taxation & representation in africa - mcgill university · taxation & representation in...

TRANSCRIPT

Taxation & Representation in

Africa Determinants of Local and State Budgeting

and Revenue Generating Priorities

Olufunmbi M. Elemo

Department of Political Science

Michigan State University

Institute for the Study of International

Development

McGill University

Friday, March 22, 2013

Main Question

Under what conditions are African local and state governments more likely to spend public revenues on public services?

◦ Growing Duties for Local and State Governments

◦ New Authority to Raise Revenue via Taxation

◦ What determines Local and State Government spending?

So What?

Practical Implications ◦ Africans report “representing the people” as

elected official’s most important responsibility

◦ Concrete policy prescriptions for expanding representation across levels of government

Theoretical Implications: Revenue and Governance ◦ Taxation Representation

◦ “Oil impedes Democracy”

Literature is Too Broad

Theoretical Framework

Gibson and Hoffmann (2006)

◦ Local Governments in Tanzania and Zambia

◦ “Do sources of revenue affect government

expenditure?”

◦ Tax Revenue Spending on Public Services

◦ Non-Tax Revenue Spending on

Government Salaries

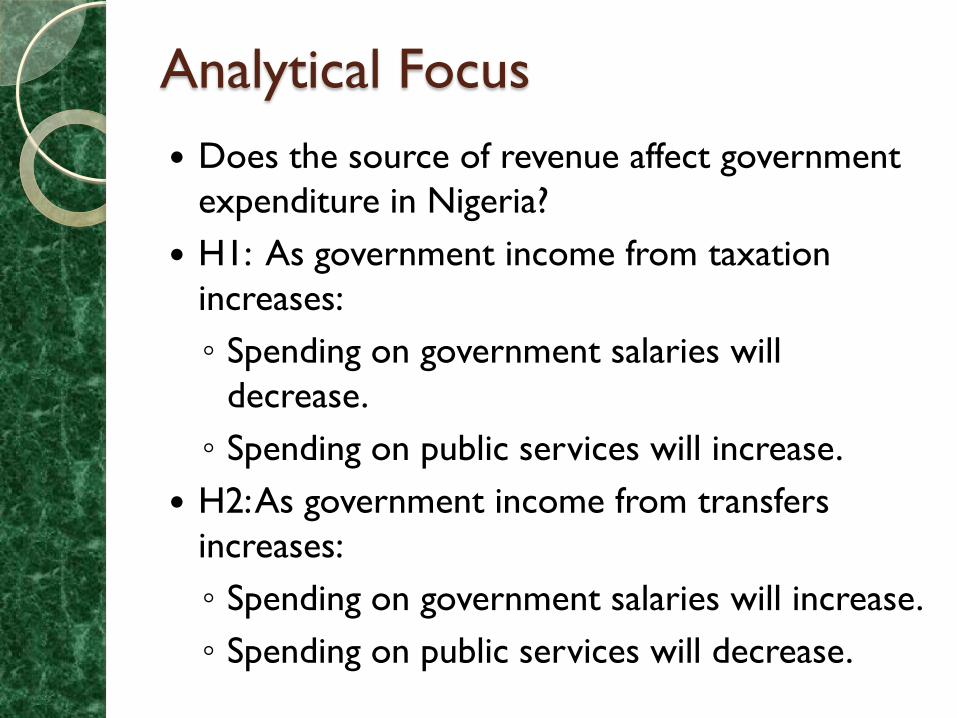

Analytical Focus

Does the source of revenue affect government

expenditure in Nigeria?

H1: As government income from taxation

increases:

◦ Spending on government salaries will

decrease.

◦ Spending on public services will increase.

H2: As government income from transfers

increases:

◦ Spending on government salaries will increase.

◦ Spending on public services will decrease.

Analytical Focus: Why Nigeria?

6

Analytical Focus: Why Nigeria?

