(tarvainen 2008) marketing strategies for champagne

TRANSCRIPT

BSc Business Studies (2005–2008)

Cass Business School

Marketing

strategies

for

Champagne

Author: William Tarvainen

Supervisor: Prof. George Balabanis

Submission: 27 March 2008

Grade: Distinction

I certify that I have complied with the guidelines on plagiarism outlined in the Course

Handbook in the production of this dissertation and that it is my own, unaided work.

! [email protected] | " +358 (0)40 721 1276, +44 (0)79 1497 0781

Tarvainen (2008)

1

ACKNOWLEDGEMENTS

I would like to dedicate this dissertation to my beloved father, who has not only made it

financially possible for me to study several degrees, but also contributed at a deeper level –

constantly encouraging, never doubting, always inspiring.

My sincere thanks to Professor George Balabanis, who has supervised this

dissertation and been a truly stimulating guide to marketing. I would also like to thank the

academia at Cass Business School for creating an academic environment in which intellectual

discussion challenges students to find their full potential. From the academia, I would

especially like to thank Doctors David Edelshain and Ajay Bhalla for offering not only

outstanding academic support but also for encouraging and building me as an individual.

I am grateful to all the 13 interviewees for taking the time to meet me personally – I

sincerely hope you will find this research useful. I am especially honoured to have worked

with what I consider to be among the very greatest Champagne houses – and some of my

personal favourites.

Lastly, I would like to thank my family and friends. My sister has been an academic

inspiration and also a comfort in my dissertation preparation; and without the inspired late-

night tastings with my Champagne-drinking friends, I would have had a much harder time in

deciding on the dissertation topic.

Tarvainen (2008)

2

ABSTRACT

This dissertation looks at what makes for a good marketing strategy in the Champagne sector.

With global demand outstripping the supply of Champagne, there has been pressure to

manage this demand by getting consumers to trade up to more specialist value-added styles

from the lower-value non-vintage style of Champagne. This changing nature of the

Champagne market generates new opportunities and challenges, and the prominent role of

brands in this market creates unique opportunities for marketing strategies.

To gain a better understanding of marketing strategies and brands in this market, 13

people were interviewed from different parts of the trade, and the findings were analysed in

the light of modern academic thinking in luxuries, brands, and wine. The interviews showed

that among the most crucial aspects for marketing Champagne are visual branding and

distribution channel management, with consistency and quality becoming more vital in the

long term. Shifting the marketing focus onto more value-added styles has clear benefits, but

this has to be carefully managed to avoid confusing the consumer or diluting the brand

identity. The findings resulted in four recommendations for current areas of improvement:

brand the mid-sector; tailor your offering to your customer’s values; communicate your

speciality; and send a consistent message.

Tarvainen (2008)

3

TABLE OF CONTENTS

INTRODUCTION ______________________________________________6 Dissertation structure _________________________________________________________________ 7

PART I: LITERATURE REVIEW __________________________________8

1. Luxury _______________________________________________________________8 Luxury consumers___________________________________________________________________ 10 Veblenian consumers ________________________________________________________________ 11 Snob consumers ____________________________________________________________________ 12 Bandwagon consumers _______________________________________________________________ 13 Hedonist consumers _________________________________________________________________ 13 Perfectionist consumers ______________________________________________________________ 14 The role of culture___________________________________________________________________ 15 New luxury markets _________________________________________________________________ 15

2. Brands ______________________________________________________________16 Brand extensions ____________________________________________________________________ 16 Brand portfolios ____________________________________________________________________ 17 Brand knowledge and linking brands to other entities _______________________________________ 17

3. Wine ________________________________________________________________19 Wine as a hedonic product ____________________________________________________________ 19 Wine consumption and purchasing ______________________________________________________ 19 Wine marketing_____________________________________________________________________ 20

PART II: INDUSTRY OVERVIEW ________________________________22 Definition of Champagne _____________________________________________________________ 23 The history of Champagne (Appendix 1) _________________________________________________ 23 Champagne sales____________________________________________________________________ 24 Champagne markets _________________________________________________________________ 25 Environmental analysis (Appendix 2)____________________________________________________ 27 Industry analysis (Appendix 3) _________________________________________________________ 28 Brands in Champagne ________________________________________________________________ 29 Champagne styles (Appendix 4) ________________________________________________________ 30

PART III: RESEARCH PROCESS ________________________________31 Before the interview _________________________________________________________________ 31 The interview process (Appendix 5) _____________________________________________________ 31 The discussion guide (Appendix 6)______________________________________________________ 32 The interviewees ____________________________________________________________________ 34 Analysing the interviews______________________________________________________________ 35 Interpreting the interviews ____________________________________________________________ 36

PART IV: FINDINGS AND ANALYSIS _____________________________38 Marketing Champagne _______________________________________________________________ 38 Marketing mistakes __________________________________________________________________ 39 The Champagne market ______________________________________________________________ 39 The Champagne consumer ____________________________________________________________ 40 Purchasing Champagne_______________________________________________________________ 41 Indicators of quality and prestige _______________________________________________________ 42 Linking brands to other entities_________________________________________________________ 42 Product lines _______________________________________________________________________ 43 Perception differences________________________________________________________________ 45 Validity and reliability _______________________________________________________________ 46

Tarvainen (2008)

4

PART V: RECOMMENDATIONS_________________________________49 Brand the mid-sector _________________________________________________________________ 49 Tailor your offering to your customer’s values_____________________________________________ 50 Communicate your speciality __________________________________________________________ 51 Send a consistent message ____________________________________________________________ 52

CONCLUSION_______________________________________________53 Further research_____________________________________________________________________ 54

REFERENCES_______________________________________________55

APPENDICES _______________________________________________70

Appendix 1: History of Champagne ________________________________________70 History of Champagne _______________________________________________________________ 70 The process ________________________________________________________________________ 70 The trade __________________________________________________________________________ 70 History of Champagne brands__________________________________________________________ 71

Appendix 2: Environmental analysis _______________________________________72 Political ___________________________________________________________________________ 72 Economic _________________________________________________________________________ 72 Social_____________________________________________________________________________ 73 Technological ______________________________________________________________________ 73 Environmental______________________________________________________________________ 74 Legal _____________________________________________________________________________ 74 Demographic_______________________________________________________________________ 75

Appendix 3: Industry analysis_____________________________________________76 Suppliers __________________________________________________________________________ 76 Buyers ____________________________________________________________________________ 76 New entrants _______________________________________________________________________ 76 Substitutes _________________________________________________________________________ 77 Industry rivalry _____________________________________________________________________ 77

Appendix 4: Champagne styles ____________________________________________78 Non-vintage________________________________________________________________________ 78 Prestige cuvée ______________________________________________________________________ 78 Vintage ___________________________________________________________________________ 78 Rosé______________________________________________________________________________ 79 Blanc de blancs, blanc de noirs _________________________________________________________ 79 Ultra brut__________________________________________________________________________ 79 Sec and demi-sec____________________________________________________________________ 79 Mono-crus _________________________________________________________________________ 80 New combinations___________________________________________________________________ 80

Appendix 5: Discussion guide _____________________________________________81

Appendix 6: Approach letter ______________________________________________83

Appendix 7: Interview codebook___________________________________________84

Tarvainen (2008)

5

LIST OF TABLES

Table 1: Values of luxury...................................................................................................... 9 Table 2: Champagne brand collaborations........................................................................... 30 Table 3: Interviewee perception differences by role in the industry ..................................... 45 Table 4: Interviewee perception differences by experience .................................................. 47 Table 5: Consumer types and Champagne ........................................................................... 51

LIST OF FIGURES

Figure 1: Luxury consumer grid .......................................................................................... 10 Figure 2: Luxury consumer motivations .............................................................................. 11 Figure 3: Global Champagne sales 1997–2007 .................................................................... 24 Figure 4: The proportion of Champagne sales in the top 6 markets...................................... 25 Figure 5: Top 10 Champagne export markets ...................................................................... 26 Figure 6: Environmental factors for Champagne ................................................................. 27 Figure 7: Champagne industry factors ................................................................................. 28

Tarvainen (2008)

6

INTRODUCTION

Champagne is the great success story of wine. Its status as the celebratory sparkling wine is

undisputed – even other wine-producing countries serve Champagne at their embassies

(Lowe 2006). It is often seen as being closer to a luxury commodity than a wine (Stevenson

2005 b), and has arguably one of the strongest-ever unique selling points (Boothman 2005).

