system status briefing - eskom.co.za · system status briefing phakamani hadebe group chief...

TRANSCRIPT

System Status Briefing

Phakamani Hadebe

Group Chief Executive

16 November 2018

1

Operational performance

3 Future outlook

Conclusion

4

2

Summary of system performance

9 point recovery plan

5

Contents

While Distribution, Transmission and Koeberg are operating efficiently, the rest of Generation faces operational challenges

Summary of Eskom system performance

While Distribution, Transmission and Koeberg are operating efficiently, the rest of Generation

faces operational challenges

Causes:

• Deterioration of coal fired power stations

• 10 stations with less than 20 coal stock days, as per grid code requirement

• While inherent, other challenges happened in our midst

Outcome:

• Increased utilisation of emergency resources (OCGT’s1, interruptible load shedding and

demand response)

Manifestation of the above:

• EAF FY19 is 74.2%, is currently inadequate

• Current system status is therefore not optimal

While we have a recovery plan, load shedding cannot be ruled out for the remainder of 2018

South Africans can support by reducing their usage, especially at peak times

1

3

4

1.OCGT – Open Cycle Gas Turbine, 2. EAF - Energy Availability Factor . As at end October ’18 ,

3. Current financial year ends In March 2019

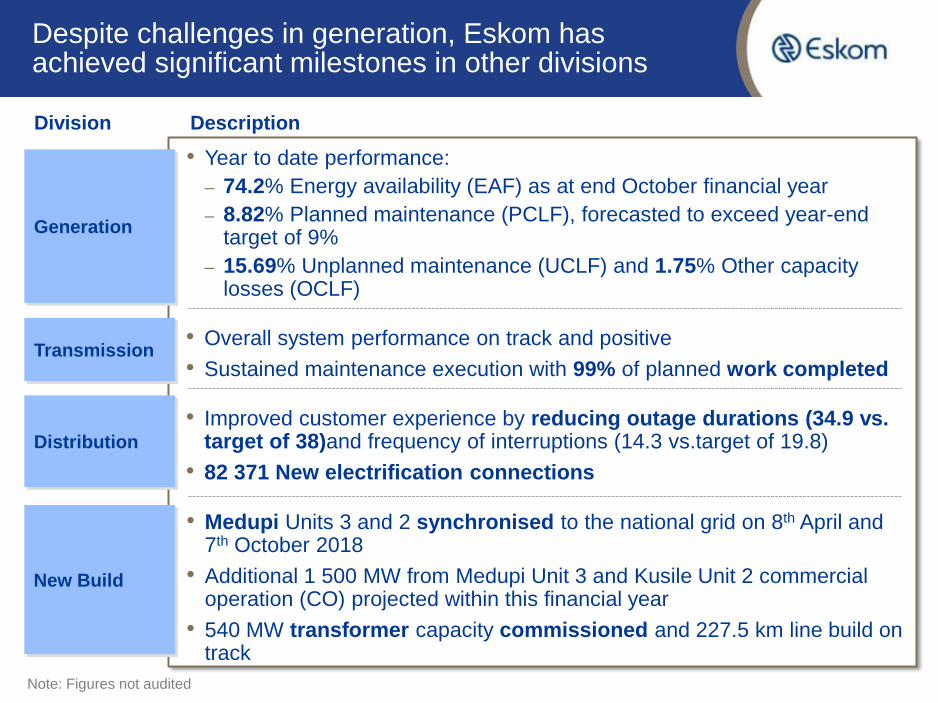

Despite challenges in generation, Eskom has achieved significant milestones in other divisions

Description

Generation • Year to date performance:

‒ 74.2% Energy availability (EAF) as at end October financial year

‒ 8.82% Planned maintenance (PCLF), forecasted to exceed year-end target of 9%

‒ 15.69% Unplanned maintenance (UCLF) and 1.75% Other capacity losses (OCLF)

Division

Transmission

New Build

• Medupi Units 3 and 2 synchronised to the national grid on 8th April and 7th October 2018

• Additional 1 500 MW from Medupi Unit 3 and Kusile Unit 2 commercial operation (CO) projected within this financial year

• 540 MW transformer capacity commissioned and 227.5 km line build on track

Distribution

Generation

• Overall system performance on track and positive

• Sustained maintenance execution with 99% of planned work completed

• Improved customer experience by reducing outage durations (34.9 vs. target of 38)and frequency of interruptions (14.3 vs.target of 19.8)

• 82 371 New electrification connections

Note: Figures not audited

The Capacity Outlook is based on planned outages and the ‘Tetris’ chart assists in optimising outage schedules

Source: Tetris Plan V4.37 – 15 November 2018

20000

25000

30000

35000

40000

45000

50000

Nov Dec Jan Feb Mar

2018 2019

Available Capacity Gas units Operating Reserves PCLF UCLF Peak Demand Installed Capacity

Summer UCLF

7000 MW Summer UCLF

7500 MW UCLF

PCLF

Operating Reserve

Available Capacity

Gas

5300 MW

Average Planned Maintenance (PCLF)

To accommodate the anticipated planned maintenance, OCGT’s will likely be required for most months up

until March 2019.

