table of contents - public safety business agency · 2019-10-02 · management certificate ... 4...

TRANSCRIPT

2018-19 Annual Report Public Safety Business Agency

55

Financial statements – Table of Contents Statement of comprehensive income ...................................................................................................... 56Statement of financial position ................................................................................................................. 57Statement of changes in equity ............................................................................................................... 58Statement of cash flows .......................................................................................................................... 59Notes to the statement of cash flows ....................................................................................................... 60Notes to and forming part of the financial statements 2018–19 .............................................................. 61Management Certificate .......................................................................................................................... 89Independent Auditor’s Report .................................................................................................................. 90

Public Safety Business AgencyStatement of comprehensive incomefor the year ended 30 June 2019

Income from continuing operationsAppropriation revenueUser charges and fees *Grants and other contributions*Other revenueTotal revenue

Gains on disposal/remeasurement of assetsGain on revaluation of assetsTotal income from continuing operations

Expenses from continuing operationsEmployee expensesSupplies and servicesDepreciation and amortisationGrants and subsidiesImpairment losses/(gains)Revaluation decrementOther expensesTotal expenses from continuing operations

Operating result for the year

Other comprehensive income not reclassifiedsubsequently to operating result

Increase/(decrease) in asset revaluation surplusTotal other comprehensive income

Total comprehensive income

The accompanying notes form part of these statements.

6

5

9,287 1,245

Notes

3

4,922

16,059 443,870

9

169,271 137,876

10 (584)

423,416

429,793

15

2019 2018

15

(87)

1,386

291,504 4 138,968

13,785

10,052 37,118

120,131 125,018

33

3,218

138,882

5,189 42,017

477,593

1,245

147,688 130,775

433,468

10,546

2,010

480,989

$'000 $'000

621

11

* Revenue received from Queensland Fire and Emergency Services (QFES) and Queensland Ambulance Service (QAS)previously included under Grants and other contributions in 2017-18 has been reclassified to User charges and fees as perNote 4.

9,941

272,118

457

-

814, 15

19,339

9,287

38,363

56

2018-19 Annual Report Public Safety Business Agency

Statement of comprehensive income

Public Safety Business AgencyStatement of financial positionas at 30 June 2019

AssetsCurrent assets

CashReceivablesInventoriesOther current assetsNon-current assets classified as held for saleTotal current assets

Non-current assetsIntangible assetsProperty, plant and equipmentTotal non-current assets

Total assets

LiabilitiesCurrent liabilities

PayablesAccrued employee benefitsQueensland Treasury Corporation borrowingsOther current liabilitiesTotal current liabilities

Non-current liabilitiesQueensland Treasury Corporation borrowingsTotal non-current liabilities

Total liabilities

Net assets

EquityContributed equityAccumulated surplusAsset revaluation surplusTotal equity

The accompanying notes form part of these statements.

193,419

16,637 13

135,444 39,610

806

$'0002018

5,832

18,941

8,701

2019

205,402199,458

12,248 2,591,949 2,604,198

157,492

1,038

2,510,186

Notes

80,352

2,654,177

16

53,983

23,599

2,755

77,597

12

2,529,127

164,434 2,303,265

202,706

1,901

2,091

61,162

2,734,5292,803,656

14

2,755

2,367,802

17

15

2,654,177

2,734,942

$'000

131,653

-

-

3,172 68,714

-

-

5,599 59,943

68,714

2,734,942

2018-19 Annual Report Public Safety Business Agency

Statement of financial position

57

Public Safety Business AgencyStatement of changes in equityfor the year ended 30 June 2019

Notes

Contributed equityOpening balance Transactions with owners as owners:

Appropriated equity adjustment 3Net transfers from/(to) other departments

Closing balance

Accumulated surplus/(deficit)Opening balance Operating result Net effect of changes in accounting policiesPrior year adjustment *Closing balance

Asset revaluation surplusOpening balanceIncrease/(decrease) in asset revaluation surplusClosing balance

Total equity

The accompanying notes form part of these statements.

23

$'000

* During 2018-19, an accounting correction was undertaken between capital and operating categories to adjust prior periodproperty, plant and equipment transactions relating to machinery-of-government changes. This change does not have amaterial effect on the statement of financial position and is disclosed in accumulated surplus in accordance with AASB 108Accounting Policies, Changes in Accounting Estimates and Errors.

-

193,419

$'000

-157,492

120,373

193,419

60,292

2,734,942 2,654,177

The closing balance for asset revaluation surplus is comprised of: Land $92m (2018: $83m), Buildings $110m (2018:$108m) and Major plant and equipment $Nil (2018: $2m).

9,287192,175

1,245

157,49210,052

2,303,265

164,434

2,367,802

2,242,973

2018

37,118

202,706

2019

- 2,303,265

4,199

(3,134)

60,338

2018-19 Annual Report Public Safety Business Agency

Statement of changes in equity

58

Public Safety Business AgencyStatement of cash flowsfor the year ended 30 June 2019

Cash flows from operating activitiesInflows:Service appropriation receiptsUser charges and fees*Grants and other contributions* GST input tax credits from ATOGST collected from customersOther Outflows:Employee expensesSupplies and services Grants and subsidiesGST paid to suppliersGST remitted to ATOOther

Net cash provided by/(used in) operating activities

Cash flows from investing activitiesInflows:Sales of property, plant and equipmentOutflows:Payments for property, plant and equipmentPayments for intangibles

Net cash provided by/(used in) investing activities

Cash flows from financing activitiesInflows:Equity injectionsOutflows:Equity withdrawals Borrowing repayments

Net cash provided by/(used in) financing activities

Net increase/(decrease) in cash Cash at beginning of financial year

Cash at end of financial year

* Refer to Note 4 and Note 5 for prior year reclassification.

The accompanying notes form part of these statements.

131,65386,385

58,737

135,444

(60,510)

3,791 45,268131,653

56,736

(2,347)(1,785)(193,897)(225,491)

(151,499)

(13,629)(3,323)

(41,764)

(125,895)

(7,622)

18,147

(209,129)

(60,510)(1,995)(494)

38,613

294,845

(621)

117,740 121,242

160,552

(183,975)

2018

12,269

12,475

2019

(119,573)

(3,582)

156,184 170,506

$'000

3,582

(33)

5,807

(38,279)

(160,078)

39,871

$'000

40,971

263,417121,192

3,3237,940

2018-19 Annual Report Public Safety Business Agency

Statement of cash flows

59

Public Safety Business AgencyNotes to the statement of cash flowsfor the year ended 30 June 2019

Operating result

Non-cash items included in operating result:Depreciation property, plant and equipmentAmortisation intangiblesDonationsAssets written onRevaluation decrementGain on revaluation of property, plant and equipmentNet (gains)/losses on disposal of property, plant and equipmentImpairment lossesAccrued interest expense on loan

Change in assets and liabilities:(Increase)/decrease in receivables(Increase)/decrease in inventory(Increase)/decrease in net GST receivables(Increase)/decrease in other current assetsIncrease/(decrease) in creditorsIncrease/(decrease) in employee entitlementsIncrease/(decrease) in other current liabilitiesNet cash from operating activities

Accounting Policy - Cash

Cash assets include cash on hand and all cash and cheques receipted but not banked as at 30 June.

Opening balance as at 1 July 2018

Non-cash changes:InterestTransfers to/(from) other Queensland Government Entities

Cash flows:Cash repayments

Closing balance as at 30 June 2019 *

Opening balance as at 1 July 2017

Non-cash changes:Interest

Cash flows:Cash repayments

Closing balance as at 30 June 2018

(1,995)

156,184

19

$'000

10,052 37,118

37

(41)

4,656

2,894

170,506

4,656

(87)

9,941

(353)

-

* Fixed rate loans transferred from the Public Safety Business Agency to Queensland Treasury for centralised management,effective from 5 November 2018.

6,522

37(4,199)

(494)

Borrowings

129

-

2,389

540

2,692

2018

$'000

(3,151)

2019

122,298

(988)

(16,442) 20,799

(6,962)

8,674

The agency has authorisation to operate in overdraft with a specified limit in accordance with the Financial AccountabilityAct 2009. The approved overdraft limit is $30m.

(1,386)

8,066

(1,268)

16

(234)

8,477

(5,529)

232

Reconciliation of liabilities arising from financing activities

129 (584)

129,810

(9) (4)

(457)

Reconciliation of operating result to net cash from operating activities

$'000

2018-19 Annual Report Public Safety Business Agency

Notes to the statement of cash flows

60

Public Safety Business AgencyNotes to and forming part of the financial statements for the year ended 30 June 2019

1 Basis of financial statement preparation

(a) General information

(b) Statement of compliance

(c) Taxation

(d) Basis of measurement

The historical cost convention is used unless fair value is stated as the measurement basis.