7

Research Design

Research Design

774 Local Governments, 2000 – 2004 and 2008

36 State Governments, 2000 – 2003 and 2007 –

2009

Central Bank of Nigeria Annual Statements, 1999

– 2009

Controls: Population, Area, Socio-Economic

Capacity, Size of Economy

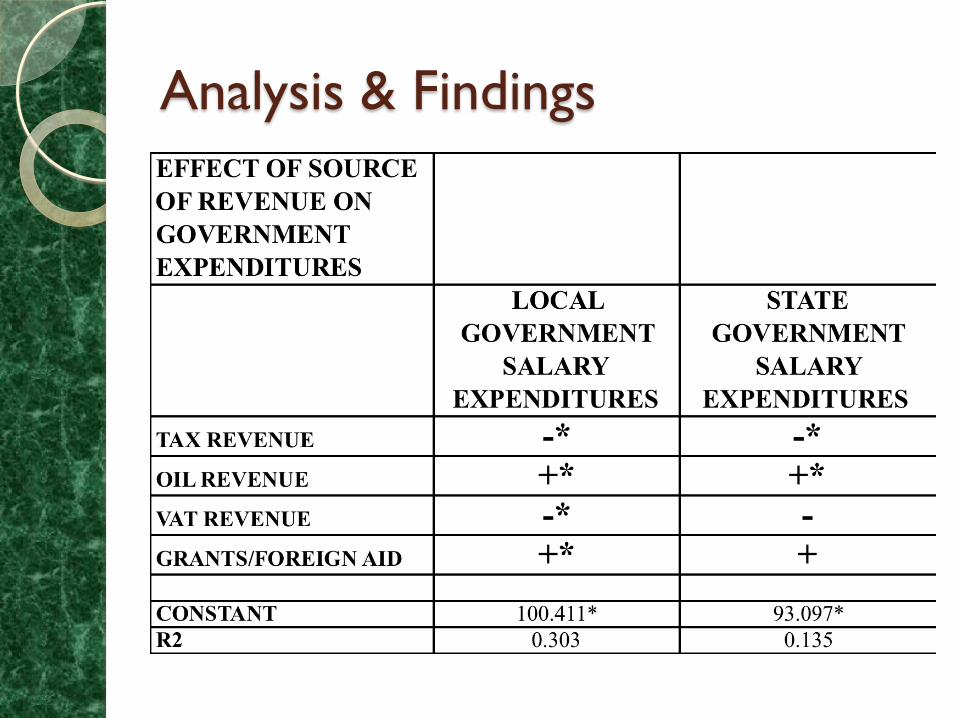

Analysis & Findings

Disaggregating the Results

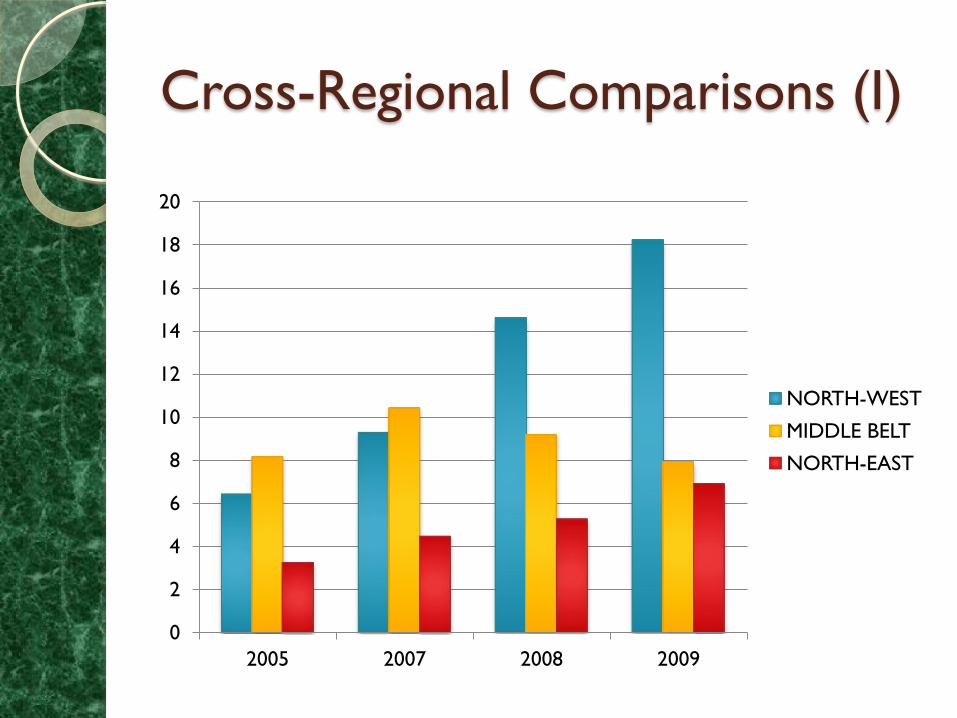

Cross-Regional Comparisons (I)

