targetjobs breakfast news feb 2013

DESCRIPTION

Getting your message across held at The Brasserie at The CumberlandTRANSCRIPT

GETTING YOUR MESSAGE ACROSS

BRYAN FINN 1954–2012

FIVE BREAKFAST NEWS EVENTS IN 2013

• • • • •

WE WANT TO HEAR FROM YOU VIA TWITTER

WWW.BREAKFAST-NEWS.COM

THE GUARDIAN UK 300 - 2013

• 2013 list has been confirmed • Ranking will be revealed mid-April • Opportunities to appear NOW! • 30 unique editorial slots • 100,000 copies sent to UK

campuses in September 2013 • we’ll be in touch!

To buy tickets or a table go to www.targetjobsawards.co.uk or call 020 7061 1927

Shortlists now online – find out the winners on 3 April 2013 at London’s Grosvenor House

AGENDA FOR TODAY

THE ECONOMIC FORECAST

IS GRADUATE RECRUITMENT CHANGING?

GETTING YOUR MESSAGE ACROSS

WHAT ARE YOU SAYING?

THE ECONOMIC FORECAST

THE RECESSION IS OVER

A DEEP RECESSION

-6.0

-4.0

-2.0

0.0

2.0

4.0

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

%

QUARTERLY

ANNUAL

Long-term average

BUT A FRAGILE RECOVERY

LEGACY ISSUES

CONSUMERS WERE THE DRIVING FORCE

-3

-2

-1

0

1

2

3

4

5

6

7

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

% C

HA

NG

E

CONSUMER SPENDINGRETAIL SALES

BUT UNDERPINNED BY BORROWING

-1

1

3

5

7

9

11

13

15

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

%

75

85

95

105

115

125

135

145

155

165

INTEREST REPAYMENTS/DISPOSABLE INCOMES(LHS)

DEBT / DISPOSABLE INCOMES(RHS)

%

THE BIG HOUSEHOLD SQUEEZE

-4

-2

0

2

4

6

2001 2003 2005 2007 2009 2011

% a

nnua

l gro

wth

-4

-2

0

2

4

6

% annual grow

thReal household income*

Inflation Earnings

UNEMPLOYMENT STUBBORNLY HIGH

500

750

1,000

1,250

1,500

1,750

2,000

2007 2008 2009 2010 2011 20120

1

2

3

4

5

6

7%

of workforce

Unemployed 000s (L axis)Unemployment rate (R axis)

Num

ber 0

00s

A DIFFICULT CONSUMER ENVIRONMENT

-3.5

-2.5

-1.5

-0.5

0.5

1.5

2.5

3.5

4.5

5.5

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

% C

HA

NG

E

CONSUMER

SURGE IN PUBLIC SECTOR BORROWING

GOVERNMENT FINANCES WEAKENED

-15

-10

-5

0

5

10

15

20

1999/00 2001/02 2003/04 2005/06 2007/08 2009/10

% o

f GD

P

20

25

30

35

40

45

50

% of G

DP

CURRENT REVENUE (RHS)

CURRENT EXPENDITURE (RHS)

SURPLUS/DEFICIT (LHS)

SO NET DEBT (AS A % OF GDP) SOARED

25

33

41

49

57

65

73

1990-91 1992 1994-95 1996 1998-99 2000 2002-03 2004 2006-07 2008 2010-11 2112 2114-15 2116

% of

GDP

Sustainable Investment Rule

Autumn Statement, December 2012

GOVT RECEIPTS AND SPENDING

35

40

45

50

55

2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16 2016-17 2017-18

% of

GDP

Autumn Statement, December 2012

NEW ISSUES

EUROZONE FRAGILITY

IN THE WRONG PLACES

0

20

40

60

200820031998

%

0

20

40

60

%

Western Europe

Central & Eastern Europe

BRIC (Brazil, Russia,India, China)

Euro Area southern fringe (Greece, Spain, Italy,Portugal)

Share of UK exports (goods & services):