(e) Accounting estimates and judgements

(f) Presentation matters

The agency is a not-for-profit entity and has no controlled entities.

Amounts included in the financial statements are in Australian dollars and have been rounded to the nearest $1,000or, where that amount is less than $500, to zero, unless disclosure of the full amount is specifically required.

These financial statements are general purpose financial statements and have been prepared on an accrual basisin accordance with Australian Accounting Standards and Interpretations. In addition, the financial statementscomply with Queensland Treasury's Financial Reporting Requirements for the year beginning 1 July 2018 and otherauthoritative pronouncements.

The agency is a State body as defined under the Income Tax Assessment Act 1936 (Cwth) and is exempt fromCommonwealth taxation with the exception of Fringe Benefits Tax (FBT) and Goods and Services Tax (GST).

The agency has prepared these financial statements in compliance with section 42 of the Financial andPerformance Management Standard 2009.

Estimates and assumptions that have a potential effect on the financial statements are outlined in the followingfinancial statement notes:

- Valuation of property, plant and equipment - Note 15

Such estimates, judgements and underlying assumptions are reviewed on an ongoing basis. Revisions toaccounting estimates are recognised in the period in which the estimate is revised and in future periods as relevant.

The Public Safety Business Agency ('agency') is a Queensland Government public sector office established underthe Public Safety Business Agency Act 2014 .

- Depreciation and amortisation - Note 14 and Note 15.

The preparation of financial statements necessarily requires the determination and use of certain critical accountingestimates, assumptions and management judgements that have a potential to cause a material adjustment to thecarrying amounts of assets and liabilities within the next financial year.

Comparative information has been restated where necessary to be consistent with disclosures in the current yearreporting period.

2018-19 Annual Report Public Safety Business Agency

Notes to and forming part of the financial statements 2018–19

61

Public Safety Business AgencyNotes to and forming part of the financial statements for the year ended 30 June 2019

1 Basis of financial statement preparation (continued)

(g) Future impact of accounting standards not yet effective

AASB 15 - Revenue from contracts with customers

The agency does not currently have any revenue contracts with a material impact for the period after 1 July 2019,and will monitor the impact of any such contracts subsequently entered into before the new standard takes effect.

The transition date for AASB 15 is 1 July 2019. The standard contains detailed requirements for the accounting forcertain types of revenue from customers.

Grants that are not enforceable and/or not sufficiently specific will not qualify for deferral, and will continue to berecognised as revenue as soon as the monies are received by the agency. Grants received whereby specificperformance obligations exist under a contract will be initially recognised as a liability, and subsequently recognisedprogressively as revenue as the agency satisfies its performance obligations under the grant. The agency hasreviewed the impact and expects grants to continue being recognised as revenue when received (refer to Note 5).

Depending on the specific contractual terms, the new requirements may result in a change to the timing of revenuerecognition from sales of the agency's goods and services, with some revenue deferred to a later reporting periodwhere the agency has received cash but has not met its associated obligations (such amounts would be reported asa liability, being unearned revenue). The agency has completed its analysis of current arrangements for the sale ofits goods and services (refer to Note 4).

As at the date of authorisation of the financial report, the expected impacts of the following accounting standardsand interpretations issued but with future effective dates are set out below:

AASB 1058 - Income of Not-for-Profit Entities

The transition date for AASB 1058 is 1 July 2019. The standard contains detailed requirements for the accountingfor certain types of revenue from customers.

AASB 1058 amends AASB 16 Leases so that the right-of-use assets arising from 'peppercorn leases' are measuredat fair value (instead of cost under AASB 16 paragraphs 23-24). This applies to all leases with significantly below-market terms and conditions principally to enable the lessee entity to further its objectives. However this has beenamended by AASB 2018-8 which provides a temporary option for Not-for-profit lessees to not initially fair value aright-of-use asset arising from leases that have significantly below market terms when AASB 1058 and AASB 16become effective from 1 January 2019. The option relief is expected to remain in place until further guidance hasbeen developed to assist Not-for-profit entities in fair valuing such right-of-use assets and the financial reportingrequirements for private sector and Not-for-profit entities have been finalised. The agency has elected to apply thistemporary option, resulting in 'peppercorn leases' being measured at cost with no change to the current financialreporting identified.

2018-19 Annual Report Public Safety Business Agency

Notes to and forming part of the financial statements 2018–19 (cont’d)

62

Public Safety Business AgencyNotes to and forming part of the financial statements for the year ended 30 June 2019

1 Basis of financial statement preparation (continued)

(g) Future impact of accounting standards not yet effective (continued)

The right-of-use asset will be initially recognised at cost, consisting of the initial amount of the associated leaseliability, plus any lease payments made to the lessor at or before the effective date, less any lease incentivereceived, the initial estimate of restoration costs and any initial direct costs incurred by the lessee. The right-of-useasset will give rise to a depreciation expense.

The lease liability will be initially recognised at an amount equal to the present value of the lease payments duringthe lease term that are not yet paid. Current operating lease rental payments will no longer be expensed in thestatement of comprehensive income. They will be apportioned between a reduction in the recognised lease liabilityand the implicit finance charge (the effective rate of interest) in the lease. The finance cost will also be recognisedas an expense.

In accordance with Queensland Treasury's policy, the agency will apply the 'modified retrospective approach'. Under this approach, the agency will not need to restate comparative information. For leases that were operating leasesunder AASB 117, the agency will measure the new lease liability at 1 July 2019 by discounting the remaining leasepayments at the agency's incremental borrowing rate.

This results in a net increase of $22k in total expenses.

The agency has completed its review of existing operating leases and has identified the following impacts ofapplying AASB 16.

During the 2018-19 financial year, the PSBA held operating leases under AASB 117 from the Department ofHousing and Public Works (DHPW) for commercial office accommodation through the Queensland GovernmentAccommodation Office (QGAO). Lease payments under these arrangements totalled $3.7m p.a. The agency hasbeen advised by Queensland Treasury and DHPW that, effective 1 July 2019, amendments to the frameworkagreements that govern QGAO will result in the above arrangements being exempt from lease accounting underAASB 16. This is due to DHPW having substantive substitution rights over the commercial office accommodationassets used within these arrangements. From 2019-20 onwards, costs for these services will continue to beexpensed as supplies and services when incurred.

The agency has also been advised by Queensland Treasury and DHPW that, effective 1 July 2019, motor vehiclesprovided under DHPW's QFleet program will be exempt from lease accounting under AASB 16. This is due toDHPW holding substantive substitution rights for vehicles provided under the scheme. From 2019-20 onwards,costs for these services will continue to be expensed as supplies and services when incurred. Existing QFleetleases were not previously included as part of non-cancellable operating lease commitments.

The agency has quantified the transitional impact on the statement of financial position and statement ofcomprehensive income of all qualifying lease arrangements that will be recognised on-balance sheet under AASB16, as follows:

Statement of financial position impact on 1 July 2019:

Statement of comprehensive income impact expected for the 2019-20 financial year, as compared to 2018-19:$419k increase in depreciation expense

$1.29m increase in lease liabilities$1.29m increase in right-of-use assets.

Under this standard, lessees will be required to recognise a right-of-use asset representing rights to use theunderlying leased asset and a liability representing the obligation to make lease payments for all non-cancellableleases with a term of more than 12 months, unless the underlying asset is of low value.

This standard will first apply to the agency from its financial statements for 2019-20.

$16k increase in interest expense$413k decrease in supplies and services expense

AASB 16 - Leases

2018-19 Annual Report Public Safety Business Agency

Notes to and forming part of the financial statements 2018–19 (cont’d)

63

Public Safety Business AgencyNotes to and forming part of the financial statements for the year ended 30 June 2019

1 Basis of financial statement preparation (continued)

(g) Future impact of accounting standards not yet effective (continued)

Other standards and interpretations

(h) Accounting standards applied for the first time

AASB 139 measurement category

ReceivablesTrade and other receivables Amortised cost

2 Objectives and principal activities of the agency

-

- ICT services to the Queensland Ambulance Service;

- Queensland Government Air Services.

- Fees for services, including aviation user charges;- Commercial contract services;- Service agreements for ICT and network support services, and- Grants and other contributions.

The Public Safety Business Agency (PSBA) is committed to its vision to be a leader in corporate services innovationand delivery. The agency supports the Queensland Government's objectives to keep communities safe and be aresponsive Government. The agency's commitment to leadership in services, technology and capability will enhance access to Government services and strengthen Queensland's responsiveness to emergency events through thedelivery of corporate and air services, including:

Management determined that the existing methodology of calculating the impairment of receivables was moreappropriate as at 30 June 2018. The results of the assessment performed at 30 June 2018 indicated that therevised provision would not be sufficient to reflect management's future planned actions in relation to bad debtassessment and write-offs. Following on from the recognition of bad debts totalling $557k in 2018-19 it is nowconsidered appropriate to implement AASB 9's new impairment model. This resulted in the agency recognisingreduced impairment losses of $40k on its trade receivables. This resulted in an increase in opening accumulatedsurplus of $23k. Below is a reconciliation of the ending impairment allowance under AASB 139 to the loss allowancereported under AASB 9.