9 Point

Recovery Plan

However, Generation availability has deteriorated to below what we aspired to achieve

Percentage (%)

*Year to date figures.

FY 2019 Performance data unaudited and subject to change

EAF higher in winter due to lower levels of planned maintenance

9.2 8.8 7.2 5.3 7.5 9.9 8.6

Ja

n ’18

14.8

3.2

11.8

15.3

16.6

69.7

2.5 0.7

14.5

2.6

15.3 12.7

70.2 78.2

Ap

r ’1

8

Fe

b ’1

8

16.6

2.8

11.1

15.7

69.6

14.4

Ma

r ’1

8

0.8

74.0

16.0

76.1

1.7

Ma

y ’18

14.2 15.4

76.2

Ju

n ’18

Ju

l ’1

8

1.7

73.7 A

ug ’18

2.2

72.3

Sp

et ’1

8

3.5

Oct

’18

69.4

1.9

74.2

FY

19

*

12.3

UCLF OCLF EAF PCLF

Contributing factors

• Undesired coal quality

• Recent strikes

• Financial and capacity

constraints leading to

minimal refurbishments

and maintenance on

ageing fleet

• Outage execution

(overruns)

• Ops and maintenance

skills – availability and

training

• Maintenance cost

decreased in past five

years leading to

unsustainability

Generation performance for the 2019 financial year

7

Build-up of UCLF for FY19 from major contributors

0.44

1.56

1.61

0.93

1.33

2.79

14

15

16

13

12

4

5

2

0

3

1

12.12

5.64 15.29

Partial load loss

Boiler tube leaks

Full load loss

Outage Slip

13.68

0.14

6.49

Total unplanned losses (UCLF)

Full and partial losses were the highest contributors with a total of 12.12% of total UCLF for FY19 YTD

Outage slips contributed 1.56% to the total UCLF

Boiler tube leaks also contributed significantly at 1.61% of total UCLF

UCLF DV 4 KR 2 GV 2 LT 5

Note: All figures are year to date and unaudited

Source: Generation UCLF performance Analysis FY2019 YTD (14 Nov 2018 – unaudited data)

Key insights

Major incidents, as well as full and partial losses were key contributors to the increase in unplanned losses

Percentage (%)

A 9 point recovery plan has been put in place to address our key operational challenges

Fixing coal stock piles

Prepare for increased

OCGT usage

Fixing human capital

Prepare for rain

Fixing new plant

Fixing outage duration

and slips

Fixing units on long-

term forced outages

Fixing full load losses

and trips

Partial losses and

Boiler tube leaks

1

3

4

2

5

7

8

6

9

Fixing new plant – To reduce Full load losses from 2.79%

1

• New build units are expected to have initial unreliability.

• Especially Kusile, unreliability is even higher than expected.

• Experience from previous new builds (Majuba and Kendal) showed high initial

unreliability followed by excellent performance

• Spending on addressing known design errors

• 1.5 billion Capex investment

• Established an expert SWAT team to guide recovery

Objectives

State of new units

Source: Wikipedia, Bathtub curve

10

Fixing full load losses and trips - To reduce Full load losses from 2.79%

2

Process

Actions

• Relinking: a shift from centrally led approach

• Improve usage of Local Purchase Orders at site level

Maintenance

(Online and

Offline)

• Maintenance Effectiveness Assessments (MEAs) for

online and offline works

• Spares management optimisation

• Complete project to improve maintenance strategies and

work packages

Optimize

procurement

processes to

enable swifter

purchases when

required

Improve planning,

execution and

effectiveness of

maintenance

Objective Description

11

Fixing units on long-term forced outages - To

reduce impact of major incidents on UCLF 3

Lethabo

Unit 5

(600MW)

• High Pressure (HP) steam pipe failure on 10 October ‘18

• Investigation ongoing so required scope on HP pipework not

yet defined

• Planned outage scope to be executed during repair time

Grootvlei

Unit 2

(200 MW)

• Auxiliary steam range pipe burst on 26 January ‘18

• Also experience Generator issues

• Initial delay due to funding constraints

Kriel

Unit 2

(600MW)

• Stator earth fault on 03 May ‘18

• Spare generator stator now on site (insurance and

commercial process delays)

• Next planned outage being executed during repair time.

