tax considerations for publicly traded partnerships ... · pdf filetax considerations for...

TRANSCRIPT

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

Tax Considerations for Publicly Traded Partnerships

Gregory V. Nelson

April 18, 2013

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

2

Structure Economics Qualified Income MLP Capitalization Tax Shield Remedial Allocations Mergers & Acquisitions

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

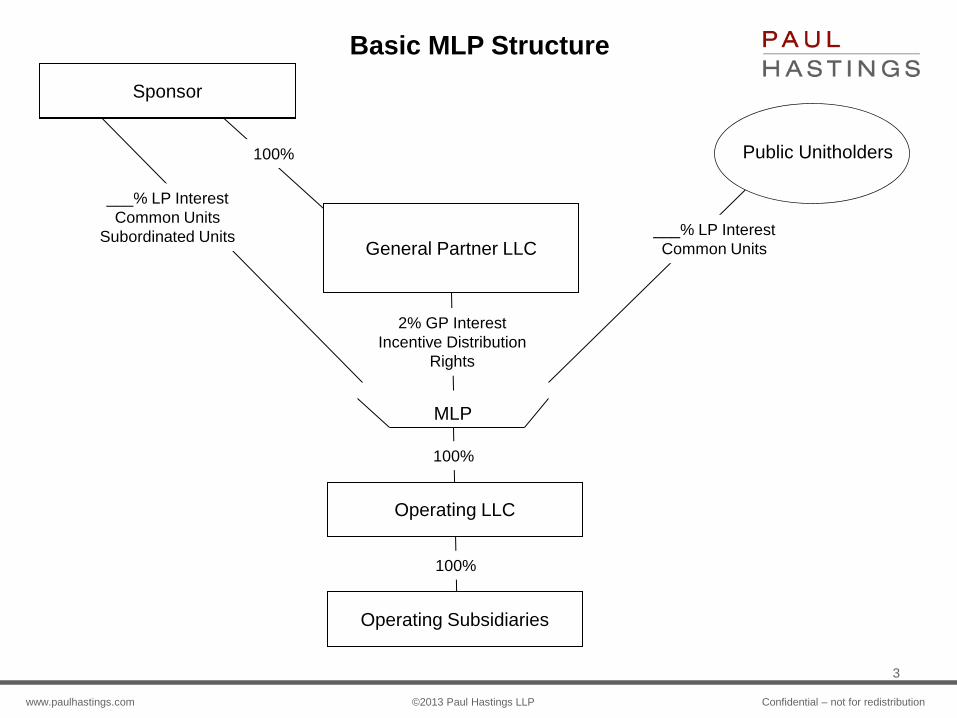

Sponsor Sponsor

Operating LLC

Operating Subsidiaries

Sponsor General Partner LLC

100%

100%

___% LP Interest Common Units

Subordinated Units

100%

___% LP Interest Common Units

2% GP Interest Incentive Distribution

Rights

MLP

Basic MLP Structure

Public Unitholders

3

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

Cash Waterfall

• The MLP first establishes a Minimum Quarterly Distribution (“MQD”) equal to a yield on the initial offering price. If the initial offering price is $20 and if the yield is 7%, then the MQD is $1.40 per year or $0.35 per quarter.

• MLP cash is typically shared as follows:

• first, 98% to holders of Common Units and 2% to GP until Common Units have received the MQD (including MQD arrearages);

• second, 98% to holders of Subordinated Units and 2% to GP until each Subordinated Unit has received the MQD (but no MQD arrearages);

• third, 98% to LPs and 2% to GP until each LP unit has received 115% of the MQD;

• fourth, 85% to LPs and 15% to GP until each LP unit has received 125% of the MQD;

• fifth, 75% to LPs and 25% to GP until each LP unit has received 150% of the MQD; and

• thereafter, 50% to LPs and 50% to GP.

4

Economics

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

Subordinated Units

• MLP has a capital structure that is made up of:

• 2% General Partner Interest

• 49% Limited Partner Interest represented by Common Units

• 49% Limited Partner Interest represented by Subordinated Units

• Typically, and assuming the public holders own less than 49% of the MLP, the public unit holders are issued only Common Units. The Sponsor is issued the remaining Common Units and all the Subordinated Units.

• The Subordinated Units are not entitled to any distributions until the holders of the Common Units have received the MQD and all MQD arrearages.

• The Subordinated Units typically are not entitled to any MQD arrearages.

• The use of Subordinated Units allows the Common Units to have 2:1 coverage.

• The Subordinated Units convert to Common Units on a one-to-one basis when the MLP has earned and has paid the MQD for the three preceding four-quarter periods.

• The Subordinated Units also typically convert to Common Units if 150% of the MQD has been earned and has been paid for four quarters.

