taxation of shares & securities · · 2012-01-09taxation of shares & securities ca vishal...

TRANSCRIPT

1

Taxation of Shares & Securities

CA Vishal Gada

Securities- Special emphasis on

taxation issues relating to non-residents

7 January 2012WIRC - Mumbai

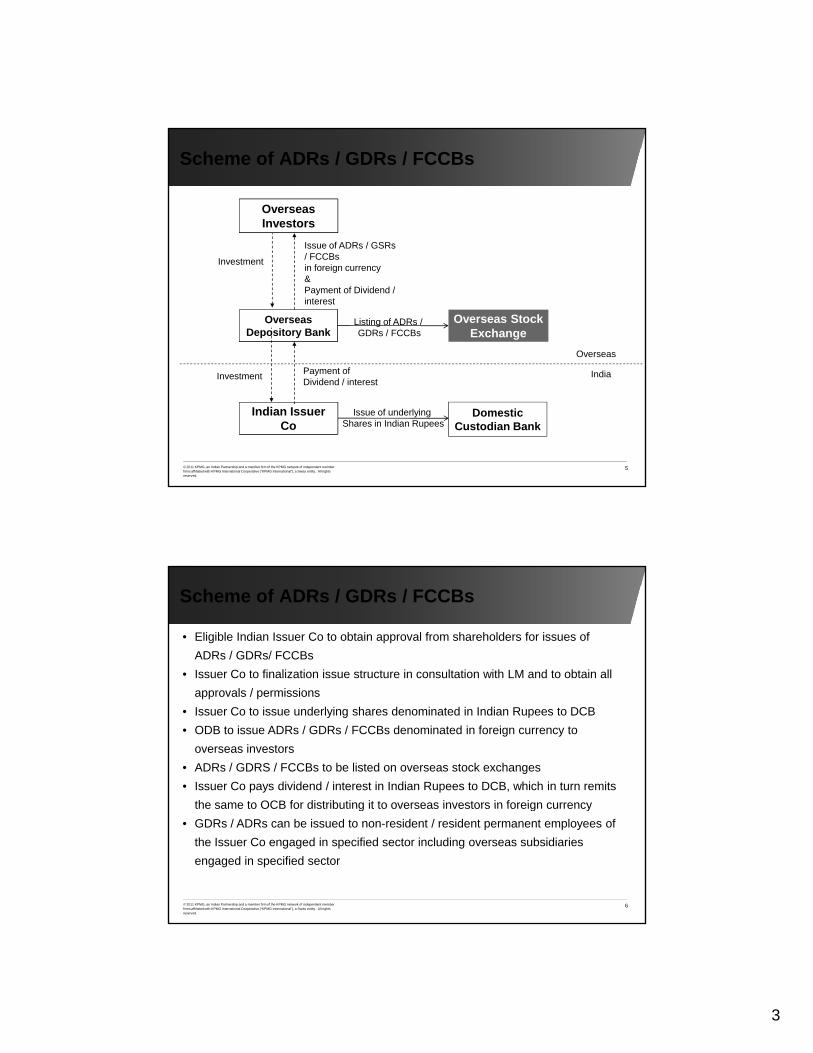

Scheme of ADRs / GDRs / FCCBs

Investment avenue for Non-residents

Contents

Scheme of FCEB & salient features

Taxation of ADRs / GDRs, etc

Benefit of lower rate as per proviso to Section 112(1)

Special Regime - taxation of NRIs, FIIs & OFs

2© 2011 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Zero Coupon Bonds

2

Investment avenues for NRs

Equity Shares

Non-residents

Foreign Currency

ExchangeableBonds (FCEBs)

Preference Shares

AmericanDepository R i t /

Foreign

3© 2011 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Receipts / Global

Depository Receipts

Currency Convertible

Bonds (FCCBs)

