tax counselor quick reference guide -...

TRANSCRIPT

The Ohio Benefit BankTax Counselor Quick Reference Guide

November 2015Version 1.5

TM

The Ohio Benefit Bank (OBBTM) Counselor Support Website:support.ohiobenefits.org

Contents

Websites & Login Information for the OBB .......................................................................iv

Your First Tax Appointment .................................................................................................v

Section One | Getting Started with The Ohio Benefit BankWorking Together: Network Roles ..................................................................................... 8

Your Role as an OBB Counselor ........................................................................................ 8

Counselor Support Website ............................................................................................... 9

The Online Service ...........................................................................................................10

Understanding the Counselor Homepage ......................................................................11

QuickCheck .......................................................................................................................12

Client Creation ..................................................................................................................13

Client Login and Agreements ..........................................................................................14

Where to Find Help ..........................................................................................................15

Section Two | Income Tax SpecificsIntroduction to Income Taxes .......................................................................................... 17

Filing Status ......................................................................................................................18

Qualifying Children ...........................................................................................................20

Qualifying Relatives ..........................................................................................................22

Qualifying Person Decision Tree ......................................................................................23

Income ..............................................................................................................................24

Sample Income Forms .....................................................................................................25

Adjustments and Deductions ..........................................................................................29

The Affordable Care Act ...................................................................................................31

Tax Credits ........................................................................................................................34

Filing Your Return .............................................................................................................36

After Filing ......................................................................................................................... 37

Accessing the Training Website .......................................................................................38

Page iv

Websites & Login Information for the OBB

Your Counselor Loginsuppport.ohiobenefits.org

Login Name:

Password:

Training Logintraining.thebenefitbank.org

Login Name: oh_____

Password: tbb12345

Important Contact Information

The Benefit Bank® Help Desk 1.855.TBB.HELP (855.822.4357)

The Ohio Association of Foodbanks 614.221.4336http://ohiofoodbanks.org

The Ohio Benefit Bank Counselor [email protected]://support.ohiobenefits.org

Ohio State Legal Services 1.866.529.6446

Helpful Websites

Job and Family Services Information Centerhttp://jfs.ohio.gov/ocomm_root/0001InfoCenter.stm

Locate your Community Action Agencyhttp://development.ohio.gov/is/is_epp_locate.htm

Check the status of a HEAP applicationhttps://portal.ocean.ohio.gov/OCEANClientPortal/IVRAuthorization.aspx

FAFSA PIN Retrievalwww.pin.ed.gov

Ohio | Benefitswww.benefits.ohio.gov/

Ohio Medicaid Hotlinewww.ohiomh.com

Page iv Page v

Your First Tax Appointment

Your first tax appointment as a counselor with The Ohio Benefit Bank is an important milestone where you can finally apply the knowledge you’ve gained through training. Below, we’ve outlined the steps to a successful tax appointment to help get you started.

Steps to a Successful Tax Appointment

1. Client’s first contact with the OBB2. Pre-screen the client’s income and documentation3. Read & review the Terms and Conditions of Use4. Log into your counselor account

• Go to support.ohiobenefits.org• Click counselor log in• Enter your login and password

5. Create a new client account or log into an existing account6. Click filing this year’s taxes7. Complete each section of the return8. Review and print each return9. Review any necessary next steps10. Provide the client with your organization’s contact information

Section OneGetting Started with The Ohio Benefit BankOverview

Each year, more than $2.2 billion in tax credits and work support programs go unclaimed by Ohioans. Nearly 95 percent of these dollars are federal funds and must be returned for re-allocation to other states or programs.The Ohio Benefit Bank (OBB) strives to assist Ohioans in accessing these dollars as:

▪ They are revenue for our local economies. ▪ They help stabilize families. ▪ They help low and moderate-income people overcome the devastating effects of poverty.

Implementation

The Ohio Benefit Bank is a program of the Ohio Association of Foodbanks and is implemented through a public-private partnership between the State of Ohio, four federal agencies, eight state agencies, and over 1,200 faith-based and community organizations across Ohio. Since inception in 2006, the OBB has connected over hundreds of thousands of Ohioans with more than $1.42 billion in tax credits and potential benefits, infusing federal dollars into local economies.Key Features

▪ Internet-based ▪ Question-guided ▪ Counselor-assisted ▪ An eligibility estimator and application completion tool ▪ Secure and confidential ▪ Built in expertise so you do not need to be a benefits or tax expert to make an impact ▪ Easy to use, simple instructions, no math required

Page 7

Working Together: Network Roles

Solutions for Progress “The Benefit Bank” The State of Ohio

Funding and SupportTBB Programming & Maintenance, Help Desk

Lead Agencies

Ohio Association of FoodbanksLead Agency, Training, Grants, Coordination and Marketing

Your Role as an OBB CounselorAn OBB Counselor DOES:

▪ Provide a welcoming and safe environment for client sessions

▪ Show all clients courtesy and respect ▪ Complete required training ▪ Attend update training, including tax year

refresher training ▪ Verify client identity, if required ▪ Interview the client and enter responses into

The Benefit Bank ▪ Provide a printed copy of client forms

An OBB Counselor DOES NOT:

▪ Sign client forms or tax returns ▪ Charge for services, solicit or accept donations

for OBB services ▪ Help clients make decisions ▪ Steer clients toward a certain choice ▪ Store client applications, client documentation,

or client login names or passwords, on site, on a computer, or on a computer server

▪ Choose or enter client passwords and security questions

▪ Determine final eligibility on programs for which a client applies

▪ Enter counselor information such as phone number or email address into client forms