Duvha

Unit 4

(600MW)

• On 23 August ‘17, turbine tripped on generator stator earth

fault

• Duration due to long lead-time for major components

Description

Repair time

between 6 and 12

months

24 November

2018

30 April 2019

6 November 2018

Expected return date

Source: GPSS outage schedule for coal fleet (Nov 2018)

4 Fixing partial load losses - To reduce partial losses and boiler tube leaks

• 59 outages are planned for the

coal fleet between Sep ’18 and

Dec ‘19 to address PLL’s and

maintain critical plant systems

• Next 12 months funding plan:

‒ R11,5b Capex

• 12 to 24 months funding plan:

‒ R8.2b Capex

Key insights:

Planned outages for coal fired generating fleet until Nov ‘19

Fixing partial load losses includes addressing major contributors per plant and system

Generation UCLF performance per plant and system for FY19 (YTD)

Key Insights from analysis of YTD partial load losses

• Arnot, Kendal and Duvha contribute ~50% to the total Partial Load Losses

• Draught Plant and Gas Cleaning contribute about 55% to the total Partial Load Losses YTD

4

Percentage (%)

14

Fixing outage duration and slips to reduce contribution to UCLF from 1.56%

5

Offline maintenance (outages)

• Allocate specialist resources at each station for additional

focus on:

• Drive Rotek outage performance improvement in 4 focus

areas: Enabling contracts, personnel skills, spares management

and quality

• OPEX and CAPEX funds need to be available early

(Oct in previous year) to execute works effectively

Improve

outage

planning

and

execution

performance

to improve

PCLF

Objective Description

Up front

planning

Outage

readiness

Execution

quality

Fixing Human Capital to improve operations

15

6

Human Capital Initiatives

Make appointments in critical positions

• Appoint permanent Power Station Managers and

their critical subordinates

• Relinking and relocation of Commercial and Human

Resources personnel to Generation to keep

accountability at Generation group level

• Internal recruitment plan initiated, plan to effect

appointments 1 February 2019

16

Prepare for increased OCGT usage 7

INCREASE OCGT

USAGE

1. Fixing partial load

loses

2. To minimise risk of

load shedding or

reduce degree of

load shedding if

unavoidable

Budget:

• R 750m to R 1bn

forecast by end of

March 2019

• This does not

include OCGT

usage to mitigate

for risk of rain

Excerpt of OCGT historical performance Recovery plan

Prepare for rain

17

Measures are in place to reduce the impact of the rain season and in

compliance with the various power stations Wet Coal Handling Procedures

8

• At least 3 days strategic stockpiles for use during

sustained rainfall at all critical power stations

• Procedures in place for how and when to use strategic

stockpiles

• Ensure adequate fuel oil stocks for combustion

support when coal is wet

• Funding available and diesel supply assured for

extended OCGT usage in case required for system

support

Strategic

Stockpiles

Procedures

Fuel Oil

OCGT usage

1

3

4

2

Fix Coal Stockpiles to recover 10 stations that fell below Grid code requirement

9a

Focus area

Challenge

Stock days

Description

‒ 10 power stations below the Grid Code requirement of 20 days

‒ 5 of the 10 stations are below the minimum (<10 days of coal stock)

‒ Total stock days1 was 25.6 days as at 15 November 2018

‒ It is projected to grow to 28.2 days by 31 March 2019 from existing

and new signed contracts, ending with 6 stations still below the Grid

Code.