Debentures

Scheme of issue of ADRs / GDRs /of ADRs / GDRs / FCCBs

3

Overseas Investors

Issue of ADRs / GSRs

Scheme of ADRs / GDRs / FCCBs

Overseas Depository Bank

Overseas

Overseas Stock Exchange

Issue of ADRs / GSRs / FCCBs in foreign currency&Payment of Dividend / interest

Listing of ADRs / GDRs / FCCBs

P f

Investment

5© 2011 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Indian IssuerCo

Domestic Custodian Bank

IndiaInvestment

Issue of underlying Shares in Indian Rupees

Payment of Dividend / interest

• Eligible Indian Issuer Co to obtain approval from shareholders for issues of

ADRs / GDRs/ FCCBs

• Issuer Co to finalization issue structure in consultation with LM and to obtain all

Scheme of ADRs / GDRs / FCCBs

approvals / permissions

• Issuer Co to issue underlying shares denominated in Indian Rupees to DCB

• ODB to issue ADRs / GDRs / FCCBs denominated in foreign currency to

overseas investors

• ADRs / GDRS / FCCBs to be listed on overseas stock exchanges

• Issuer Co pays dividend / interest in Indian Rupees to DCB, which in turn remits

the same to OCB for distributing it to overseas investors in foreign currency

6© 2011 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

the same to OCB for distributing it to overseas investors in foreign currency

• GDRs / ADRs can be issued to non-resident / resident permanent employees of

the Issuer Co engaged in specified sector including overseas subsidiaries

engaged in specified sector

4

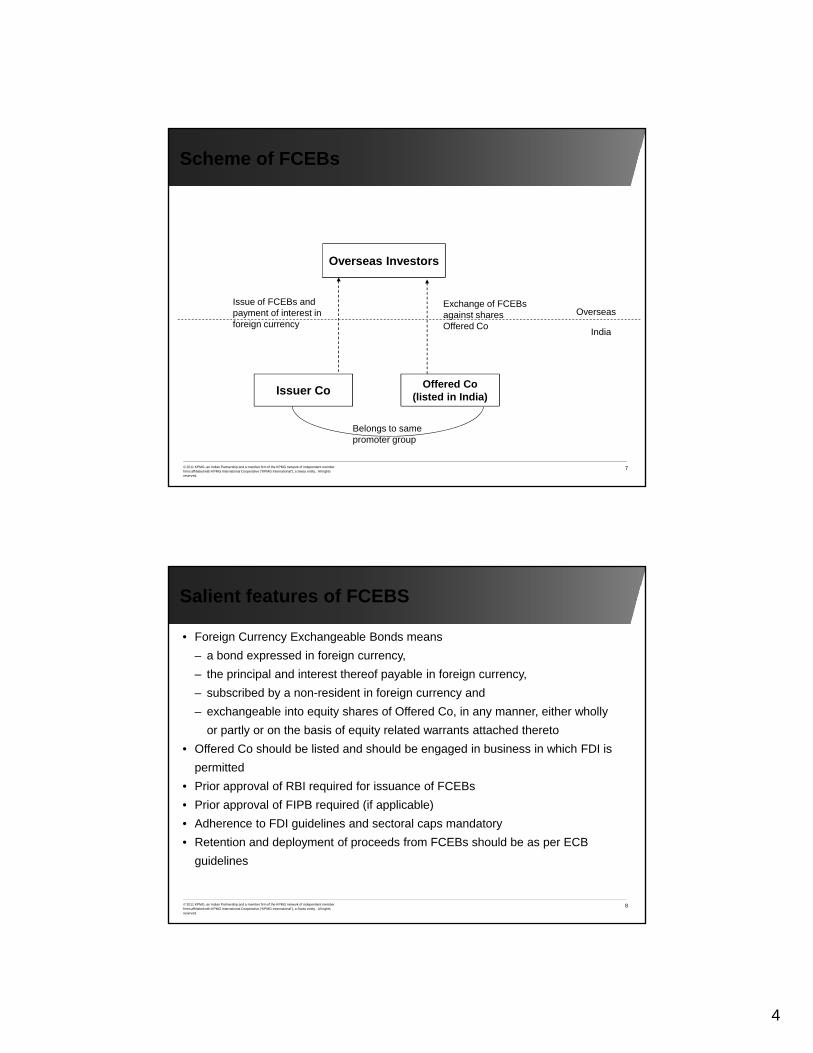

Scheme of FCEBs

Overseas Investors

Issue of FCEBs and payment of interest in foreign currency

Exchange of FCEBs against shares Offered Co

India

Overseas

7© 2011 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Offered Co (listed in India)Issuer Co