0

2

4

6

8

10

12

14

16

18

20

2005 2007 2008 2009

NORTH-WEST

MIDDLE BELT

NORTH-EAST

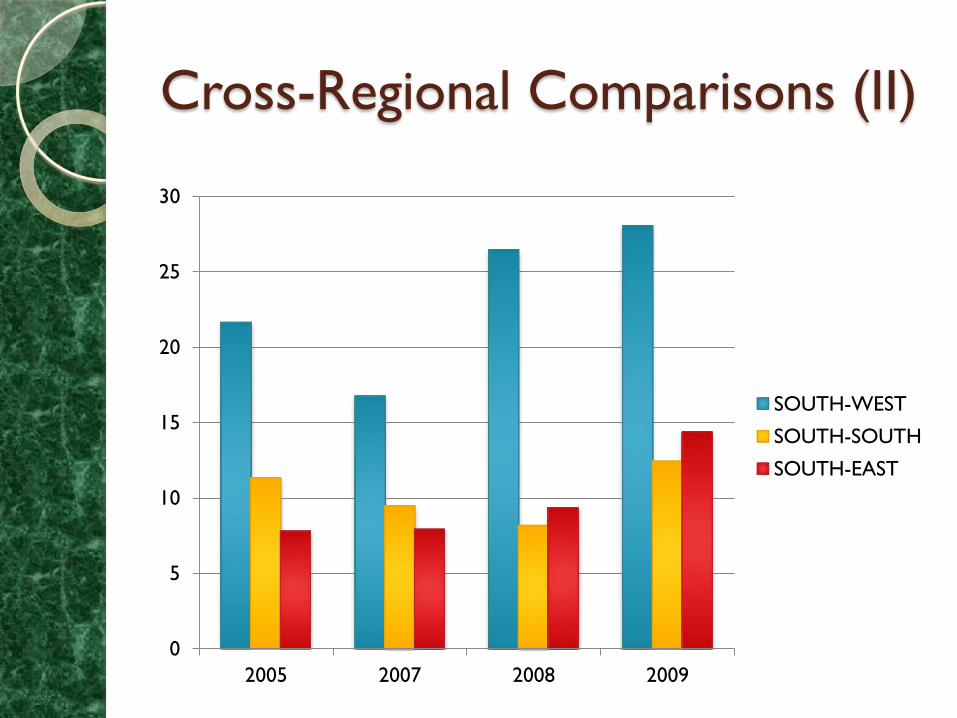

Cross-Regional Comparisons (II)

0

5

10

15

20

25

30

2005 2007 2008 2009

SOUTH-WEST

SOUTH-SOUTH

SOUTH-EAST

Cross-Regional Comparisons (III)