Re-measurement

$'000

(581)

AASB 9 requires the loss allowance to be measured using a forward-looking expected credit loss approach,replacing AASB 139's incurred loss approach. AASB 9 also requires a loss allowance to be recognised for allreceivables rather than only on those receivables that are credit impaired.

(581)

Impairment allowance 30

June 2018$'000

621621

AASB 9 measurement

category$'000

Loss allowance 1

July 2018

Funding for the departmental services delivered by the agency has come from parliamentary appropriations andother revenue sources including:

There is no change to either the classification or valuation of the cash item and all financial liabilities listed in Note21 will continue to be measured at amortised cost.

information and communications technology (ICT), financial, procurement, asset management, human resourcesand other corporate services to the Queensland Police Service (QPS), Queensland Fire and Emergency Services(QFES) (including the Rural Fire Service and the Queensland State Emergency Service) and the Office of theInspector-General Emergency Management (IGEM);

All other Australian accounting standards and interpretations with future effective dates are either not applicable tothe agency or have no material impact.

$'000

4040

PSBA's corporate and business services includes the ownership and management of assets on behalf of the publicsafety entities. Refer to Note 15 Property, plant and equipment for details of the asset classes used by QPS andQFES.

The agency applied AASB 9 Financial Instruments for the first time in 2018-19. The standard addressesrecognition, classification, measurement and de-recognition of financial assets and financial liabilities andimpairment of financial assets, including statutory receivables. Comparative information for 2017-18 has not beenrestated and continues to be reported under AASB 139 Financial Instruments: Recognition and Measurement.

2018-19 Annual Report Public Safety Business Agency

Notes to and forming part of the financial statements 2018–19 (cont’d)

64

Public Safety Business AgencyNotes to and forming part of the financial statements for the year ended 30 June 2019

3

Budgeted appropriation revenueTransfers from/(to) other departmentsTransfers from/(to) other headingsLapsed appropriation revenueTotal appropriation receipts Plus: Opening balance of deferred appropriation payable to Consolidated FundLess: Closing balance of deferred appropriation revenue payable to Consolidated FundNet appropriation revenuePlus: Deferred appropriation payable to Consolidated Fund (expense)Appropriation revenue recognised in Statement of comprehensive income

Budgeted equity adjustment appropriationTransfers from/(to) other headingsLapsed equity adjustmentEquity adjustment receiptsLess: Opening balance of equity adjustment receivablePlus: Closing balance of equity adjustment receivablePlus: Opening balance of equity adjustment payableLess: Closing balance of equity adjustment payableEquity adjustment recognised in contributed equity

Accounting Policy - Appropriation revenue

8,701

263,417 286,080

-

-63,872

(440)

2018

-

(3,095)

-

57,294

282,803

60,796(996)

269,023

2,080-

$'000

Reconciliation of payments from Consolidated Fund to appropriation revenue recognised in Statement of comprehensive income

(33,750)

-

2019

279,896

8,701 5,424

2,604

71,634

291,504

Reconciliation of payments from Consolidated Fund to equity adjustment recognised in contributed equity

272,118

(8,701)

3,095

(16,479)

317,750

-440

(64)-

Appropriation revenue

(14,340)(2,080)

Appropriations provided under the Appropriations Act 2018 are recognised as revenue when received or receivable. Whereappropriation revenue has been approved but not yet received, it is recorded as a receivable at the end of the reportingperiod.

$'000

60,338 60,292

2018-19 Annual Report Public Safety Business Agency

Notes to and forming part of the financial statements 2018–19 (cont’d)

65

Public Safety Business AgencyNotes to and forming part of the financial statements for the year ended 30 June 2019

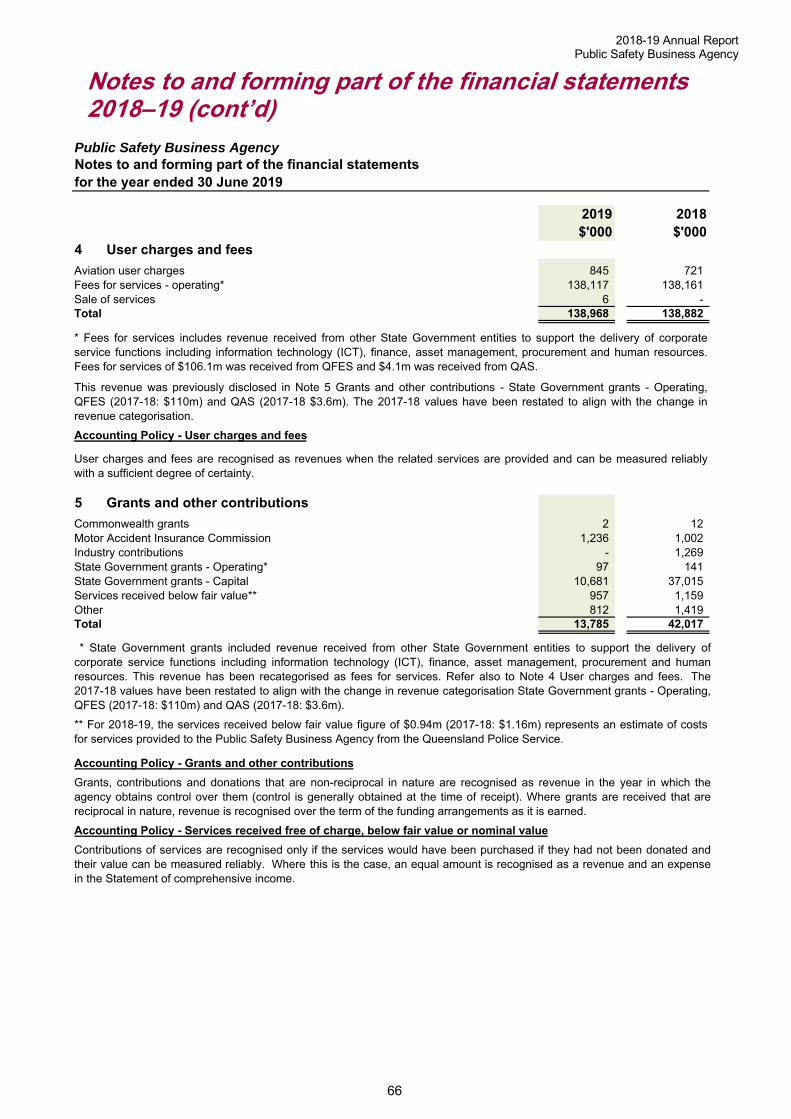

4

Aviation user chargesFees for services - operating*Sale of servicesTotal

Accounting Policy - User charges and fees

5

Commonwealth grantsMotor Accident Insurance CommissionIndustry contributionsState Government grants - Operating*State Government grants - CapitalServices received below fair value** OtherTotal

2018

957

138,882-

* Fees for services includes revenue received from other State Government entities to support the delivery of corporateservice functions including information technology (ICT), finance, asset management, procurement and human resources.Fees for services of $106.1m was received from QFES and $4.1m was received from QAS.

13,785

2019

1,002

141

138,117845

1,159

138,161

1,269

812 1,419

138,968

2 12

721

$'000

37,01597

-

10,681

$'000

This revenue was previously disclosed in Note 5 Grants and other contributions - State Government grants - Operating,QFES (2017-18: $110m) and QAS (2017-18 $3.6m). The 2017-18 values have been restated to align with the change inrevenue categorisation.

6

User charges and fees

User charges and fees are recognised as revenues when the related services are provided and can be measured reliablywith a sufficient degree of certainty.

1,236

42,017

Grants and other contributions

* State Government grants included revenue received from other State Government entities to support the delivery ofcorporate service functions including information technology (ICT), finance, asset management, procurement and humanresources. This revenue has been recategorised as fees for services. Refer also to Note 4 User charges and fees. The2017-18 values have been restated to align with the change in revenue categorisation State Government grants - Operating,QFES (2017-18: $110m) and QAS (2017-18: $3.6m).

** For 2018-19, the services received below fair value figure of $0.94m (2017-18: $1.16m) represents an estimate of costs for services provided to the Public Safety Business Agency from the Queensland Police Service.

Accounting Policy - Grants and other contributions

Grants, contributions and donations that are non-reciprocal in nature are recognised as revenue in the year in which the agency obtains control over them (control is generally obtained at the time of receipt). Where grants are received that are reciprocal in nature, revenue is recognised over the term of the funding arrangements as it is earned.

Accounting Policy - Services received free of charge, below fair value or nominal value

Contributions of services are recognised only if the services would have been purchased if they had not been donated and their value can be measured reliably. Where this is the case, an equal amount is recognised as a revenue and an expense in the Statement of comprehensive income.

