tata corus final report

TRANSCRIPT

Mergers & Acquisitions

Tata’s Corus Acquisition

Nishant Patel

2 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

ACKNOWLEDGEMENT

Preparing a project is an arduous task, but I was fortunate enough to get support

from large number of people to whom I shall always remain grateful and who

helped me directly or indirectly in completion of the project on ―Merger &

Acquisition: Tata‘s Corus Acquisition‖. The project has given me an opportunity

to learn many aspects. I am very grateful to my guide Mr. Vijay Vora, for giving

me this privilege to work under him and for all his support during the entire

duration as well as for his invaluable guidance that helped me to complete my

project.

Nishant Patel

3 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

PREFACE

What are Mergers and Acquisitions? It is defined as a combination of two or

more companies into a single company. A merger can take place either as an

amalgamation or absorption. In other words it is the combination of assets and

liabilities of two firms to form a single business entity. An amalgamation refers to

the fusion of two or more companies which results in the formation of a new

company. This generally happens between firms of equal sizes e.g. Brooke Bond

India Ltd. Merged with Lipton India Ltd. to form Brooke Bond Lipton India Ltd.

Absorption involves the fusion of a small company with a larger company in which

the former loses its identity, this is also called as an acquisition, e.g. the merger

between HDFC Bank and Times Bank after which the latter ceased to exist while

the former continued. Such corporate combinations can be accomplished in

broadly three different ways:

Pooling of interests: This is generally accomplished by a common stock swap at a

specified ratio. For example when M&I Bank merged with National City

Bancorporation, the common stock of the two companies were swapped at a ratio

between .655 and .5363 shares of M&I for every share of National City. Such

mergers are only allowed if they meet certain legal requirements.

Purchase acquisition: This involves one company (the acquirer) purchasing the

common stock or assets of the target company. The acquiring company offers to

purchase the target company‘s stock at a given price in cash, securities or both.

This offer is called a tender offer because the acquiring company offers to pay a

certain price if the target‘s shareholders will surrender or tender their shares of

stock. Generally, this offer is higher than the stock‘s current price to encourage the

4 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

shareholders to tender their stocks. The difference between the share price and the

tender offer is called the acquisition premium.

Consolidation: The existing companies are dissolved and a new company is

formed to combine the assets of the existing companies. Both companies stocks are

surrendered and new stock is issued in its place. E.g. both Daimler-Benz and

Chrysler ceased to exist when the two firms merged and a new firm

DaimlerChrysler was created. Some other related terms are horizontal, vertical and

conglomerate mergers. Horizontal mergers happen when a company merges with

another company which is a direct competitor in the same product lines and

markets. A vertical merger occurs when the company merges with the suppliers or

customers. Conglomerate mergers occur when the companies combined have no

relationship to one another.

Why do mergers occur? All mergers and acquisitions have one common goal: to

create synergy, that makes the value of the combined companies greater than the

sum of the two parts. The success of a merger or acquisition depends on whether

this synergy has been achieved or not. Synergy takes the form of revenue

enhancement and cost savings in the following ways:

Staff Reductions – Mergers are generally followed by staff reduction from

various departments as well as the top management of the acquired firm which

helps in reducing costs.

Economies of scale – A bigger company placing larger orders can save more on

costs as it has greater power for negotiation.

Improved market reach and visibility- Companies acquire other companies to

enter new markets and increase their revenues. A merger may also expand the two

5 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

companies marketing and distribution, giving them new sales opportunities. This is

the prime driving force behind the Bharti MTN deal, as the competition is

intensifying in India and the ARPU is falling, Airtel is looking for a synergy with

MTN which will provide it access to a new market, bring down operational cost

and help in raising the ARPU.

6 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

EXECUTIVE SUMMARY

On 20 October 2006 the board of directors of Anglo-Dutch steelmaker Corus

accepted a $7.6 billion takeover bid from Tata Steel, the Indian steel company. The

following months saw a lot of negotiations from both sides of the deal. Tata Steel's

bid to acquire Corus Group was challenged by CSN, the Brazilian steel maker.

Finally, on January 30, 2007, Tata Steel purchased a 100% stake in the Corus

Group at 608 pence per share in an all cash deal, cumulatively valued at $12.04

Billion. The deal was the largest Indian takeover of a foreign company and made

Tata Steel the world's fifth-largest steel group.

To finance the acquisition, Tata Steel put together a package consisting of many

securities, including a new security entitled Convertible Alternative Reference

Security. Market watchers were divided not only on Tata Steel‘s ability to create

value through the acquisition because of the high price paid but also on the likely

outcome of the issue of the chosen securities.

7 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

INDEX

S. No. Chapters Page No.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

8 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

MERGERS & ACQUISITIONS FOR DUBIOUS PURPOSE?

Companies originating from emerging economies have been increasingly pursuing

international acquisitions. This is to be expected and has been predicted for a long

time. Companies need certain ownership-specific advantages to compete

successfully outside their home markets. Such advantages are likely to increase as

emerging economies reach higher levels of development. This internationalization

trend by emerging economy firms has been driven by various factors such as, the

liberalization of their domestic economies, globalization of their industries,

intensity of competition, managerial capabilities, and access to capital markets.

The share of emerging economies in global cross-border acquisitions rose from 4%

in 1987 to 13% in 2005 to 20% in 2008. Furthermore, in the last decade, the scale

of these foreign acquisitions has increased significantly. Tata Steel from India

acquired Corus Steel for $13 billion; Hindalco Industries purchased Novelis for

$5.7 billion. Chinese oil company CNPC acquired PetroKazakhastan for $4.2

billion; Lenovo Group bought IBM's personal computer business for $1.8 billion.

Mexican building materials company CEMEX acquired the British RMC Group

for $5.8 billion and the Australian Rinker Group for $14.2 billion. The Brazilin

mining company Vale acquired Inco for $18.9 billion. These mega-deals involving

acquisitions by emerging economy firms have attracted much attention from the

business press. In the developed countries, some welcome this as a positive trend: a

new source of capital and knowledge; this is globalization at its best and benefits

everybody. Others regard these acquisitions as a threatening trend; the world

becoming 'flat' is leading to new competition from unexpected places. Some have

even called for protectionist intervention. Not surprisingly, in the emerging

economies, the business press has been unequivocally positive, even euphoric

about these foreign acquisitions. There is much talk about emerging giants and new

9 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

powerhouses. Some see this as the revenge of the former colonies against the

imperialist powers. The Indian newspaper The Economic Times exclaimed "Corus,

the erstwhile British Steel and one of the icons of Her Majesty's Empire will now

fly the [Indian] Tricolor." But, what often is under-emphasized or assumed away in

this discussion by the popular press is to what extent the acquiring firms create

value for their shareholders. This issue might be less critical if the acquisition is

carried out by a state owned enterprise or a sovereign wealth fund pursuing

national interest. But many of the acquiring firms are private, publicly listed firms

that have a fiduciary responsibility to their shareholders. This paper addresses the

question whether such publicly listed companies from emerging economies

create shareholder value through foreign acquisitions, and in particular, through

large Acquisitions. The popular business press usually views foreign acquisitions

by emerging economy firms very positively. The stock markets have often reacted

negatively to the acquisitions. The management always claims that the acquisition

is in the long term strategic interests of the firm. This article attempts to shed light

on these conflicting positions: short term versus long term, and financial versus

strategic logic.

On 31 January 2007, Tata Steel increased its offer price to acquire Corus Steel to

608p a share, topping the 603p offer from rival bidder, the Brazilian company

CSN, thus clinching the deal. The Managing Director of Tata Steel, B.

Muthuraman, cast his firm's victory in broad light as a milestone for Indian

business and the country's economy. This upbeat mood was echoed by India's

finance minister, Palaniappan Chidambaram, who said the successful bid reflected

the new-found confidence of Indian industry. The shareholders of Tata Steel were

not nearly so enthused, and penalized the stock by 11% the next day. Ratan Tata,

the chairman of the Tata group, responded "Quite frankly I do feel [the stock

10 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

market] is taking a short-term and harsh view. In the future somebody will look

back and say we did the right thing." Analysts argued that Tata was overpaying for

the acquisition, citing, for example, that the price was 9 times Corus's (EBITDA)

earnings that dwarfed the 6 times that Mittal Steel recently paid to acquire Arcelor.

Mr. Muthuraman accepted that the deal "may look expensive" but was in fact in

the strategic interests of both companies allowing Tata Steel access to Corus's

markets and Corus the access to cheap raw materials and low costs of steel making.

INDUSTRY OUTLOOK

Worldwide demand for steel products grew 11.5% in 2006 to 1,147m ton, led by

strong demand growth in most regions. However, production in most regions

except China could not keep pace 1 In India currency units are quoted in crores

rather than millions; INR 1 crore = INR 10 million with demand growth. United

States of America (USA) was the largest importer in 2006. Total import of steel

products by the US grew 42% to 40.4m ton in 2006. Chinese demand for steel was

expected to grow 5.9% in 2007 and 6.1% in 2008 on a larger base. This meant

additional steel consumption of 40-60m ton in absolute terms. The former USSR

and the Middle East countries were also expected to post demand growth of 7-8%.

Apparent demand for steel in China, Europe and CIS region had been stronger than

the projections of IISI. Except North America, all other economies of the world

had been reporting strong growth in demand for steel, driven by construction

activity and consumption of capital goods, automobiles and consumer

durables. The annual rate of growth in finished steel consumption in India

accelerated from 3.4% in 2002 to 10.8% in 2006. However, India continued to

have a low per capita consumption of 40kg, far below the global average of 185kg

(China: 240kg; EU: 400kg; Japan: 600kg; and Korea: 1,000kg). Analysts believed

11 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

that consumption in India would accelerate further to support the envisaged strong

GDP growth, on the back of ongoing US$320b infrastructure investment planned

for the 11th Five Year Plan (2007-2012). Strong demand had been driving up steel

prices since the beginning of 2007. Rising international prices drove exports from

China, which topped 7.2m ton in April 2007 despite a number of steps taken by the

Chinese authorities to curb exports to avoid trade friction with partner countries.

Along with strong prices in the world market, Chinese exporters rushed to ship as

much material as they could before the deadlines of export disincentives were

announced. However, Chinese exports started showing signs of weakening. Export

volumes declined 14% in May 2007 and were expected to decline further in the

coming months. Steel prices in China started weakening due to declining exports–

landed cost of Chinese material in Europe and Middle East was higher than the

prices offered by Russia and Ukraine. Also, industrial and construction activities in

Europe and Middle East were becoming seasonal. Analysts believed that steel

prices would settle a little under early 2007 levels before picking up once again

towards the end of August or beginning of September, 2007. Prices of all raw

materials and logistics costs had moved up during 2003-07 due to strong growth

in steel production and a decade of under-investment. Prices of iron ore rose three

hundred percent during the same time period. Coking coal prices too moved up

manifold and had eased during 2005-07. Rising costs and high level of

consolidation among miners were expected to continue to keep the prices of raw

materials high. Therefore, the structural shift in the cost curve of the industry was

expected to support steel prices at higher levels.

12 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

STEEL INDUSTRY BACKGROUND

Steel was an alloy of iron and carbon containing less than 2 per cent carbon and

1per cent manganese and small amounts of silicon, phosphorus, sulphur and

oxygen. Steel was the most important engineering and construction material in the

world. It was used in every aspect of our lives, from automotive manufacture to

construction products, from steel toecaps for protective footwear to refrigerators

and washing machines and from cargo ships to the finest scalpel for hospital

surgery. Most steel was made via one of two basic routes:

§ Integrated (blast furnace and basic oxygen furnace).

§ Electric arc furnace (EAF).

The integrated route used raw materials (that is, iron ore, limestone and coke) and

scrap to create steel. The EAF method used scrap as its principal input.

The EAF method was much easier and faster since it only required scrap steel.

Recycled steel was introduced into a furnace and re-melted along with some other

additions to produce the end product.

Steel could be produced by other methods such as open hearth. However, the

amount of steel produced by these methods decreased every year. Of the steel

produced in 2005, 65.4per cent was produced via the integrated route, 31.7percent

via EAF and 2.9 percent via the open hearth and other methods. At a steel mill, the

crude steel production process turned molten steel into ingots, blooms, billets or

slabs. These were called semi-finished products. Semi-finished products were solid

blocks of steel, usually with a square or rectangular cross section. A flat steel

product was typically made by rolling steel through sets of rollers to produce the

final thickness. There were two types of flat steel products:

§ Plate products. Varied in thickness from 10 mm to 200 mm. Plate products were

13 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

used for ship building, construction, large diameter welded pipes and boiler

applications.

§ Strip products. Could be hot or cold rolled and vary in thickness from 1 mm to

10 mm. Thin flat products were used in automotive body panels, domestic white

goods (for example, refrigerators and washing machines), steel (or tin) cans, and a

number of other products from office furniture to heart pacemakers. A long

product was a rod, a bar or a section. Typical rod products were the reinforcing

rods used in concrete, engineering products, gears, tools etc. Sections were the

large rolled steel joists (RSJ) that were used in building projects. Wire-drawn

products and seamless pipes were also part of the long products group.

Supply of raw materials was a key issue for the world steel industry. IISI managed

projects which looked at the availability of raw materials such as iron ore, coking

coal, freight and scrap. Scrap iron was mainly used in electric arc furnace

steelmaking. Apart from scrap arising in the making and using of steel, obsolete

scrap from demolished structures and end-of life vehicles and machinery was

recycled to make new steel. About 500 million tons of scrap was melted each year.

Iron ore and coking coal were used mainly in the blast furnace process of iron

making. For this process, coking coal was turned into coke, an almost pure form of

carbon which was used as the main fuel and reductant in a blast furnace. Typically,

it took 1.5 tons of iron ore and about 450kg of coke to produce a ton of pig iron,

the raw iron that came out of a blast furnace. Some of the coke could be replaced

by injecting pulverized coal into the blast furnace. Iron was a common mineral on

the earth‘s surface. Most iron ore was extracted in opencast mines in Australia and

Brazil, carried to dedicated ports by rail, and then shipped to steel plants in Asia

and Europe. Iron ore and coking coal were primarily shipped in capesize vessels,

huge bulk carriers that could hold a cargo of 140,000 ton or more. Sea freight was

14 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

an area of major concern for steelmakers, as the high demand for raw materials

was causing backlogs at ports, with vessels delayed in queues.