Section One • Page 9

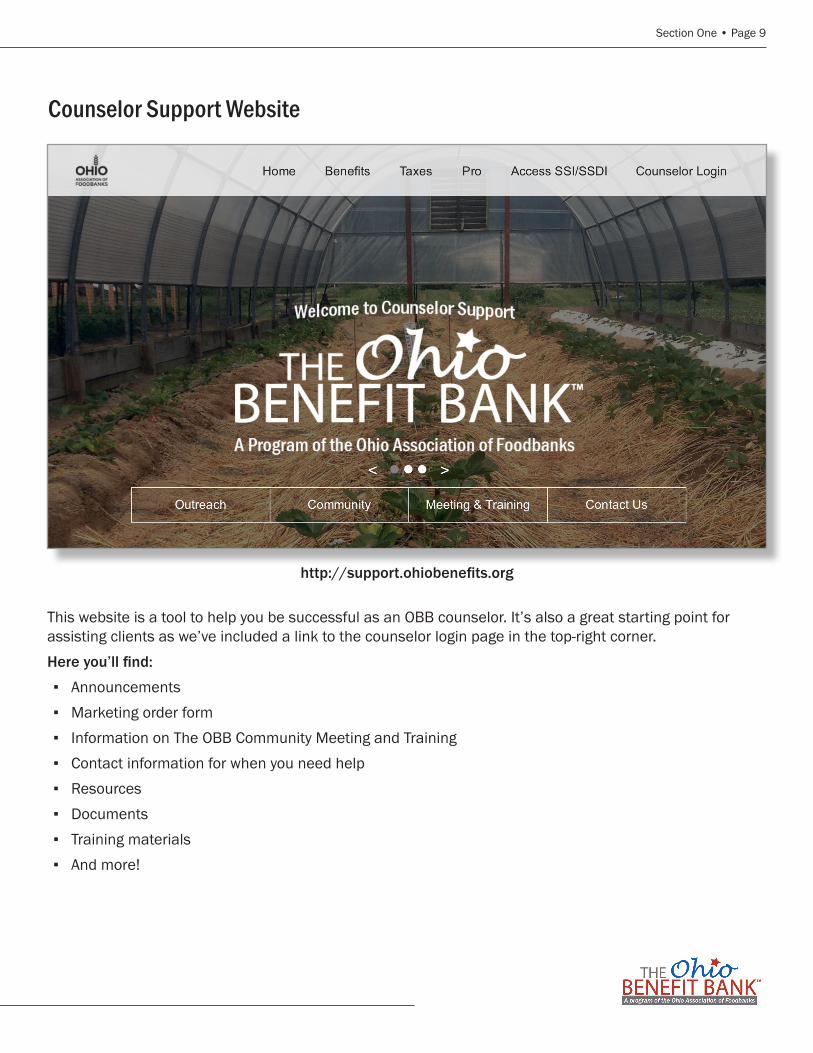

Counselor Support Website

This website is a tool to help you be successful as an OBB counselor. It’s also a great starting point for assisting clients as we’ve included a link to the counselor login page in the top-right corner.Here you’ll find:

▪ Announcements ▪ Marketing order form ▪ Information on The OBB Community Meeting and Training ▪ Contact information for when you need help ▪ Resources ▪ Documents ▪ Training materials ▪ And more!

http://support.ohiobenefits.org

Page 10 • Section One

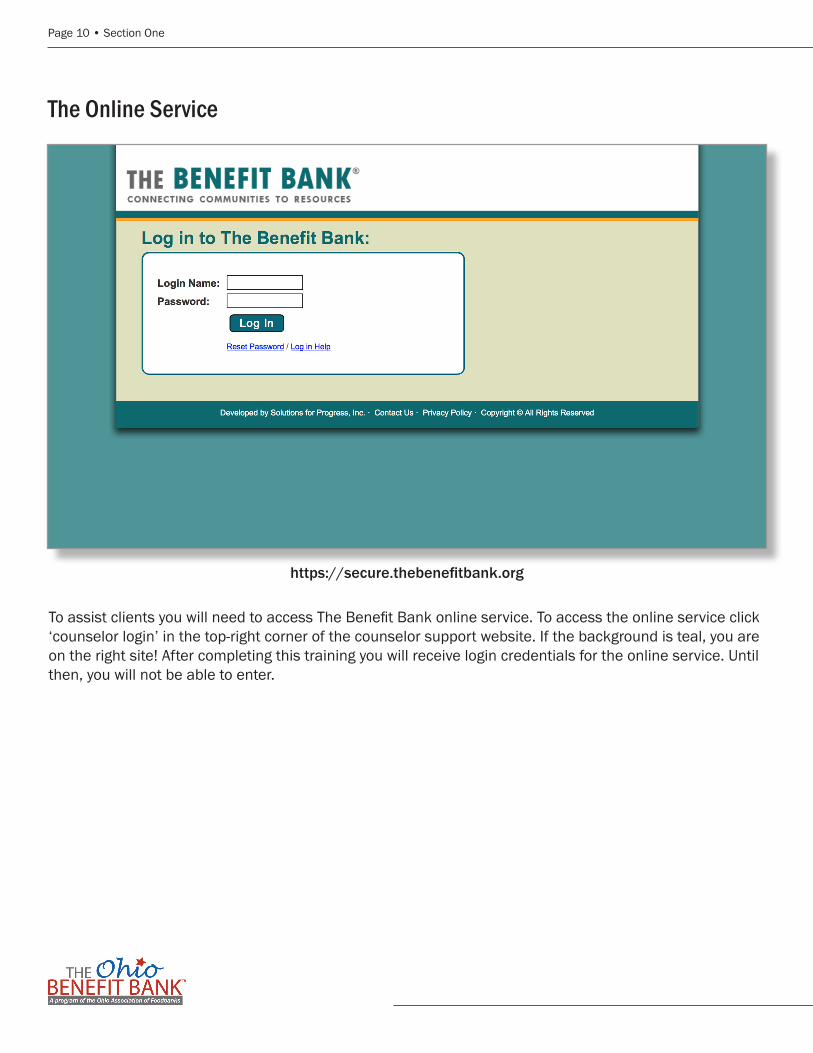

The Online Service

https://secure.thebenefitbank.org

To assist clients you will need to access The Benefit Bank online service. To access the online service click ‘counselor login’ in the top-right corner of the counselor support website. If the background is teal, you are on the right site! After completing this training you will receive login credentials for the online service. Until then, you will not be able to enter.