GETTING THE DEBT DOWN

50

60

70

80

90

100

110

120

130

Euro Area France Germany Italy

% o

f GD

P

50

60

70

80

90

100

110

120

130

% of G

DP

2009 2010 2011 2012 2013 2014

GETTING THE DEBT DOWN

50

60

70

80

90

100

110

120

130

140

150

160

Greece Portugal Spain Belgium

% o

f GD

P

50

60

70

80

90

100

110

120

130

140

150

160

% of G

DP

2009 2010 2011 2012 2013 2014

IMBALANCES: THE KEY TO DEBT

-250

-200

-150

-100

-50

0

50

100

150

200

250

2003 2004 2005 2006 2007 2008 2009 2010 2011

€ bn

, ann

ual t

otal

s

-250

-200

-150

-100

-50

0

50

100

150

200

250

€ bn, annual totals

Germany Ireland Italy Spain Greece Portugal

Current account balances

ALL STICKS AND NO CARROTS

20102011

2013

2012

-8

-6

-4

-2

0

2

4

6

%

-8

-6

-4

-2

0

2

4

6

%

Euro Area Greece Portugal Spain

GDP growth

OUTLOOK

INFLATION – LIKELY TO EASE

-2

-1

0

1

2

3

4

5

6

2009 2010 2011 2012 2013

% c

hang

e m

onth

on

mon

th

CPI RPI

Forecast

Target

Range

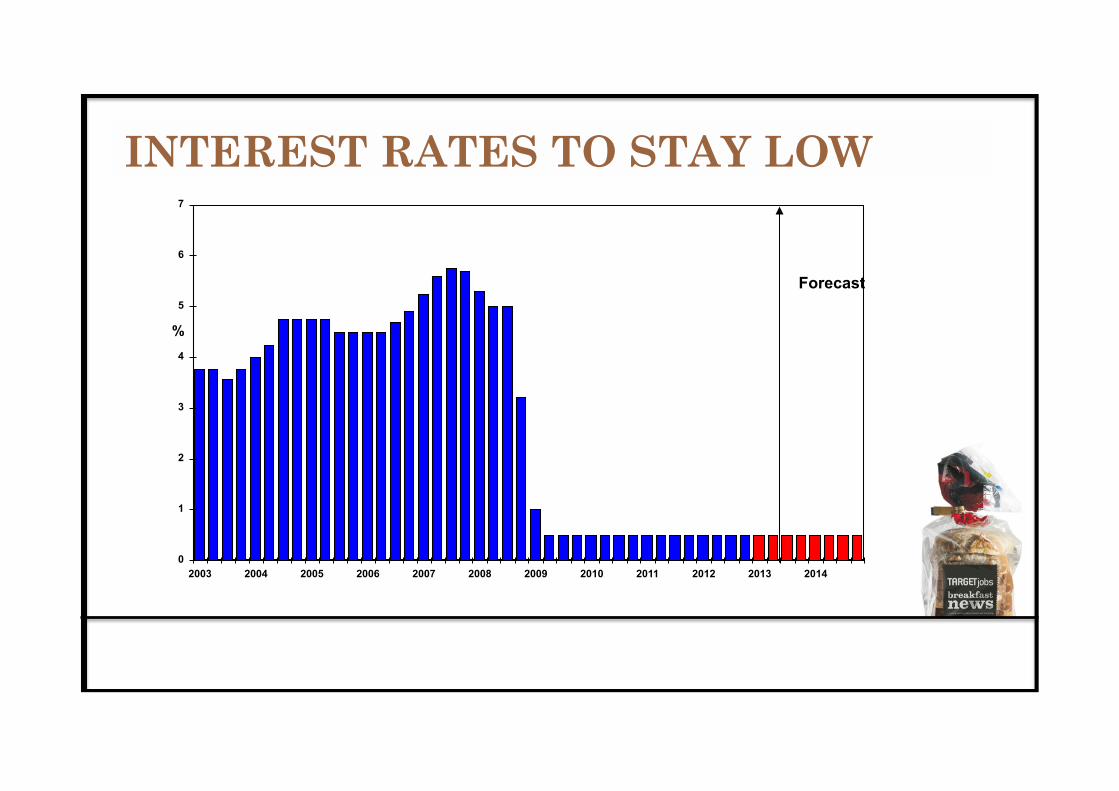

INTEREST RATES TO STAY LOW

0

1

2

3

4

5

6

7

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

%

Forecast

SO STERLING TO REMAIN COMPETITIVE

1.4

1.5

1.6

1.7

1.8

1.9

2.0

2.1

2005 2006 2007 2008 2009 2010 2011 2012 2013

$/£

1.0

1.1

1.2

1.3

1.4

1.5

€/£

Sterling weaker

US$ / £ (L axis)

euro / £ (R

axis)

Forecast

GDP (100%) = Consumer spending (64%)

WHERE IS GROWTH COMING FROM?

REAL EARNINGS GROWING AGAIN

-4

-3

-2

-1

0

1

2

3

4

5

6

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Average earnings growthConsumer price inflation

Real earnings growth

%

DEBT REPAYMENT UNDERWAY

75

100

125

150

175

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011

%

75

100

125

150

175

%

Household debt:income ratios

A SLOW CONSUMER RECOVERY

-3.5

-2.5

-1.5

-0.5

0.5

1.5

2.5

3.5

4.5

5.519

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

1220

1320

14

% C

HA

NG

E

CONSUMER Forecast

GDP (100%) = Consumer spending (64%) +

Investment (15%)

WHERE IS GROWTH COMING FROM?

CORPORATE SECTOR IN GOOD SHAPE

30

40

50

60

70

80

2001 2003 2005 2007 2009 2011

£ bi

llion

8

10

12

14

16

18

%

Gross operating surplus

Profitability

Operating surplus and profitability of UK private non-financial companies

BUT COMPANIES NOT SPENDING

50

60

70

80

90

100

110

120

2001 2003 2005 2007 2009 2011

%

40

50

60

70

80

90

100

110

120

130

140

£ billion

Investment relative to post-tax surplus(L axis)

Level of investment (R axis) Investment by Private Non-financial Corporations

INVESTMENT TO PICK UP……AT LAST

-16

-12

-8

-4

0

4

8

12

16

20

24

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

% a

nnua

l gro

wth

Business Investment Forecast – OBR 2012

GDP (100%) = Consumer spending (64%) +

Investment (15%) +

Government spending (23%)

WHERE IS GROWTH COMING FROM?

