technology and strategy - skynet blogsstatic.skynetblogs.be/media/180303/692314324.pdf · practices...

TRANSCRIPT

Technology and Strategy

GEST-S-464

Pr Manuel Hensmans

Deadline

• Please hand in the case-study

– both an electronic and paper version

– by Tue May 22 at 12am

• My mailbox is on the 4th floor (« salle de détente CEB »)

2 |

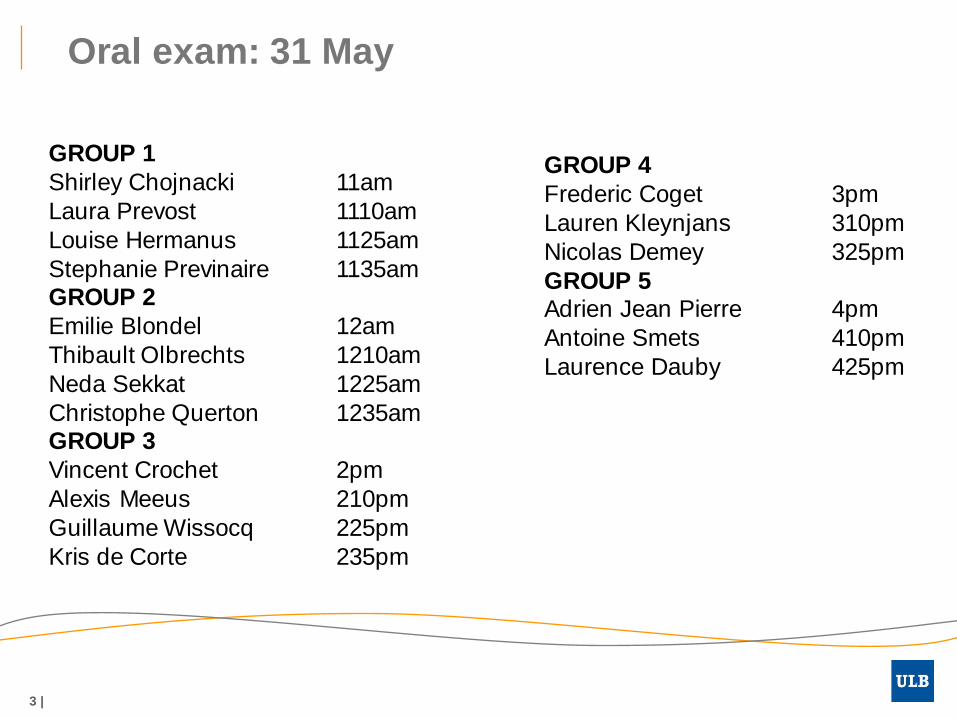

Oral exam: 31 May

3 |

GROUP 1

Shirley Chojnacki 11am

Laura Prevost 1110am

Louise Hermanus 1125am

Stephanie Previnaire 1135am GROUP 2

Emilie Blondel 12am

Thibault Olbrechts 1210am

Neda Sekkat 1225am

Christophe Querton 1235am GROUP 3

Vincent Crochet 2pm

Alexis Meeus 210pm

Guillaume Wissocq 225pm

Kris de Corte 235pm

GROUP 4

Frederic Coget 3pm

Lauren Kleynjans 310pm

Nicolas Demey 325pm

GROUP 5 Adrien Jean Pierre 4pm

Antoine Smets 410pm

Laurence Dauby 425pm

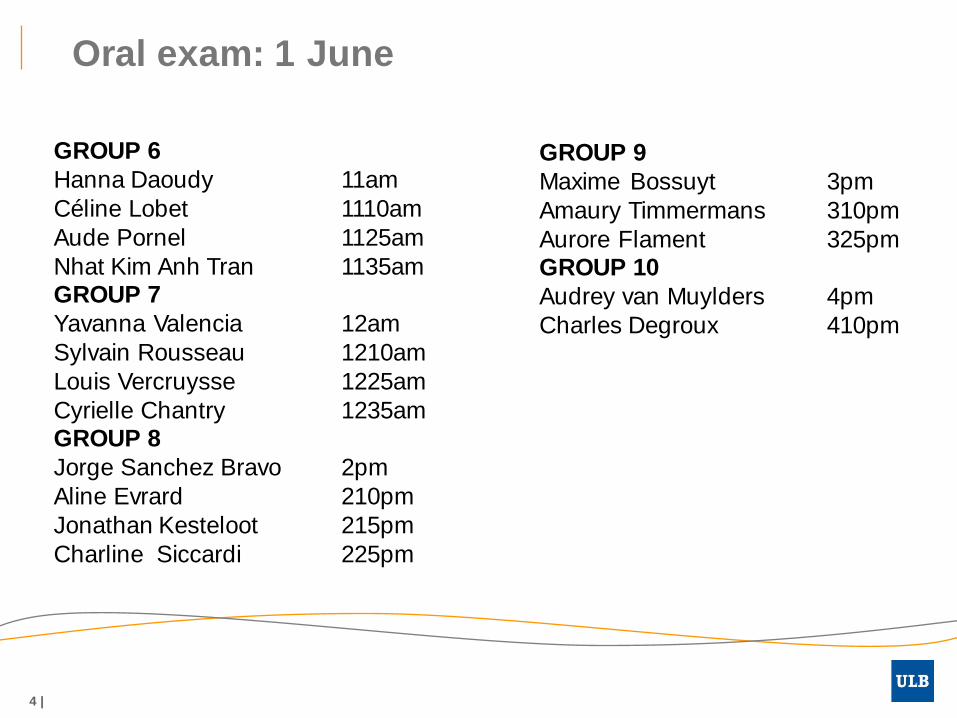

Oral exam: 1 June

4 |

GROUP 6

Hanna Daoudy 11am

Céline Lobet 1110am

Aude Pornel 1125am

Nhat Kim Anh Tran 1135am GROUP 7

Yavanna Valencia 12am

Sylvain Rousseau 1210am

Louis Vercruysse 1225am

Cyrielle Chantry 1235am GROUP 8

Jorge Sanchez Bravo 2pm

