taxes & investing - cboe · this edition of taxes & investing: a guide for the individual...

TRANSCRIPT

1

Table Of Contents

Introduction 3

Dividends 3

Capital Gains and Losses 6

Short Sales and Constructive Sales 7

Wash-Sale Rule 12

One-Sided Equity Option Positions 14Long Stock and Long CallsShort CallsLong PutsShort Puts

Offsetting Positions 16Exceptions to Offsetting Position RulesIdentified Straddles

Non-Equity and Stock Index Instruments 26

Single Stock and Narrow Based Stock

Index Futures 28

Exchange Traded Fund Shares 29

Mixed Straddles 30

Bonds and Other Debt Instruments 31Original Issue DiscountMarket DiscountShort-Term ObligationsAmortizable Bond PremiumConvertibles and Exchangeables

Conversion Transactions 37

Investment Income and 39Other Investment Expenses

Appendix I 40In-the-Money Qualified Covered Calls for Stock Priced $25 or Less

Appendix II 41Effects of Various Strategies

For More Non-Tax-Related Information 50

For More Tax-Related Information 51

February 2005

A Guide for the Individual Investor

TAXES & INVESTING

The lower rate applies to sales andexchanges on or after May 6, 2003, butnot with respect to years beginning afterDecember 31, 2010.

On page 26, please add this additionalsubheading before the "Non-Equityand Stock Index Instruments" section:

Physical Settlement RuleThe physical settlement of a straddleposition (e.g., an options contract) estab-lished after October 21, 2004, that if ter-minated would result in a realization of aloss, is treated as a two-step transactionfor purposes of applying the anti-strad-dle rules (page 17). First, the position istreated as having been terminated for itsfair market value immediately before thesettlement. Then, the property (e.g.,stock) used to physically settle the posi-tion is treated as having been sold at fairmarket value.

On page 40, please replace the secondand third sentences with:- In 2006, that number is $150,500

($75,250 for married taxpayers filing separately).

- In 2007, that number is $156,400 ($78,200 for married taxpayers filing separately).

AddendumFebruary 2007

On page 2, please add at the end of thefirst full paragraph, as part of the paragraph, the following additional disclaimer:Any U.S. tax advice contained in thisbooklet is not intended or written to beused, and cannot be used, for the purpose of (i) avoiding penalties thatmay be imposed under the InternalRevenue Code or applicable state orlocal tax law provisions, or (ii) providing, marketing or recommendingto another party any transaction or matter addressed herein.

On page 3, please substitute the following sentence for the second paragraph under the heading"Introduction:"This edition of Taxes & Investing: AGuide for the Individual Investor reflectschanges in the federal income tax lawthrough January 31, 2007.

On page 3, please substitute the following sentence for the last sentencein the first paragraph under the head-ing "Dividends:"

Prior law will apply to years beginningafter December 31, 2010.

On page 6, please substitute the following sentence for the second sentence in the second paragraphunder the heading "Capital Gains andLosses:"

Introduction

This booklet summarizes the basic rules governingthe federal income taxation of certain investmentsby individuals who are citizens or residents of theUnited States and who dispose of an investment ina taxable transaction. It is not a treatise on the tax-ation of securities. Examples have been providedwhenever appropriate. Generally, the effect ofcommissions has not been taken into account.Corporations, tax-exempt entities and other similarprofessional investors may be subject to somewhatdifferent rules than those described herein and arenot the subject of this booklet.

This edition of Taxes & Investing: A Guide forthe Individual Investor reflects changes in the feder-al income tax law through and including theAmerican Jobs Creation Act of 2004 (the "2004Act").

Dividends

Dividends received after 2002 by an individualshareholder from domestic corporations and "quali-fied foreign corporations" are generally taxed at thesame rates that apply to net capital gain for purpos-es of both the regular tax and the alternative mini-mum tax. See discussion on page 6. Thus, divi-dends are taxed at a top rate of 15%. Prior law willapply for years beginning after December 31, 2008.

Dividends paid by a foreign corporation withrespect to stock that is "readily tradable on an estab-lished securities market in the United States" aregenerally eligible for the lower rates. Under guidanceissued by the Internal Revenue Service, common orordinary stock, or preferred stock, or an American

3

Prepared at the request of The Options IndustryCouncil by

The opinions and conclusions expressed herein arethose of Ernst & Young LLP.

The information in this booklet provides onlya general discussion of the tax law affecting invest-ments and is not intended to be applicable to anyindividual investment and tax situation. Special taxrules may apply to certain financial instruments andtransactions not specifically covered herein. Further,material contained in this booklet may be affected bychanges in law subsequent to publication. Investorsare strongly advised to contact their own tax consul-tants and legal advisors in considering the tax conse-quences of their own specific circumstances.

This publication discusses many types of secu-rities, futures contracts and options, includingexchange-traded options issued by The OptionsClearing Corporation. No statement in this publi-cation is to be construed as a recommendation topurchase or sell a security, or to provide investmentadvice. Options involve risks and are not suitable forall investors. Prior to buying or selling an option, aperson must receive a copy of Characteristics andRisks of Standardized Options. Copies of this docu-ment may be obtained from your broker, from any ofthe exchanges on which options are traded, or fromThe Options Clearing Corporation, One NorthWacker Dr., Suite 500, Chicago, IL 60606. See page50 for exchange addresses.

February 2005Copyright 2005, The Options Clearing Corporation.All Rights Reserved.

2

investor buys an ABC/October/55 put. The closingprice of ABC Co. stock on July 21, 2004 is $56. OnAugust 13, 2004, the investor sells the put. OnAugust 19, 2004, ABC Co. stock goes ex-dividendwith respect to a distribution to shareholders ofrecord on August 23, 2004. On October 15, theinvestor sells the ABC Co. stock. The investor isentitled to the lower tax rate on the dividend paidbecause the ABC Co. stock is held for more than 60good holding period days during the 121-day periodbeginning 60 days before August 19, the ex-divi-dend date. Days on which the investor held theABC/October/55 put are not taken into account.

EExxaammppllee::

On September 9, 2005, an investor buys 100shares of XYZ Co. stock for $38. On October 13,2005, the investor writes an XYZ/December/40call. The closing price of XYZ Co. stock onOctober 12, 2005 is $41. The option is an in-the-money qualified covered call. On November 14,2005, the investor unwinds his/her position in theXYZ/December/40 call by making a closing pur-chase. On November 16, 2005, the XYZ Co. stockgoes ex-dividend with respect to a distribution toshareholders of record on November 18, 2005. Theinvestor sells the XYZ Co. stock on December 2,2005. The investor is not entitled to the lower taxrate on the dividend paid because the XYZ Co.stock is not held for more than 60 days of goodholding period during the 121-day period begin-ning 60 days before November 16, 2005, the ex-div-idend date. Days on which the investor is the writerof the XYZ/December/40 call are not taken intoaccount.

The lower tax rates are not available for divi-dends received to the extent that the taxpayer is oblig-ated to make related payments with respect to positionsin substantially similar or related property (e.g., "pay-ments in lieu of dividends" under a short sale).Similarly, owners whose shares are lent in connectionwith short sales are not entitled to the lower rates on

5

depositary receipt in respect of such stock, is consid-ered “readily tradable on an established securitiesmarket in the United States" if it is listed on anational securities exchange that is registered underSection 6 of the Securities Exchange Act of 1934, oron the Nasdaq Stock Market. Registered nationalexchanges include the American Stock Exchange,Boston Stock Exchange, Chicago Stock Exchange,Cincinnati Stock Exchange, New York StockExchange, Philadelphia Stock Exchange and thePacific Stock Exchange, Inc.

Treasury and the IRS are considering for futureyears the treatment of dividends with respect to stocklisted only in a manner that does not meet the defini-tion of "readily tradable on an established securitiesmarket in the United States," such as on the OTCBulletin Board or on the electronic "pink sheets."

To be eligible for the lower tax rate, the share-holder must hold a share of stock for more than 60days during the 121-day period beginning 60 daysbefore the ex-dividend date for a particular dividendpayment (more than 90 days during the 181-dayperiod beginning 90 days before the ex-dividenddate in the case of certain preferred stock). Theholding period must be satisfied for each dividendpayment. Days on which the stock position ishedged, other than with "qualified covered calls"(described on pages 19-25), are generally not con-sidered "good" holding period days. However,effective for positions established on or afterOctober 22, 2004, days on which a stock position ishedged with in-the-money qualified covered callsare not considered good holding period days(regardless of when the hedged position is estab-lished). The requisite days of good holding periodneed not be consecutive days. In determining hold-ing period, the day on which stock is disposed istaken into account, but not the day on which it isacquired.

EExxaammppllee::

On July 7, 2004, an investor buys 100 sharesof ABC Co. stock for $53. On July 22, 2004, the

4

However, the tax law conforms the capital gains taxrate a taxpayer would pay under the regular tax withthe rate for AMT purposes through an AMT capi-tal gains tax rate. This rate equals the capital gainstax rate under the regular tax, depending on thetype of asset and the length of holding period.Accordingly, capital gains alone should not affectwhether a taxpayer becomes subject to the AMT.

Losses are subject to certain limitations.Capital losses (long-term as well as short-term) areallowed in full to the extent of capital gains plus$3,000 of ordinary income. Special netting rulesapply to take into account the multiple rates forlong-term capital gains.

The use of the installment method of report-ing for sales of publicly traded property is not per-mitted. Individuals are required to recognize gainor loss on the sale of publicly traded stock and secu-rities on the day the trade is executed.

Short Sales and Constructive SalesThe short-sale rules deal with the selling of proper-ty in a short sale where the taxpayer holds or subse-quently acquires "substantially identical property."Historically, the effect of the short-sale rules hasbeen that if the long position has been held for oneyear or less at the time of the short sale, or if sub-stantially identical property is acquired after theshort sale, gain on closing that short sale is a short-term capital gain (notwithstanding the period oftime any property used to close the short sale hasbeen held). In addition, the holding period of thelong position (to the extent of the quantity soldshort, in the order of the dates of acquisition) is ter-minated, not suspended. The holding period of thelong position begins only after the short sale has

7

amounts received in respect of the shares lent; the lowerrates do not apply to payments in lieu of dividends.

Dividends are not treated as "investmentincome" for purposes of determining the limitationon deductibility of investment interest expense (seepage 39) unless the investor elects to treat the divi-dends as not eligible for the lower tax rates.

Capital Gains and Losses

Short-term capital gains, as well as compensation,business profits and interest, are subject to a mar-ginal tax rate of up to 35%. Absent further legisla-tion, a marginal tax rate of up to 39.6% will againapply for tax years beginning after December 31,2010.