GETTING THE DEFICIT DOWN

0

30

60

90

120

150

180

2009/10 2010/11 2011/12 2012/13 2013/14 2014/15 2015/16 2016-17

£ bn

0

2

4

6

8

10

12

%

Net borrowing (L axis)

% of GDP* (R axis)

GDP (100%) = Consumer spending (64%) +

Govt consumption (23%) +

Investment (15%) +

Net trade (-2%) (Exports 30% – Imports 32%)

WHERE IS GROWTH COMING FROM?

EXPORTS STARTING TO RESPOND

-30

-20

-10

0

10

20

30

15/03/2002 15/03/2003 15/03/2004 15/03/2005 15/03/2006 15/03/2007 15/03/2008 15/03/2009 15/03/2010 15/03/2011

GoodsServices

Ann

ual P

erce

ntag

e ch

ange

LIGHT AT THE END OF THE TUNNEL

SLUGGISH GROWTH AS GOOD AS IT GETS

-6.0

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

2007 2008 2009 2010 2011 2012 2013

%

QUARTERLY

ANNUAL

Long-term average

Forecast

THANK YOU

IS GRADUATE RECRUITMENT CHANGING?

WHAT HAS CHANGED (OVER THE PAST 5 YEARS)

CHANGES IN PRIORITIES

CHANGES IN RESOURCES

CHANGES IN THE MEDIA LANDSCAPE

CHANGES TO THE EMPLOYER BRAND

CHANGES IN THE QUALITY OF GRADUATES RECRUITED

CHANGES IN THE PROFILE OF GRADUATE RECRUITMENT WITHIN THE BUSINESS

WHAT WILL CHANGE (IN THE NEXT 5 YEARS)

