds extra cost to the business activity.

IT use is extremely low compared to competitors and the larger companies that do use computers make limited use of IT potential to manage production, inventories, and finance. Only about 1 per cent of companies have ever engaged in B2B e-commerce transactions.

The minimum wages for manufacturing and industry activities are particularly high compared with the situation in the recent EU member countries

Quality standards are relatively low and few firms have quality certifications (ISO 9000, HACCP).

Low productivity in the Food processing sector (as the largest sub-sector in the manufacturing). One of the reasons why some processors have low productivity is because of low upstream productivity in agriculture and in public marketing enterprises. The productivity of farms in the northern part of the island is low compared with the situation in the recent EU member countries.

Low investment demand in manufacturing and the lack of innovation and technical learning that accompanies it is a binding constraint on growth in the northern part of the island.

Sustainable Economic Development in TCc - Private Sector Development Strategy 2011 - 2015

Page | 33

2.4. Telecommunications& ICT sector

Information and Communication Technologies (ICT) is a crucial field for the TCc future both as a new potential business activity but also as a tool that is needed to raise the productivity of all sectors, particularly in high-potential service businesses.

The institutional framework of this sector consists the following local authorities:

The highest local authority

Local authority for Economy and Energy

Local authority for Public works and Communication

Local authority for Interior Affairs

Telecommunication Board under Public works and Communication

Telecommunications Office under Public works and Communication

Official Registrar under Economy and Energy authority

MAPS, Land Registry office under Interior Affairs authority

Public Network Committee (KAMUNET) under Prime State Administration

Municipalities

Currently the legal framework for the development of ICT sector has been put in place:

Regulation Description Number/Date

Law E-Signature Law 93/2007

Bylaw Legislation and bylaw for Operation of e-Signature Law 2007

Law Law for Privacy of Information 89/2007

Law Law for the Rules regarding the use of the private information

12/2006

The following laws are still under preparation:

Regulation Description Status

Law Electronic Communication Law in Commission

Law Cyber Crime Law In preparation

Law e-Invoice/e-Payment (e-Commerce) In preparation

Law Intellectual Property Rights In preparation

Law e-Government Not yet planned

Although considerable progress has been achieved in the regulatory framework of the ICT sector, there are still areas for improvement which need to be addressed, like: Central Bank Law, Revenue Tax Law, Sanctions Law, etc.

Regarding the development of existing Infrastructure for ICT, it has been assessed that ADSL, satellite, 3G, 2G and broad-band internet connection are very expensive and the quality of the services is low; and other options are not possible. The broadband connections provided by ISPs are used in an uncontrolled way.

The telecommunications sector is currently not up to the EU standards. In order to reach these standards, is necessary to ensure long-term sustainability and quality service provision, capacity needs to be built up, and in particularly is needed an infrastructure that facilitates the operation of competitive players in a liberalised telecom market.

Currently, telecommunication services are provided to the TCc by three suppliers:

Sustainable Economic Development in TCc - Private Sector Development Strategy 2011 - 2015

Page | 34

- two of these service providers are GSM operators, and

- one service provider is responsible for providing fixed lines services.

The mobile operators are owned and operated by two big GSM operators in Turkey. Since the GSM networks are run by private companies, they have better infrastructures, and allow for 3G technology usage.

Fixed telephony services and communication infrastructure are provided by a utility subordinated to the TCc administration (the “Telecommunications Office”) of the TCc. Telecommunications Office is the sole infrastructure provider in northern part of Cyprus. The organisation’s structure and operation should become in the future as much flexible as it is required to meet the demand for fixed line connection. As currently this is not in place, alternative solution has to be identified; particularly, broadband data services (Internet) and high bandwidth requirements by individuals and businesses particularly in rural areas need to be developed. Since the current status of Telecommunications Office is not sufficient to increase the services for having better and reliable voice and internet communications, privatization or liberalisation is foreseen as a possible alternative to improve the quality of voice and internet services. Even the revenues of Telecommunication Office are high and contribute considerably to the TCc budget, the office is not capable of making investments to solve the problems totally because the amount of money they can invest is limited by the budget.