tbr software business quarterly vendor performance review

TRANSCRIPT

TBR

TECHNOLOGY BUSINESS RESEARCH, INC.

TBR’s Software Business QuarterlySM

Research Highlights and OutlookTechnology Business Research Quarterly Webinar Series

Sept. 26, 2012

TBR

2 TBR Quarterly Webinar Series | 9.26.12 | www.tbri.com | ©2012 Technology Business Research Inc.

Software Business Quarterly Research Highlights and Outlook: Webinar Presenters

Elizabeth Hedstrom HenlinAnalyst, Software [email protected]@EAHHTBR

Stuart WilliamsDirector, TBR’s Software [email protected]@s2_williams

TBR

3 TBR Quarterly Webinar Series | 9.26.12 | www.tbri.com | ©2012 Technology Business Research Inc.

Go to Market (GTM): Target new partnerships and acquisitions to rapidly expand GTM routes.

Corporate Reinvention: Invest in areas needed to drive CY13 success in product and GTM.

With cloud and mobility continuing to transform software consumption, enterprise software vendors are “holding the line” with three key tactics

SBQ 2Q12 Research Highlights and 2012 Outlook

Software Vendor Trends for 2012

Product Portfolio: Expand capabilities, attaching to high-interest trends and satisfying the install base.

SOURCE: TBR RESEARCH AND ESTIMATES; COMPANY DATA AND ESTIMATES

TBR

4 TBR Quarterly Webinar Series | 9.26.12 | www.tbri.com | ©2012 Technology Business Research Inc.

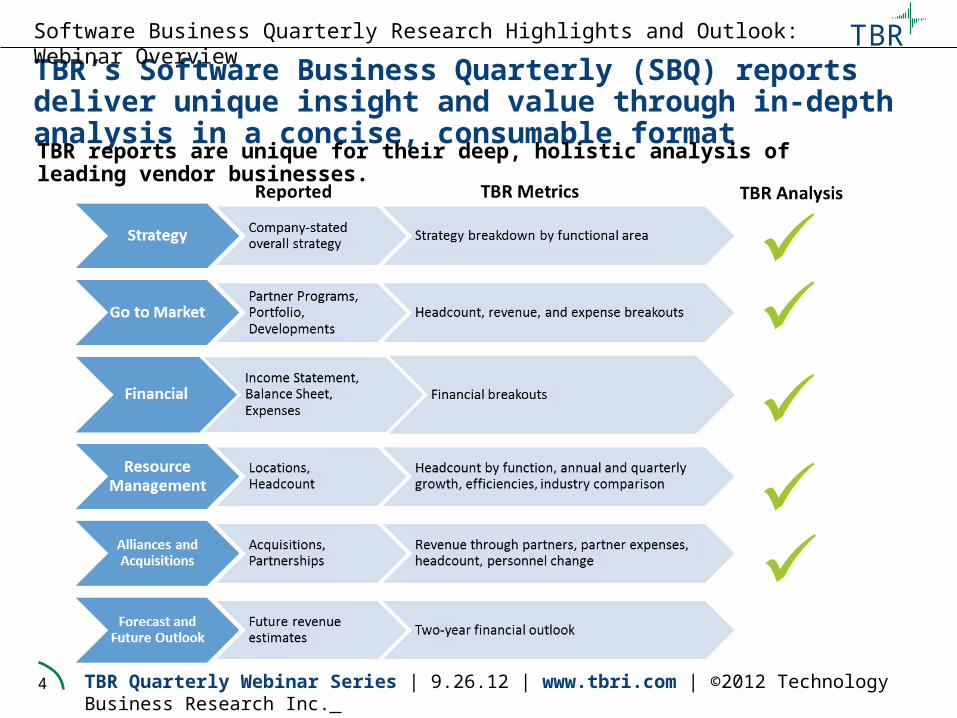

TBR’s Software Business Quarterly (SBQ) reports deliver unique insight and value through in-depth analysis in a concise, consumable format TBR reports are unique for their deep, holistic analysis of leading vendor businesses.

Software Business Quarterly Research Highlights and Outlook: Webinar Overview

TBR

5 TBR Quarterly Webinar Series | 9.26.12 | www.tbri.com | ©2012 Technology Business Research Inc.

TBR’s Software Business Quarterly covers the vendors that make and shape enterprise software markets

Software Business Quarterly Research Highlights and Outlook: Webinar Overview

TBR Software Business Quarterly Portfolio

Vendor Reports:

• BMC Software

• CA Technologies

• HP Software

• IBM Software

• Microsoft Corp

• Oracle Corp.

• Red Hat, Inc.

• SAP AG

• SAS Institute, Inc. (semiannual)

• Symantec Corp.

• VMware, Inc.

Software Vendor Benchmark (29): Oracle Corp.

IBM Software

VMware

Microsoft

SAP

Symantec

BMC

CA

HP Software

Salesforce.com

Adobe

Autodesk

Check Point

Citrix

CommVault

Compuware

EMC

Informatica

Intuit

JDA

NetSuite

Open Text

Progress Software

Quest Software (Dell)