Aline Evrard 210pm

Jonathan Kesteloot 215pm

Charline Siccardi 225pm

GROUP 9

Maxime Bossuyt 3pm

Amaury Timmermans 310pm

Aurore Flament 325pm GROUP 10

Audrey van Muylders 4pm

Charles Degroux 410pm

Last class

• Setting a strategic direction for the future

– Analyse present resources and competences

• Apply VRIN framework

– Valuable

– Rare

– Inimitable

– Non-substitutable

– SWOT

• Internal & external analysis

– TOWS

• Generate future options

5

Last class: create vision for the future

8 Steps (pharmaceutical industry)

• PESTEL analysis (10-20 years)

• Scenario analysis

• Strategic customer

• Key success factors

• Strategic groups and strategic capabilities

• Mobility barriers

• Vision

• Acquire, ally or develop internally?

6

7

Significant innovation

Strategic groups & growth potential Less / More

8

Justification

premium pricing

Generic

Biotech

Conventional

Vaccines

OTC

Bio-

similar

Significant innovation (lmore targeted, harder to imitate,

but slower throughput)

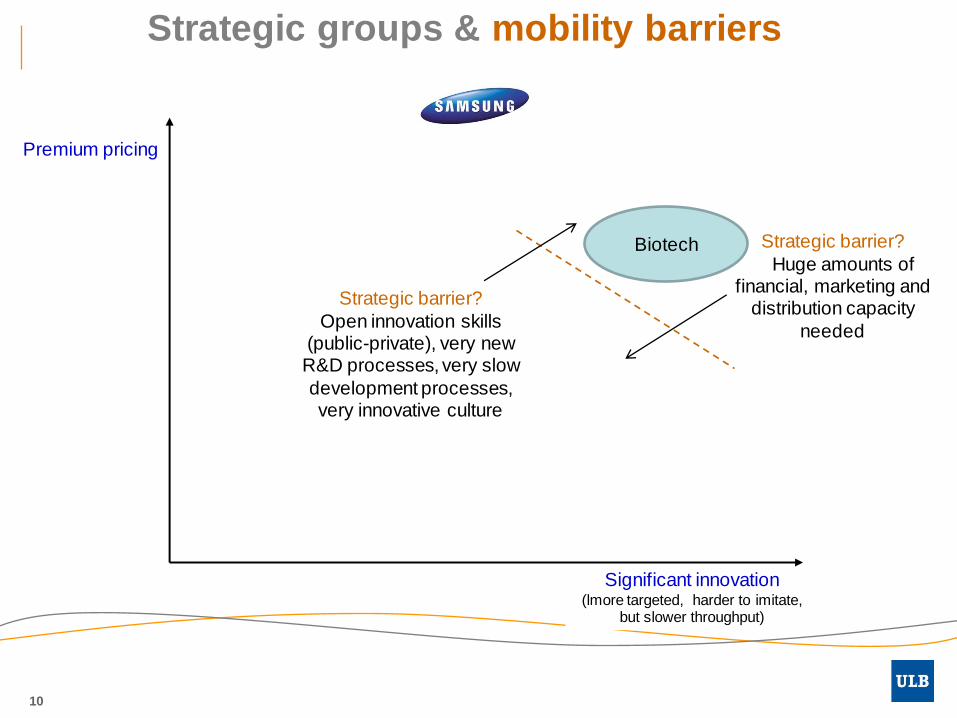

Strategic groups & mobility barriers

9

Premium pricing

Bio-

similar

Strategic barrier?

