tax policy center urban institute and brookings institution the individual alternative minimum tax...

TRANSCRIPT

Tax Policy Tax Policy CenterCenter

Tax Policy Tax Policy CenterCenter

Urban InstituteAnd

Brookings Institution

www.taxpolicycenter.org

The Individual Alternative Minimum Tax

President’s Advisory Panel on

Federal Tax Reform

3 March 2005

Leonard E. Burman

Senior Fellow, The Urban Institute

Codirector, The Tax Policy Center

Visiting Professor, Georgetown Public Policy Institute

Tax Policy Tax Policy CenterCenter

Tax Policy Tax Policy CenterCenter

Urban InstituteAnd

Brookings Institution

www.taxpolicycenter.org

Background

• 1966: 155 high-income taxpayers paid no income tax

• 1969: creation of a minimum tax designed to ensure high income filers did not exploit tax laws to reduce or eliminate their federal income tax liability

• 2010: AMT will affect 30 million taxpayers, including virtually all upper middle class families with two or more kids.

Tax Policy Tax Policy CenterCenter

Tax Policy Tax Policy CenterCenter

Urban InstituteAnd

Brookings Institution

www.taxpolicycenter.org

Determination of AMT Liability

• Add preferences and adjustments to taxable income

• Subtract AMT exemption• Calculate tax using AMT rate schedule

and rules• If more than regular tax, pay the

difference as AMT• (Many complexities left out of this

simplified explanation.)

Tax Policy Tax Policy CenterCenter

Tax Policy Tax Policy CenterCenter

Urban InstituteAnd

Brookings Institution

www.taxpolicycenter.org

AMT Exemptions and Schedule

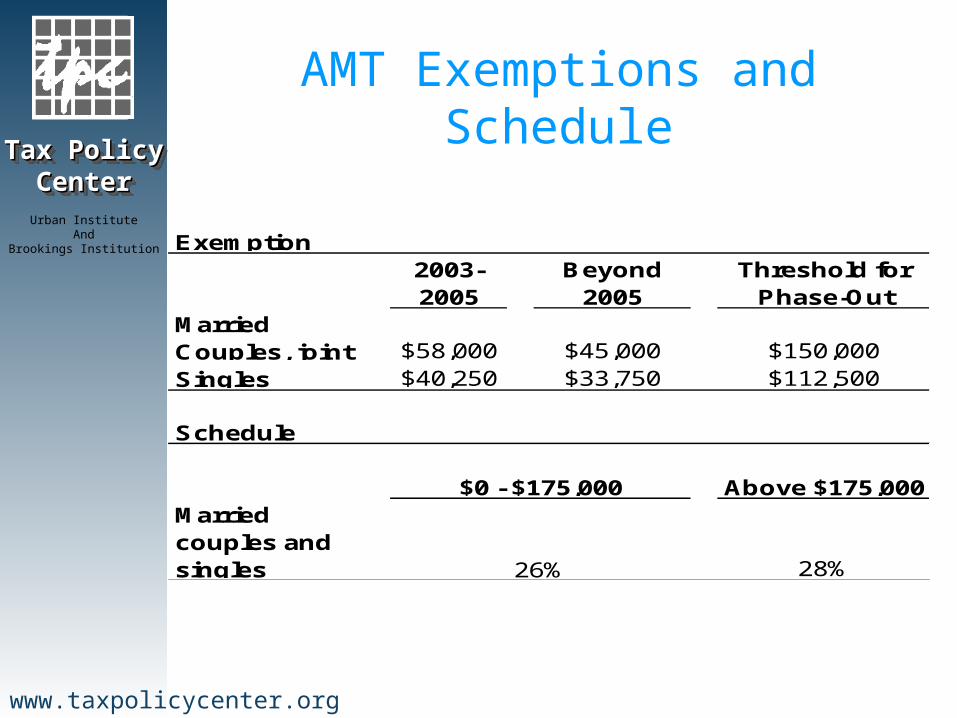

• AMT exemption currently $58,000 for couples, $40,250 for singles– In 2006, exemption drops to $45,000/$33,750

• Exemption phases out at higher incomes, creating high implicit tax rates

• Statutory rates = 26% and 28%, but exemption phaseout creates phantom rates of 32.5% and 35%