Belongs to same promoter group

• Foreign Currency Exchangeable Bonds means

– a bond expressed in foreign currency,

– the principal and interest thereof payable in foreign currency,

Salient features of FCEBS

– subscribed by a non-resident in foreign currency and

– exchangeable into equity shares of Offered Co, in any manner, either wholly

or partly or on the basis of equity related warrants attached thereto

• Offered Co should be listed and should be engaged in business in which FDI is

permitted

• Prior approval of RBI required for issuance of FCEBs

• Prior approval of FIPB required (if applicable)

8© 2011 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

• Prior approval of FIPB required (if applicable)

• Adherence to FDI guidelines and sectoral caps mandatory

• Retention and deployment of proceeds from FCEBs should be as per ECB

guidelines

5

Taxation of ADRs, GDRs, etc.

© 2011 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Taxation of Dividend / interest

• Dividend on ADRs / GDRs / Shares

– Exempt from tax in India in the hands of overseas investors

– Indian Co to pay DDT @ 16.223% under Section 115O

• Interest on FCCBs / FCEBs

– Taxable in India @ 10%* under Section 115AC

– Indian Co liable WHT under Section 196C

– Applicability of tax treaty?

10© 2011 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

*plus applicable surcharge and cess

6

Transfer / redemption of ADRs etc outside India

• Transfer of ADRs / GDRs / FCCBs / FCEBs outside India by NR to NR is not

taxable transfer in India under Section 47(viia)

• Transfer / Conversion of FCEBs/ FCCBs into shares is not taxable in India

under Section 47(xa)

• Redemption of ADRs / GDRs into underlying shares – whether taxable in India?

11© 2011 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Transfer of ADRs etc in India

• Held of 3 years or more - long term capital gains on transfer of ADRs / GDRs /

FCCBs / FCEBs taxable in India in the hands of NRs / resident employees @

10%* under Section 115AC / 115ACA

• Held for less then 3 years - short term capital gains on transfer of ADRs / GDRs

/ FCCBs / FCEBs taxable in India in the hands of NRs / resident employees as

per normal tax rates (as applicable)

12© 2011 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

*plus applicable surcharge and cess

7

Taxation of shares after redemption

• Underlying shares held for 1 year or more - Long term capital gains taxable @ 10%*

• Underlying shares held for less than 1 year - short term capital gains taxable as

normal income or @ 15%* under Section 111A (as applicable)

C t f i iti f d l i h ld b i ili t k h• Cost of acquisition of underlying shares would be price prevailing on stock exchange

on the date on which the ODB advises the DCB

• Period of holding of underlying shares shall be reckoned from the date on which the

ODB advises the DCB

• Cost of acquisition of shares on conversion of FCCBs

– As per Section 49 – cost in relation to FCCBs,

– As per Scheme# – price determined on the basis of the price of the shares on

13© 2011 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Indian stock exchange on the date of conversion of FCCBs into shares

• Right or Bonus ADRs / GDRs / Shares – not taxable

*plus applicable surcharge and cess# Issue of Foreign Currency Convertible Bonds and Ordinary Shares (Through Depository Receipt Mechanism) Scheme, 1993

Whether Act will prevail over Scheme to determine cost of acquisition of shares on conversion of FCCBs?