CHANGES TO TALENT ENTRY ROUTES

•

• •

•

CHANGING PRIORITIES IN GRADUATE ATTRACTION

CHANGES IN DELIVERY OF GRADUATE RECRUITMENT

• • • •

THINGS HAVE CHANGED AND WILL CONTINUE TO CHANGE BUT EVOLUTION, NOT

REVOLUTION

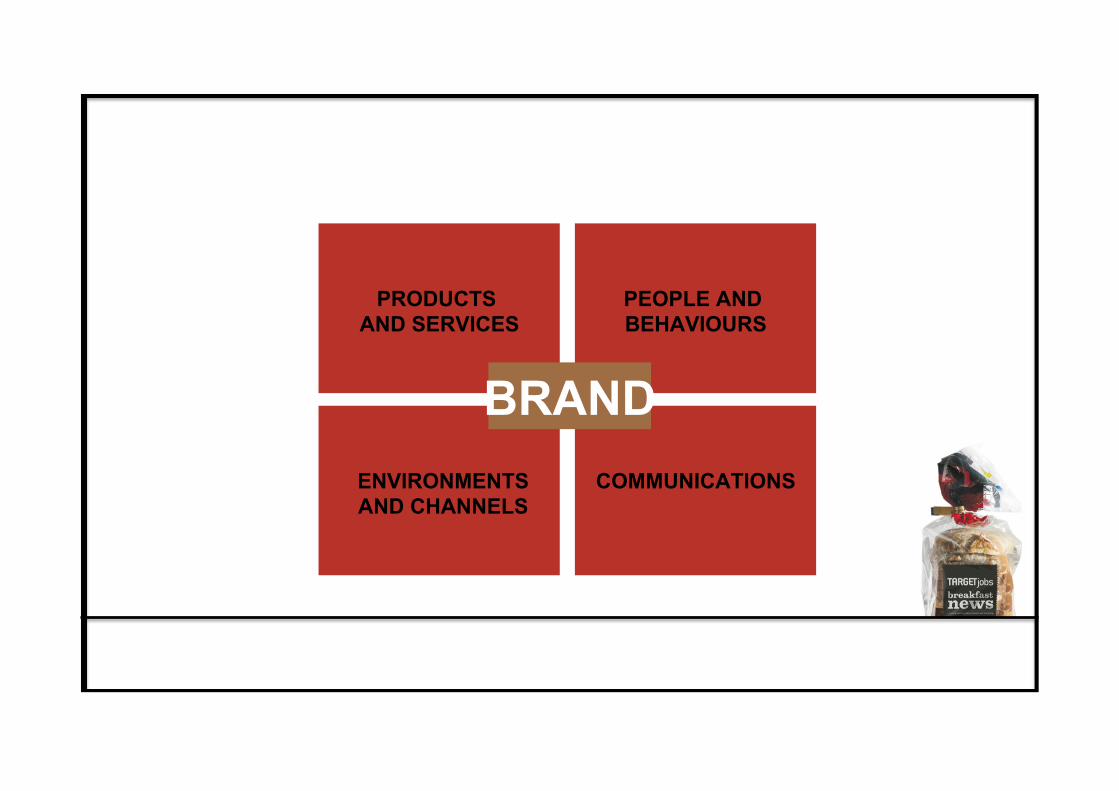

GETTING YOUR MESSAGE ACROSS

PRODUCTS AND SERVICES

PEOPLE AND BEHAVIOURS

ENVIRONMENTSAND CHANNELS

COMMUNICATIONS

CLARITY CONSISTENCY LEADERSHIP

GETTING YOUR MESSAGE ACROSS

SEARCH

WATCH VIDEO ON

PHONE

DOWNLOAD IPHONE

APP

COMPARE SHOP ONLINE

LIKE US ON

BUY ITEM

SHOP ON WEBSITE

WATCH YOUTUBE

COMMERCIAL

VIEW PRINT AD

READ BLOG

VIEW BANNER

AD

READ REVIEWS

WATCH TUTORIAL

DEMO PRODUCT IN STORE

66%

65%

63%

61%

61%

60%

56%

51%

48%

45%

44%

42%

38%

0% 10% 20% 30% 40% 50% 60% 70%

They pay fairly compared to the competition

They have a positive impact on people’s lives

They give me responsibility to make a difference

They set high standards for the quality of work

They are well known for looking after their customers

They treat employees respectfully

Their products or services are seen as being the best

They are praised for their ethical standards

They give back to the community

They have a celebrated heritage

They consistently produce great financial results

They have inspiring senior managers

They are represented positively in the media

Ranking score (%)

WHAT MAKES YOU PROUD AT WORK?

0.23

0.27

0.31

0.34

0.34

0.35

0.36

0.38

0.39

0.44

0.47

0.52

0.63

0.00 0.10 0.20 0.30 0.40 0.50 0.60 0.70

They have a celebrated heritage

They give back to the community

They consistently produces great financial results

They are represented positively in the media

They are praised for their ethical standards

They pay fairly compared to the competition

They have a positive impact on people's lives

They give me responsibility to make a difference

They have inspiring senior managers

They treat employees respectfully

They are well known for looking after their customers

They set high standards for the quality of work

Their products or services are seen as being the best

Correlation score

WHICH FACTORS SHOW THE STRONGEST CORRELATION?

“ to promote the development of China’s brand commodities so as to benefit the world’s people . development of brand commodities concerns China’s economic growth and social progress”

0

50

100

150

200

250

Interbrand Top 100 Portfolio

S&P 500 Index MSCI World Index

BEST GLOBAL BRANDS BY SECTOR Sector Breakdown

FINANCIAL SERVICES 14

ELECTRONICS 14

FMCG 11

AUTOMOTIVE 12

ALCOHOL 7

LUXURY 7

BUSINESS SERVICES 5

DIVERSIFIED 5

BEVERAGES 4

INTERNET SERVICES 4

RESTAURANTS 4

APPAREL 3

MEDIA 3

COMPUTER SOFTWARE 2

SPORTING GOODS 2

ENERGY 1

HOME FURNISHINGS 1

TRANSPORTATION 1

Names Visual identity

Product ranges External communications

Vision Values

Management controls

Business processes

Training and recruitment

Beliefs and personality

Employee communication

Clear brand strategy

Methods of rewards Sense of purpose

Shared sense of fate

BRAND AS CENTRAL ORGANISING PRINCIPLE

SALES

MARKETING

MANUFACTURING/ RETAIL OPERATIONS

DISTRIBUTION

R&D

FINANCE

TO THIS:

BRAND STRATEGY

TRADITIONAL COMMUNICATION

HR

SALES

MARKETING

MANUFACTURING/ RETAIL OPERATIONS

DISTRIBUTION

R&D

FINANCE

HR

BRAND STRATEGY

BUSINESS STRATEGY

FROM THIS:

BUSINESS STRATEGY

Brand strategy

HR strategy & practice

Business strategy

PRODUCTS AND SERVICES

PEOPLE AND BEHAVIOURS

ENVIRONMENTSAND CHANNELS

COMMUNICATIONS

BRAND

People Brand

People & Behaviours

Environment/channels

Appraisals

Feedback mechanisms

Career customisation

Competencies & Behaviours

Development

Performance management

How people feel when they walk into your office

Interview rooms and experience

Organisational design (team structure)

Job mobility

Recruitment fairs

Roadshows

Products & Services

Communications

Offer letters

Induction packs

Learning and development programmes

Flexible working practices

Comp. & Bens

Advice and guidance for non HR colleagues

Intranet

Milk-rounds

Referral programmes

Recruitment advertising

Newsletters

Social medis

CLARITY CONSISTENCY

CLARITY CONSISTENCY LEADERSHIP

STRONG PEOPLE BRANDS SHARE 5 KEY TRAITS

1. Distinctive stance and reputation as an employer

2. Evokes both emotive and tangible benefits

3. Built into and brought to life by company policies, procedures, and practices

4. Consistently communicated in company actions and behaviours

5. Modelled by leadership

VISION Man is the creator of change in this world and should not be subordinate to machines or systems. MISSION Providing human tools. Dedicated to the empowerment of man, helping change the way we work, learn and communicate. VALUES Individualistic, thinking differently, clarity, clever.