Red Hat

Sage

Software AG

Tibco

Trend Micro

TBR

6 TBR Quarterly Webinar Series | 9.26.12 | www.tbri.com | ©2012 Technology Business Research Inc.

SBQ 2Q12 Research Highlightsand 2012 Outlook

TBR

7 TBR Quarterly Webinar Series | 9.26.12 | www.tbri.com | ©2012 Technology Business Research Inc.

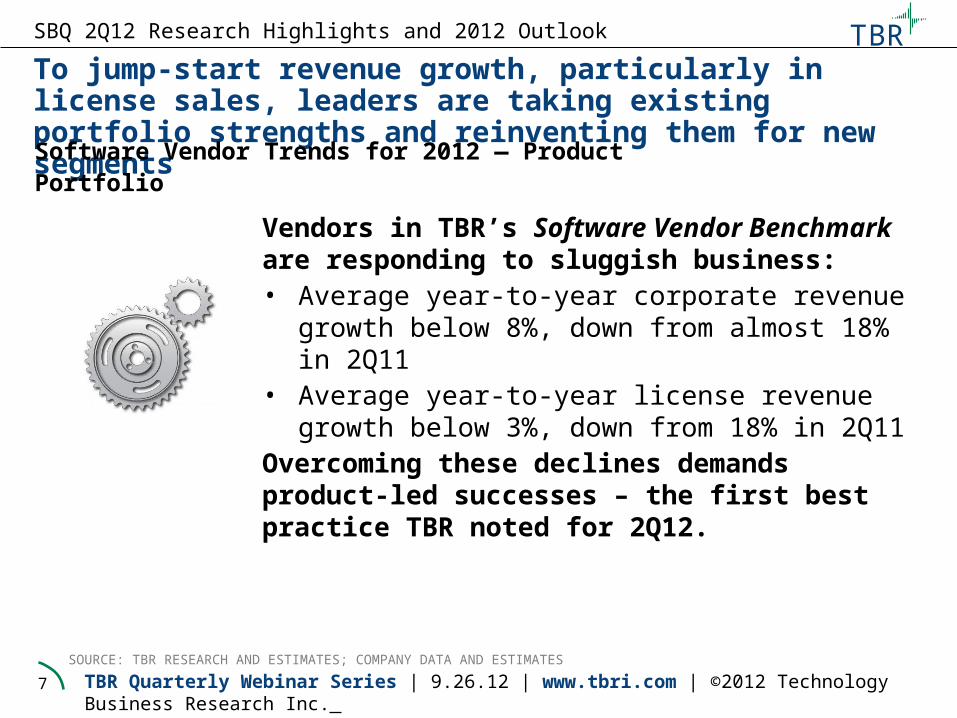

Vendors in TBR’s Software Vendor Benchmark are responding to sluggish business:• Average year-to-year corporate revenue growth below

8%, down from almost 18% in 2Q11• Average year-to-year license revenue growth below 3%,

down from 18% in 2Q11 Overcoming these declines demands product-led successes – the first best practice TBR noted for 2Q12.

To jump-start revenue growth, particularly in license sales, leaders are taking existing portfolio strengths and reinventing them for new segments

SBQ 2Q12 Research Highlights and 2012 Outlook

Software Vendor Trends for 2012 — Product Portfolio

SOURCE: TBR RESEARCH AND ESTIMATES; COMPANY DATA AND ESTIMATES

TBR

8 TBR Quarterly Webinar Series | 9.26.12 | www.tbri.com | ©2012 Technology Business Research Inc.

SBQ 2Q12 Research Highlights: Key Trends

SOURCE: TBR RESEARCH AND ESTIMATES; COMPANY DATA AND ESTIMATES

TBR projects license revenue growth will remain in single digits through 2012 as vendors integrate product portfolios to accelerate go-to-market gains in 2013

License revenue growth fell precipitously in 1Q12, with leaders driving licensing gains through security and subscription-delivered solutions

TBR

9 TBR Quarterly Webinar Series | 9.26.12 | www.tbri.com | ©2012 Technology Business Research Inc.

Customer adoption of disruptive trends are influencing software vendors’ portfolio road maps to include new features, defending install bases

BMC Software:BMC cloud-related sales are rising — now roughly 25% of BMC’s total ESM revenue. BMC Cloud Lifecycle Manager is enjoying large enterprise success with strong sales and customer acceptance but has yet to penetrate the midmarket.Microsoft:With mobile functionality added to the pending launch of Office (set for late 2012), Microsoft will augment both on-premises and cloud Office suite deployments — creating cross-sell and upsell opportunities for direct and indirect teams.Red Hat:Red Hat’s 2Q12 launch of CloudForms adds to its portfolio an open-source cloud management platform designed to span deployment and delivery methods — creating an infrastructure layer with on- and off-premises integration points.VMware:VMware refreshed the vFabric suite during 2Q12, expanding its cloud infrastructure automation and management capabilities. Executives credited solution sales for CY2Q12 double-digit revenue growth.

SBQ 2012 Research Outlook: Product Portfolio

Highlighted Vendor Best Practices — 2Q12 SBQ Vendor Reports

SOURCE: TBR RESEARCH AND ESTIMATES; COMPANY DATA AND ESTIMATES

TBR

10 TBR Quarterly Webinar Series | 9.26.12 | www.tbri.com | ©2012 Technology Business Research Inc.

Highlights from TBR’s Assessment of BMC Software’s Two-year Strategic OutlookKey TakeawaysFinancial: Numara will serve as a template for midmarket and channel success in other BMC business segments. Go to Market: Cloud and mobile computing dominate BMC’s go-to-market, while it continues to take advantage of demand for mainframe solutions. Resource: BMC will invest squarely in sales force automation and training to continue on to the next phase of sales team development.

Strategic Outlook• The TBR outlook for BMC is

expected to remain negative for several quarters while BMC works with its sales team and better defines its distribution and product strategies. • BMC faces challenges from

Microsoft, IBM, Oracle, HP, CA Technologies, Dell and upstarts including ServiceNow. • However, BMC holds substantial

intellectual property that, if positioned and marketed effectively, we believe will improve the company’s results and competitive standing.

Robust distribution and concise product strategies are needed to address anticipated performance lags from BMC

9.0%

10.8%

1.5% 0.4% 0.4% 0.7%

5.0% 6.1%7.5%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$3,000,000

2Q11 3Q11 4Q11 1Q12 2Q12 Est.3Q12

2010 2011 2012Est.

In $

Tho

usan

ds

BMC NET REVENUE, GROWTH AND PROJECTIONS

Revenue Revenue Growth Year-to-Year

Net

Rev

enue

Gro

wth

Yea

r-to

-Yea

r

TBR

SOURCE: TBR AND BMC

SBQ Vendor Profiles: BMC Software

TBR

11 TBR Quarterly Webinar Series | 9.26.12 | www.tbri.com | ©2012 Technology Business Research Inc.

Highlights from TBR’s Assessment of Microsoft’s Two-year Strategic OutlookKey TakeawaysFinancial: Leverage product updates to restore positive growth in core businesses.Go to Market: Integrate mobile and cloud capabilities to capitalize on the growing markets through core solutions.Resource: Invest in acquisitions to complement core portfolio capabilities.