• Not indexed for inflation

Tax Policy Tax Policy CenterCenter

Tax Policy Tax Policy CenterCenter

Urban InstituteAnd

Brookings Institution

www.taxpolicycenter.org

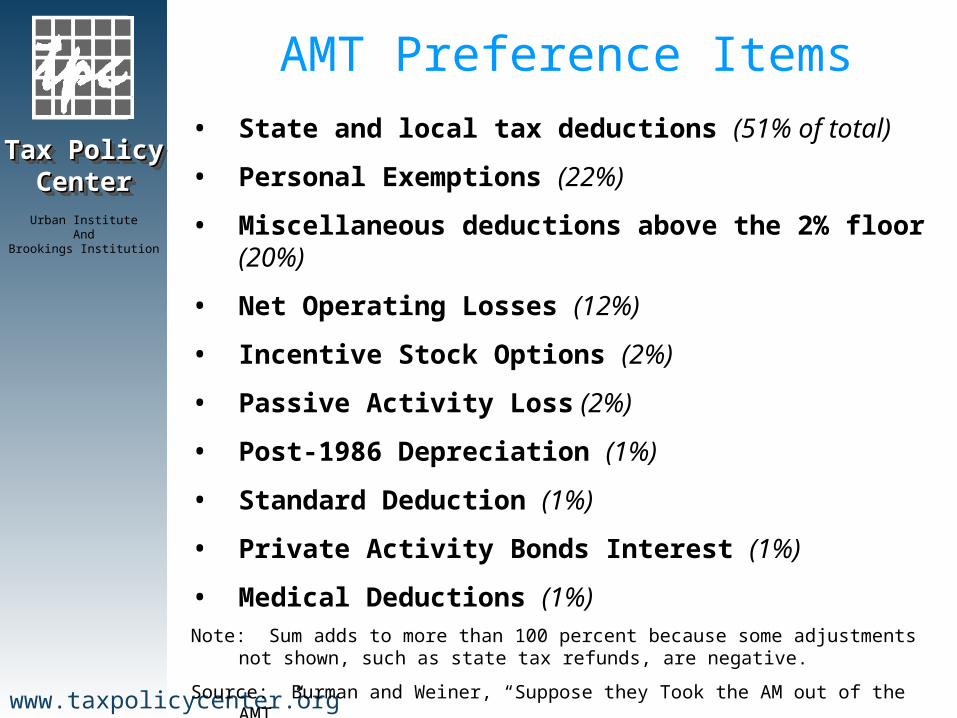

AMT Preference Items• State and local tax deductions (51% of total)

• Personal Exemptions (22%)

• Miscellaneous deductions above the 2% floor (20%)

• Net Operating Losses (12%)

• Incentive Stock Options (2%)

• Passive Activity Loss (2%)

• Post-1986 Depreciation (1%)

• Standard Deduction (1%)

• Private Activity Bonds Interest (1%)

• Medical Deductions (1%)Note: Sum adds to more than 100 percent because some adjustments not shown, such

as state tax refunds, are negative.

Source: Burman and Weiner, “Suppose they Took the AM out of the AMT.”

Tax Policy Tax Policy CenterCenter

Tax Policy Tax Policy CenterCenter

Urban InstituteAnd

Brookings Institution

www.taxpolicycenter.org

0

5

10

15

20

25

30

35

40

45

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015Year

Num

ber o

f AMT

Ta

xpay

ers (

Millio

ns)

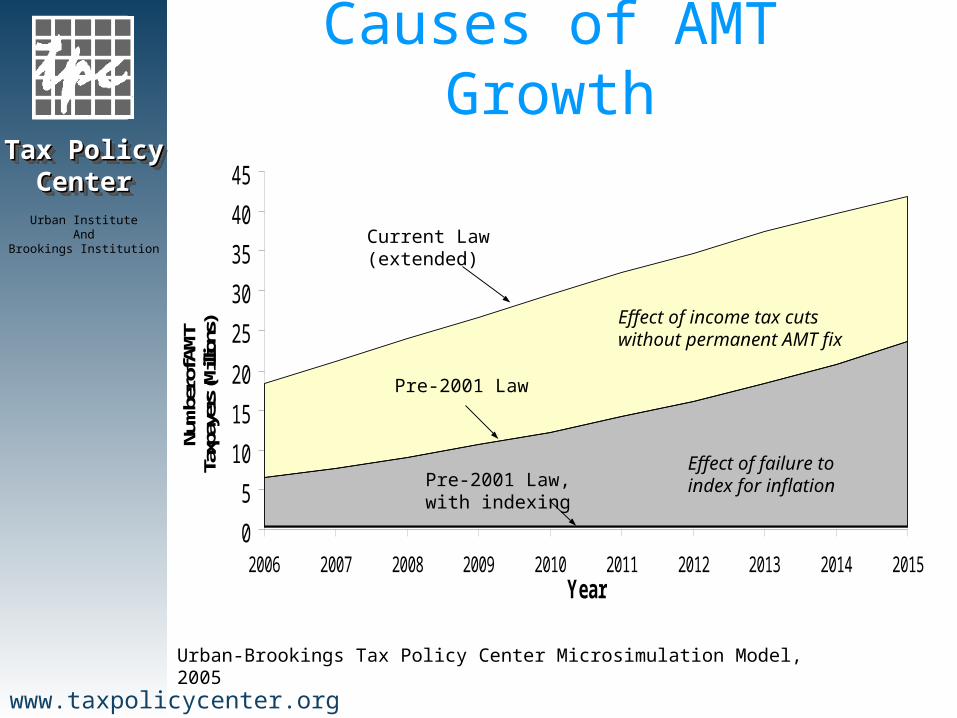

Causes of AMT Growth

Effect of failure to index for inflationPre-2001 Law,

with indexing

Current Law (extended)