PRODUCTS AND SERVICES

PEOPLE AND BEHAVIOURS

ENVIRONMENTSAND CHANNELS

COMMUNICATIONS

BRAND

HUMANISING TECHNOLOGY COMMUNICATIONS

PRODUCTS AND SERVICES

ENVIRONMENTS AND CHANNELS

PEOPLE AND BEHAVIOURS

DELIVERING THE BRAND

• • • •

• •

• •

GOOGLE – LANGUAGE AND TONE OF VOICE

CLEAR AND CONSISTENT BRAND IDENTITY

BMW – CONSISTENT TRAINING AND DEVELOPMENT

“At BMW Brand Academy, we train staff and produce training materials around the BMW brand, as well as bringing best practice and knowledge for the management to share”

‘Our mission is to be the earth’s most customer-centric company it’s the job of every person in this company to reinforce the culture, including me.’

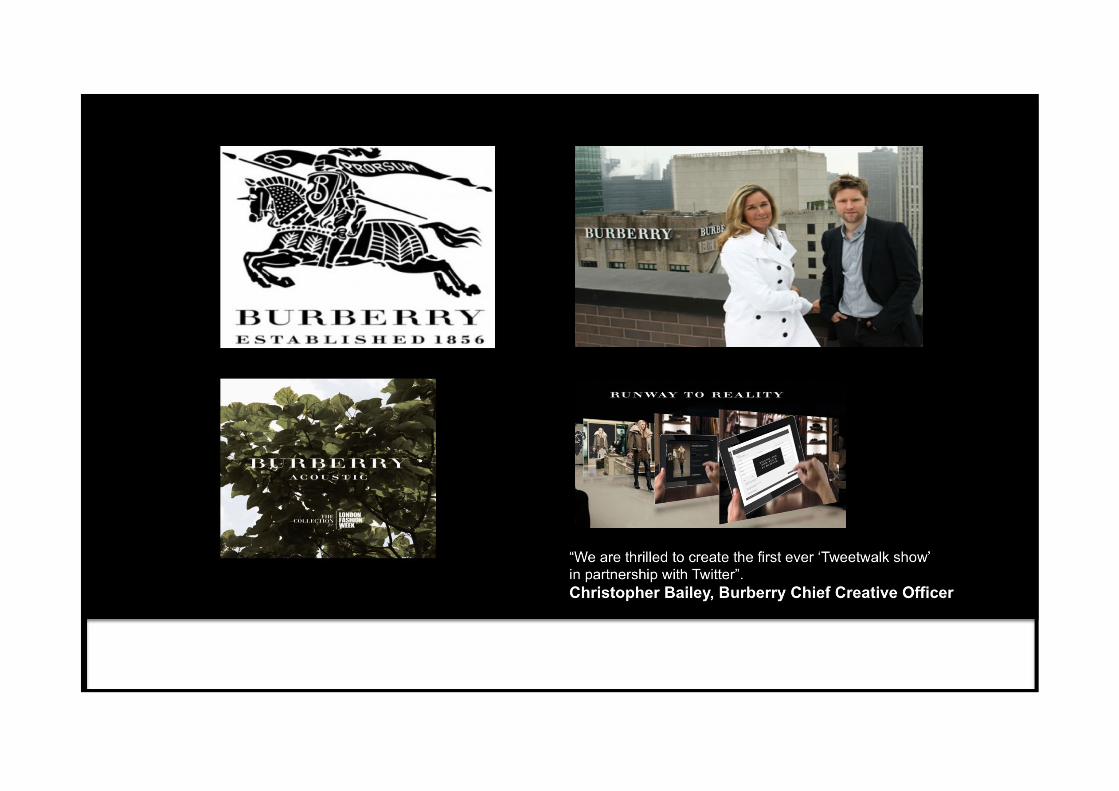

“We are thrilled to create the first ever ‘Tweetwalk show’ in partnership with Twitter”. Christopher Bailey, Burberry Chief Creative Officer

• Consistent rigorous training programs • Fact based and hypotheses • Call assignments “engagements” • Confidentiality is cardinal • Never work alone, always in a team • Coaching/ mentoring as soon as you arrive

BEST PRACTICE? GOLDMAN SACHS

GOLDMAN SACHS - LANGUAGE

• Excerpts from the Goldman Sachs Business Principles • superior returns to our shareholders • profitability is critical • uncompromising determination to achieve excellence • We make an unusual effort to identify and recruit the very best person for every job. Although our activities are measured in billions of dollars, we select our people one by one • Being diverse is not optional; it is what we must be. • We have no room for those who put their personal interests ahead of the interests of the firm and its clients. • The dedication of our people to the firm and the intense effort they give their jobs are greater than one finds in most other organizations. • We consider our size an asset that we try hard to preserve • Our business is highly competitive, and we aggressively seek to expand our client relationships .