5

Economics

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

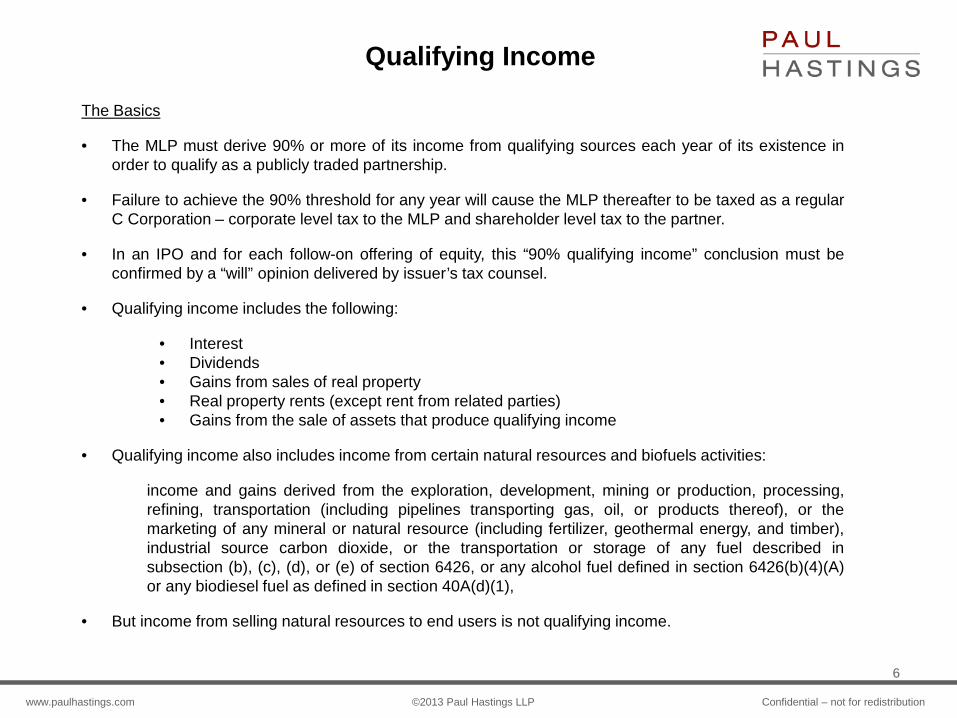

Qualifying Income

The Basics

• The MLP must derive 90% or more of its income from qualifying sources each year of its existence in order to qualify as a publicly traded partnership.

• Failure to achieve the 90% threshold for any year will cause the MLP thereafter to be taxed as a regular C Corporation – corporate level tax to the MLP and shareholder level tax to the partner.

• In an IPO and for each follow-on offering of equity, this “90% qualifying income” conclusion must be confirmed by a “will” opinion delivered by issuer’s tax counsel.

• Qualifying income includes the following:

• Interest • Dividends • Gains from sales of real property • Real property rents (except rent from related parties) • Gains from the sale of assets that produce qualifying income

• Qualifying income also includes income from certain natural resources and biofuels activities:

income and gains derived from the exploration, development, mining or production, processing, refining, transportation (including pipelines transporting gas, oil, or products thereof), or the marketing of any mineral or natural resource (including fertilizer, geothermal energy, and timber), industrial source carbon dioxide, or the transportation or storage of any fuel described in subsection (b), (c), (d), or (e) of section 6426, or any alcohol fuel defined in section 6426(b)(4)(A) or any biodiesel fuel as defined in section 40A(d)(1),

• But income from selling natural resources to end users is not qualifying income.

6

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

Recent Private Letter Ruling Guidance on Qualifying Income

• More rulings are being issued generally

• More rulings are issued regarding the oil field services industry activities

• “Integral to” the exploration or development or production of mineral and natural resources

• More rulings are issued to the processing of natural gas:

