symex holdings limited for personal use only2012/02/29 · this presentation has been prepared by...

TRANSCRIPT

Investor Presentation

29 Feb 2012

SYMEX HOLDINGS LIMITED F

or p

erso

nal u

se o

nly

This presentation has been prepared by Symex Holdings Limited (SYM). The information in the presentation is current as at 29th Feb 2012.

This presentation is not an offer or invitation for subscription or purchase of securities or a recommendation with respect to any security. Information in this presentation should not be considered advice and does not take into account the investment objectives, financial situation and particular needs of an investor. Before making an investment in SYM, any investor should consider whether such an investment is appropriate to their needs, objectives and circumstances and consult with an investment adviser if necessary. Past performance is not a reliable indication of future performance.

SYM has prepared this presentation based on information available to it. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness or correctness of the information, opinions and conclusions contained in this presentation. To the maximum extent permitted by law, none of SYM, its directors, employees or agents, nor any person accepts any liability, including, without limitation, any liability arising from fault or negligence on the part of any of them or any other person, for any loss arising from the use of this presentation or its contents or otherwise arising in connection with it.

This presentation may contain forward looking statement that are subject to a range of risk factors and uncertainties. Whilst the statements are considered to be based on reasonable assumptions, the statements themselves and the assumptions upon which they are based may be affected by a range of circumstances which could cause actual results to differ significantly from the results expressed or implied in these forward looking statements.

Disclaimer F

or p

erso

nal u

se o

nly

Summary

• Disappointing result impacted by high costs and fierce competition ! Gross revenue increased from $88.1m to $93.4m ! Underlying net loss before significant items of -$1.4m for the half ! Impacted by difficult retail environment, high levels of competition in the grocery space and

high input prices ! Specialty Chemicals continues to be impacted by high input prices, competition and a high

AUD exchange rate ! Goodwill impairment charges of $14.15m and other asset write downs of $6.5m (total $20.7) ! Reported half year loss after significant items of - $20.6m ! No dividend declared for the period

• Strategic review providing plans for recovery ! Strategic review completed ! Management are implementing a plan to substantially improve returns and reduce debt ! Annualised cost savings of $8.0m identified ! Sale of non-core assets to repay debt

3

For

per

sona

l use

onl

y

HALF YEAR RESULTS - FY12 -

For

per

sona

l use

onl

y

Overview

• 1H FY12 results reflect challenging trading environment

• Revenue increased due to contribution from White King acquisition

• Consumer product division suffered from weak retail demand, higher costs and inability to increase prices

• Specialty chemicals division adversely affected by the relatively high cost of tallow versus palm oil, the corresponding loss of volume and margins and the exchange rate

• Goodwill impairment and asset write downs of $20.7m

• No dividend

• Significant improvement expected in second half

Consolidated Income Statement ($m)

1H FY12

1H FY11

% Change

Revenues 93.4 88.1 +6%

EBITDA* 3.3 8.5 -61%

EBIT* 1.7 7.1 -76%

NPAT* -1.4 4.1 >100%

Earnings per share (cents)* -0.75 3.21 >100%

EBITDA margin 3.5% 9.6%

Significant Items -20.7 -2.9

Reported NPAT -20.6 2.1

Key Observations

5

*Before significant items

For

per

sona

l use

onl

y

! Result reflects challenging retail environment

! Decline in Consumer Products sales due to deletion of Huggie from major retailers in June 2011 and loss of market share in Sunlight dishwashing liquid in New Zealand

! Sales of White King / Janola were in line with expectations

! Sales rebates and discounts increased in order to maintain shelf space

! Increase in costs and inability to increase selling prices adversely impacted margins

! Goodwill impairment charge of $10.0m

! Directors confident of substantial improvement in second half

Consumer Products

6

*Relate to Consumer Products sales only

Consumer Products - Sales ($m) 1H FY12 1H FY11

Consumer Products Sales (Pre White King acq.) 31.6 36.3

White King / Janola Sales 22.4 0

Total 54.0 36.3

Sales rebates and discounts* -14.4 -8.6

Sales rebates and discounts (%)* 27% 24%

Consumer products ($m)

1H FY12

1H FY11

% Change

Gross Sales Revenues 54.0 36.3 49%

Underlying EBIT 2.7 4.1 -34%

EBIT margin 5.0% 11.2%

For

per

sona

l use

onl

y

! Key driver of performance was input cost – Tallow

! Decline in sales and margins due to lower volumes and selling prices caused by relative cost of tallow versus palm oil

! Conditions have improved from February 2012 as there has been a 20% fall in the tallow price