GOLDMAN SACHS - LANGUAGE

• Excerpts from the Goldman Sachs Business Principles • superior returns to our shareholders • profitability is critical • uncompromising determination to achieve excellence • We make an unusual effort to identify and recruit the very best person for every job. Although our activities are measured in billions of dollars, we select our people one by one • Being diverse is not optional; it is what we must be. • We have no room for those who put their personal interests ahead of the interests of the firm and its clients. • The dedication of our people to the firm and the intense effort they give their jobs are greater than one finds in most other organizations. • We consider our size an asset that we try hard to preserve • Our business is highly competitive, and we aggressively seek to expand our client relationships .

“In a future where physical and virtual worlds will blend every brand

will have the possibility of becoming both a powerful medium and a power retailer - if they can

quickly build strong enough relationships.”

The Future of Brands

SEARCH

WATCH VIDEO ON

PHONE

DOWNLOAD IPHONE APP

COMPARE SHOP

ONLINE

LIKE US ON

BUY ITEM

SHOP ON WEBSITE

WATCH YOUTUBE

COMMERCIAL

VIEW PRINT AD

READ BLOG

VIEW BANNER

AD

READ REVIEWS

WATCH TUTORIAL

DEMO PRODUCT IN STORE

CLARITY CONSISTENCY LEADERSHIP

THE BENEFITS OF HAVING A PEOPLE BRAND

– Higher levels of staff retention and therefore reduced staff turnover costs

– Reduced candidate attraction costs as people want to work for your organisation

– Reduced recruitment costs as you attract higher performers – Higher employee morale and potentially greater productivity – The opportunity to build and reinforce the culture and work

practices of the organisation both internally and externally – Making your overall corporate brand more valued and

valuable

WHAT ARE YOU SAYING?

Change is the

only constant.

Rip Van Winkle

Washington Irving, 1819

Your true nature may

only emerge when you

find yourself cornered.

<---------------18cm------------>

<---

----

----

----

----

--26

cm--

----

----

----

----

--->

THE TROPESCOPE

A ‘TROPE’ ORIGINALLY MEANT A

FIGURATIVE EXPRESSION, BUT

INCREASINGLY IT IS TAKEN TO MEAN

THOSE COMMON CONVENTIONS,

DEVICES AND CLICHĒS FOUND IN

CREATIVE WORKS.

Trope #1

A young person holds up a sign with

SOMETHING WRITTEN ON IT.

Bob Dylan - Subterranean Homesick Blues, 1965

2007

2008

2007

2011

Trope #2

Young people jump into the air in

unison, expressing joy and excitement

that scarce may be contained.

Cultural reference: A-level results day in the local press

2002

2002

2001

2009

The question facing creative teams in the

middle of the first decade of the twenty-

first century was, “Can we create even

more visual impact and exhilaration than

we have seen here?”

The question facing creative teams in the

middle of the first decade of the twenty-

first century was, “Can we create even

more visual impact and exhilaration than

we have seen here?”

The answer was, “Yes we can.”

THE DIATROPE In which two tropes are combined to

create an impact that is EVEN MORE

striking than the sum of its parts.

2009

Trope #3

Young persons sitting on strange

things in high places, the better to

view their future prospects.

2007 2013

Again, the devil taketh him up into an exceeding high mountain, and showeth him all the kingdoms of the world, and the glory of them; and saith unto him, All these things will I give thee, if thou wilt fall down and worship me. Then saith Jesus unto him, Get thee hence, Satan: for it is written, Thou shalt worship the Lord thy God, and him only shalt thou serve.

The Gospel According to St Matthew, Chapter 4, Verses 8-10

Trope #4

The re-purposing of the classic jigsaw

puzzle to express the integration of the skills

and sensibilities of the individual with the

culture and purposes of the enterprise.

2013

Trope #5

Typographical noodling that seeks to

invest a commonplace thought with

anarchic energy and graphic vitality.

2013

What dire offence from am'rous causes springs,

What mighty contests rise from trivial things…

The Rape of the Lock, Alexander Pope, 1712

What dire offence from

am'rous causes springs,

What mighty contests rise

from trivial things “I wanted to give it more impact, it’s like a word cloud, right ?” Graphic design early 21st century.

Trope #6

Tragic hubris that sometimes

provokes the gods to wrath.

2007

Trope #7

Exploring the unique and limitless

potential of recruitment language.

2001 2006 2012

The Inexorable Rise of the Big Four

Experts at the heart of a new economy

Helping power our ambition to remain the foremost professional services firm in the world are a wealth of highly

talented graduates, enjoying work of spectacular range and variety.

A career worth aspiring to

Ambition is a good thing. So are aspirations. Ours have helped to keep us ahead in the global marketplace for

professional services. It’s the ambition of exceptional individuals like you that has helped us achieve our goals. For

you, it’s the promise of a career that can take you further – and faster – than you ever thought possible.