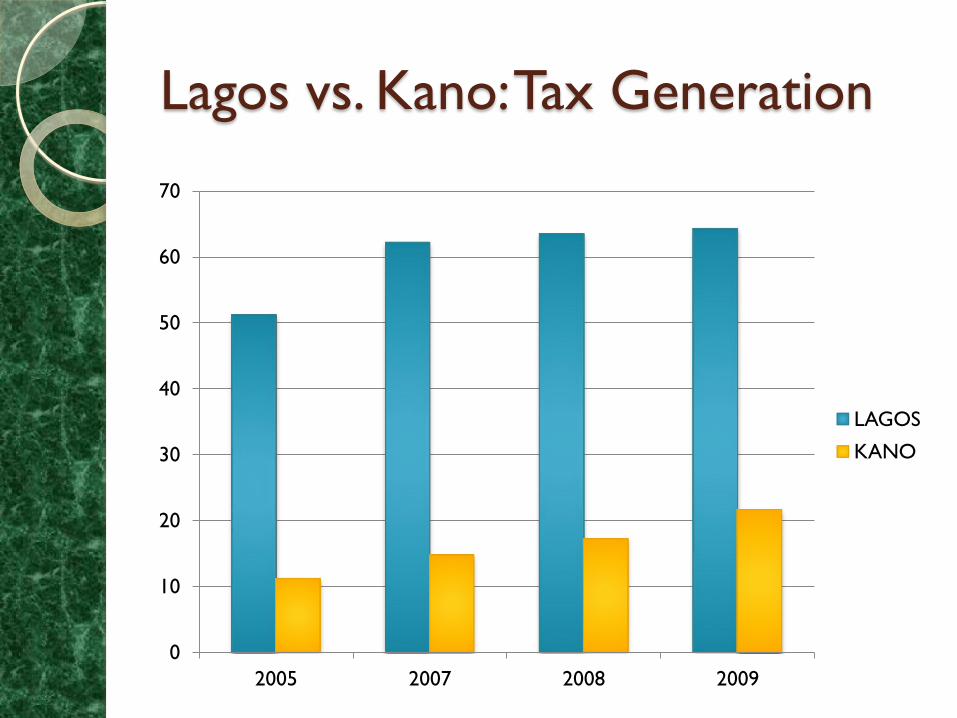

Lagos vs. Kano: Tax Generation

0

10

20

30

40

50

60

70

2005 2007 2008 2009

LAGOS

KANO

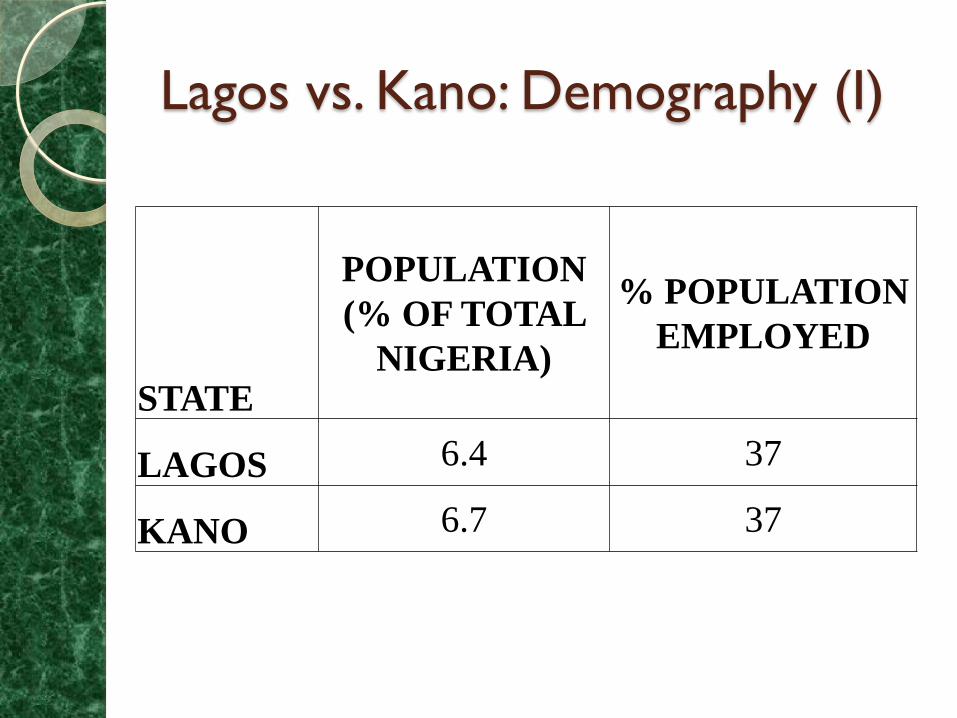

Lagos vs. Kano: Demography (I)

STATE

POPULATION

(% OF TOTAL

NIGERIA)

% POPULATION

EMPLOYED

LAGOS 6.4 37

KANO 6.7 37

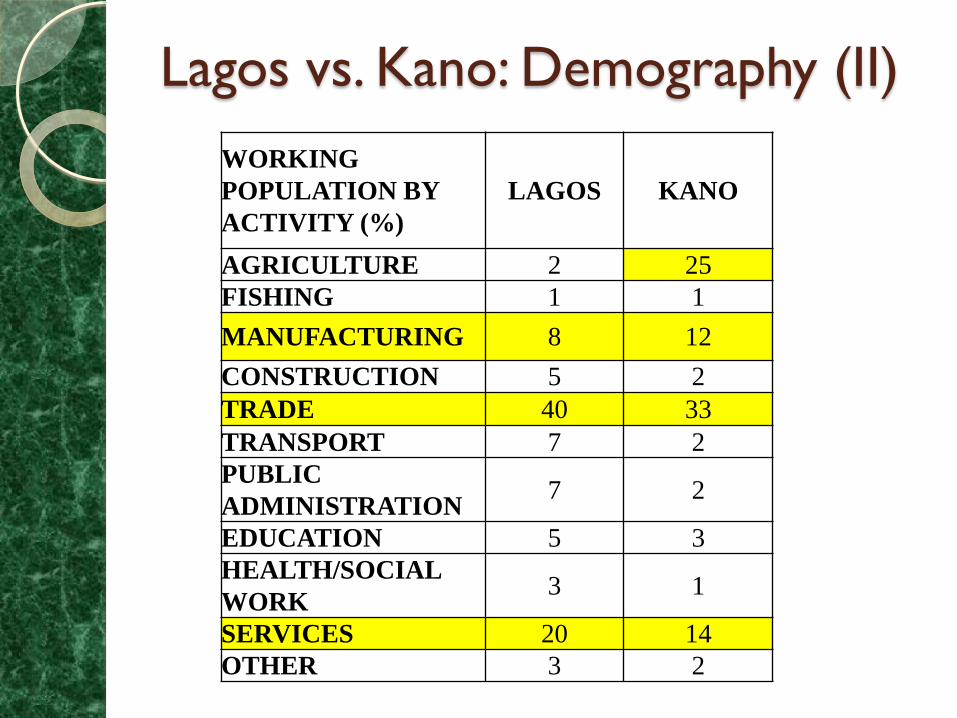

Lagos vs. Kano: Demography (II)