Since the World War II, the steel industry had experienced three distinct phases-

growth (1950-73), stagnation (1974-2001) and boom (2002-2006)3. The demand

for steel grew at an annual rate of 5.8per cent during 1950-73 as the industrializing

nations were building their civil infrastructure. The oil shocks of 1973 through

1979 slowed consumption in the second phase. The production of crude steel grew

at 0.6per cent p.a. over the entire period. Steel prices declined by 2-3 per cent p.a.

During 1999-2001 the industry‘s overcapacity hovered near 25per cent globally.

Only a few companies were able to sustain.

Since 2002 the annual steel production had grown at 7-8per cent driven almost

entirely by the double digit growth in China. The huge demand from China had

caused a commensurate leap in steel prices. The industry had experienced a drop in

the over capacity from 23per cent in 2001 to about 17per cent from 2003-2005. But

the demand from China had also witnessed a structural change. From 2002-2004

China‘s capacity for producing crude steel increased on average by 55per cent. By

2005 China became a net exporter of steel. In the first half of 2006 China overtook

Japan, Russia and the EU 25 to become the world‘s largest steel exporting country.

In June 2006 that winning companies in the steel industry would have somewhere

between 150m-200m tons of annual capacity by 2015 and that scale was crucial in

the pursuit of value. Shanghai Baosteel, which, although founded in 1998, had

already become the world‘s fifth largest steel maker producing 22.7 m tons in

2005. The potential acquisition of Corus by Tata Steel would create a new entity

with a production volume close to Baosteel‘s.

15 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

COMPETITION: US, EUROPE & EMERGING MARKETS

In the past, industry consolidation contributed to reduced cyclicality. The top 10

steel makers represented about 28per cent of global production. Besides Arcelor

Mittal, four of the top 10 were in Asia, three in Europe and two in the U.S. In

addition to China‘s plan for consolidation many of the leading steel producers had

ambitious growth plans that would entail further consolidation. Lakshmi Mittal, the

CEO of Arcelor Mittal stated June 2006 that winning companies in the steel

industry would have somewhere between 150m-200m tons of annual capacity by

2015 and that scale was crucial in the pursuit of value. Shanghai Baosteel, which,

although founded in 1998, had already become the world‘s fifth largest steel maker

producing 22.7 m tons in 2005. The potential acquisition of Corus by Tata Steel

would create a new entity with a production volume close to Baosteel‘s.

16 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

COMPANY BACKGROUNDS

Tata Steel, formerly known as TISCO (Tata Iron and Steel Company Limited),

was the world's 56th largest and India's 2nd largest steel company with an annual

crude steel capacity of 3.8 million tonnes. Based in Jamshedpur, India, it was part

of the Tata group of companies. Post Corus merger, Tata Steel was India's second-

largest and second-most profitable company in private sector with consolidated

revenues of Rs 1, 32,110 crore1 and net profit of over Rs 12,350 crore during the

year ended March 31, 2008. The company was also recognized as the world's best

steel producer by World Steel Dynamics in 2005. Tata Steel was one of the world‘s

lowest cost producers of steel because of its high level of vertical integration and

process improvisation, excellent product mix and good perception regarding

product quality. On the flip side, Tata steel imported about 35% of its total coking

coal requirement, leading to some dependence on coking coal contract price

movements. With a low cost structure and strong balance sheet, the company could

foray into the Asian markets through acquisitions and brown field and Greenfield

expansions. The company was listed on Bombay Stock Exchange and National

Stock Exchange; and, as of 2007, employed about 82,700 people.

Corus was formed from the merger of Koninklijke Hoogovens N.V. with British

Steel Plc on 6 October 1999. It had major integrated steel plants at Port Talbot,

South Wales; Scunthorpe, North Lincolnshire; Teesside, Cleveland (all in the U.K)

and Ijmuiden in the Netherlands. It also had rolling mills in England. Group

turnover for the year to December 31, 2005 was £10.142 billion. Profits were £580

million before tax and £451 million after tax.

17 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

RATIONALE FOR ACQUISITION

There were a lot of apparent synergies between Tata Steel, a low cost steel

producer in a fast developing region of the world and Corus, a high value product

manufacturer. Some of the prominent synergies that could arise from the deal were

as follows:

• Tata was one of the lowest cost steel producers in the world and had self

sufficiency in raw material. Corus was fighting to keep its productions costs under

control and was on the lookout for sources of iron ore.

• Tata had a strong retail and distribution network in India and South East

Asia. This would give the European manufacturer an inroad into the emerging

Asian markets. Tata was a major supplier to the Indian auto industry and the

demand for value added steel products was growing in this market. Hence there

would be a powerful combination of high quality, developed and low cost, high

growth markets.

• There would be technology transfer and cross-fertilization of R&D

capabilities between the two companies that specialized in different areas of the

value chain.

• There was a strong culture fit between the two organizations both of which

highly emphasized on continuous improvement and ethics.

18 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

THE COUNTERBID BY CSN

As expected by observers, CSN announced on November 11, 2006 that it had made

an informal bid approach to Corus, setting the stage for a bidding war and throwing

Tata Steel's agreed takeover into jeopardy. CSN's offer of 475 pence per share for

Corus, which would value the firm at $5.3 billion pounds, including debt, topped

Tata's bid of 455 pence. Both companies had a significant presence in the

manufacture of tinplate in Europe. Interestingly, in 2002, Corus had made an offer

for CSN, but it was shelved over debt concerns. Companhia Siderúrgica Nacional

was founded on April 9, 1941, becoming operational on October 1, 1946. As the

first integrated flat steel producer in Brazil, CSN played a historical role in the

country's industrialization process. Steel from its mills permitted the implantation

of the nation's first domestic industries, the nucleus of the modern day Brazilian

industrial park. Privatized in 1993, with over six decades in the market, the

company continued to make history. A listed public company, with shares traded

on the São Paulo and New York (NYSE) stock exchanges, CSN was one of the

largest and most competitive integrated steel companies in Latin America. With an

annual production capacity of 5.8 million tons and around eight thousand

employees, CSN was focused on steel production, mining and infrastructure. The

company had one of the most comprehensive lines of high added value flat steel on

offer throughout the continent. The acquisition of the assets of Heartland Steel and

the subsequent incorporation of CSN LLC in the United States in 2001 was the

first step towards the internationalization of the company. The company‘s assets

consisted of an integrated steel mill, five industrial units, two of them abroad (the

United States and Portugal), iron ore, limestone and dolomite mines, a major flat

steel distributor, port terminals, as well as shares in railroads and two hydroelectric

plants. Even as Tata Steel was mulling over its next move in the race for Corus

19 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

Group, CSN, along with bankers and brokers allied to it, scaled up its holding in

the Corus group to a little less than 23 per cent. The combined holding of CSN and

its allies stood at 19.5 per cent on November 25. The increased holding came from

UBS AG, which emerged as the largest shareholder in Corus with 10.23 per cent

stake. UBS was acting as a joint broker to CSN for this deal. CSN's other financial

advisors Barclays Capital and Goldman Sachs, held 4.7 per cent and 4.01 per cent

in Corus respectively. Further, the Brazilian steelmaker held a 3.8 per cent stake in

Corus. The combined holding was inching towards the crucial 25 per cent that

could block Tata Steel's offer at the extraordinary general meeting if such a

situation were to arise. According to the rules, a resolution pertaining to the bid

would have to garner support from 50 per cent of shareholders and 75 per cent of

shares at the EGM, which was adjourned to December 20. Corus had around

158,000 registered shareholders. Institutional investors accounted for around 90

per cent of the total shareholders. The remaining 10 per cent was held by

individual investors. As of November, the major shareholders in the Corus group

apart from the ones connected to Corus were Standard Life Investments at 7.81 per

cent, Legal & General Investment Management at 3.82 per cent, Lehman Brothers

at 3.45 per cent and Capital Group at 3.05 per cent. The UK takeover regulator had

set a deadline of January 30 for the two bidders to make their final offers. The

commission had set a provisional deadline of February 5 for ruling on the proposed

transaction of CSN. As on December 7, Deutsche Bank, the financial advisor to

Tata Steel, had 4,786,061 Corus shares. The chronology of bidding events is

presented in Exhibit 21 and a summary of the UK takeover code is presented in

Exhibit 22. Exhibit 23 presents a comparison of the two bidders.

20 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

MARKET REACTION

Tata Steel share prices fell upon announcement of the acquisition and continued to

slide during the next two months. After a battering of two-and-a-half months (in

December), shares of Tata Steel staged a partial recovery with a gain of over 5

percent with some market players speculating that the company might withdraw its

bid to acquire Anglo-Dutch steelmaker Corus. Tata Steel shares had lost about 20

per cent ever since the reports first poured early in October that it was planning to

acquire Corus, as it was felt that the costly takeover would have an adverse impact

in the company's balance sheet. The brokers said the deal might have significant

long-term synergies, but market players were worried about the adverse impact in

the short term. Tata Steel's share price closed 5.4 per cent higher at Rs 459.25, after

hitting an intra-day high of Rs 461.45 at the Bombay Stock Exchange. However,

the stock was still 14 per cent below the level it was trading at in the beginning of

October. Interestingly, the CSN stock price went up when it announced its bid.

21 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

TATA STEEL & CORUS

Tata Steel belongs to the Tata group, which is the largest business group in India

with presence in a wide variety of industries ranging from information technology

to chemicals to hotels. After the initial announcement in October 2006, Tata Steel

and the Brazilian firm CSN engaged in a bidding war to acquire Corus Steel, an

Anglo-Dutch company previously known as British Steel. The stock market did

not move much in reaction to the initial announcement. On 31 January 2007 Tata

Steel increased the offer price and clinched the acquisition. The stock price of Tata

Steel immediately plunged by 11%. The top management of Tata Steel responded

by saying that the stock market reaction was short sighted, and that the acquisition

would create shareholder value in the long term. The stock price, which was at Rs.

459 the day before the increased offer, quickly recovered to Rs. 471 on 16 April

2007. In apparent vindication of top management‘s position, the stock price

zoomed up to Rs. 935 on 2 January 2008, far exceeding the gains in the Sensex

index. Managing Director Muthuraman said that Corus brought to Tata Steel

capacity of million tons per year at a cost of about $710 per ton, which is little

more than half the cost of Greenfield capacity of $1200 to $1300 per ton. It gave

Tata Steel access to the developed and mature markets in Europe where product

quality and service is important. Corus also brought high R&D capability. He also

forecast up to $350 million in savings after about three years from synergies in

procuring materials, in marketing and in shared services. Steel prices would rise

driven by demand from explosive growth in the biggest markets in the developing

world: India and China. Finally, he also believed there was a tremendous amount

of cultural fit between Tata Steel and Corus. For the deal to work, Tata had to

improve the efficiency of Corus, whose profit margins at 7% were a quarter of

those of Tata Steel. Ratan Tata stated ―I think our plan would be to try to make the

22 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

UK operations more profitable.‖17 Maybe the strategic logic of the acquisition was

right after all, and it had taken the stock market about 15 months to fully appreciate

the complexities and subtleties involved in the acquisition. Or, more likely the

strategic logic of the acquisition was flawed, and some other confounding event

explains the rise in the stock price. Tata Steel's cost of production at around

$450/ton is among the lowest in the world. Even in 2009 when the global average

cost had reached about $700-750/ton, Tata Steel managed to control its costs to

about $500/ton. But this advantage is not transferable to Corus. Captive raw

materials are the primary source of Tata Steel‘s competitive advantage. Tata Steel

meets 100% of its iron ore requirements and 50% of its coking coal requirement

through backward integration.Whereas Corus is completely exposed to raw

material price volatility due to lack of any significant backward integration. One

important synergy stated at the time of the acquisition was the leveraging of low

cost slabs from India that could be used by Corus to produce various finished

products. But in 2006 Tata Steel did not have spare slab capacity. Tata Steel also

benefits from low labor cost and tight capacity in its primary market of India.

Corus, on the other hand, has high labor costs, strong unions and excess capacity.

Tata Steel paid about $710 per ton of capacity, which is low compared to

Greenfield cost of $1200-1300 per ton. This is a false comparison since Corus was

one of the highest cost producers in Europe and there is excess steel capacity in the

European markets. When Tata Steel acquired two smaller Asian steel companies,

NatSteel and Millennium Steel in 204 and 2005, it paid a price of $374 and $333

per ton, respectively. In 2010, Anand Rathi Financial Services values Corus

capacity at around US$360-400/ton, which implies that Corus is worth little more

than half what Tata Steel paid for it three years ago.18 Anand Rathi projects that in

2011, Corus would comprise 65% of Tata Steel's consolidated revenues but only

about 23% of EBITDA earnings. Even based on expectations for 2012, Anand

23 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

Rathi does not expect Corus‘ return on capital employed to exceed 3%, which is

clearly low even compared to global peers. Tata Steel paid 9 times EBITDA to

acquire Corus. In comparison, Mittal Steel acquired Arcelor in 2006 for an

EBITDA multiple of 6. This was in spite of the fact that Corus was less profitable

and less efficient compared to Arcelor. Also, the entire amount was paid in cash by

Tata Steel as opposed to a combination of cash and share swap in case of the

Arcelor deal. Tata Steel probably overpaid for Corus. In 2009 Corus began

decommissioning its Teesside Cast Products plant in UK, thus confirming that the

Corus capacity was not that valuable. Angry unions threatened strike action against

Tata Steel-Corus because this capacity reduction would lead to laying off 1,600

workers, with a possible 8,000 more job losses in the local supply chain. A

company statement said the Teesside plant was a major drag on profitability,

denting it with $177 million losses during the September 2009 quarter, due to

restructuring costs. It can be argued that the acquisition involved minimal

synergies and that Tata Steel overpaid for Corus. The rise in the stock price of Tata

Steel is driven more by the steel cycle rather than by the acquisition. Steel prices

(represented by FOB price of hot rolled steel) in the international market increased

from an average of $564/ton in 2007 to $714/ton in 2008. However, as global steel

demand cracked in the second half of 2008, Steel prices in the international market

started declining significantly. Prices declined from the highs in 2008 to $380 in

June 2009. Steel prices have recovered and in 2010 are hovering at $575/ton.19 In

parallel to the steel cycle, the stock price of Tata Steel moved from Rs. 410 on 31

January 2007 (the day the acquisition was clinched), to a peak of Rs. 922 on 21

May 2008, to a trough of Rs. 151 on 28 November 2008, to its recent price of Rs.