‒ It is projected that stations will reach expected level between September

2019 and February 2020

10 Stations

impacted

Risks

‒ Risk of rain

• Mitigations in place include compacted dry strategic stockpiles

1. Excluding Medupi and Kusile 2. NERSA has been duly informed as required by the Grid Code

‒ Arnot, Camden, Duvha, Hendrina, Komati, Kriel, Kendal, Majuba, Matla,

and Tutuka

‒ All in Mpumalanga Province

Coal shortages are a result of a number of factors 9b

Initial shortages in 2017 And long term reasons… As a result of short term reasons…

• Levels improved until

October ‘17

• Majuba and Tutuka fell

below Eskom minimum

but were above the Grid

Code required level of

20 days

• Total system coal stock1

was more than 40 days

• Decline started in

November ‘17 due to

undersupply from

existing suppliers and

long period to conclude

new coal contracts

• In 2018 only 8.3 Mt of required 12.2 Mt

coal was contracted & supplied

• 6 Mt cost plus mines undersupply due to

lack of capital investment

• Increased burn at stations with low stock

levels – low EAF at stations with sufficient

coal

• 750 Kt per month/8.5 Mt per annum coal

supply stoppage when 3 collieries2 were

placed under business rescue in

February 2018.

• Impact to date is 5.7Mt unplanned

shortfall 3

• We have diverted coal from other stations

to Hendrina and Komati. These stations

received 100% of their coal supply from

Optimum and Koornfontein

• Inability to renew

/conclude long-term

contracts with Arnot,

Optimum and New Largo

• Procurement process

takes ~1 year to conclude

• Lack of capital investment

in cost plus results in

reduced production

• Limited investment in

opening new mines

1. Excluding Medupi and Kusile 2. Optimum, Koornfontein and Brakfontein collieries 3. equivalent to 15 system stock days

Progress on 4 Mt urgent procurement

National Treasury engaged on process to

execute urgent procurement

Eskom then issued 2 requests to all existing

suppliers for above maximum contractual

supply and alternative coal offers

~4 Mt coal offered to be supplied above

max level of existing contracts over 11

months

Confirmation of supply above max coal on

existing contract issued for commencement

More than 30 Mt of alternative coal offered

for supply in excess of two years

3.2 Mt coal from offers can be delivered

within four months against 4 Mt target

Alternative coal offers are subject to

National Treasury approval

First coal expected December 2018

27 new coal contracts

have been concluded

between January 2018

and October 2018 for

supply of 15.8 Mt in the

current financial year.

Total contracted volume

is 73 Mt (need 116

Mt/annum)

Additional contracts in

the pipeline are at

advanced tender stage

Limited transfer of

Medupi coal by road has

commenced

1.4 Mt per annum Medupi

coal transfer by rail is

planned to commence in

Dec 2018

Short term provisions Fast tracking recovery

Eskom is executing

urgent purchasing of 4

Mt for immediate supply

to recover all power

stations to above

minimum level by 31

March 2019.

Success in procuring this

coal will see system stock

increasing to 36.3 days

by 31 March 2019

Only 1.1 Mt of the

required 4M t through

urgent procurement is

currently firm

Progress to date on short term coal stock recovery and recovery acceleration

9c

Simulating the inclusion of 4Mt potential emergency coal shows an increase in total stock days

21 Source: November 2018 Supply Plan (02Nov2018) v1A Including Pipeline sources

9d

• The success of sourcing the urgent 4Mt will see all stations reaching healthy alarm level and 36.3 system stock days by

March 2019 – work in progress

• Only 1.1 Mt of the required 4M t through urgent procurement is currently firm

• The 2.9 Mt balance is still to be contracted through the urgent procurement process for first coal in December 2018

Key insights

Simulating the

inclusion of 4Mt

potential

emergency coal

shows an increase

in total stock days

on 31 March 2018

to 36.3 days from

the 28.2 days

reflected in the

recovery plan

Actual and forecasted stock days for total system between Jun ’17 and Mar ‘20

Our strategy is to revert coal supply to dedicated long term coal contracts

Coal strategy

Eskom Long Term Coal Strategy revised to revert Eskom’s coal supply to

dedicated long term coal contracts for the life of the stations, with preference for

conveyor delivered coal.

• Cost plus contract extension to match power stations life and utilize the

dedicated coal reserve for supply to other power station

• Reinvestment in cost plus mines to enable contractual supply and more

• Extension of existing long term fixed price contracts for designated power

stations and options to supply other power stations

• Coal Open Tender to source uncontracted coal for the life of power stations

• Transnet to provide rail solutions for Eskom on Build, Own, Operate basis –

Eskom to focus on core business (generation and supply of electricity)

1

2

3

4

5

9e

In conclusion, the 9-point system recovery plan aims to return EAF to 75% by November 2019

Eskom’s 9 point plan aims to achieve 5 key objectives

We are currently implementing a 9-point system recovery plan that will return EAF

to 75% by November 2019.