For generic players: Substantial R&D

investment, competitive

advantage is manufacturing excellence

Strategic barrier?

For conventionals: Time-to-market skills needed; very different

non-proprietary culture; more about

manufacturing than sales or innovation

Significant innovation (lmore targeted, harder to imitate,

but slower throughput)

Strategic groups & mobility barriers

10

Premium pricing

Strategic barrier?

Open innovation skills (public-private), very new R&D processes, very slow

development processes, very innovative culture

Strategic barrier?

Huge amounts of financial, marketing and

distribution capacity

needed

Biotech

11

Partial Vision

Global Vision & Mission

• Vision (desired future state)

– Transform from a leading « infotainment » to a leading « lifecare »

company

• Mission (purpose: what business are we in and why?)

– Develop and commercialise high-quality, low-cost healthcare

products for more patients in the world

– Improve the world by providing poor countries and rural areas with

medical equipment and drugs they cannot afford

12

This class

• Choosing a strategic method to realise vision

– Develop internally / go solo

– Mergers & Acquisitions

– Alliances

• Strategic agility

adapt quickly to scenarios and realise vision

• Strategic sensitivity

– Pros & cons of planning

• Leadership quality

– Pros & cons of visionary leadership

• Resource fluidity

– Importance resource allocation rules to beat politics

13

Advantages of going solo? also called organic growth

• Knowledge and learning can be enhanced

– Focus & develop own strategic capability

• Spread investment over time – easier to finance.

• No availability constraints – no need to search for suitable

partners or acquisition targets.

• Strategic independence – less need to make compromises

or accept strategic constraints.

• Minimise disruption - slower rate of change to avoid

political & cultural acrimony of acquisitions / alliances

14 |

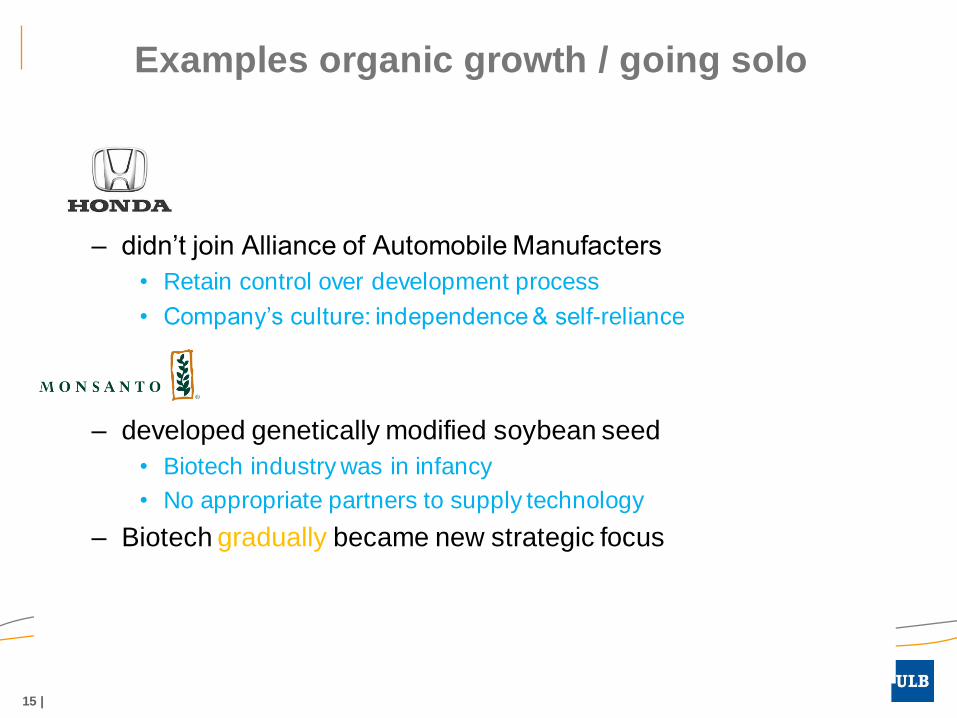

Examples organic growth / going solo

– didn’t join Alliance of Automobile Manufacters

• Retain control over development process

• Company’s culture: independence & self-reliance

– developed genetically modified soybean seed

• Biotech industry was in infancy

• No appropriate partners to supply technology

– Biotech gradually became new strategic focus

15 |

Disadvantages of going solo?

• Significant portion innovation comes from collaborative

efforts of multiple organizations / individuals outside firm

• Paradigm change?