WORKING

POPULATION BY

ACTIVITY (%)

LAGOS KANO

AGRICULTURE 2 25

FISHING 1 1

MANUFACTURING 8 12

CONSTRUCTION 5 2

TRADE 40 33

TRANSPORT 7 2

PUBLIC

ADMINISTRATION 7 2

EDUCATION 5 3

HEALTH/SOCIAL

WORK 3 1

SERVICES 20 14

OTHER 3 2

Culture of Cooperation in Lagos (I)

“For sustainable and meaningful

development, taxation is necessary. Nigeria

cannot only have an oil economy…It’s not

sustainable for economic

development…Taxes are the only viable

means…”

--Director, Lagos Internal Revenue Service

Culture of Cooperation in Lagos (II)

“Recently, there’s even more realization

that states can’t survive without internally

generated revenue. Politicians have put

pressure on the civil service to improve the

tax administration. They have also been

encouraging citizens to make their

payments.”

--Director, Lagos Internal Revenue Service

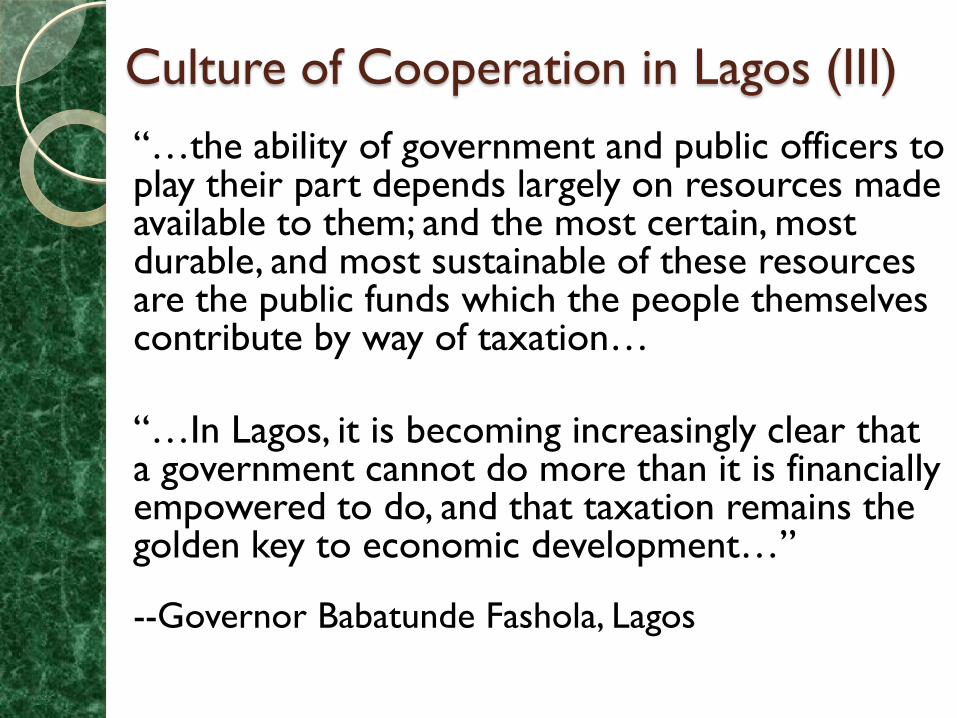

Culture of Cooperation in Lagos (III)

“…the ability of government and public officers to play their part depends largely on resources made available to them; and the most certain, most durable, and most sustainable of these resources are the public funds which the people themselves contribute by way of taxation…

“…In Lagos, it is becoming increasingly clear that a government cannot do more than it is financially empowered to do, and that taxation remains the golden key to economic development…”