Section One • Page 11

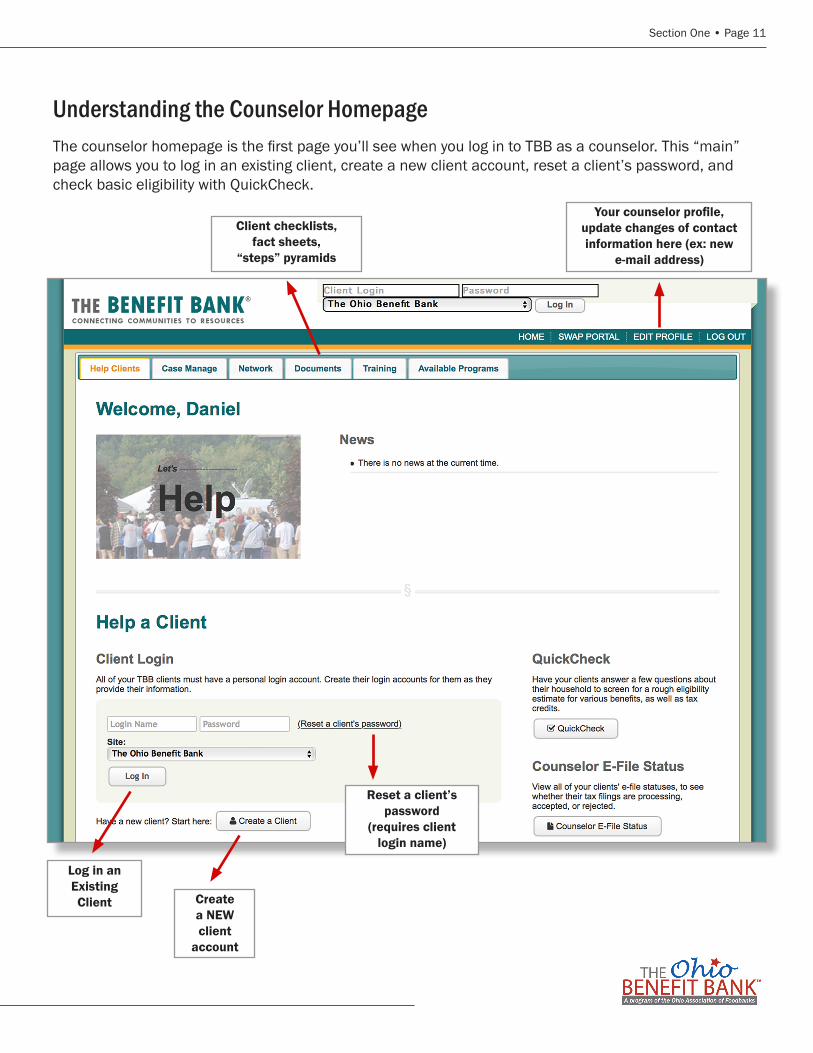

Understanding the Counselor HomepageThe counselor homepage is the first page you’ll see when you log in to TBB as a counselor. This “main” page allows you to log in an existing client, create a new client account, reset a client’s password, and check basic eligibility with QuickCheck.

Client checklists, fact sheets,

“steps” pyramids

Your counselor profile, update changes of contact information here (ex: new

e-mail address)

Create a NEW client

account

Log in an Existing Client

Reset a client’s password

(requires client login name)

Page 12 • Section One

QuickCheckQuickCheck is a tool you can use to estimate a client’s potential eligibility for various benefits and work support programs within a few minutes.Advantages of QuickCheck:

▪ You do not have to be an OBB counselor to use QuickCheck ▪ Very little personal information is required and it will not be saved ▪ You can use QuickCheck as a pre-screening tool before scheduling a counseling session with a client

How to Use QuickCheck

5. The amount of stars under a program or tax credit indicates how likely a person is to be eligible.

Two or more stars generally indicates a good possibility that a person would qualify for the program or tax credit.

2. Choose Ohio and click “Continue” 3. Enter each household member separately

4. Enter client’s household information and click “Finish”

1. Select “QuickCheck” from the counselor homepage

Section One • Page 13

Client Creation

Each OBB client must have their own personal account for the online service. Counselors structure the client login and clients choose their own password, security question, and answer.It is important that counselors:

▪ Have each client write down their login and password ▪ Standardize the structure of each client login (For example: <first initial of first name><last name> or

tsmith) ▪ Let clients know that passwords are case sensitive, must be 8 characters long, and contain both letters

and numbers ▪ Allow client to enter their own password, security question, and answer

Page 14 • Section One

Client Login and Agreements

Allow the Client to LoginWhen you have successfully created the client account, you will return to the counselor portal page and see a red confirmation message saying the account has been created.

You can then log into the client account. When assisting clients please enter the login and allow the client to enter his/her password.

Terms and Conditions of UseThe Terms and Conditions of Use contain protections for the client, the counselor, and the counselor’s organization. Clients must agree to these terms to use the online service. It may be a good idea to have several copies of this document pre-printed. It is available under the documents tab on the Counselor Portal Page.

Consent to Contact and Share InformationThe OBB works hard to keep client contact information private and secure. We do not sell or provide clients’ contact information to anyone. However, occasionally staff may reach out to clients to offer information about new programs and gather feedback on their experience using The Benefit Bank. Also, our staff sometimes works with other organizations to find ways to improve services. To do this, we may share client information with an outside educational institution for research purposes only. Clients may say yes or no to this question. Whatever they decide will have no effect on their eligibility for services.