A "maximum" tax rate of 15% applies to netcapital gains (net long-term capital gains minus netshort-term capital losses) with a holding period ofmore than 12 months. The lower rate applies tosales and exchanges on or after May 6, 2003, butnot with respect to years beginning after December31, 2008. This 15% rate, as well as the marginal taxrates on "ordinary" and short-term capital gainincome noted above, may effectively be even higherdue to the impact of the limitation on itemizeddeductions and the phase-out of personal exemp-tions for certain taxpayers.

With an up to 20 percentage point spreadbetween the 15% long-term and 35% short-termcapital gain tax rates, individual investors with prof-itable positions may in some cases have an incentiveto hold such positions for an extended period oftime. In evaluating investment decisions, investorsmust take into account any effect of the individualalternative minimum tax ("AMT").

In general, the AMT is imposed on a gradu-ated two-tier basis, 26% and 28%, based on theamount of alternative minimum taxable income.

6

fied in Treasury regulations to be issued.Upon a constructive sale event, gain is recog-

nized as if the position were sold at its fair marketvalue on the date of sale and immediately repur-chased. The basis of the appreciated position isincreased by any gain realized, and a new holdingperiod begins as if the position had been acquiredon the date of the constructive sale.

The constructive sale rule does not apply tocertain closed transactions during a taxable year thatmeet three conditions: (1) the transaction is closedbefore the end of the 30th day after the close ofsuch taxable year; (2) the position is held through-out the 60-day period beginning on the date suchtransaction is closed; and (3) during such 60-dayperiod, the taxpayer does not enter into certaintransactions (except "qualified covered calls", dis-cussed on pages 19-25) that would diminish the riskof loss during that time on such position. Effectivefor positions established on or after October 22,2004, the qualified covered call exception is limitedto at-the-money and out-of-the-money qualifiedcovered calls.

A special constructive sale rule applies whereanother risk reducing transaction is entered intowithin that 60-day period and that other transactionis closed before the 30th day after the close of theyear of the initial transaction. The InternalRevenue Service has taken the position that succes-sive short sales of stock are not subject to the con-structive sale rule if all of the short sales are closedbefore the 30th day after the close of the taxableyear of the initial short sale and the appreciatedposition is unhedged thereafter for 60 days.

A transaction that results in a constructivesale of one appreciated position is not treated asresulting in the constructive sale of another appreci-ated position so long as the taxpayer holds the posi-tion which was treated as constructively sold.However, when that position is sold or otherwisedisposed, the transaction can cause a constructivesale of another appreciated position.

9

been closed, or the substantially identical property issold or otherwise disposed, whichever occurs first.

Also, if the long position has already beenheld more than 12 months at the time of the shortsale, no termination of holding period occurs andany loss on closing the short sale is a long-term cap-ital loss. A taxpayer can deliver against the shortposition, for long-term capital gain, stock held morethan 12 months at the time of the short sale, pro-vided that no other substantially identical propertywas held short-term at the time of, or acquired after,the short sale.

Reducing the risk of loss by being under acontractual obligation to sell or holding an option tosell (a "put") has been treated as a short sale for pur-poses of the short-sale rules, but a "married put" hasbeen exempted from these short-sale rules. See dis-cussion of the "Married Put" on page 19.

The "substantially identical" test requires thatthe securities be of the same issuer and be commer-cially identical in all major respects, including inter-est rate, maturity date, dividend provisions, liquidat-ing preferences and other similar priorities. If theinstruments are virtually similar or identical, theoverriding test is whether or not the marketplaceviews them as such, i.e., whether or not movementof one security correlates to the price movement ofthe other security. Thus, if a graph of relative pricemovements produces parallel lines, the securities aregenerally substantially identical. If such a resultdoes not occur, they are not substantially identical.

As a result of the "constructive sale" rule andsubject to various exceptions, a taxpayer must recog-nize gain (but not loss) upon entering into a con-structive sale of any appreciated position in stock, apartnership interest or certain debt instruments thateffectively eliminates both the taxpayer’s risk of lossand upside gain potential. Entering into short sales,futures or forward contracts are examples of transac-tions that may generate constructive sales. Where ashort position has appreciated, the acquisition ofstock may result in a constructive sale. Other trans-actions to be covered by these rules may be identi-

8

EExxaammppllee::

Using the prior example, the investor acquires 100shares of X Co. "in the market" on January 6, 2004for $65 per share and delivers those shares to coverthe short position. The investor holds the shares ofX Co. acquired in June "naked" for 60 days after thecovering of the short position. There is no con-structive sale of X Co. stock in 2003. However, theinvestor realizes a $5 per share loss on covering theshort position in 2004. For stock positions estab-lished on or after October 22, 2004, see page 18.

EExxaammppllee::

On May 4, 2004, an investor buys 100 shares of YCo. for $25 per share. On July 12, 2004, theinvestor sells 100 shares of Y Co. short for $20 pershare. There is no constructive sale on July 12because the investor’s Y Co. shares were notappreciated at the time of the short sale. For stockpositions established on or after October 22, 2004,see page 18.

EExxaammppllee::

On February 3, 2004, an investor buys 200 shares ofZ Corp. stock at $30 per share. On April 22, 2005,the investor buys at-the-money puts (exercise priceequals current market price of the underlying stock)on the 200 shares when the stock is $40 per share.The acquisition of the at-the-money put does nottrigger the constructive sale rules because the optionreduces only the investor’s risk of loss. However,the anti-straddle rules may apply. See page 16.

According to the Internal Revenue Service, ifa taxpayer enters into a short sale and subsequentlydirects a broker to purchase shares of the stock soldshort and close the short sale in the following year,and if at the time of the purchase the value of theshort position has appreciated (the stock has gonedown in value), then there is a "constructive sale" ofthe short position in the current year on the pur-chase of the stock. However, if at the time of thepurchase, the value of the short position has depre-

11

If less than all of a position is constructivelysold, the taxpayer may specifically identify what hasbeen "sold". Absent that identification, the positionis deemed to be sold in the order acquired (i.e., on a"first in, first out" basis).

The constructive sale provision is generallyeffective for constructive sales entered into afterJune 8, 1997. Special rules apply to transactionsbefore that date that would otherwise have beenconstructive sales under this new provision.

Options are not specifically covered, but thelegislative history is very clear that many transac-tions involving options, including the buying orwriting of certain in-the-money options, will besubject to the constructive sale rule through theissuance of Treasury regulations. In determiningwhether a particular transaction will be treated as aconstructive sale, the Treasury regulations may takeinto account the yield and volatility of the underly-ing stock, the length of time until maturity andother terms of the option. The regulations may alsorely on option prices and option pricing models.However, transactions involving stock and also out-of-the-money options, at-the-money options orqualified covered calls should not trigger the con-structive sale rule.

Transactions discussed in this bookletinvolving options do not reflect the potentialapplication of the constructive sale rule inadvance of regulatory guidance.

EExxaammppllee::

On June 3, 2003, an investor buys 100 shares of X Co. for $50 per share. On August 18, 2003,the investor sells short 100 shares of X Co. for $60per share. On January 6, 2004, the investor closesthe short position by delivering the 100 sharesowned. Entering the short sale on August 18 is aconstructive sale, resulting in a $1,000 gain in 2003.Since the 100 shares bought on June 3 are treated assold and repurchased for $60 upon entering theshort sale, no further gain or loss is realized on clos-ing the short position.

10

tical property" is generally the same as in the case ofthe short-sale rules.

When the wash-sale rule is applicable, theloss is disallowed and the basis of the new propertyis deemed to be the basis of the original property,increased or decreased, as the case may be, by thedifference between the cost of the new property andthe price at which the old property was sold. Theholding period of the original property is added tothe holding period of the newly-acquired property.

In addition, the Internal Revenue Service hastaken the position that the wash-sale rule will disal-low a loss on the sale of stock if, within 30 daysbefore or after the sale of the stock, the taxpayersells an "in-the-money" put option with respect tothe stock and, on the basis of objective factors at thetime the put was sold, there is a substantial likeli-hood that the put will be exercised. These factorsinclude the spread at the time the put is soldbetween the value of the underlying stock and theexercise price of the put, the premium paid and thehistoric volatility in the value of the stock.

EExxaammppllee::

On January 6, 2004, an investor sells short 100 sharesof ABC Co. for $50 per share. On April 5, 2004, theinvestor purchases 100 shares of ABC Co. at $55 pershare and delivers the stock to close the short posi-tion, resulting in a $500 loss. The constructive salerule does not apply because there is no appreciatedposition. On April 28, 2004, the investor sells short100 shares of ABC Co. for $50 per share. The $500loss on the closing of the first short sale is disallowedbecause the investor, within 30 days after closing theshort sale at a loss, entered into another short sale ofsubstantially identical stock. That loss will reduceany gain in the case of a subsequent constructive sale,or will increase any loss on the closing of the secondshort sale if there is no constructive sale.

EExxaammppllee::

On January 6, 2004, an investor sells short 100shares of DEF Co. for $30 per share. On February

13

ciated (the stock has gone up in value), loss is real-ized when the short sale is closed by delivering thestock.

EExxaammppllee::

On January 7, 2004 an investor directs a broker toborrow 100 shares of ABC Co. stock and to sell itshort. The investor does not own any ABC Co.stock. On December 30, 2004, when the stock'svalue has decreased and the value of the investor'sshort position has increased, the investor directs thebroker to purchase 100 shares of stock to close theshort sale, and those shares are delivered to thelender of the stock on January 3, 2005. Under theconstructive sale rule, since the short position hasappreciated at the time of the purchase of the stock,the investor realizes the gain on December 30.Conversely, if at the time of the stock purchase, thevalue of the investor's short position has decreased(the stock price has increased since January 7,2004), the short sale is not complete until the stockis delivered to close the short sale on January 3,2005.

Wash-Sale Rule

The wash-sale rule prevents taxpayers who are notdealers from selling stock or securities (includingoptions) at a loss and reacquiring "substantiallyidentical" stock or securities (or options to acquiresubstantially identical stock or securities) within a30-day period before or after the loss. The wash-sale rule also prevents such taxpayers from currentlyrecognizing losses on the closing of short sales if,within 30 days before or after the closing, substan-tially identical stock or securities are sold or the tax-payer enters into another short sale of substantiallyidentical stock or securities.

The meaning of the term "substantially iden-

12

Short CallsPremium received for writing a call is not includedin income at the time of receipt, but is held in sus-pense until the writer’s obligation to deliver theunderlying stock expires or until the writer eithersells the underlying stock as a result of the assign-ment of the call or closes the option (other than byexpiration or assignment). If the writer’s obligationexpires, the premium is short-term capital gain tothe writer upon expiration, regardless of the lengthof time the call is outstanding.