Champagne is currently enjoying a boom in global sales, and supply is struggling to keep up

with demand (Beckett 2005 a & 2006; Straker 2007 b).

The great majority of Champagne is a blend of several vintages, and as the entry-level

product to any producer’s product line, non-vintage Champagne also sells at the lowest price

(Juhlin 2004). With limited supply and booming demand, many producers are now

attempting to shift the emphasis from lower-value non-vintage Champagne toward higher-

priced value-added styles; these are more specialist cuvées (blends) such as vintage

Champagne (Evans 2007; Fallowfield 2006 a). However, the value of new Champagne styles

might be more difficult to communicate to the consumer who is more driven by lifestyle than

wine quality. With these emerging opportunities in mind, this dissertation answers to the

research question, “What makes for a good marketing strategy for Champagne?”

To answer the research question, 12 trade interviews are conducted and the findings

examined in the light of past academic research and current industry trends.

This dissertation is targeted toward brand managers and other Champagne sector

decision-makers. Most of the interviewed people work in the United Kingdom (UK), the

largest export market for Champagne (Hey 2008), and thus the findings of this research are

best suited for UK brand managers.

An interesting aspect for research in Champagne marketing is that much cutting-edge

research on marketing is done in countries outside the European Union (EU) that do not

recognise the Madrid Agreement Concerning the International Registration of Marks

(Madrid Treaty) (WIPO 1891), which protects the intellectual property rights (IPRs) of the

word “Champagne”. Thus, there is very limited research on applying concepts of luxury

consumer behaviour (e.g., Liebenstein 1950; Vigneron and Johnson 1999) or brand

management (e.g., Aaker and Joachimsthaler 2000; Keller 2005) to Champagne. This is not

to suggest a total lack of research in Champagne marketing – merely that considerable scope

for further research exists in this area. This dissertation explores this gap in research, adding

Tarvainen (2008)

7

value by combining modern academic thinking on luxuries, brands, and wine with the insight

from the 12 trade interviews.

Dissertation structure

To provide a balanced picture of marketing Champagne, this dissertation combines past

research and current industry analysis to the new information gathered from trade interviews.

The structure of this report is divided into five distinct parts.

To provide an understanding of what is already known of Champagne marketing, Part

I: Literature Review examines past research. Since research into Champagne marketing in

itself is in woefully scant supply, research into three different aspects of Champagne is

reviewed; luxury, brands, and wine – these aspects help to understand the consumption and

marketing of Champagne as a luxurious branded wine.

However, Champagne is more than just a luxurious branded wine, and the

Champagne market has unique characteristics. To understand the speciality of Champagne,

Part II: Industry overview provides a look at the current markets, analysing Champagne from

the perspectives of history, the macro-environment, the industry environment, brands, and

different Champagne styles.

Part III: Research process explains how this particular research was conducted,

helping to understand where the findings might be most applicable.

In Part IV: Findings and analysis, the findings from the 12 interviews are presented

and analysed in the light of theoretical and market knowledge.

Finally, Part V: Recommendations arrives to four recommendations for the modern

Champagne marketer, and the Conclusion sums up what has been researched and where

further research might be directed.

Tarvainen (2008)

8

PART I: LITERATURE REVIEW

An important first step in research into a new area is recognising past research, and how the

aspects of past research can contribute to the new research. Although Champagne is a very

prominent brand in itself, academic research into Champagne marketing is miniscule. Thus,

to get an understanding of what research might be valuable for Champagne marketing,

research into three different aspects of Champagne are reviewed separately. The first part of

the literature review examines past luxury research, and especially the theories of luxury

consumer behaviour. The second part looks at past research in brands, looking at areas such

as brand portfolios and linking brands to other entities. Finally, the third part examines the

specific attributes of marketing wine, also explaining the differences between hedonic and

utilitarian products.

1. Luxury

The word luxury derives from the Latin word for excess, luxus, and it has been researched for

over a century (Soanes and Stevenson 2005). Veblen’s The Theory of the Leisure Class

(1899) was the breakthrough work on luxury consumer behaviour; so influential in the field

that latter research often talks of the conspicuous consumer as the Veblenian consumer. Rae’s

(1834) earlier work examined conspicuous consumption along similar lines. With the

introduction of the concept of “prestige value” (Keasbey 1903), it became easier to examine

and understand luxury products and luxury consumer behaviour.

Research into luxury products has suffered from differing definitions of key terms.

Vigneron and Johnson (1999) define prestige brands as the umbrella category for upmarket,

premium, and luxury brands. This dissertation, however, uses the terminology of the

Champagne industry, where prestige cuvées are at the very highest end of luxury brand

portfolio.

Luxury products can be defined as those “whose ratio of functional utility to price is

low while the ratio of intangible and situational utility is high” (Nueno and Quelch 1998 p.

62). Luxury products present the very extreme in high-involvement decision-making

(Vigneron and Johnson 1999), and people may buy luxury products for what they symbolise

Tarvainen (2008)

9

(Dubois and Duquesne 1993). Luxury also makes people dream, and these attached

emotional and aspirational values justify some of the price premiums of luxury (Dubois and

Paternault 1995). As research has progressed, several aspects of luxury value have been

identified. Table 1 segments and aggregates some research examples of perceived luxury

values into five main categories (the dark areas have not been researched by the given

authors).

Table 1: Values of luxury

The different values of luxury (Table 1) imply that people perceive luxury in different

ways. It is thus important to understand how luxury is perceived – understanding the luxury

consumer is the key to understanding luxury marketing. The following looks at these

different consumer types in more depth.

Tarvainen (2008)

10

Luxury consumers

In early research to different luxury consumer types, Leibenstein (1950) differentiates

between the Veblenian, snob, and bandwagon consumer. The bandwagon effect makes the

luxury consumer more price-sensitive, and the snob effect makes the consumer less price-

sensitive than otherwise. The Veblen effect makes the luxury consumer so price-insensitive

that a higher price can actually increase demand.

Vigneron and Johnson’s (1999) model divides luxury consumers into four different

categories, as indicated in Figure 1. Self-consciousness is defined as the consistent tendency

to direct attention inward or outward: publicly self-conscious consumers are more concerned

on how they appear to others, while privately self-conscious consumers reflect more on their

personal thoughts and feelings. The private or public value of luxury goods is built on the

strong communicative status of these items (Dawson and Cavell 1987). Building on

Leibenstein’s (1950) three consumer types, Vigneron and Johnson (1999) add two further

consumer types: the hedonist and the perfectionist consumer (Figure 2).

Figure 1: Luxury consumer grid

Understanding the differences between luxury consumer types can contribute to

segmenting – value-based segmenting may be a more efficient way to target modern

consumers than traditional demographic segmenting (Forsyth et al. 1999). Understanding

Tarvainen (2008)

11

these consumers also allows researchers to adjust their advertising message to underline the

values perceived as most important in determining the level of luxury (Vigneron and Johnson

1999). Further research on this framework presents tools to measure perceptions of luxury

along the dimensions of Figure 2 in order to manage marketing activities more efficiently

(Vigneron and Johnson 2004). As the primary values of these consumers are very different, it

is important to understand these five consumer types in more depth – the following examines

the specific traits of the Veblenian, snob, bandwagon, hedonist, and perfectionist consumers.