! Domestic sales were also impacted by high AUD

! Sales for ‘White King’ shifted from being an external sale to Sara Lee to an intercompany sale with Symex’s acquisition of White King

! Predictability of future performance is difficult but lower raw material prices is expected to improve performance in second half FY12

Specialty Chemicals

7

Specialty Chemicals - Sales ($m) HY FY12 HY FY11

Domestic 9.2 11.8

Export 30.3 34.7

Sales for White King/Janola 5.4 5.7

Elimin. inter co sales (5.5) (0.3)

Total 39.4 51.9

Specialty Chemicals ($m)

HY FY12

HY FY11

% Change

Revenues 39.4 51.9 -24%

Underlying EBIT -0.9 3.0 -130%

EBIT margin n/m 5.8%

For

per

sona

l use

onl

y

Balance Sheet and capital management

• Goodwill has been written down by $14.15m

– Consumer products $10m

– Specialty Chemicals $4.15m

• Other asset write down of $6.5m including Specialty Chemicals plant and equipment of $5.0m and Land and buildings of $1.0m

• Whilst gearing is high the bank remains very supportive and agreed plan to reduce debt

Balance Sheet ($m) HY FY12 FY11

Net assets 85.0 107.7

Net debt 60.9 60.6

Working Capital 40.5 45.1

Property, Plant and Equipment 40.0 47.3

Goodwill 60.4 83.3

Net tangible assets 9.5 18.0

Net debt / Equity 71.6% 56.3%

EBITDA / Interest (times)* 1.03 5.22

Key Observations

8

* Before significant items

For

per

sona

l use

onl

y

! Symex and its bank have agreed to a debt reduction plan

! Scheduled quarterly repayments of $2.0m until the end of March 2013 rising to quarterly payments of $2.25m from June 2013. Management expects these repayments will continue to be made from operating cashflows

! One off lump sum payments of $11.0m to be made by 30 June 2012 and $18.0m to be made by 31 March 2013. These payments to be made from non-core asset sales including land and buildings

! The total repayments (as per above) to the bank are $37m by the end of March 2013

Debt Reduction

9

For

per

sona

l use

onl

y

$59.4m

$22.4m

$2.0m$11.0m

$2.0m$2.0m

$2.0m$18.0m

$0m

$10m

$20m

$30m

$40m

$50m

$60m

$70m

Current NetDebt*

30-Jun-12 30-Jun-12 30-Sep-12 31-Dec-12 31-Mar-12 31-Mar-13 Pro Forma NetDebt 31 Mar

2013

Debt Reduction Plan

10

*Balance as at 31 Dec 2011 less $1.25m payment made in Feb 2012 For

per

sona

l use

onl

y

STRATEGIC REVIEW

For

per

sona

l use

onl

y

Need for Strategic Review

12

Unacceptable Earnings Performance

Challenging external environment " Severe retail competition " Uncertainty in raw material costs

Tough Competition " Product de-listings " Share losses to private label

Margin decline " Need to reduce cost base " Price rises very difficult to pass on

Diversified versus focused operations " Mix of specialty chemical and consumer products " Debt too high for unpredictability of Specialty Chemicals

earnings

For

per

sona

l use

onl

y

The scope of this review was as follows: ! Defining the strategic direction of the company ! Identifying assets that are non-strategic to the future of the business ! Exploring divestment of assets which are considered non-strategic to the future of the business ! A review of our operations of our consumer goods business – in Australia and New Zealand

Strategic Review: Purpose

13

A key focus in the six months ended 31 December 2011 was a strategic review of operations as announced to the market in August 2011.

