swot analysis in challenging times - danske bank

TRANSCRIPT

SWOT analysis in challenging times

Carnegie Large Cap Seminar 2008

Tonny Thierry Andersen CFO & Member of the Executive Board22 September 2008

2

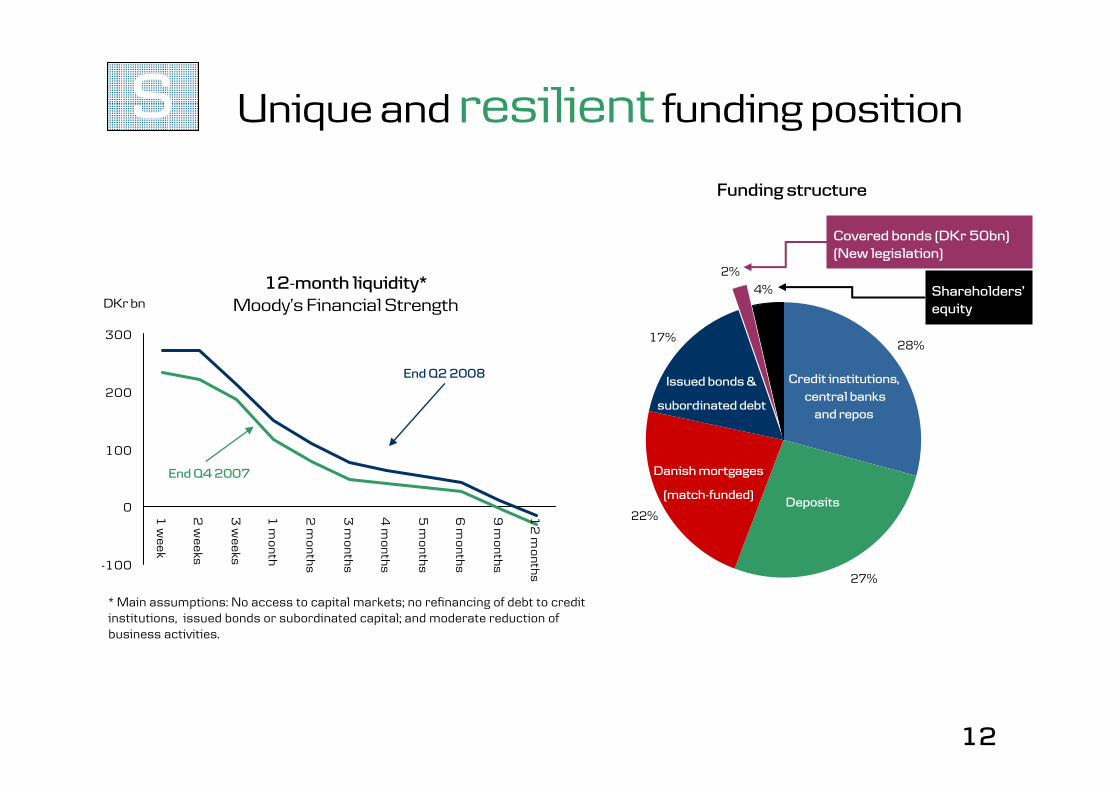

11m positive liquidity

Funding of Danish mortgages

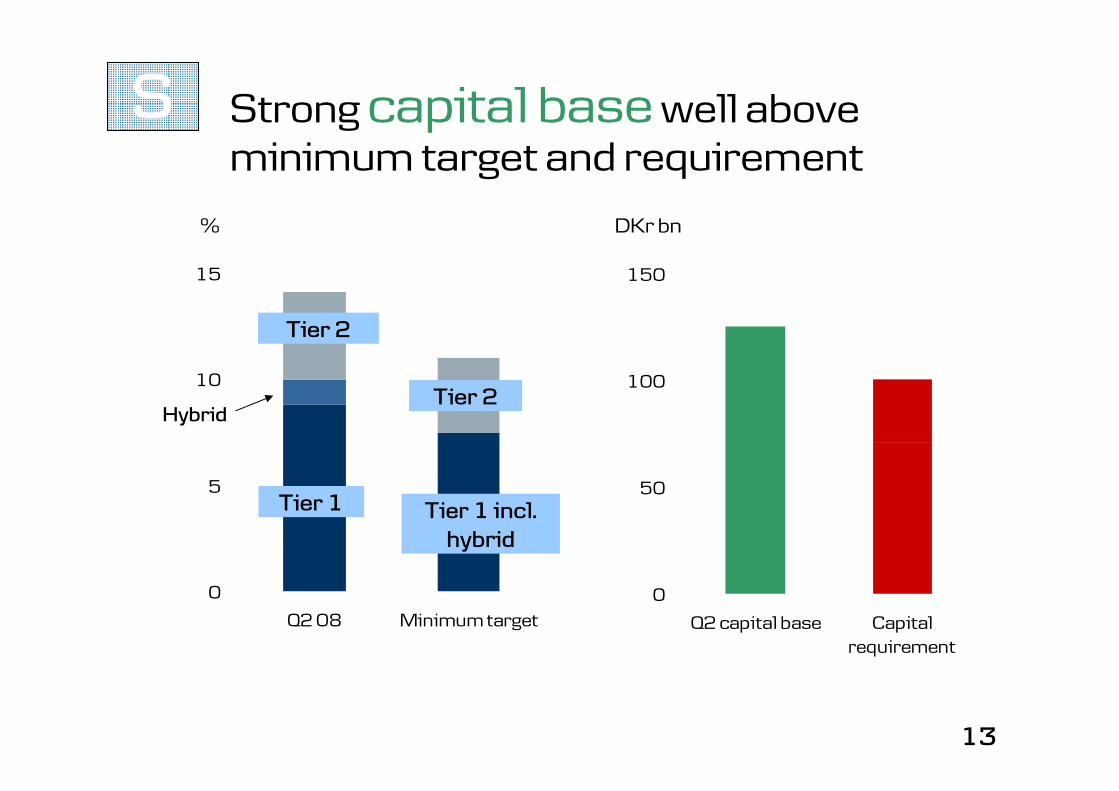

Excess capital

Resilient income

Cost under control

Higher lending margins

Lower relative funding costs

Organic growth opportunities

Higher funding costs

Wholesale

Retail

Low economic growth

Increasing credit losses

International financial turmoil

Protracted recession

Breakdown of banking infrastructure

3

Something rotten in the state ofDenmark?

4

GDP growth (%) Budget balance (% of GDP) Gross pub. debt (% of GDP) Unemp. rate (%)

1.0 4.5 21.6 1.8

2.6 *5.3 *35.4 6.3

2.1 2.4 37.4 6.2

3.3 *19.3 **48.9 2.6

1.4 **-0.6 *66.6 7.3

= lower than EU average = higher than EU average

* Figures from 2007. ** Figures from 2006.

Low growth, but a very healthy economy

S

5

-4

-2

0

2

4

6Fi

nlan

d

EK

Sw

eden

Spa

in

Irel

and

Bel

gium E

U

Ital

y

Fran

ce

Uni

ted

Kin

gdom

Uni

ted

Sta

tes

Source: OECD.

General government budget balance (% of GDP, 2007)

Significant fiscal elbow room

S

6

35%

40%

>60%

Is disposable income useful in analysing consumer leverage?

Welfare system or not�

W

7

Gross saving (% of GDP, 2006)

High level of national savings

14

15

25

S

8

0 20 40 60 80 100 120 140

Denmark

Netherlands

Switzerland

Canada

United Kingdom

Finland

Australia

Portugal

Spain

Norway

Japan

Austria

% of GDP

Source: OECD, Economic survey of Denmark.