– From “successful innovation requires control”

– To “open innovation” (Chesbrough, 2003)

16 |

Solution of

• Settle in leading foreign cluster (e.g. memory chips)

– Built R&D lab in (1983)

• Developed own DRAM technology in cluster

• Hired 300 experienced Korean engineers from

– Led development of 256K DRAM

– Trained many Korean engineers

• Built parallel unit in S-Korea to transfer technology

• « Incrementally improve on others’ ideas »

– Use huge capital investment

• to boost high-quality, low-cost manufacturing in rapidly growing niches

17 |

Not only in-house, also acquisitions & alliances

Vision Part II

18 |

Samsung chairman Lee Kun-Hee: “The majority of our products today will be gone in 10 years.

To survive, we have to open ourselves up to work with partners and even

make acquisitions”

Mergers and acquisitions

A merger is… the combination of two previously separate organisations, typically as more or less equal partners.

An acquisition involves… one firm taking over the ownership (‘equity’) of another, hence the alternative term ‘takeover’.

19

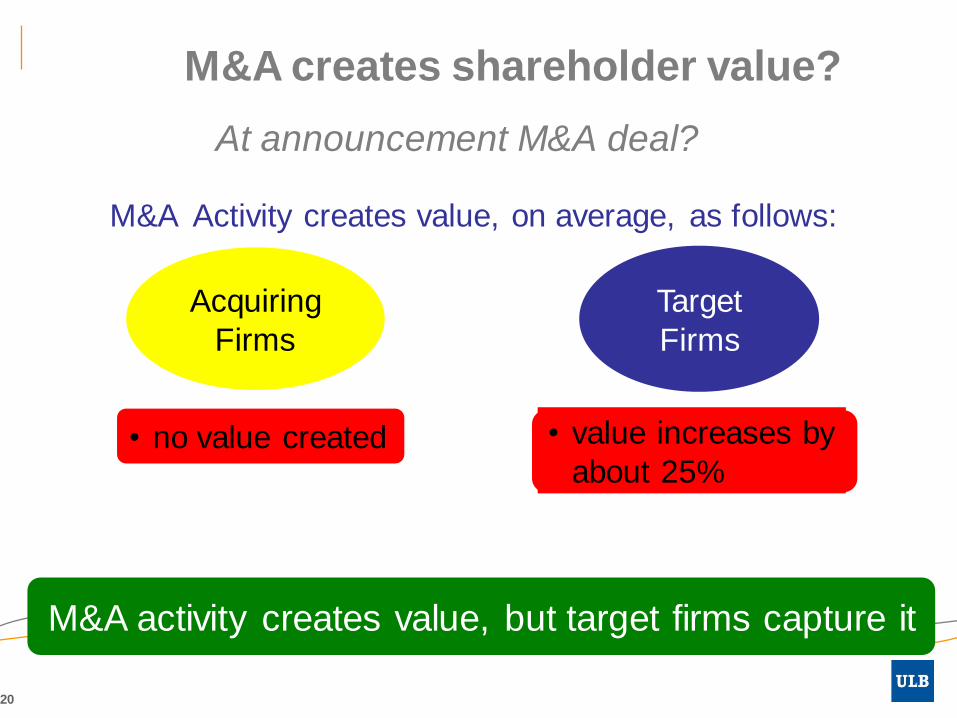

M&A creates shareholder value?

At announcement M&A deal?

Acquiring

Firms

Target

Firms

M&A Activity creates value, on average, as follows:

• no value created • value increases by

about 25%

M&A activity creates value, but target firms capture it

20

21

Long-term failure record acquisitions! 70% acquisitions end with failed strategic integration &

lower returns to shareholders of both organizations – due to

paying too much, lack of acquisition experience, poor

financial advice, over-optimism

M&A creates shareholder value?

Long-term?