Strategic Outlook• Microsoft’s 2Q12 financial results reflect the

maturation of major products in the market, with top-line revenue rising 4% and Windows revenue dropping 12.6% from 2Q11. • For Microsoft, 2012 is becoming a year in

which the company is positioning itself for long-term growth in its core PC base and the emerging cloud and mobility markets. • Through the remainder of 2012, the launch of

Windows 8 and the new version of Office will continue to position Microsoft to capture future revenue growth outside of its core PC customer base. • Microsoft’s 2Q12 Yammer acquisition will

position Microsoft to better combat cloud competitors (e.g., Google, Salesforce.com) with collaboration functionality that can be added to core portfolio products.

Microsoft is writing the script in 2012 for its long-term growth in the cloud and mobility markets

8.3%

7.3%

4.7%

6.0%

4.0%

2.5%

13.6%

7.5% 7.5%

0.0%1.0%2.0%3.0%4.0%5.0%6.0%7.0%8.0%9.0%

$0$10$20$30$40$50$60$70$80$90

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12Est.

CY11 CY12Est.

In $

Bill

ions

MICROSOFT NET REVENUE, GROWTH AND PROJECTIONS

Net Revenue Revenue Growth Year-to-Year

Net

Rev

enue

Gro

wth

Yea

r-to

-yea

r TBR

SOURCE: TBR AND MICROSOFT

SBQ Vendor Profiles: Microsoft

TBR

12 TBR Quarterly Webinar Series | 9.26.12 | www.tbri.com | ©2012 Technology Business Research Inc.

Executives’ disruptive vision will shape Red Hat’s near-term prospects — but the risk rises if competitors, rather than markets, are the targetHighlights from TBR’s Assessment of Red Hat’s Two-year Strategic OutlookKey Takeaways Strategic AssessmentFinancial: Focus on rapid monetization of headcount, infrastructure and ecosystem investments.Go to Market: Balance aggressive direct sales growth with alliance opportunities, incenting all to execute as a team.Resource Allocation: Expand the company’s storage business end to end while growing its support infrastructure to address a growing install base.

• Red Hat will grow its customer base and accelerate revenue growth with an integrated product strategy, but winning mindshare in the C-suite without leaving behind longstanding relationships with IT will demand investment and strategic sales growth.• With products tied to an addressable market

expansion strategy relying on virtualization, storage and cloud, Red Hat’s portfolio is well aligned with customer purchasing needs in its install base and across market segments.• Red Hat may see competitive challenges from

vendors such as Microsoft and Oracle when elevating its discussion from IT to the C-Suite. Competitors can entrench install bases by ensuring IT and executives alike see the value in existing relationships.

SBQ Vendor Profiles: Red Hat

TBR

13 TBR Quarterly Webinar Series | 9.26.12 | www.tbri.com | ©2012 Technology Business Research Inc.

Highlights from TBR’s Assessment of VMware’s Two-year Strategic OutlookKey Takeaways Strategic AssessmentFinancial: Ongoing investments will extend VMware’s reach but erode margin through the end of 2012.Go to Market: Reinforce portfolio strengths and cloud commitments while improving end-to-end performance.Resource Allocation: Attention will shift to cost management, positioning VMware to improve margins in CY13.

• TBR believes that 2013 will be a critical growth year for VMware — with Gelsinger as CEO along with products and personnel aligned to deliver growth. We see VMware ready with products designed to combat headwinds as the company challenges Microsoft and IBM in systems management.• The addition of Pat Gelsinger to VMware’s

leadership team as CEO adds end-to-end solutions expertise to the substantial technology expertise already in house — most notably that of Dr. Steve Herrod, CTO and senior vice president of R&D.• We believe Gelsinger will be asked not only

to continue VMware’s cloud-computing reinvention but also to establish himself as a trusted advisor to VMware’s core server virtualization install base.

VMware will balance its portfolio and corporate expansion to realize long-term growth without complicating its go-to-market execution

36.7%31.9%

26.9% 25.1%21.9% 20.0%

41.2%

31.8%12.0%

0%

10%

20%

30%

40%

50%

$0

$1,000

$2,000

$3,000

$4,000

$5,000

2Q11 3Q11 4Q11 1Q12 2Q12 3Q12Est.

CY10 CY11 CY12Est.

In $

Mill

ions

VMWARE NET REVENUE, GROWTH AND PROJECTIONS

Revenue Revenue Growth

Net

Rev

enue

Gro

wth

Yea

r-to

-yea

r

SOURCE: VMWARE AND TBRNOTE: Annual revenue and projections are for CY 2010, 2011 and 2012,

TBR

SBQ Vendor Profiles: VMware

TBR

14 TBR Quarterly Webinar Series | 9.26.12 | www.tbri.com | ©2012 Technology Business Research Inc.

Go to Market (GTM): Target new partnerships and acquisitions to rapidly expand GTM routes.

Corporate Reinvention: Invest in areas needed to drive CY13 success in product and GTM.

With cloud and mobility continuing to transform software consumption, enterprise software vendors are “holding the line” with three key tactics

SBQ 2Q12 Research Highlights and 2012 Outlook

Software Vendor Trends for 2012

Product Portfolio: Expand capabilities, attaching to high-interest trends and satisfying the install base.

SOURCE: TBR RESEARCH AND ESTIMATES; COMPANY DATA AND ESTIMATES

TBR

15 TBR Quarterly Webinar Series | 9.26.12 | www.tbri.com | ©2012 Technology Business Research Inc.

High-growth markets and high-interest trends are evolving customers’ preferred methods and routes of delivery.Leading vendors are making alliances, acquisitions and investments designed to evolve go-to-market strategies in order to stay ahead of customers — the second best practice TBR noted in 2Q12.