--Governor Babatunde Fashola, Lagos

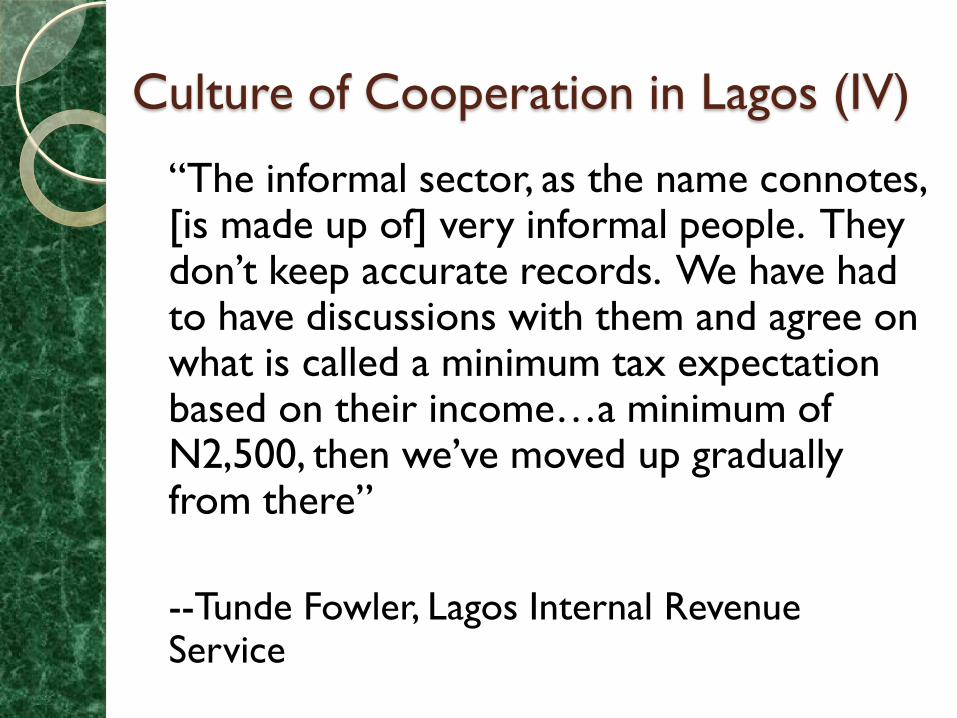

Culture of Cooperation in Lagos (IV)

“The informal sector, as the name connotes, [is made up of] very informal people. They don’t keep accurate records. We have had to have discussions with them and agree on what is called a minimum tax expectation based on their income…a minimum of N2,500, then we’ve moved up gradually from there”

--Tunde Fowler, Lagos Internal Revenue Service

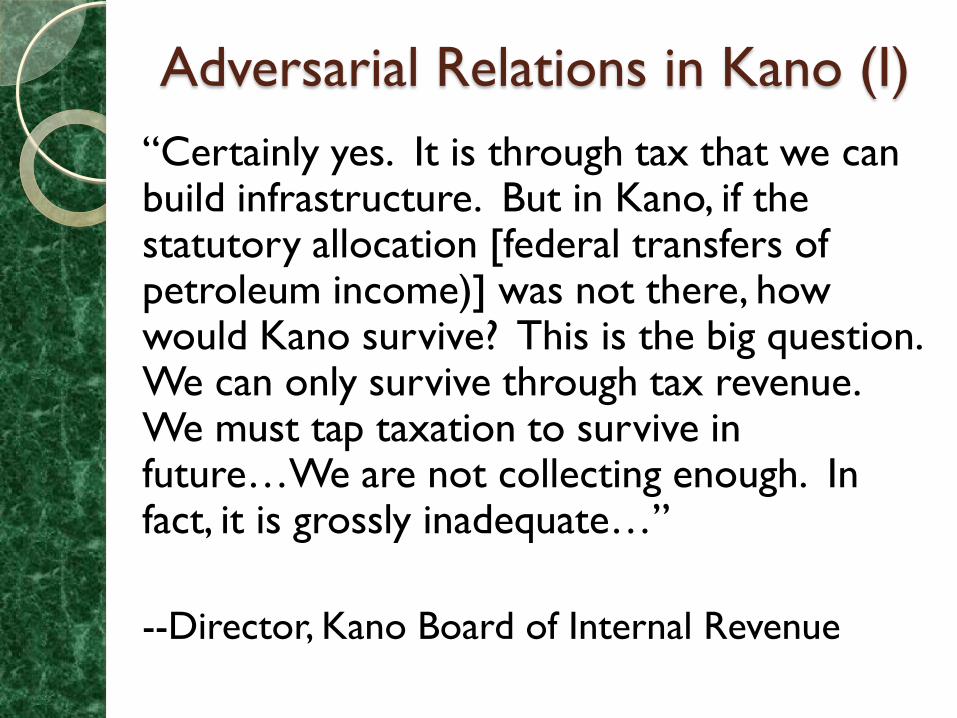

Adversarial Relations in Kano (I)