• Olefins plants

• Cracking facilities

7

Qualifying Income

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

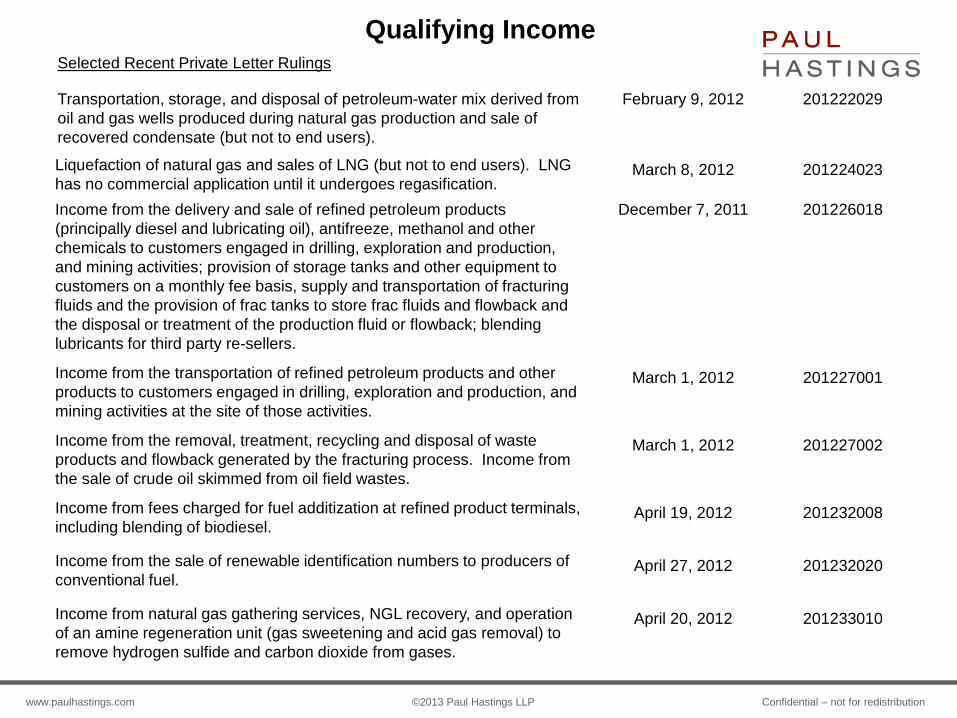

Selected Recent Private Letter Rulings

8

Transportation, storage, and disposal of petroleum-water mix derived from oil and gas wells produced during natural gas production and sale of recovered condensate (but not to end users).

February 9, 2012 201222029

Liquefaction of natural gas and sales of LNG (but not to end users). LNG has no commercial application until it undergoes regasification.

March 8, 2012 201224023

Income from the delivery and sale of refined petroleum products (principally diesel and lubricating oil), antifreeze, methanol and other chemicals to customers engaged in drilling, exploration and production, and mining activities; provision of storage tanks and other equipment to customers on a monthly fee basis, supply and transportation of fracturing fluids and the provision of frac tanks to store frac fluids and flowback and the disposal or treatment of the production fluid or flowback; blending lubricants for third party re-sellers.

December 7, 2011 201226018

Income from the transportation of refined petroleum products and other products to customers engaged in drilling, exploration and production, and mining activities at the site of those activities.

March 1, 2012 201227001

Income from the removal, treatment, recycling and disposal of waste products and flowback generated by the fracturing process. Income from the sale of crude oil skimmed from oil field wastes.

March 1, 2012 201227002

Income from fees charged for fuel additization at refined product terminals, including blending of biodiesel.

April 19, 2012 201232008

Income from the sale of renewable identification numbers to producers of conventional fuel.

April 27, 2012 201232020

Income from natural gas gathering services, NGL recovery, and operation of an amine regeneration unit (gas sweetening and acid gas removal) to remove hydrogen sulfide and carbon dioxide from gases.

April 20, 2012 201233010

Qualifying Income

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

Selected Recent Private Letter Rulings

9

Income from the supply and transportation of water to oil and gas producers for use in hydraulic fracturing.

May 11, 2012 201234005

Income from the conversion of ____________ into __________ through dehydrogenation or catalytic cracking.

June 5, 2012 201236005

Income from processing NGLs (ethane and propane) into olefins through a cracking process — the use of heat and pressure to remove hydrogen atoms and thereby decrease the size of the NGL molecules. Income from storing and transporting olefins.

July 2, 2012 201241004

Income from the lease of an offshore oil and gas platform. September 6, 2012 201250003

Income from refining, blending, processing, packaging, marketing and distributing refined products and lubricants, including bulk sales to government, commercial and industrial users in quantities and at prices not consistent with a retail sales transaction.

September 28, 2012 201301010

Income from selling fertilizer products to non-agriculture industries (e.g., automotive) if the products could be used for agriculture purposes; no sales to end users.

November 5, 2012 201308004

Income from providing services of engineers and technicians to the owner of equipment to compress natural gas for transportation.