Private pension assets reduce the need for real property equity

S

9

>3-month arrears (%)

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

2001 2002 2003 2004 2005 2006 2007

Source: Council of Mortgage Lenders and Danske Bank.

This quality gap is not new�

Danske Bank�s Mortgage Finance division

S

10

0

4

8

12

16

1980 1984 1988 1992 1996 2000 2004 2008

0

500

1.000

1.500

2.000

Unemployment is a leading indicator to look for

No.

Source: Danske Research.

<=Unemployment

Foreclosures =>

<= 10-year yield

S

Foreclosures, unemployment and 10-year yield

Source: Danske Research

%

,

,

,

11

Size (� bn) 258 111 10 app. 4,000 1,600

30-year fixed rate Yes No No No No

Maturity match 100% < 100% < 100% < 100% < 100%

Pricing risk No Yes Yes Yes Yes

LTV max Yes Yes Yes No No

Originate/Distribute No No No Yes Yes

Use of brokers No No No Yes Yes

Infrastructure and governancemodel are proven pillars of the Danish mortgage system

Mortgage market characteristics

S

12

-100

0

100

200

300

1 w

eek

2 w

eeks

3 w

eeks

1 m

onth

2 m

onths

3 m

onths

4 m

onths

5 m

onths

6 m

onths

9 m

onths

12

months

DKr bn

12-month liquidity*Moody�s Financial Strength

End Q4 2007

End Q2 2008

28%

27%

22%

17%

2%4%

Funding structure

Deposits

Issued bonds &

subordinated debt

Danish mortgages

(match-funded)

Credit institutions, central banks

and repos

Unique and resilient funding position

Covered bonds (DKr 50bn)(New legislation)

Shareholders�equity

* Main assumptions: No access to capital markets; no refinancing of debt to credit institutions, issued bonds or subordinated capital; and moderate reduction of business activities.