Step into the best career in business

An extraordinary future in business opens up when you join us. Few will be able to match the network you’ll build, the

exposure you’ll gain and the expertise you’ll develop with us. In fact, we’ll give you all you need to become someone

the world’s biggest businesses turn to for advice.

A superlative decade

Face challenges with confidence. Nimbly navigate every obstacle in your path. It’s that

unique quality that’s positioned you where you are today. And it’s what we value here.

Join our team and we’ll open your career path and give you new opportunities to take the

possible and make it real. We’ll solicit your input and provide training, mentorship and

support to boost your aspirations to a global level. And as part of the world’s leading

financial institution, you can create the kind of opportunity that begets greater opportunity

and bigger impact than you ever imagined.

What the Dickens

Your unleashed potential is our most powerful asset. Your ideas, ambition and

talent have the power to drive the future of our business. We reward your

commitment by offering you unparalleled training, support and global

opportunities – because we see cultivating top talent as a critical business

opportunity, not just a nice-to-have. So expect to be stretched. Expect to go

further, faster and higher. And expect to have your potential fulfilled.

Good Heavens Missus

Death Star 2002

In the knowledge economy ideas are the new currency. Here the

ideas of our people are literally re-shaping the business world. It

takes a particular type of mind to play a full part: Intelligent. Lateral.

Curious. For those who aren’t satisfied with just part of the picture,

we offer the widest possible perspective. Clients large and small,

well-established and newly-founded. Projects which span

management consulting, risk, tax, law and every other discipline

An extraordinary future in business opens up when you join us. Few will be able to match the network you’ll build, the exposure you’ll gain and the expertise you’ll develop with us. In fact, we’ll give you all you need to become someone the world’s biggest businesses turn to for advice. It’s your future. How far will you take it? Our clients across the world demand people with exceptional skills and knowledge to help them make vital business decisions every day. That’s why we provide world-class mentoring, training and professional qualifications to take you from strength to strength. If you’re the kind of person who can’t wait to make a difference, consider a career here. We believe that good ideas and innovations can come from anyone, at any level. We offer meaningful opportunities, best-in-class training and a wide variety of career paths for talented people from all academic backgrounds. Plus, with access to important clients and projects, you’ll have the chance to make an impact with global significance. Some advice just states the obvious. But the kind of insight that adds real value to dynamic organisations, such as our clients, takes reason, instinct and the confidence to challenge assumptions right from day one. You’ll enjoy tough challenges, seek out opportunities and be ready to kick start a career as a trusted adviser at the heart of business. The way the world does business is changing. We’ve invested in an economic future led by emerging markets and grounded in established economies. That’s why we’re looking for graduates with open minds, international perspectives and a focus on change. We can offer exposure to global markets and experience, training and experts that will prepare you for a long and successful career. Unless you’ve grown up in a boardroom, things like dealing with corporate politics, working directly with big business clients, having to travel at short notice, having to report to someone, knowing when to express your opinion and when to keep schtum are unknown quantities to you right now. Rest assured though, we get that and will give you the training, development and support you need to deal with every aspect of your new working world. Do you have bursting ambition? If you can lead and inspire as part of a team, take the next step now towards applying to work for a world-class business. Your career is just that, yours. You choose it. You live it. You make it happen. To get the best from it, you need the best opportunities. That’s why opportunity is at the heart of a career with us. Opportunities to grow as an individual, to build lasting relationships and make an impact in a place where people, quality and value mean everything. The fresh-thinking you generate. The conversations you instigate. The skills you develop. The relationships you grow. The unique contribution you make will help shape the future of our organisation. You’ll need to be able to work in a constantly changing environment and there will be plenty of challenges along the way – but, in return, you can expect to build a truly rewarding career. Ready to make a lasting difference?

Tropes are teleologically

ambiguous and subjective:

how are we to chart our

critical landscape without

numerical expression?

The Portland-Kirby Index®

Towards a thematic and contextual taxonomy of

semiological concepts employed in twenty-first-

century graduate marketing.

