taxation of capital gains including indirect transfers. s. r. patnaik... · indirect transfers s....

TRANSCRIPT

Taxation of Capital Gains including

Indirect Transfers

S. R. PatnaikPartner

Amarchand & Mangaldas & Suresh A. Shroff & Co.Peninsula Chambers, Peninsula Corporate Park,

Ganpatrao Kadam Marg, Lower Parel, Mumbai - 400 013

Tel: (91-22) 2496-4455 Fax:(91-22) 2496-3666

Email: [email protected]

December 20, 2014

Workshop on Taxation of Foreign Remittances

Outline of the Presentation

Taxability of Capital Gains under the IT Act

Taxability of Capital Gains under the DTAA

Salient Features of some DTAAs signed by India

Taxability of indirect transfers under the DTAAs

Withholding tax obligations

Purchase of capital assets from an NRI

Case Studies

2

Taxability of Capital Gains

under the IT Act

Taxability of Capital Gains under the IT Act

Every person is liable to pay tax annually on its total income computed in

accordance of the provisions of the IT Act [Section 4]

Non residents are taxable in India on income that accrues or arises, or is

deemed to accrue or arise or is received or is deemed to be received in

India. [Section 5 ]

As per Section 9(1)(i) of the IT Act, the following income is deemed to

accrue or arise in India:

“all income accruing or arising, whether directly or indirectly,

…....through the transfer of a capital asset situated in India”

4

Meaning of terms used in Section 9(1)(i)

‘Capital asset’ means property of any kind held by a taxpayer whether or

not connected with his business or profession subject to certain specific

exemptions [Section 2(14)]

‘Transfer’ is defined to include inter alia sale, exchange, relinquishment of

assets, the extinguishment of any right therein and compulsory acquisition

under law [Section 2(47)]

‘Property’ includes any rights in or in relation to an Indian company,

including rights of management or control or any other rights whatsoever

[Explanation to section 2(14)]

‘Through’ means and include ‘by means of’, ‘in consequence of’ or ‘by

reason of’[Explanation 4 to section 9(1)(i)]

‘Capital asset situated in India’ would include any share or interest in a

foreign company or entity, if such share or interest derives, directly or

indirectly, its value substantially from the assets located in India

5

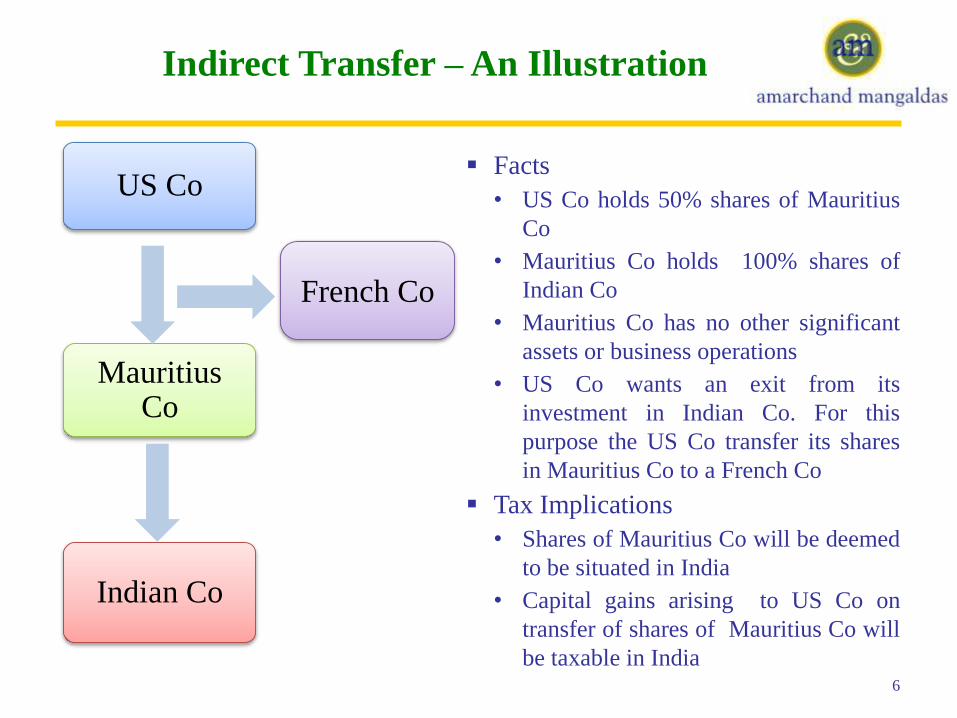

Indirect Transfer – An Illustration

Facts

• US Co holds 50% shares of Mauritius

Co

• Mauritius Co holds 100% shares of

Indian Co

• Mauritius Co has no other significant

assets or business operations

• US Co wants an exit from its

investment in Indian Co. For this

purpose the US Co transfer its shares

in Mauritius Co to a French Co

Tax Implications

• Shares of Mauritius Co will be deemed

to be situated in India

• Capital gains arising to US Co on

transfer of shares of Mauritius Co will

be taxable in India6

US Co

Mauritius Co

Indian Co

French Co

Issues In Indirect Transfer

Meaning of the term ‘substantial’