Figure 2: Luxury consumer motivations

Veblenian consumers

Veblenian consumers are motivated by ostentation – conspicuous consumption can be used to

signal wealth, and by inference, status (Veblen 1899; Leibenstein 1950). Conspicuous

products are typically consumed publicly, and thus have primarily interpersonal motivations

(Bearden and Etzel 1982). Highly visible brands are thus best positioned for this consumer

segment.

In addition to high visibility, conspicuous consumers place high importance on price.

Not only is price a perceived as an indicator of quality (Erickson and Johansson 1995), it is

Tarvainen (2008)

12

also a signal of luxury (Lichtenstein et al. 1993). The price of conspicuous products can be

divided into two categories; the real price refers to the actual price the consumer paid for the

product, whereas the conspicuous price is the price other people think the consumer paid for

it (Leibenstein 1950). This has led to a conscious effort to add value to the product by

applying a prestige-pricing strategy in support of other marketing activities of luxury

products (Groth and McDaniel 1993). Conspicuous consumption can also be linked to

materialism through envy – as envy is usually directed at expensive products one cannot

obtain oneself, the envious person consequently places higher value on acquiring and

consuming these products (Wong and Ahuvia 1998).

Snob consumers

Whereas the Veblen effect is directed solely outward, snob consumers also considers

personal desires in luxury consumption (Leibenstein 1950). The snob effect may occur in two

directions; the snob can either take advantage of the limited nature of consumers at the launch

of a new luxury product, or reject a product when it is perceived to lose the rarity value and

becomes more widely available to the masses (Rogers 1995). The primary perceived value of

luxury thus lies in its uniqueness, and the snob consumer emphasises his non-conformity to

the mass by avoiding popular brands (Leibenstein 1950; Vigneron and Johnson 1999; Wong

and Ahuvia 1998).

Like the Veblenian consumer, the snob consumer is also highly aware of price.

Relative scarcity can increase the value the consumer attaches to a brand (Bearden and Etzel

1982; Verhallen 1982), and this limited supply has an even stronger effect on demand if the

product is also seen as expensive (Verhallen and Robben 1994). Prestige pricing can thus also

be used to communicate luxury to the snob consumers, as it can concurrently be an indirect

indication of exclusivity (Groth and McDaniel 1993; Vigneron and Johnson 1999).

Tarvainen (2008)

13

Bandwagon consumers

Whereas snob consumers seek non-conformity to the undesired social group, bandwagon

consumers seek conformity to the desired prestigious social group (Leibenstein 1950). Snob

and bandwagon consumers have the same basic motivation for buying luxury products:

enhancing their self-concept through luxury consumption (Dubois and Duquesne 1993).

Bandwagons can also be seen as the antecedent of the snob effect (Miller et al. 1993). The

bandwagon decision-making process can be seen through the materialistic model; measuring

success by the things one owns (Belk 1985; Richins 1994). The desire to possess and

consume prestige brands can also be seen as a symbolic marker of group membership (Belk

1988); this can mark between the consumption and non-consumption of a luxury brand

(Vigneron and Johnson 1999; Tian and Belk 2005).

Price is relatively weak indicator of luxury for bandwagons, who are the most price-

sensitive of the Leibenstein’s (1950) three luxury consumer types. Consumers may try to

imitate stereotypes of affluence by consuming similar luxury products, which act as devices

for locating other people in the social hierarchy (Dittmar 1994).

The three discussed consumer types reviewed – Veblenian, snob, and bandwagon –

consume luxury for primarily inter-personal motivations. However, many consumers also

consume luxury for primarily personal motivations, such as emotional (hedonist) or quality

(perfectionist) reasons.

Hedonist consumers

Hedonist consumers are more concerned about their own feelings when consuming luxury,

and thus place less emphasis on price as an indicator of luxury. They focus more on the

subjective, intangible benefits of the products, such as sensory pleasure, aesthetic beauty, or

excitement. Hirschman and Holbrook (1982 p.1) define hedonic consumption as the “multi-

sensory, fantasy, and emotive aspects of one’s experience with products”. Hedonist

consumers absorb experiences from luxury products, sometimes escaping from reality by

Tarvainen (2008)

14

engaging in fantasy (Hirschman 1982; Hirschman and Holbrook 1982). Research into

product-fantasy relationships shows that certain products have a “dream premium”; they

possess and communicate this hedonistic value more strongly than other products (Dubois

and Paternault 1995). (Vigneron and Johnson 1999.)

Although hedonist consumers place less importance in the social context of their

consumption (Vigneron and Johnson 1999), differences in consumers’ emotional responses to

products are closely tied to subcultures (Hirschman and Holbrook 1982). The value of

hedonistic goods thus exceeds their functional utility, feeding into consumers’ aspirations of

a better life (Silverstein and Fiske 2003). Those consumers who decide what to buy while

remaining “intentionally oblivious to social demands” are referred to as role-relaxed

consumers (Kahle 1995 p. 1) – this type of behaviour is at the extreme end of personal self-

consciousness (Figure 1).

Perfectionist consumers

In addition to social (Veblenian, snob, bandwagon) and emotional (hedonist) factors,

consumers may evaluate the level of luxury on the basis of perceived quality. Perfectionist

consumers seek reassurance of this superior quality through their own assessment of product

attributes, but also from price (Vigneron and Johnson 1999). Maintaining a quality leadership

and developing quality indicators are key elements in marketing premium products (Quelch

1987).

Price is perceived as an indicator of quality (Erickson and Johansson 1995), and for

some consumers, higher prices can make luxury products even more desirable (Leibenstein

1950; Groth and McDaniel 1993). Although perfectionist consumers rely on their own

perception of the product’s quality, the price cue may serve as further evidence to support the

quality offering (Vigneron and Johnson 1999).

Personal preferences shape the primary values of luxury, as discussed with the five

consumer types. In addition to these internal determinants, external factors also affect how

luxury is consumed; culture plays an important part in luxury consumption.

Tarvainen (2008)

15

The role of culture

Although income is the single most important determinant of luxury consumption, culture

influences luxury consumption across all income classes – the propensity to consume luxury

products may triple in moving from a luxury-to a more luxury-endorsing (Dubois and

Duquesne 1993). Culture also determines how consumers are allowed to respond to luxury,

shaping not only the amount but also the type of luxury products consumed (Hirschman and

Holbrook 1982).

The strongest recent growth in luxury consumption has been in the emerging markets,

and modern research has consequently compared attitudes toward luxury consumption across

different cultures (Dubois and Laurent 1996; Dubois and Paternault 1997; Wong and Ahuvia

1998). New luxury markets can emerge not only in new cultures, but also in unexpected

demographics, as discussed below.

New luxury markets

In addition to searching more and more exclusive markets, the luxury sector has also

extended downward. Whole new market segments have emerged between the old mass

market and the high-end luxury market; these mass affluent can be targeted by slightly

modifying the luxury consumption context (Nunes et al. 2004). Other ways to reach these

new markets are using unconventional price points and extending the distribution channels

downward (Johnson and Nunes 2002). So-called new-luxury products differ from old-luxury

products by being able to generate high volumes despite their premium prices (Silverstein

and Fiske 2003). To support the mass marketing of luxury, special strategies have been

identified (e.g., Nueno and Quelch 1998; Silverstein and Fiske 2003).

This section has identified key values for luxury, and explained how different consumers

value the aspects of luxury. In addition to these internal reasons, external reasons such as the

culture affect luxury consumption, and new markets are emerging at unconventional price

points. Luxury can be communicated through a prestigious brand (Liebenstein 1950; Wong

and Ahuvia 1998), and the next section reviews the aspects of brands in more depth.

Tarvainen (2008)

16

2. Brands

Kotler et al. (2005 p. 549) define a brand as a “name, term, sign, symbol or design, or a

combination of these, intended to identify the goods or services of one seller or group of

sellers and to differentiate it from those of competitors.” However, these external attributes

are only one dimension to brands – a brand can also be viewed more internally as a collection

of associations, consisting of benefits and attributes connected to the brand as a consequence

of marketing efforts and personal experiences (Keller 1993).