629 on 22 March 2010. The stock price of Tata Steel has been extremely volatile

driven by the steel cycle and the economic cycle. The Corus acquisition is

equivalent to the shareholders of Tata Steel placing a highly leveraged (of the $13

24 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

billon acquisition price, $9 billion came from increased debt) bet on steel prices. If

that is what the shareholders wanted, they could easily have done it on their own in

the stock and futures markets, without an expensive acquisition.

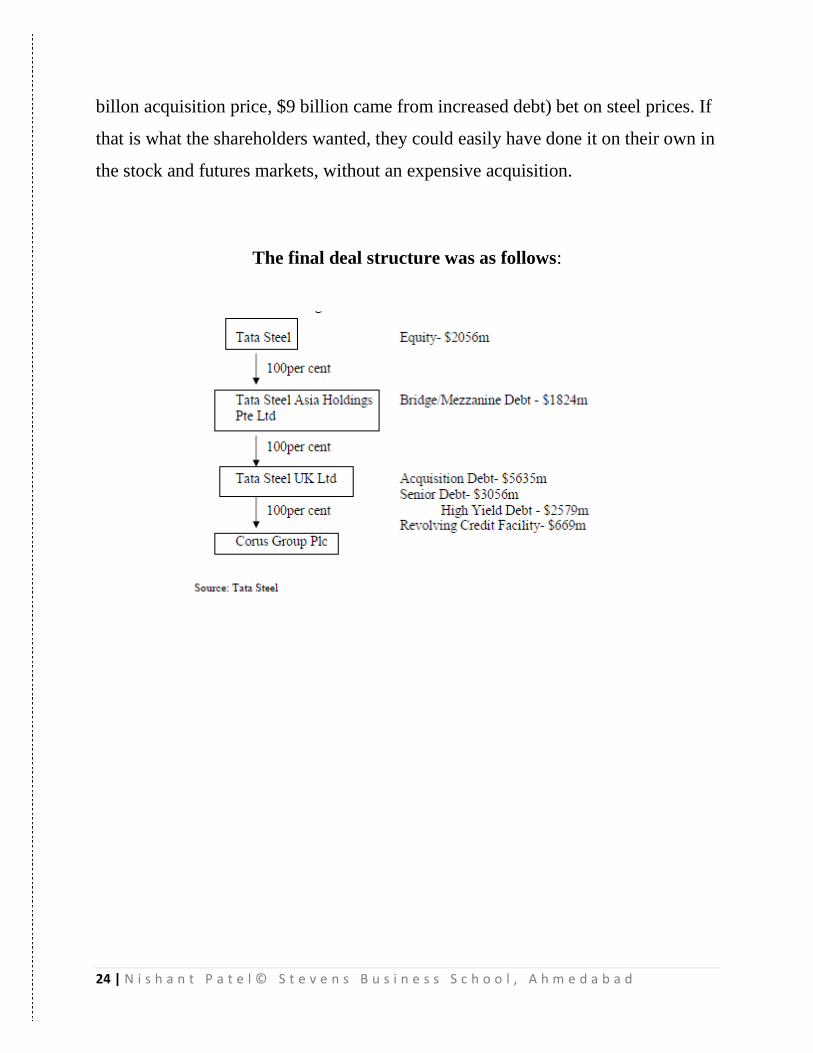

The final deal structure was as follows:

25 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

• $3.5 - $3.8 b infusion from Tata Steel ($2b as its equity contribution, $1-.5-1.8 b

through a bridge loan

• $5.6b through a LBO ($3.05b through senior term loan, $2.6 b through high yield loan)

A new board consisting of Ratan N Tata, chairman of Tata Steel, Jim Leng of Corus group,

Muthuraman, Managing Director of Tata Steel, Ishaat Hussain and Arun Gandhi, directors of

Tata Sons was formulated to develop and execute the integration and further growth plans.

26 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

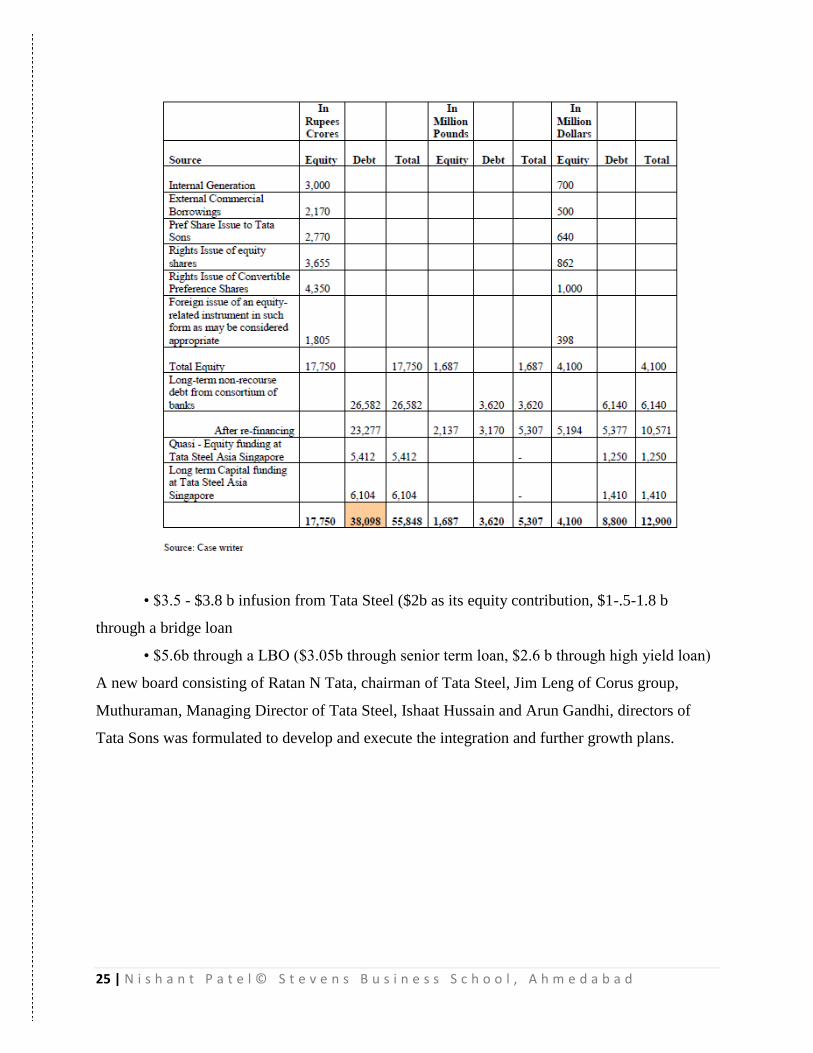

FUNDING THE CORUS ACQUISITION

Financing India's largest leveraged buyout comprised of a $3.88 billion equity

contribution from Tata Steel, a fully underwritten non-recourse debt package of

$5.63 billion, and a revolving credit facility of $669 million. As per the acquisition

plan a special purpose vehicle, a wholly owned subsidiary, called Tata Steel UK

would be set up by Tata Steel. The acquisition was proposed to be effected under

section 425 of the English Companies Act 1985 and upon approval from the Corus

shareholders. Tata Steel UK would offer a price of 455 pence per Corus share

valuing Corus at £4.3b ($8.04b). This price represented a multiple of 7.9 times the

EBITDA of Corus from continuing operations for the twelve months to July 1,

2006. The acquisition was to be structured as a 100 percent leveraged buy-out

funded through cash resources and loans raised by Tata Steel and the SPV. Under

the plan, Tata Steel UK would arrange a loan of £1.6 b ($3056m), a revolving

credit facility and a bridge loan and the rest would come from Tata Steel (to the

SPV). Tata Steel appointed Credit Suisse, ABN AMRO and Deutsche Bank to

arrange bridge financing. Of the £3.3 billion of financing being raised at the SPV

level, Credit Suisse would provide 45% and ABN AMRO and Deutsche 27.5%

each. The $1.8 billion bridge debt being raised at the Tata Steel level in India

would be shared between Standard Chartered and ABN AMRO. Once the

acquisition was completed, at the Board Meeting held on April 17, 2007, the Board

approved the following sources of funding Tata Steel's investment of USD 4.1

billion (about Rs.177.5b) in its wholly-owned subsidiary Tata Steel Asia Holdings

(Singapore) Ltd. (which would in turn invest the same in Tata Steel UK which

acquired Corus plc. U. K).

27 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

1) A Rights Issue of equity shares to the shareholders in the ratio of 1:5 at a

price of Rs.300 per share (Face Value of Rs.10 each). This would involve

issue of equity shares at a face value of Rs.1220m and provide Rs.36.55 b

(USD 862 million).

2) A simultaneous but un-linked Rights Issue of Convertible Preference Shares

in the ratio of 1:7 having a coupon rate of 2% with conversion into equity

shares after two years at a price in the range of Rs.500 to Rs.600 per share as

may be determined at the time of the issue. This issue would provide a total

amount of about Rs.43.50b (about $1000 million).

3) A foreign issue of an equity-related instrument up to an amount of up to

$500 million (about Rs. 21b including the premium) in such form as may be

considered appropriate. This issue would be made on an ex-Rights basis and

on terms as may be determined at the time of the issue subject to approval of

the shareholders. The post-tax cost of this total financing package on

completion was expected to be around 4.3% per annum. The long term

financing pattern for the net acquisition consideration of Corus would be

$12.9 billion and Tata Steel UK would be funded in the long term from the

following sources:

As part of Tata Steel's contribution, the Company had already invested the

following as part of its equity commitment:

a) Internal Generation - Rs.30b (USD 700 million).

b) External Commercial Borrowings - Rs.21.70b (USD 500 million).

c) Funds from the Preferential Issues of equity shares to Tata Sons Ltd. comprising

equity shares of the face value of Rs.560m at an average price of Rs.499.7 per

share, which provided a total amount of Rs.27.70b (USD 640 million).

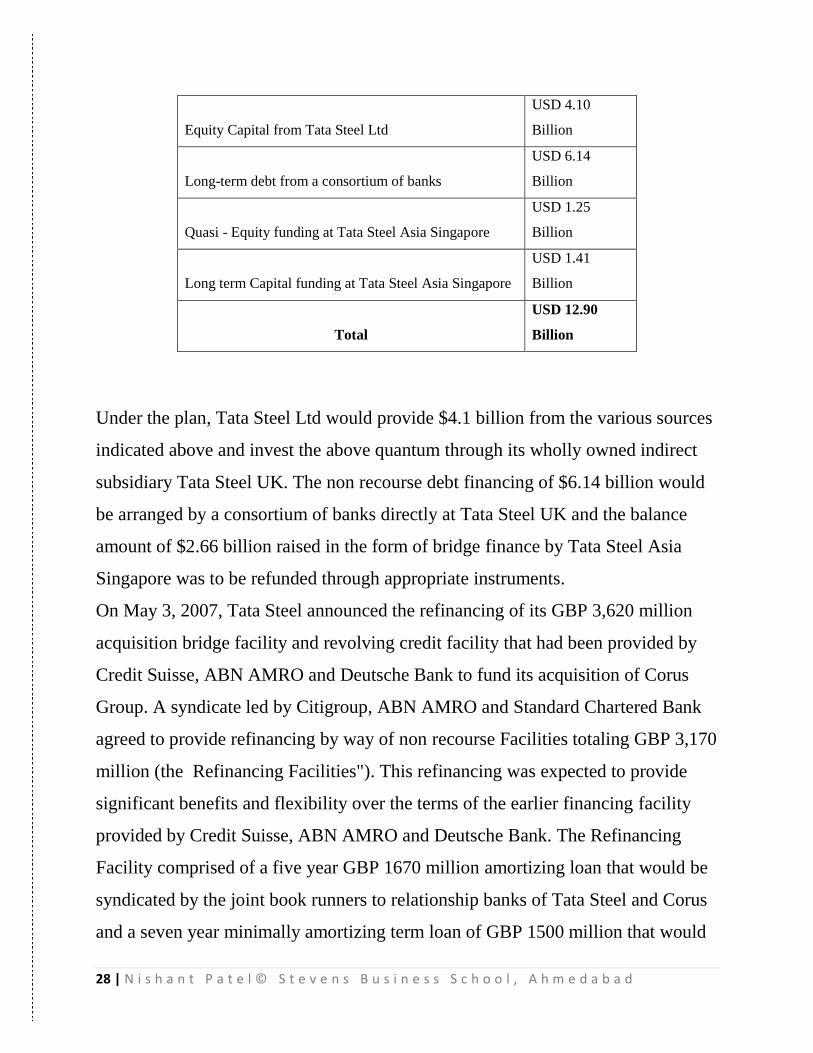

28 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

Equity Capital from Tata Steel Ltd

USD 4.10

Billion

Long-term debt from a consortium of banks

USD 6.14

Billion

Quasi - Equity funding at Tata Steel Asia Singapore

USD 1.25

Billion

Long term Capital funding at Tata Steel Asia Singapore

USD 1.41

Billion

Total

USD 12.90

Billion

Under the plan, Tata Steel Ltd would provide $4.1 billion from the various sources

indicated above and invest the above quantum through its wholly owned indirect

subsidiary Tata Steel UK. The non recourse debt financing of $6.14 billion would

be arranged by a consortium of banks directly at Tata Steel UK and the balance

amount of $2.66 billion raised in the form of bridge finance by Tata Steel Asia

Singapore was to be refunded through appropriate instruments.