• Term not defined in the IT Act for the purpose of indirect transfer

• Other sections of the IT Act prescribes a threshold in the range of 20% to 50%

• Shome Committee Report prescribed a threshold of 50%

• DTC 2010 had prescribed a threshold of 50%. DTC 2013 brought down the

threshold to 20%

• Timing of determination of substantial

• Delhi HC in 2014 in the Copal case prescribed a threshold of 50%

‘Shareholding threshold’ in the intermediate company

• No threshold under the IT Act

• Shome Committee Report has prescribed a threshold of 26% of voting power and

share capital in the intermediate company

• DTC 2013 has prescribed a threshold based on the control and management and

effective holding of 5% of voting share capital in the Indian Co

7

Issues In Indirect Transfer

Quantum of tax liability in India

• No mechanism to compute the proportionate tax liability in India

• In fact, section 9(1)(i) seems to suggest that the entire gains arising from transfer

of shares of foreign company may be taxable in India

• LTCG / STCG could be determined based on the period of holding of the shares

of the intermediate company

• What if a significant business of the Indian entity was bought recently?

• Indexation benefit may be available

Rate of tax

• Short term capital gains at the rate of 40%

• Long term capital gains at the rate of 20%/ 10% - debatable

8

Taxability of Capital Gains under

the DTAA

Overview of Capital Gains Article

Taxability of capital gains - Article 13 of OECD MC and UN MC

Taxability of capital gains derived on alienation of properties is dependent

on the nature of asset alienated

‘may be taxable’ - Articles 13(1), 13(2), 13(4) and 13(5) v. ‘shall be taxable

only’ [Articles 13(3) and 13(6)]

No distinction is drawn between Long Term and Short Term Capital Gains

The mode of computation is not provided in the DTAA. Accordingly,

provisions of IT Act dealing with sale consideration, cost of acquisition,

period of holding , rate of tax would be applicable

10

Meaning of certain terms

Capital Gains not defined under the DTAA – to be interpreted as per IT Act

[Section 2(14)]

Meaning of the term ‘alienation’

• Not defined in most DTAAs

• Commentary to UN MC (2011) defines ‘alienation’ to include sale or exchange of

property and also partial alienation, expropriation, transfer to a company in

exchange for stock, sale of a right, gift and passing of property on death

• India–Mauritius DTAA and India- Sri Lanka DTAA defines ‘alienation’ to

include sale, exchange, transfer, or relinquishment of property or the

extinguishment of any rights therein or compulsory acquisition under law

• The definition of ‘transfer’ as used under the IT Act cannot be used to interpret

the term alienation [Sanofi Pasteur Holding SA, [2013]30 taxmann.com 222

(Andhra Pradesh)]

• Protocol to India-Canada DTAA specifically provides that the term ‘alienation’

includes ‘transfer’within the meaning of the IT Act

11

Article 13(1) – Immovable Property

Article 13(1) of UN MC

“Gains derived by a resident of a Contracting State from the alienation of

immovable property referred to in Article 6 and situated in the other

Contracting State may be taxed in that other State”

Article 13(1) of OECD MC is pari materia to Article 13(1) of UN MC

Immovable property would inter alia include

• property accessory to immovable property;

• livestock and equipment used in agriculture and forestry;

• usufruct of immovable property

Situs of immovable property

• Immovable property should be situated in the source state

• Article 13(1) would not apply if immovable property is situated in the state of

residence or in a third State

12

Article 13(2) - Movable property of a PE

Article 13(2) of UN MC

“Gains from the alienation of movable property forming part of the

business property of a permanent establishment which an enterprise of a

Contracting State has in the other Contracting State or of movable property

pertaining to a fixed base available to a resident of a Contracting State in

the other Contracting State for the purpose of performing independent

personal services, including such gains from the alienation of such a

permanent establishment (alone or with the whole enterprise) or of such

fixed base, may be taxed in that other State.”

Article 13(2) of OECD MC is similar to Article 13(1) of UN MC

The term ‘movable property’ is not defined in UN MC

• IT Act also does not define movable property

• Indian General Clauses Act, 1897 defines movable property to mean all property

other than ‘immovable property’

• Includes intangible property [Vikas Sales Corporation v. CCT (1996) 4 SCC 433

(SC)]

13

Article 13(2) - Movable property of a PE

Article 13(2) may apply to gains derived on alienation of the PE or the fixed

base itself . (e.g. sale of Indian branch)

Article 13(2) may apply even if the movable property is sold after PE ceases

to exist [Cartier Shipping Co. Ltd. v. DDIT (2010) 131 TTJ 129 (Mum)]

In the following decisions it has been held that Article 13(2) may not apply

on return of movable property by PE to HO:

• Van Oord Dredging and Marine Contracts BV v. ADIT (2011 –TII-111-ITAT-

Mumbai)

• Cartier Shipping Co. Ltd. v. DDIT (2010) 131 TTJ 129 (Mum)