Brands that have favourable, strong, and unique associations are better differentiated

from competing brands, and can also be more easily extended into other product categories

(Keller 1993). Brands are the most important aspect for marketing when emotional and

experiential aspects of the purchase are strong, and when the experiences are passed from one

person to another (Lemon 2001).

Brand extensions

If a brand is strong, its value can be further utilised by brand extensions. Modern research has

assessed the attractiveness of brand extensions (Aaker and Keller 1990); conditions under

which brand extensions are likely to have favourable associations (Keller and Aaker 1992);

and how this can be done without damaging the core brand (John et al. 1998).

A balance needs to be struck – extensions outside the apparent category may dilute

the image of the parent brand, whereas a too narrowly defined brand makes any future

extensions difficult to justify (Meyvis and Janiszewski 2004). In general, consistent brand

associations are more easily and quickly recalled than diffuse associations, and brands with

narrow category associations thus seem to have a greater potential for extensions (Anderson

and Spellman 1995).

Without explicitly extending the brand, even implicit retail environment cues

implying some commonality between a higher- and a lower-established brand can benefit the

latter (Simmons et al. 2000). Brands, however, have boundaries – they can only be stretched

so far.

Tarvainen (2008)

17

Brand portfolios

When the core brand cannot be further stretched, managing multiple brands as a portfolio can

have significant benefits (Barwise and Robertson 1992; Kotler and Keller 2006). The many

brands can also be seen as a family, with an umbrella mother brand and possible sister brands

(Aaker 2004; Randall 1997) – recent research has even identified “problem child” brands in

some families (Harrison and Hartley 2007).

Brands can be viewed strategically, as a portfolio of assets to be leveraged and

managed to maximise their total worth to the company (Day 1998; Randall 1997). Although

typically seen as the sum of the company’s own brands, an alternative definition of brand

portfolios suggests they should encompass all brands influencing the consumer’s purchase

decision, whether owned or not (Hill and Lederer 2001). This definition would include brand

alliances, brand extensions, and ingredient brands as a part of a company’s brand portfolio.

Coordinating brand portfolio management strategically helps to identify which brands

deserve most attention and investment, and to avoid customer confusion or investment in

overlapping product development or marketing efforts (Carlotti et al. 2004).

Brand knowledge and linking brands to other entities

Brand knowledge means all the brand-related information a consumer has, whether positive

or negative, true or false (Keller 2003). Earlier research examined how these brand

knowledge structures were organised and their effects on consumers (Johnson and Russo

1984; Mitchell 1982). Aaker (1997) suggests five basic perceptual dimensions of brands:

sincerity, excitement, competence, sophistication, and ruggedness. Further research has

helped grasp the relationships that consumers form with brands (Fournier 1998), and the

community relationships among brand users (Muniz and O’Guinn 2001).

Linking brands to other entities give a chance to “borrow” equity from other brands.

This wider brand knowledge can affect how the consumer perceives and responds to the

brand. (Keller 2003.) The most sustainable form of differentiating the brand is when the point

of difference itself can be branded – Aaker (2003) calls this the branded differentiator. The

consumer does not need to thoroughly understand the differentiator – as long as the

differentiator is perceived as delivering something special, it can work to the brand’s

advantage. (Aaker 2003.)

Tarvainen (2008)

18

Understanding how the values of luxury differ across consumers and what kind of

possibilities new modern thinking in brand management can offer have given some insight

into luxury brands, such as Champagne. However, Champagne is also a wine, and it is

important to finally review the research on wine marketing to fully appreciate the

multidimensionality of marketing Champagne.

Tarvainen (2008)

19

3. Wine

Wine as a hedonic product

The core benefit of wine is quenching thirst – but as consumers are willing to pay significant

amounts for wine, there has to be something more to it than fulfilling a basic need. To

understand why consumers might be willing to pay more for wines such as Champagne, it is

important to distinguish between hedonic and utilitarian products. Hedonic products should

not be mixed with the hedonist consumers, although the terms may sound similar.

The underlying rationale behind hedonic products is that consumers do not buy

products merely on the basis of rationally maximising their functional utility (Hirschman and

Holbrook 1982; Millar and Tesser 1986; Tauber 1972). In some instances, emotional desires

are even more important than the basic utilitarian motives in choosing products (Maslow

1999); and consumers may also inject subjective meaning to a product to supplement the

product’s concrete attributes (Hirschman 1980). Measuring exactly how weight consumers

base on the utilitarian attributes of a product is very difficult, but Babin et al. (1994) have

arrived to a scale for assessing these utilitarian and hedonic values of shopping experiences

more accurately.

Empirical research supports this theory of hedonic and utilitarian sources of consumer

attitudes, and they appear as varyingly important across different products and consumer

behaviours (Batra and Ahtola 1991). Due do differences in the nature of different products,

the Batra and Ahtola (1991) findings might not be generalisable to all product categories

(Crowley et al. 1991); research continues in this area (Voss et al. 2003). Segmenting

consumers based on their utilitarian/hedonic shopping goals may offers benefits, as firms can

better adjust their marketing communications to highlight the benefits for the different

consumers (Guido 2006).

Wine consumption and purchasing

Consuming wine is very complex, even for a hedonic product – it is more similar to art

appreciation, with its complex combination of sensory, emotional, and cognitive responses

and a strong role of personal taste (Charters and Pettigrew 2005).

The main bases of wine choice are risk reduction and familiarity; factors indicating

familiarity include previous tastings (Dubow 1992), type or style (Mitchell and Greatorex

Tarvainen (2008)

20

1989), price (Mitchell and Greatorex 1989; Nerlove 1995), brand (Gluckman 1990; Mitchell

and Greatorex 1989), and region (Gluckman 1990; Spawton 1991). When purchasing wine

for an occasion, the first consideration is typically style suitability, then value, endorsement,

and wine character (Halstead 2005). Understanding the consumer motivations allows for

creating marketing strategies specifically tailored for the wine consumer.

Wine marketing

The move toward more branded wines is inevitable (The Economist 16 Dec 1999), and

marketing strategies mark success from failure to wine producers (Felzensztein et al. 2004).

Wine branding differs significantly across global regions, with two different commercial

strategies – European wines based on strictly defined destinations of origins, and new world

wines based on the grape variety (Martinez-Carrasco et al. 2005).

Marketing wine to specific consumer groups is a relatively new concern (Thomas and

Pickering 2003). Producers have been slow to adopt segmentation concepts, being more

preoccupied with wine quality (Spawton 1991). Occasion-based segmentation in the wine

markets may be more useful than user-based segmentation, providing clearer differences in

positioning for brands (Dubow 1992). However, behavioural segmentation using number of

bottles purchased might still be the clearest method for examining a wine market (Thomas

and Pickering 2003). Regional differences persist in channels and retail structures (Malhotra

et al. 1998), but strategies aimed at identifying high-involvement wine consumers may still

be successful on a global scale (Lockshin et al. 2001). Further, strategic partnerships with the

right channels are crucial for a wine producer’s global success (Thach and Olsen 2006).

The price hedonic model is often used as a basis for wine research (e.g., Landon and

Smith 1997; Combris et al. 1997; Oczkowski 2001). The model suggests that the product’s

price is an additive function of a bundle of attributes (Lancaster 1966). In the context of

wines, these attributes may refer to more objective features such as production district, grape

varieties, and the vintage year, or more subjective attributes (Thrane 2004). Although unable

to untangle the supply and demand effects on price (Unwin 1999), these models can provide

important insight to the price implications of a wine’s region, vintage, and subjective

qualities (Combris et al. 2000; Thrane 2004). Empirical research suggests that a wine’s

quality rating is strongly correlated with its price range and producer rating (Horowitz and

Lockshin 2002).