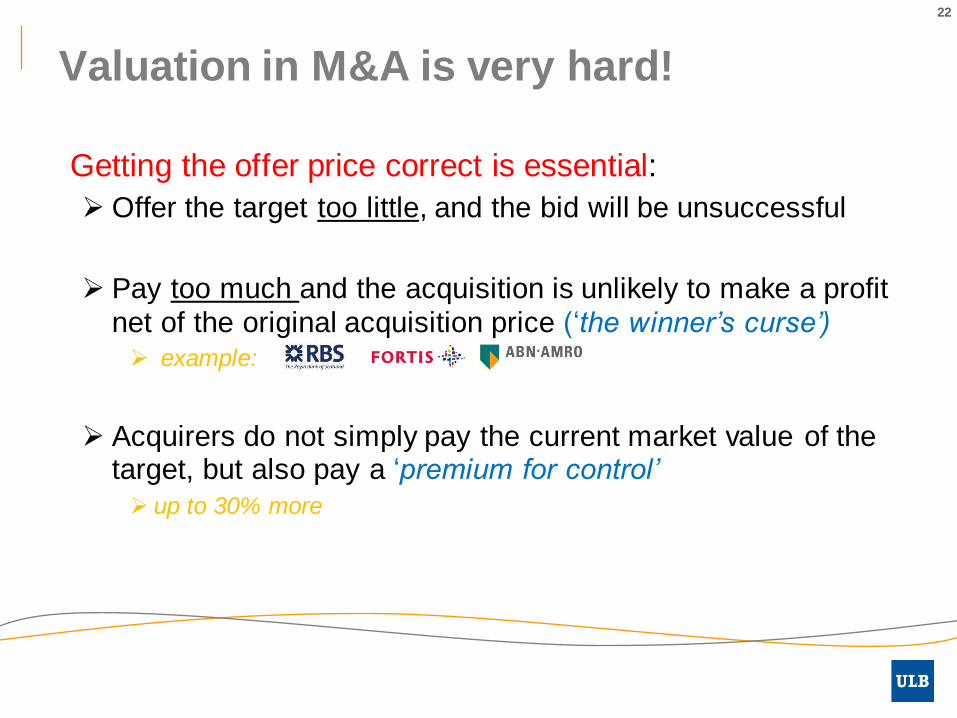

Valuation in M&A is very hard!

Getting the offer price correct is essential:

Offer the target too little, and the bid will be unsuccessful

Pay too much and the acquisition is unlikely to make a profit

net of the original acquisition price (‘the winner’s curse’)

example:

Acquirers do not simply pay the current market value of the target, but also pay a ‘premium for control’

up to 30% more

22

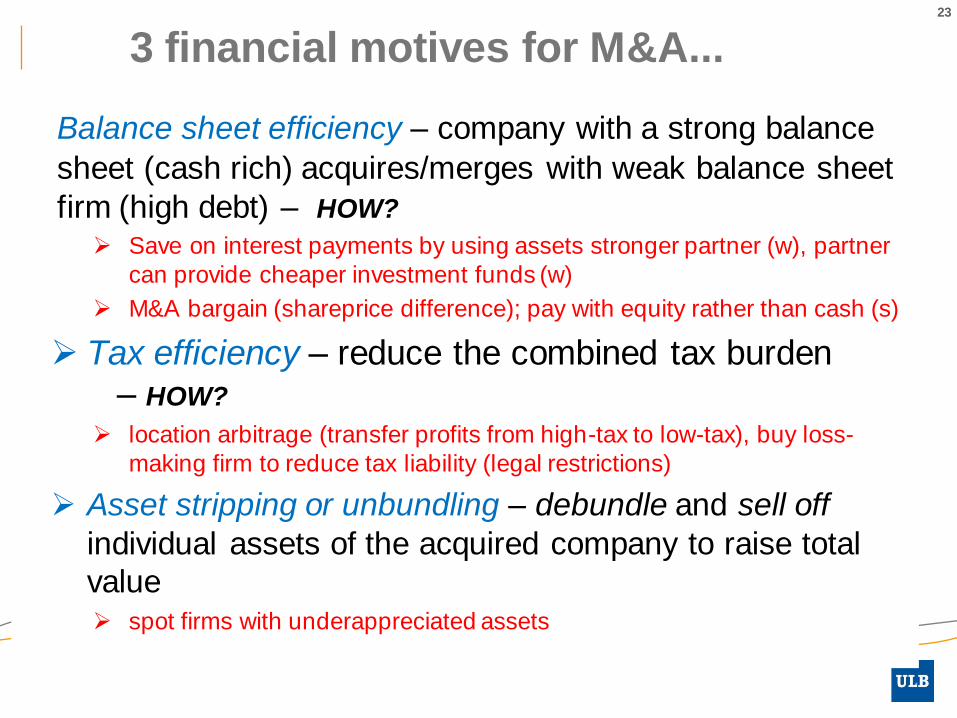

Balance sheet efficiency – company with a strong balance

sheet (cash rich) acquires/merges with weak balance sheet

firm (high debt) – HOW?

Save on interest payments by using assets stronger partner (w), partner

can provide cheaper investment funds (w)

M&A bargain (shareprice difference); pay with equity rather than cash (s)

Tax efficiency – reduce the combined tax burden – HOW?

location arbitrage (transfer profits from high-tax to low-tax), buy loss-

making firm to reduce tax liability (legal restrictions)

Asset stripping or unbundling – debundle and sell off

individual assets of the acquired company to raise total

value spot firms with underappreciated assets

3 financial motives for M&A... 23

3 Strategic motives for M&A...

Speedy extension – in terms of geography, products,

markets

Consolidation – increase market power, increase

efficiency, increase bargaining power with suppliers

Boost innovation capabilities –

acquire entrepreneurial companies as part of R&D effort...

often useful when industries are converging (Microsoft adaptation to

Internet and video games)

24

2 Managerial motives for M&A

M&A may serve managerial self-interest for two

reasons: Personal ambition – financial incentives tied to short-term growth

or share-price targets; boosting personal reputations; giving

friends and colleagues greater responsibility or better jobs.