Irrelevant Factors

• Location of movable property whether within or outside the source state

• Sale of movable property whether within or outside the source state

14

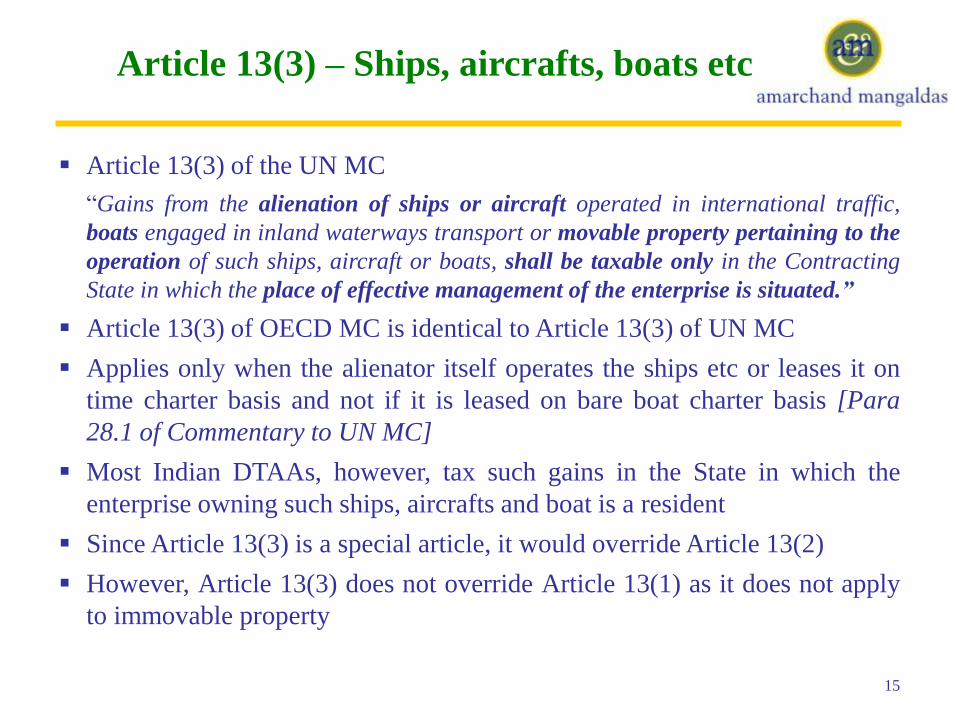

Article 13(3) – Ships, aircrafts, boats etc

Article 13(3) of the UN MC

“Gains from the alienation of ships or aircraft operated in international traffic,

boats engaged in inland waterways transport or movable property pertaining to the

operation of such ships, aircraft or boats, shall be taxable only in the Contracting

State in which the place of effective management of the enterprise is situated.”

Article 13(3) of OECD MC is identical to Article 13(3) of UN MC

Applies only when the alienator itself operates the ships etc or leases it on

time charter basis and not if it is leased on bare boat charter basis [Para

28.1 of Commentary to UN MC]

Most Indian DTAAs, however, tax such gains in the State in which the

enterprise owning such ships, aircrafts and boat is a resident

Since Article 13(3) is a special article, it would override Article 13(2)