Section One • Page 15

Where to Find Help

Glossary Terms and Clarifying QuestionsThe online service contains glossary terms and clarifying questions throughout each application module. Glossary terms are single words or terms that appear as blue hyperlinks. Click to view a definition or clarifying text. Clarifying questions are blue hyperlinks preceded by a question mark icon. These questions will appear on the same page as the topic they help to clarify.

The Help DeskOur partners who maintain the online service provide a Help Desk that responds to phone and e-mail inquiries from counselors. The Help Desk is available for support as you assist clients.Contact the Help Desk when:

▪ You forget your login and/or password ▪ Your client forgets their login and/or password ▪ The online service is not responsive or behaving unexpectedly ▪ You need help finding answers to client questions

Contact the Help Desk1-855-TBB-HELP1-855-822-4357

[email protected](response within 2 business days)

Hours During Tax Season9 AM - 8PM M-F9 AM - 5 PM SaNormal Hours

9 AM - 5 PM M-F

Page 17

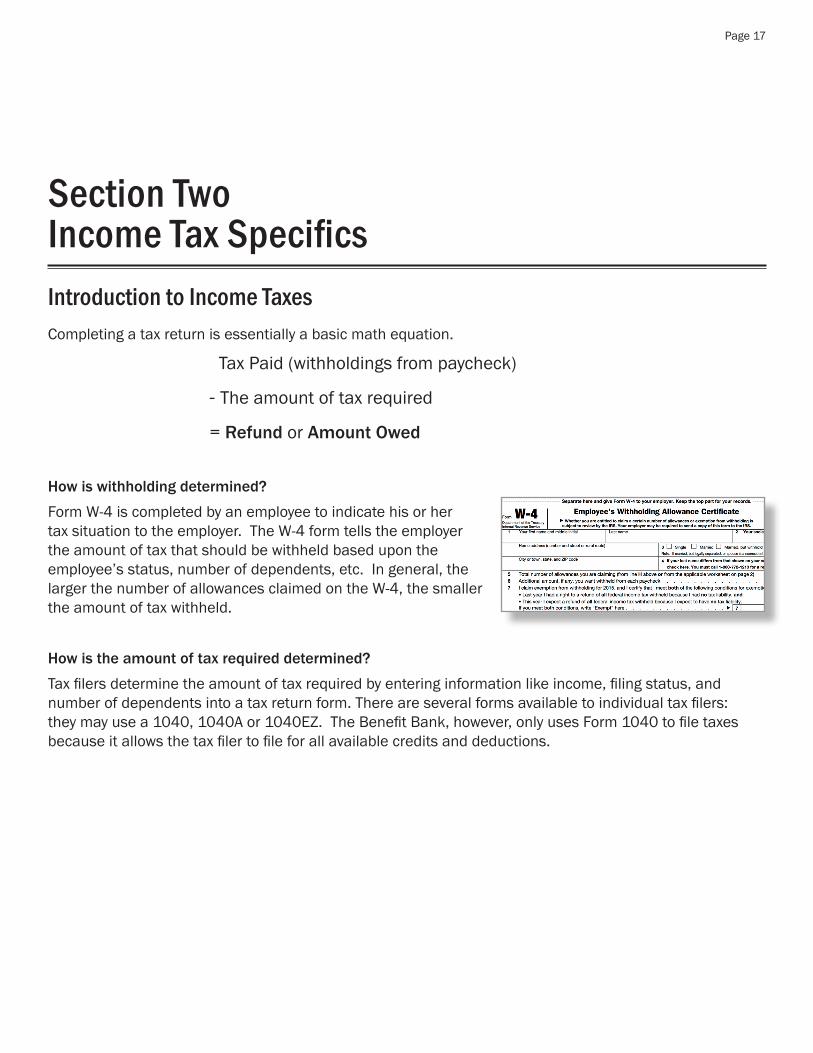

Section TwoIncome Tax SpecificsIntroduction to Income TaxesCompleting a tax return is essentially a basic math equation.

How is withholding determined?

Form W-4 is completed by an employee to indicate his or her tax situation to the employer. The W-4 form tells the employer the amount of tax that should be withheld based upon the employee’s status, number of dependents, etc. In general, the larger the number of allowances claimed on the W-4, the smaller the amount of tax withheld.

How is the amount of tax required determined?

Tax filers determine the amount of tax required by entering information like income, filing status, and number of dependents into a tax return form. There are several forms available to individual tax filers: they may use a 1040, 1040A or 1040EZ. The Benefit Bank, however, only uses Form 1040 to file taxes because it allows the tax filer to file for all available credits and deductions.

Tax Paid (withholdings from paycheck)

- The amount of tax required

= Refund or Amount Owed

Page 18 • Part Two

Filing Status

Your client’s filing status will determine the amount of their standard deduction as well as the tax credits for which they may be eligible. There are five filing statuses: single, married filing jointly, married filing separately, head of household, and qualifying widow(er) with a dependent child.

SingleThe single filing status is for people who are unmarried. A taxpayer can claim single when they meet one of the following requirements:

▪ Unmarried on December 31st of the tax year ▪ Legally separated on December 31st of the tax year

Married Filing JointlyMarried filing jointly is used by couples who were married on or before December 31st of the tax year. This status will increase both the standard deduction and the income limits for credits like the Earned Income Tax Credit. Taxpayers can claim married filing jointly if any of the following apply:

▪ They were married on or before December 31st of the tax year ▪ Their spouse died during the tax year and they did not remarry during the tax

year

Married Filing SeparatelyMarried filing separately is used by couples who were married on or before December 31st of the tax year who want to complete their taxes on their own. Clients who choose to file married filing separately will not be eligible for the Earned Income Tax Credit and may pay more in taxes. If your client wants to avoid the financial liabilities of their spouse they may be able to file a joint return by mail and include form IRS-8379, the injured spouse allocation.