On May 3, 2007, Tata Steel announced the refinancing of its GBP 3,620 million

acquisition bridge facility and revolving credit facility that had been provided by

Credit Suisse, ABN AMRO and Deutsche Bank to fund its acquisition of Corus

Group. A syndicate led by Citigroup, ABN AMRO and Standard Chartered Bank

agreed to provide refinancing by way of non recourse Facilities totaling GBP 3,170

million (the Refinancing Facilities"). This refinancing was expected to provide

significant benefits and flexibility over the terms of the earlier financing facility

provided by Credit Suisse, ABN AMRO and Deutsche Bank. The Refinancing

Facility comprised of a five year GBP 1670 million amortizing loan that would be

syndicated by the joint book runners to relationship banks of Tata Steel and Corus

and a seven year minimally amortizing term loan of GBP 1500 million that would

29 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

be syndicated to institutional investors and banks in the US, Europe and Asia. The

balance amount of the acquisition bridge was to be repaid by an additional equity

contribution by Tata Steel / Tata Steel Asia. At the Board Meeting of the Company

held on July 30, 2007, it was decided to increase the contribution from Tata

Steel/Tata Steel Asia Holdings Pte Ltd. from U.S. $ 6.7 billion to about U.S $ 7.4

billion. This increase would essentially be covered by increasing the amount of the

Rights Issue of 2% Convertible Preference Shares (announced earlier) from Rs

43.5b up to about Rs 60b. On August 6, 2007, as part of the long term financing

plan, Tata Steel announced that it had priced the issue of Foreign Currency

Convertible Alternative Reference Securities (―CARS™‖) aggregating to US$

725m with a green shoe option of US$150m. The CARS would be listed on SGX

(Singapore Exchange). The CARS would be convertible into either Qualifying

Securities (which may be in the form of depositary receipts with restricted rights of

withdrawal representing underlying ordinary shares with differential rights as to

voting) or ordinary shares. The CARS would be convertible at an initial conversion

price of Rs.876.6225 per share, which was at a premium of 35% to the Company's

closing share price on the National Stock Exchange of India Limited as on August

06, 2007. The CARS carried a 1% coupon and the effective YTM was 5.15%. The

outstanding CARS, if any, at maturity would be redeemable at a premium of

23.3419% of the principal amount. Citigroup acted as the sole global coordinator

and book-runner to the offering with ABN AMRO Rothschild and Standard

Chartered Bank acting as joint book runners. The details of the rights issue of

shares and cumulative convertible preference shares and CARS are provided in

Chart 6. The company's overall borrowings during 2006-07 would increase by over

600 per cent from Rs 33.77 b to Rs 249.26 b, principally in connection with its

acquisition of Corus and expenditure in connection with other

cquisitions/expansion. The rights issue would result in an increase in the

30 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

company's equity base of 20 per cent to 35 per cent after conversion of CCPS into

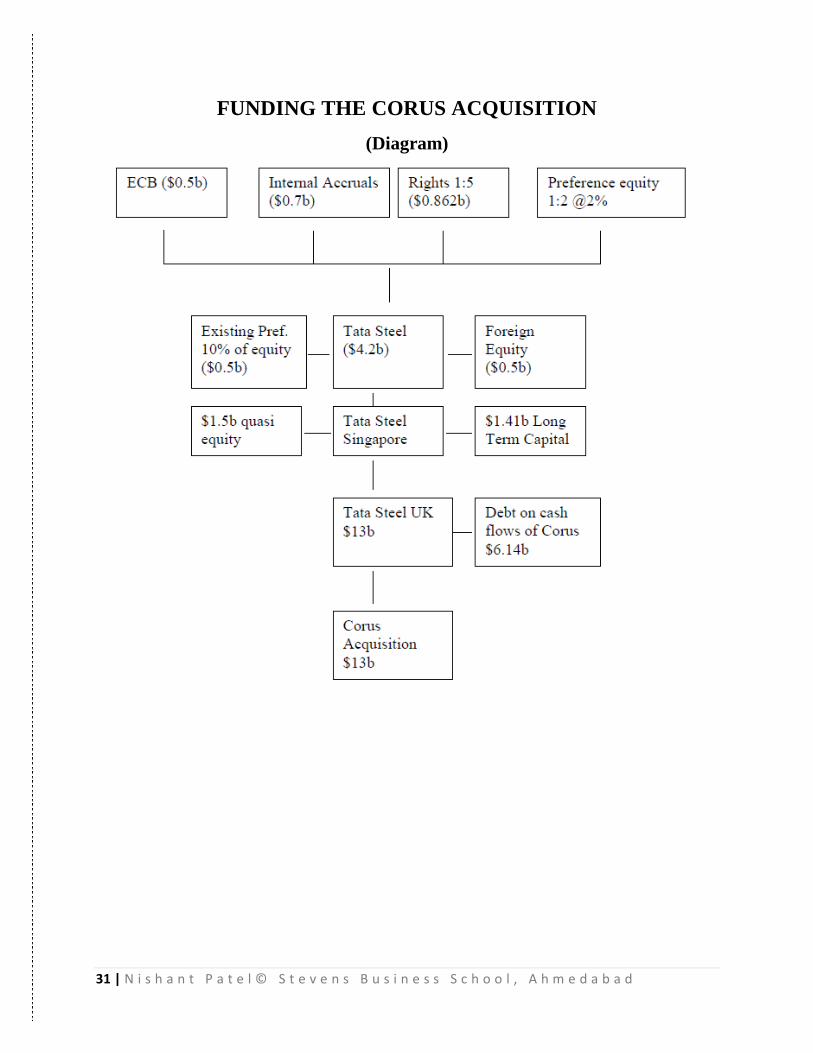

equity. Chart 7 presents the final funding structure of the Corus acquisition.

In 2006, Tata Steel had a Baa2 rating from Moody‘s. On July 5, 2007 Moody‘s

Investors service downgraded the corporate family rating of Tata Steel from Ba1 to

Baa2. The rating reflected Tata Steel's weakened balance sheet liquidity and

financial profile as a result of its largely debt-funded acquisition of Corus Group

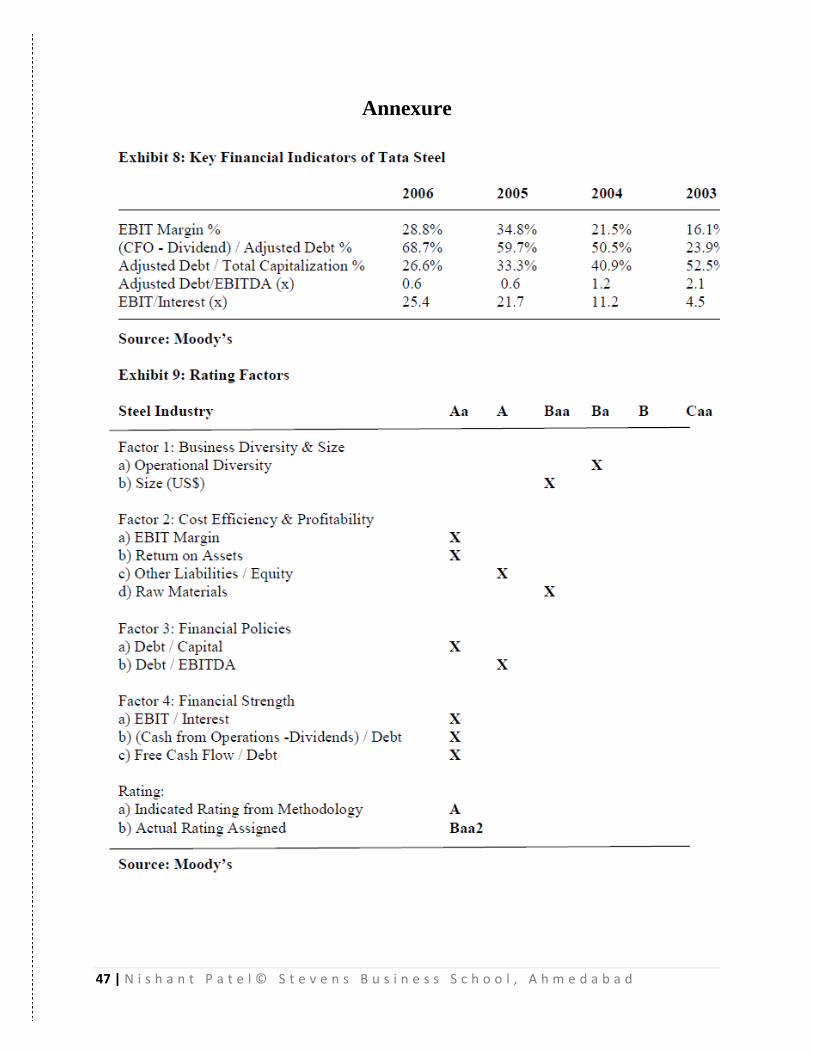

plc. Chart 8 and 9 present the key financial indicators and the rating factors used

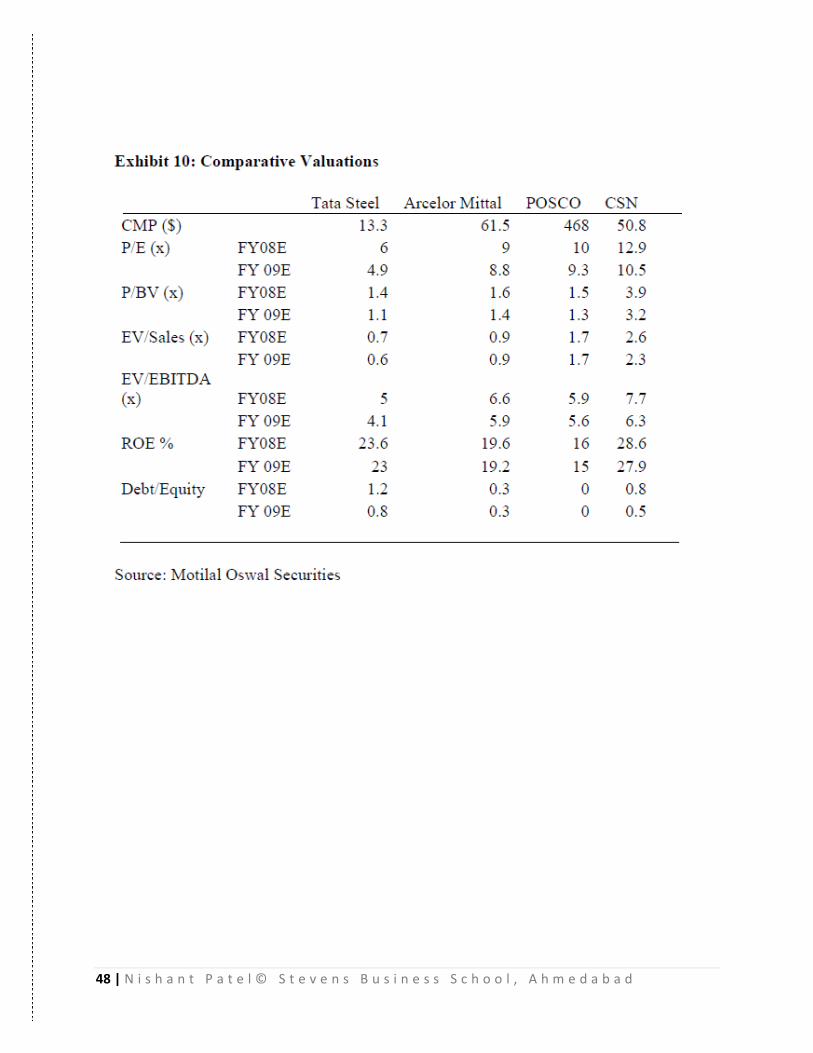

by Moody‘s. Chart 10 provides a summary of (estimated) comparative valuations

of major steel companies.

31 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

FUNDING THE CORUS ACQUISITION

(Diagram)

32 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

FOCUS ON INTEGRATION

A strong economic or strategic rationale for synergies is the starting point for any

successful acquisition. Virtually no acquiring company would dispute this

statement. But, many of the unsuccessful acquisitions involve weak logic dressed

up with vacuous statements, such as 'global footprint,' 'scale,' and 'optimal balance.'

There is no need for an acquisition to achieve an objective that the shareholders

can easily achieve on their own, such as diversify to reduce non-systematic risk. A

succinct but powerful way to state the logic of synergy is that an acquisition can

create value when the company can exploit a (usually intangible) firm-specific

resource that cannot be easily traded in a marketplace. Kaushik Chatterjee, the

CFO of Tata Steel, calls this the Oriental approach as opposed to the Western

approach. He described the current Tata Steel-Corus conglomerate as two separate

entities bridged together by the support functions like

finance and HR.

DETAILS OF SHARES

Rights Issue of Shares

Equity Shares in the ratio of one Equity Share for every five Equity Shares held at

a price of Rs.300 per share (i.e. face value of Rs.10 each at a premium of Rs.290

per share); Issue Size is

Rs. 36.54 billions.

33 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

Rights Issue of Convertible Preference Shares

The Company issued CCPS of Rs 54.81b in the ratio of 1:7 to existing equity

shareholders. The six CCPS of the face value of Rs 100 each compulsorily and

automatically converted into one Equity Share fully paid up of Rs 10 each at a

premium of Rs 590. The CCPS compulsorily and automatically converted into

Equity Shares fully paid up on September 01, 2009 without any application or any

further act on the part of the CCPS holders. On conversion of CCPS into Equity

Shares, the Equity Share Capital would increase to 822.1 m shares of Rs 10 each.

Convertible Alternative Reference Securities

The CARS carried a coupon rate of 1% paid semiannually in arrears on March 4

and September 4 except the last payment of interest, which would be paid on

September 5, 2012. The CARS would be issued in denominations of $100,000

each. Each CARS would have 4591.58 options. The holders of CARS would have

the right to convert their CARS at any time during the conversion period. The

conversion rights attached to the CARS might be exercised at the option of the

holder any time on or after September 4, 2011 and by 3 PM on August 6, 2012 or

if such CARS had been called for redemption by the issuer prior to maturity date

then by 3 PM on the 7th day prior to the date fixed for such redemption. The initial

conversion price would be Rs 876.6625 per share at a fixed exchange rate of Rs

40.25/$. The SEBI (Securities Exchange Board of India) floor price for the same is

Rs 691.83 per share.

34 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

TIMELINE OF TATA’S ACQUISITION OF CORUS

It is important to gain an understanding of the events that led to Corus‘s desire to

be acquired before launching into a detailed discussion of the acquisition activity.