Applicability of tax treaty

• Paragraph 10 of the Scheme# provide that

– During the period of fiduciary ownership of shares by ODB, the provision of

tax treaty between India and country of residence of ODB will apply to

determine taxation of dividend and interest

– During the period, when the redeemed underlying shares are held by NR, the

provisions of tax treaty between India and country of residence of NR will

apply to determine taxation of dividend, interest and capital gains on transfer

of underlying shares

14© 2011 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

# Issue of Foreign Currency Convertible Bonds and Ordinary Shares (Through Depository Receipt Mechanism) Scheme, 1993

8

Case Study 1

• A Ltd., a company incorporated under the Indian

Laws, has issued Foreign Currency Convertible

Bonds (‘FCCB’) with an option of conversion of

the same to equity shares or redemption at athe same to equity shares or redemption at a

premium at the end of the tenure / at the time of

maturity.

• In such a scenario request you to share your

thoughts in relation to the following:

– Tax treatment of the premium at the time of

redemption under the Income-tax Act,

15© 2011 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

p

1961(i.e. whether the same would be

treated as interest or capital gains)– Withholding tax implications (i.e. rate at which

tax needs to be withheld at the time of

redemption)

Case Study 2

• ABC Ltd., a company incorporated under

the Indian Laws, has issued FCCB through

its overseas depository bank i.e., Deutsche

Bank, London (a branch of Germany).

• In this connection, request you to share

your thoughts in relation to the applicability

of the Tax Treaty vis-à-vis payment of

interest.

16© 2011 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Para10 of Scheme# - Application of Avoidance of Double Taxation Agreement in case of Global Depositary Receipts

# Issue of Foreign Currency Convertible Bonds and Ordinary Shares (Through Depository Receipt Mechanism) Scheme, 1993

9

Case Study 3…

• ABC Ltd., an Indian Company, had

issued FCCB and are listed on

Singapore Stock Exchange.

• The funds were raised with an intention

of using them for capital expenditure,

including capacity expansion and for any

other uses as may be permitted from

time to time under relevant laws,

regulations and guidelines.

17© 2011 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

• ABC Ltd. is contemplating to buyback

FCCBs, which are quoted at a discount,

through the Stock Exchange at the

prevailing market price and will be

cancelled after the buy back.

…Case Study 3

In such a scenario request you to share your

thoughts on taxability of the gain arising on buy back

and cancellation of FCCB under the provisions of the

Income Tax Act, 1961:

• Whether the gain arising on buy-back (being the

difference between the buy-back price and issue

price) and subsequent cancellation of the FCCB

can be considered as an income?

• Whether the gain is a revenue receipt or capital

receipt?

18© 2011 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

• If the income is a capital receipt, whether it is

specifically liable to tax by virtue of:

– Section 41(1) of the Act as business income; or

– Section 28 of the Act as business income; or

– Section 45 of the Act as capital gains

10

Benefit of lower rate as per proviso to Section 112(1)

19© 2011 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Benefit of lower rate of tax

• Section 112(1) provides for tax rates in respect LTCG for residents as well asNRs (@ 20%*)

• Proviso to Section 112(1) provides that where the tax payable in respect of• Proviso to Section 112(1) provides that where the tax payable in respect ofLTCG arising from the transfer of “listed securities” or “units” or “ZCB” exceeds10 percent of the amount of capital gains ‘before giving effect to the provisionsof the second proviso to Section 48 of the Act’, then, such excess shall beignored for the purposes of computing tax payable by the assessee

20© 2011 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Whether benefit of lower rate of tax u/s 112 is available to non-residents vis-à-vis sale of shares or debentures?

*plus applicable surcharge and cess

11

Benefit of lower rate of tax

• Section 48 of the Act provides the computation mechanism for capital gains

arising under Section 45 of the Act. As per Section 48, capital gains should be

computed after reducing the cost of acquisition and cost of improvement from

the sale consideration of the capital assetthe sale consideration of the capital asset

– First proviso to S. 48 (applicable only to NRs) – provides for the computation

mechanism of capital gains arising from transfer of shares or debentures of

an Indian company (acquired in foreign currency)

– Second proviso to S. 48 (applicable to all assessees) – provides for the

indexation benefit to residents on all capital assets and to NRs on capital

assets other than specified in first proviso

Thi d i t S 48 B d d D b t l d d f th

21© 2011 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

– Third proviso to S. 48 - Bonds and Debentures are excluded from the

indexation benefit (except Capital indexed bonds issued by the Government)

Whether benefit of lower rate of tax u/s 112 is available to non-residents vis-à-vis sale of shares or debentures?