Part Two • Page 19

Head of HouseholdThe head of household filing status offers tax filers who are single or considered single and have dependents a significantly higher deduction on their taxes and may dramatically increase their tax refund. To claim head of household the tax filer must:

▪ Have a qualifying child or relative; ▪ Be unmarried or considered unmarried; ▪ And have paid over half the cost of keeping up the home

Qualifying Widow(er) with a Dependent Child The qualifying widow or widower with a dependent child filing status is for individuals whose spouse died within the last two tax years and they did not remarry before December 31st of the tax year. They must also claim at least one dependent to be eligible for this filing status.

Page 20 • Part Two

Qualifying ChildrenA qualifying child can be used for the following purposes on a tax return:

▪ Head of Household ▪ Dependency ▪ Child and Dependent Care Credit ▪ Child Tax Credit ▪ Additional Child Tax Credit ▪ Earned Income Tax Credit

There are five tests a child must pass to be considered a Qualifying Child: Relationship, Age, Support, Joint Return and Residency.

Relationship Test

To pass this test, the child must be your son, daughter, stepchild, eligible foster child, brother, sister, stepbrother, stepsister, or a descendant of any of them (for example, your grandchild, niece, or nephew).

Age Test

The age test varies from credit to credit. View the box below to see how old the child must be to qualify for a specific credit.

Head of HouseholdDependency

Earned Income Tax Credit

Child and Dependent Care Credit

Child Tax CreditAdditional Child Tax

Credit ▪ Under 19

▪ Under 24 if a full time student

▪ Any age if permanently and totally disabled

▪ Under 13

▪ Any age if permanently and totally disabled

▪ Under 17

Part Two • Page 21

Support Test

The child cannot have provided more than half of their total support during the tax year. This means that this child must not be paying for a majority of things associated with maintaining themselves. This includes shelter, food, and utilities. Note: A child does not have to pass the Support test for the Earned Income Tax Credit.

Joint Return Test

The child may not file a joint tax return with anyone.

Residency Test

To pass this test, the child must have lived with you for more than half the year. Temporary absences such as school, vacation, business, medical care, military service, or detention in a juvenile facility DO count as time lived at home.A child who is born or died during the year is considered to have lived with you for the entire year.Note: A child of divorced or separated parents may be considered the qualifying child of the noncustodial parent if certain conditions are met. Each child may only be claimed by one parent each year. When filing their taxes the noncustodial parent could claim an exemption for the child and the child tax credit but no benefits like the Head of Household filing status, Earned Income Tax Credit, and Credit for Child and Dependent Care Expenses.

Page 22 • Part Two

Qualifying RelativesTaxpayers may also claim a person who meets the criteria for a qualifying relative as a dependent. A person must pass the following tests to be considered your qualifying relative.

Member of Household or Relationship Test

A qualifying relative is a person who lived with you for the entire year OR is related.Related is defined as:

▪ child, stepchild, foster child, or descendant of any of them (like a grandchild) ▪ sibling(s), including stepbrother, stepsister, brother-in-law, or sister-in-law ▪ niece or nephew ▪ parents, including stepfather or stepmother ▪ parent’s siblings like aunt or uncle ▪ grandparents

Income Test

The qualifying relative must have had a gross income of less than $4,000 during the tax year.

Support Test

You must have provided over half of the relative’s total support during the tax year.

Citizenship/Residency Test

The relative must be a U.S. citizen, national, or resident alien or a resident of Canada or Mexico.

Joint Return Test

The relative may not file a joint tax return with anyone.

Part Two • Page 23

Qualifying Person Decision Tree

Yes

The child is your qualifying child. The child is also your

dependent.

Qualifying Child Tests Qualifying Relative Tests

The child is your son, daughter, stepchild, fosterchild, sibling,

stepsibling, or descendant of any of them.

The child is under age 19, under 24 and a full-time student, or any age if

disabled.

The child did not provide more than half of his or her own support.

The child lived with you for more than half of the tax year.

Yes

Person is a member of your household OR related (like a

parent).

Yes

Yes

Person’s income is under the income limit.

Person received more than half of his or her support from you.

No

You cannot claim this

person as a dependent.

Yes

Yes

Yes

You can claim this

person as a dependent.

NoNo

No

No

No No

No

NoPerson will not file a joint return.

Person is a U.S. citizen, U.S. resident, U.S. national, or a resident of Canada or Mexico for some part

of the year.

Yes

Yes

Yes

Person is a U.S. citizen, U.S. resident, U.S. national, or a resident of Canada or Mexico for some part

of the year.

Yes

Yes

No

Note: This is an overview of the requirements. More specific rules apply in certain cases.

Page 24 • Part Two

IncomeIncome is reported on Reporting Forms which vary depending upon the type of income being reported. The Benefit Bank does not support all types of income. TBB will ask about all forms of taxable income, but will only allow the client to move forward if each of their income types are accepted by the The Benefit Bank. Clients’ taxable income must be lower than $95,000 for joint filers or $65,000 for all other filers.