However, Article 13(3) does not override Article 13(1) as it does not apply

to immovable property

15

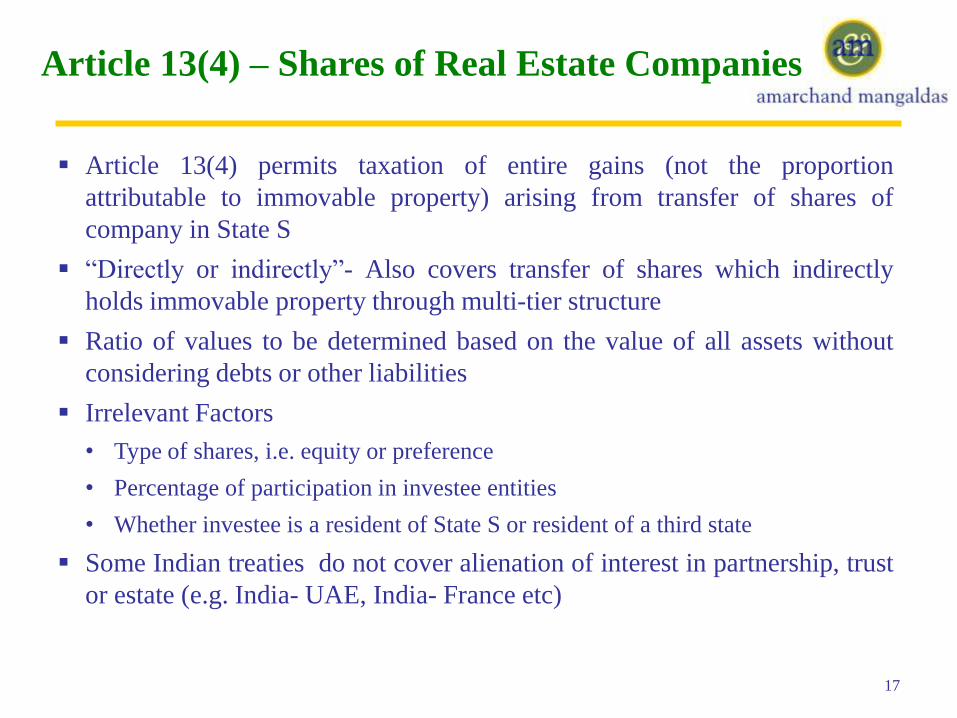

Article 13(4) – Shares of Real Estate Companies

Article 13(4) of the UN MC

“Gains from the alienation of shares of the capital stock of a company, or

of an interest in a partnership, trust or estate, the property of which

consists directly or indirectly principally of immovable property situated in

a Contracting State may be taxed in that State…..”

It also provides specific exemption from application of Article 13(4) to

entities engaged in the business of management of immovable property

To meet the threshold of ‘principally’, value of immovable property should

be >50 % of the aggregate value of all assets

Differences between OECD MC and UN MC

• OECD MC does not cover alienation of interest in partnership, trust or estate

• OECD MC does not exclude companies which is engaged in the business of

management of immovable property

16

Article 13(4) – Shares of Real Estate Companies

Article 13(4) permits taxation of entire gains (not the proportion

attributable to immovable property) arising from transfer of shares of

company in State S

“Directly or indirectly”- Also covers transfer of shares which indirectly

holds immovable property through multi-tier structure

Ratio of values to be determined based on the value of all assets without

considering debts or other liabilities

Irrelevant Factors

• Type of shares, i.e. equity or preference

• Percentage of participation in investee entities

• Whether investee is a resident of State S or resident of a third state

Some Indian treaties do not cover alienation of interest in partnership, trust

or estate (e.g. India- UAE, India- France etc)

17

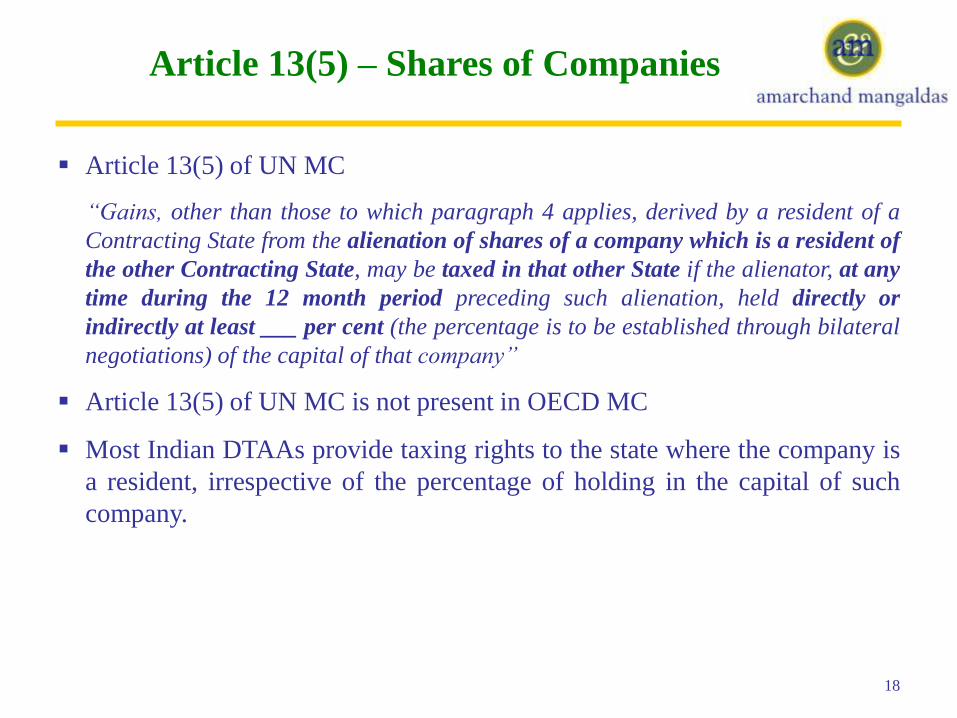

Article 13(5) – Shares of Companies

Article 13(5) of UN MC

“Gains, other than those to which paragraph 4 applies, derived by a resident of a

Contracting State from the alienation of shares of a company which is a resident of

the other Contracting State, may be taxed in that other State if the alienator, at any

time during the 12 month period preceding such alienation, held directly or

indirectly at least ___ per cent (the percentage is to be established through bilateral

negotiations) of the capital of that company”

Article 13(5) of UN MC is not present in OECD MC

Most Indian DTAAs provide taxing rights to the state where the company is

a resident, irrespective of the percentage of holding in the capital of such

company.

18

Article 13(6) – Residuary Provision

Article 13(6) of UN MC

“Gains from the alienation of any property other than that referred to in paragraphs

1, 2, 3, 4 and 5 shall be taxable only in the Contracting State of which the alienator

is a resident.”