Similarly, gain or loss on the termination ofthe writer’s obligation through closing the optionother than by expiration or assignment is short-term capital gain or loss, regardless of the length oftime the call is outstanding. However, if a call isassigned, the strike price plus the premium receivedbecomes the sale price of the stock in determininggain or loss. The resulting gain or loss dependsupon the holding period and the basis of the under-lying property used to make the delivery to satisfythe assignment. It is possible that previously ownedstock will be long-term and, thus, without takinginto account the offsetting position rules discussedon page 16, may result in long-term capital gain orloss.

Long PutsIf a put option is acquired and sold prior to exercise,any gain or loss is short-term or long-term capitalgain or loss, depending on the holding period of theput. The expiration of a long put results either in ashort-term capital loss if the put is held one year orless or in a long-term capital loss if held for morethan one year. If the put is exercised, the cost of theput and the commission on the sale of the stockreduce the amount realized upon the sale of theunderlying stock delivered to satisfy the exercise.

Short PutsLike the call premium, the put premium is held insuspense until the put writer’s obligation is termi-nated. Closing an uncovered put before assignment

15

14, 2004, the investor purchases 300 shares of DEFCo. at $35 per share and delivers 100 of the sharesto close the short sale. The constructive sale ruledoes not apply because there is no appreciated posi-tion. On February 25, 2004, the investor sells 100of the shares of DEF Co. The $500 loss on theclosing of the short sale is disallowed because theinvestor, within 30 days after closing the short saleat a loss, sold substantially identical stock. This losswill reduce any gain (increase any loss) on the sale ofthe remaining DEF Co. stock.

One-Sided Equity Option PositionsThe treatment of gain or loss as long-term or short-term may have great significance for equity optionsbecause of the potentially substantial long-termcapital gain rate differential.

Long Stock and Long CallsIf stock or a call option is acquired and held formore than one year, the resulting gain or loss on thesale is a long-term capital gain or loss (see page 6).If the stock or call is purchased and sold in one yearor less, any resulting gain or loss is short-term.Expiration of a call is treated as a sale or exchangeon the expiration date and results in a short-termor long-term capital loss, depending on the holdingperiod of the call. If the call is exercised, the pre-mium paid, the strike price, the brokerage commis-sion paid upon exercise, and the commission on thecall’s purchase are included in the basis of thestock. The holding period of the stock acquiredbegins on the day after the call is exercised anddoes not include the holding period of the call.

14

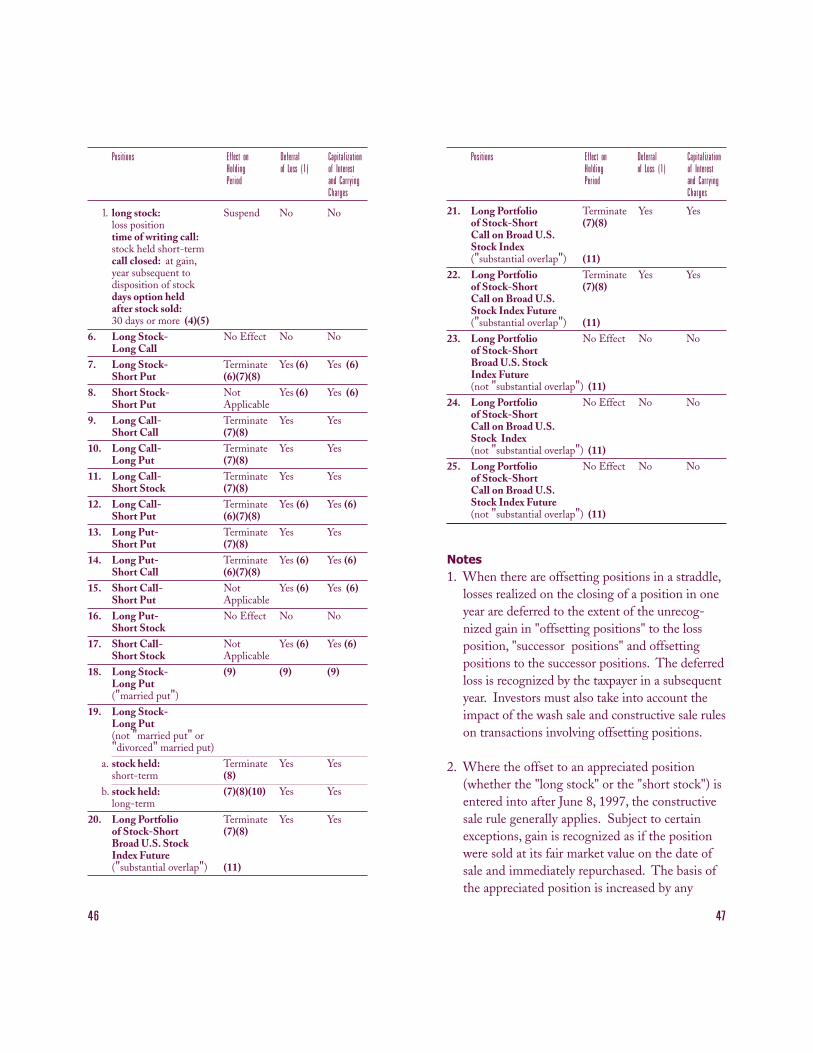

1. There is a suspension or termination of the hold-ing period during the period of offset (seeAppendix II).

2. The wash-sale rule applies to defer losses real-ized on certain straddle positions (see page 12).

3. No current deduction for losses is allowable tothe extent of the unrecognized gain (if any) atthe end of the taxable year in "offsetting posi-tions" to the loss position, "successor positions"and "offsetting positions to the successor posi-tions." Deferred losses are treated as sustained inthe next taxable year, but they are again deferredto the extent of any offsetting unrecognized gainat the end of such year and not otherwise deferredunder the wash-sale rule. However, see discus-sion of "Identified Straddles" on page 25.

In general, a "successor position" is a positionwhich is on the same side of the market (long orshort) as was the original position, whichreplaces a loss position and which is entered intoduring a period commencing 30 days prior toand ending 30 days after the disposition of theloss position. However, a position entered intoafter all positions of a straddle have been dis-posed will not be considered a successor position.

4. All carrying charges and interest expenses(including margin) incurred during the period of offset are required to be capitalized and addedto the basis of the long position. Such capital-ized charges are, however, reduced by dividendsreceived on stock included in the straddle. Suchexpenses are not deductible but, instead, decreasethe potential capital gain or increase the poten-tial capital loss upon disposition.

Stock acquired prior to January 1, 1984should not be subject to these anti-straddle rules,irrespective of how long the stock may be held bythe taxpayer or the nature of any other position

17

always results in short-term capital gain or loss. Ifthe put expires, the writer realizes a short-term cap-ital gain to the extent of the premium received. Ifthe put is assigned, the strike price plus commissionless the premium received for writing the putbecome the basis of the stock acquired, and a newholding period begins for the stock on the day afterthe stock’s purchase.

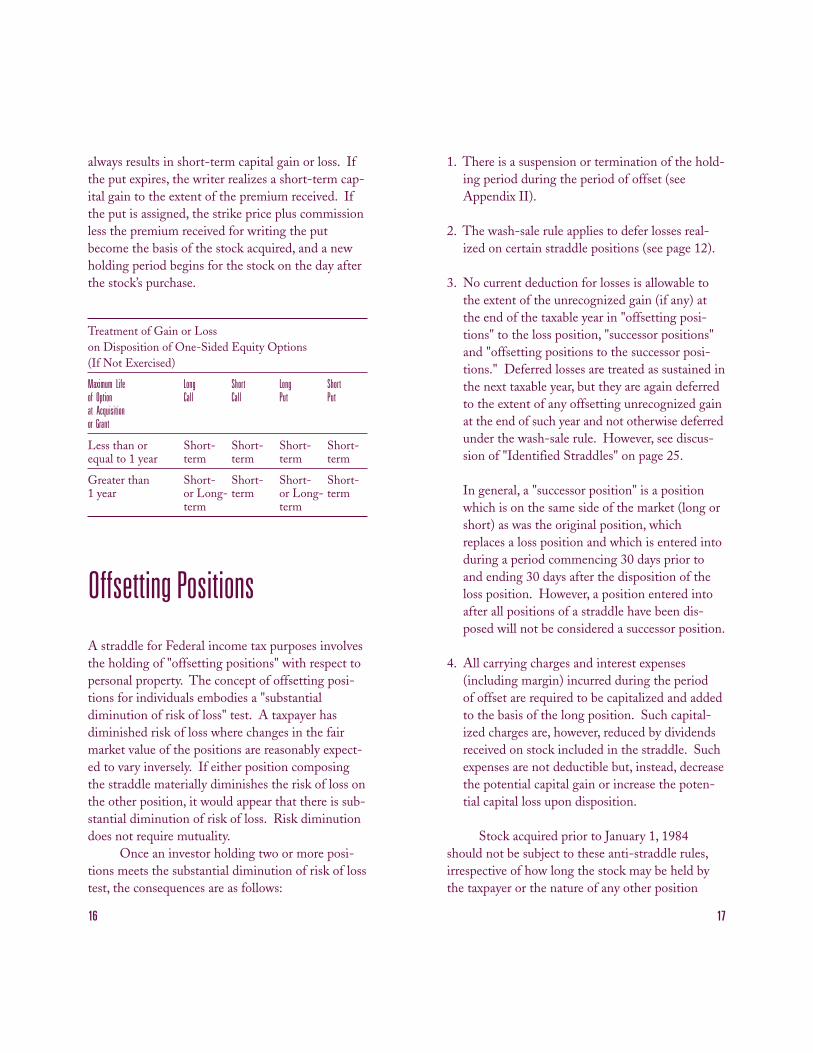

Treatment of Gain or Losson Disposition of One-Sided Equity Options(If Not Exercised)

Maximum Life Long Short Long Shortof Option Call Call Put Putat Acquisitionor Grant

Less than or Short- Short- Short- Short-equal to 1 year term term term term

Greater than Short- Short- Short- Short-1 year or Long- term or Long- term

term term

Offsetting Positions

A straddle for Federal income tax purposes involvesthe holding of "offsetting positions" with respect topersonal property. The concept of offsetting posi-tions for individuals embodies a "substantialdiminution of risk of loss" test. A taxpayer hasdiminished risk of loss where changes in the fairmarket value of the positions are reasonably expect-ed to vary inversely. If either position composingthe straddle materially diminishes the risk of loss onthe other position, it would appear that there is sub-stantial diminution of risk of loss. Risk diminutiondoes not require mutuality.

Once an investor holding two or more posi-tions meets the substantial diminution of risk of losstest, the consequences are as follows:

16

rules requires that stock and options on stock be ofthe same issuer.

