tax index with the support of the inmind research company eba tax index results of the 1 st wave,...

TRANSCRIPT

Tax Index with the support of theInMind research company

EBA Tax INDEXResults of the 1st wave,

the year 2011

Conducted by the EBA

with the support of

InMind research company

May 2012

Tax Index with the support of theInMind research company

2

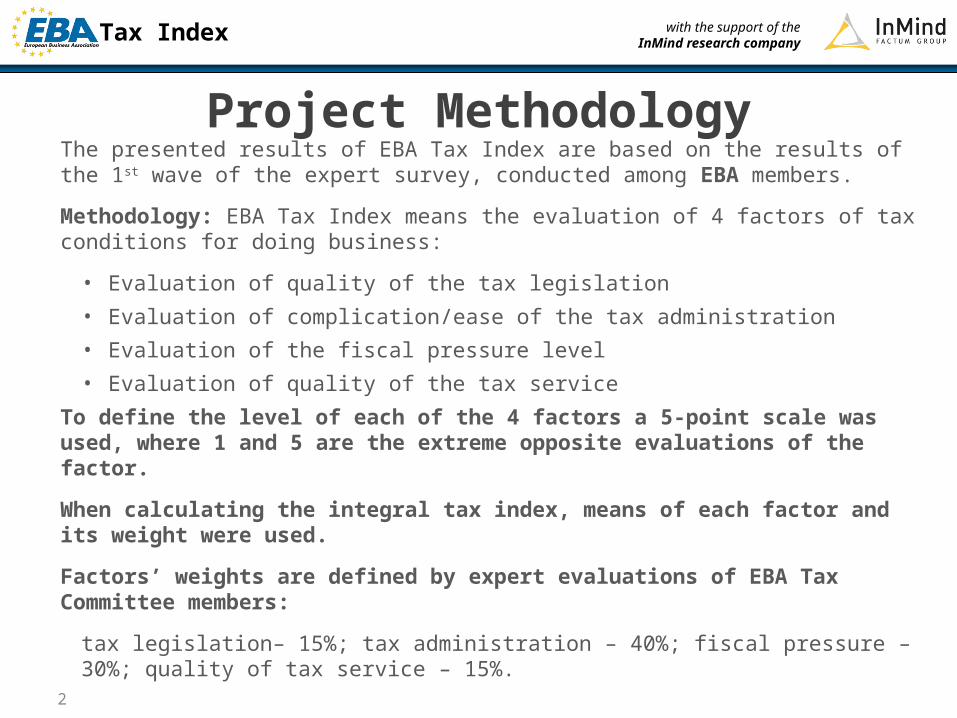

Project MethodologyThe presented results of EBA Tax Index are based on the results of the 1st wave of the expert survey, conducted among EBA members.

Methodology: EBA Tax Index means the evaluation of 4 factors of tax conditions for doing business:

• Evaluation of quality of the tax legislation

• Evaluation of complication/ease of the tax administration

• Evaluation of the fiscal pressure level

• Evaluation of quality of the tax service

To define the level of each of the 4 factors a 5-point scale was used, where 1 and 5 are the extreme opposite evaluations of the factor.

When calculating the integral tax index, means of each factor and its weight were used.

Factors’ weights are defined by expert evaluations of EBA Tax Committee members:

tax legislation– 15%; tax administration – 40%; fiscal pressure – 30%; quality of tax service – 15%.

Tax Index with the support of theInMind research company

3

Report noticeThe results are presented by each of 4 factors, in particular:

• Mean of each factor

• Numeric value, which divides the upper half of the sample from the lower part (median)

The results are also segmented by company size in accordance to Commercial Code of Ukraine:

– Small enterprises: 50 or less employees, gross income – less than UAH 70 million during the financial year 2011

– Medium enterprises: 50 to 250 employees, gross income – UAH 70 to 100 million during the financial year 2011

– Large enterprises: more than 250 employees, gross income – більше UAH 100 million during the financial year 2011

Participants: 117 representatives of EBA member companies

Timeframes: the data is collected in the 1st half of the year 2012 and reflects the situation in 2011