Software Vendor Trends for 2012 — Go to Market

To keep up with customers’ evolving purchasing needs, vendors are expanding go-to-market reach and efficiency with new investments

SBQ 2Q12 Research Highlights and 2012 Outlook

SOURCE: TBR RESEARCH AND ESTIMATES; COMPANY DATA AND ESTIMATES

TBR

16 TBR Quarterly Webinar Series | 9.26.12 | www.tbri.com | ©2012 Technology Business Research Inc.

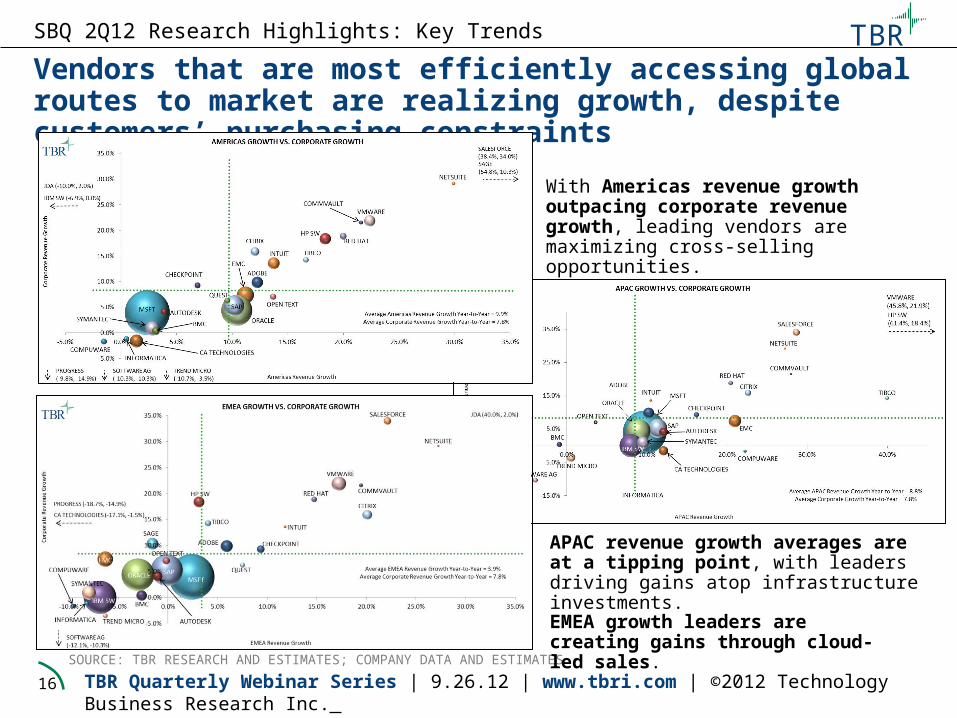

Vendors that are most efficiently accessing global routes to market are realizing growth, despite customers’ purchasing constraints

SBQ 2Q12 Research Highlights: Key Trends

SOURCE: TBR RESEARCH AND ESTIMATES; COMPANY DATA AND ESTIMATES

With Americas revenue growth outpacing corporate revenue growth, leading vendors are maximizing cross-selling opportunities.

APAC revenue growth averages are at a tipping point, with leaders driving gains atop infrastructure investments.

EMEA growth leaders are creating gains through cloud-led sales.

TBR

17 TBR Quarterly Webinar Series | 9.26.12 | www.tbri.com | ©2012 Technology Business Research Inc.

CA Technologies:CA Technologies established a development/ innovation center in Tel Aviv, Israel, and is expanding channel partners for ARCserve in India, supporting high-growth opportunities in cloud, security and big data.Oracle:With a diverse portfolio, a newly unified cloud story and an expanded sales force and partner network, Oracle will drive cross-segment increases, provided direct sales and indirect sales can coexist without cannibalizing near-term opportunities. SAP:SAP is successfully juggling new segments (cloud, mobility, databases), geographies (with record performance in growth markets, including Latin America and expanding investments in China and Russia) and expanded alliances (such as Accenture’s support of SAP HANA and mobility) to realize its lengthy list of 2015 growth objectives.

Investments in global centers of innovation and go-to-market alliances are driving vendors’ competitive advantages in core and new markets

SBQ 2012 Research Outlook: Go-To-Market

Highlighted Vendor Best Practices — 2Q12 SBQ Vendor Reports

SOURCE: TBR RESEARCH AND ESTIMATES; COMPANY DATA AND ESTIMATES

TBR

18 TBR Quarterly Webinar Series | 9.26.12 | www.tbri.com | ©2012 Technology Business Research Inc.

Highlights from TBR’s Assessment of CA Technologies’ Two-year Strategic OutlookKey TakeawaysFinancial: Return to positive revenue growth will be slow as field adjustments are made to address account instability. Go to Market: Channel partner recruitment and support programs are a significant change in distribution strategyResource: R&D investments will support cloud and mainframe developments while other resource areas remain flat.

Strategic Outlook• CA Technologies’ strategy is threefold:

maximize value and distribution of profitable mainframe offerings; nurture and expand the distribution channel; and focus innovation efforts internally on integration and cloud with the goal of helping customers with private and hybrid cloud initiatives. • TBR does not see CA Technologies making

smaller-sized acquisitions around its cloud portfolio in coming quarters, as its cloud-based, acquired technologies grew only 1% year-to-year. • Mainframe margins and prospect acquisition

are critical to CA Technologies’ financial success. CA will continue to make mainframe solutions more available in the market and may acquire niche mainframe vendors.

R&D investments will modestly increase as CA Technologies works to integrate its growing cloud portfolio

6.6%

10.3% 10.4%

5.3%

-1.5%1.4%

3.4%

7.4% 6.7%

-3%

0%

3%

6%

9%

12%

$0$500

$1,000$1,500$2,000$2,500$3,000$3,500$4,000$4,500$5,000$5,500

2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 Est. CY10 CY11 CY12Est.