December 11, 2012 201313014

Qualifying Income

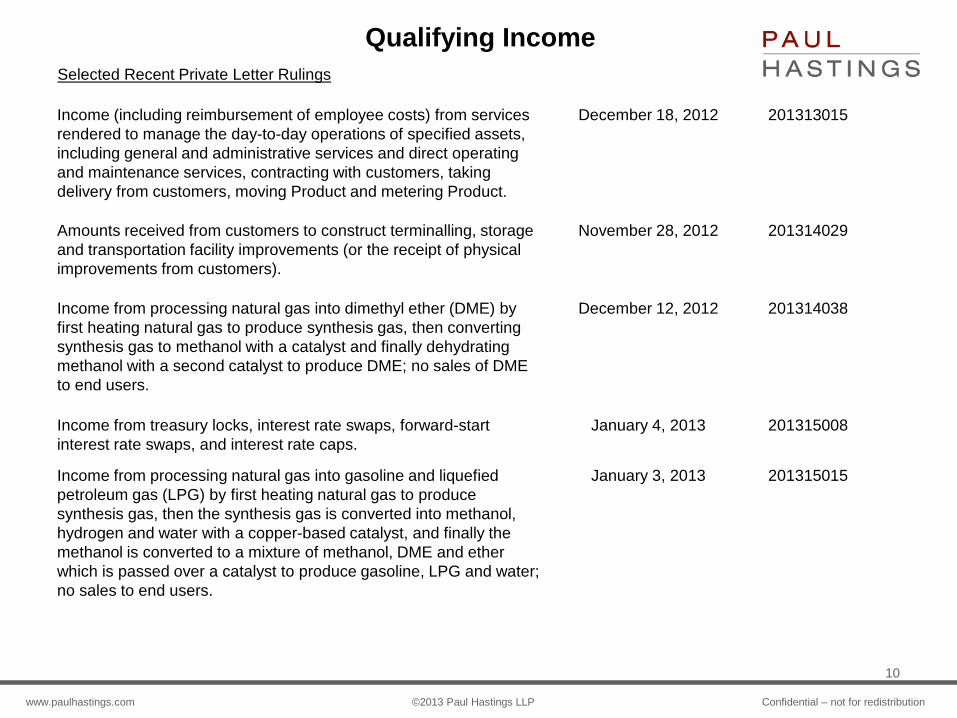

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

Selected Recent Private Letter Rulings

10

Income (including reimbursement of employee costs) from services rendered to manage the day-to-day operations of specified assets, including general and administrative services and direct operating and maintenance services, contracting with customers, taking delivery from customers, moving Product and metering Product.

December 18, 2012 201313015

Amounts received from customers to construct terminalling, storage and transportation facility improvements (or the receipt of physical improvements from customers).

November 28, 2012 201314029

Income from processing natural gas into dimethyl ether (DME) by first heating natural gas to produce synthesis gas, then converting synthesis gas to methanol with a catalyst and finally dehydrating methanol with a second catalyst to produce DME; no sales of DME to end users.

December 12, 2012 201314038

Income from treasury locks, interest rate swaps, forward-start interest rate swaps, and interest rate caps.

January 4, 2013 201315008

Income from processing natural gas into gasoline and liquefied petroleum gas (LPG) by first heating natural gas to produce synthesis gas, then the synthesis gas is converted into methanol, hydrogen and water with a copper-based catalyst, and finally the methanol is converted to a mixture of methanol, DME and ether which is passed over a catalyst to produce gasoline, LPG and water; no sales to end users.

January 3, 2013 201315015

Qualifying Income

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

Sponsor

Operating LLC

MLP

Public contributes cash to MLP in exchange for Common Units.

Sponsor contributes to the MLP operating assets and interests in flow-through entities that own operating assets.

The MLP transfers assets and LLC interests to Operating LLC.

The MLP issues MLP equity interests (GP interest, Common Units and Subordinated Units) to Sponsor. The MLP may also assume (and refinance) debt of the Sponsor and may pay cash to the Sponsor.

Assets and LLC Interests

Cash Debt Assumption General Partner Interest Subordinated Common Units Common Units

Assets and

LLC Interests

11

Public

Common Units

Cash

MLP Capitalization

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

Asset Drop Down

• Sponsor should drop down directly-owned assets and assets owned by flow-through entities.

• Sponsor should avoid dropping down stock in a C Corporation.

• If the MLP issues only MLP equity to the Sponsor, the drop-down is generally tax-free.

• If the MLP issues MLP equity and pays cash to the Sponsor for the drop down assets, the cash is generally taxable except to the extent that the cash reimburses the Sponsor for acquisition and development costs incurred by the Sponsor with respect to the contributed assets during the 24 months ending with the date of the drop down (the “CapEx Exception”).

• The CapEx Exception only applies to the extent the cash received does not exceed 20% of the fair market value of the contributed assets.

• If the MLP assumes debt of the Sponsor (and refinances that debt), the Sponsor is generally treated as recognizing gain to the extent of the debt assumed by the MLP, unless:

• The debt was incurred to purchase or improve the contributed asset;

• The debt constitutes trade payables associated with the contributed assets; or

• The Sponsor remains secondarily liable on the debt assumed by the MLP (or is secondarily liable on the MLP debt that refinances the assumed debt).

12

MLP Capitalization

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

$200 MM Cash

$200 MM Loan

13

$400 MM Assets

MLP

Public Sponsor

Capitalization – No Lakehead Structure

Holding Company

100%

$200 MM Cash

• MLP issues common units to Public in exchange for $200 million in cash.

• Sponsor contributes assets with a value of $400 million and tax basis of zero to MLP in exchange for common units and $200 million in cash.

• Sponsor loans $200 million to Holding Company.