Research Conduction: The research is conducted by the EBA, analytic support provided by InMind research company

Tax Index with the support of theInMind research company

4

Overall results the year 2011

On a 1 to 5 scale On a 1 to 7 scale

TAX INDEX(integral rate)

1,90 2,66

Tax legislation 1,76 2,47

Easiness of tax administration 1,62 2,27

Fiscal pressure 2,11 2,95

Quality of tax service 2,36 3,30

Tax Index with the support of theInMind research company

5

EBA Tax INDEX:

Components

Tax Index with the support of theInMind research company

6

Tax Legislation

Mean2,47

Median2,00

Mean on a scale from 1 to 51,76

1

2

3

4

5

6

7

23%

34%

21%

15%

6%

0%

0%

Negative values

Neutral value

Positive values

Evaluations by 7-point scale with extreme values:

1 – tax regime was profoundly preventing your company’s progress:

7 – tax regime was definitely promoting your company’s business progress

Question: To what extent tax regime was facilitating investments and your company’s activity in 2011?

Small N=37 Medium N=27 Large N=531

2

3

4

5

6

7

2.51 2.26 2.55

Means of evaluation of tax legislation depending on the enterprise size

Tax Index with the support of theInMind research company

7

Ease of Tax Administration

Mean2,27

Median2,00

Mean on a scale from 1 to 51,62

1

2

3

4

5

6

7

31%

30%

23%

14%

3%

0%

0%

Negative values

Neutral value

Positive values

Evaluations by 7-point scale with extreme values:

1 – very complicated

7 – very easy

Question:

Could you, please evaluate the complication/easiness of tax accounting and tax administration in the year 2011?

Small N=37 Medium N=27 Large N=531

2

3

4

5

6

7

2.46 2.15 2.21

Means of evaluation of ease of tax administration depending on the enterprise size

Tax Index with the support of theInMind research company

8

Fiscal Pressure

Mean2,95

Median3,00

Mean on a scale from 1 to 52,11

1

2

3

4

5

6

7

27%

14%

27%

16%

4%

11%

1%

Negative values

Neutral value

Positive values

Evaluations by 7-point scale with extreme values:

1 – fiscal pressure caused significant difficulties in company’s activity

7 – there were no signs of fiscal pressure at all in the activity of the company

Question: Could you, please evaluate fiscal pressure on your company in the year 2011?

Small N=37 Medium N=27 Large N=531

2

3

4

5

6

7

3.46 2.96

2.58

Means of evaluation of the fiscal pressure level depending on the enterprise size

Tax Index with the support of theInMind research company

9

Tax Service

Mean3,30

Median2,00

Mean on a scale from 1 to 52,36

1

2

3

4

5

6

7

16%

19%

19%

21%

18%

6%

2%

Negative values

Neutral value

Positive values

Evaluations by 7-point scale with extreme values:

1 – complete dissatisfaction by the quality of the received service

7 – complete satisfaction by the received service

Question: Could you please estimate the quality of the service your company received from tax bodies in the year 2011 ( by the quality of the service you should understand the stuffs’ affability and competence, the transparency of the received answers, the operational efficiency and convenience of the declaration submitting process etc.)?

Small N=37 Medium N=27 Large N=531

2

3

4

5

6

7

3.03 3.44 3.42

Means of evaluation of the tax service depending on the enterprise size

Tax Index with the support of theInMind research company

10

EBA Tax INDEX:

Auxiliary Indicators

Tax Index with the support of theInMind research company

11

Effectiveness of the Tax Reform

Mean2,77

Median3,00

Mean on a scale from 1 to 51,98

1

2

3

4

5

6

7

21%

21%

26%

24%

7%

0%

1%

Negative values

Neutral value

Positive values

Evaluations by 7-point scale with extreme values:

1 – it became definitely worse than it had been before the 1st January 2011

7 – became definitely better than it had been before the 1st January 2011

Question: Could you please evaluate the effectiveness of the tax reform (using the results of the 2011 financial year)?