Effect of income tax cuts without permanent AMT fix

Pre-2001 Law

Urban-Brookings Tax Policy Center Microsimulation Model, 2005

Tax Policy Tax Policy CenterCenter

Tax Policy Tax Policy CenterCenter

Urban InstituteAnd

Brookings Institution

www.taxpolicycenter.org

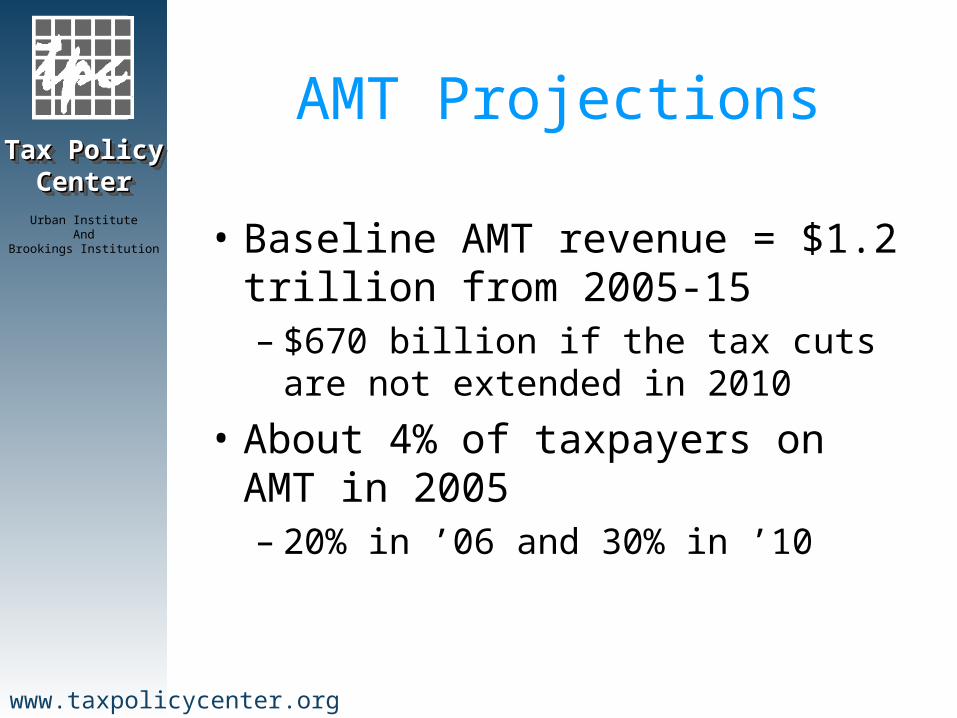

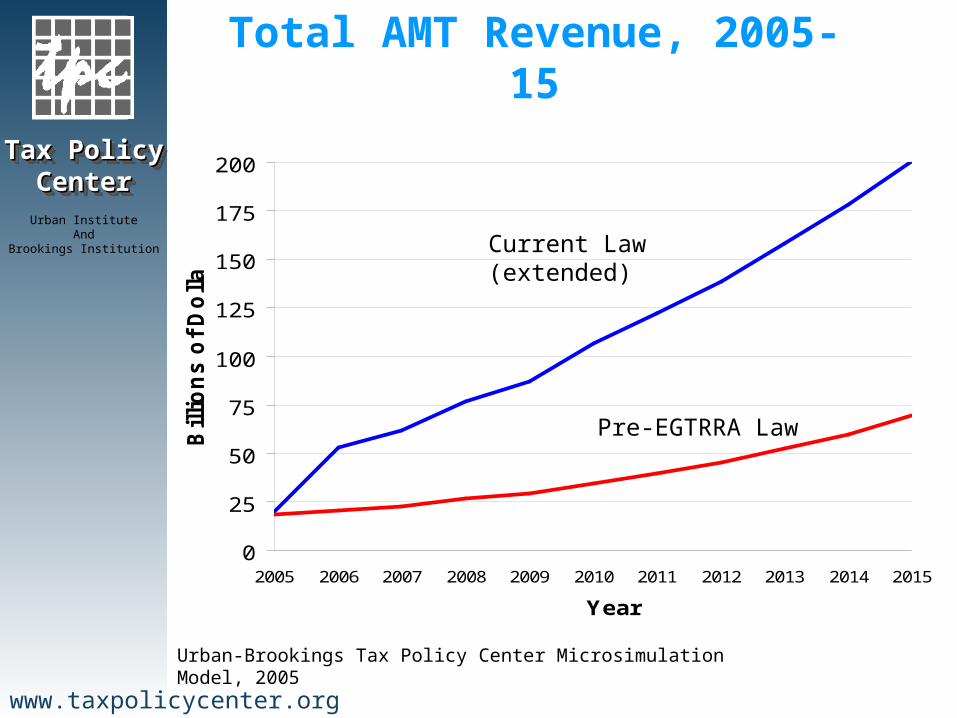

AMT Projections

• Baseline AMT revenue = $1.2 trillion from 2005-15– $670 billion if the tax cuts are