• Gain Calculation:

Amount Realized $200MM Less: Tax Basis ($0MM) Gain $200MM

MLP Capitalization

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

$200 MM Cash

14

$400 MM Assets

MLP

Public Sponsor

Capitalization with Lakehead Structure

Holding Company

100%

• MLP issues common units to Public in exchange for $200 million in cash.

• Sponsor contributes assets with a value of $400 million and tax basis of zero to MLP in exchange for common units.

MLP Capitalization

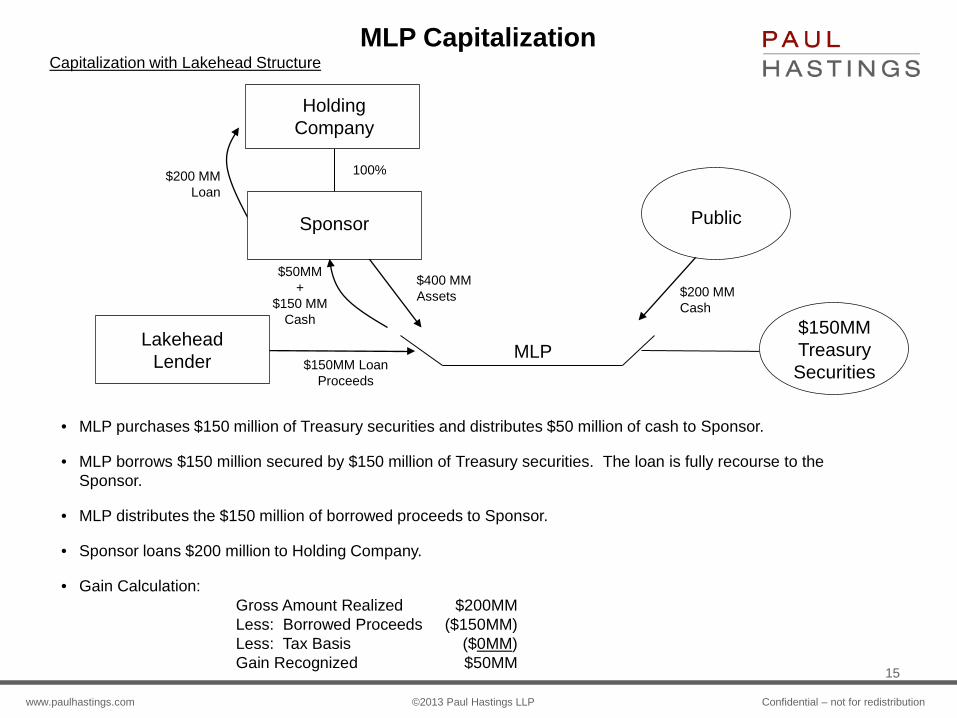

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

$150MM Loan Proceeds

$50MM +

$150 MM Cash

$200 MM Cash

$200 MM Loan

15

$400 MM Assets

MLP

Public Sponsor

Capitalization with Lakehead Structure

Holding Company

100%

• MLP purchases $150 million of Treasury securities and distributes $50 million of cash to Sponsor.

• MLP borrows $150 million secured by $150 million of Treasury securities. The loan is fully recourse to the Sponsor.

• MLP distributes the $150 million of borrowed proceeds to Sponsor.

• Sponsor loans $200 million to Holding Company.

• Gain Calculation:

Gross Amount Realized $200MM Less: Borrowed Proceeds ($150MM) Less: Tax Basis ($0MM) Gain Recognized $50MM

$150MM Treasury Securities

Lakehead Lender

MLP Capitalization

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

16

• The deferred tax is recognized when Sponsor sells its interest in the MLP – the debt amount is included in Sponsor’s amount realized.

• The deferred tax is also recognized when the MLP makes a principal payment on the debt – a principal payment is a deemed cash distribution to Sponsor.

• Lakehead structure should be used when the MLP contemplates refinancing the Lakehead debt and selling the Treasury securities to make future capital expenditures.

• The Sponsor should have sufficient assets to support its recourse liability to the Lakehead lender – the Sponsor loans the proceeds to the Holding Company instead of paying a dividend to the Holding Company. Canal Corp. v. Commissioner, 135 T.C. 199 (2010).

MLP Capitalization

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

• MLP typically provides tax shield to the public investors.

• Tax shield means the amount of taxable income allocated to the investor per dollar of cash distributed to the investor.

• Depending on the particular industry, the taxable income may be 20% or less of distributable cash. In the case of $1.40 MQD per Common Unit per year referred to above, the taxable income allocated per Common Unit would typically not exceed $0.28 per year.

• Tax Shield is made possible by tax deductions not obtained through the current expenditure of cash.

• Examples of non-cash deductions are depletion, depreciation and amortization of goodwill.

• The MLP S-1 disclosure usually gives the public investors a projection of their tax shield over a 2-year period.