2018-19 Annual Report Public Safety Business Agency

Notes to and forming part of the financial statements 2018–19 (cont’d)

66

Public Safety Business AgencyNotes to and forming part of the financial statements for the year ended 30 June 2019

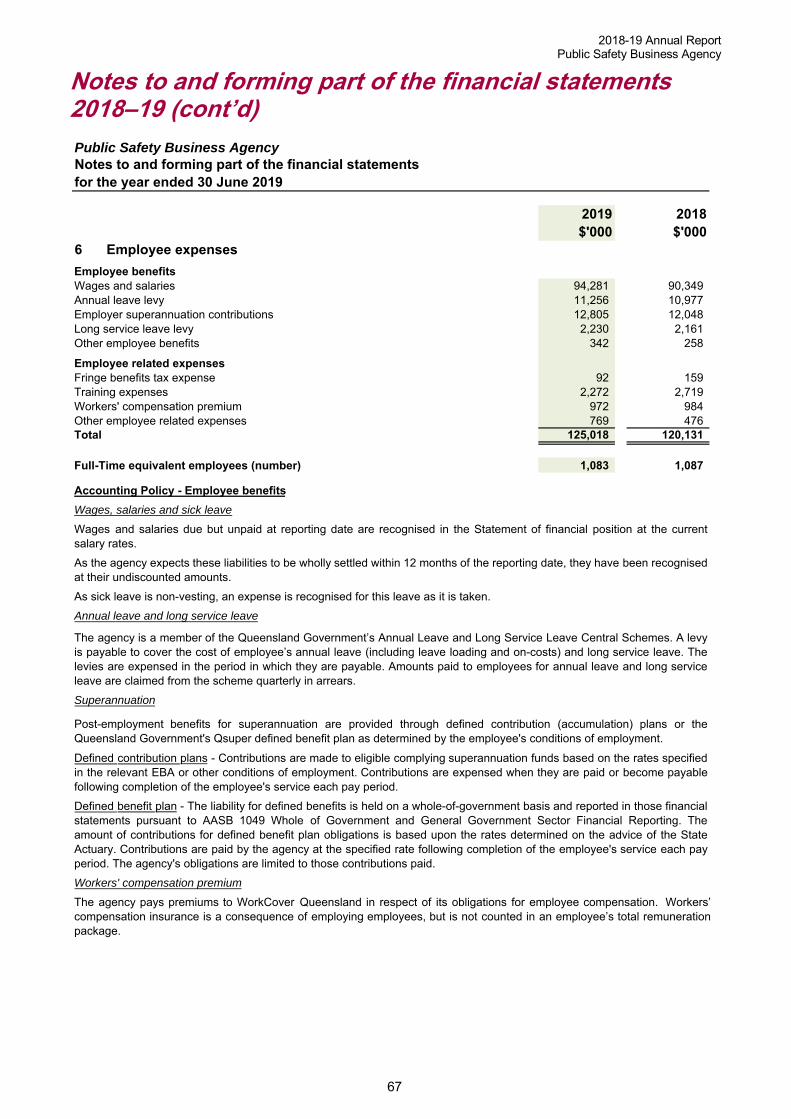

6

Employee benefitsWages and salaries Annual leave levyEmployer superannuation contributionsLong service leave levyOther employee benefits

Employee related expensesFringe benefits tax expenseTraining expenses Workers' compensation premiumOther employee related expensesTotal

Accounting Policy - Employee benefits

1,083

476

Employee expenses

2,230

90,349

125,018

258

11,256

2,272

94,281

15992

769984

Wages, salaries and sick leave

10,977

3422,161

972

2019 2018$'000 $'000

2,719

1,087

12,805

120,131

Full-Time equivalent employees (number)

12,048

Wages and salaries due but unpaid at reporting date are recognised in the Statement of financial position at the current salary rates.

As the agency expects these liabilities to be wholly settled within 12 months of the reporting date, they have been recognised at their undiscounted amounts.

As sick leave is non-vesting, an expense is recognised for this leave as it is taken.

Annual leave and long service leave

The agency is a member of the Queensland Government’s Annual Leave and Long Service Leave Central Schemes. A levy is payable to cover the cost of employee’s annual leave (including leave loading and on-costs) and long service leave. The levies are expensed in the period in which they are payable. Amounts paid to employees for annual leave and long service leave are claimed from the scheme quarterly in arrears.

Superannuation

Post-employment benefits for superannuation are provided through defined contribution (accumulation) plans or the Queensland Government's Qsuper defined benefit plan as determined by the employee's conditions of employment.

Defined contribution plans - Contributions are made to eligible complying superannuation funds based on the rates specified in the relevant EBA or other conditions of employment. Contributions are expensed when they are paid or become payable following completion of the employee's service each pay period.

Defined benefit plan - The liability for defined benefits is held on a whole-of-government basis and reported in those financial statements pursuant to AASB 1049 Whole of Government and General Government Sector Financial Reporting. The amount of contributions for defined benefit plan obligations is based upon the rates determined on the advice of the State Actuary. Contributions are paid by the agency at the specified rate following completion of the employee's service each pay period. The agency's obligations are limited to those contributions paid.

Workers' compensation premium

The agency pays premiums to WorkCover Queensland in respect of its obligations for employee compensation. Workers’ compensation insurance is a consequence of employing employees, but is not counted in an employee’s total remuneration package.

2018-19 Annual Report Public Safety Business Agency

Notes to and forming part of the financial statements 2018–19 (cont’d)

67

Public Safety Business AgencyNotes to and forming part of the financial statements for the year ended 30 June 2019

7 Key Management Personnel disclosures

(a) Details of Key Management Personnel (KMP)

(b) Remuneration policies

• Short term employee expenses include:-

- • Long term employee benefits include amounts expensed in respect of long service leave entitlements earned.• Post employment benefits include amounts expensed in respect of employer superannuation obligations.•

non-monetary benefits - may include provision of a motor vehicle and fringe benefits tax applicable to the benefit.

Gives effect to any direction of the Board and is responsible for day-to-day operationsof the PSBA.

salaries, allowances and leave entitlements earned and expensed for the entire year, or for that part of the year during which the employee was a KMP;

QPS Commissioner (Chair)*

From 1 July 2016, a PSBA Board of Management has been established as the governing body of PSBA, and is responsiblefor providing leadership and oversight of the agency. The Chair of the Board, working with the Board Members, is the headof the agency and is supported by the Chief Operating Officer, whose role is to help the Board perform its functions and beresponsible for the day-to-day operations of the PSBA.

Provides extensive corporate services experience from Queensland Treasury.

Remuneration policy for the agency's other KMP is set by the Queensland Public Service Commission as provided for underthe Public Service Act 2008 . The remuneration and other terms of employment for the KMP are specified in employmentcontracts.

The agency's responsible Minister is identified as part of the agency's KMP, consistent with additional guidance included inthe revised version of AASB 124 Related Party Disclosures . That Minister is the Minister for Police and Minister forCorrective Services.

No KMP remuneration packages provide for performance or bonus payments.

The efficient and proper administration, management and functioning of the QPS inaccordance with law. The Commissioner provides the business direction andrepresents QPS at local, community, state, national and international forums as well asceremonial functions.

Position Position Responsibility

QFES Commissioner (Board Member)

Executive General Manager, Queensland Treasury (Board

Member)

Chief Operating Officer

Termination benefits include payments in lieu of notice on termination and other lump sum entitlements (excluding annual and long service leave entitlements) payable on termination of employment or acceptance of an offer of termination of employment.

Remuneration expenses for KMP comprise the following components:

Leading and managing the efficient functioning of the Fire and Rescue Service, RuralFire Service, State Emergency Service, and emergency management and disastermitigation programs and services throughout Queensland. The Commissionerrepresents QFES at local, community, state, national and international forums.

The following details for non-Ministerial KMP include those positions that had authority and responsibility for planning,directing and controlling the activities of the agency during 2018-19 and 2017-18. Further information on these positions canbe found in the body of the Annual Report under the section relating to Executive Management.

Ministerial remuneration entitlements are outlined in the Legislative Assembly of Queensland's Members' RemunerationHandbook. The agency does not bear any cost of remuneration of Ministers. The majority of Ministerial entitlements arepaid by the Legislative Assembly, with the remaining entitlements being provided by Ministerial Services Branch with theDepartment of the Premier and Cabinet. As all Ministers are reported as KMP of the Queensland Government, aggregateremuneration expenses for all Ministers are disclosed in the Queensland General Government and Whole of GovernmentConsolidated Financial Statements, which are published as part of Queensland Treasury's Report on State Finances.

* The chair position is on an annual rotation with the QFES Commissioner.