“Certainly yes. It is through tax that we can build infrastructure. But in Kano, if the statutory allocation [federal transfers of petroleum income)] was not there, how would Kano survive? This is the big question. We can only survive through tax revenue. We must tap taxation to survive in future…We are not collecting enough. In fact, it is grossly inadequate…”

--Director, Kano Board of Internal Revenue

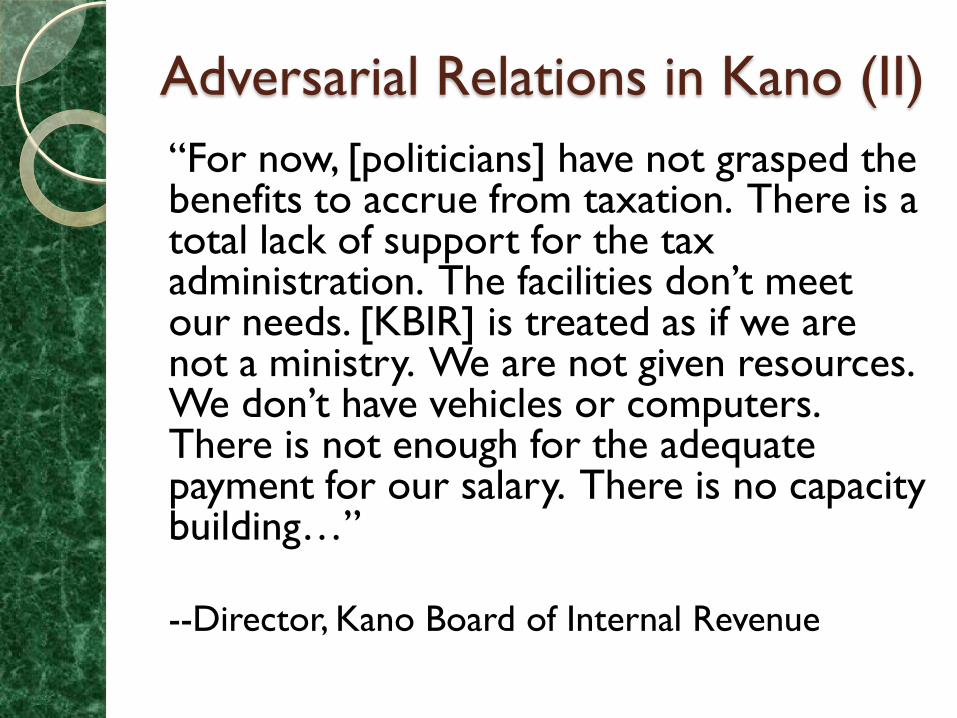

Adversarial Relations in Kano (II)

“For now, [politicians] have not grasped the benefits to accrue from taxation. There is a total lack of support for the tax administration. The facilities don’t meet our needs. [KBIR] is treated as if we are not a ministry. We are not given resources. We don’t have vehicles or computers. There is not enough for the adequate payment for our salary. There is no capacity building…” --Director, Kano Board of Internal Revenue

Adversarial Relations in Kano (III)

“It is irresponsible to ask for more revenue

based on what is given to oil bearing states.

Rather than ask for more funds from the

federal government, Kano should explore

ways of making more money for itself.

Leaders should concentrate on diversifying

of our revenue base and use sustainable

alternatives like taxes.”

--Director, Kano Board of Internal Revenue

Adversarial Relations in Kano (IV)

“…As regards physical infrastructure, the

Kano State BIR offices are housed in rented

premises making it very difficult for long

term planning. The buildings, furniture and

general office equipment are largely in a

dilapidated state and are unsuitable for

modern ways of working…”

--2009 KBIR Modernization Plan, World Bank

Summary

Differences in political leadership help

explain why Lagos and Kano have two

different tax cultures.

◦ This ultimately results in two different

rates of tax generation.

In Lagos: Cooperation and compliance.

In Kano: Indifference and a lack of

engagement.

Conclusion

Non-Tax Income Decreased Public

Service Spending

Tax Income Increased Public Service

Spending

Political leadership and relationships to tax

agencies influence state tax generation.

◦ Cooperative Stronger Tax Generation

(LAGOS)

◦ Adversarial Weaker Tax Generation (KANO)

Thank You!