Article 13(5) of OECD MC is similar to Article 13(6) of UN MC

Article 13(6) would, inter alia, cover gains from

• Bonds, debentures and units

• Index futures, index options, stock options and stock futures (exchange traded

derivatives)

• Intangibles such as trademark and technology

19

Salient features of some DTAAs

signed by India

Salient features of some DTAAs signed by India

Some of the peculiar characteristics found in the DTAAs signed by India

have been illustrated below:

• No right to tax capital gains arising from transfer of shares of an Indian company

(India-Singapore, India-Mauritius, etc.)

• Right to tax capital gains on transfer of shares of Indian companies if such shares

represent participation of at least 10% (e.g. India- France )

• Right to tax capital gains from alienation of any shares of Indian companies

(Most Indian Treaties including India – Singapore, India – UAE, India – Sri

Lanka)

• Right to tax all types of capital gains to be determined as per the respective

domestic laws (e.g. India-US, India-UK, India-Canada)

21

Salient features of some DTAAs signed by India

India - Singapore DTAA

• Capital Gains from alienation of shares of an Indian company is exempt from tax

in India and taxable only in Singapore

• Such exemption is subject to the Limitation of Benefit clause which provides that

the exemption will not be available if

− Affairs are arranged with the primary objective of taking advantage of the benefits of

capital gains exemption

− Entity which claims to be a resident of Singapore is a shell / conduit. A Singapore

resident is deemed not to be a shell/conduit company if

a. its total annual expenditure on operations in Singapore is not less than S$200,000,

in the immediately preceding period of 24 months from the date the gains arise, or

b. it is listed on a recognized stock exchange of Singapore

22

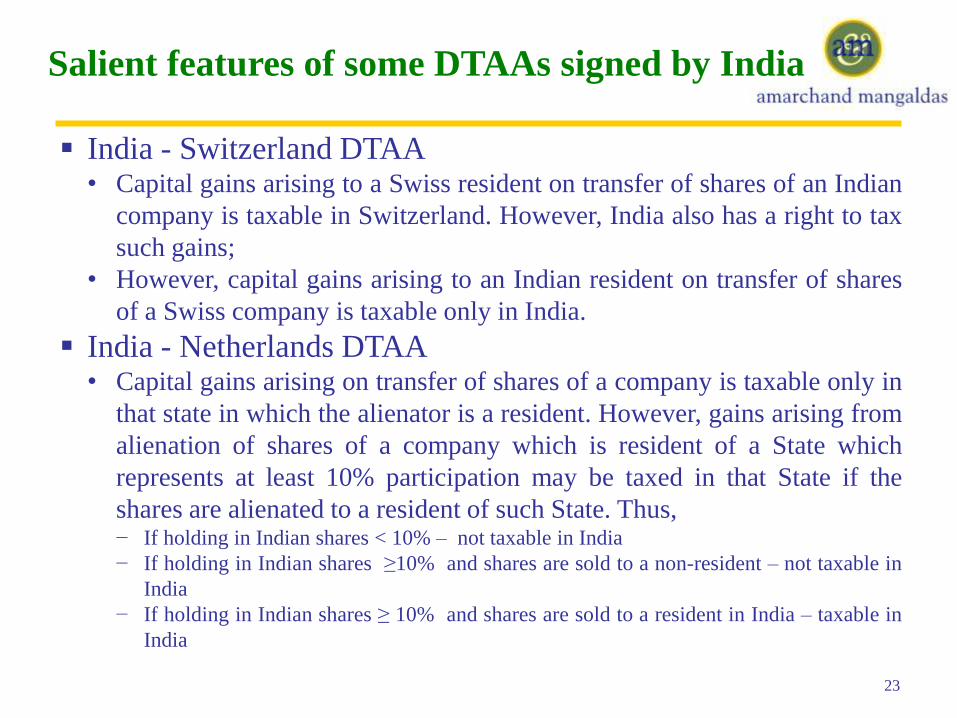

Salient features of some DTAAs signed by India

India - Switzerland DTAA• Capital gains arising to a Swiss resident on transfer of shares of an Indian

company is taxable in Switzerland. However, India also has a right to tax

such gains;

• However, capital gains arising to an Indian resident on transfer of shares

of a Swiss company is taxable only in India.

India - Netherlands DTAA• Capital gains arising on transfer of shares of a company is taxable only in

that state in which the alienator is a resident. However, gains arising from

alienation of shares of a company which is resident of a State which

represents at least 10% participation may be taxed in that State if the

shares are alienated to a resident of such State. Thus,− If holding in Indian shares < 10% – not taxable in India

− If holding in Indian shares ≥10% and shares are sold to a non-resident – not taxable in

India

− If holding in Indian shares ≥ 10% and shares are sold to a resident in India – taxable in

India

23

Salient features of some DTAAs signed by India

India - Malaysia DTAA

• No Article on capital gains

• Article 23 on income from other sources will apply – taxable in India if it ‘arises’

in India

India - Libya DTAA

• No Article on capital gains

• No Article on income from other sources also

• Capital gains may be taxed based on their domestic tax laws - Debatable

India - Ukraine DTAA

• Gains from alienation of properties covered by Article 13(6), i.e. residuary

provision is taxable only in the state where alienator is resident provided that the

gains is subject to tax in that state.