In $

Mill

ions

CA TECHNOLOGIES NET REVENUE, GROWTH AND PROJECTIONS

Revenue Revenue Growth Year-to-year

Net

Rev

enue

Gro

wth

Yea

r-to

-yea

r

NOTE: Annual revenue and projections are for calendar 2009, 2010 , 2011, and 2012 respectively.SOURCE: CA TECHNOLOGIES AND TBR

TBR

SBQ Vendor Profiles: CA Technologies

TBR

19 TBR Quarterly Webinar Series | 9.26.12 | www.tbri.com | ©2012 Technology Business Research Inc.

Realizing Oracle executives’ FY2013 growth vision will require unified go-to-market strategy and execution spanning all business linesHighlights from TBR’s Assessment of Oracle’s Two-year Strategic Outlook

Key Takeaways Strategic AssessmentFinancial: Continued attention to margins positions Oracle for cross-segment gainsGo to Market: Need for consistent go-to-market leadership and execution to ensure consistent performance Resources and Investments: Use acquisitions and a proven integration strategy to drive segment growth.

• For Oracle to realize CEO Larry Ellison’s ambition to challenge IBM in the high end, Oracle must develop the same market-making power IBM invests into its solutions-focused Smarter Planet initiatives, driven by investment and also by growth momentum from Oracle’s hardware business.• Oracle’s core strengths in applications remain

its primary growth drivers. • However, Oracle has positioned itself well for

near-term growth across business segments by developing a robust portfolio that complements core databases with high-margin, high-profile engineered systems and cloud solutions.

SBQ Vendor Profiles: Oracle

TBR

20 TBR Quarterly Webinar Series | 9.26.12 | www.tbri.com | ©2012 Technology Business Research Inc.

Highlights from TBR’s Assessment of SAP’s Two-year Strategic OutlookKey Takeaways Strategic OutlookFinancial: SAP will build revenue growth with its focus on sales execution.Go to Market: Recruit partners to HANA ecosystem, opening up new customer bases and opportunities for share growth.Resource Management: Cross-company investment stands to expand long-term reach but erode margin until early CY13.

• The scale of SAP’s addressable market ambitions could drive headwinds in 2013 as SAP continues to invest in disaggregating sales opportunities between direct and indirect teams.• SAP is engaged in a delicate balancing act —

growing direct sales capacity, expanding partner opportunities and simplifying customer deployments across its portfolio, reinforced by SAP’s ongoing investment in its partner ecosystem.• Competitors, including Oracle, Microsoft,

Infor and Epicor, should stay aware of SAP’s increasing channel focus, particularly the channel’s role in driving SAP HANA growth.

Long-term growth for SAP is contingent on consistent sales execution and monetizing investments designed to expand its reach

SAP’s reported currency of record is euros — TBR is working with IFRS results and has converted those results to U.S. dollars via average quarterly exchange rates — 2Q11: $1.44/€, 3Q11: $1.41/€, 4Q11:$1.35/ €, 1Q12: $1.31/€, 2Q12: $1.28/€, 3Q12: 1.28 /€ (Estimate)

SBQ Vendor Profiles: SAP AG

TBR

21 TBR Quarterly Webinar Series | 9.26.12 | www.tbri.com | ©2012 Technology Business Research Inc.

Go to Market (GTM): Target new partnerships and acquisitions to rapidly expand GTM routes.

Corporate Reinvention: Invest in areas needed to drive CY13 success in product and GTM.

With cloud and mobility continuing to transform software consumption, enterprise software vendors are “holding the line” with three key tactics

SBQ 2Q12 Research Highlights and 2012 Outlook

Software Vendor Trends for 2012

Product Portfolio: Expand capabilities, attaching to high-interest trends and satisfying the install base.

SOURCE: TBR RESEARCH AND ESTIMATES; COMPANY DATA AND ESTIMATES

TBR

22 TBR Quarterly Webinar Series | 9.26.12 | www.tbri.com | ©2012 Technology Business Research Inc.

With industrywide growth rates showing continued signs of being slowed by macroeconomic conditions, vendors are challenged to invest for long-term growth without eroding near-term performance — the third best practice TBR noted in 2Q12.

With product and go-to-market investments as part of the picture, vendors are evolving processes and strategies to set up for long-term growth

SBQ 2Q12 Research Highlights and 2012 Outlook

Software Vendor Trends for 2012 — Corporate Reinvention

SOURCE: TBR RESEARCH AND ESTIMATES; COMPANY DATA AND ESTIMATES

TBR

23 TBR Quarterly Webinar Series | 9.26.12 | www.tbri.com | ©2012 Technology Business Research Inc.

Average operating margin for vendors across TBR’s Software Vendor Benchmark was 17.7%, declining nearly 8% from 2Q11.

Sustaining market positions against disruptive entrants is driving industry leaders to accelerate investments, balanced against current margins