Tarvainen (2008)

21

Part I: Literature review has examined past research on luxuries, brands, and wine – three

different aspects of Champagne. Wine consumption has idiosyncratic characteristics, as does

luxury consumption; brand knowledge gives tools to market to these luxury wine consumers.

Marketing Champagne is not only affected by the consumer behaviour, though –

industry-specific factors are looked at in Part II: Industry overview before going on to the

main research process.

Tarvainen (2008)

22

PART II: INDUSTRY OVERVIEW

The Champagne market is not only unique in relation to other wine markets, but it is also at a

unique point in its history. It has enjoyed its biggest boom ever over the past years, and is

now faced with different choices: whether to increase supply by expanding the area; to

increase the price of generic Champagnes; or to increase the proportion of higher-value

Champagnes to manage the demand.

To gain an inclusive picture of the Champagne market, Part II: Industry overview

examines it through various angles. The part looks at how the history of Champagne has

contributed to its unique status as a world-famous sparkling wine, and current global sales

and regional markets are also reviewed. What happens in the macro-environment of

Champagne affects the industry environment, and factors affecting both environments are

analysed. Having reviewed these factors, brands in Champagne are reviewed from the

perspectives of AC Champagne itself and the various Champagne producers’ brands; and

finally the different styles are mentioned. To begin, though, Champagne is defined more

exactly.

Tarvainen (2008)

23

Definition of Champagne

The word “Champagne” has four meanings. Geographically, it denotes both the Champagne

province in northeastern France, and the delimited area inside the Champagne province that

can produce sparkling wine under the denomination Appellation Champagne Contrôlée (AC

Champagne) as defined by the Institut National des Appellations d’Origine (INAO).

Champagne is also the famous sparkling wine itself produced by the Champenois

(Champagne locals) in that area with the specific production standards set by the INAO.

Fourthly, champagne (with a lower case “c”) can be a generic word for any sparkling wine in

those countries that do not recognise Champagne IPRs (WIPO 1891). This report is on

Champagne, the French sparkling wine defined by the INAO. (Juhlin 2004; Stevenson 2002)

The history of Champagne (Appendix 1)

The wines of Champagne have had a celebratory status for centuries. As explained in greater

detail in Appendix 1, the unique history and characteristics of the region have led to brands

being more dominant than in any other wine area. Champagne differs from most other wine

areas in several respects: even of the best Champagnes can be sold under the same generic

AC Champagne denomination as the poorest ones, and most Champagne is a blend of several

vintages, several grape varieties, and several villages. As consumers often cannot use the

denomination, vintage, grape variety, or village name as an indicator of quality, the

producer’s brand has become one of the few quality indicators for the consumer. (Juhlin

2004; Robinson 2006)

Tarvainen (2008)

24

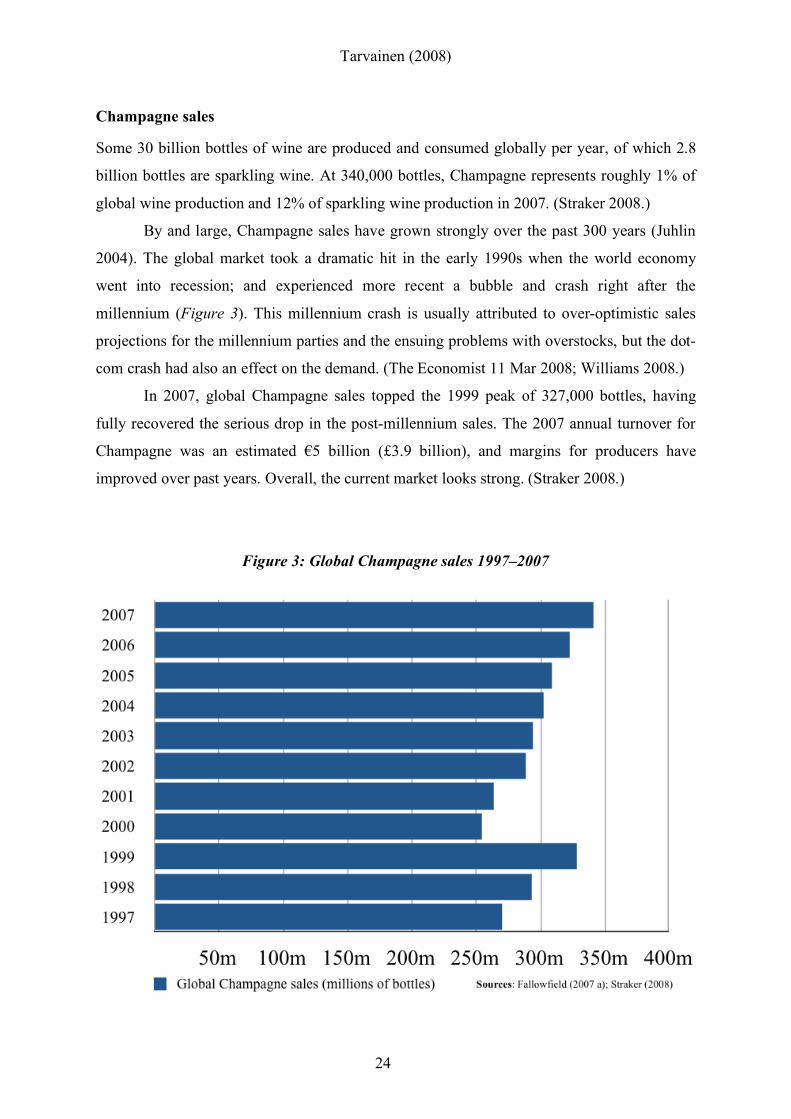

Champagne sales

Some 30 billion bottles of wine are produced and consumed globally per year, of which 2.8

billion bottles are sparkling wine. At 340,000 bottles, Champagne represents roughly 1% of

global wine production and 12% of sparkling wine production in 2007. (Straker 2008.)

By and large, Champagne sales have grown strongly over the past 300 years (Juhlin

2004). The global market took a dramatic hit in the early 1990s when the world economy

went into recession; and experienced more recent a bubble and crash right after the

millennium (Figure 3). This millennium crash is usually attributed to over-optimistic sales

projections for the millennium parties and the ensuing problems with overstocks, but the dot-

com crash had also an effect on the demand. (The Economist 11 Mar 2008; Williams 2008.)

In 2007, global Champagne sales topped the 1999 peak of 327,000 bottles, having

fully recovered the serious drop in the post-millennium sales. The 2007 annual turnover for

Champagne was an estimated !5 billion (£3.9 billion), and margins for producers have

improved over past years. Overall, the current market looks strong. (Straker 2008.)

Figure 3: Global Champagne sales 1997–2007

Tarvainen (2008)

25

Champagne markets

Despite its international appeal, more than half of Champagne is still consumed domestically

(Figure 4). The domestic French market still accounts for 54% of the sales, but exports are

growing more rapidly at 7.9%, compared to the domestic growth of 4.6% between January

and November 2007. The average bottle price is higher for exports, and they also seen as an

attractive buffer against domestic demand volatility. (Hey 2008; Williams 2008.)

Figure 4: The proportion of Champagne sales in the top 6 markets

Tarvainen (2008)

26

Of the export markets the UK is clearly the largest, with sales more than those of the United

States and Germany combined (Figure 5). The UK’s role as the market leader is often

attributed to geographic proximity and a long, shared history with the French. Although the

emerging markets still have very small sales volumes, booming sales growth in them has

created hopes that Champagne could shrug off a possible western recession. (Hey 2008.)

Figure 5: Top 10 Champagne export markets

Tarvainen (2008)

27

Environmental analysis (Appendix 2)

A standard framework for examining the environmental factors is the PEST (political,

economic, social, technological) analysis, which categorises macro-environmental factors by

their source (Grant 2008). The framework here is extended to incorporate environmental,

legal, and demographic aspects as well. Figure 6 presents the currently most relevant macro-

environmental factors for the Champagne industry, and these are analysed in more depth in

Appendix 2.