Exceptions to Offsetting Position RulesIn general, any offsetting position that includesstock and provides a substantial diminution of riskof loss is subject to the anti-straddle provisions.Exceptions include the "qualified covered call" and,possibly, the "married put" discussed below.

Married PutIn order for a "married put" to be deemed"married," the put must be acquired on the sameday as the stock and the stock must be identified asthe stock to be delivered upon exercise of the put.Furthermore, the married put criteria may only bemet either by delivering the married stock or byallowing the put to expire. If the put expires, thecost of the put is added to the cost basis of thestock. While the married put is exempted from theshort-sale rules (see page 7), it remains unclearwhether or not the married put is also exempt fromthe offsetting position rules.

However, temporary Treasury regulations sug-gest that, in the view of the Treasury, the married putis not so exempt. Further clarification is required infinal Treasury regulations yet to be issued.

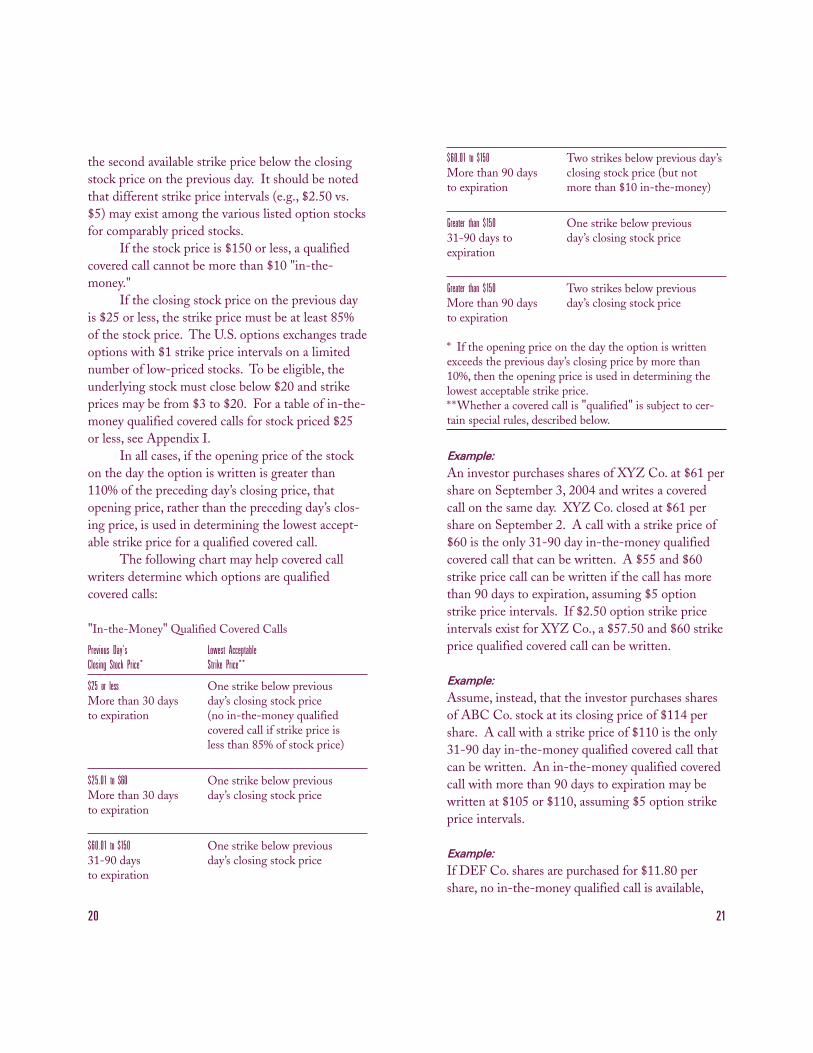

Qualified Covered CallsA "qualified covered call" is generally an exchange-traded call option written on stock held by theinvestor (or stock acquired by the investor "in con-nection with" the writing of the option) that resultsin capital gain or loss treatment to the writer. Thecall option must have more than 30 days to expira-tion and a strike price not less than the first avail-able strike price below the closing price of the stockon the day before the option was written.However, see discussion on page 24 regardingoptions entered into after July 28, 2002.

For an option written with more than 90 daysto expiration and with a strike price over $50, thecovered call must have a strike price no lower than

19

held. However, it is possible that the InternalRevenue Service could take a different position.

As a result of the 2004 Act, long stock versusshort stock may now be treated as an offsettingposition for purposes of the anti-straddle rules,effective for positions established on or afterOctober 22, 2004 (regardless of when the hedgedposition is established). Previously, stock could bepart of, but not all of, a straddle involving offsettingpositions.

EExxaammppllee::

An investor purchases 100 shares of XYZ Co.common stock at $30 per share on November 15,2004. On December 16, 2004, the investor sells100 shares of the stock short ("against-the-box") at$50 per share. On May 5, 2005, the investor pur-chases 100 shares of XYZ Co. stock at $50 pershare. On May 16, 2005, the November 15 stock isdelivered to close the short sale. The application ofthe constructive sale rule results in a $20 per shareshort-term capital gain on entering into the shortsale on December 16.

EExxaammppllee::

On May 3, 2004, an investor purchases 100shares of X Co. for $35 per share. On December15, 2004, the investor sells 100 shares of X Co.short for $30 per share. There is no constructivesale on December 15 because the investor's X Co.shares were not appreciated at the time of the shortsale. However, the anti-straddle rules may applybecause the short position was established afterOctober 22, 2004.

The substantial diminution of risk of loss testdoes not require that offsetting positions be of thesame issuer. As a result, stock of one issuer andoptions on the stock of another may be viewed asoffsetting positions in appropriate circumstances.

In contrast, the concept of "substantially iden-tical" for purposes of the wash-sale and short-sale

18

$60.01 to $150 Two strikes below previous day’sMore than 90 days closing stock price (but not to expiration more than $10 in-the-money)

Greater than $150 One strike below previous31-90 days to day’s closing stock priceexpiration

Greater than $150 Two strikes below previousMore than 90 days day’s closing stock priceto expiration

* If the opening price on the day the option is writtenexceeds the previous day’s closing price by more than10%, then the opening price is used in determining thelowest acceptable strike price.* *Whether a covered call is "qualified" is subject to cer-tain special rules, described below.

EExxaammppllee::

An investor purchases shares of XYZ Co. at $61 pershare on September 3, 2004 and writes a coveredcall on the same day. XYZ Co. closed at $61 pershare on September 2. A call with a strike price of$60 is the only 31-90 day in-the-money qualifiedcovered call that can be written. A $55 and $60strike price call can be written if the call has morethan 90 days to expiration, assuming $5 optionstrike price intervals. If $2.50 option strike priceintervals exist for XYZ Co., a $57.50 and $60 strikeprice qualified covered call can be written.

EExxaammppllee::

Assume, instead, that the investor purchases sharesof ABC Co. stock at its closing price of $114 pershare. A call with a strike price of $110 is the only31-90 day in-the-money qualified covered call thatcan be written. An in-the-money qualified coveredcall with more than 90 days to expiration may bewritten at $105 or $110, assuming $5 option strikeprice intervals.

EExxaammppllee::

If DEF Co. shares are purchased for $11.80 pershare, no in-the-money qualified call is available,

21

the second available strike price below the closingstock price on the previous day. It should be notedthat different strike price intervals (e.g., $2.50 vs.$5) may exist among the various listed option stocksfor comparably priced stocks.

If the stock price is $150 or less, a qualifiedcovered call cannot be more than $10 "in-the-money."

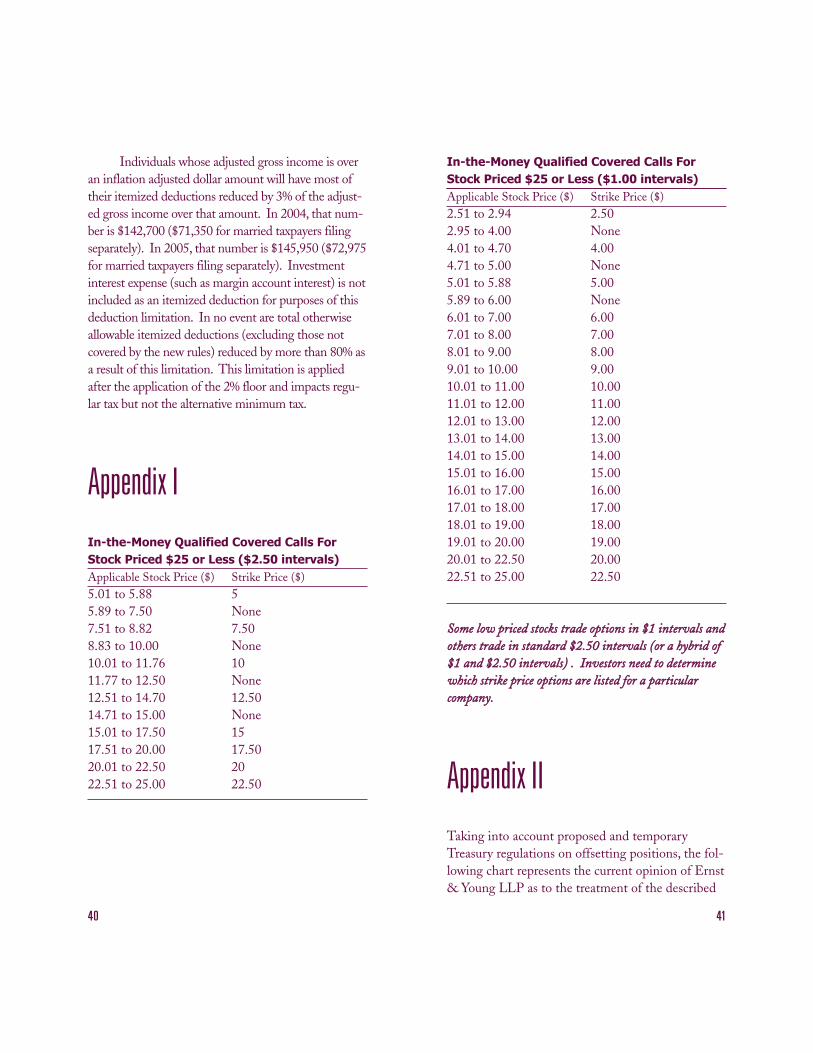

If the closing stock price on the previous dayis $25 or less, the strike price must be at least 85%of the stock price. The U.S. options exchanges tradeoptions with $1 strike price intervals on a limitednumber of low-priced stocks. To be eligible, theunderlying stock must close below $20 and strikeprices may be from $3 to $20. For a table of in-the-money qualified covered calls for stock priced $25or less, see Appendix I.

In all cases, if the opening price of the stockon the day the option is written is greater than110% of the preceding day’s closing price, thatopening price, rather than the preceding day’s clos-ing price, is used in determining the lowest accept-able strike price for a qualified covered call.