2018-19 Annual Report Public Safety Business Agency

Notes to and forming part of the financial statements 2018–19 (cont’d)

68

Public Safety Business AgencyNotes to and forming part of the financial statements for the year ended 30 June 2019

7 Key Management Personnel (KMP) disclosures (continued)

(c) Remuneration expenses

1 July 2018 – 30 June 2019

* This position was previously called Assistant Under Treasurer in 2017-18.

1 July 2017 – 30 June 2018

(d) Related party transactions with people/entities related to KMP

302

$'000

Total Expenses

Non-Monetary Benefits

$'000

Short Term Employee Expenses

Post- Employment

Expenses

-

QFES Commissioner (Chair)

$'000 $'000

Long Term Employee Expenses

$'000

6

Remuneration is reported by Queensland Fire & Emergency Services. No additional remuneration was provided by PSBA.

Termination Benefits

-

$'000

Remuneration is reported by Queensland Fire & Emergency Services. No additional remuneration was provided by PSBA.

$'000

301 28

$'000

Position

Remunerated by Queensland Treasury. No additional remuneration was provided by PSBA.

6

- -

QFES Commissioner (Board Member)

QPS Commissioner (Chair)

Executive General Manager, Queensland Treasury (Board

Member)*

Chief Operating Officer

Monetary Expenses

$'000

Short Term Employee Expenses

28

Long Term Employee Expenses

There were no material related party transactions associated with the agency's KMP during 2018-19 (2017-18: Nil).

Chief Operating Officer

Post- Employment

Expenses

Non-Monetary Benefits

$'000

Monetary Expenses

$'000

267

$'000

Termination Benefits

QPS Commissioner (Board Member)

Assistant Under Treasurer (Board Member)

Remunerated by Queensland Treasury. No additional remuneration was provided by PSBA.

Remuneration is reported by Queensland Police Service. No additional remuneration was provided by PSBA.

Position

268

Total Expenses

Remuneration is reported by Queensland Police Service. No additional remuneration was provided by PSBA.

2018-19 Annual Report Public Safety Business Agency

Notes to and forming part of the financial statements 2018–19 (cont’d)

69

Public Safety Business AgencyNotes to and forming part of the financial statements for the year ended 30 June 2019

8 Supplies and services

Aircraft related costsCommunication expensesComputer expensesContractorsMaintenance and repairsMarketing expensesMotor vehicle expensesOperating lease rentalsOperational and other equipment purchasesProfessional servicesProperty expensesShared service provider expensesTravel and accommodationOtherTotal

Accounting Policy - Operating lease rentals

9

Community Helicopter Providers General grants to other organisationsTotal

10

Impairment losses on assets classified as held for sale*Impairment losses on trade receivablesTotal

Accounting Policy - Impairment

- Receivables - Note 12- Intangible Assets - Note 14- Property, Plant and Equipment - Note 15.

4,771

2018

-

40533-

2,30131,656

169,271

13,93130,350

Impairment losses may arise on assets held by the agency from time to time. Accounting for impairment losses is dependentupon the individual asset (or group of assets) subject to impairment. Accounting policies and events giving rise to impairmentlosses are disclosed in the following notes:

(123)

4,369

Grants and subsidies

Impairment losses/(gains)

2,543

36

621

147,688

(584)

$'000

11,878

33

1,992

17,549

17,961

573,409

4,286

(87)(584)

3,037

19,813

* The impairment loss on assets classified as held for sale arises because of the transfer of land and buildings from non-current property, plant and equipment as it is no longer measured at its fair value but at fair value less selling costs.

2019

216

7,131

37,051

15,120

6,896

Operating lease payments are representative of the pattern of benefits derived for the leased assets and are expensed inthe periods in which they are incurred. Material incentives received on entering into an operating lease are recognised asliabilities.

23,328

$'000

15,51916,204

9,335

31

5,4714,5606,412

2018-19 Annual Report Public Safety Business Agency

Notes to and forming part of the financial statements 2018–19 (cont’d)

70

Public Safety Business AgencyNotes to and forming part of the financial statements for the year ended 30 June 2019

11 Other expenses

Audit fees *Deferred appropriation payable to Consolidated FundInsurance premiums-otherInsurance premiums-QGIFInterest expenseLoss on disposal of non-current assetsServices received below fair value **Special paymentsLicence and registration expensesOther ***Total

2,550

417 372

1,950

$'000

-

2,484

$'000

111

158

37

5716,05910,546

3398,701

2,466

2018

957 1,159

1,243

296

129

3,095

2019

84

* Total audit fees quoted by the Queensland Audit Office for the 2018–19 financial statements are $270,000 (2017-18:$270,000).

** For 2018-19, the services received below fair value figure of $0.94m (2017-18: $1.16m) represents an estimate of costs for services provided to the Public Safety Business Agency from the Queensland Police Service.

*** Includes clearing of prior year aged items.

Accounting Policy - Insurance

The majority of the agency’s non-current physical assets and other risks are insured through the Queensland Government Insurance Fund (QGIF) with premiums being paid on a risk assessment basis.

For litigation purposes, under the QGIF policy, the agency would be able to claim back, less a $10,000 deductible, the amount paid to successful litigants.

The department has no contingent liabilities which would have a material impact on the information disclosed in the 2018-19 financial statements.

Accounting Policy - Special payments

Special payments include ex gratia expenditure and other expenditure that the agency is not contractually or legally obligated

to make to other parties.

There were nil special payments over $5,000 made during 2018-19.

Accounting Policy - Losses

Certain losses of public property are insured with the Queensland Government Insurance Fund (QGIF). The claims made in respect of these losses have yet to be assessed by QGIF and the amount recoverable cannot be estimated reliably at reporting date. Upon notification by QGIF of the acceptance of claims, revenue will be recognised for the agreed settlement amount and disclosed as 'Other Revenue'.

Accounting Policy - Services received free of charge, below fair value or nominal value

Contributions of services are recognised only if the services would have been purchased if they had not been donated and their value can be measured reliably. Where this is the case, an equal amount is recognised as a revenue and an expense in the Statement of comprehensive income.

2018-19 Annual Report Public Safety Business Agency

Notes to and forming part of the financial statements 2018–19 (cont’d)

71

Public Safety Business AgencyNotes to and forming part of the financial statements for the year ended 30 June 2019

12 Receivables

CurrentTrade debtorsLess: Allowance for impairment loss

GST receivableGST payable

Accrued debtorsAnnual leave reimbursementsLong service leave reimbursementsEquity injection receivableOther

Total

Accounting Policy - Receivables

Accounting Policy – Impairment of receivables

Disclosure - Credit risk exposure of receivables

13 Other current assets

Prepayments - generalPrepayments - capitalOtherTotal

1,6422,054

293

No loss allowance is recorded for receivables from Queensland Government agencies or Australian Government agencieson the basis of materiality.

Where the agency determines that an amount owing by a debtor becomes uncollectible (after the appropriate range of debtrecovery actions), the debt is written-off by directly reducing the receivable against the loss allowance. Where the amount ofdebt written off exceeds the loss allowance, the excess is recognised as an impairment loss.

The agency uses a provision matrix to measure the expected credit losses on trade and other debtors. Loss rates arecalculated for groupings of customers with similar loss patterns. The agency has determined only one material grouping formeasuring expected losses. The calculations reflect historical observed default rates calculated using credit lossesexperienced on past sales transactions during the last 5 years preceding 30 June 2019. The historical default rates are thenadjusted by reasonable and supportable forward-looking information for expected changes in macroeconomic indicators thataffect the future recovery of those receivables. For PSBA, a change in the CPI rate is determined to be the most relevantforward-looking indicator for receivables. The historical default rates are adjusted based on expected changes to thatindicator.

424

6,538

-

The maximum exposure to credit risk at balance date for receivables is the gross carrying amount of those assets. Nocollateral is held as security and there are no other credit enhancements relating to the agency's receivables.

39,610

3,387

13,892

13,271

360

The allowance for impairment reflects lifetime expected credit losses and incorporates reasonable and supportable forward-looking information. Economic changes impacting the agency's debtors, and relevant industry data, also form part of theagency's documented risk analysis.

Trade debtors are recognised at the amounts due at the time of sale or service delivery. The agency's standard settlementterms is 30 days from invoice date.

55

3,630

2018

15,387

16,637

1,250

2019

592

19,801

2,604 -

$'000

1,250

23,599

19,815

37,324

(243)

53,983

The amount of impairment losses recognised for receivables is disclosed in Note 10.

22,294

Other receivables generally arise from transactions outside the usual operating activities of the agency and are recognisedat their assessed values.