Figure 6: Environmental factors for Champagne

Tarvainen (2008)

28

Industry analysis (Appendix 3)

The history of Champagne and the current macro-environmental trends have shaped the

industry environment where the brands compete, and the Champagne market is distinctly

different from other wine markets. Figure 7 analyses the industry environment through the

five aspects of Porter’s (1979) Five Forces analysis, and the factors are viewed in more depth

in Appendix 3.

Whereas growers elsewhere usually make wine of their own grapes, Champagne is

characterised by large producers purchasing and blending grapes from several producers and

villages. Although Champagne houses can own some vineyards, they are restricted from

owning or renting more than 15 hectares of land (Stevenson 2005 a). The 100 or so

Champagne houses account for 90% of exports (Mintel 2006), and largest houses are referred

to as the grandes marques. The rest is dispersed between some cooperatives of producers,

and grower-producers doing all or part of the process themselves. (Juhlin 2004.)

What is curious in the UK market is that although Champagne is the most profitable

sector of the British wine trade (Rose 2005), it is the only wine regularly sold on discount

(Mintel 2006). Even the current shortage of Champagne has not restricted high-profile price

promotions, which have had a big impact on the industry – the editorial of The Drinks

Business Champagne Report 2008 remembers 2007 as “the year of half-price Dom Pérignon”

(Schmitt 2008 p. 5), and the same report describes discounting as “deconstructing the value

of Champagne as a luxury good (Cawood 2008 p. 33).

Figure 7: Champagne industry factors

Tarvainen (2008)

29

Brands in Champagne

Demand for Champagne outstrips its supply, and the industry can sustainedly address this

issue not by heavy price increases in the non-vintage, but by moving toward more

differentiated, higher-value Champagnes (Fallowfield 2006 a; Evans 2007). The combination

of intra-industry consolidation and the need for varied product offerings create a particular

need for effective brand portfolio management. Brands in Champagne can be looked from

two perspectives: the following first looks at brand of AC Champagne itself, and the brands

of the individual Champagne producers.

Although the name Champagne itself holds unique brand value (Williams 2007 b), its

sub-brands are less known. In the nearby Burgundy, the terms Premier Cru or Grand Cru on

the bottle label carry enormous value, acting as strong indicators of prestige for the consumer

(Johnson and Robinson 2001; Robinson 2006). In contrast to Burgundy, most Champagne is

a blend of many crus and consumers remain largely unaware about Premier Cru or Grand

Cru Champagnes (Fallowfield 2006 b). To address this gap, some leading Champagne critics

have called for a reshuffle in the classification: Stevenson has called for a dozen or so

hierarchical appellations (Redman 2002), and Juhlin (2004) suggests demoting Champagne

from the Aube area to a secondary status. There has also been a recent counter-trend toward

regionality, as the big Champagne houses promote more mono-cru Champagnes (Fallowfield

2005 b & 2008 a). What is peculiar is that the effort toward finally branding mono-crus and

smaller regions has come from the large houses, although smaller grower-producers would be

optimally positioned to capitalise on this (Stevenson 2005 b). The ongoing debate about the

expansion of AC Champagne has raised some concerns regarding the long-term brand value

of the AC Champagne itself (Hickman 2007 b; Stevenson 2007).

The producer’s brand is the key determinant of consumers’ Champagne purchases

(Juhlin 2004; Fallowfield 2008 b). A prestigious etiquette creates feelings of which hedonic

consumers are willing to pay without apparent limits (Nuikki 2007; Vigneron and Johnson

1999). External cues such as packaging are seen as increasingly important, as Champagne is

becoming more popular as a gift (Boothman 2005). Consumers are not usually told when the

batch for non-vintage Champagnes changes (Juhlin 2004; Edwards 2006), and producers

create a house style that consumers assume to stay consistent and reliable through the years

(Parkinson 2006) – the consumer thus learns to trust the producer’s brand more than

anything. Veuve Clicquot herself showed exemplary branding sense when she patented the

orange colour used in her Champagne labels (Juhlin 2004); now 200 years later, anything in

Tarvainen (2008)

30

Champagne with bright orange is automatically connected to the brand (Boothman 2005).

Not all brands enjoy the unique strength of Veuve Clicquot, though, and linking Champagne

brands to other entities is seen as increasingly important for distinguishing the brand from

competition (Sheppard 2007). Table 2 presents examples of some key brand collaborations of

the leading Champagne producers.

Table 2: Champagne brand collaborations

Champagne styles (Appendix 4)

As Champagne houses are trying to make the most out of the limited grape supply by selling

more added-value products such as the vintage, there has been a pronounced move from the

dominance of the brut non-vintage toward different styles of Champagne (Fallowfield 2006

c). With current high grape prices, the higher returns from selling more premium styles of

Champagne are not only attractive for companies, but also vital for many (Fallowfield 2007

b). Appendix 4 explains the characteristics and trends in different styles.

Part II has analysed the Champagne market from different perspectives: history, sales,

macro-environment, industry environment, brands, and styles. The big picture conveyed was

that Champagne is doing very well, supply is limited, and one way to manage demand is to

shift the emphasis into more specialist value-added styles. Before linking the theory of Part I

and industry insight of Part II to the findings of the 12 interviews, Part III: Research process

explains in more depth how this research was conducted.

Tarvainen (2008)

31

PART III: RESEARCH PROCESS

The dissertation is exploratory and interpretive in nature, and based on face-to-face

interviews and analysis thereof (Sanday 1979). As it is more effective to aim the work for a

specified external audience (Shugan 2003), the target audience of this research consists of

Champagne brand managers and other Champagne industry decision-makers.

Before the interview

The researcher’s personal work history in wine industry had provided a unique opportunity to

scan the challenges and opportunities in the Champagne industry with managers – this served

as a starting point for gathering relevant information. For example, work experience at a wine

shop had suggested that consumers behave differently when buying Champagne to when

buying less aspirational products; that consumers link Champagnes to other entities so

strongly that they might ask for “the Formula 1 Champagne”; and that product lines seemed

to be proliferating.

Secondary sources for research included academic journals and books, trade reports

and magazines, and business papers and magazines. Wine industry reports and wine

magazines such as Decanter, The Drinks Business, Harpers, and Wine & Spirit were used to

identify further issues to be brought up in the interviews, helping also to put the observed

industry trends into perspective. Academic articles were also used, and concepts from

Vigneron and Johnson (1999), Dittmar (1994), and Keller (2005), among others, were used to

shape the discussion guide. Academic jargon was avoided, and rather than asking about

“Veblenian” behaviour, the interviews used more understandable wordings like ostentation,

status, and price perception to define the mentioned ostentations or “Veblenian” behaviour

(Leibenstein 1950; Veblen 1899).

The interview process (Appendix 5)

Face-to-face interviews were selected as the only source of gathering primary data. As this

research looks into the makings of a good marketing strategy, qualitative data seemed to be

more appropriate for exploring this. Interviewing face-to-face allowed for the optimal

Tarvainen (2008)

32

combination of flexibility and depth for this research. Focus groups were not selected as a

tool, since the interviewees were mainly senior managers and organising a focus group for

this sample would not have been feasible regarding their schedules. More quantitative

methods such as surveys do give differential insight, but a combination of qualitative and

quantitative methods were not feasible due to the time and scope limitations of this

dissertation. (McDaniel and Gates 2006.)

For the primary research, 12 face-to-face interviews with professionals from different

parts of the Champagne trade were conducted. Depending on how much time the

interviewees had, the length of the interviews was between 40 and 100 minutes, typically

around 50–60 minutes. Effort was made to avoid assumptions by keeping the questions as

open-ended as possible. All interviews were conducted in greater London, typically at a

conference room at the interviewee’s office or a café. Because the interview discussions did

not go into very sensitive personal areas, a completely private was not as imperative as for

other research projects.