S

13

Strong capital base well above minimum target and requirement

0

5

10

15

Q2 08 Minimum target0

50

100

150

Q2 capital base Capitalrequirement

Tier 1 Tier 1 incl. hybrid

Tier 2

Tier 2

Hybrid

% DKr bn

S

14

0

1,000

2,000

3,000

4,000

Q2 07 Q3 07 Q4 07 Q1 08 Q2 08

Profit before credit loss expenses ex trading and insurance

Trading and Insurance income

DKr m

Resilient income base from well-diversified retail banking operations

S

15

Capital structure in the light of comparability

Tier 1 capital : 10.0%

Deductions from Tier 1:Pension deficit: YESHTM: NASolvency margin: 50%

Tier 1 capital: 7.3%*

Deductions from Tier 1:Pension deficit: ?HTM: ?Solvency margin: ?

* Source: Morgan Stanley & Danske Bank.

Selected European banks

S

16

-500

0

500

1,000

1,500

2,000

2,500

2007 2008 2009

Integration Costs Amortisations Synergies, Sampo

Expenses: Net impact on integration costs and synergies: 2007 vs. 2009: -DKr 1.8bn

DKr m

Tailwind from �low complexity� cost reductions coming through the P&L

S

17

The spreads are validating the same story � staying much narrower than peers

European covered bonds (5-yr bullets)Swap spreads (bp)

W

-20

0

20

40

60

80

100

120

01

/07

03

/07

05

/07

07

/07

09

/07

11

/07

01

/08

03

/08

05

/08

07

/08

Spain

Denmark

Sweden

UK

18

Also pressure from lower deposit margins

0.0

0.2

0.4

0.6

0.8

1.0Ja

n-0

3

May

-03

Sep

-03

Jan

-04

May

-04

Sep

-04

Jan

-05

May

-05

Sep

-05

Jan

-06

May

-06

Sep

-06

Jan

-07

May

-07

Sep

-07

Jan

-08

May

-08

% Deposit margins - Denmark

W

*Source: Nationalbanken.

19

Banks17%

Personal customers

30%

Govts & public authorities

2%

Subsidied housing companies

5%

Health care1%

Commercial property

8%

IT1%

Other industrials3%

Materials2%

Tele-communication

0%

Tranportation and shipping

3%Consumer

9%Energy and utilities

2%

Construction & bldg mat.

2%

Div. financials11%Other financials

4%

Diversified loan book

Credit exposure, end Q2 2008(DKr 2,699bn)

BUSINESS TRENDS

W

20

Developer, commercial property and construction exposure

Construction & building materials

DKr bn Denmark Ireland GroupContractors 4.2 5.1 23.6Others 10.1 0.7 24.1Total 14.3 5.8 47.7

Commercial property

DKr bn Denmark Ireland GroupRental comm. 52.0 12.0 172.9Developers 1.6 6.5 15.7

Others 7.1 2.1 22.6

Total 60.7 20.6 211.2

W

21

-5

0

5

10

15

Q207 Q307 Q407 Q108 Q208

Credit loss expensesbp

Collective impairment chargesOther credit loss expenses

Safe loan book, yes � but losses are on the rise

W

22

Between large US banks and regional Danish banks

T

23

Long-term decline in lending margins at a turning point

% Lending margins - Denmark

1.0

2.0

3.0

4.0

5.0Q

1 1

99

5

Q3

19

96

Q1

19

98

Q3

19

99

Q1

20

01

Q3

20

02

May

-03

Nov

-03

May

-04

Nov

-04

May

-05

Nov

-05

May

-06

Nov

-06

May

-07

Nov

-07

May

-08

O

* Source: Nationalbanken.

24

Time for a much-needed rebound in lending margins

O

25

2007 2008

Total lending margin

Lending margins in Denmark are coming up

O

1,5

1,8

2,0

Q2 Q3 Q4 Q1 Q2

%

1.5

1.8

2.015 bp

26

☺☺

But spread management is quite different in different markets

☺

What�s holding the banks back from repricing?

Northern Ireland & Ireland

Norway

Sweden:

Denmark

Finland

The Baltics

O

☺?

27

Summary

Slow growth, but a

very healthy Danish economy

Danish consumers not overleveraged

Unique Danish mortgage model

The financial storm will be managed

through

active and proven widening of lending

spreads

cost reductions with low execution risk

solid liquidity and capital management

28www.danskebank.com/ir