Small N=37 Medium N=27 Large N=531

2

3

4

5

6

7

2.68 2.85 2.79

Means of evaluation of effectiveness of the tax reform depending on the enterprise size

Tax Index with the support of theInMind research company

Negative changes for your company related to implementation of the Tax Code-2011

• Complication of reporting, increase of working and financial expenses on accounting and software, poor administration of electronic reporting by the Tax Service (27%)

• The Tax Code of Ukraine is sophisticated, it contains inconsistencies, understood ambiguously; inability to receive consultations, lack of subordinate documents (21%)

• Increase of number of inspections, inquiries for information, lawlessness and absence of responsibility for tax inspectors (21%)

• Tax administration pressure has increased: tax payments in advance; setting of the tax burden disregarding results of real activity, indicatory prices on import, etc. (19%)

• Other – continued on the next slide

• There was no negative impact on our company (3%)

Positive changes for your company related to implementation of the Tax Code-2011

• Reduction of the profit tax rate (19%)• Simplification of the taxation procedure due

to the reduction of number of taxes and reporting standardisation (21%)

• Systematisation of tax legislation, reduction of number of the regulating documents (13%)

• Approximation of the taxing and accounting (8%)

• Expansion of the list of expenses (6%)• Automated VAT refund (5%)• VAT exemption for certain services (3%)• Other: certain changes for agricultural market,

banks, staff leasing, absence of penalties during the first half of the first year action of the Code, inflow of clients for consulting companies (9%)

• There are no positive changes – 37% of companies

12

Positive and Negative Consequences of the Tax Reform

Tax Index with the support of theInMind research company

• Frequent changes in the Tax Code, implementation of procedures, reporting formats and changes in taxation without prior notice and any possibility of previous familiarisation and examination of the legislation (12%)

• Prohibition of attribution of expenses to individual entities, complication of interaction with individual entities (11%)

• Prohibition of tax losses carryforward (10%)• Expansion of the tax base (VAT on consulting and audit service, increase of PIT, ecology tax, etc.)

(9%)• Problems related to the registration of tax invoices and change of their forms (7%)• Senseless taxation order for expenses on warranty liabilities, ecology tax, transport expenses, etc.

(7%)• Complication of reporting when importing goods, implementation of UCCFEA into tax invoices,

registration of every invoice when importing (7%)• The Tax Code of Ukraine does not promote legal doing business (preferences for those close to

authorities, payoffs, shadowing, etc.) (6%)• Problems related to VAT refunds (5%)• Problems related to registration as a VAT-payer (4%)• VAT payment of first event remained, that’s why double accounting exists; no real approximation of

tax and financial accounting has taken place (3%)• Complication in representative offices of foreign companies’ activity (2%)• Reduction in royalty percentage, which is attributed to gross expenses (2%)

Negative Consequences of the Tax Reform(continued)

13

Tax Index with the support of theInMind research company

14

Effective Tax Rate: Tax Reform Impact

Change of the effective tax rate in 2011

Definition:

Effective tax rate – ratio of the income as to the financial accounting and the income as to the tax report

30%

19%

51%

Unchanged

Change of the effective tax rate in 2011 depending on

the enterprise size

Small

Medium

Large

14%

18%

23%

70%

52%

38%

16%

30%

39%

reduced unchanged increased

Increased

Decreased

Tax Index with the support of theInMind research company

15

Fiscal Pressure Manifestation

Which evidence of the fiscal pressure have you experienced in the 2011 year?

“Proposals” to pay the taxes in advance

Groundless information requests

Heavy inspections

Receiving “tasks” as for budget filling

Refusals or artificial barriers while submitting declaration

Preconceived verdicts of court and tax bodies

Use of force by taxmen (the so-called 'mask shows')

Another

There were no signs of fiscal pressure

77%

50%

42%

41%

37%

33%

14%

16%

4%

0

1

2

3

4

5

6

7

21%

20%

14%

12%

8%

5%

3%

17%

No inspections

7 or more inspections

Number of tax inspections in your company in 2011

Tax Index with the support of theInMind research company

+38 044 496 06 01

www.eba.com.ua