Two managers came to the interview from Ruinart, but all the other managers were

interviewed individually; no differences in response were noted between the Ruinart

interview and other interviews. The interviews were conversational, with some freedom to

focus more on those areas the interviewees felt they had to most to say about. (Gubrium and

Holstein 2001; Hermanowicz 2002; Warren et al. 2003.)

The interviews were semi-structured, following a discussion guide with five main

areas – Champagne marketing, the Champagne market, consumer motives, linking brands to

other entities, and product lines (Appendix 5). Rather than serving as an extensive handbook

for strategic marketing, the research focused on marketing issues of particular relevance in

the current Champagne market, and the discussion topics were selected accordingly.

The discussion guide (Appendix 6)

The interviews began with an ethical disclosure that the interviews would be recorded for

personal records. The background of the interviewee(s) was also inquired to understand how

it might affect their views (Schaeffer and Presser 2003; Reynolds and Gutman 1988).

The first part of the actual interview asked open-ended questions about marketing

Champagne – this allowed the interviewees to spontaneously bring up whatever they

perceived as the most relevant aspects. To understand both positive and negative aspects, the

Tarvainen (2008)

33

interviewees were also asked about most common mistakes, whether currently or in

hindsight.

The second section discussed the Champagne market itself – how the market is and

how it differs from other markets. This included the trends, challenges, and substitutes.

The third section discussed different aspects of Champagne consumers – what roles

and occasions Champagne has for consumers, and what kinds of differences exist. The main

emphasis was on how consumers buy champagne – what aspects are important, what aspects

indicate quality and prestige, and how price is perceived (Gluckman 1990; Mitchell and

Greatorex 1989; Vigneron and Johnson 1999). Without explicitly explaining the five

discussed luxury consumer types (Vigneron and Johnson 1999), questions on private/public

motives (direction of self-consciousness), perceptions of price, imitation, and exclusivity

gave a good picture of who the consumers might be.

Brand partnerships have become very current in the marketing of Champagne

(Boothman 2005; Sheppard 2007), and the fourth section examines them as a form of linking

brands to other entities (Aaker 1997; Fournier 1998; Keller 2003). Event sponsorships and

branded bars were used as current examples of linking brands to other entities.

The fifth section discussed product lines, whether in brand extensions into new styles

or to geographical areas (Aaker and Keller 1990; John et al. 1998; Keller and Aaker 1992), or

by focusing the brand’s attention more to a certain direction (Meyvis and Janiszewski 2004).

This was to understand how to best manage the limited supply of Champagne, and what kind

of implications adding new items to the brand portfolio might have (Aaker and Keller 1990;

Day 1998; John et al. 1998).

To conclude the interviews, the interviewees were asked what advice they would give

to a new marketing manager in the Champagne sector. To end with a positive personal note,

the interviews concluded with a personal vision for Champagne.

In addition to the questions described in the discussion guide, prompting questions

were used to understand the cause and implications of the discussed matter. Prompts included

asking why; why not the other one; how; what is driving this; how sustainable is this; how

does this affect/translate into profitability; how does this affect the brand; how does this

affect the consumer; and is this specific to you or general. These prompts turned the

discussions from descriptive (what is happening) into more analytical (why it is happening)

in nature, going into higher levels of abstraction. (Hermanowicz 2002; Schaeffer and Presser

2003.)

Tarvainen (2008)

34

The interviewees

A total of 13 people were interviewed for this research in 12 sessions. Managers were better

suited than consumers to be interviewed about marketing strategies, although consumer

interviews would certainly have given further insight into how the marketing strategies were

actually perceived. To gain a more balanced view, managers were interviewed both from the

producer and the retailer side – the producers had worked with several retailers and the

retailers with several producers’ brands. Further, the retailer side was more in contact with

actual end-users, whereas the producer side might have a more coherent view of the longer-

term marketing strategies.

The people were interviewed not as official spokespeople of their representative

companies, but rather as individuals with unique experience and insight. It should be noted

that all interviewees had worked at a number of companies in the trade, and thus could also

provide insight into Champagne marketing over and above their current role.

From the producer side, managers from three grande marque Champagne houses

(Bollinger, Pol Roger, Ruinart) were interviewed, as well as a person from the leading

holding company, Moët Hennessy. In addition to these, a manager from a leading Italian

sparkling wine producer (Bisol) was interviewed, not only as a competitor to Champagne, but

also for his long tenure as the manager of Wines & Spirits floor for Harrods. Lastly, one

Champagne consultant was also interviewed to hear the views of someone who had worked

with many different sides of the trade.

o Jonathan Stevens is the Brand Manager at Mentzendorff, owner of Champagne

brands Bollinger and Ayala.

o James Simpson, Master of Wine (MW) is the Director at Pol Roger in the UK.

o Giles Henton and Max Helm are Sales Managers for Ruinart in the UK.

o Sophie Janion is a Sales Assistant at Moët Hennessy UK; despite being at a junior

position, her knowledge and experience into linking luxury brands exceed her status

o Roberto Cremonese is the European Export Manager at Prosecco Bisol Desiderio &

Figli, a leading sparkling wine producer, having also worked as the Sales Manager for

the Harrods Wine Department for six years.

o Maggie McNie MW is a long-time Champagne consultant to producers and

Champagne bodies, buyer, educator, and author of the influential book Champagne

(McNie 1999).

Tarvainen (2008)

35

The secondary data seemed to imply that certain distribution channels were more

desirable for Champagne producers than others; preferred off-trade channels were wine

merchants and high-prestige outlets, and preferred on-trade channels were restaurants and

clubs (Cawood 2007 c; Grant 2007; Woodard 2007 b). Thus, managers from these channels

were interviewed. Although supermarkets are increasingly important retail channels for

Champagne, this dissertation only interviewed managers from specialist or luxury outlets.

From the retailer side, managers were interviewed from London’s big three luxury

department stores (Harrods, Selfridges, Harvey Nichols), a leading wine merchant chain

(Oddbins), an independent fine wine merchant (Roberson Wine), and a restaurant (Harrods

restaurants).

o Dawn Davies is the Sommelier at Selfridges.

o Jeremy Lithgow is the Floor Manager for Wines & Spirits at Harrods.

o Jeremy Lee is the Wine Shop Manager at Harvey Nichols.

o Joe Gilmour is the Manager of Roberson Wine, a past agent for Champagne Devaux.

o Amelia Aragón is a Manager at Oddbins and Export Manager at Cillar de Silos, a

Spanish wine producer.

o Penny Johns is a Restaurant Manager at Harrods, having also managed a Champagne

bar and a wine merchant.

To get 12 responses, 25 companies were contacted. Some companies had a policy of only

commenting in writing; others’ managers were not available for the interview period; still

others never answered. No major trend was seen in what kind of companies either accepted

or rejected the invitation. The standard approach email is shown in Appendix 6.

Analysing the interviews

After the interviews had been completed, they were personally transcribed into written form.

As in interpretive research, the data was observed, selected, coordinated, and interpreted by

the researcher (Sanday 1979). Spiggle’s (1994) guide was used as a basis for disaggregating

the analysis and interpretation of the qualitative research data into separate operations.

The first step in analysing the data was categorising it. As the discussion guide for the

interviews included five topics, data was labelled and codified along these lines (Lincoln and

Tarvainen (2008)

36

Guba 1985; Weston et al. 2001). As some comments referred to more than just one specific

area, the data was categorised using both deductive and inductive methods (Spiggle 1994).

Closely following the categorisation, the data was then abstracted into fewer, more

general categories to enable comparison of common features (Spiggle 1994). Comparing the

comments of the different interviewees helped to understand how the views of interviewees

from different parts of the trade differed, and what views were shared across the sample.

Comparing the findings of previous interviews also served as a tool for refining the

subsequent interviews to address the most interesting aspects (Lincoln and Guba 1985).