not extended in 2010

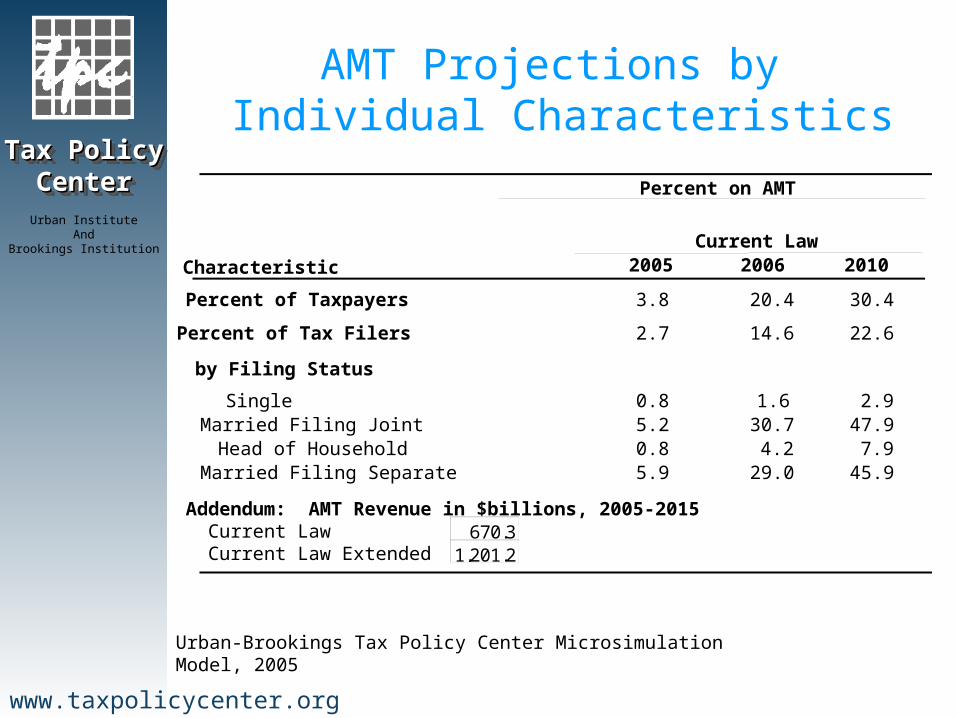

• About 4% of taxpayers on AMT in 2005– 20% in ’06 and 30% in ’10

Tax Policy Tax Policy CenterCenter

Tax Policy Tax Policy CenterCenter

Urban InstituteAnd

Brookings Institution

www.taxpolicycenter.org

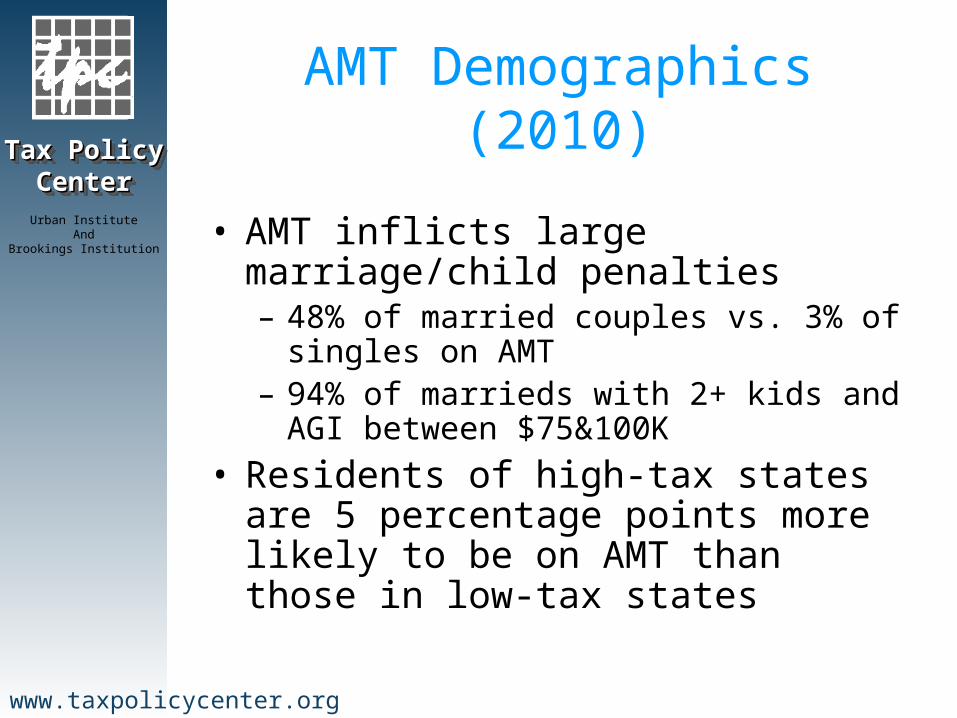

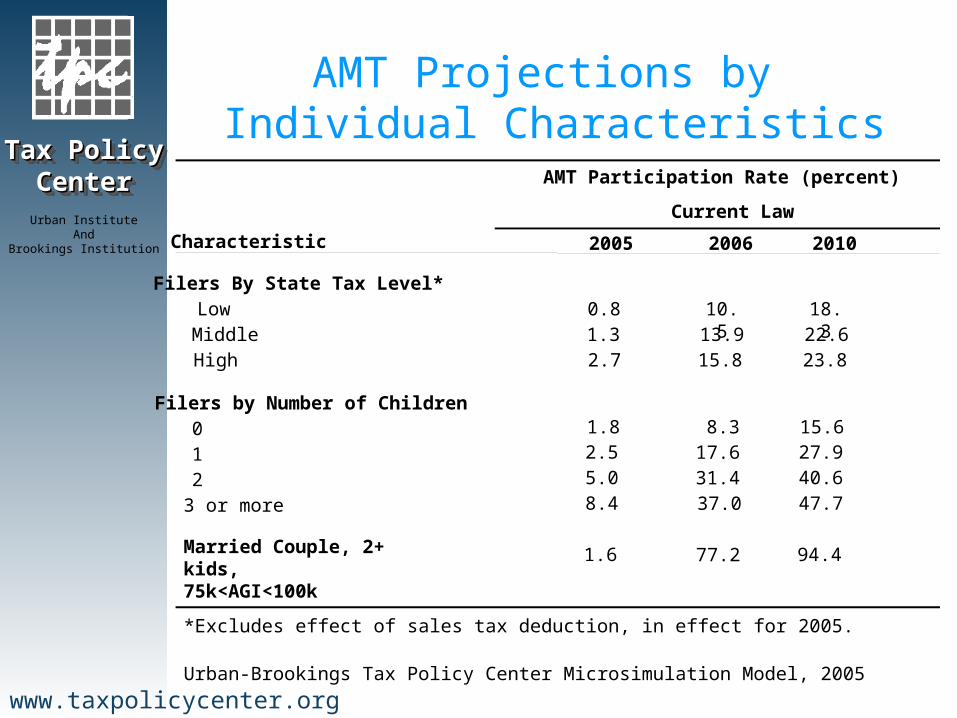

AMT Demographics (2010)