6,727

7,596

(188)

$'000

(13) (621)

13,270

35,030

2018-19 Annual Report Public Safety Business Agency

Notes to and forming part of the financial statements 2018–19 (cont’d)

72

Public Safety Business AgencyNotes to and forming part of the financial statements for the year ended 30 June 2019

14 Intangible assets

Reconciliation

Transfer between classes *

Reconciliation

Accounting Policy - Intangible assets

Accounting Policy - Amortisation of intangible assets

Class

626

23 1,285

(7,697)

Amortisation rate (%)

Less: Accumulated amortisation

For each class of intangible asset the following amortisation rates are used:

591Transfer between classes *

683

794

(369)

Intellectual Property

$'000

-

* Transfers between classes include transfers from property, plant and equipment - refer to Note 15 property, plant andequipment reconciliation.

-507

17,219

Software - Purchased

18,941928

4,675

7.3 - 33.333.3

(8,066)

794112,718(95,500)

Opening balance

(302)

1,839Acquisitions

124,462

12,248

(10,022)

24,659

2018

Gross value

Software purchased

$'000

1,108

(8,477)

(5,371)102,961

Amortisation

794

Software - Internally generated

Closing balance

Each intangible asset, less any anticipated residual value, is amortised over its estimated useful life to the agency. Theresidual value is zero for all the agency's intangible assets as at 30 June 2019.

7.8 - 25.5

18,941928

18,941

Less: Accumulated amortisation

17,219

19,301

Intangible assets are recognised and carried at their historical cost less accumulated amortisation and accumulatedimpairment losses, as there is no active market for any of the agency's intangible assets.

Intangible assets with a cost or other value equal to or greater than $100,000 are recognised in the financial statements,items with a lesser value are expensed.

5,083

670

Intangibles work in

progress

96,293

676

626-

Acquisitions 637

2019

(8,175)

Intangibles work in

progress

2019

(762)

Closing balance 670-

Total

(90,712)(85,341)

$'000

794Opening balance 17,219

1,870

10,952

Software internally

generated

$'000

Total

38

670

2018

928

$'000

Amortisation

12,248

Software purchased

20192019

Software internally

generated

2018

10,950

$'000

5,997

$'000$'000

10,952

531(5,167)

2018

-

Gross value

(105,521)

Accounting Policy - Impairment of intangible assets

All intangible assets are assessed for indicators of impairment on an annual basis. If an indicator of possible impairment exists, the agency determines the asset's recoverable amount. Any amount by which the asset's carrying amount exceeds the recoverable amount is recorded as an impairment loss.

2018-19 Annual Report Public Safety Business Agency

Notes to and forming part of the financial statements 2018–19 (cont’d)

73

Public Safety Business AgencyNotes to and forming part of the financial statements for the year ended 30 June 2019

15 Property, plant and equipment

Reconciliation

Donations receivedDonations made

Infrastructure

(3,377)(1,090,399)

$'000

Buildings Heritage and Plant and equipment

2019$'000

49,322 919,539

cultural

2019

93,875

Land

$'000

656,601

673,273

2019 2019

1,299,119

$'000

673,273-

- - 457 - (9,941)

74,845 43,912

Gross valueLess: Accumulated depreciation

2,389,518(1,891)

7,74667,308

7,541(28,139) (512,327)

(5)- (3,861)- - (2,200)

-

(5) - -

-

353

21,183

12,960 372,275

407,212

1,282,746

90,498

Opening balance as at 1 July 20188,275 476

-40,867 121 -

253 45 --

--

- 9,287

- (15,554)

- (9,483)

(192,120) (1,108)-

Net revaluation increments/(decrements) in operating surplus/(deficit)

6

-

TotalWork in progress

Major plant and

equipment

93,124

$'000$'000

4,228,082

174,693

2,591,949

224,432

2019 2019

9,431

93,124

110,550 2,510,186

(1,636,133)

2019$'000$'000

2019

Closing balance as at 30 June 2019 407,21221,183673,273 1,299,119 93,1247,541 2,591,94990,498

55 -

63,222 8,307Disposals - (1,653)

Assets reclassified as held for sale (1,335) (327)- - -

Transfers between classes * 721

Acquisitions

Net revaluation increments/(decrements) in asset revaluation surplus 9,011 2,603 -Depreciation - (48,004) (541) - (122,298)

(13,901) -

-

(67,123)-- (2,328)

(6,419) (211)

2018-19 Annual Report Public Safety Business Agency

Notes to and forming part of the financial statements 2018–19 (cont’d)

74

Public Safety Business AgencyNotes to and forming part of the financial statements for the year ended 30 June 2019

15 Property, plant and equipment (continued)

Reconciliation

Acquisitions

Donations madeAssets reclassified as held for sale

987

(507)(25,503)

(4)

(11,729)

- 1,386

(182,294)

2,510,186110,550

15

- (129,810)1,229

* Transfers between classes include transfers from intangibles - refer to Note 14 intangible assets reconciliation.

-- 37,059 2,434 - 174,741 220,846

-- - -

- -(132)

-- (4)

(2,118)

67,308

(11,581)

7,746372,275(47,687) (688) (60,545) (212)(20,677)17,205

-- -

1,282,746

3,809 2,803

(22,291) (827)

677,999

27,057(105) 70,552

Less: Accumulated depreciation9,426

Heritage and cultural

Plant and equipment

Donations received

Transfers between classes *

-

(267)-

656,601

- 462 137388

1,226,567

-

Opening balance as at 1 July 2017

(1,669,102)

$'000 $'000

872,741

$'000

446 (1,680)(31,941) (500,466)

2018 2018$'000

110,550656,601 2,418,207

2018 2018 2018

- (1,135,461) -

$'000 $'000

Land Buildings

$'000

66,862

2018

Work in progress

Total

2018$'000

2018

InfrastructureMajor plant and

equipment

Gross value

2,510,186

12,368

12,960

8,036

67,308

71,758

372,275 7,746

118,103 2,453,278338,447

110,550

44,901 4,179,288

Closing balance as at 30 June 2018 656,601 1,282,746 12,960

- 1,386Impairment losses recognised in operating result -

-

- -

Net revaluation increments/(decrements) in operating surplus/(deficit)

Depreciation

Net revaluation increments/(decrements) in asset revaluation surplus (2,900)

-15

Disposals (16)- 84,283

- - (79)(12,997)

- - ---

-

- -

2018-19 Annual Report Public Safety Business Agency

Notes to and forming part of the financial statements 2018–19 (cont’d)

75

Public Safety Business AgencyNotes to and forming part of the financial statements for the year ended 30 June 2019

15 Property, plant and equipment (continued)

Accounting Policy - Ownership and acquisitions of assets

Accounting Policy - Recognition thresholds for property, plant and equipment

151,282Software - Internally generated 4,824

Land 466,342

27,585202,542

3,910

Buildings 949,484

Assets under construction are recorded as capital work in progress until the date of practical completion, at which time theyare transferred to the appropriate asset class.

Items of property, plant and equipment with a historical cost or other value equal to or in excess of the following thresholdsare recognised in the financial statements in the year of acquisition:

186,955342,088

181

$5,000

Where assets are received free of charge from another Queensland department (whether as a result of a machinery-of-Government change), the acquisition cost is recognised at the carrying amount in the accounts of the transferor immediatelyprior to the transfer together with any accumulated depreciation.

Major plant and equipment

7,515 17

LandBuildings

Infrastructure $10,000

Plant and equipment $5,000

Assets acquired at no cost or for nominal consideration, other than from an involuntary transfer from another Queenslandgovernment department, are recognised at their fair value at the date of acquisition in accordance with AASB 116 Property, Plant and Equipment .

120Software - purchased 21

Plant and equipment

Class QFESNBV ($'000)

QPS

Heritage and cultural

PSBA was established to provide corporate and business services including the ownership and management of assets onbehalf of the public safety entities. These assets are recognised as property, plant and equipment and intangibles in thePSBA asset register. The current net book value (NBV) of these assets that are estimated to be directly attributable at 30June 2019 is as follows:

$5,000

21,002

$10,000$1

Heritage and cultural assetsMajor plant and equipment

Historical cost is used for the initial recording of all asset acquisitions. Cost is determined as the value given asconsideration plus costs incidental to the acquisition, including all other costs incurred in getting the assets ready for use.However, any training costs are expensed as incurred.

NBV ($'000)

8,466

Infrastructure

Items purchased or acquired for a lesser value are expensed in the year of acquisition.

Land improvements undertaken by the agency are included with buildings.

Accounting Policy - Componentisation of complex assets

Complex assets comprise separately identifiable components (or groups of components of significant value, that require replacement at regular intervals and at different times to other components comprising the complex asset.

On initial recognition, the asset recognition thresholds outlined above apply to the complex asset as a single item. Where the complex asset qualifies for recognition, components are then separately recorded when their value is significant relative to the total cost of the complex asset.

When a separately identifiable component (or groups of components of significant value is replaced, the existing component(s is derecognised. The replacement component(s are capitalised when it is probable that future economic benefits from the significant component will flow to the agency in conjunction with the other components comprising the complex asset and the cost exceeds the asset recognition thresholds specified above. Replacement components that do not meet the asset recognition thresholds for capitalisation are expensed.