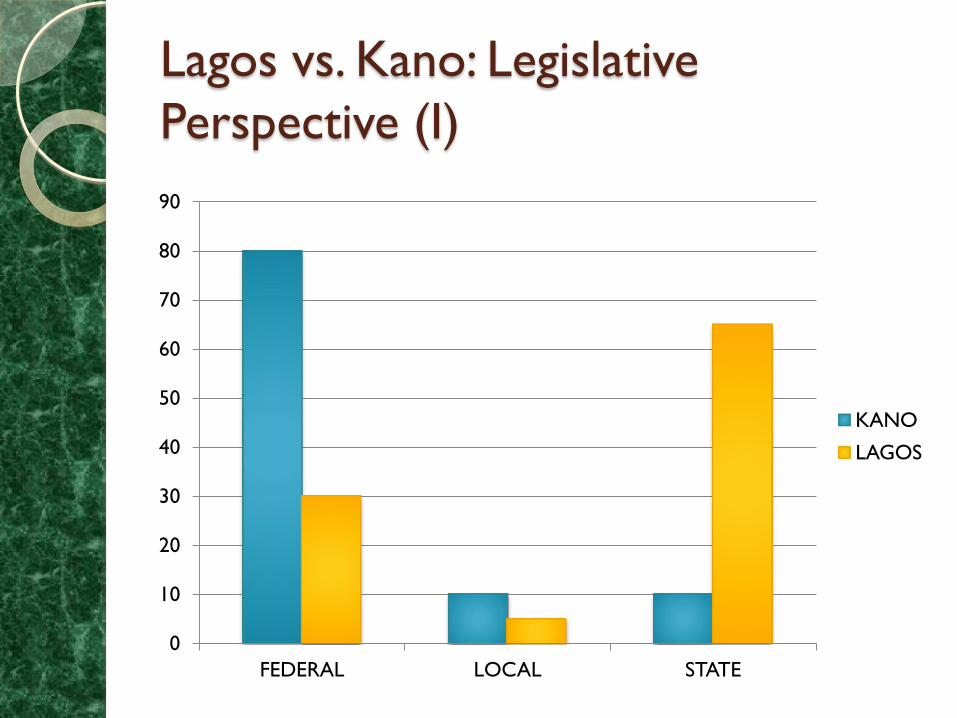

Lagos vs. Kano: Legislative

Perspective (I)

0

10

20

30

40

50

60

70

80

90

FEDERAL LOCAL STATE

KANO

LAGOS

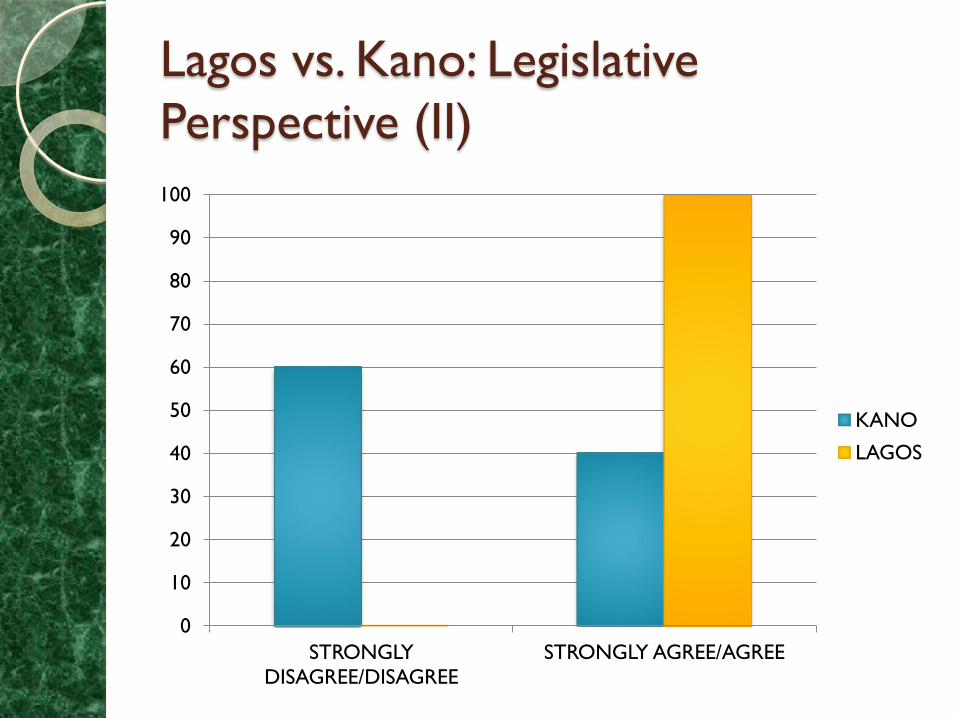

Lagos vs. Kano: Legislative

Perspective (II)

0

10

20

30

40

50

60

70

80

90

100

STRONGLY

DISAGREE/DISAGREE

STRONGLY AGREE/AGREE

KANO

LAGOS