24

Taxability of indirect transfers

under the DTAAs

Taxability of indirect transfers under the DTAAs

As per IT Act, where indirect transfer provisions apply, shares of foreign

company is deemed to be situated in India and accordingly taxed in India

Tax on indirect transfer would be subject to the benefits available under

DTAA [Sanofi Pasteur Holding SA, [2013] 30 taxmann.com 222 (Andhra Pradesh)]

As per Article 13 of the UN MC, shares of foreign company will be covered

under Article 13(6) as

• Article 13(1) – Shares are not an immovable property

• Article 13(2) – Such shares may not be a movable property of a PE

• Article 13(3) – Shares are not ships, aircrafts, boats etc

• Article13(4) – Such shares may / may not be share of a company whose

value consist of principally immovable property in India

• Article 13(5) – Such shares are not shares of an Indian company

• Article 13(6) – Shares of foreign company would, thus, fall within the

ambit of residuary provisions and hence would be taxable only

in the state of which the alienator is a resident

26

Taxability of indirect transfers under the DTAAs

India – US DTAA (Article 13)Capital gains is taxable in both the contracting states in accordance with the

provisions of their domestic law. Thus, India has the right to tax indirect transfers

under India-US DTAA

India – France DTAA (Article 14)• Gains from alienation of shares representing a participation of at least 10 per

cent in an Indian company would be taxable in India

• Gains from alienation of all other shares would be taxable only in France

• India would not have the right to tax indirect transfers under India-France DTAA

India – Singapore DTAA (Article 13)Gains from alienation of all shares is taxable only in the state in which the alienator

is a resident. Thus, India would not have the right to tax indirect transfers under

India- Singapore DTAA

India – Bangladesh (Article 14)Gains from alienation of any shares of a company is taxable only in the state where

the company is incorporated. Thus, India would not have the right to tax indirect

transfers under India- Bangladesh DTAA27

Withholding tax obligations

Withholding tax obligations

Withholding tax obligation on Purchasers

• A Purchaser is required to withhold tax u/s 195 of the IT Act on capital

gains arising to a non-resident seller, if such gains are taxable in India;

• To determine whether the sum is taxable in India, beneficial provisions

of DTAA shall have to be taken into consideration

Risk Mitigation measures

• Seller may obtain a certificate u/s 197 from the tax authorities

• Purchaser may obtain a certificate u/s 195 from the tax authorities

• AAR ruling may be obtained

• Funds may be retained in an Escrow account to cover tax, interest and

penalties

• Appropriate tax indemnities may be negotiated from the Seller

• Tax Insurances may be obtained

29

Purchase of Capital Assets

from an NRI

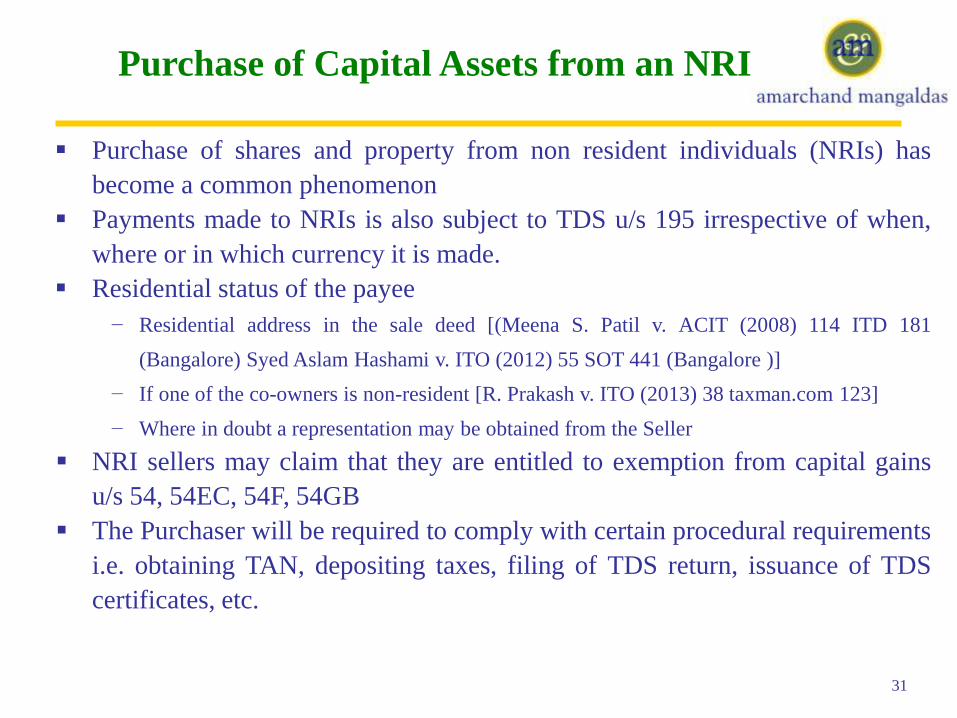

Purchase of Capital Assets from an NRI

Purchase of shares and property from non resident individuals (NRIs) has

become a common phenomenon

Payments made to NRIs is also subject to TDS u/s 195 irrespective of when,

where or in which currency it is made.