Components are valued on the same basis as the asset class to which they relate.

The agency's aircraft are categorised as complex assets.

2018-19 Annual Report Public Safety Business Agency

Notes to and forming part of the financial statements 2018–19 (cont’d)

76

Public Safety Business AgencyNotes to and forming part of the financial statements for the year ended 30 June 2019

15 Property, plant and equipment (continued

Accounting Policy - Measurement of property, plant and equipment using fair value

Land, buildings, infrastructure, major plant and equipment and heritage and cultural assets are measured at fair value as required by Queensland Treasury’s Non-Current Asset Policies for the Queensland Public Sector. These assets are reported at their revalued amounts, being the fair value at the date of valuation, less any subsequent accumulated depreciation and impairment losses where applicable.

The cost of items acquired during the financial year has been judged by management of the agency to materially represent their fair value at the end of the reporting period.

Accounting Policy - Measurement of property, plant and equipment using cost

Plant and equipment, (that is not classified as major plant and equipment is measured at cost in accordance with AASB 116 Property, Plant and Equipment . The carrying amounts for such plant and equipment at cost has been assessed as not materially different from their fair value.

Accounting Policy - Revaluation of property, plant and equipment measured at fair value

Property, plant and equipment classes measured at fair value are revalued on an annual basis either by appraisals undertaken by an independent professional valuer, internal experts or by the use of appropriate and relevant indices.

Revaluations for land, buildings, infrastructure and heritage and cultural assets using an independent professional valuer are undertaken on a rolling basis over a four year period. However, if a particular asset class experiences significant or volatile changes in fair value, that class is subject to specific appraisals in the current reporting period, where practicable, regardless of the timing of the last specific appraisal. Major plant and equipment assets (aircraft are independently revalued on an annual basis.

The fair values reported are based on appropriate valuation techniques that maximise the use of available and relevant observable inputs and minimise the use of unobservable inputs.

Where assets have not been specifically appraised in the reporting period, their previous valuations are materially kept up-to-date via the application of relevant indices. The agency ensures that the application of such indices results in a valid estimation of the assets' fair values at reporting date. The Australis Asset Advisory Group (AAAG supply the indices used for the land, buildings, infrastructure and heritage and cultural assets. Such indices are either publicly available, or are derived from market information available. AAAG provides assurance of their robustness, validity and appropriateness for application to the relevant assets. Indices used are also tested for reasonableness by applying the indices to a sample of assets, comparing the results to similar assets that have been valued by an independent professional valuer or internal expert, and analysing the trend of changes in values over time. Through this process, which is undertaken annually, management assesses and confirms the relevance and suitability of indices provided by AAAG based on the agency's own particular circumstances.

Any revaluation increment arising on the revaluation of an asset is credited to the asset revaluation surplus of the appropriate class, except to the extent it reverses a revaluation decrement for the class previously recognised as an expense. A decrease in the carrying amount on revaluation is charged as an expense, to the extent it exceeds the balance, if any, in the revaluation surplus relating to that asset class.

2018-19 Annual Report Public Safety Business Agency

Notes to and forming part of the financial statements 2018–19 (cont’d)

77

Public Safety Business AgencyNotes to and forming part of the financial statements for the year ended 30 June 2019

15 Property, plant and equipment (continued

Revaluation methodology

All revaluations were performed by Australis Asset Advisory Group as at 31 March 2019. The fair value as at 30 June 2019 is materially the same as the valuation completed as at 31 March 2019.

Land

Independent revaluations were performed for land in the QFES Northern and Far North Queensland regions and QPS Northern Region as at 30 June 2019, as part of the four year rolling program, by the Australis Asset Advisory Group.

Land not subject to market specific appraisal were revalued using indices supplied by the AAAG based on individual factor changes for each property as derived from a review of market transactions and having regard to the review of land values undertaken for local government locations.

Buildings and Heritage and cultural assets

Independent revaluations were performed for buildings in the QFES Northern and Far North Queensland regions and QPS Northern Region as at 30 June 2019, as part of the four year rolling program, by the Australis Asset Advisory Group.

The process involved physical inspection and was based on current replacement cost, unless a market price in an active and liquid market existed.

Buildings and Heritage and cultural assets not subject to market specific appraisal were revalued using the most appropriate method of indexation, determined by the type of asset, as provided by the AAAG. AAAG calculates the indices by a weighted matrix based on various sources for both a cost approach and market approach. The indices data for the built asset classes are based on construction movements as well as other factors intrinsic to the construction process. These indices were determined to be the most appropriate when considering the agency’s asset types and were accepted and applied by management on the basis they resulted in a materially accurate representation of the fair value of buildings as at 30 June 2019.

Infrastructure

Independent revaluations were performed for infrastructure assets in the QFES Northern and Far North Queensland regions and QPS Northern Region as at 30 June 2019, as part of the four year rolling program, by the Australis Asset Advisory Group.

Infrastructure assets not subject to market specific appraisal were revalued using the most appropriate method of indexation, determined by the type of asset, as provided by the AAAG. AAAG calculates the indices by a weighted matrix based on various sources for both a cost approach and market approach.

Major plant and equipment

Aircraft were independently revalued by the Australis Asset Advisory Group as at 31 March 2019. The revaluations were determined using current market values.

2018-19 Annual Report Public Safety Business Agency

Notes to and forming part of the financial statements 2018–19 (cont’d)

78

Public Safety Business AgencyNotes to and forming part of the financial statements for the year ended 30 June 2019

15 Property, plant and equipment (continued)

Accounting Policy - Fair value measurement

Categorisation of fair values recognised as at 30 June:

1,154,178 1,058,402

Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction betweenmarket participants at the measurement date under current market conditions (i.e. an exit price) regardless of whether thatprice is directly derived from observable inputs or estimated using another valuation technique.

Level 3Level 2

2018656,601

144,941 1,299,11912,960

67,308

2019

Total

1,282,747224,345Buildings

$'000$'000

All assets and liabilities of the agency for which fair value is measured or disclosed in the financial statements arecategorised within the following fair value hierarchy, based on the data and assumptions used in the most recent specificappraisals:

Fair Value Measurement Hierarchy

• Level 1 – represents fair value measurements that reflect unadjusted quoted market prices in active markets for identicalassets and liabilities;• Level 2 – represents fair value measurements that are substantially derived from inputs (other than quoted prices includedwithin level 1) that are observable, either directly or indirectly; and• Level 3 – represents fair value measurements that are substantially derived from unobservable inputs.

None of the agency’s valuations of assets or liabilities are eligible for categorisation into level 1 of the fair value hierarchy.

2019

A fair value measurement of a non-financial asset takes into account a market participant’s ability to generate economicbenefits by using the asset in its highest and best use.

Major plant and equipment

247,746

-

-

7,7467,541

67,308

-

90,498-

21,159 12,960Infrastructure

90,498

7,541

673,273 -Land

Heritage and cultural

673,273

21,183-

656,601 -

Observable inputs are publicly available data that are relevant to the characteristics of the assets/liabilities being valued.Observable inputs used by the agency include, but are not limited to, published sales data for land and general officebuildings.

2019 20182018

Unobservable inputs are data, assumptions and judgements that are not available publicly, but are relevant to thecharacteristics of the assets/liabilities being valued. Significant unobservable inputs used by the agency include, but are notlimited to, subjective adjustments made to observable data to take account of the characteristics of the agency’sassets/liabilities, internal records of recent construction costs (and/or estimates of such costs), assets'characteristics/functionality, and assessments of physical condition and remaining useful life. Unobservable inputs are usedto the extent that sufficient relevant and reliable observable inputs are not available for similar assets/liabilities.