Reporting Forms Supported by TBB

W2: Wage & Tax Statement

1099INT/1099OID: Interest Income

1099MISC: Miscellaneous Income (i.e. Nonemployee or Other Income)

1099DIV: Dividends

1099R: Pensions, Annuities, IRAs, & Insurance Contracts

1098E: Student Loan Interest Statement

SSA1099: Social Security Benefit Statement

1098T: Tuition Statement

RRB1099/RRB1099R: Railroad Retirement Board Statements

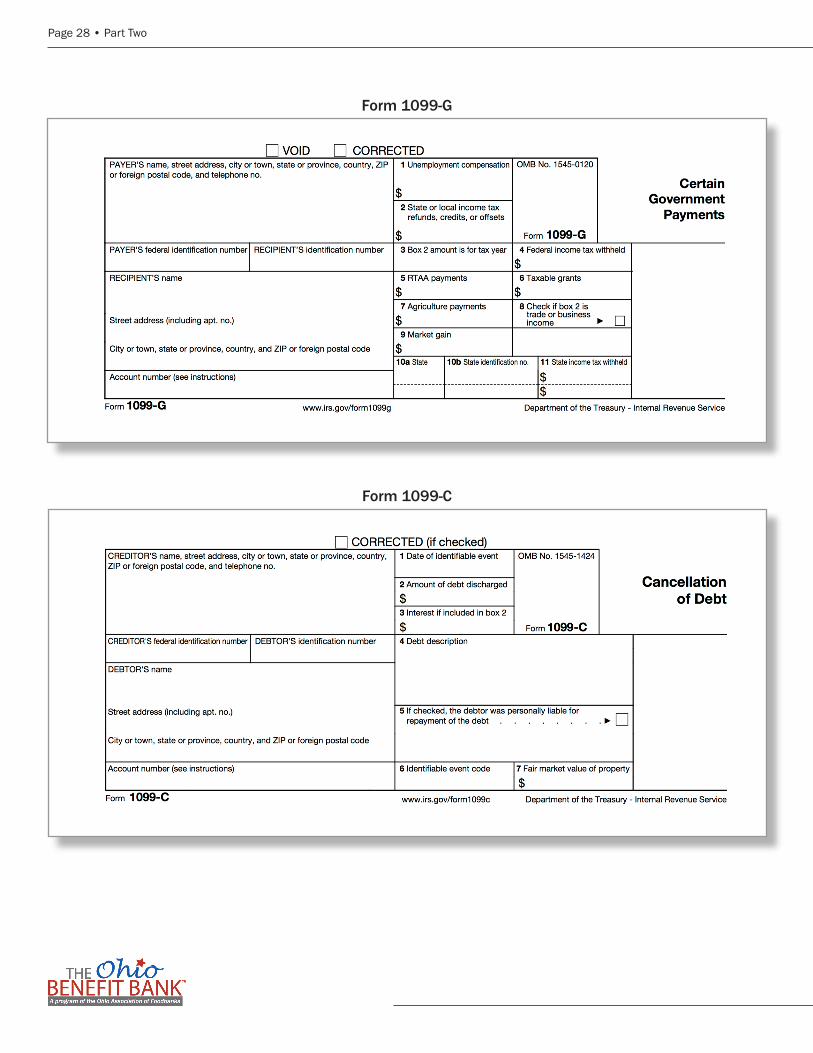

1099G: Government Payments (Unemployment or State/Local Tax Refunds)

CSA 1099R/CSF 1099R: Statement for U.S. Civil Service Retirement Benefits

W2G: Certain Gambling Winnings

5498: IRA Contribution Information

1099C: Cancellation of Debt

1098: Mortgage Interest Statement

1099SA: Health Savings Account (HSA) distribution

Income Unsupported by TBB

Business income reported on Schedule C

Tips not reported on a W-2

Rental and Real Estate Income

Capital Gains

Farm Income Income reported on a 1099-B

Codes R, P or T in box 12 of a W-2

Non-Taxable IncomeTBB will not ask about the following types of income because they are not subject to federal tax:

▪ Child Support

▪ Cash Assistance

▪ Food Assistance

▪ Supplemental Security Income (SSI)

▪ Veterans Benefits

Sample Income FormsForm W-2

Form 1099-MISC

Page 26 • Part Two

Form 1099-R

Form SSA-1099

Form 1099-INT

Form 1099-DIV

Page 28 • Part Two

Form 1099-G

Form 1099-C

Part Two • Page 29

Adjustments and Deductions

When individuals pay taxes throughout the year, they are paying an estimated tax. When you complete a tax return, you figure out if you can get some or all of that money back. You can reduce the taxes you owe through adjustments and deductions.

AdjustmentsTaxpayers can subtract certain expenses, payments, contributions, fees, and other costs from their total income, which reduces the amount they may be taxed. The figure remaining after computing the taxpayer’s adjustments to income is their Adjusted Gross Income (AGI).

Adjustments include: ▪ Alimony payments ▪ Cost of supplies teachers purchase for their classroom ▪ One half of self-employment tax paid during the tax year ▪ Tuition and school fees (Note: It is sometimes better to take these payments as a credit; TBB will

determine the best choice for you) ▪ Student loan interest payments ▪ Portion of health insurance premiums paid by individuals who are self-employed ▪ Money contributed to a traditional Individual Retirement Account (IRA) ▪ Contributions to a Health Savings Account (HSA)

DeductionsDeductions are subtracted from your AGI and they further reduce the amount of income that is taxed. Taxpayers have a choice of taking the standard deduction or itemizing deductions. Taxpayers should use the type of deduction that results in the lowest amount of tax.

Standard DeductionThe standard deduction varies depending on your filing status. The smallest deduction is for a single taxpayer and the largest is married filing jointly or qualifying widow(er) with a dependent child.

Standard Deduction

Single $6,300

Married Filing Jointly $12,600

Married Filing Separately $6,300 (each)

Head of Household $9,250

Qualifying Widow(er) with a Dependent Child $12,600

Page 30 • Part Two

Itemizing DeductionsItemizing deductions is an alternative to the standard deduction where we add up each of the qualified expenses to deduct from the taxpayer’s AGI. We only want to itemize if the total of the qualified expenses is greater than the standard deduction. Expenses that can be claimed as deductions include:

▪ State and local income taxes or sales taxes ▪ Real estate taxes paid ▪ Home mortgage interest paid ▪ Gifts to charity ▪ Gambling losses ▪ Impairment related work expenses for disabled persons ▪ Losses from casualty ▪ Un-reimbursed employment expenses ▪ Fees for tax filing ▪ Medical and dental expenses ▪ Mortgage insurance premiums

Part Two • Page 31

The Affordable Care Act

IntroductionThe implementation of the Affordable Care Act brought potentially life-saving health insurance benefits to millions of Americans in 2014. It also introduces several new intricacies to filing income taxes. The changes include new tax forms that report health coverage status, a new tax credit called the Premium Tax Credit, and penalties for not obtaining health insurance coverage.