SBQ 2Q12 Research Highlights: Key Trends

SOURCE: TBR RESEARCH AND ESTIMATES; COMPANY DATA AND ESTIMATES

TBR

24 TBR Quarterly Webinar Series | 9.26.12 | www.tbri.com | ©2012 Technology Business Research Inc.

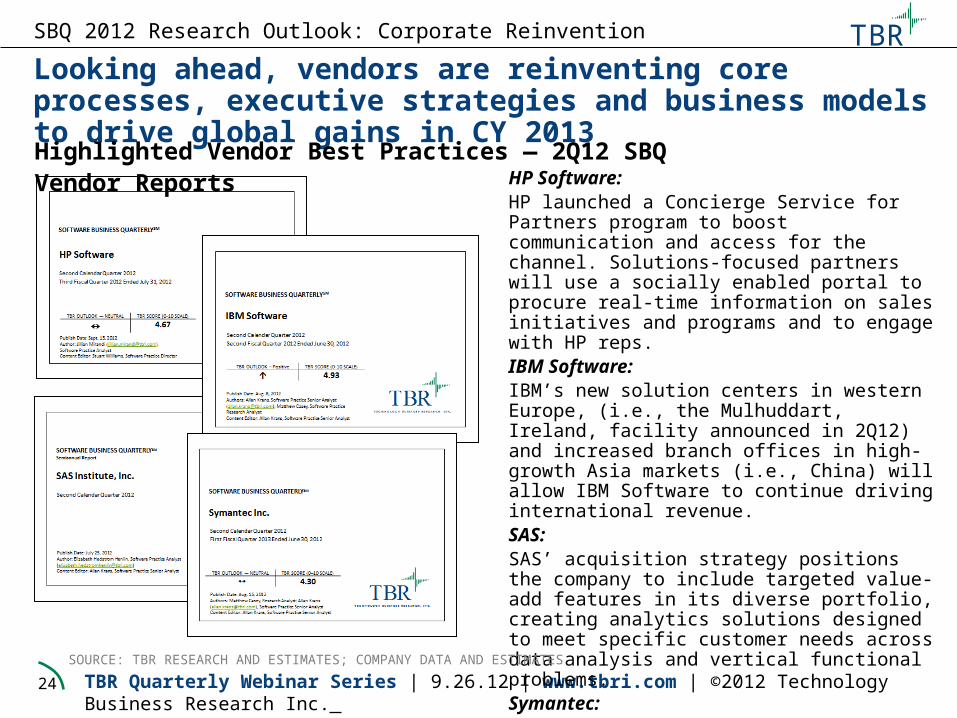

Looking ahead, vendors are reinventing core processes, executive strategies and business models to drive global gains in CY 2013

SBQ 2012 Research Outlook: Corporate Reinvention

HP Software:HP launched a Concierge Service for Partners program to boost communication and access for the channel. Solutions-focused partners will use a socially enabled portal to procure real-time information on sales initiatives and programs and to engage with HP reps. IBM Software:IBM’s new solution centers in western Europe, (i.e., the Mulhuddart, Ireland, facility announced in 2Q12) and increased branch offices in high-growth Asia markets (i.e., China) will allow IBM Software to continue driving international revenue. SAS:SAS’ acquisition strategy positions the company to include targeted value-add features in its diverse portfolio, creating analytics solutions designed to meet specific customer needs across data analysis and vertical functional problems.Symantec:Highlighted by the 2Q12 divestiture of AdvisorSquare and its 4Q11 divesture of its stake in Huawei-Symantec, Symantec is realigning its portfolio to drive revenue within its core businesses.

Highlighted Vendor Best Practices — 2Q12 SBQ Vendor Reports

SOURCE: TBR RESEARCH AND ESTIMATES; COMPANY DATA AND ESTIMATES

TBR

25 TBR Quarterly Webinar Series | 9.26.12 | www.tbri.com | ©2012 Technology Business Research Inc.

Highlights from TBR’s Assessment of HP Software’s Two-year Strategic OutlookKey TakeawaysFinancial: Layer software across other HP segments to help unify the company, improve customer perception of HP as a solutions vendor and increase profits.Go to Market: Expand partnerships across segments to accelerate customer acquisition.Resource: Tightly manage staffing while leadership is adjusted to improve execution.

Strategic Outlook•Companywide, HP Software has the highest operating margin (18% in 2Q12) and expanding software sales across the business will increase overall profits.•HP Software has an ambitious goal of driving 40% (up from an est. 25%) of its sales through partners in 2012 — a target TBR believes will not be within reach until 2013 due to changes in channel management and the time required to mature its channel programs. •HP Software faces many challenges, including improving core revenue streams to make up for Autonomy’s lost impact, addressing the hardware barrier to business-solution technology sales and maintaining positive momentum while HP undergoes long-term restructuring.

HP Software will leverage channel-based business solution sales to address challenges and improve its revenue opportunities

19.5%

28.8%

30.5%

21.7%

18.4%

10.0% 8.7% 5.0%10.0%

0%5%10%15%20%25%30%35%

$0$500

$1,000$1,500$2,000$2,500$3,000$3,500$4,000$4,500

2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 Est. 2010 2011 2012 Est.

In $

Tho

usan

ds

HP SOFTWARE NET REVENUE, PROFITABILITY, GROWTH AND PROJECTIONS

Total Revenue Operating Income Revenue Growth

Net

Rev

enue

Gro

wth

Yea

r-to-

Yea

r

NOTE: Annual revenue and projections are for calendar 2009, 2010 ,2011,and 2012 respectively.SOURCE: HP SW AND TBR