Cairn UK Holdings Ltd.*, In re

• Proviso to Section 112 is applicable to both, residents as well as NRs

• Phrase ‘before giving effect to’ implies that for application of proviso to Section 112 of the Act, the asset must be qualified for CII benefit under second proviso q pto Section 48 of the Act

• If proviso to Section 112 was supposed to apply also to the first proviso to Section 48 which gives benefit of exchange fluctuation protection to NR taxpayers, specific inclusion to that effect would have been made

• Since the benefit of lower rate of tax at 10% was already available to NRs, in order to bring level playing field for the residents, concessional rate of 10% was

22© 2011 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

g p y g ,inserted by the Finance Act, 1999

• NRs which are given protection against inflation in respect of shares/debentures of an Indian company and which are kept out of CII benefit in respect of such assets, are not eligible for double benefit of 10% under S. 112 of the Act

* (2011) 12 taxmann.com 266 (AAR)

12

Timken France*, In re

• Benefit of the proviso to section 112(1) could not be denied to foreign

companies who were also entitled to relief in terms of first proviso to section 48.

Clear words would have been deployed in the proviso if one particular category

i.e. non-residents were to be excluded. The eligibility to avail the benefit of

indexed cost of acquisition was not a sine qua non for applying the reduced rate

of 10 percent. It was only a mode of computation of capital gains

• If tax authorities’ contention accepted, even Zero coupon bonds (ZCBs) and

debentures will go out of the purview of section 112 which not intended

23© 2011 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

• As per CBDT Circular No. 554, the first proviso to section 48 was introduced to

compensate non-resident Indian investors for the lower earning in foreign

currency on account of the decline of rupee value.

* (2007) 294 ITR 513 (AAR)

Timken France, In re

• As per CBDT Circular No. 636, the second proviso to section 48 was introduced as a measure to off-set the effect of inflation. Further, non-residents were excluded from the purview of second proviso. As protection from fluctuation in rupee value in terms of foreign currency ensured protection from inflation,rupee value in terms of foreign currency ensured protection from inflation, further relief in terms of indexation would not be available to non-residents who would enjoy the concession available in the first proviso to section 48.

• The tax authorities contended that the taxpayer could not claim double benefit. However, the AAR held that double benefit or additional relief was not a taboo under the law. Merely because the non-residents got protection from rupee value fluctuation in terms of foreign currency, it did not follow that the non-

id t h ld t t th b fit f d d t f t hi h th id t

24© 2011 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

residents should not get the benefit of reduced rate of tax which the residents were getting. The protection in terms of first proviso to section 48, made available to a non-resident, might be a justification to deny the benefit of cost of indexation as stated in CBDT Circular No. 636, but, the same could not be said to apply to lesser rate of tax.

13

Other relevant decisions

Favourable decisions

• Alcan Inc. v. DDIT (2007) 112 TTJ 328 (Mum)

• Mc Leod Russel Kolkata Ltd. (2008) 215 CTR (AAR) 230

B rmah Castrol Plc In re (2008) 307 ITR 324 (AAR)• Burmah Castrol Plc , In re (2008) 307 ITR 324 (AAR)

• Fujitsu Services Ltd., In re (2009) 225 CTR 121 (AAR)

• Four Star Oil & Gas Co., In re (2009) 312 ITR 104 (AAR)

• Compagnie Financiere Hamon, In re (2009) 310 ITR 1 (AAR)

• Chicago Pneumatic Tool Company v. DDIT [2009-TII-110-ITAT-MUM-INTL]

• Hoechst GMBH v. ADIT [2010-TII-54-ITAT-MUM-INTL ]