The following chart may help covered callwriters determine which options are qualified covered calls:

"In-the-Money" Qualified Covered Calls

Previous Day’s Lowest AcceptableClosing Stock Price* Strike Price**

$25 or less One strike below previousMore than 30 days day’s closing stock priceto expiration (no in-the-money qualified

covered call if strike price is less than 85% of stock price)

$25.01 to $60 One strike below previousMore than 30 days day’s closing stock priceto expiration

$60.01 to $150 One strike below previous 31-90 days day’s closing stock price to expiration

20

at a loss in one year and the stock is still owned onthe first day of the subsequent year, there is arequirement that the stock be held an additional 30days from the date of disposition of the call in orderfor the covered call to be treated as "qualified" forpurposes of the loss deferral rule (see page 17).Generally, only days on which the stock is held"naked" may be counted in determining whether the30-day holding period is satisfied. However, forthis rule the holding period continues to run whilethe taxpayer is the writer of qualified covered calls.Effective for positions established on or afterOctober 22, 2004, the holding period continues torun while the taxpayer is the writer of at-the-moneyor out-of-the-money (but not in-the-money) quali-fied covered calls.

Similarly, a covered call is not treated as"qualified" for purposes of the loss deferral rule ifthe covered call is not held for 30 days after therelated stock is disposed of at a loss, where gain onclosing the option is included in the subsequentyear. This rule applies to positions established afterDecember 31, 1986.

EExxaammppllee::

On December 1, an investor purchases 100 shares ofABC Co. stock at $36 per share. On the same day,the investor writes an ABC/February/35 call, receiv-ing a premium of $3. On December 15, the investorunwinds his/her position in the ABC/February/35call by making a closing purchase at $5. On May 1of the subsequent year, the investor sells the 100shares of ABC Co. stock at $45 per share. No posi-tions, long or short, in ABC Co. stock or options areestablished by the investor after the option closingpurchase on December 15 and prior to the sale ofthe stock on May 1. The covered call is qualified,because the ABC Co. stock is held for 30 days ormore after the close of the call at a loss in the yearpreceding the sale of the stock at a gain.

EExxaammppllee::

On November 6, 2004, an investor purchases 100

23

assuming $2.50 option strike intervals (see AppendixI), since the strike price must be at least 85% of thestock price (note that the $10 strike price options areless than 85% of $11.80). However, if $1 strike priceintervals exist, an $11 strike price qualified coveredcall can be written.

EExxaammppllee::

An investor purchases 100 shares of BCD Co. stockat $42 per share on June 28, 2004. On August 6,2004, the investor writes a BCD/September/40 call,receiving a premium of $3. BCD Co. closes at $42per share on August 5. On September 13, 2004, theinvestor unwinds his/her options position by mak-ing a closing purchase at $5. Since the call waswritten on stock held by the investor, it is a "quali-fied covered call."

Even if the stock price/strike rules aresatisfied, a call that is not an option to purchasestock acquired by the investor "in connection with"the granting of the option would not be qualified.For example, a call written on October 12, 2004 willnot be qualified if the stock is purchased onOctober 18, 2004.

Covered Calls - Special RulesThe basic thrust of the anti-straddle rules is toprevent mismatching of gain and loss. This isaccomplished by requiring loss deferral. Writing anat-the-money (strike price of call equals the stockprice used in determining the lowest acceptablestrike) or an out-of-the-money (above-the-market)qualified covered call allows the holding period ofthe underlying stock to continue. However, an in-the-money qualified covered call suspends the hold-ing period of the stock during the time of theoption’s existence. Further, any loss with respect toan in-the-money qualified covered call is treated aslong-term capital loss, if at the time the loss is real-ized, gain on the sale or exchange of the underlyingstock would be treated as long-term capital gain.

Additionally, when a covered call is disposed

22

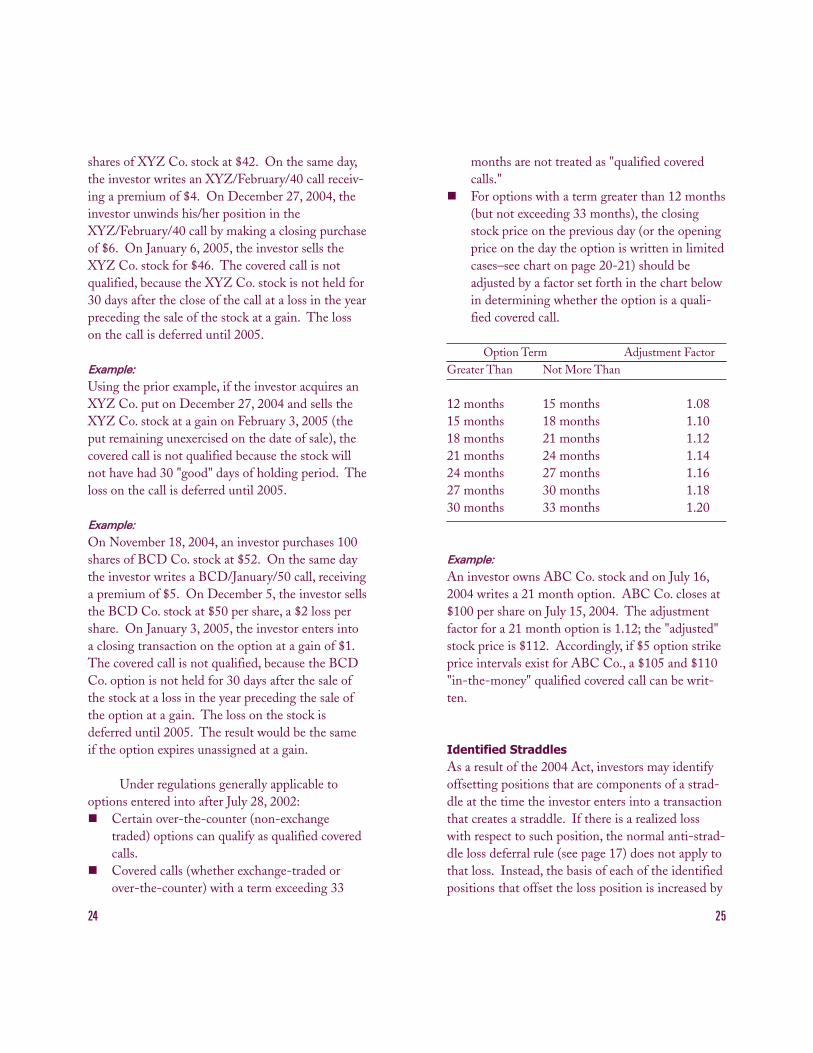

months are not treated as "qualified covered calls."For options with a term greater than 12 months(but not exceeding 33 months), the closing stock price on the previous day (or the opening price on the day the option is written in limitedcases–see chart on page 20-21) should be adjusted by a factor set forth in the chart below in determining whether the option is a quali-fied covered call.

Option Term Adjustment FactorGreater Than Not More Than

12 months 15 months 1.0815 months 18 months 1.1018 months 21 months 1.1221 months 24 months 1.1424 months 27 months 1.1627 months 30 months 1.1830 months 33 months 1.20

EExxaammppllee::

An investor owns ABC Co. stock and on July 16,2004 writes a 21 month option. ABC Co. closes at$100 per share on July 15, 2004. The adjustmentfactor for a 21 month option is 1.12; the "adjusted"stock price is $112. Accordingly, if $5 option strikeprice intervals exist for ABC Co., a $105 and $110"in-the-money" qualified covered call can be writ-ten.

Identified StraddlesAs a result of the 2004 Act, investors may identifyoffsetting positions that are components of a strad-dle at the time the investor enters into a transactionthat creates a straddle. If there is a realized losswith respect to such position, the normal anti-strad-dle loss deferral rule (see page 17) does not apply tothat loss. Instead, the basis of each of the identifiedpositions that offset the loss position is increased by

25

shares of XYZ Co. stock at $42. On the same day,the investor writes an XYZ/February/40 call receiv-ing a premium of $4. On December 27, 2004, theinvestor unwinds his/her position in theXYZ/February/40 call by making a closing purchaseof $6. On January 6, 2005, the investor sells theXYZ Co. stock for $46. The covered call is notqualified, because the XYZ Co. stock is not held for30 days after the close of the call at a loss in the yearpreceding the sale of the stock at a gain. The losson the call is deferred until 2005.

EExxaammppllee::

Using the prior example, if the investor acquires anXYZ Co. put on December 27, 2004 and sells theXYZ Co. stock at a gain on February 3, 2005 (theput remaining unexercised on the date of sale), thecovered call is not qualified because the stock willnot have had 30 "good" days of holding period. Theloss on the call is deferred until 2005.

EExxaammppllee::

On November 18, 2004, an investor purchases 100shares of BCD Co. stock at $52. On the same daythe investor writes a BCD/January/50 call, receivinga premium of $5. On December 5, the investor sellsthe BCD Co. stock at $50 per share, a $2 loss pershare. On January 3, 2005, the investor enters intoa closing transaction on the option at a gain of $1.The covered call is not qualified, because the BCDCo. option is not held for 30 days after the sale ofthe stock at a loss in the year preceding the sale ofthe option at a gain. The loss on the stock isdeferred until 2005. The result would be the sameif the option expires unassigned at a gain.

Under regulations generally applicable tooptions entered into after July 28, 2002:

Certain over-the-counter (non-exchange traded) options can qualify as qualified covered calls.Covered calls (whether exchange-traded or over-the-counter) with a term exceeding 33

24

comprises more than 30% of the index’s weightingor (3) the five highest weighted component securi-ties in the aggregate comprise more than 60% of theindex weighting. Previously, options on a stock indexof a type that had neither been designated by theCommodity Futures Trading Commission (CFTC)as eligible for trading on a commodity futuresexchange nor had been determined by the Treasuryto be eligible for such designation generally weretreated as narrow based unless the Securities andExchange Commission had determined that theindex was broad based for regulatory purposes.

Foreign equity index warrants traded on U.S.exchanges are subject to the same tax considerationsas options. Thus, foreign equity index warrants gen-erally should be treated as Section 1256 contracts.

For individual investors, assets which requiremark-to-market treatment generally must be treatedas sold at their fair market value on the last businessday of the taxable year (and simultaneously repur-chased), even if they have not been disposed. For allof these assets, the gains and losses, both actuallyrealized during the year and deemed realized (byvirtue of being marked-to-market at year-end), areaggregated. The combined gains and losses are net-ted, and the net gain or loss is then treated as 60%long-term capital gain or loss (entitled to the maxi-mum 15% long-term tax rate) and 40% short-termcapital gain or loss. This long-term and short-termcapital gain is treated as any other capital gain.Therefore, other capital losses offset these gains. Netshort-term capital gain but not net long-term capitalgain is investment income for investment interestlimitation purposes. See discussion of "InvestmentIncome and Other Investment Expenses" on page 39.