• AMT inflicts large marriage/child penalties– 48% of married couples vs. 3% of

singles on AMT– 94% of marrieds with 2+ kids and AGI

between $75&100K

• Residents of high-tax states are 5 percentage points more likely to be on AMT than those in low-tax states

Tax Policy Tax Policy CenterCenter

Tax Policy Tax Policy CenterCenter

Urban InstituteAnd

Brookings Institution

www.taxpolicycenter.org

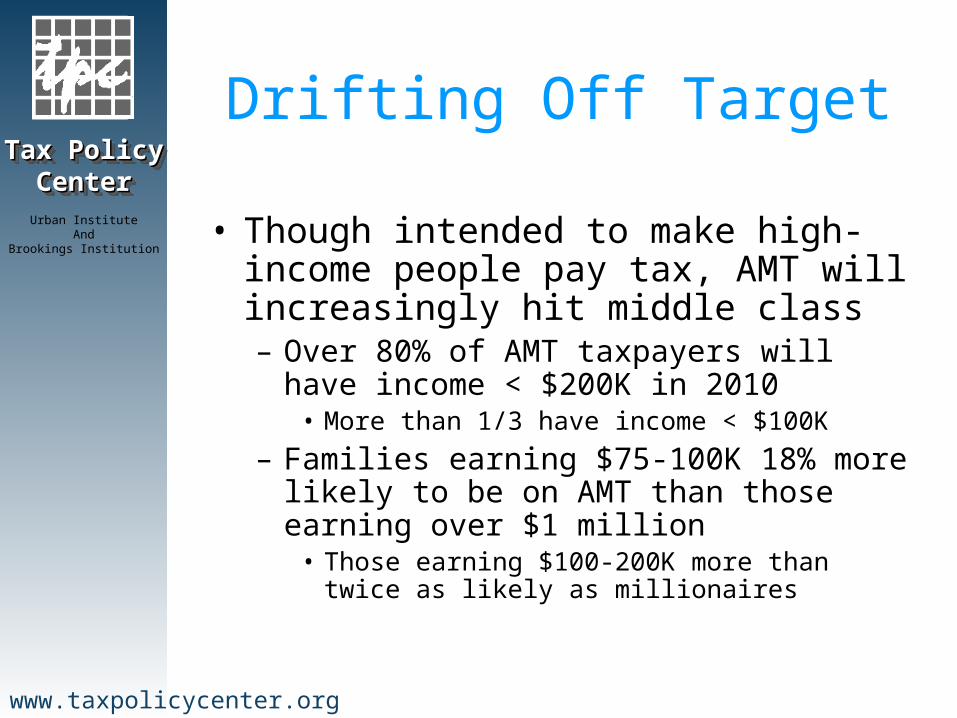

Drifting Off Target

• Though intended to make high-income people pay tax, AMT will increasingly hit middle class– Over 80% of AMT taxpayers will have

income < $200K in 2010• More than 1/3 have income < $100K

– Families earning $75-100K 18% more likely to be on AMT than those earning over $1 million

• Those earning $100-200K more than twice as likely as millionaires

Tax Policy Tax Policy CenterCenter

Tax Policy Tax Policy CenterCenter

Urban InstituteAnd

Brookings Institution

www.taxpolicycenter.org

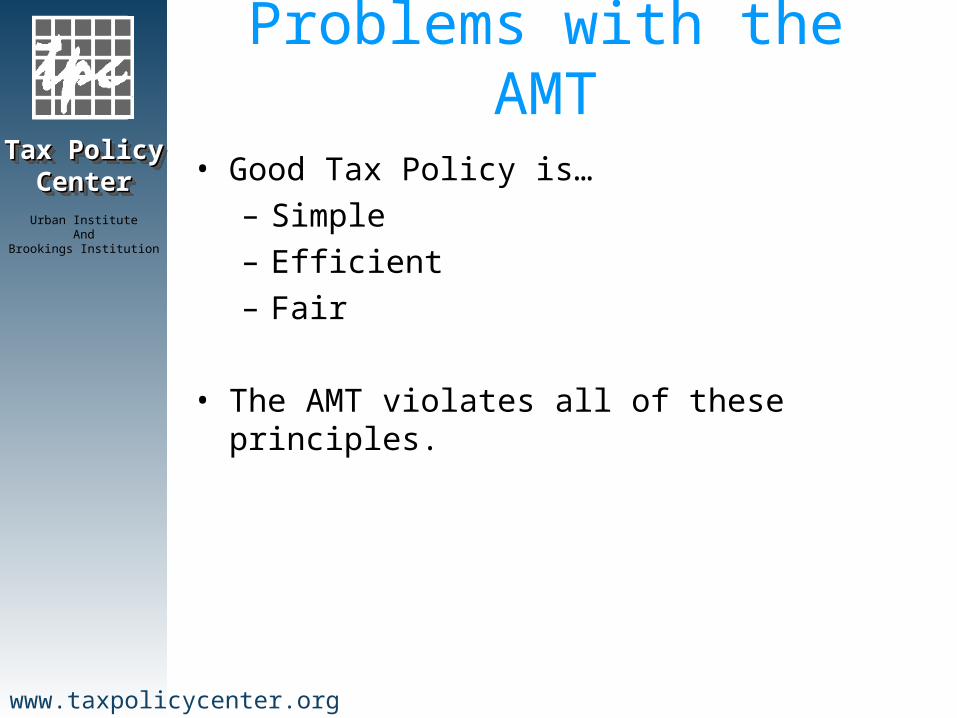

Problems with the AMT

• Good Tax Policy is…– Simple– Efficient– Fair

• The AMT violates all of these principles.