Work Group © 2012

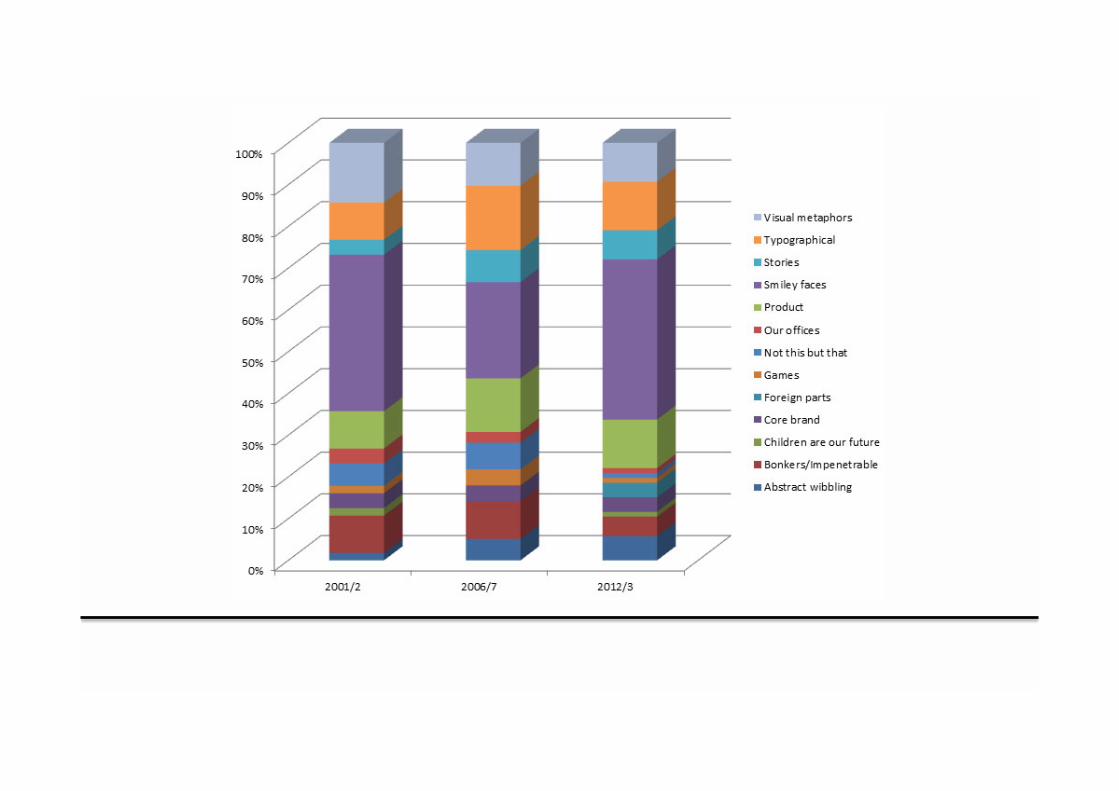

Abstract wibbling

Bonkers/impenetrable

Children are our future

Core brand

Foreign parts

Games

Not this but that

Our offices

Product

Smiley faces

Stories

Typographical

Visual metaphors

The Portland-Kirby Index®

A theoretical construct based

on forced-recall studies with

salient target audiences.

Work Group © 2012

PORTLAND-KIRBY INDEX Phylum 1: “Abstract wibbling”

If you don’t have time to think through what you

want to say, abstract expressionism may be the

way to go. Chuck it all in, but beware of

unfortunate juxtapositions

The most obvious answer

to the question is “job centre plus”

2013

PORTLAND-KIRBY INDEX Phylum 2: “Bonkers/Impenetrable”

Sometimes, you just wish you had been at the

meeting where the idea was presented - and

bought. It probably made sense at the time

2007

2007

PORTLAND-KIRBY INDEX Phylum 3: “Children are our future”

EITHER, (i) the emotive use of a winsome infant to impart the

social and community value of your contribution; OR (ii) the child

as symbolic quintessence of idealistic, all-is-possible aspiration.

2013

PORTLAND-KIRBY INDEX Phylum 13: “Visual metaphors”

(Class 13a: “Signposts”)

Signposts are often used to symbolise a choice

of direction, either in literal geographical terms or

as a broader metaphor for career options.

2001

2010

PORTLAND-KIRBY INDEX Phylum 13: “Visual metaphors”

(Class 13b: “Living things”)

Flora and fauna-based metaphors may be used to borrow

dynamism and meaning from the natural world. It is important to

select organisms that resonate with the target audience.

2007

2007

Fruit & Veg 2012, 2013

PORTLAND-KIRBY INDEX Phylum 7: “Not this, but that ”

Oft beginning with a presumptuous summary of

the reader’s misconceptions and prejudices, the

writer offers to share a profundity that would else

be hidden from the common intelligence

2007

2007

Abstract wibbling

Bonkers/impenetrable

Children are our future

Core brand

Foreign parts

Games

Not this but that

Our offices

Product

Smiley faces

Stories

Typographical

Visual metaphors

The Portland-Kirby Index®:

a thematic and contextual

taxonomy of conceptual

treatments employed

in twenty-first-century

graduate marketing.

Work Group © 2012

A multivariate regression analysis using the Portland-Kirby

Index provides compelling proof that creativity in graduate

marketing is not infinite, but ordered by structured and

limited rules, the close examination of which can provide

clues to the state of the economy.

2001/2002

2012/2013

2006/2007

What this means for the economy.

What does the world leader in marketing communications recommend?

I lied...

Two glorious pieces of

graduate communication

2013

SMILEY, HAPPY FACE [ ] BRAND CHECK [ ] ARBITRARY RANKING [ ] MISCHIEVOUS WORDPLAY [ ] INVESTOR IN PEOPLE [ ]

2013

THE NEXT BREAKFAST NEWS – THURSDAY 25 APRIL