For those positions marked-to-market at year-end, the basis for determining gain or loss is the newmark-to-market value. This prevents the gain or lossfrom being counted twice. It is possible that aSection 1256 contract having a gain attributable to itin one year could have a loss attributable to it in thenext. These gains and losses cannot be netted in oneyear’s return, but are shown in the separate years as a

27

a specified portion of the loss. This rule is effectivefor positions established on or after October 22,2004 that substantially diminish the risk of lossfrom holding offsetting positions (regardless ofwhen such offsetting position was established).

Non-Equity and Stock Index Instruments"Mark-to-market" and "60/40" (i.e., 60 percent long-term, 40 percent short-term) treatment applies to"broad-based" U.S. stock index options (such as theStandard & Poor’s® 100 Index option, the NYSEComposite Index® option, the Dow Jones IndustrialAverageSM option at the Chicago Board OptionsExchange and the Major Market Index option at theAmex) and options on broad-based stock indexfutures, such as the option on the Standard & Poor’s®500 Stock Index future at the Chicago MercantileExchange and the option on the NYSE CompositeIndex® future at the New York Futures Exchange.

This tax treatment also applies to regulatedfutures contracts and certain options where theunderlying property is not equity based, such asinterest rate, foreign currency (for example, thosetraded on the Philadelphia Stock Exchange), andcommodity options and futures options. Theseinstruments are referred to as "Section 1256 con-tracts."

Options on a stock index that is "narrowbased" are subject to the rules governing the taxationof equity options and are not entitled to 60/40 mark-to-market treatment.

As of December 21, 2000, what constitutes anarrow based index has been significantly limited.Under the current definition, an index generally isnarrow based only if (1) it contains nine or fewercomponent securities, (2) a component security

26

sale rules. See discussion on pages 7-14. For exam-ple, an investor who sells stock at a loss and entersinto a long securities futures contract to purchase thesame stock within 30 days before or after the sale at aloss is subject to the wash sale rule. Similarly, aninvestor who holds an appreciated stock position andenters into a short securities futures contract withrespect to the same stock will have a constructive saleevent unless three conditions (as set forth in the con-structive sale provisions) are met: (1) the securitiesfutures contract is unwound before the end of the30th day after the close of the taxable year; (2) thestock position is held throughout the 60-day periodbeginning on the date the short securities futures con-tract is unwound; and (3) during the 60-day period,the stock position remains unhedged (with limitedexception).

Exchange Traded Fund Shares

Exchange traded fund shares are generally interestsin open-end investment companies that hold secu-rities constituting or based on an index or portfolioof securities. Examples of such shares are Standard& Poor’s Depositary Receipts ("SPDRs"), Nasdaq-100 Index Tracking Stock and DIAMONDS.These shares are generally taxed as interests in aregulated investment company ("mutual fund") forFederal income tax purposes. Thus, dividends paidfrom investment income (including dividends,interest and net short-term capital gains) are tax-able to beneficial owners as ordinary income.Similarly, capital gain distributions from net long-term capital gains are taxable as long-term capitalgains regardless of the length of time an investorhas owned the fund shares.

Exchange traded funds may also be structuredas investment trusts, with issued shares represent-ing units of fractional undivided beneficial interests

29

separate gain and a separate loss (that is, combinedwith all the other Section 1256 contracts). Theexercise of a Section 1256 contract is generally treat-ed as a disposition of a Section 1256 contract.

Single Stock and Narrow Based Stock Index FuturesAs a result of legislation enacted in late 2000, trad-ing in single stock and narrow based stock indexfutures and options on stock futures is now permit-ted. These are referred to as "securities futures con-tracts." Trading in such instruments began inNovember, 2002.

For investors, securities futures contracts aretaxed in a manner similar to equity options ratherthan futures contracts. Accordingly, they are notsubject to 60% long-term, 40% short-term capital,mark-to-market treatment. See discussion of"Non-Equity and Stock Index Instruments" onpage 26. Investor gains and losses from securitiesfutures contracts have the same character (capital orordinary) as the character of the securities underly-ing the contract in the investor's hands. As a result,gain or loss on the sale of a securities futures con-tract results in capital gain or loss treatment. Gainor loss on the sale of a "long" securities futures con-tract held more than one year will be long-term, andshort-term if held for one year or less. Gain or losson the sale of a "short" securities futures contract willbe short-term regardless of how long the investorhas held the contract (except as provided in futureanti-straddle regulations). The holding period forsecurities acquired pursuant to a long securities futurescontract includes the investor's holding period for thecontract.

Securities futures contracts are subject to thewash sale, short sale, anti-straddle and constructive

28

Bonds and Other Debt InstrumentsThe Federal income tax consequences of investing incorporate debt obligations are somewhat more com-plex than the tax consequences of investing in stocks.The general rule is that an investor will realize long-term or short-term capital gain, or may sustain long-term or short-term capital loss, as the case may be, onthe sale of corporate debt obligations.

In recent years, however, the general rule hasbeen eroded by a series of provisions dealing with"original issue discount," "market discount," "premi-um" and "short-term" obligations. In addition, spe-cial rules apply if the obligation is debt-financed(e.g., "margined"). These rules typically convertcapital gain to ordinary income, cause certainincome to be recognized currently for tax purposes,or match interest income and interest expense.

Original Issue DiscountThe original issue discount (OID) provisions applyto debt obligations issued at a discount from theprincipal amount of the obligation. The amount ofOID is the excess of the stated redemption price atmaturity over the issue price of the obligation. Theminimum amounts of OID (less than 1/4 of 1% ofthe stated redemption price at maturity multipliedby the number of complete years to maturity) arenot taken into account. A holder of a debt obliga-tion with OID is required to currently include inincome, during the period the bond is held, theamount of OID attributable to each taxable year.The OID included in income is treated as ordinaryinterest income. With respect to corporate obliga-tions issued after July 1, 1982, OID is computed onan "economic accrual" (constant interest) basis.OID on corporate obligations issued before July 2,1982 is included in income ratably. The amount of

31

in and ownership of the trust. Examples are certainexchange traded funds that track the price of gold.In this case, investors generally are treated as if theydirectly own a pro rata share of the underlyingassets held in the trust. Investors are also treated asif they directly received their respective pro ratashares of the trust's income, if any, and directlyincurred their respective shares of the expenses.Upon a sale of some or all of an investor's shares,the investor is treated as having sold the portion ofhis/her pro rata share of the trust's underlyingassets at the time of the sale attributable to theshares sold.

In addition, there are listed options on certainexchange traded fund shares. Where the underly-ing portfolio or index is not broad based (see page26), the related option is taxed as a regular equityoption (page 14). The taxation of options onexchange traded fund shares where the underlyingportfolio or index is broad based is currently uncer-tain and requires guidance from the Treasury.

Mixed Straddles

When a straddle consists of both Section 1256 con-tracts (see page 26) and non-Section 1256 positions,a "mixed straddle" results. The taxation of mixedstraddles is exceedingly complex and is dependent,in part, on whether certain elections are made,whether net gain or loss is attributable to theSection 1256 or to the non-Section 1256 positionsand whether mark-to-market rules apply.

The significance of a mixed straddle can begreat as a result of the rate differential betweenlong-term and short-term capital gain and loss.Loss deferral and capitalization rules also apply(page 17). A straddle where at least one position isordinary and one is capital will also be a mixedstraddle.

30

taxpayer’s basis for the obligation immediately afterits acquisition.

As with OID, market discount is generallytreated as ordinary interest income. However, it isnot taxable until the disposition of the obligation bythe taxpayer. The taxable amount of market dis-count is the amount that has accrued during theperiod the taxpayer has held the bond. If the mar-ket discount is less than 1/4 of 1% of the statedredemption price at maturity multiplied by thenumber of complete years to maturity (after the tax-payer acquired the bond), the market discount istreated as zero.

This ordinary income treatment did not gen-erally apply to tax-exempt obligations or to marketdiscount obligations issued on or before July 18,1984. Special rules applied to debt-financed marketdiscount obligations issued on or before July 18,1984, but acquired after that date. This ordinarytreatment applies to tax-exempt obligations and toall market discount obligations issued on or beforeJuly 18, 1984 if the obligations are acquired afterApril 30, 1993.

Market discount is treated as accruing inequal daily installments; however, at the election ofthe taxpayer on an obligation-by-obligation basis, itcan be computed on an economic accrual method.

EExxaammppllee::

On July 2, 2001, an investor acquires $100,000 faceamount XYZ 12s, due July 1, 2005, for $96,000.The obligations were issued January 1, 1999 at par.The obligations are sold on July 1, 2003 for$99,000. The tax consequences in the year of saleare as follows (assuming straight line accrual ofmarket discount and excluding the effect of accruedcoupon interest purchased and sold):

Realized gain ($99,000–$96,000) $3,000Gain treated as ordinary income($4,000 market discount x 729/1460) $1,997Long-term capital gain $1,003

33

OID included in income in either case is added tothe basis of the obligation.

Under the economic accrual method, OIDaccrues in a manner similar to the accrual of intereston deposits by financial institutions. The ratableshare of OID is based on the number of days thetaxpayer holds the obligation after its acquisitionrelative to the number of days until maturity.

Although OID on tax-exempt obligations isnot includible in the investor’s taxable income, itmust still be taken into account. OID on tax-exempt obligations accrues on an economic accrualbasis and increases the investor’s basis in the obliga-tion for purposes of determining gain or loss on itsdisposition or payment at maturity.

Zero coupon bonds are generally subject tothe OID rules.

OID concepts also apply to certainredeemable preferred stock issued after October 9,1990 with redemption premium. Like OID,redemption premium exists if the redemption priceat maturity exceeds the issue price by more than ade minimis amount (same standard is applied in thecase of OID). While such stock is not debt forFederal income tax purposes, the entire amount ofthe redemption premium is treated as being distrib-uted to holders on an economic accrual basis overthe period that the stock is outstanding. Theincome tax consequences of such a distribution toan individual shareholder depend on the paying cor-poration’s current and accumulated earnings. Thedistribution could result either in currently taxableordinary income, capital gain, or nontaxable returnof capital (in the latter case with an equivalentreduction in the basis of the stock).

Market DiscountDebt obligations are subject to the market discountrules in addition to the OID rules. The marketdiscount rules apply to debt obligations acquired ata discount in contrast to those issued at a discount.Market discount is the difference, if any, betweenthe stated redemption price at maturity and the

32

the taxpayer during the taxable year.With respect to any market discount bond, net

direct interest expense is the amount of interestexpense incurred by the taxpayer in excess of all inter-est income (including OID) includible in the taxpay-er’s gross income for the taxable year from that bond.Any disallowed interest expense will be deductible inthe year the taxpayer disposes of the bond. Aninvestor may elect, on an obligation-by-obligationbasis, to deduct the deferred interest expense in a yearin which there is net interest income (in excess ofinterest expense) on the obligation.