17

Tax Shield

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

Assets $500 FMV $100 Basis

10-year remaining tax life

$500 Cash

• The public investors are entitled to tax deductions attributable to their share of the MLP’s assets equal to the deductions that would be allocated to them if the MLP assets had a tax basis equal to the fair market value of those assets.

• Under the remedial allocation method (which all MLPs are required to use) the first step is to allocate all MLP tax deductions to the public so that they are allocated deductions equal to what those deductions would have been if the assets had a tax basis equal to their value.

• If there is not enough tax basis to provide a full share of tax deductions to the public investors, the MLP nevertheless supplements those deductions with remedial deductions and allocates phantom income to the Sponsor in the same amount.

• Example

18

Remedial Allocations

MLP

Public Sponsor

• Assume the public contributes $500 in cash for a 50% interest in the MLP and that the Sponsor contributes assets with a fair market value of $500 for a 50% interest in the MLP. Assume further that the contributed assets have a $100 tax basis and a remaining tax life of 10 years.

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

• Assume the public contributes $500 in cash for a 50% interest in the MLP and that the Sponsor contributes assets with a fair market value of $500 for a 50% interest in the MLP. The public’s cash is used to repay debt.

• Assume further that the contributed assets have a $100 tax basis and a remaining tax life of 10 years.

• The public is entitled to an annual tax deduction of $50 using the straight-line method ($500 ÷ 10).

19

Remedial Allocations

$0 tax deductions $40 remedial income $50 book deductions

MLP

Public Sponsor

$10 tax deductions $40 remedial deductions $50 book deductions

Book Deductions $500 ÷ 10 = $50/yr. Tax Deductions $100 ÷ 10 = $10/yr.

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

• The MLP only has $10 of tax deductions available ($100 ÷ 10) and allocates all of those tax deductions to the public.

• The MLP then allocates an additional $40 of remedial deductions to the public, giving them a total of $50 of deductions ($10 of actual tax deductions and $40 of remedial deductions).

• The MLP allocates $40 of phantom income to the Sponsor to balance out the public’s $40 of remedial deductions.

• The remedial income allocations need to be modeled to make sure that there are no unanticipated phantom income effects on the Sponsor.

• The remedial allocations operate to cause the Sponsor to recognize the built-in gain in the contributed asset that is attributable to the percentage interest held by the public and to recognize that built-in gain over the remaining tax life of the contributed asset.

20

Remedial Allocations

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

21

Mergers & Acquisitions

Kinder Morgan Energy Partners LP (KMP)

KMP Public

Kinder-Morgan – Copano Merger Structure

CPNO Public

Kinder Morgan GP

Copano Energy LLC (CPNO)

Merger of two flow-through entities.

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

KMP Shares

CPNO Shares

merger

22

Mergers & Acquisitions

Kinder Morgan Energy Partners LP (KMP)

KMP Public

Kinder-Morgan – Copano Merger Structure

CPNO Public

Kinder Morgan GP

Copano Energy LLC (CPNO) Merger Sub LLC

Exchange is tax-free except to account for a deemed distribution in excess of basis for the excess of a partner’s share of the pre-merger Copano nonrecourse debt, over the partner’s share of post-merger Kinder-Morgan nonrecourse debt.