For

per

sona

l use

onl

y

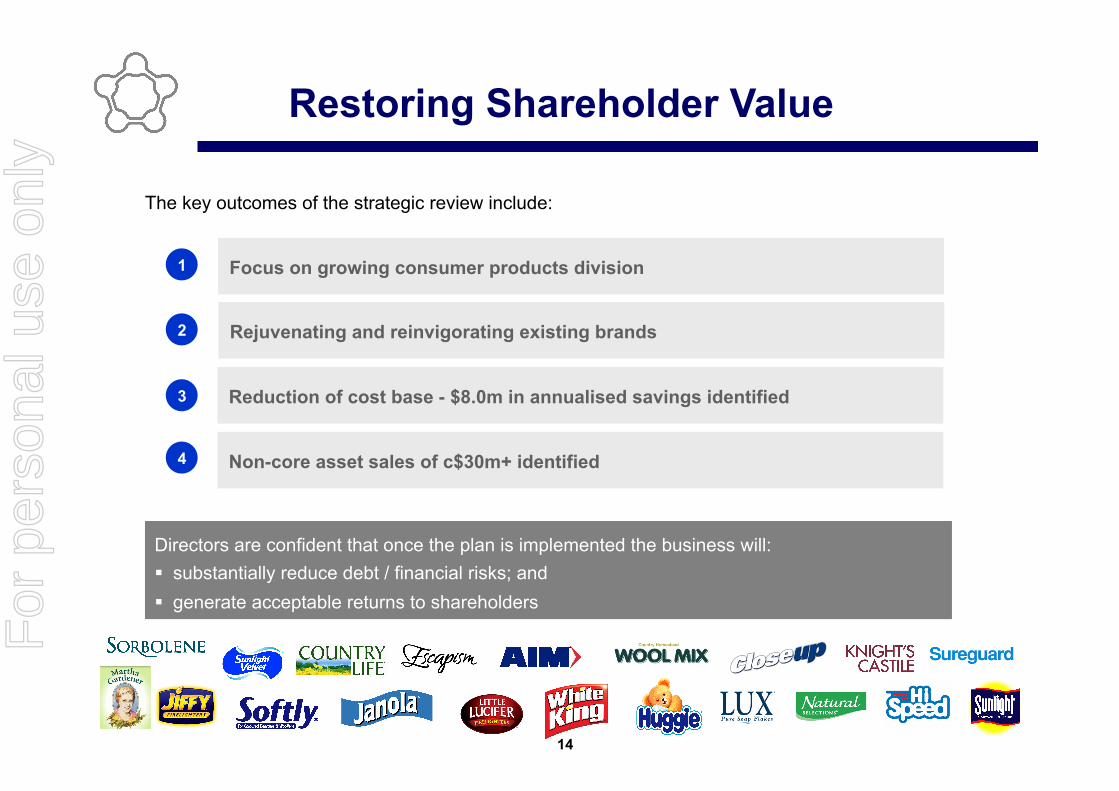

Restoring Shareholder Value

14

The key outcomes of the strategic review include:

1

2

3

4

Focus on growing consumer products division

Rejuvenating and reinvigorating existing brands

Reduction of cost base - $8.0m in annualised savings identified

Non-core asset sales of c$30m+ identified

Directors are confident that once the plan is implemented the business will: " substantially reduce debt / financial risks; and " generate acceptable returns to shareholders

For

per

sona

l use

onl

y

Focus on Consumer Products

15

1

! Portfolio includes top tier brands in category e.g. White King

! Opportunity to grow supply to private label utilising spare capacity

! Earnings certainty higher than Specialty Chemicals

! Opportunity to grow through new market channels – industrial markets including hospitals, mining, schools, government

! Opportunity to expand portfolio through product development and innovation (eg White King Bleach Tablets, White King Outdoor Spray)

For

per

sona

l use

onl

y

! Introduction of new products utilising existing brands e.g. Country Life, Velvet, Sunlight, White King

! New General Manager (May 2011) of consumer goods division - driving investment in innovation

! Amalgamation of non-core brands with core brands to concentrate marketing effort. Implemented 2H FY12

! Deletion of small or unprofitable SKU’s. Implemented 2H FY12

! Opening of White King factory outlet in March/April 2012 at Port Melbourne site

Rejuvenation and reinvigorating portfolio

16

2

For

per

sona

l use

onl

y

! Annualised cost savings of $8m p.a. have been identified – raw materials, packaging, freight and warehousing

! Implementation began in November 2011. Full year benefits to be realised in FY13

! Very small capital expenditure required to implement, and additional resources in procurement required

! Relocate some manufacturing to Shepparton and Port Melbourne from third parties

! Supply chain improvements have been identified and being implemented since December 2011

! Restructuring New Zealand operations -

! Some third party manufacturing to be brought in-house at Shepparton.

! Some cost saving initiatives implemented in December 2011 and March 2012

! Some Directors have reduced or waived their fees - $120k p.a. until June 30th 2013

Reduction of cost base

17

3

For

per

sona

l use

onl

y

! Sale and lease back of Shepparton site

– Marketing campaign to begin March 2012

– Auction to be held on March 30th 2012

– Proceeds to debt reduction

! Proposed sale and leaseback of Port Melbourne site

– Currently evaluating all options

– Expect process to be progressed by May 2012

– Proceeds to be applied to debt reduction

! Other non-core assets

– Expect proceeds to be realised before June 30th 2012

– Proceeds to be applied to debt reduction

Non-core asset sales

18

4

For

per

sona

l use

onl

y

Plan will improve returns to shareholders

19

Acceptable returns on sustainable capital structure

More focused business " Focus on Consumer Products division " Reduce reliance on Specialty Chemicals which has uncertain earnings