Bandwagon effects – managers may be branded as conservative

if they don’t follow an M&A trend; the company may itself become

a takeover target.

25

Main reason for cyclical character M&A Waves of over-optimism and over-pessimism

2007: record €4.6bn

2009: down to €2.5bn

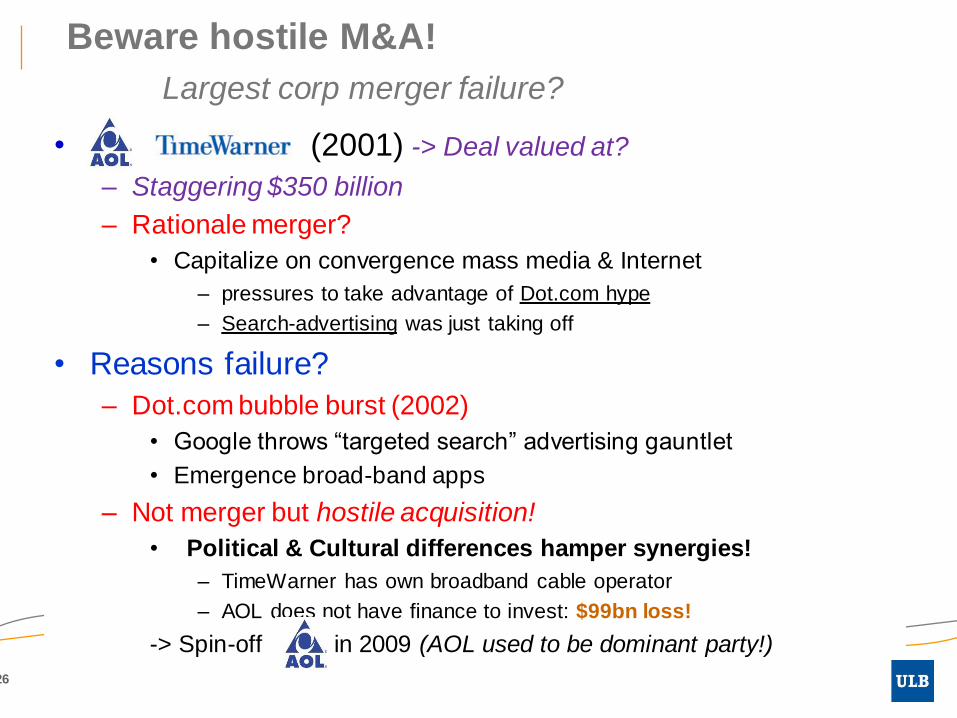

Beware hostile M&A!

Largest corp merger failure?

• (2001) -> Deal valued at?

– Staggering $350 billion

– Rationale merger?

• Capitalize on convergence mass media & Internet

– pressures to take advantage of Dot.com hype

– Search-advertising was just taking off

• Reasons failure?

– Dot.com bubble burst (2002)

• Google throws “targeted search” advertising gauntlet

• Emergence broad-band apps

– Not merger but hostile acquisition!

• Political & Cultural differences hamper synergies!

– TimeWarner has own broadband cable operator

– AOL does not have finance to invest: $99bn loss!

-> Spin-off in 2009 (AOL used to be dominant party!)

26

Target choice in M&A

Two main criteria apply:

• Strategic fit

– does the target firm strengthen or complement the acquiring firm’s

strategy? (N.B. It is easy to over-estimate this potential synergy).

• Organisational fit

– is there a match between the management practices, cultural

practices and staff characteristics of the target and the acquiring

firm?

27

Takeover by

• Strategic fit?

– Yes for Roche

• can strengthen weak innovation pipeline

• access to data on trials and experiments

• savings US headquarters expenses

– Doubtful for Genentech

• doesn’t need lots of additional investment capital

• Organizational fit?

– Swiss versus Californian

– Family firm versus entrepreneurial

– Biotech versus chemicals

• How can Roche ensure the success of its takeover?