Residential status of the payee

− Residential address in the sale deed [(Meena S. Patil v. ACIT (2008) 114 ITD 181

(Bangalore) Syed Aslam Hashami v. ITO (2012) 55 SOT 441 (Bangalore )]

− If one of the co-owners is non-resident [R. Prakash v. ITO (2013) 38 taxman.com 123]

− Where in doubt a representation may be obtained from the Seller

NRI sellers may claim that they are entitled to exemption from capital gains

u/s 54, 54EC, 54F, 54GB

The Purchaser will be required to comply with certain procedural requirements

i.e. obtaining TAN, depositing taxes, filing of TDS return, issuance of TDS

certificates, etc.

31

Case Studies

Copal Research Mauritius Limited, Moody’s

Analytics, USA & Ors.

Facts

• Copal Ltd., Jersey was an offshore entity

which had various subsidies including

Copal Mauritius 1

• Copal Mauritius 1 further owned shares

of Copal India and Copal Mauritius 2

• Copal Mauritius 2 had another

underlying subsidiary, Exevo India

Transactions: (in chronological order)

• Sale of 100% shares of Copal India by

Copal Mauritius 1 to Moody Cyprus

• Sale of 100% Exevo US by Copal

Mauritius 2 to Moody US

• Sale of 67% of Copal Jersey shares held

by its shareholders to Moody UK

33

Issues before Delhi HC

Tax Avoidance

• Whether Transactions 1 and 2 were put in place prima facie for the avoidance of

income tax under the IT Act?

Indirect Transfer

• Whether, if a single transaction (i.e. Transaction 3) had been undertaken, it would

fall within the ambit of indirect transfer under section 9(1)(i) of the IT Act and

hence gains derived there from would have been taxable in India?

34

Delhi HC Judgment

On the issue of tax avoidance

• The Delhi HC held that the set of transactions undertaken was not to avoid tax but

to achieve specific commercial results;

• Effecting the Transactions 1, 2 and 3 by way of a single transaction (Transaction 3)

would not achieve the same commercial result as three separate transactions would

since:

− Transaction 3 would only entitle the Moody Group to an indirect 67% economic interest

in Copal India & Exevo US as opposed to 100% direct control by way of Transactions 1

and 2

− Sale consideration received by Copal Mauritius 1 and Copal Mauritius 2, were ultimately

distributed to the shareholders of Copal Jersey, including banks and financial institutions.

This would not have been possible had the transaction been structured only in the form of

Transaction 3

35

Delhi HC Judgment

On issue of indirect transfer

• The term ‘substantially’ was read by the Delhi HC to be synonymous with

‘principally’, ‘mainly’ or ‘majority’

• The Delhi HC interpreted ‘substantially’ to mean that the shares of the overseas

which is being sold, must derive more than 50% of their value from assets

situated in India

• Relied on

− Shome Committee Report

− Direct Taxes Code Bill, 2010

− OECD MC and UN MC

• Since shares of Copal Jersey derived less than 50% of their value from the

underlying assets in India, even if the entire transaction was structured using only

Transaction 3, it would not have be taxable under section 9(1)(i) of the IT Act

36

Sanofi Pasteur Holding SA

Facts

• SBL was an Indian company 79% of

whose shares were held by ShanH, a

French Company

• Shares of ShanH were in turn held

by two French companies – 80% by

MA and 20% by GIMD

• MA and GIMD transferred their

shares in ShanH to Sanofi, another

France company

Issue

Whether retrospective amendments in

law would impact the provisions of the

DTAA and/or otherwise render the

transaction liable to tax under the

provisions of the IT Act?