TBR

SBQ Vendor Profiles: HP Software

TBR

26 TBR Quarterly Webinar Series | 9.26.12 | www.tbri.com | ©2012 Technology Business Research Inc.

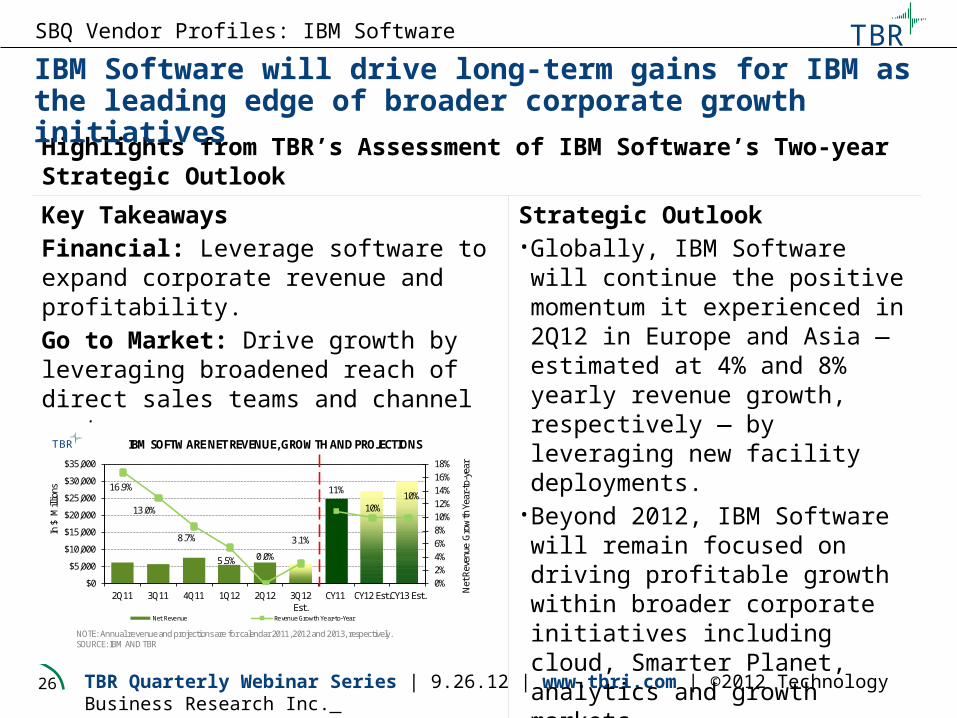

Highlights from TBR’s Assessment of IBM Software’s Two-year Strategic OutlookKey TakeawaysFinancial: Leverage software to expand corporate revenue and profitability.Go to Market: Drive growth by leveraging broadened reach of direct sales teams and channel partners.Resource: Accelerate global revenue gains by expanding physical presence through facility deployment in high-growth regions.

Strategic Outlook• Globally, IBM Software will continue

the positive momentum it experienced in 2Q12 in Europe and Asia — estimated at 4% and 8% yearly revenue growth, respectively — by leveraging new facility deployments. • Beyond 2012, IBM Software will

remain focused on driving profitable growth within broader corporate initiatives including cloud, Smarter Planet, analytics and growth markets. • In addition to geographic expansion,

IBM Software will remain focused on extending its core capabilities to capitalize on the growing cloud and mobility markets.

IBM Software will drive long-term gains for IBM as the leading edge of broader corporate growth initiatives

SBQ Vendor Profiles: IBM Software

16.9%

13.0%

8.7%

5.5% 0.0%

3.1%

11%

10%10%

0%2%4%6%8%10%12%14%16%18%

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

2Q11 3Q11 4Q11 1Q12 2Q12 3Q12Est.

CY11 CY12 Est.CY13 Est.

In $

Mill

ions

IBM SOFTWARE NET REVENUE, GROWTH AND PROJECTIONS

Net Reve nue Re venue Growth Ye ar-to-Year

Net

Rev

enue

Gro

wth

Yea

r-to

-yea

r

NOTE: Annual revenue and projections are for calendar 2011, 2012 and 2013, respectively.SOURCE: IBM AND TBR

TBR

TBR

27 TBR Quarterly Webinar Series | 9.26.12 | www.tbri.com | ©2012 Technology Business Research Inc.

Highlights from TBR’s Assessment of SAS’ Two-year Strategic OutlookKey Takeaways Strategic OutlookFinancial: Though SAS is privately held, annual reports show accelerating year-to-year total revenue growth (reaching 12% between 2010 and 2011).Go to Market: SAS’ technology focus fuels a go-to-market strategy that appeals to customers across the purchasing spectrum.Resource: Investments will keep SAS close to customers as enterprise vendors acquire their way into the analytics segment.

• SAS' focus on products, customers and investments help SAS remain at the leading edge of analytics and will ensure accelerating revenue growth into CY 2013.• Broad-based economic trends and analytics

customers’ purchasing behavior position SAS for near- and long-term revenue growth within its core businesses.• SAS has the segment advantage of a long-

time first mover, amplified by its depth of portfolio and corporate flexibility and influenced by its privately held status.• SAS’ analytics focus and track record lend

additional credibility as laggard industries consider analytics, and SAS is realizing resultant growth.

SAS’ stable leadership, long-term strategy and technology-led, go-to-market strategy will drive revenue growth atop expanding analytics purchasing

SOURCE: TBR BI & ANALYTICS PURCHASING BEHAVIOR AND MATURITY STUDY

SBQ Vendor Profiles: SAS

TBR

28 TBR Quarterly Webinar Series | 9.26.12 | www.tbri.com | ©2012 Technology Business Research Inc.

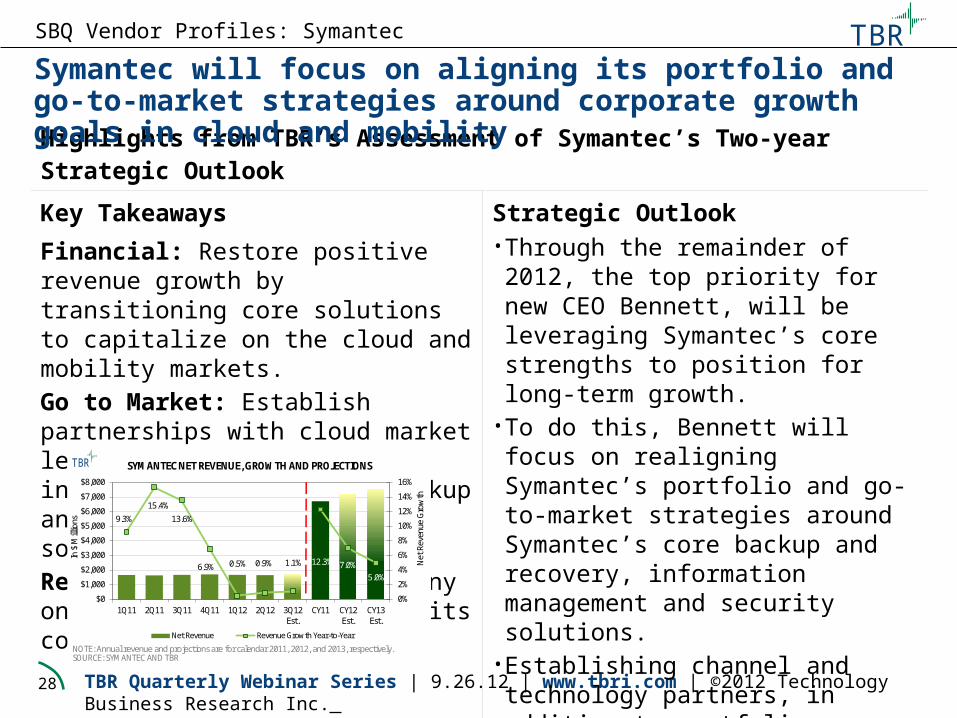

Highlights from TBR’s Assessment of Symantec’s Two-year Strategic OutlookKey TakeawaysFinancial: Restore positive revenue growth by transitioning core solutions to capitalize on the cloud and mobility markets.Go to Market: Establish partnerships with cloud market leaders to extend core information management, backup and recovery, and security solutions.Resource: Refocus the company on long-term growth within its core brands.