This will result in:

A robust emergency procurement process that will shorten maintenance

restoration times

Significant head-way in returning long-term outage plants back to service

Reduction in full load losses (FLL’s) and partial load losses (PLL’s)

Critical vacancies filled in Generation

Coal stock levels returned to grid code heights

Comparison of aspirational versus achievable YTD EAF for Nov ’18- Nov ‘20

77.0

75.5

0.0

Sep 20

73.5

Mar 20 Sep 19 Jul 19

76.5

75.0

Jan 21 Jan 19

76.0

Nov 18 Mar 19 Jan 20

77.5

Nov 19 May 20

74.0

Nov 20 Mar 21 Jul 20

74.5

May 19

Aspirational

YTD Trend

YT

D E

AF

(%

)

Probable

YTD Trend

Source: Generation EAF improvement estimates required to achieve 78% by FY2021

Nov ‘18 Nov ‘19 Nov ‘20

75.8%

75.1%

Arrest EAF

deterioration

and plan for

EAF recovery

77.1%

76.3%

EAF improvements

based on 80% of

aspirational trends

The recovery plan is forecasted to improve EAF, and extra

effort will be made to get closer to our aspiration

Based on analysis and the recovery plan, the green line is the aspirational recovery trend while the red line represents the

most likely recovery trajectory.

Backup

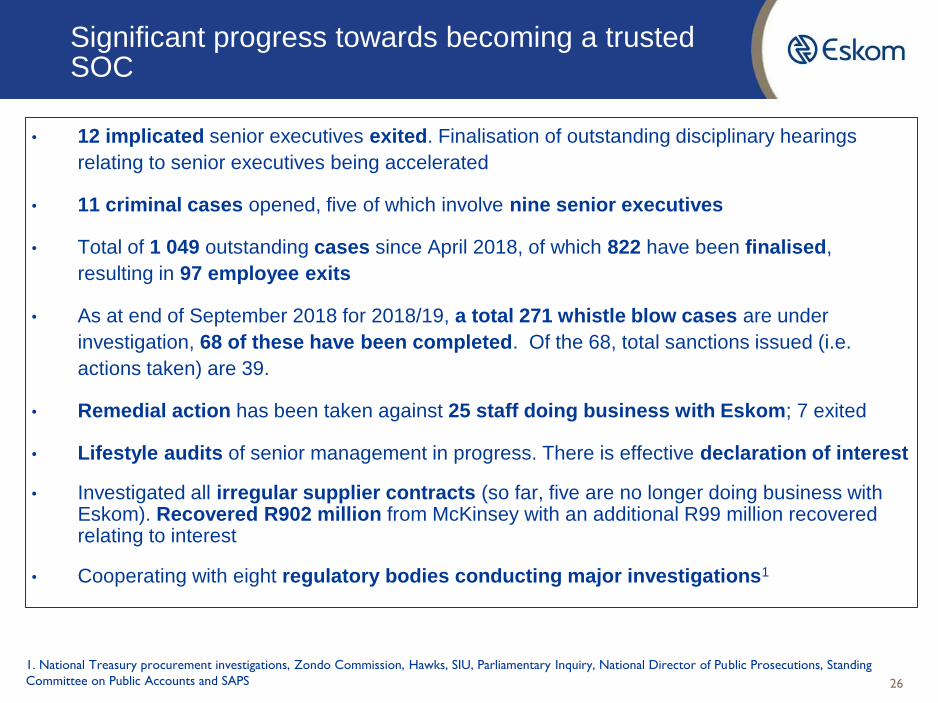

• 12 implicated senior executives exited. Finalisation of outstanding disciplinary hearings

relating to senior executives being accelerated

• 11 criminal cases opened, five of which involve nine senior executives

• Total of 1 049 outstanding cases since April 2018, of which 822 have been finalised,

resulting in 97 employee exits

• As at end of September 2018 for 2018/19, a total 271 whistle blow cases are under

investigation, 68 of these have been completed. Of the 68, total sanctions issued (i.e.

actions taken) are 39.

• Remedial action has been taken against 25 staff doing business with Eskom; 7 exited

• Lifestyle audits of senior management in progress. There is effective declaration of interest

• Investigated all irregular supplier contracts (so far, five are no longer doing business with Eskom). Recovered R902 million from McKinsey with an additional R99 million recovered relating to interest

• Cooperating with eight regulatory bodies conducting major investigations1

1. National Treasury procurement investigations, Zondo Commission, Hawks, SIU, Parliamentary Inquiry, National Director of Public Prosecutions, Standing

Committee on Public Accounts and SAPS 26

Significant progress towards becoming a trusted SOC