A i t d i i

25© 2011 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Against decision

• BASF Aktiengesellschaft v. DDIT (2007) 12 SOT 451 (MUM)

Special Regime -taxation of NRIs, ,FIIs and Offshore Funds

26© 2011 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

14

Taxation of NRIs

• Transfer of foreign exchange asset purchased by NRIs in convertible foreign

exchange

– Investment income taxable @ 20%* under Section 115E

– Long term capital gains taxable @ 10%* under Section 115E

o In case, sale proceeds are invested in specified assets within a period of six

months, the following amount, subject to total amount of capital gains, will

not be taxable:Cost of specified asset X capital gains

Net consideration of sale of foreign exchange assets

27© 2011 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

*plus applicable surcharge and cess

Taxation of FIIs

• Long term capital gains on transfer of securities taxable @ 10%* under Section

115AD

• Short term capital gains on transfer of securities taxable @ 30%* under Section

115AD

– Short term capital gains on transfer of equity shares on recognized stock

exchange and upon payment of STT is taxable @ 15%* under Section

111A

28© 2011 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

*plus applicable surcharge and cess

Can FIIs opt out of 115AD and choose to be governed by proviso to Section 48, if the same is beneficial?

15

Taxation of Offshore Funds

• Income in respect of units of Mutual Fund purchased in foreign currency taxable

@ 10%* under Section 115AB

• Long term capital gains on transfer of such units taxable @ 10%* under Section

115AB

• Benefit of indexation not available

• Short term capital gains on transfer of such units taxable as per normal tax rates

(as applicable)

29© 2011 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

*plus applicable surcharge and cess

Zero Coupon Bonds

30© 2011 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

16

Zero Coupon Bonds

• Zero Coupon Bond are defined under Section 2(48) to mean a bond issued

by infrastructure capital company / fund or public sector company or schedule

bank on or after 1 June 2005, in respect of which no payment and benefit is

received or receivable before maturity of redemption from issuer and which thereceived or receivable before maturity of redemption from issuer and which the

Central Government notify

• Definition of ‘transfer’ under Section 2(47) includes inter alia ‘the maturity or

redemption of a zero coupon bond’

• Third proviso to Section 48 - “Provided also that nothing contained in the

second proviso shall apply to the long-term capital gains arising from the

31© 2011 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

second proviso shall apply to the long term capital gains arising from the

transfer of a long term capital asset being bond or debenture other than capital

indexed bonds issued by the Government”

Zero Coupon Bonds

• Proviso to Section 112(1) – “Provided that where the tax payable in respect of

any income arising from the transfer of long term capital asset, being listed

securities or units or zero coupon bond*, exceeds 10 percent of the amount of

capital gains ‘before giving effect to the provisions of the second proviso tocapital gains before giving effect to the provisions of the second proviso to

Section 48 of the Act’, then, such excess shall be ignored for the purposes of

computing tax payable by the assessee”

• Memorandum to Finance Bill 2005 – concerning taxation of zero coupon

bonds - With a view to rationalizing the tax treatment of zero coupon bonds, it is

proposed to treat the income on transfer of a zero coupon bond (not being

stock-in-trade) as capital gains……Provisions of Section 112 are also proposed

32© 2011 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

stock in trade) as capital gains……Provisions of Section 112 are also proposed

to be amended so as to bring parity with other securities. Consequently long

termcapital gains on zero coupon bonds will be subject to tax at ten per cent. if

the tax payer does not claim the benefit of indexation.

17

Relevant Decisions

• Relevant observations in Timken France, In re (2007) 294 ITR 513 (AAR)

“We shall first turn our attention to ZCBs. The third proviso to Section 48 which was

introduced by the Finance Act, 1997, ordains "nothing contained in the second proviso

shall apply to the long-term capital gains arising from the transfer of a long-term capital

asset being bond or debenture other than capital indexed bonds issued by the

Government". Thus, for computation of capital gains under Section 48 in respect of ZCBs,

the benefit of second proviso to Section 48 is specifically excluded by the third proviso to

Section 48. When the second proviso to Section 48 is thus excluded in relation to ZCBs, it

should logically follow, if the revenue’s contention is accepted, that ZCBs should also go

out of purview of the proviso to Section 112(1) whereas ZCB was specifically included by

way of amendment of the proviso admittedly with a view to extend the benefit of

33© 2011 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

concessional rate of 10 per cent to such bonds . Otherwise, the amendment inserting

ZCBs in the proviso to Section 112(1) will be infructuous. It is nobody’s case that ZCBs

answering the description of long-term assets should be subjected to the normal 20 per

cent tax under the substantive provision of Section 112.”