An investor may avoid the limitation on inter-est expense deductions by electing to include marketdiscount currently in income during each taxableyear. This election must be made for all market dis-count bonds held at the time of the election or sub-sequently acquired.

There are no similar provisions disallowinginterest expense deductions on debt-financed OIDobligations. However, interest expense on debtincurred to carry OID obligations is subject to theinvestment interest limitation rules (see page 39). Theinvestment interest limitation also applies to interestexpense on debt-financed market discount obliga-tions, after the application of the disallowance rule.

Short-Term ObligationsDiscount on short-term obligations is not included asincome by individual investors until the obligation isdisposed or paid at maturity. For this purpose, anobligation is short-term if the period from issue dateto maturity is one year or less. Any gain on disposi-tion is treated as ordinary interest income to theextent of the ratable share of the discount for the peri-od the taxpayer has held the short-term obligation.Any excess gain or any loss realized is short-term.

If a short-term obligation held by an individ-ual investor is financed, under rules similar to thoseapplying to market discount bonds, the net directinterest expense is deferred until the discount istaken into income by the taxpayer (i.e., at disposi-

35

The market discount and OID provisions canapply simultaneously to an obligation. An investorwill have market discount if an OID obligation ispurchased for less than the issue price plus theamount of accrued OID on the obligation sincethe date of issue.

EExxaammppllee::

XYZ Corp. $1,000 face amount 12s, due September1, 2004, were issued on September 1, 2000 for $960.On September 1, 2001, an investor acquires$100,000 face amount of the bonds for $95,913.The amount of OID that has accrued on the bondssince the issue date (using the economic accrualmethod) is $813. Therefore, since the purchaseprice is less than the issue price plus the accruedOID ($96,813), the investor has market discount of$900 ($96,813–$95,913). The remaining OID onthe obligation is $3,187 ($100,000–$96,813), whichwill be included in the investor’s taxable incomeduring the period the bonds are held and willincrease his/her basis in the bonds. If the bonds areheld until maturity, the investor will include the$900 of market discount in taxable income as ordi-nary interest income at that time.

EExxaammppllee::

Using the prior example, assume that the bonds areinstead issued by State Z. The remaining OID of$3,187 is tax-exempt interest and will increase theinvestor’s basis in the bonds as it accrues. As in theprior example, if the bonds are held until maturity,the investor will include the $900 of market dis-count in taxable income as ordinary interest incomeat that time.

Investors are limited in the amount of interestexpense they are able to currently deduct on indebt-edness incurred to purchase or carry an obligationwith market discount. A taxpayer is able to deductthe "net direct interest expense" only to the extentthat it exceeds the amount of accrued market dis-count on the obligation for the period it is held by

34

subject of active consideration by the TreasuryDepartment and Internal Revenue Service. The useof these instruments continues to evolve, as do thetax rules that apply.

Conversion Transactions

For transactions entered into after April 30, 1993,the Internal Revenue Code re-characterizes as ordi-nary income certain amounts that would otherwisebe considered capital gain (short-term or long-term) which arise from a "conversion transaction."In a conversion transaction, the investor is in theeconomic position of a lender — the investor has anexpectation of a return from the transaction that insubstance is in the nature of interest and undertakesno significant risks other than those typical of alender. A conversion transaction is a transaction forwhich substantially all of an investor’s return isattributable to the time value of the net investmentand the investor (1) bought property and, at thesame time, agreed to sell the same or substantiallyidentical property for a higher price in the future;(2) created a "straddle" of actively traded property(see page 16); or (3) entered into a transaction thatwas marketed or sold as producing capital gain.Also, the Treasury Department is authorized toissue regulations in the future describing othertransactions it will treat as conversion transactionssubject to these rules.

In general, the amount of gain re-character-ized as ordinary income will not exceed the amountdetermined by applying 120% of the appropriateapplicable Federal interest rate to the investor’s netinvestment in the conversion transaction.

While the application of this provision to thetaxation of investments by individuals is currentlyunclear pending the issuance of official Treasury

37

tion or maturity). A taxpayer may avoid this limita-tion by electing to include discount currently on allshort-term obligations held.

These rules apply with respect to both OID onshort-term non-governmental obligations and "acqui-sition discount" on short-term governmental obliga-tions (such as Treasury bills). Acquisition discount isthe difference between the stated redemption price atmaturity and the taxpayer’s basis in the obligation.

Amortizable Bond PremiumBond premium is the amount paid for a bond inexcess of its face value. The premium effectivelyreduces the yield on the bond. In the case of taxablebonds, a taxpayer may elect to amortize the bondpremium over the remaining life of the bond. Thiselection is binding for all taxable bonds held oracquired in the first year to which the electionapplies or in subsequent years.

The premium is amortized on an economicaccrual basis (for obligations issued after September27, 1985). Such amortizable premium is appliedagainst and reduces the interest income on thebond. A taxpayer’s basis in the bond is decreased toreflect the premium so applied. In the case of tax-exempt bonds, the premium (which must be amor-tized) is not deductible, but basis is reduced by theamount of the amortized bond premium.

Convertibles and ExchangeablesThe conversion of bonds into stock of the sameissuer is generally not a taxable transaction. Thestock received will have the same holding periodand basis as the converted bonds. Any unaccruedOID will not be recognized. Accrued market dis-count at the time of the conversion will be recog-nized when the stock received is disposed. In con-trast, the exchange of debt obligations of one issuerfor debt obligations or stock of another issuer willgenerally be a taxable transaction.

A detailed discussion of the taxation of"hybrid instruments" ostensibly in debt form isbeyond the scope of this booklet. However, it is the

36

Investment Income andOther Investment ExpensesSubject to the application of the anti-straddle rules(see page 16) an individual investor may currentlydeduct interest on debt incurred to purchase orcarry investment property ("investment interest") inan amount equal to the individual’s net investmentincome. Investment interest paid during the yearthat exceeds the limitation may be carried forwardand may be deducted in future years (subject to thelimitation applicable in that year).

Margin interest, otherwise deductible shortsale expenses and amortizable bond premium withrespect to premium obligations acquired afterOctober 22, 1986 are examples of investment interest. Net investment income does not includenet capital gain (net long-term capital gain minusnet short-term capital loss). An investor can elect to include in investment income so much ofhis/her net capital gain as he/she chooses, but theamount of net capital gain eligible for the 15% capi-tal gain rate must be reduced by the same amount.Net short-term capital gains are included in invest-ment income. Similarly, dividends are not treated asinvestment income unless the investor elects to treatthe dividend as not eligible for the lower tax rates.See discussion on page 3.

Itemized deductions for investment advisory,custody and trust administration fees, subscriptionsto investment advisory publications and similarexpenses of producing income (other than trade orbusiness expenses) are limited. Such "miscellaneousitemized deductions" and certain employee businessexpenses are deductible only to the extent that, in theaggregate, they exceed 2% of the taxpayer’s adjustedgross income. However, certain expenses deductibleas miscellaneous itemized deductions are not subjectto the 2% floor. These include bond premium amor-tization and short-sale expenses.

39

guidelines, the legislative history of this section suggests the following:

Buying stock and writing an option where thereis no substantial certainty that the holder of theoption will exercise the option (e.g., long the stock, short an out-of-the-money call on the stock) is not a conversion transaction.An investor’s net investment in a conversion transaction is the total amount invested less any amount received by the investor for entering into any position as part of the overall conversion transaction – for example, the receipt of option premium in granting an option.In determining an investor’s net investment in aconversion transaction, the source of the investor’s funds generally will not be taken into account. Thus, if an investor purchased stock for $1,000 but borrowed $900, the net invest-ment would still be $1,000.Amounts that a taxpayer may be committed to pay in the future (e.g., through a futures con-tract) generally will not be treated as an invest-ment until such time as the amounts are in fact committed to the transaction and are unavailable to invest in other ways. A margin "deposit" is not viewed as an investment.

EExxaammppllee::

On January 6, 2004, an investor enters into a longfutures contract committing the investor to pur-chase a certain quantity of gold on March 1, 2004for $10,000. Also on January 6, the investor entersinto a short futures contract to sell the same quanti-ty of gold on April 1, 2004 for $10,060. Theinvestor makes the required margin deposit. OnFebruary 3, 2004 both contracts are terminated for anet profit of $20. No part of that $20 is subject tore-characterization because the investor has noinvestment in the transaction on which the $20could be considered an interest equivalent return.

38

In-the-Money Qualified Covered Calls ForStock Priced $25 or Less ($1.00 intervals)Applicable Stock Price ($) Strike Price ($)2.51 to 2.94 2.502.95 to 4.00 None4.01 to 4.70 4.004.71 to 5.00 None5.01 to 5.88 5.005.89 to 6.00 None6.01 to 7.00 6.007.01 to 8.00 7.008.01 to 9.00 8.009.01 to 10.00 9.0010.01 to 11.00 10.0011.01 to 12.00 11.0012.01 to 13.00 12.0013.01 to 14.00 13.0014.01 to 15.00 14.0015.01 to 16.00 15.0016.01 to 17.00 16.0017.01 to 18.00 17.0018.01 to 19.00 18.0019.01 to 20.00 19.0020.01 to 22.50 20.0022.51 to 25.00 22.50

SSoommee llooww pprriicceedd ssttoocckkss ttrraaddee ooppttiioonnss iinn $$11 iinntteerrvvaallss aannddootthheerrss ttrraaddee iinn ssttaannddaarrdd $$22..5500 iinntteerrvvaallss ((oorr aa hhyybbrriidd ooff$$11 aanndd $$22..5500 iinntteerrvvaallss)) .. IInnvveessttoorrss nneeeedd ttoo ddeetteerrmmiinneewwhhiicchh ssttrriikkee pprriiccee ooppttiioonnss aarree lliisstteedd ffoorr aa ppaarrttiiccuullaarr ccoommppaannyy..