$'000

2018-19 Annual Report Public Safety Business Agency

Notes to and forming part of the financial statements 2018–19 (cont’d)

79

Public Safety Business AgencyNotes to and forming part of the financial statements for the year ended 30 June 2019

15 Property, plant and equipment (continued)

Level 3 fair value reconciliation:

AcquisitionsDisposalsTransfers into level 3 from level 2Transfers out of level 3 to level 2

Gains/(losses) recognised in operating result*

Depreciation

Net revaluation increments/(decrements)

** Gains/(losses) recognised in other comprehensive income comprises:

Net revaluation increments/(decrements)Impairment losses

(932)Assets reclassified as held for sale

Gains/(losses) recognised in other comprehensive income** (8,417) - - -

(40,558) (541) - (211)(40,743)1,058,402

(688)12,960

(20,677)67,308

(8,417)

(8,417)

InfrastructureBuildings Heritage and cultural Major plant and equipment

TotalLevel 3 assets

- 457 - - 457- 1,386 - - 1,386

2018$'000

1,219,2335,159(132)

-

426

(79)-

(79)

(8,417)(79)

-

(13,427)(124)

(13,551)

(4)

101,7871,386

(13,551)

(62,320)1,146,417

1,386

(41,310)(212)7,746

2018$'000

12,368---

$'000

71,7582,434(132)

-(1,653)

- 94,176

1,182,878

-

- --

$'000

1,127,0712,725

--

289-

74,835(665)

$'000

8,036---

(475)

457-

(12,997)

- - 457- 1,386 -

(8,417)(351) -

- - - (8,417)--

(124) -- (12,997)

-

2019 2019 2019 20192018 2018

7,746 1,146,416225 - - -

2019$'000 $'000 $'000 $'000 $'000

225

2018

Carrying amount as at 1 July 1,058,402 12,960 67,308

Donations received - - --

94,176 - -(1,653) - -

(2,005) (104,635) (24) - (67,308) (104,635)

Carrying amount as at 30 June 1,154,178 21,159 - 7,541

Donations made - -

(69,337)

- -

(475) - (12,997)-

(105)457

62,563

-(241)- - -

* Gains/(losses) recognised in operating result comprises:

- - - -- -

- 457

-

-

-

-

-Transfer between classes 54,250 8,307 - 6

(241) -

1,386 -

(267)

--

--

137(4)

27,057

-

2018-19 Annual Report Public Safety Business Agency

Notes to and forming part of the financial statements 2018–19 (cont’d)

80

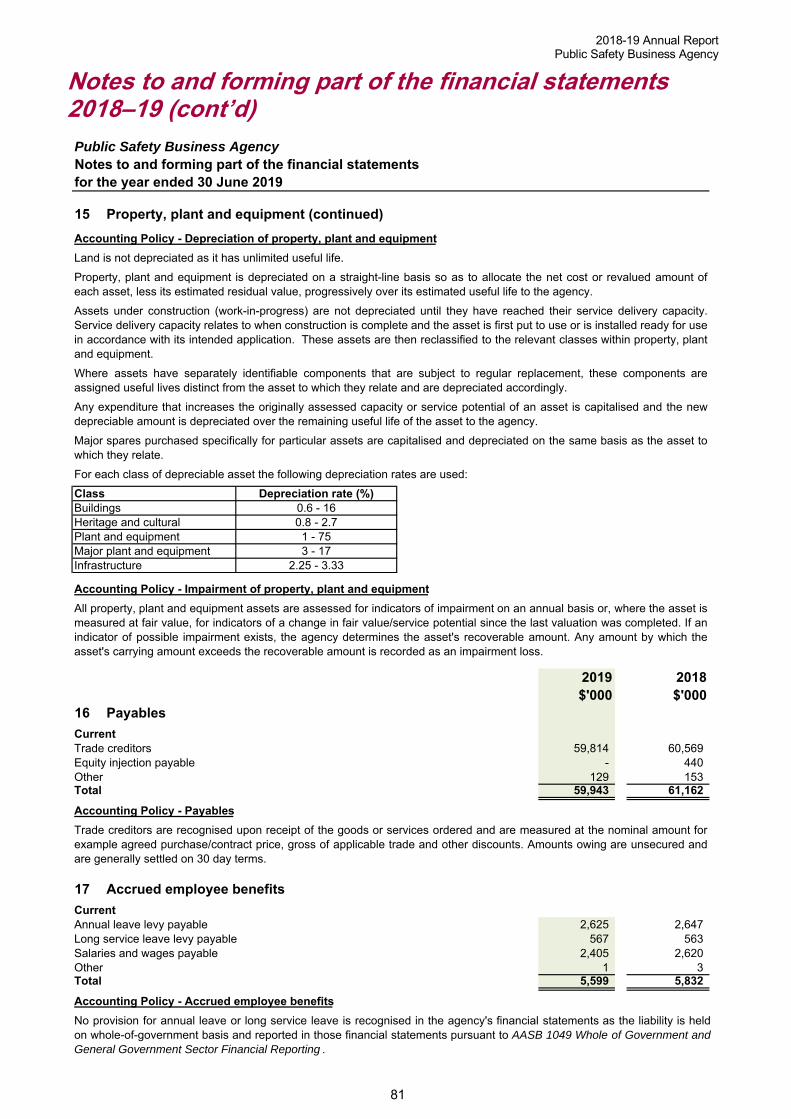

Public Safety Business AgencyNotes to and forming part of the financial statements for the year ended 30 June 2019

15 Property, plant and equipment (continued)

Accounting Policy - Depreciation of property, plant and equipment

Accounting Policy - Impairment of property, plant and equipment

16 Payables

CurrentTrade creditors Equity injection payableOther Total

Accounting Policy - Payables

17 Accrued employee benefits

CurrentAnnual leave levy payableLong service leave levy payableSalaries and wages payableOtherTotal

Accounting Policy - Accrued employee benefits

5,8323

- 440

2,647

$'0002019

Major spares purchased specifically for particular assets are capitalised and depreciated on the same basis as the asset towhich they relate.

5,599

5635672,620

3 - 17

129

59,814

Trade creditors are recognised upon receipt of the goods or services ordered and are measured at the nominal amount forexample agreed purchase/contract price, gross of applicable trade and other discounts. Amounts owing are unsecured andare generally settled on 30 day terms.

59,943 61,162

InfrastructureMajor plant and equipment

2018$'000

2,625

2.25 - 3.33

60,569

Property, plant and equipment is depreciated on a straight-line basis so as to allocate the net cost or revalued amount ofeach asset, less its estimated residual value, progressively over its estimated useful life to the agency.

1 - 75

Any expenditure that increases the originally assessed capacity or service potential of an asset is capitalised and the newdepreciable amount is depreciated over the remaining useful life of the asset to the agency.

Assets under construction (work-in-progress) are not depreciated until they have reached their service delivery capacity.Service delivery capacity relates to when construction is complete and the asset is first put to use or is installed ready for usein accordance with its intended application. These assets are then reclassified to the relevant classes within property, plantand equipment.

Buildings

Plant and equipment

Where assets have separately identifiable components that are subject to regular replacement, these components areassigned useful lives distinct from the asset to which they relate and are depreciated accordingly.

For each class of depreciable asset the following depreciation rates are used:

0.6 - 160.8 - 2.7

Class

Heritage and cultural

Depreciation rate (%)

Land is not depreciated as it has unlimited useful life.

All property, plant and equipment assets are assessed for indicators of impairment on an annual basis or, where the asset ismeasured at fair value, for indicators of a change in fair value/service potential since the last valuation was completed. If anindicator of possible impairment exists, the agency determines the asset's recoverable amount. Any amount by which theasset's carrying amount exceeds the recoverable amount is recorded as an impairment loss.

2,4051

153

No provision for annual leave or long service leave is recognised in the agency's financial statements as the liability is held on whole-of-government basis and reported in those financial statements pursuant to AASB 1049 Whole of Government and General Government Sector Financial Reporting .

2018-19 Annual Report Public Safety Business Agency

Notes to and forming part of the financial statements 2018–19 (cont’d)

81

Public Safety Business AgencyNotes to and forming part of the financial statements for the year ended 30 June 2019

18 Related party transactions with other Queensland Government-controlled entities

Below fair value services provided$ 216.4m$ 0.498m

19 Financial liabilities

CurrentQueensland Treasury Corporation borrowings

Non-currentQueensland Treasury Corporation borrowingsTotal

20 Commitments

(a) Non-cancellable operating lease commitments

Payable - minimum lease paymentsNot later than one yearLater than one year and not later than five yearsLater than five yearsTotal

(b) Capital expenditure commitments

BuildingsNot later than one yearLater than one year and not later than five yearsTotal

Plant and EquipmentNot later than one yearTotal

33,214

PSBA provides services at nil cost to partner agencies as well as other Queensland Government-controlled entities.Services provided and recognised as below fair value include PSBA assets utilised by other entities, fleet and property andfacilities management, human resource services, financial and procurement services and information and communicationservices. The cost of services provided at below fair value materially represents the fair value of the goods and servicesprovided.

Department/Office

20182019

Operating lease commitments inclusive of non-recoverable GST input tax credits at the reporting date are payable as follows:

39,368

5,42924,545

Material classes of capital expenditure commitments inclusive of non-recoverable GST input tax credits at the reporting dateare payable as follows:

-

8,442

71,761

19,6726,894

48,181

Operating leases are entered into as a means of acquiring access to accommodation and storage facilities. Lease paymentsare generally fixed, but with inflation escalation clauses on which contingent rentals are determined. The agency has enteredinto significant leasing arrangements for airport hangars at the Cairns airport and for office accommodation at 30 MakerstonStreet, Brisbane.

48,181

34,133

33,544

7,546

4,656

The agency's primary ongoing sources of funding from Government for its services are appropriation revenue and equityinjections, both which are provided in cash via Queensland Treasury.

1,901

$'000

-

$'000

2,755