Tax Policy Tax Policy CenterCenter

Tax Policy Tax Policy CenterCenter

Urban InstituteAnd

Brookings Institution

www.taxpolicycenter.org

Pointless Complexity

• Many middle class taxpayers must file AMT Form 6251, but owe no AMT

• AMT rules regarding credits, capital gains, dividends, deferral preferences very complex

• Most deferral preferences don’t even generate much revenue, just change the timing of tax payments

• Vastly complicates tax planning

Tax Policy Tax Policy CenterCenter

Tax Policy Tax Policy CenterCenter

Urban InstituteAnd

Brookings Institution

www.taxpolicycenter.org

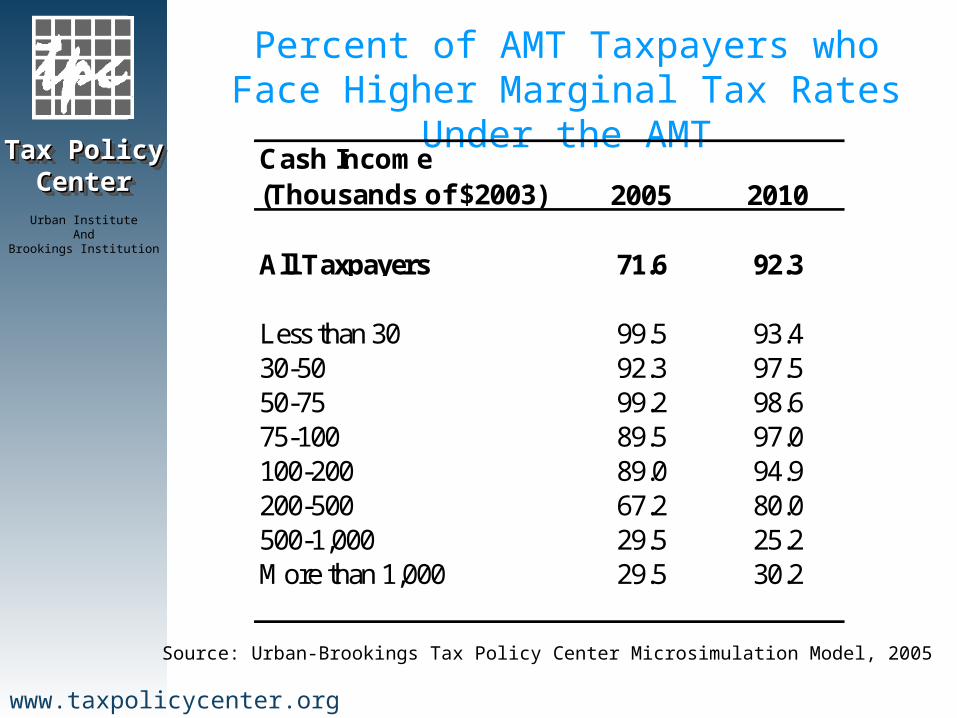

Efficiency

• The AMT raises marginal tax rates for most– 71% of AMT taxpayers face higher marginal tax rates

under AMT in 2005– 92% will be in that situation in 2010– People creep into higher brackets over time

because, unlike the regular income tax, AMT is not indexed

• Might enhance efficiency to extent that it deterred tax shelters, but 90% of AMT preferences have nothing to do with shelters

Tax Policy Tax Policy CenterCenter

Tax Policy Tax Policy CenterCenter

Urban InstituteAnd

Brookings Institution

www.taxpolicycenter.org

Equity

• Nasty marriage/child penalties• Some legitimate adjustments to ability to pay

are disallowed under AMT (e.g., contingent legal fees)

• AMT makes the tax system more progressive, but less so over time

• Relatively little tax collected from very rich

Tax Policy Tax Policy CenterCenter

Tax Policy Tax Policy CenterCenter

Urban InstituteAnd

Brookings Institution

www.taxpolicycenter.org

Conclusions

• Pointless complexity and bizarre pattern of taxes

• Increasingly a tax on the upper middle class

• Better to build anti-tax shelter provisions into regular tax and adjust rates to hit revenue target