Corus, the Anglo- Dutch steelmaker, was formed in 1999 by the merger of British

Steel with Hoogovens of the Netherlands. With 47,300 employees working in

plants across Britain, the Netherlands, Germany, France, Norway, and Belgium,

Corus had the highest cost of production among the world‘s steel makers. After the

merger, a rift developed between the two camps. Matters became worse when the

British half of the business sustained serious losses while the Dutch side was quite

profitable. The Dutch contended that the UK side of the business was causing the

entire organization to be unprofitable. Corus‘s management realized that the status

quo was unsustainable given the increased competition from steelmakers in

developing economies who had access to cheaper labor and raw materials.

Additionally, higher raw material and energy costs were impacting profitability. So

they decided to look for a suitable partner outside Western Europe to acquire

Corus, and began negotiations with key players in the steel industry from India,

Russia, and Brazil. ($=US dollars; GB pounds=Great Britain Pounds; p=pence; Rs.

= Indian Rupees)

35 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

TIMELINE

11/2005 Corus‘s top management meet Ratan Tata in Mumbai.

Mid-2006 Ratan Tata made an offer of 455p per share to buy Corus

10/17/06 Tata Steel makes a cash offer of GB 5.1billion pounds ($10 billion) bid

for Corus worth 455p a share in cash.

10/20/06 Corus‘s Board of Directors recommend acceptance of Tata Steel‘s offer.

11/17/06 Companhia Siderurgica Nacional (CSN) of Brazil makes a bid of GBP

5.3 billion for Corus, worth 475p a share in cash.

11/27/06 Corus postpones shareholder meeting from December 4 to December 20

to give CSN time to prepare a formal bid.

11/28/06 Corus reports a 63 per cent increase in quarterly profits.

12/10/06 Tata Steel raises its offer by 10 per cent and makes an offer of GBP 5.5

billion including debt, worth 500p a share in cash.

12/11/06 CSN raises its formal offer for Corus from 500p to 515p a share in cash.

1/21/07 Corus accepts a 515 pence per share offer from CSN, but speculation in

the financial markets anticipating a counter offer result in Corus‘s shares closing at

545 p per share, well above CSN‘s latest offer.

1/27/07 Tata Steel and CSN agreed to terms for an auction that will begin January

30 at 4:30 p.m. London time and end by 2:30 a.m. with an announcement of the

winner by 3:00 a.m. There will be up to nine rounds of bidding. 1/30/07 The

British press bills the bid for Corus as a clash between Tata Steel and CSN as a

battle to ―decide the fate of more than two centuries of British industrial history‖

(Knight Ridder, 2007 January 30).

1/31/07 The ―battle for Corus‖ starts. It is seen as a clash of two steel titans: Ratan

Tata and CSN‘s Benjamin Steinbruch. (Thomas, 2007 January 31).

36 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

2/1/07 After three months of bids and counter-bids, Tata Steel wins a fiercely

contested 8-hour closed-door auction against Brazil‘s CSN for Corus. Tata Steel

acquires 21.1 percent of the equity share capital for 608 pence per share ($11.7),

besting the CSN bid of 603 pence, paving the way to acquire Corus.

4/2/07 The courts officially approved Tata Steel‘s acquisition of Corus in a deal

valued at GBP 6.2 billion ($12 billion dollars).

4/11/07 Tata Steel‘s board of directors meet on 4/17 to consider proposals for

raising equity funds to finance the Corus acquisition. Tata Steel shares trade at Rs.

495.55 on the Bombay Stock Exchange.

4/18/07 Tata Steel announces that it has deployed teams to work on synergies in

areas of manufacturing, procurement, logistics, marketing, iron and steel making.

By the end of May, long-term strategic issues and specific areas of synergy were

close to conclusion.

4/28/07 Tata Steel announces it will raise $4.1 billion equity capital as partial

payment for Corus using a rights issue and a convertible preference share issue

along with other financial methods.

5/4/07 Tata Steel will borrow $7.3 billion in loans as part of its long-term financing

arrangements in the takeover of Corus. It took advantage of high liquidity in the

leveraged loan market and went with a long-term arrangement with Citigroup,

Standard Chartered and ABN Amro.

5/17/07 Tata Steel announced plans that would potentially make it the second

largest steel maker in the world within five years. Manufacturing capacity is

planned to increase from about 25 million tons a year to 40 million by 2012, and

then to 50 million by 2015.

37 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

DID TATA OVERBID FOR CORUS? VIEWPOINTS OF

FINANCIAL ANALYSTS

Many financial analysts felt that Tata Steel overpaid for the Corus acquisition.

Immediately after the acquisition announcement, Tata Steel‘s share price fell by

10.7 percent to Rs. 463.95 on the Bombay Stock Exchange. According to Martin

Stanley, London based head of spread betting at the brokerage firm of GFT Global

Markets, ―The consensus view seems to be that Tata have probably overpaid, but if

further consolidation in this sector occurs going forward then this will look like

very fair value‖ (International Herald Tribune, 1/30/07). Additional concerns were

raised about the debt liability of Tata Steel which borrowed more money to fund

the acquisition. According to Standard & Poor‘s analyst Anushkant Taneja, ―The

size of the Tata acquisition and the potential cash outflow in Tata Steel‘s offer for

Corus could have an adverse impact on its financial risk profile.‖ Standard &

Poor‘s rating service in India, Crisil, placed Tata Steel on the ―negative

implications‖ watch list after its Corus acquisition. The contention was that Tata

Steel had overstretched itself due to execution risk and lack of experience by

Indian companies in acquiring international businesses (Range, 2007, April 26).

Moody‘s Investor Services downgraded Tata Steel‘s rating from Baa2 (investment

grade) to Ba1 (speculative grade). The primary reason cited was Tata Steel‘s

weakened balance sheet liquidity and financial profile resulting from its largely

debt-funded acquisition of Corus. Moody‘s Senior V.P. Alan Greene stated Tata

Steel‘s current high leverage constrains its financial strength and flexibility and

―the main challenge facing management is to de-risk the large capital structure

while not neglecting existing operations and opportunities for rapid growth in

Asia.‖ He further stated that ―Tata Steel‘s ambitious capacity expansion plan will

lead to higher project execution risk over several years and materially elevate

38 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

financial leverage unless it is deferred.‖ (Businessline, 2007, July 7). According to

Sreesankar, head of research at Il&Fs investments in Mumbai, ―They (Tata Steel)

wanted the company and they have got it. But we have to see how the finding

happens and how the integration progresses. One distinction is that EBITDA

(earning before income taxes and depreciation allowance) margins for Tatas are

about 40 percent and for Corus is about 7 percent.‖ Clearly, the financial industry

analysts were skeptical about the long-term financial viability of this acquisition.

According to Shriram Iyer, head of research at Edelweiss in umbai, ―…the time

horizons of investors and of the company may not be aligned‖ (Leahy, 2007, 16).

DID TATA OVERBID FOR CORUS? VIEWPOINT OF TATA

STEEL’S EXECUTIVES

This proposed acquisition represents a defining moment for Tata Steel and is

entirely consistent with our strategy of growth through international expansion.

This creates a well balanced company, strategically well placed to compete in an

increasingly competitive global environment. (Ratan Tata quoted in Financial

Express; 2007, February 13) The Tata Steel board of directors approved the project

to acquire Corus, as it was consistent with stated objectives of growth and

globalization. Although Tata Steel ended up paying more for Corus than its

original bid, its management felt that there were many favorable strategic and

financial outcomes to be realized. To begin with, this acquisition would position

the combined group as the fifth largest steel company in the world by production

output. The new entity would have a meaningful market presence in both Europe

(where Corus was a well established brand name) and Asia (where Tata was a well

established brand name). Combining the low cost upstream production in India

39 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

with the high-end downstream processing facilities of Corus in Europe was

intended to create synergies that would significantly improve the competitiveness

of European operations. Tata Steel will retain access to low cost developed

markets. There was tremendous potential to create cross-fertilization of research

and development capabilities in the automotive, packaging and construction

sectors with transfer of technology, best practices and managerial from Europe to

India. (www.tatasteel.com, 2006, October 20). Tata Steel formed teams to work on

synergies in areas of manufacturing, procurement, logistics, marketing, iron and

steel making. There were 15-18 teams consisting of 3-4 members from both

companies. Each team worked on realizing various potential synergies by sharing

know-how, adopting best practices, and information to develop efficient practices

aiding in cost reduction. B. Muthuraman, Managing Director of Tata Steel

expected the synergies to be achieved within three years and to have a higher

valuation than $350 million per year indicated at the time of the deal. Muthuraman

further noted that the acquisition price for Corus placed production costs at $710

per ton, far less than $1,200 to $1,300 per ton that would have been the price for a

Greenfield plant with a production capacity for 19 million tons (Bremner and

Lakshman, 2007). During 2007, benefits of the merger for Tata were realized in

manufacturing, whereas benefits for Corus were gained through reductions in taxes

and shared services. In 2008, Tata made the Fortune 500 list on the basis of its

revenues. In large part, this was due to the acquisition of Corus. From the very

inception of the merger project, Tata Steel officials had maintained that funding the

acquisition would be supported by Tata Sons and any subsequent borrowing would

not be a balance sheet burden. The initial plan was to fund the acquisition of Corus

through a debt-equity ratio of 53:47 for an amount of $4.1 billion. The remaining

amount was to be acquired though a series of long-term loans which would be

serviced through Corus‘s cash flows. Corus‘s revenues at the time of takeover were

40 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

approximately $20 billion (Leahy, 2007, January 26). Tata Steel‘s senior

executives estimated that cost cutting measures alone could make the acquisition a

successful one. The potential existed for production and distribution costs to be

spread across Europe, India and other Asian markets. Tata Steel‘s EBIDTA

(earnings before interest, tax, depreciation and amortization) margin of 30 percent

was significantly higher compared to Corus‘ EBITDA of 10 percent. The new

entity was estimated to have a combined EBIDTA margin of 14 percent (taking

into account that Corus‘s revenues were five times more that of Tata Steel). The

EBITDA was expected to increase to 25 percent by 2012. Shortly after Tata Steel

successfully outbid CSN for Corus, Tata finance director Ishaat Hussain noted that

the Corus deal was a ―must-do‖. ―Consolidation [in the steel industry] will take

place going forward. It [Corus] was perhaps the only significant player which we

could see as a possible acquisition in this consolidating phase. That‘s why Corus

was so important to Tata Steel.‖ (Lea, 2007, January 31)

IMPACT OF CORUS ACQUISITION ON INDIAN CORPORATE

MORALE

There was tremendous outpouring of nationalistic euphoria and economic

patriotism in the Indian press after this deal. During the early weeks of 2007, The

Times of India the bestselling English daily newspaper, was reportedly ―inviting its

readers to discuss the new ‗India poised for global supremacy‘ Johnson, 2007,

February 3). The Tata deal has fed an unmistakable undertone of triumph as the

country‘s status as the world‘s second fastest growing economy.‖ The Economic

Times, India‘s best selling business newspaper reported ―For India, this deal is not

about size—it‘s the first step towards what we call the Global Indian Takeover.‖

(Johnson, 2007, February 3). According to Ratan Tata, who spoke at the time of

41 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

the acquisition, ―It‘s a tremendous strategic acquisition. I believe this will the first

step in showing that Indian industry can in fact step outside the shores of India in

an international marketplace and acquit itself as a global player‖ (International

Herald Tribune, 2007, January 30). Kamal Nath (Johnson, 2007 January 15, 4), the

Indian Minister for Commerce and Industry felt that the ―global perception of India

is changing…it‘s a two-way street now….not only is India seeking foreign

investment, but Indian companies are emerging investors in other countries.‖ The

Confederation of Indian Industry, India‘s largest business association described the

acquisition as ―path breaking‖ which would enable emerging Indian firms to gain

greater respect from the global business community. For the first time in 2006,

overseas acquisitions by Indian firms exceeded the value of foreign companies

buying in India. During the first six months of 2006, Indian companies had

completed approximately 78 cross-border acquisitions worth $5.2 billion. For the

year ending 2006, outbound deals by Indian companies totaled $22.4 billion

compared with $11.3 billion in purchases from abroad. (Harris 2007, March 9).

Indian business executives attribute this new confidence in part to a decade of

restructuring that started in 1991 when newly drafted laws allowed greater foreign

competition. Others point to the successes of Indian based firms such as Infosys

Technologies, Wipro and TCS who have proven to be world class competitors

from a cost/quality perspective. In the wake of Tata Steel‘s acquisition of Corus,

the chief executive of ICICI, India‘s second largest bank, proposed that Indian

firms now ―have the confidence to go out and buy‖ buoyed by substantial

corporate profits which have provided large cash surpluses over the last 18

quarters. He believed that the Tata-Corus deal would most likely lead to a string of

takeovers in the UK by Indian companies (Knight Ridder, 2007, April 27). An

article published in the Wall Street Journal predicted a global shopping spree by

Indian companies due to easier access to funds, an annual growth rate of over 8%,

42 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

and a strong desire to engage in worldwide competition (Range, 2007). In the first

two months of 2007, Indian companies seeking new technology, better overseas

market access, and greater production capacity arranged or closed on foreign

purchase deals worth $21 billion. Mr. P. K. Vijayaraghavan, Associate Director,

PricewaterhouseCoopers Private Ltd. spoke on the importance of corporate

restructuring for India and noted that Tata Steel‘s acquisition of Corus was an

outstanding example of Indian corporate thinking. (Businessline, 2007, March 8).

The easy availability of global funds drove many Indian companies toward

acquisitions following the Tata Steel acquisition of Corus which spurred

transactions from rivals such as Essar group taking over two steel companies in

North America. India‘s largest bank, State Bank of India which is government-

controlled, and ICICI, India‘s largest private bank responded to the surge in deal-

making and investment by raising capital. ―The banking sector is facing a growing

need for capital because of the expected rise in capital expenditure by the corporate

sector over the next few years to meet funding requirements.‖ (Leahy, 2007, July

7). A proposed amendment to Competition (Amendment) Bill of 2006 and the

Competition Act (2002) required companies undertaking mergers or acquisitions in

India or overseas to compulsorily report the proposal to the Competition

commission of India before making such a deal. The proposal would limit

acquisitions that might have an appreciably adverse effect on competition within

India markets. The dollar limit thresholds are $2 billion if the acquirer is a group in

India and $6 billion if the acquirer is outside of India (Businessline, 2007, May 6).

Cross-border mergers and acquisitions have gained tremendous popularity among

Indian executives as a means to achieve growth and secure a global presence.