– Roche’s ability to retain key personnel

28

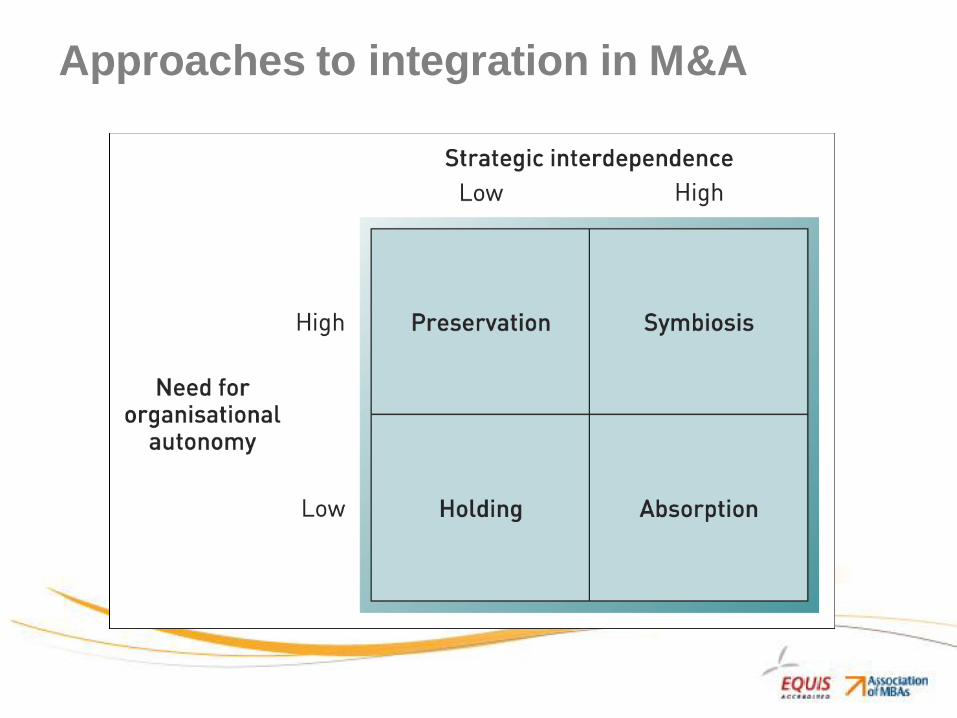

Approaches to integration in M&A

Approaches to Integration

Absorption – strong strategic interdependence and little need for organisational autonomy. Rapid adjustment of the acquired company’s strategies, culture and systems.

• Preservation – little interdependence and a high need for

autonomy. Old strategies, cultures and systems can be continued much as before.

• Symbiosis – strong strategic interdependence, but a high need for autonomy. Both the acquired firm and acquiring firm

learn and adopt the best qualities from each other.

• Holding – a residual category – with little to gain by

integration. The acquisition will be ‘held’ temporarily before being sold on, so the acquired unit is left largely alone.

• Ideal scenario in terms of synergies?

30

Strategic alliances

• A strategic alliance is where two or more organisations

share resources and activities to pursue a strategy.

Top 500 global companies each +- 60 alliances

Due to complexity of globalization, information technology,

growth of international governance rules...

31

0

500

1000

1500

2000

2500

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

Ne

w T

ech

no

log

y o

r R

es

ea

rch

A

llia

nc

es

Year

Worldwide

formation of

technology or

research

alliances

varies over

time

Advantages of alliances?

• Obtain skills or resources more quickly than

internally

• Reduce asset commitment and increase flexibility

• Learn from partner

• Share costs and risks

• Build cooperation around a common standard

32

Strategic alliance processes

Two themes are vital to success in alliances:

• Co-evolution

the need for flexibility and change as the environment, competition

and strategies of the partners evolve.

• Trust

partners need to behave in a trustworthy fashion throughout the

alliance

33

Alliance co-evolution

34

case

• In what respects did co-evolution break down in the

Areva NP joint venture?