Tax Policy Tax Policy CenterCenter

Tax Policy Tax Policy CenterCenter

Urban InstituteAnd

Brookings Institution

www.taxpolicycenter.org

Appendix

• Supplemental tables and charts

• Further reading

Tax Policy Tax Policy CenterCenter

Tax Policy Tax Policy CenterCenter

Urban InstituteAnd

Brookings Institution

www.taxpolicycenter.org

2003-2005

Beyond 2005

Threshold for Phase-Out

Married Couples, joint $58,000 $45,000 $150,000 Singles $40,250 $33,750 $112,500

Above $175,000Married couples and singles 28%

$0 - $175,000

26%

Exemption

Schedule

AMT Exemptions and Schedule

Tax Policy Tax Policy CenterCenter

Tax Policy Tax Policy CenterCenter

Urban InstituteAnd

Brookings Institution

www.taxpolicycenter.org

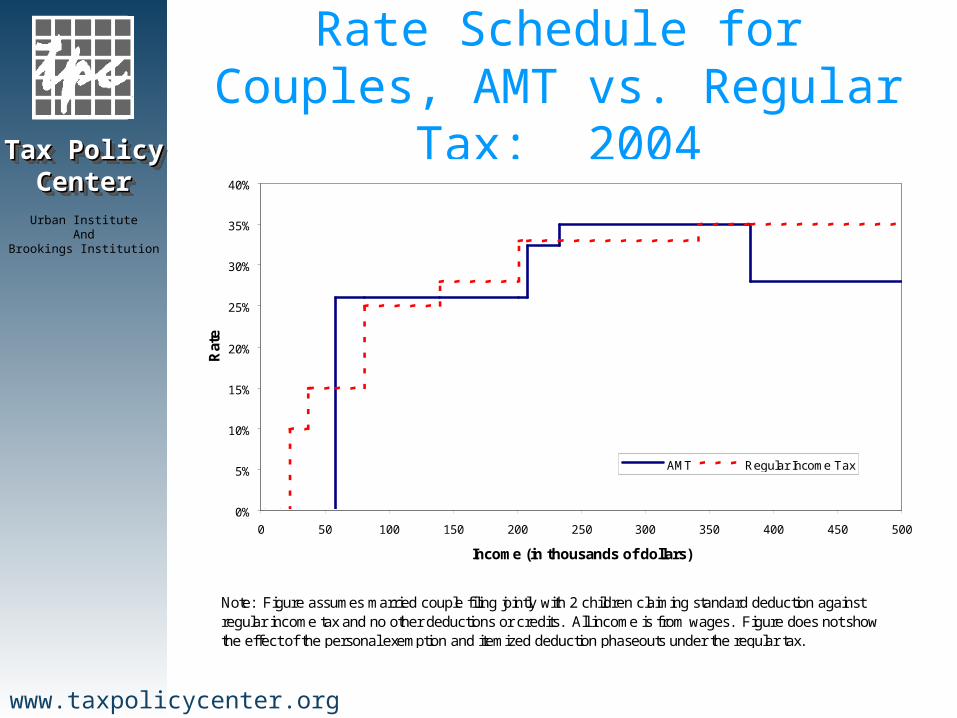

Rate Schedule for Couples, AMT vs. Regular Tax: 2004

0%

5%

10%

15%

20%

25%

30%

35%

40%

0 50 100 150 200 250 300 350 400 450 500

Income (in thousands of dollars)

Rat

e

AMT Regular Income Tax

Note: Figure assumes married couple filing jointly with 2 children claiming standard deduction against regular income tax and no other deductions or credits. All income is from wages. Figure does not show the effect of the personal exemption and itemized deduction phaseouts under the regular tax.

Tax Policy Tax Policy CenterCenter

Tax Policy Tax Policy CenterCenter

Urban InstituteAnd

Brookings Institution

www.taxpolicycenter.org

0

25

50

75

100

125

150

175

200

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Year

Billio

ns

of

Do

lla

rs

Urban-Brookings Tax Policy Center Microsimulation Model, 2005

Total AMT Revenue, 2005-15

Current Law (extended)

Pre-EGTRRA Law

Tax Policy Tax Policy CenterCenter

Tax Policy Tax Policy CenterCenter

Urban InstituteAnd

Brookings Institution

www.taxpolicycenter.org

0

40

80

120

160

200

2005 2006 2007 2008 2009 2010

Year

Revenue C

ost in

$B

illio

ns

By 2008, it will cost more to repeal the AMT than the regular income tax.

Urban-Brookings Tax Policy Center Microsimulation Model, 2005

Cost of repealing the regular tax

Cost of repealing the AMT

Tax Policy Tax Policy CenterCenter

Tax Policy Tax Policy CenterCenter

Urban InstituteAnd

Brookings Institution

www.taxpolicycenter.org

AMT Projections by Individual Characteristics

Percent on AMT

Current Law

Characteristic 2005 2006 2010

Percent of Taxpayers 3.8 20.4 30.4

Percent of Tax Filers 2.7 14.6 22.6

by Filing Status

Single 0.8 1.6 2.9Married Filing Joint 5.2 30.7 47.9Head of Household 0.8 4.2 7.9Married Filing Separate 5.9 29.0 45.9

Urban-Brookings Tax Policy Center Microsimulation Model, 2005

Addendum: AMT Revenue in $billions, 2005-2015 Current Law Current Law Extended

670.31,201.2

Tax Policy Tax Policy CenterCenter

Tax Policy Tax Policy CenterCenter

Urban InstituteAnd

Brookings Institution

www.taxpolicycenter.org

AMT Projections by Individual Characteristics

AMT Participation Rate (percent)

Current Law

Characteristic 2005 2006 2010

Filers by Number of Children0 1.8 8.3 15.6

1 2.5 17.6 27.9

2 5.0 31.4 40.6

3 or more 8.4 37.0 47.7

Filers By State Tax Level*Low 0.8 10.5 18.3Middle 1.3 13.9 22.6High 2.7 15.8 23.8

*Excludes effect of sales tax deduction, in effect for 2005.