Health Coverage StatusUnder the Affordable Care Act, you are required to have health insurance that qualifies as “minimum essential coverage” for the year. All tax filers will be responsible for reporting health coverage status for themselves and their dependents to the IRS when filing their taxes. If your clients or any of their dependents do not have minimum essential coverage, then they are responsible for paying a fee on their tax return. Some exemptions exist. Minimum essential coverage includes insurance policies through the Health Insurance Marketplace, job-based coverage, Medicare, Medicaid, CHIP, TRICARE, and certain other coverage.

Individual Shared Responsibility PaymentIf your clients or their dependents do not have insurance that qualifies as minimum essential coverage during the year, they will make an additional payment on their tax return, called the individual shared responsibility payment, unless they qualify for an exemption from the fee.

The payment to be charged will be the higher of: ▪ 2% of yearly household income. (Maximum: Total yearly premium for the national average price of a

Bronze plan sold through the Marketplace) ▪ $325 for adults and $162.50 for children under 18. (Maximum: $975)

TBB will ask questions to determine if your clients meet any of the following exemption qualifications: ▪ They are uninsured for less than 3 months of the year ▪ The lowest-priced coverage available to them would cost more than 8% of their household income ▪ They don’t have to file a tax return because their income is too low (this exemption still applies even if

they choose to file a tax return) ▪ They are a member of a federally recognized tribe or eligible for services through an Indian Health

Services provider; a recognized health care sharing ministry; or a recognized religious sect with religious objections to insurance, including Social Security and Medicare

▪ They are incarcerated and not being held pending disposition of charges ▪ They are not lawfully present in the U.S. ▪ They have a hardship exemption which affects their ability to purchase health insurance coverage (this

is decided on an individual basis)

Page 32 • Part Two

Your clients will need to apply for an exemption for all instances except for being uninsured for less than 3 months or if their income is low enough that they are not required to file taxes. These exemptions automatically apply when they file their taxes. To apply for an exemption, go to healthcare.gov or call 1-800-318-2596. If your clients have applied for and have been granted an exemption, the Marketplace will mail a unique exemption certificate number (ECN) that they will need for tax filing.

If clients were uninsured for three months or more, 1/12 of the yearly fee will apply to each month that they were uninsured.

TBB will determine if clients are responsible for paying a fee on their return. If so, TBB will calculate the total amount owed. The fee will be included on Form 1040 and will either reduce the refund or increase the amount of tax owed.

Premium Tax CreditIf your clients get health insurance coverage through the Health Insurance Marketplace, they may be eligible for the Premium Tax Credit. Clients can choose to receive the credit in advance, called the Advanced Premium Tax Credit (APTC), or get the credit when they file taxes. This credit can help make health insurance coverage more affordable for individuals with low to moderate incomes.

They may be eligible for a credit if they meet all of the following: ▪ Bought health insurance through the Marketplace ▪ Are ineligible for coverage through an employer or government plan ▪ Are within certain income limits ▪ Will not file a Married Filing Separately tax return (except in certain instances of domestic abuse and

spousal abandonment) ▪ Cannot be claimed as a dependent by another person

If your clients are eligible for the Premium Tax Credit, TBB will calculate the total credit amount and this will be included on their tax return.

Claiming the CreditIf your client chose to get the credit in advance: Money is paid throughout the year directly to the insurance company to lower their out-of-pocket monthly premiums. When they file their taxes, the total amount of payments that were sent to the health insurance provider during the year will be subtracted from the total amount of the premium tax credit that is calculated on the return. If the calculated total credit is more than the advanced payments made for your client, then the difference will either increase the refund or lower the amount of taxes owed. If the calculated credit is less than the advance payments made to your client’s insurance company, then the difference will either decrease the refund or increase the amount of taxes owed. TBB will reconcile the amount of your client’s credit and calculate the final credit amount on their tax return.

If your client chose to get the credit later: They will receive the credit all at once when they file their taxes;

Part Two • Page 33

this will either increase the refund or lower the amount of taxes owed. TBB will calculate the total credit amount and this will be included on the tax return.

The amount of your client’s Premium Tax Credit may be different from what was projected when they applied for health coverage if they had a change in income, household size, or filing status. Clients should always report these changes to the Health Insurance Marketplace when they happen in order to help get the proper type and amount of financial assistance. This will help ensure that the amount received in advance is not too much or too little.

IRS Forms used to report health coverage and calculate the credit1095-A Health Insurance Marketplace Statement: This reporting form will be sent to you if you or a family member is enrolled in health insurance coverage through the Health Insurance Marketplace. It will provide information you need to complete Form 8962 if you are eligible for the Premium Tax Credit and/or if you received the APTC. 1095-B Health Coverage: This reporting form will be sent to you if you, your spouse, or your dependents had minimum essential coverage for some or all of the months during the year. It will provide information you need to answer questions about your minimum essential health coverage on your tax return.

1095-C Employer Provided Health Insurance Offer and Coverage: This reporting form will be sent to you if you are offered any health coverage by your employer, regardless of whether or not you are enrolled in it. It will provide information you need to answer questions about your health coverage on your tax return.

TBB will ask you to report information from Form 1095-A, Form 1095-B, and Form 1095-C if you received any of these forms. The information from these forms and additional questions will determine your credit eligibility and amount and will be used to fill out Form 8962.

Form 8962 Premium Tax Credit: Forms part of your tax return if you are eligible for the Premium Tax Credit, regardless of whether you chose to get advanced payments or receive the credit all at once. It will be used to calculate the amount of your premium tax credit, and if you opted to receive the APTC, it will reconcile the amount that was paid on your behalf.