35

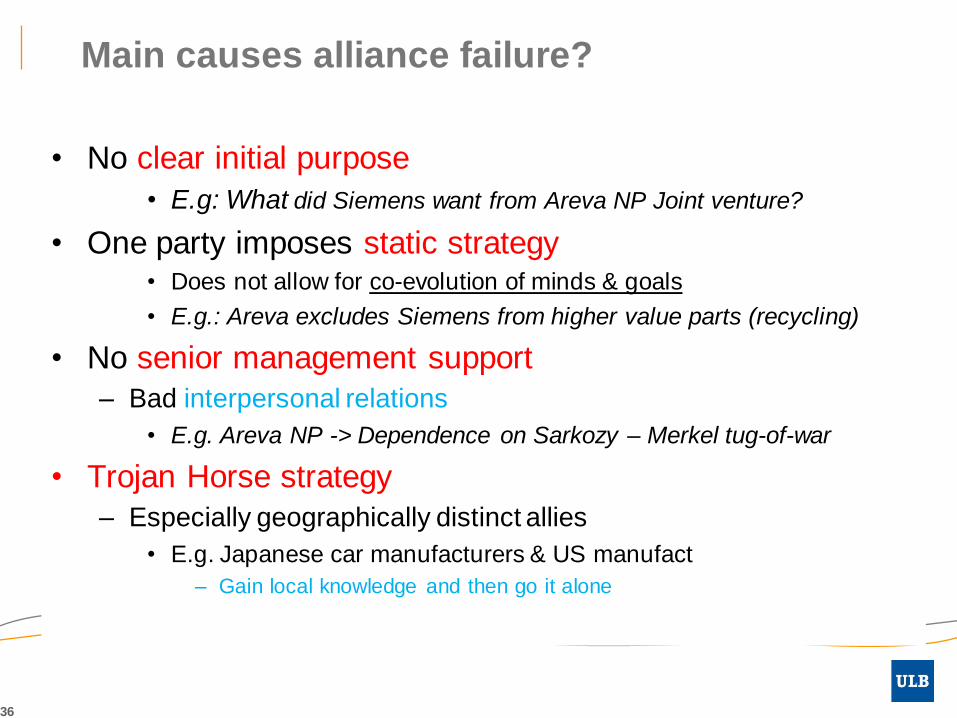

Main causes alliance failure?

• No clear initial purpose

• E.g: What did Siemens want from Areva NP Joint venture?

• One party imposes static strategy • Does not allow for co-evolution of minds & goals

• E.g.: Areva excludes Siemens from higher value parts (recycling)

• No senior management support

– Bad interpersonal relations

• E.g. Areva NP -> Dependence on Sarkozy – Merkel tug-of-war

• Trojan Horse strategy

– Especially geographically distinct allies

• E.g. Japanese car manufacturers & US manufact

– Gain local knowledge and then go it alone

36

Comparing acquisitions, alliances and organic

development

Four key factors in choosing the method of strategy development

• Urgency? – internal development may be too slow, alliances can accelerate the process but acquisitions are quickest.

• Uncertainty? – an alliance means learning & risk-sharing; thus a failure does not mean the full cost is lost.

• Type of capabilities – hard versus soft - acquisitions work best with ‘hard’ resources (e.g. production units) rather than ‘soft’ resources (e.g. people). Culture clash is the big issue (avoid with organic)

• Dedicated-purpose capabilities? – if the needed capabilities can be clearly separated from the rest of the organisation an alliance may be best.

37

– Importance strategic agility

• Strategic sensitivity

– Capability to develop an early and keen awareness of

incipient trends

• Leadership quality

– Capability of top team to make bold decisions fast,

without being bogged down in politics

• Resource fluidity

– Corporate capability to reconfigure businesses and

redeploy resources rapidly and effectively

38

Realising a vision

Where did things go wrong?

39

Where did things go wrong for

« Burning platform memo » Stephen Elop

- Strategic sensitivity?

• Missed the trend from device-led to software-led

• Missed the smartphone touchscreen trend

– Why?

– Logical decisions to streamline or speed up hampered by

centralized, overly formalized structure

» Nokia outsources manufacturing chip-sets for speed

» Yet, slows downs process by insisting on own « proprietary software »

– Too complex planning!

40

Dangers associated with planning

• Confusing strategy with the plan

• Detachment from reality

• Paralysis by analysis

• Lack of ownership

– selected club of insiders

• Dampening of innovation

41

Where did things go wrong for

« Burning platform memo » Stephen Elop

– Leadership quality?

• Overly long decision-making processes, too many

management layers, lots of planning bureaucracy…

– Committees, « brand board », « capability board »,

« sustainability and investment board », …

– Even Group Executive Board!

» Had become« talking parlour »

42

Visionary leadership Jorma Ollila

• Pro

– Speed

– Unorthodox strategies that are hard to imitate

• Dyson, Brin/Page, Ollila...

• Contra

– Creativity held back

• What whould the leader think/want/do?

– Succession planning

• In many family companies

• What after Dyson, Brin/Page, Ollila...

43

Where did things go wrong for

• Resource fluidity?

• Not enough autonomy/ accountability

– Local staff e-mailed Elop:

» Local teams could were not authorised to deliver « dual-Sim »

device tailored for Indian users who wanted to switch Sim-cards

along country’s many different regional providers

» Chinese manufacturers of cheap handsets are cranking out a

device much faster than the time it takes us to polish a PPT

presentation»

» Look, I’m right here in the region. I can make this simple little

decision, [but] I’m waiting for someone who is 10 timezones away

and has three bosses of their own »

44

Case

• Innovation focus from chip manufact (DRAM)

– To designing microprocessors

• Due to pre-existing resource allocation rule! • Manufacturing cap. proportional to profit margins

• Success rule created by first financial director

– Designed to maintain Intel as tech leading-edge

• Unplanned, lots of resistance

– Both from senior mgt

– And DRAM Business unit

45