According to David (2007), there are numerous seminars dealing with mergers and

acquisitions where seasoned M&A executives offer advice on a number of topics

ranging from government rules and regulations, pitfalls to avoid, and cultural

43 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

issues impacting post-merger scenarios. raw materials, gain exposure to high

growth emerging markets, while gaining price stability in the global markets.

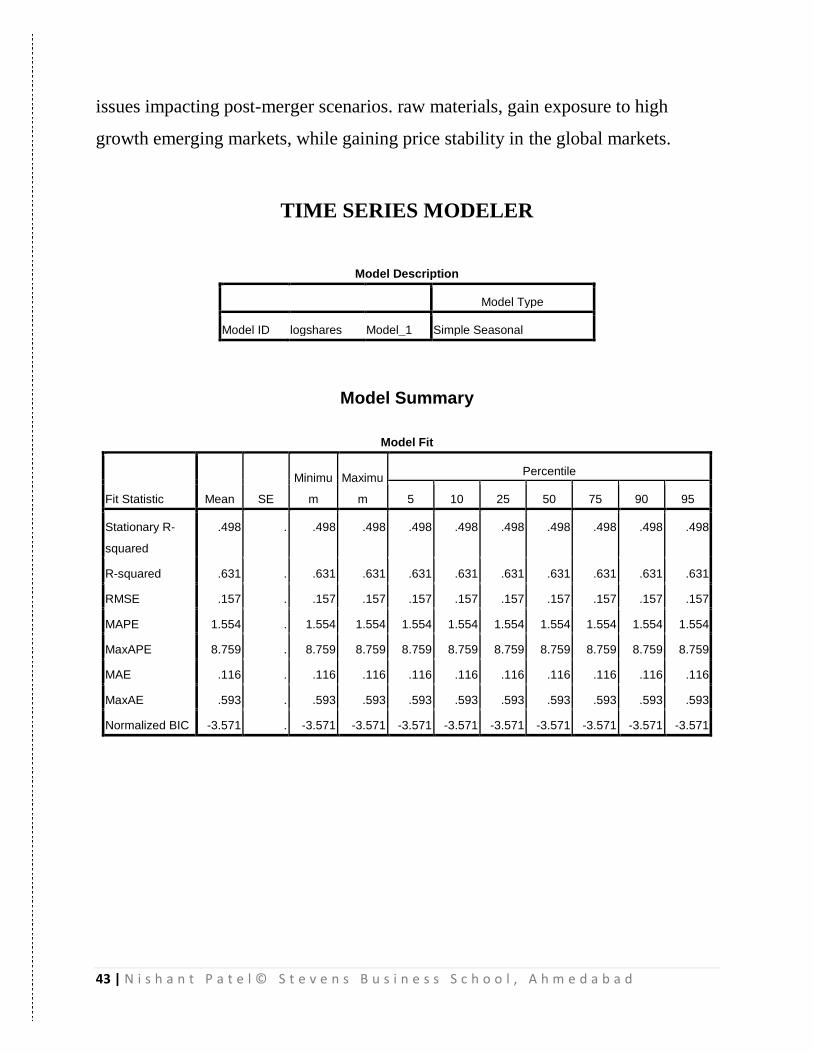

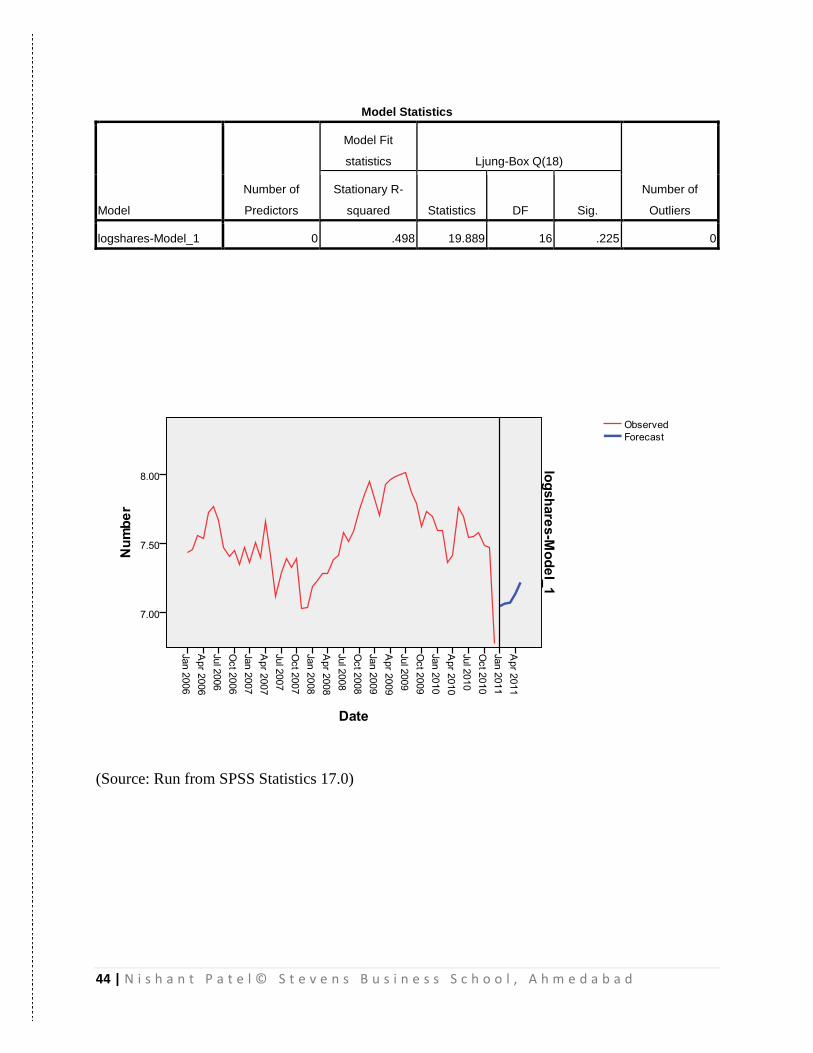

TIME SERIES MODELER

Model Description

Model Type

Model ID logshares Model_1 Simple Seasonal

Model Summary

Model Fit

Fit Statistic Mean SE

Minimu

m

Maximu

m

Percentile

5 10 25 50 75 90 95

Stationary R-

squared

.498 . .498 .498 .498 .498 .498 .498 .498 .498 .498

R-squared .631 . .631 .631 .631 .631 .631 .631 .631 .631 .631

RMSE .157 . .157 .157 .157 .157 .157 .157 .157 .157 .157

MAPE 1.554 . 1.554 1.554 1.554 1.554 1.554 1.554 1.554 1.554 1.554

MaxAPE 8.759 . 8.759 8.759 8.759 8.759 8.759 8.759 8.759 8.759 8.759

MAE .116 . .116 .116 .116 .116 .116 .116 .116 .116 .116

MaxAE .593 . .593 .593 .593 .593 .593 .593 .593 .593 .593

Normalized BIC -3.571 . -3.571 -3.571 -3.571 -3.571 -3.571 -3.571 -3.571 -3.571 -3.571

44 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

Model Statistics

Model

Number of

Predictors

Model Fit

statistics Ljung-Box Q(18)

Number of

Outliers

Stationary R-

squared Statistics DF Sig.

logshares-Model_1 0 .498 19.889 16 .225 0

(Source: Run from SPSS Statistics 17.0)

45 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

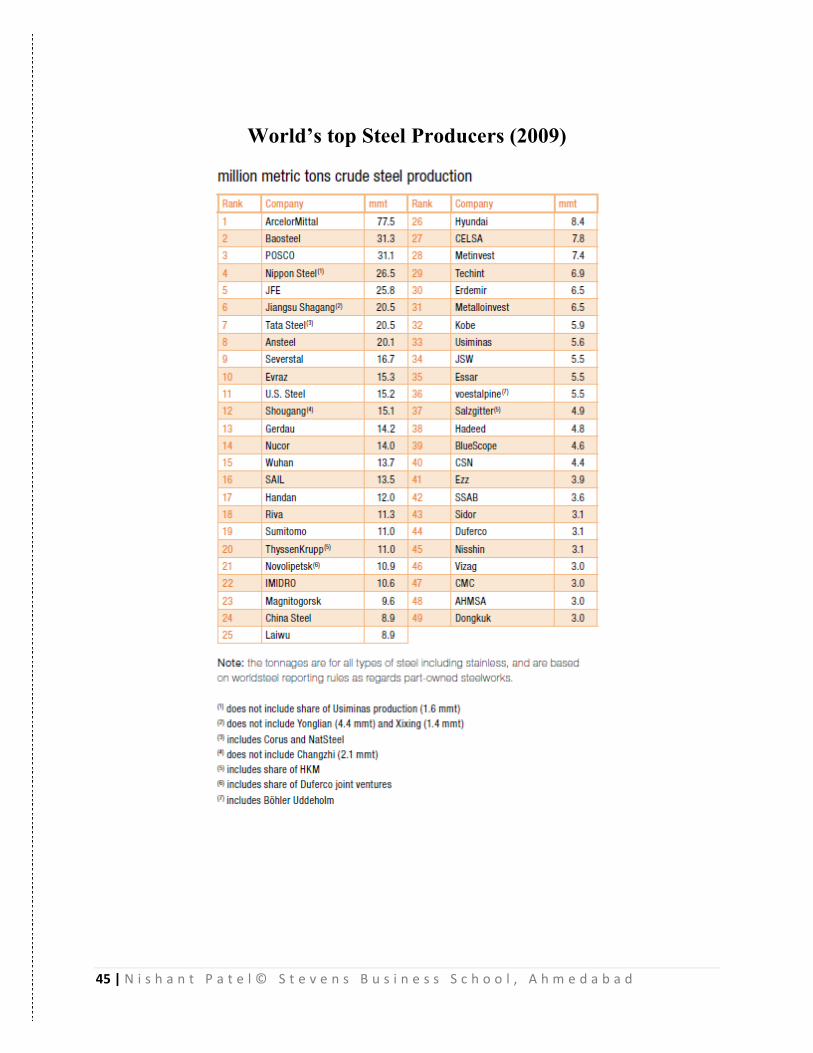

World’s top Steel Producers (2009)

46 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

Bibliography

Websites referred:

http://www.worldsteel.org/?action=programs&id=53

http://www.bseindia.com/bseplus/StockReach/AdvanceStockReach.aspx?scripcode=500470

http://www.motilaloswal.com/Research/

http://74.125.155.132/scholar?q=cache:1p4SLlOZDcQJ:scholar.google.com/+tata+corus+acquisi

tion&hl=en&as_sdt=2000

http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1358681

http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1431588

http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1118306

http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1225942

http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1461372

http://www.worldsteel.org/?action=programs&id=53

http://bcgindia.com

http://www.worldsteel.org/

http://www.tatasteel.co.in

http://www.tatasteel.com

http://www.bseindia.com

Books referred:

Mergers & Acquisition Corporate Restructuring by Godbole

The Mergers & Acquisitions handbook By Milton L. Rock, Robert H. Rock, Martin J. Sikora

Mergers & Acquisitions from A to Z

Mergers, Acquisitions & Corporate Restructuring by Rachna Jawa

The Mergers & Acquisitions by Kevin K. Boeh & Paul W. Beamish

Working Papers by:

Aneel Karnani, Stephen M. Ross School of Business, University of Michigan

John Quigley (Editor, Industry Publication Steel week)

Vishwanath S R

Software used:

Time Series Modeler has been formulated in SPSS Statistics 17.0

47 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

Annexure

48 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

49 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

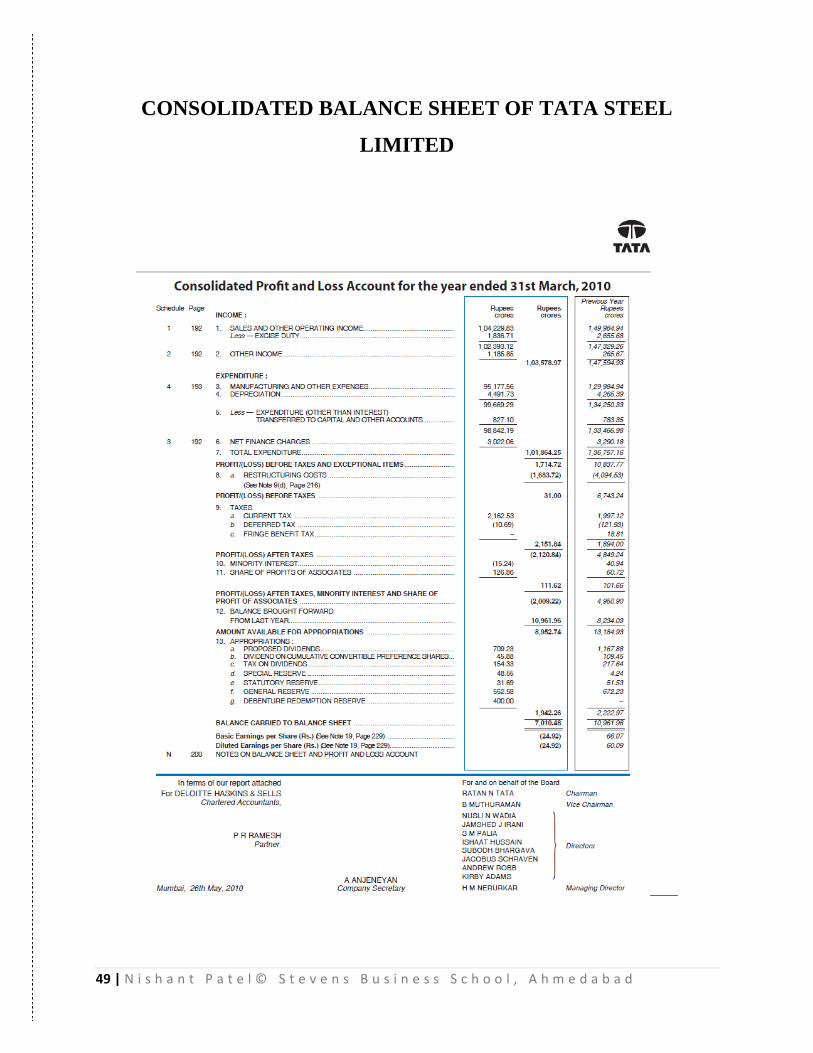

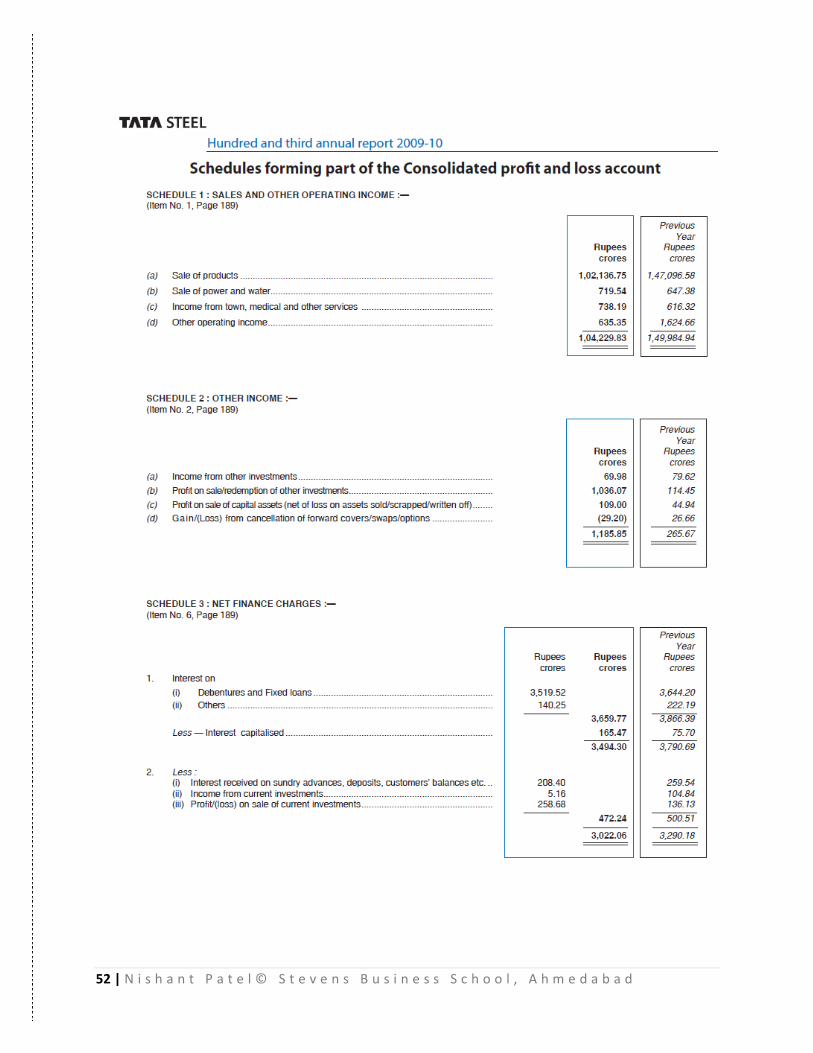

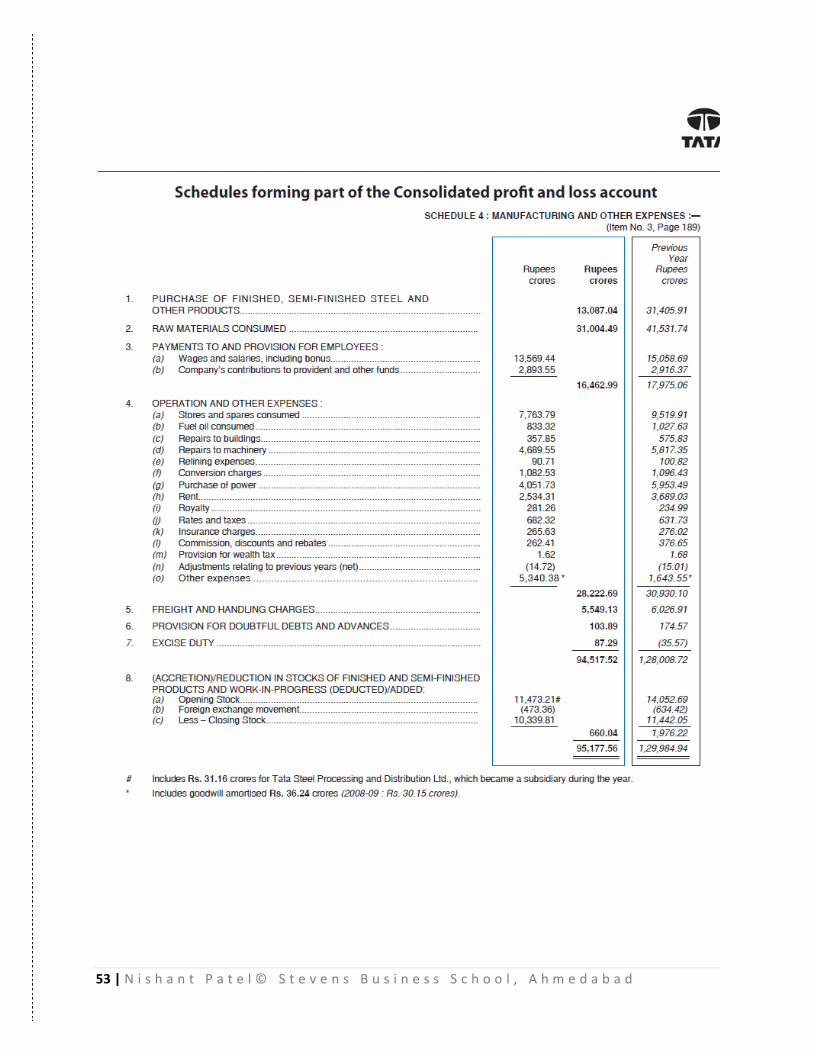

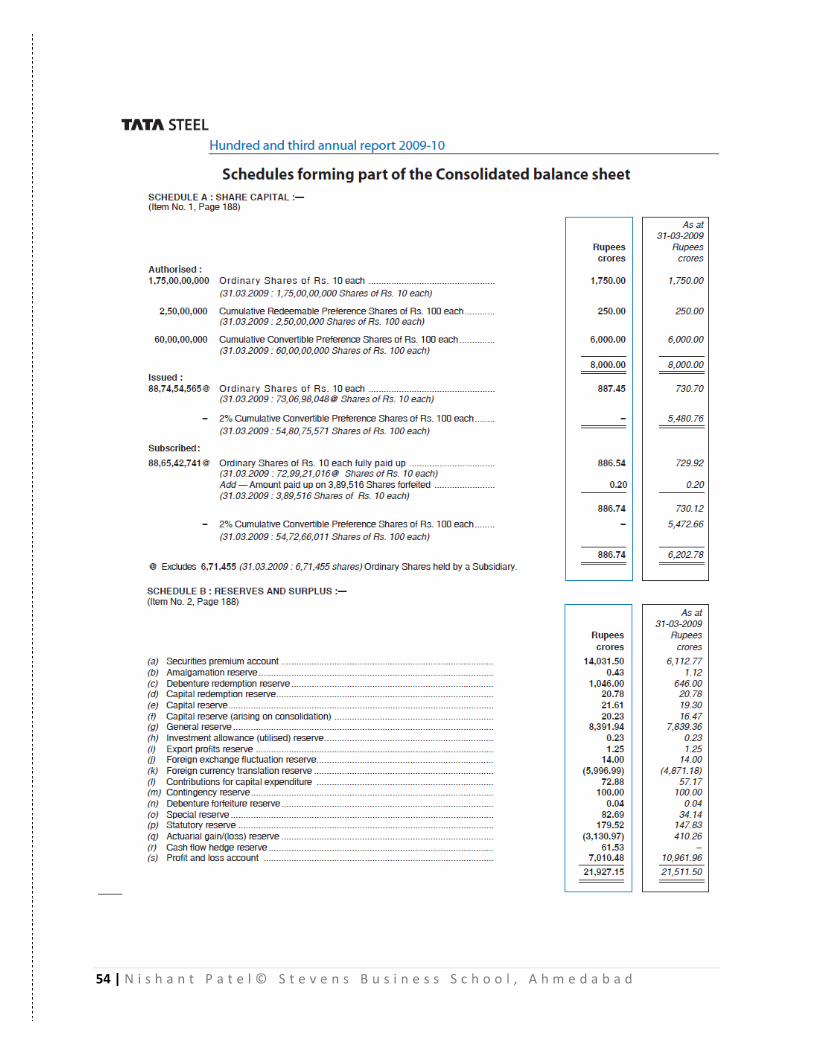

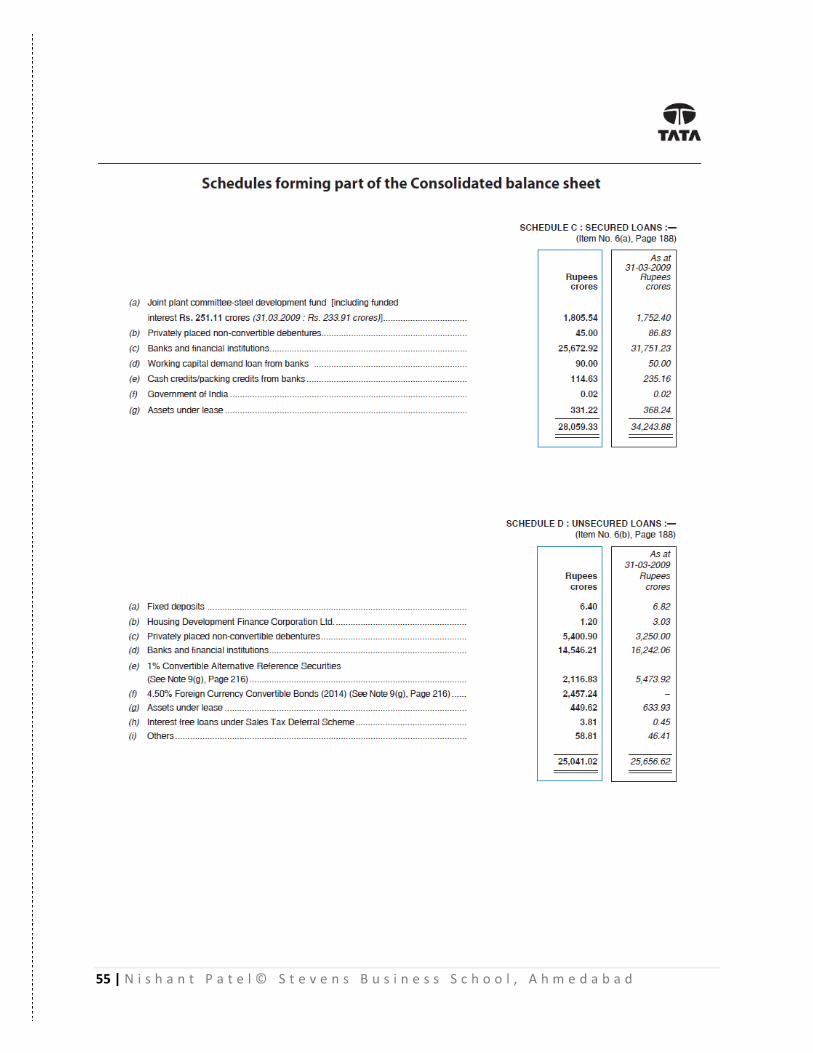

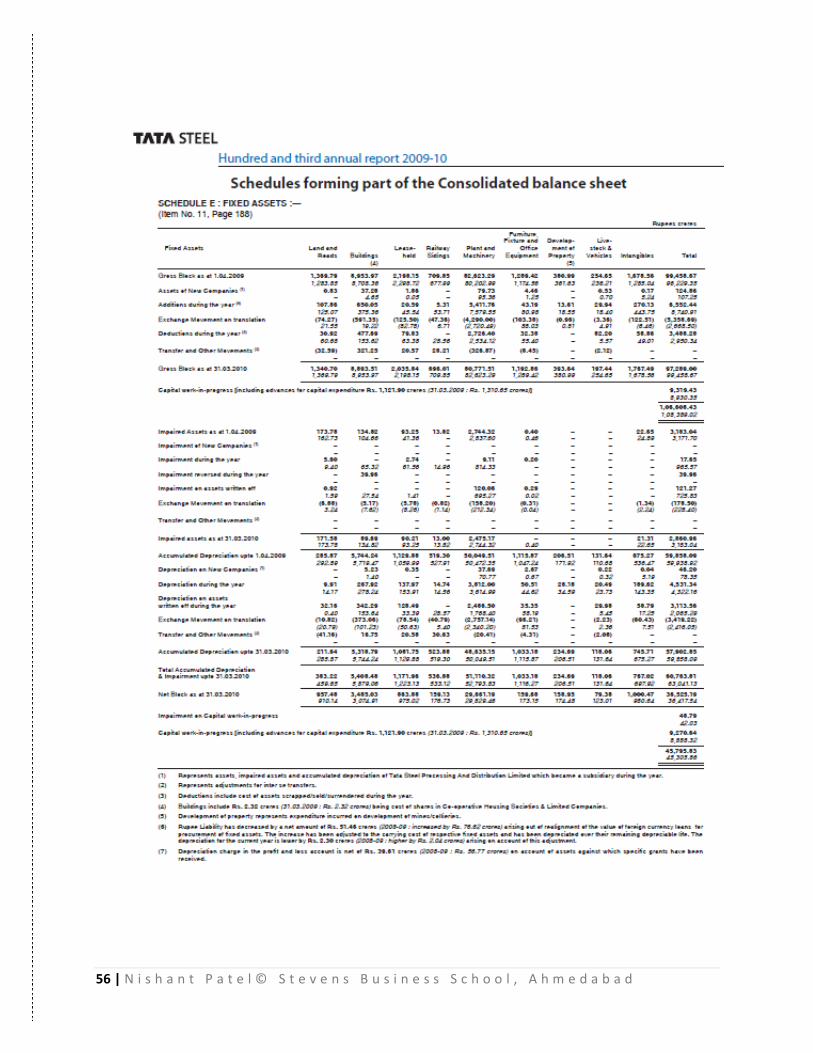

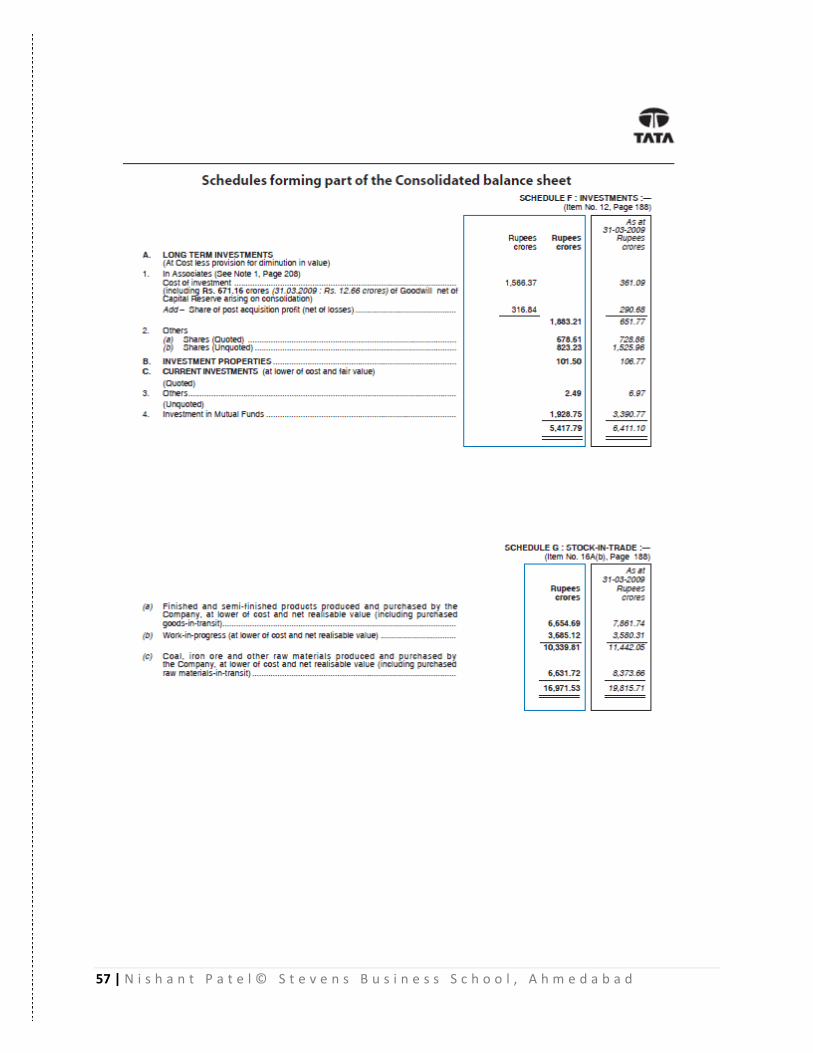

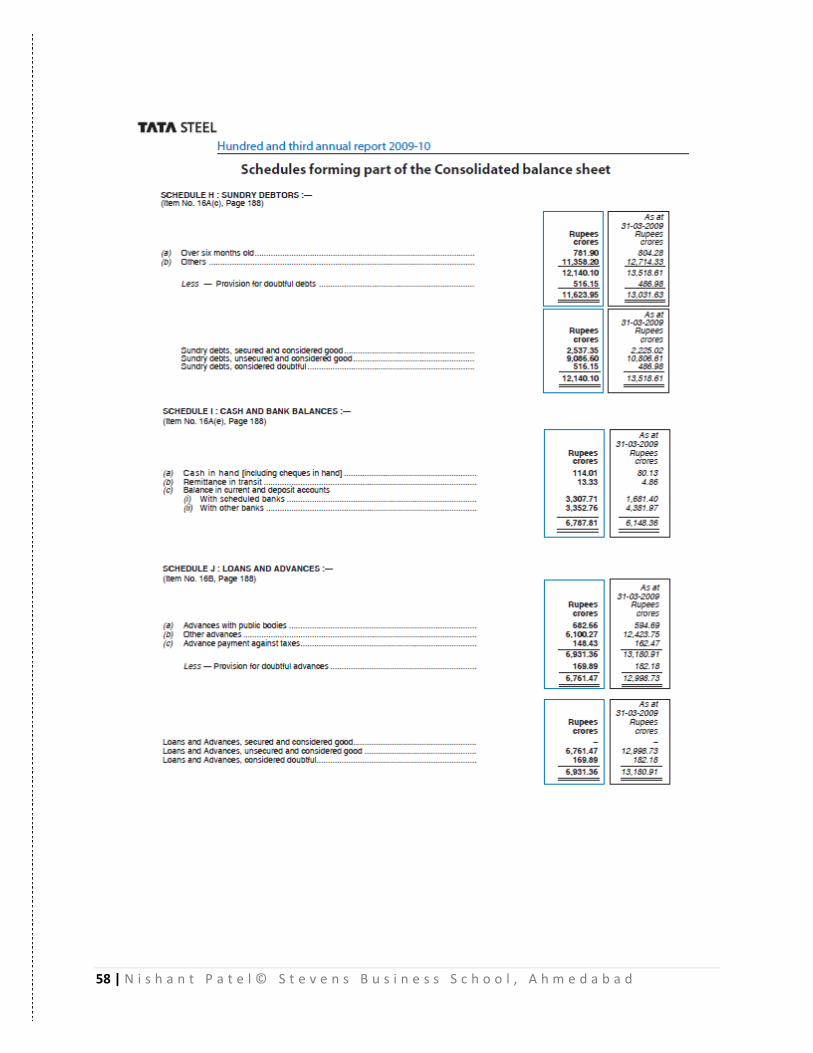

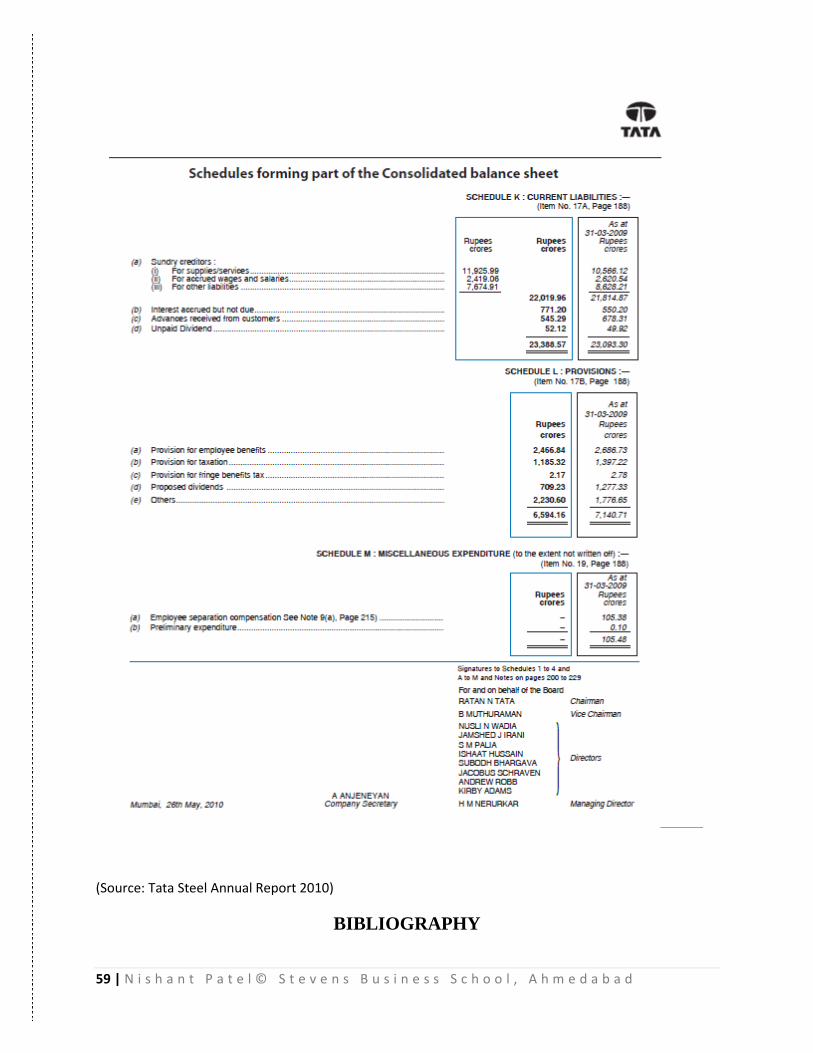

CONSOLIDATED BALANCE SHEET OF TATA STEEL

LIMITED

50 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