Strategic Outlook• Through the remainder of 2012, the top

priority for new CEO Bennett, will be leveraging Symantec’s core strengths to position for long-term growth. • To do this, Bennett will focus on realigning

Symantec’s portfolio and go-to-market strategies around Symantec’s core backup and recovery, information management and security solutions. • Establishing channel and technology

partners, in addition to portfolio realignment, will enable Symantec to extend the presence of core solutions. • A cloud partnership with Microsoft in

2Q12 positions the company to extend the presence of its disaster recovery solutions to Microsoft Azure customers.

Symantec will focus on aligning its portfolio and go-to-market strategies around corporate growth goals in cloud and mobility

9.3%

15.4%

13.6%

6.9% 0.5% 0.9% 1.1% 12.3% 7.0%5.0%

0%

2%

4%

6%

8%

10%

12%

14%

16%

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12Est.

CY11 CY12Est.

CY13Est.

In $

Mill

ions

SYMANTEC NET REVENUE, GROWTH AND PROJECTIONS

Net Revenue Revenue Growth Year-to-Year

Net

Rev

enue

Gro

wth

NOTE: Annual revenue and projections are for calendar 2011, 2012, and 2013, respectively.SOURCE: SYMANTEC AND TBR

TBR

SBQ Vendor Profiles: Symantec

TBR

29 TBR Quarterly Webinar Series | 9.26.12 | www.tbri.com | ©2012 Technology Business Research Inc.

Go to Market (GTM): Target new partnerships and acquisitions to rapidly expand GTM routes.

Corporate Reinvention: Invest in areas needed to drive CY13 success in product and GTM.

The balance of CY12 promises incremental spending growth across the enterprise landscape, with SBQ vendors in a position to drive revenue gains

SBQ 2Q12 Research Highlights and 2012 Outlook

Software Vendor Trends for 2012

Product Portfolio: Expand capabilities, attaching to high-interest trends and satisfying the install base.

SOURCE: TBR RESEARCH AND ESTIMATES; COMPANY DATA AND ESTIMATES

TBR

30 TBR Quarterly Webinar Series | 9.26.12 | www.tbri.com | ©2012 Technology Business Research Inc.

SBQ 2012 Research Outlook – 3Q12 Research Highlights

SBQ 2Q12 Research Highlights and 2012 Outlook

TBR

31 TBR Quarterly Webinar Series | 9.26.12 | www.tbri.com | ©2012 Technology Business Research Inc.

SP Research Current Topics 3Q12 Report Key Themes• SourceIT — Software

Purchasing, by Industry and Buyer

• Vendor Reports:o Oracleo SAP AGo IBM Softwareo HP Softwareo Microsofto BMC Softwareo CA Technologieso VMwareo Symanteco Red Hato SAS

• Vendor Benchmark• Software CSAT

Where are vendors investing to drive revenue growth across applications and technology business segments?

How are vendors reinventing core value propositions to increase partnering appeal?

Where are vendors allocating investments to ensure attachment to customers’ leading edge business intelligence and analytics needs?

• Where are the leading edge opportunities for

vendors to take share within verticals?• How do those opportunities and buyers vary

when viewed by industry?

How are vendors evolving core product portfolios to entrench install base loyalty while taking share in high growth segments, such as mobility and cloud computing?High-Growth

Segments

Systems Management

BI & Analytics

Industries & Verticals

Enterprise Software

NOTE: THE CLOUD BUSINESS QUARTERLY AND TBR’S SOFTWARE PRACTICE CLOUD RESEARCH WILL BE COVERED WITHIN THE CLOUD BUSINESS QUARTERLY RESEARCH HIGHLIGHTS AND OUTLOOK WEBINAR.

Vendors that can package portfolio offerings to answer the spectrum of customer needs, from niche product to solutions, will see growth in 2012

SBQ 2012 Research Outlook: 3Q12 Research Highlights

SOURCE: TBR RESEARCH AND ESTIMATES; COMPANY DATA AND ESTIMATES

TBR

32 TBR Quarterly Webinar Series | 9.26.12 | www.tbri.com | ©2012 Technology Business Research Inc.

Questions?

SBQ 2Q12 Research Highlights and 2012 Outlook

TBR

33 TBR Quarterly Webinar Series | 9.26.12 | www.tbri.com | ©2012 Technology Business Research Inc.

For further information, please contact:

Stuart Williams James McIlroyDirector, Software Practice Vice President, [email protected] [email protected]

TBR

TECHNOLOGY BUSINESS RESEARCH, INC.

About TBR

Technology Business Research (TBR) is a leading independent technology market research and consulting firm specializing in the business and financial analyses of hardware, software, networking equipment, wireless, portal and professional services vendors.

Serving a global clientele, TBR provides timely and accurate market research and business intelligence in formats that are tailored to clients’ needs. Our analysts are available to further address client-specific issues or information needs on an inquiry or proprietary consulting basis.

TBR has been empowering corporate decision makers since 1996.

To learn how our analysts can address your unique business needs, please visit our website or contact us today.

Contact Us

[email protected] Merrill DriveHampton, NH 03842USA

This report is based on information made available to the public by the vendor and other public sources. No representation is made that this information is accurate or complete. Technology Business Research will not be held liable or responsible for any decisions that are made based on this information. The information contained in this report and all other TBR products is not and should not be construed to be investment advice. TBR does not make any recommendations or provide any advice regarding the value, purchase, sale or retention of securities. This report is copyright-protected and supplied for the sole use of the recipient. Contact Technology Business Research, Inc. for permission to reproduce.