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

10% 90%

23

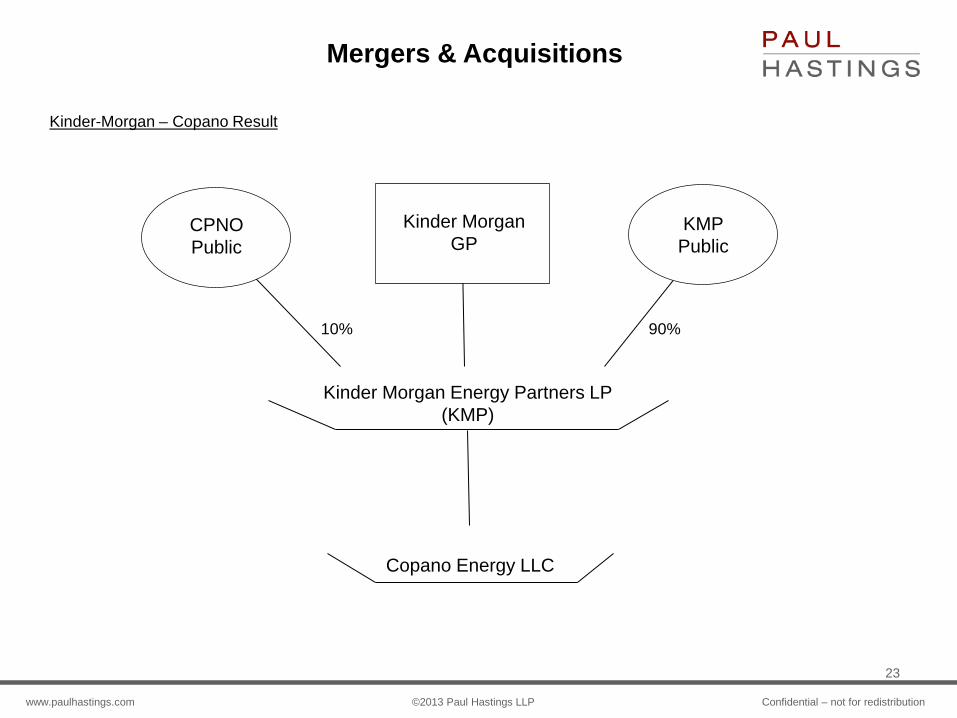

Mergers & Acquisitions

KMP Public

Kinder-Morgan – Copano Result

CPNO Public

Kinder Morgan GP

Copano Energy LLC

Kinder Morgan Energy Partners LP (KMP)

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

24

Mergers & Acquisitions

Energy Transfer Partners – Sunoco Merger Structure

ETP Public ETP GP

Energy Transfer Partners LP (ETP)

SXL Public Sunoco Logistics

GP

Sunoco Logistics LP (SXL)

Sunoco (SUN)

SUN Public

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

SUN Shares

ETP Shares

25

Mergers & Acquisitions

SUN Public

Energy Transfer Partners – Sunoco Merger

ETP Public

Energy Transfer Partners LP (ETP)

Sunoco (SUN)

ETP GP

Merger Sub Inc.

Tax-free contribution of SUN shares to ETP in exchange for SUN shares.

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

26

Mergers & Acquisitions

SXL Public

Energy Transfer Partners – Sunoco Merger

SUN Public

Energy Transfer Partners LP (ETP)

ETP GP

ETP Public

Sunoco

Sunoco GP

Sunoco Logistics LP

Dividends and interest from Sunoco are qualified income. But, Sunoco must pay corporate tax on its earnings and there is no tax shield on the dividends and interest.

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

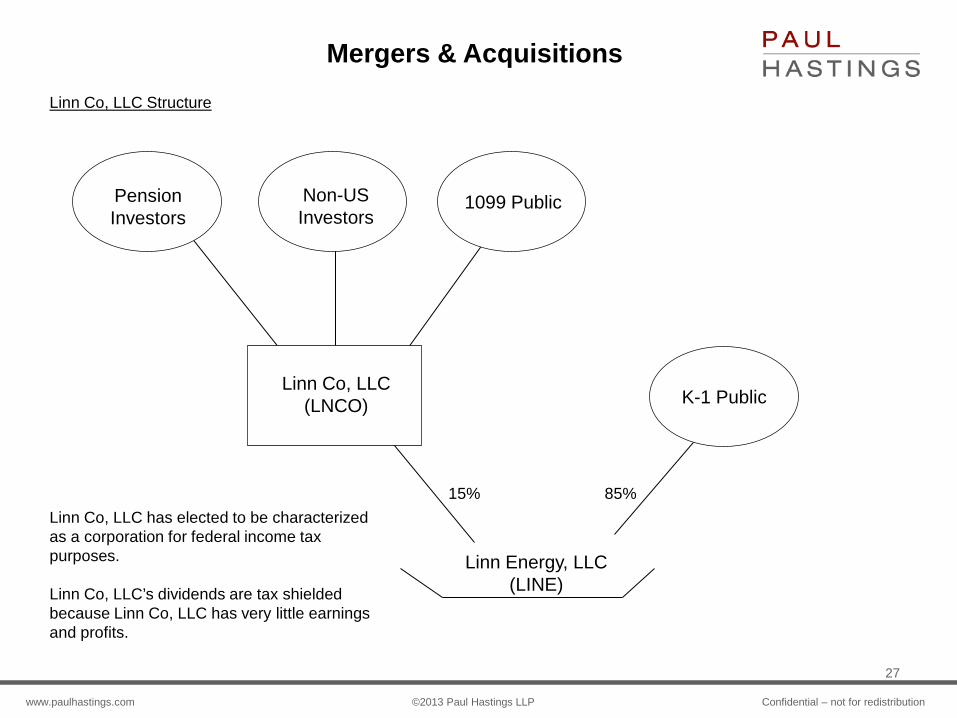

15% 85%

27

Mergers & Acquisitions

Linn Energy, LLC (LINE)

K-1 Public

Linn Co, LLC Structure

1099 Public Pension Investors

Non-US Investors

Linn Co, LLC (LNCO)

Linn Co, LLC has elected to be characterized as a corporation for federal income tax purposes. Linn Co, LLC’s dividends are tax shielded because Linn Co, LLC has very little earnings and profits.