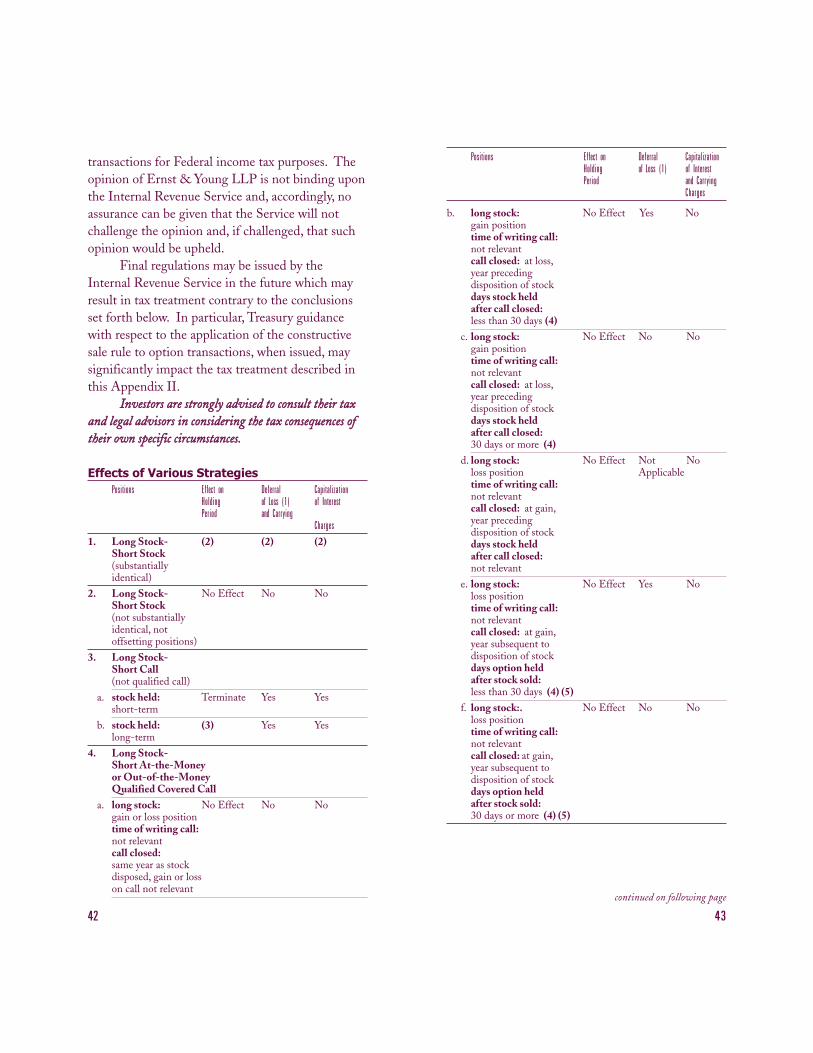

Appendix II

Taking into account proposed and temporaryTreasury regulations on offsetting positions, the fol-lowing chart represents the current opinion of Ernst& Young LLP as to the treatment of the described

41

Individuals whose adjusted gross income is overan inflation adjusted dollar amount will have most oftheir itemized deductions reduced by 3% of the adjust-ed gross income over that amount. In 2004, that num-ber is $142,700 ($71,350 for married taxpayers filingseparately). In 2005, that number is $145,950 ($72,975for married taxpayers filing separately). Investmentinterest expense (such as margin account interest) is notincluded as an itemized deduction for purposes of thisdeduction limitation. In no event are total otherwiseallowable itemized deductions (excluding those notcovered by the new rules) reduced by more than 80% asa result of this limitation. This limitation is appliedafter the application of the 2% floor and impacts regu-lar tax but not the alternative minimum tax.

Appendix I

In-the-Money Qualified Covered Calls For Stock Priced $25 or Less ($2.50 intervals)Applicable Stock Price ($) Strike Price ($)5.01 to 5.88 55.89 to 7.50 None7.51 to 8.82 7.508.83 to 10.00 None10.01 to 11.76 1011.77 to 12.50 None12.51 to 14.70 12.5014.71 to 15.00 None15.01 to 17.50 1517.51 to 20.00 17.5020.01 to 22.50 2022.51 to 25.00 22.50

40

b. long stock: No Effect Yes Nogain positiontime of writing call:not relevantcall closed: at loss,year preceding disposition of stockdays stock heldafter call closed:less than 30 days (4)

c. long stock: No Effect No Nogain positiontime of writing call:not relevantcall closed: at loss,year preceding disposition of stockdays stock heldafter call closed:30 days or more (4)

d. long stock: No Effect Not Noloss position Applicabletime of writing call:not relevantcall closed: at gain,year preceding disposition of stockdays stock heldafter call closed:not relevant

e. long stock: No Effect Yes Noloss positiontime of writing call:not relevantcall closed: at gain,year subsequent todisposition of stockdays option held after stock sold:less than 30 days (4) (5)

f. long stock:. No Effect No Noloss positiontime of writing call:not relevantcall closed: at gain,year subsequent todisposition of stockdays option held after stock sold:30 days or more (4) (5)

43

transactions for Federal income tax purposes. Theopinion of Ernst & Young LLP is not binding uponthe Internal Revenue Service and, accordingly, noassurance can be given that the Service will notchallenge the opinion and, if challenged, that suchopinion would be upheld.

Final regulations may be issued by theInternal Revenue Service in the future which mayresult in tax treatment contrary to the conclusionsset forth below. In particular, Treasury guidancewith respect to the application of the constructivesale rule to option transactions, when issued, maysignificantly impact the tax treatment described inthis Appendix II.

IInnvveessttoorrss aarree ssttrroonnggllyy aaddvviisseedd ttoo ccoonnssuulltt tthheeiirr ttaaxxaanndd lleeggaall aaddvviissoorrss iinn ccoonnssiiddeerriinngg tthhee ttaaxx ccoonnsseeqquueenncceess oofftthheeiirr oowwnn ssppeecciiffiicc cciirrccuummssttaanncceess..

Effects of Various StrategiesPositions Effect on Deferral Capitalization

Holding of Loss (1) of InterestPeriod and Carrying

Charges1. Long Stock- (2) (2) (2)

Short Stock(substantiallyidentical)

2. Long Stock- No Effect No NoShort Stock(not substantiallyidentical, not offsetting positions)

3. Long Stock-Short Call(not qualified call)

a. stock held: Terminate Yes Yesshort-term

b. stock held: (3) Yes Yeslong-term

4. Long Stock-Short At-the-Moneyor Out-of-the-MoneyQualified Covered Call

a. long stock: No Effect No Nogain or loss positiontime of writing call:not relevantcall closed:same year as stock disposed, gain or loss on call not relevant

42

Positions Effect on Deferral CapitalizationHolding of Loss (1) of InterestPeriod and Carrying

Charges

continued on following page

days stock heldafter call closed:30 days or more (4)

g. long stock: No Effect Not Noloss position Applicabletime of writing call:stock held long-termcall closed: at gain,year preceding disposition of stockdays stock heldafter call closed:not relevant

h. long stock: Suspend Not Noloss position Applicabletime of writing call:stock held short-termcall closed: at gain,year preceding disposition of stockdays stock heldafter call closed:not relevant

i. long stock: No Effect Yes Noloss positiontime of writing call:stock held long-termcall closed: at gain,year subsequent todisposition of stockdays option held after stock sold:less than 30 days (4)(5)

j. long stock: No Effect No Noloss positiontime of writing call:stock held long-termcall closed: at gain,year subsequent todisposition of stockdays option held after stock sold:30 days or more (4)(5)

k. long stock: Suspend Yes Noloss positiontime of writing call:stock held short-termcall closed: at gain,year subsequent todisposition of stockdays option held after stock sold:less than 30 days (4)(5)

45

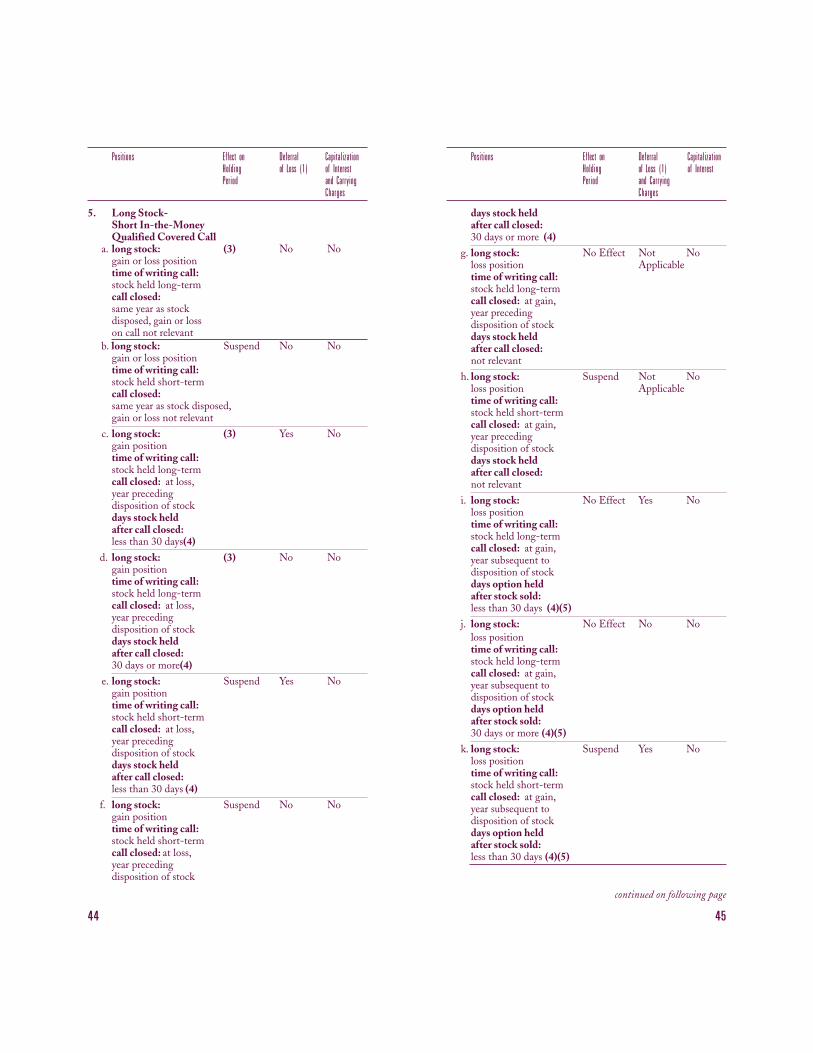

5. Long Stock-Short In-the-MoneyQualified Covered Call

a. long stock: (3) No Nogain or loss positiontime of writing call:stock held long-termcall closed:same year as stock disposed, gain or loss on call not relevant

b. long stock: Suspend No Nogain or loss positiontime of writing call:stock held short-termcall closed:same year as stock disposed,gain or loss not relevant

c. long stock: (3) Yes Nogain positiontime of writing call:stock held long-termcall closed: at loss,year preceding disposition of stockdays stock heldafter call closed:less than 30 days(4)

d. long stock: (3) No Nogain positiontime of writing call:stock held long-termcall closed: at loss,year preceding disposition of stockdays stock heldafter call closed:30 days or more(4)