Urban-Brookings Tax Policy Center Microsimulation Model, 2005

Married Couple, 2+ kids,75k<AGI<100k

1.6 77.2 94.4

Tax Policy Tax Policy CenterCenter

Tax Policy Tax Policy CenterCenter

Urban InstituteAnd

Brookings Institution

www.taxpolicycenter.org

AMT Projections by Income

AMT Participation Rate (percent)

Current LawCash Income (thousands of 2003$) 2005 2006 2010

75-100 0.86.8

53.4

1,000 and more39.3

Less than 30 0.030-50 0.150-75 0.5

100-200

500-1,000200-500

26.7

31.863.087.051.8

0.01.16.0

33.4

53.481.093.962.6

0.02.9

16.9

35.3

Urban-Brookings Tax Policy Center Microsimulation Model, 2005

Tax Policy Tax Policy CenterCenter

Tax Policy Tax Policy CenterCenter

Urban InstituteAnd

Brookings Institution

www.taxpolicycenter.org

Source: Urban-Brookings Tax Policy Center Microsimulation Model, 2005

Percent of AMT Taxpayers who Face Higher Marginal Tax Rates Under the AMT

Cash Income (Thousands of $2003) 2005 2010

All Taxpayers 71.6 92.3

Less than 30 99.5 93.430-50 92.3 97.550-75 99.2 98.675-100 89.5 97.0100-200 89.0 94.9200-500 67.2 80.0500-1,000 29.5 25.2More than 1,000 29.5 30.2

Tax Policy Tax Policy CenterCenter

Tax Policy Tax Policy CenterCenter

Urban InstituteAnd

Brookings Institution

www.taxpolicycenter.org

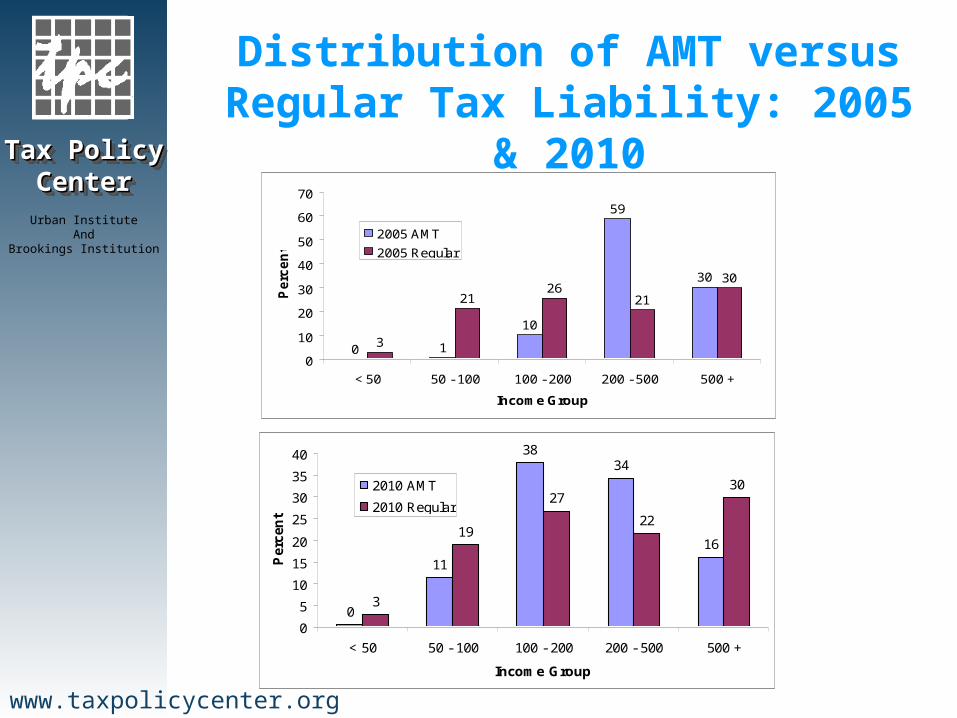

Distribution of AMT versus Regular Tax Liability: 2005 & 2010

0 1

10

59

30

3

2126

21

30

0

10

20

30

40

50

60

70

< 50 50 - 100 100 - 200 200 - 500 500 +

Income Group

Pe

rce

nt

2005 AMT

2005 Regular

0

11

3834

16

3

19

27

22

30

0

5

10

15

20

25

30

35

40

< 50 50 - 100 100 - 200 200 - 500 500 +

Income Group

Perc

en

t

2010 AMT

2010 Regular

Tax Policy Tax Policy CenterCenter

Tax Policy Tax Policy CenterCenter

Urban InstituteAnd

Brookings Institution

www.taxpolicycenter.org

Further ReadingBurman, Leonard E. and David Weiner. 2004. “Suppose They Took the AM out of the AMT?” available at

www.taxpolicycenter.org. (examines issues raised if the AMT were a standalone income tax)

Burman, Leonard E., William G. Gale, Jeffrey Rohaly, Matthew Hall, and Mohammed Adeel Saleem. 2004. “AMT: A Data Update” available at www.taxpolicycenter.org. (includes estimates of some reform options)

Burman, Leonard E., William G. Gale and Jeffrey Rohaly. 2003. “Policy Watch: The Expanding Reach of the

Individual Alternative Minimum Tax,” with Journal of Economic Perspectives 17(2): 173-186. Burman, Leonard E., William G. Gale, Jeffrey Rohaly, and Benjamin H. Harris. 2002. “The Individual AMT:

Problems and Potential Solutions,” National Tax Journal 55(3): 555-596. Feenberg, Daniel R., and James M. Poterba. 2004. “The Alternative Minimum Tax and Effective Marginal Tax

Rates,” National Tax Journal 57(2): 407-427.

General Accounting Office. 2000. “Alternative Minimum Tax: An Overview of its Rationale and Impact on Individual Taxpayers.” Report to the Chairman, Committee on Finance, U.S. Senate (GAO/GGD-00-180). August.

Harvey, Robert P. and Jerry Tempalski. 1997. “The Individual AMT: Why it Matters.” National Tax Journal 50(3):

453-473. Rebelein, Robert and Jerry Tempalski. 2000. “Who Pays the Individual AMT?” U.S. Department of the Treasury,

OTA Paper 87.