37

Andhra Pradesh HC Judgment

Retrospective amendments to the provisions of the IT Act per se cannot

operate to deflect, modify, or subject DTAA provisions to the provisions of

the IT Act

The retrospective amendments to section 9(1) of the IT Act cannot override

the provisions of the DTAA

There is no ambiguity in Article 14(5) about the meaning of ‘alienation’ or

‘participation’ and since these terms are neither employed nor defined in the

IT Act, provisions of Article 3(2) of the India-France DTAA cannot be

invoked

Corporate veil of ShanH would not be pierced, considering that ShanH was

an independent entity that had commercial substance and business purpose

As MA and GIMD had transferred shares of ShanH (a French company),

taxation of capital gains arising on transfer is allocated exclusively to France

under Article 13(5) of the India - France DTAA

38

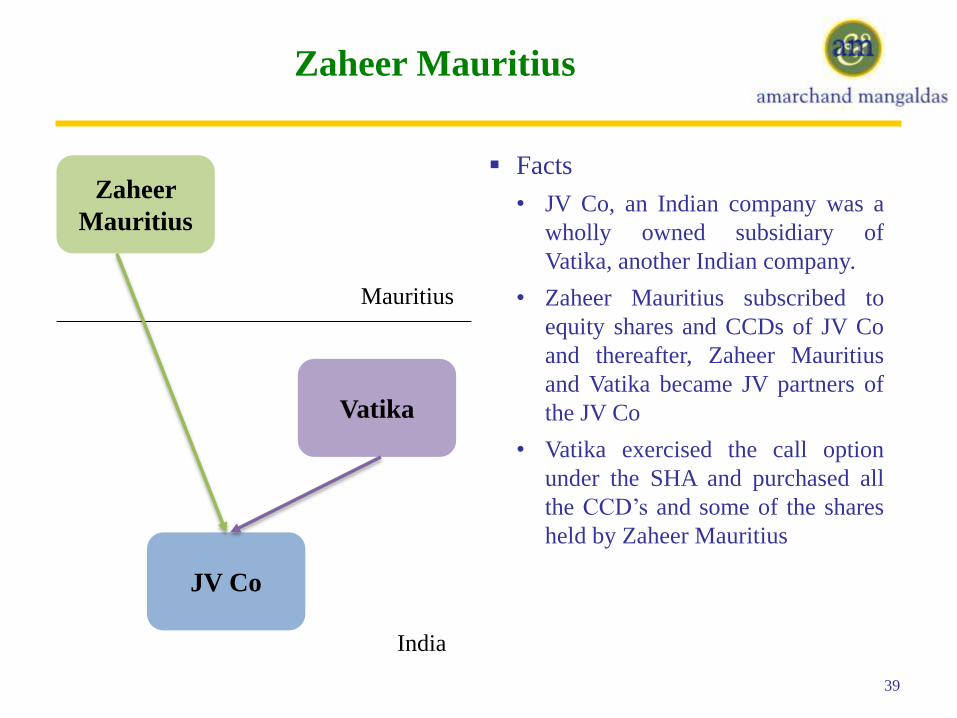

Zaheer Mauritius

Facts

• JV Co, an Indian company was a

wholly owned subsidiary of

Vatika, another Indian company.

• Zaheer Mauritius subscribed to

equity shares and CCDs of JV Co

and thereafter, Zaheer Mauritius

and Vatika became JV partners of

the JV Co

• Vatika exercised the call option

under the SHA and purchased all

the CCD’s and some of the shares

held by Zaheer Mauritius

39

Zaheer

Mauritius

Vatika

JV Co

Mauritius

India

Issues before Delhi HC

Whether the gains arising on transfer of equity shares and CCDs by Zaheer

Mauritius to Vatika is taxable as capital gains or interest income?

Whether the transaction between Zaheer Mauritius and Vatika was a sham

and was essentially a transaction of loan to Vatika camouflaged as an

investment in shares and CCDs of the JV Co?

40

Delhi HC Judgment

On characterisation of income

• The relevant factors for determining whether income on sale of CCD is capital

gains or not is whether the CCD’s are held as capital assets by its holder

• For such determination, it is immaterial whether a CCD is a loan simplicitor or in

the nature of equity

On issue of tax avoidance

• It is a common practice to have covenants for buying each others' stakes to enable

JV partners to exit from JV Co

• This does not convert CCDs into fixed return instruments, as the option to

continue with its investment as an equity shareholder continues to exist

• On review of the clauses of SHA, it held that on lifting the corporate veil, it was

found that Vatika and the JV Co were not the same entity

• Issue of CCD cannot be regarded as designed solely for the purposes of avoiding

tax.

41

Vanenburg Facilities BV

Facts

• Vanenburg NL, a company

incorporated in the Netherlands

has a wholly owned subsidiary,

namely VITPL, in India.

• VITPL is engaged in the business

of developing, operating and

maintaining infrastructure facilities

in India.

• Vanenburg sold 100% shares of

VITPL to Ascendas, a Singapore

based company

Issue

Whether the gains arising on transfer

of shares of VITPL to Ascendas is

taxable as capital gains in India?

42

Vanenburg

NL

Ascendas

VITPL

Singapore

India

Netherlands

Hyderabad Tribunal Judgment

Shares in a company owning immovable property cannot itself be

considered as immovable property

Thus , Article 13(1) of the India- NL DTAA would not apply as Vanenburg

NL did not transfer any immovable property or any rights directly attached

to an immovable property

Article 13(4) of the India- NL DTAA would also not apply as although the

infrastructure facilities held by VIPTL would qualify as immovable

property, the business of VIPTL was carried on through such assets;

Thus the capital gains on sale of shares of VIPTL falls within the ambit of

Article 13(5) being the residual provisions.

Since shares of VIPTL are sold to Ascendas, not being a resident of India,

capital gains would be taxable only in NL.

43

44

Disclaimer

The opinions expressed in this presentation are solely those of the presenter

and not necessarily those of Amarchand & Mangaldas & Suresh A. Shroff & Co.

The objective of this presentation is to provide general information about the

topics being discussed and not meant to be tax advice. Anybody acting on the

basis of this presentation is advised to obtain specific tax advice beforehand.

Thank You

© Amarchand & Mangaldas & Suresh A. Shroff & Co.