Where applicable, the data was dimensionalised in the relevant categories to empirically

clarify how the perceptions and views of the interviewees from the various professional

backgrounds differed (Bagozzi 1984; Spiggle 1994). For this, a basic codebook was used

(Appendix 7). Because the interviewer and analyser was the same person, and because the

sample size of 13 was too small for valid empirical quantitative analysis, the codebook was

very bare. The codebook did, however, enable detecting where the retailer/supplier side or

the senior/junior interviewee answers differed. MacCoun’s (1998) article on biases was used

to scrutinise the findings. (Weston et al. 2001.)

To gain a more coherent understanding of Champagne marketing, the findings were

then integrated in respect to different interviews and the relevant academic and trade

literature. Identifying where strategies, contexts, and outcomes were linked enabled the

construction of a framework for key findings from the data. (Spiggle 1994.)

In this process, the already collected data was iterated by revising the previous

interpretation of the data – hearing the views of others puts the first view into perspective and

aids induction (Spiggle 1994). The data was also refuted with inherent scepticism toward the

researcher’s own findings and ideas (Strauss and Corbin 1999).

Interpreting the interviews

Whereas data analysis is about manipulating it into more actionable forms, interpretation is

making sense of it through more abstract conceptualisations (Spiggle 1994). When going in

depth in interviewing Champagne trade professionals, years of work experience in the

industry benefited the researcher essentially in interpreting the interviews. For instance,

expressions such as “the Cristal crowd”, or “the yellow label drinkers” have specific

stereotypical connotations in the trade. Further, understanding the dynamics of the trade and

Tarvainen (2008)

37

the orientation of different Champagne houses, channels, and consumers gave more meaning

to some references in the interviews.

Some sales figures or potentially offending views of rivals were asked not to be

quoted, and were consequently not transcribed. Not disclosing some exact figures or

wordings in the few instances that this was asked was not likely to have a large impact on the

validity of the interpretation – the aim, after all, was to understand what those figures or

attitudes mean, not dwelling on exact figures for their own sake. (Spiggle 1994.)

Having explained the methods used in the research process, the results of the 12 interviews

will be presented in Part IV: Findings and analysis. As typical in qualitative research, the

findings are reported together with analysis.

Tarvainen (2008)

38

PART IV: FINDINGS AND ANALYSIS

The general feel from the interviews was that Champagne has done very well as a whole –

the main concern from the producer side was managing demand, rather than creating it. It is

natural that the producers’ views differed from those of the retailers in some area, as they had

the possibility to observe the dynamics of multiple retail channels. Similarly, retailers had the

possibility to observe the brands of multiple producers. Regarding the compatibility of the

findings with the theory of Part I, the behaviour of Champagne consumers seems to have a

better fit with luxury consumer behaviour than wine consumer behaviour; although this is not

to suggest that these areas of study would be by any means mutually exclusive.

The following discusses and analyses the findings of the interviews thematically,

loosely following the structure of the discussion guide. For reasons of research ethics, the

exact interviewees will not be identified; rather, they will be referred to as PSIs (producer

side interviewees) and RSIs (retailer side interviewees).

Marketing Champagne

In marketing Champagne, two issues rose above others in importance: visual branding and

distribution channels. Visual branding, through packaging, often determines the consumer’s

choice of brand at the point of purchase; and the channels themselves actively shape the

consumer’s perception of the brand. Brand awareness is also seen as crucial for consumers

due to the brand’s multiple roles as a source of familiarity, a social class cue, and indicator of

wealth and status through a known price.

There seems to be a fine balance between high brand awareness and the image of

exclusivity. One PSI sees their brand as the “best kept secret in Champagne”, but continues,

“We’d like, though, this secret to be shared with a few more people.”

It is important to note that what drives short-term seasonal sales is very different from

what drives longer-term sales. In the short term, new packaging and press coverage are major

forces driving the lifestyle-driven consumer, and wine press and retail endorsements are

major forces driving the quality-driven consumers.

Over the longer term, the quality of wine becomes a more critical factor – “unless you

have a monster budget” (PSI). In addition to quality, integrity and consistency are seen as

Tarvainen (2008)

39

crucial for the build-up of reputation. Consistency refers especially to the positioning as a

luxury brand, avoiding the brand-damaging discounting and over-exposure in the wrong

channels. A good long-term strategy also targets the future generation of consumers, in

addition to the current drinkers.

Marketing mistakes

Asking the interviewees to reflect on the past with hindsight allowed for identifying some

key mistakes brands have fallen victim to. The main mistake for brands is choosing the

wrong channels, leading to over-exposure in a low-prestige environment and aggressive price

promotions. A PSI crystallises it: “If you say you’re the best, stand by it”. The combination

of poor channel management and uncoordinated pricing is especially detrimental for the

perception of quality. Pushing for higher volumes through supermarket promotions has

implications both on the supply and demand side: “on the supply side you have to stretch the

quality of your product, and on the demand side you have to burn brand equity to build your

market share” (PSI).

Another looming threat is forgetting or alienating the core consumer, often by

excessive preoccupation with the prestige niche products. Rapid price changes and

turnarounds in packaging may create a short-term buzz, but may come on the expense of the

loyal core consumer.

A third threat is complacency. The Champenois have been on the top for so long that

few appreciate the massive educational task there is if consumers are to be educated to trade

up to the higher value-added styles.

The Champagne market

When asking how the Champagne market was, “buoyant” was the word most often used to

describe it. It is also seen as very dependent on the economy, as Champagne is to first wine to

go with the tightening of the belt.

Different rules seem to apply to wine and Champagne markets, as one PSI notes: “We

as a trade have set ourselves apart from wine – the sort of consumer who spends £5 on a

bottle of wine is happy to spend £35 on a bottle of Champagne. It constantly amazes me”.

Consumers are unlikely to compare Champagne to wine in terms of value for money, because

they have been taught that Champagne is the only beverage for certain occasions. The sound

Tarvainen (2008)

40

of cork coming off has an effect on people, and bubbles make it harder for consumers to

evaluate Champagne’s vinosity. Any threat of substitutes is at the very lowest end of the

Champagne market, to the inexpensive own-label Champagnes. It is peculiar that although

Champagne was seen to be at least as much a luxury as a wine, not a single interviewee

suggested that other non-drinkable luxury items, such as shoes or handbags, could be a

substitute for consumers.

The market is also highly stratified between brand-loyal people – consumers drink the

brand rather than the wine. “The idea of the brand is important for the majority of people”,

one RSI notes; “it could all taste the same and people would still be brand-loyal.”

The Champagne market is often viewed as four major price brackets: the value

Champagnes below £25; the grande marque non-vintages at £25–£40; the sparsely populated

specialist range of £40–£70; and the prestige cuvées from £70 upward.

The Champagne consumer

The Champagne market seems to incorporate all of Vigneron and Johnson’s (1999) luxury

consumer types, and bandwagons form the bulk of the market. Especially the RSIs see the

consumption of prestige cuvées as very ostentatious: “Quite frankly, if they burned £100 and

everyone was watching them, the same social function would be fulfilled.” The brands see

their consumers more as more hedonist types who do not have to prove themselves to others

– the PSIs’ perception of the consumers’ direction of self-consciousness is not as strongly

external as the RSIs’ perception. There is also a small market niche of snob and perfectionist

consumers, who may also collect Champagnes.

Inter-personal motives seem to be more important for most consumers, as the visible

external aspects of Champagne brands are easier to understand. The risk is, however, that

consumers with a purely public focus of self-consciousness will not become as emotionally

attached or brand loyal as other consumers: “The Chinese and Japanese don’t really like

Champagne, but they like the idea of being seen drinking Champagne. So the risk in those

markets is that you’re not going to get a regular consumer” (PSI).

The retailer side interviewees observed that consumers seem to follow a certain

pattern of consumption sophistication, trading up from the push-marketing bandwagon