Enroll in Health Coverage for 2016For 2016 coverage, the Open Enrollment Period is November 1, 2015 – January 31, 2016. If your clients do not have employer-sponsored health coverage or Medicaid/CHIP, they must enroll in a health care coverage plan in the Marketplace during this enrollment period in order to avoid paying a fee on next year’s tax return.

You can use TBB to help your clients apply for Medicaid and CHIP. Clients can also apply through the Ohio Benefits portal, available at benefits.ohio.gov.

The fastest way to apply for Marketplace insurance coverage is to apply online at HealthCare.gov. Clients may also apply by phone at 1-800-318-2596 or with the assistance of a Navigator or Certified Application Counselor. To find an in-person assister, visit areyoucoveredohio.org or call 1-800-648-1176.

Page 34 • Part Two

Tax Credits

There are two types of tax credits. Non-refundable tax credits reduce the tax owed or tax liability. These credits can reduce the tax liability to $0 but they will not refund any amount thereafter. Refundable tax credits are extra dollars that the government disperses to moderate and low income taxpayers which can reduce the tax liability to $0 and will be refunded if they exceed the tax liability.

Non-Refundable ▪ Child Tax Credit - This credit reduces your tax liability up to $1,000 for each child that you claim as a

dependent. To take this credit each child must meet the qualifying child requirements. ▪ Child and Dependent Care Credit - To qualify for this credit you must have paid for child and/or

dependent care expenses for a qualifying child in order to work or look for work. Keep in mind: ▪ Married taxpayers must both work (have earned income) in order to claim this credit. If a spouse is

either a full-time student during five months of the year or is not capable of caring for themselves for some period during the year, the credit can still be claimed.

▪ To claim this credit the taxpayer must provide the name, address, and taxpayer identification number or Social Security Number of the person or organization who provided care for the child or dependent.

▪ Credit for the Elderly or Disabled - You may be able to take this credit if by the end of the tax year you were age 65 or older or were retired on permanent and total disability and you had taxable disability income.

▪ Education Credits - If you paid expenses for yourself or dependents for higher education you may be eligible for these credits.

▪ Savers Credit (Formerly known as the Retirement Savings Contribution Credit) - Only certain taxpayers who make voluntary contributions to a retirement account may take this credit. Rollover contributions to a traditional or Roth IRA do not count towards this credit.

▪ Mortgage Interest Credit - A taxpayer may claim a mortgage interest credit if he/she has been issued a Mortgage Credit Certificate (MCC) by their state or local government.

Part Two • Page 35

Refundable ▪ Earned Income Tax Credit - To qualify without a qualifying child, you must be at least age 25 and under

65. You must have earned income, a valid social security number, and meet the following income limits:

Your Filing Status

No qualifying children

1 qualifying child

2 qualifying children

3 or more qualifying children

Single, head of household, or qualifying widow(er) with a dependent child

$14,820 $39,131 $44,454 $47,747

Married Filing Jointly

$20,330 $44,651 $49,974 $53,267

▪ Additional Child Tax Credit - This credit allows taxpayers to claim up to $1,000 per qualifying child. The amount depends on the taxpayer’s tax liability, modified AGI, and filing status.

▪ Refundable Education Credits - If you paid expenses for higher education, you may be eligible for this credit. Up to 40 percent of this credit is refundable.

▪ Premium Tax Credit - This credit help make health insurance, purchased through the Health Insurance Marketplace, affordable. Individuals must meet certain income guidelines and cannot be claimed as a dependent by another person. Individuals who file married filing separately will not be eligible except in certain instances.

Page 36 • Part Two

Filing Your Return

Taxpayers have two options when filing their returns. They may file electronically or paper file. If they choose to file electronically, or e-file, they will need to sign the electronic form with one of three things: last year’s PIN, last year’s AGI, or a new PIN given by the IRS. Last year’s AGI can be found on line 37 of form 1040 (Shown below).

New PINClients can request a new PIN on the IRS website. Visit irs.gov and search for electronic filing PIN request. Or, call the IRS at 1-800-704-7388 and ask for a new electronic filing PIN. Remember: Any PIN retreived from the IRS is a new PIN.

Part Two • Page 37

After Filing

Clients will receive a notification of their e-file status either via email or mail, whichever they’ve selected. Please instruct your clients to open any mail from The Benefit Bank immediately.

Counselors can also help clients find their e-file status using the e-file status tool. Typically, this information is available within 5 or 10 minutes of submission.

If there is incorrect information on the tax return, like incorrect birthdates or social security numbers, the e-file will be rejected by the IRS. E-file rejections are easily fixed and may be resubmitted to the IRS.All rejections whether received by mail or electronically will be accompanied by detailed information on why the return was rejected. Clients should bring this information with them when they return to have their information corrected. Simply log into the online service, make the appropriate corrections, and click Save and Continue until you see a message indicating that the return has been sent. Clients can also be directed to self-serve to correct their returns if they have access to the internet.

If a client’s return is accepted and they are later contacted by the IRS because they failed to report a source of income, incorrectly reported a source of income, or for some other reason owe additional tax they will need to complete an amended return. Although The Benefit Bank online service cannot assist with completing amended returns, you will be able to access the blank form to offer any interested clients.

Page 38 • Part Two

Accessing the Training Website

The Benefit Bank training website acts as a mirror to the live site. You may practice using TBB on this site any time without worrying about submitting fake client information. To access the training site:

1. Go to: https://training.thebenefitbank.org2. In the Login Name box, enter the letters oh followed by any number between 1 and 500. You do not

have to memorize these numbers, as any set of numbers will allow you access to the training site3. The password is always tbb12345

If you see an “Authentication Failed” message, pick a different set of numbers and try again.

https://training.thebenefitbank.org