Relevant Decisions

• Relevant observations in Cairn UK Holdings Ltd., In re (2011) 12 taxmann.com 266

(AAR)

“The 3rd proviso to Section 48 of the Act brings out distinction in the species of

bonds when it excludes 'bonds ' which are 'capital indexed bonds issued by the

Government'. Just as there are 'capital indexed bonds issued by the Government', there

is another specie of bonds called 'zero coupon bonds ' of separate and distinct nature to

which reference is made by the proviso to Section 112(1). The Legislature is conscious of

this fact…..

…the Finance Act, 2005 inserted 'zero coupon bond ' as one of the assets along with

'securities' and 'unit' in the proviso to Section 112(1). We have already noted that

'zero coupon bond ' and 'bond ' are different financial instruments. The 3rd proviso

34© 2011 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

therefore does not include 'zero coupon bond ' and hence the 'zero coupon bond ' is

eligible for indexation under the 2nd proviso to Section 48 of the Act.”

18

Case Study - Zero Coupon Bonds

Background

• Mr. A subscribes to Zero Coupon Bonds

issues by VG Ltd, an infrastructure capital

company

• ZCBs are issued at discount with maturity of

15 years

Issue

• Whether discount is taxable in the hands of

Mr A over the tenure of ZCBs?

35© 2011 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Mr. A over the tenure of ZCBs?

• Whether gains on redemption of ZCBs on

maturity, would be taxable?

• Whether the benefit of indexation benefit

would be available?

BangaloreSolitaire, 139/26, 3rd Floor, Inner Ring Road,Koramangala,Bangalore 560071Tel +91 80 3980 6000Fax +91 80 3980 6999

ChandigarhSCO 22-231st floor. Sector 8 CMadhya MargChandigarh 160019Tel : 0172 3935778

Kochi4/F, Palal Towers,M. G. Road,Ravipuram, Kochi 682016Tel +91 (484) 302 7000Fax +91 (484) 302 7001

KolkataInfinity Benchmark, Plot No.G-1, 10th floor, Block - EP & GP, Sector - V, Salt Lake CityKolkata 700091Tel: +91 33 44034066

© 2011 KPMG, an Indian Partnership and a member firm of the KPMG network of independent

Tel : 0172 3935778Fax 0172 3935780

ChennaiNo. 10, Mahatma Gandhi Road, Nungambakam, Chennai 600 034Tel +91 40 3914 5000Fax +91 40 3914 5999

DelhiBuilding No.10, Tower B, 8th Floor, DLF Cyber City, Phase – IIG 122002 H

Tel: +91 33 44034066Fax: +91 33 4403 4199

MumbaiLodha Excelus, 1st Floor, Apollo Mills Compound, N.M. Joshi Marg, Mahalakshmi, Mumbai 400 011Tel +9122 39896000 Fax +91 22 39836000

Pune703, Godrej Castlemaine Bund Garden Pune 411 001

Thank You

member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The KPMG name, logo and "cutting through complexity" are registered trademarks or trademarks of KPMG International Cooperative ("KPMG International").

Gurgaon 122002 HaryanaTel +91 124 3074000Fax +91 124 2549101

Hyderabad8-2-618/2Reliance Humsafar, 4th FloorRoad No. 11, Banjara HillsHyderabad 500 034Tel +91 40 6630 5000Fax +91 40 6630 5299

Tel: +91 20 3058 5764/ 65Fax: +91 20 30585775