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

merger

28

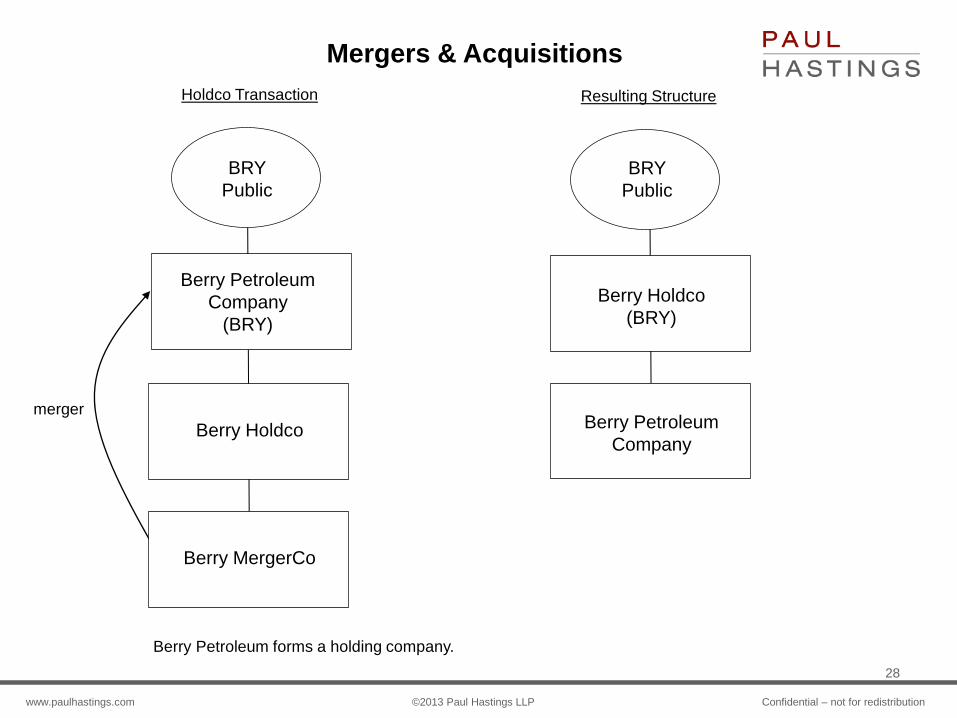

Mergers & Acquisitions Holdco Transaction

BRY Public

Berry Petroleum Company

(BRY)

Berry Holdco

Berry MergerCo

Resulting Structure

BRY Public

Berry Holdco (BRY)

Berry Petroleum Company

Berry Petroleum forms a holding company.

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

29

Mergers & Acquisitions

Berry Holdco (BRY)

Berry Petroleum Company

Berry Holdco (BRY)

Berry Petroleum LLC

Berry HoldCo causes Berry Petroleum to liquidate for federal income tax purposes by causing Berry Petroleum to convert to a limited liability company treated as a disregarded entity. The holding company formation and the liquidation effect an F Reorganization for federal income tax purposes.

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

merger

30

Mergers & Acquisitions

Linn Energy, LLC (LINE)

Berry Petroleum LLC

BRY Shareholders

Berry Holdco (BRY)

Linn Co, LLC (LNCO)

MergerCo LLC

LINE K-1 Public

Berry Petroleum Acquisition

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

31

Mergers & Acquisitions

100%

Linn Energy, LLC (LINE)

Berry Petroleum LLC

Linn Co, LLC (LNCO)

LINE K-1 Public

Old LNCO Public

BRY Public

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

Shares of Berry Petroleum LLC

32

Mergers & Acquisitions

LINE Shares

Linn Co, LLC (LNCO)

Linn Energy, LLC (LINE)

Linn Co, LLC contributes all of the shares of Berry Petroleum LLC to Linn Energy, LLC in exchange for new shares of Linn Energy, LLC.

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

65% 35%

100%

33

Mergers & Acquisitions

Linn Energy, LLC (LINE)

LINE K-1 Public

Linn Co, LLC Structure

1099 Public Pension Investors

Non-US Investors

Linn Co, LLC (LNCO)

Berry Petroleum LLC

Old BRY Shareholders

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

The combination of the remedial allocation method and the built-in gain in the Berry Petroleum assets will cause Linn Co, LLC to lose tax deductions or recognize remedial taxable income over the life of the Berry Petroleum properties.

To compensate Linn Co, LLC for Linn Co, LLC’s increased taxes, Linn Energy, LLC will distribute to Linn Co, LLC $6 million per year in cash in each of 2013, 2014, and 2015.

Further, any sale of the Berry Petroleum, LLC assets in the 7 years following the closing must be approved by a committee of independent directors of Linn Co, LLC.

34

Remedial Allocation Issues

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

35

IRS Circular 230 Disclaimer: As required by U.S. Treasury Regulations governing tax practice, you are hereby advised that any written tax advice contained herein was not written or intended to be used (and cannot be used) by any taxpayer for the purpose of avoiding penalties that may be imposed under the Internal Revenue Code.

www.paulhastings.com ©2013 Paul Hastings LLP Confidential – not for redistribution

36