51 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

52 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

53 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

54 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

55 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

56 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

57 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

58 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

59 | N i s h a n t P a t e l © S t e v e n s B u s i n e s s S c h o o l , A h m e d a b a d

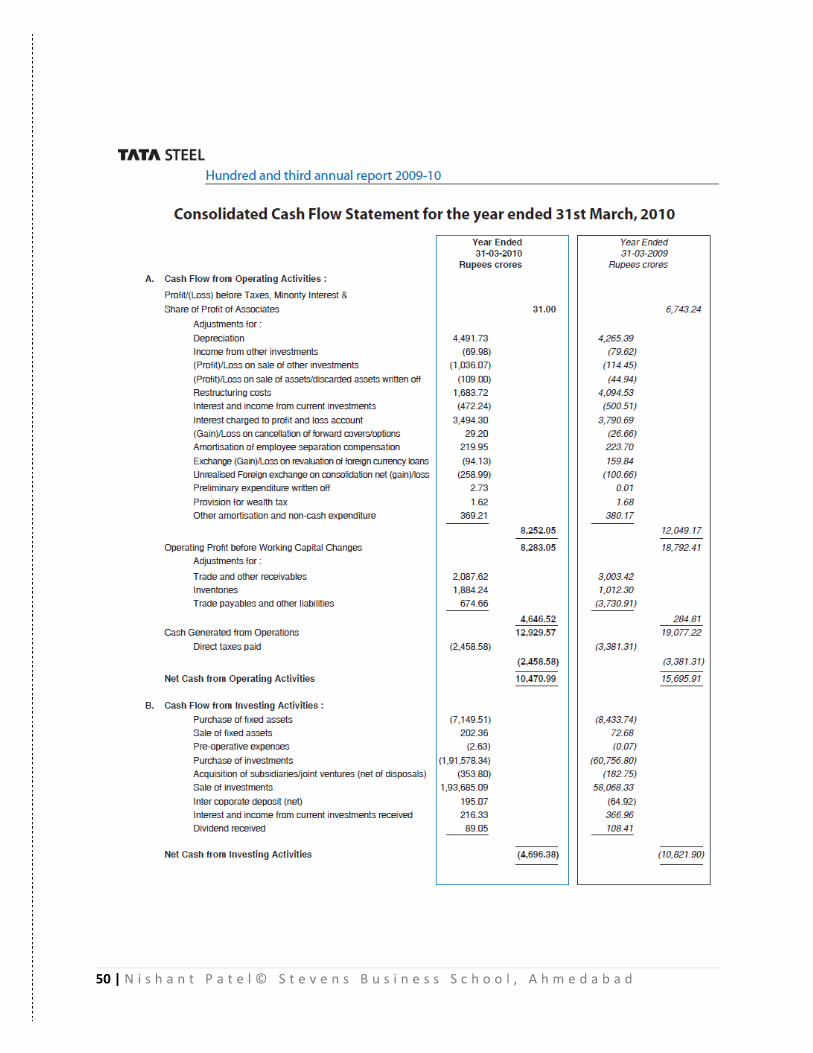

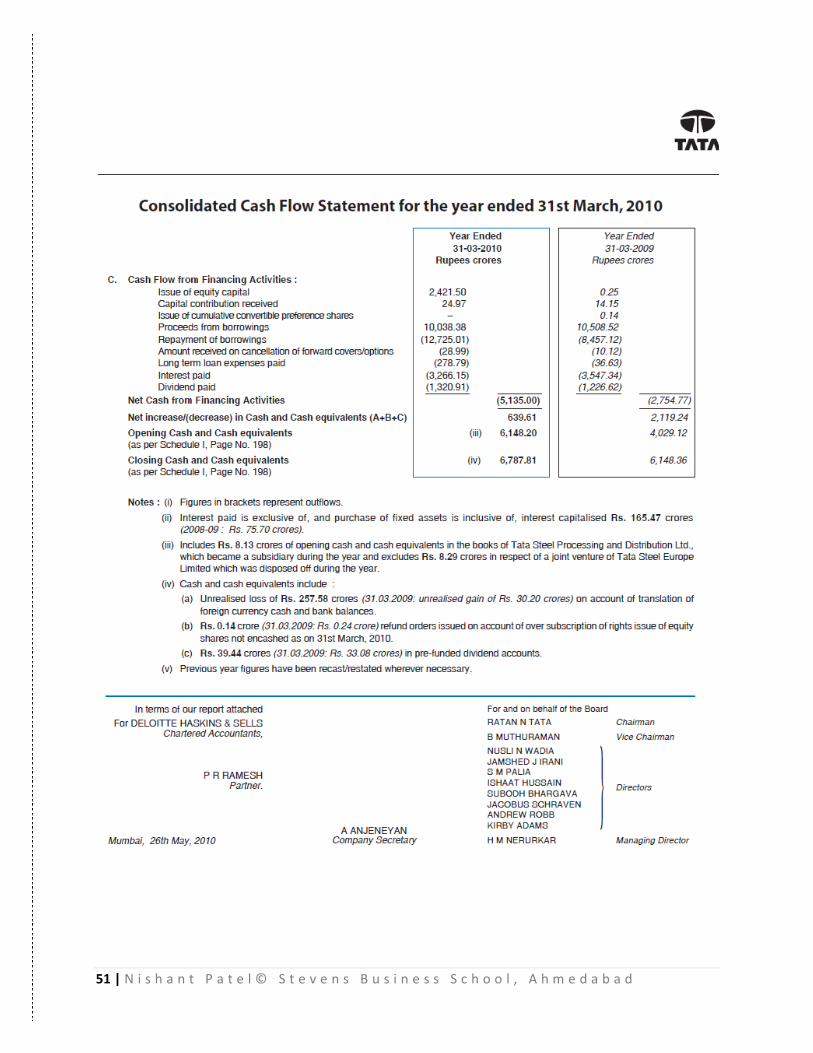

(Source: Tata Steel Annual Report 2010)

BIBLIOGRAPHY