– eg Tallow/exchange rate/commodity pricing

Sales growth " Sales improvements through innovation and new markets and products " Portfolio rationalisation /concentrated marketing spend

Cost reduction " Significant cost reduction - $8m p.a. " Some initiatives have already begun " Full impact during FY13

Debt reduction " Substantial debt reduction ($37m) by March 2013 " Banks supportive " No equity issue foreseen

For

per

sona

l use

onl

y

Consumer Products ! Despite a continuation of challenging retail conditions, Directors anticipate the business will

deliver a substantial improvement in 2H FY12 ! Competitive environment is expected to continue with limited scope for price increases to major

retailers over the foreseeable future. Price increases implemented elsewhere ! Cost reductions of approximately $8.0m p.a. are being aggressively implemented which,

combined with continued product innovation, will be the key drivers of the improved performance

Specialty Chemicals

! Although Directors expect a reduction of input prices for the second half to lead to an improved performance, the overall outlook remains challenging and is difficult to forecast.

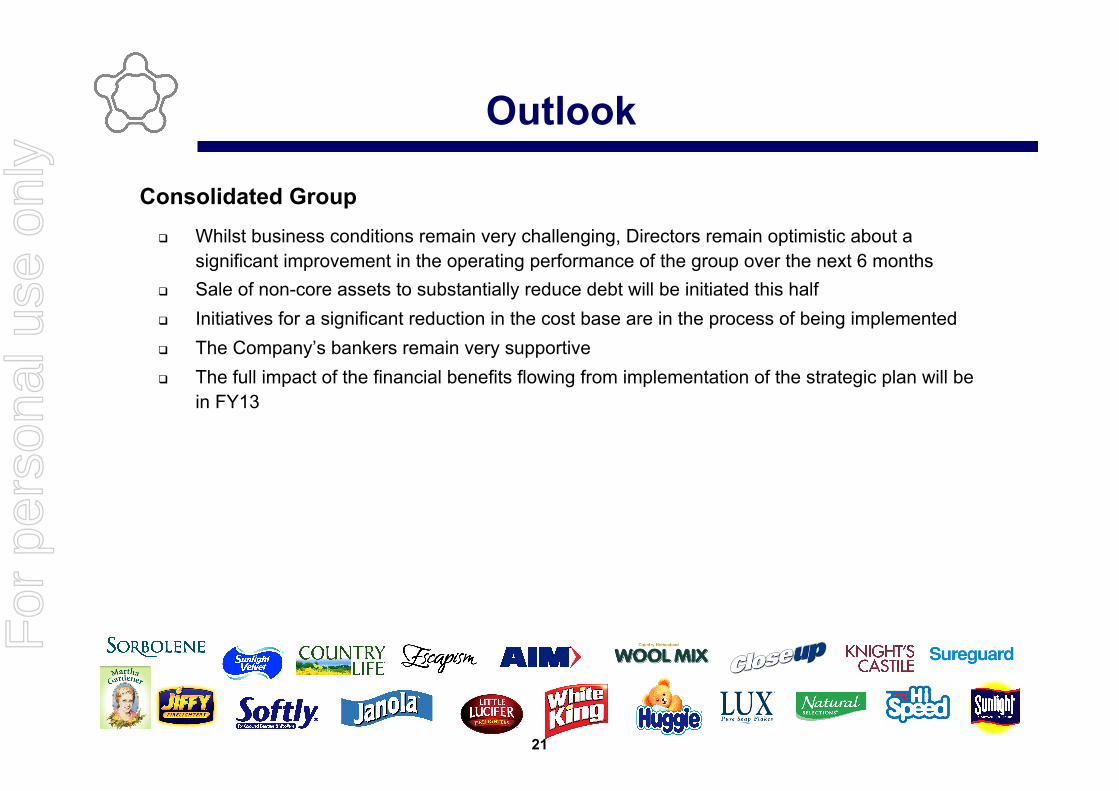

Outlook

20

For

per

sona

l use

onl

y

Consolidated Group ! Whilst business conditions remain very challenging, Directors remain optimistic about a

significant improvement in the operating performance of the group over the next 6 months ! Sale of non-core assets to substantially reduce debt will be initiated this half ! Initiatives for a significant reduction in the cost base are in the process of being implemented ! The Company’s bankers remain very supportive ! The full impact of the financial benefits flowing from implementation of the strategic plan will be

in FY13

Outlook

21

For

per

sona

l use

onl

y

Product Range F

or p

erso

nal u

se o

nly