technology & licensing strategy in a … sabic presentation at mumbai grpc...technology &...

TRANSCRIPT

TECHNOLOGY & LICENSING STRATEGY IN A CHANGING ETHYLENE VALUE CHAIN LANDSCAPE

Global Refining & Petrochemicals CongressMumbai, 25-26 May 2017

Martijn Vogelzang & Guido Crevecoeur

No. 1Global Refining & Petrochemicals Congress, Mumbai, 25 May 2017

TECHNOLOGY & LICENSING STRATEGY IN A CHANGING ETHYLENE VALUE CHAIN LANDSCAPE

Main topics:1. Changes in the ethylene landscape Supply-demand Capacity Net trade

2. SABIC’s strategic response Investments in new capacity

3. SABIC’s Technology & Innovation strategy Process & product technology Licensing of proven technologies

No. 2Global Refining & Petrochemicals Congress, Mumbai, 25 May 2017

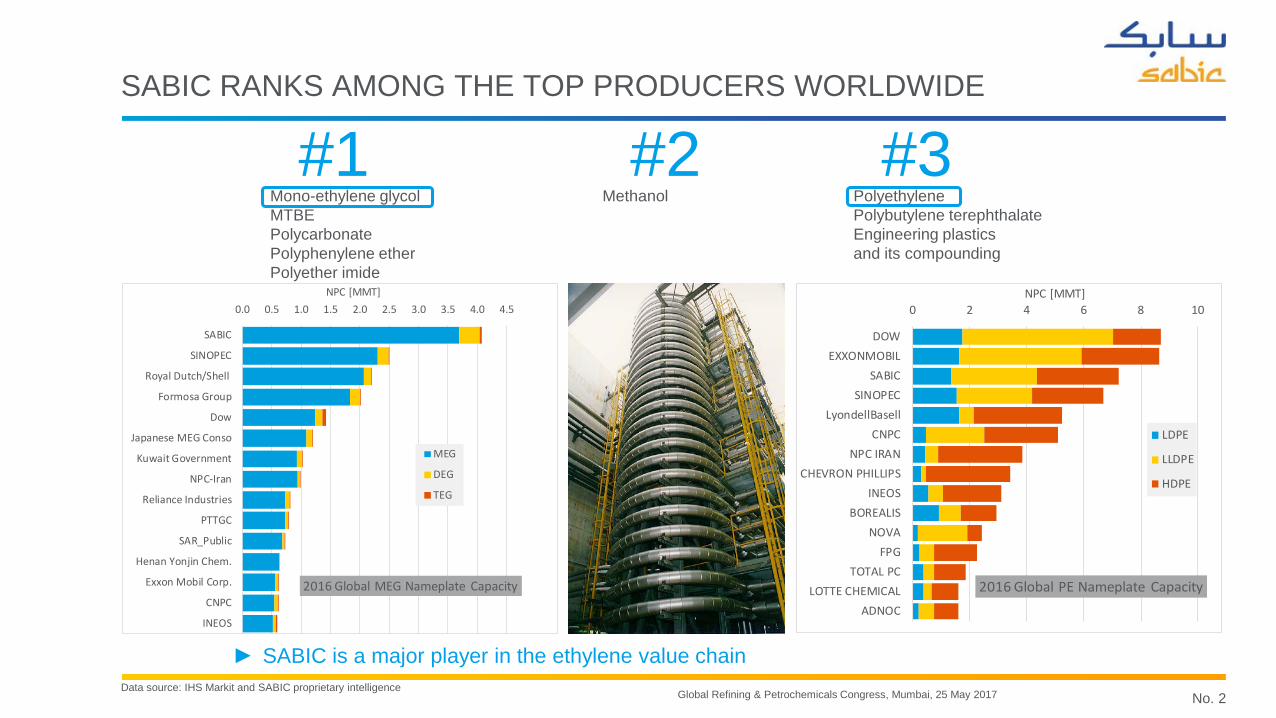

SABIC RANKS AMONG THE TOP PRODUCERS WORLDWIDE

#1 #2 #3Mono-ethylene glycolMTBEPolycarbonatePolyphenylene etherPolyether imide

Methanol PolyethylenePolybutylene terephthalateEngineering plastics and its compounding

Data source: IHS Markit and SABIC proprietary intelligence

► SABIC is a major player in the ethylene value chain

0 2 4 6 8 10

DOWEXXONMOBIL

SABICSINOPEC

LyondellBasellCNPC

NPC IRANCHEVRON PHILLIPS

INEOSBOREALIS

NOVAFPG

TOTAL PCLOTTE CHEMICAL

ADNOC

NPC [MMT]

2016 Global PE Nameplate Capacity

LDPE

LLDPE

HDPE

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5

SABIC

SINOPEC

Royal Dutch/Shell

Formosa Group

Dow

Japanese MEG Conso

Kuwait Government

NPC-Iran

Reliance Industries

PTTGC

SAR_Public

Henan Yonjin Chem.

Exxon Mobil Corp.

CNPC

INEOS

NPC [MMT]

2016 Global MEG Nameplate Capacity

MEG

DEG

TEG

No. 3Global Refining & Petrochemicals Congress, Mumbai, 25 May 2017

CHANGED ETHYLENE LANDSCAPE

Ethane is the strongest growing feedstock:► Ethane growing strongly in NA (shale gas) and in ME► Naphtha shrinking in NA and EUR but still growing in Asia► MTO (methanol-to-olefin) and CTO (coal-to-olefin) growing in

China, but remain small compared to ethane and naphtha

-

5

10

15

20

25

30

35

40

45

50

2010

2016

2022

2010

2016

2022

2010

2016

2022

2010

2016

2022

2010

2016

2022

2010

2016

2022

2010

2016

2022

2010

2016

2022

2010

2016

2022

NA SA EUR CIS ME AFR INS NEA SEA

Ethy

lene

Pro

duct

ion

[MM

T]Ethylene Production by Source & Region

Naphtha Ethane Propane Butane Gas Oil MTO CTO Other MTP

Data source: IHS Markit

Region Period Naphtha Ethane Propane Butane Gas Oil MTO CTONA 2010-->16 -16% 4% -1% 14% -21%

2016-->22 -7% 7% 1% -6% 0%SA 2010-->16 -2% -1% 7% -100%

2016-->22 2% 2% -6%EUR 2010-->16 -3% 2% 13% 8% -2%

2016-->22 -1% 6% 0% -1% -3%CIS 2010-->16 0% 12% 13% 12% -2%

2016-->22 6% 7% 29% 24% 11%ME 2010-->16 6% 6% 4% 19%

2016-->22 0% 3% 1% 2% -100%AFR 2010-->16 -100% -4% 4% -4%

2016-->22 9% 5% -4%INS 2010-->16 8% 10% 12%

2016-->22 6% 9% 5% 18%NEA 2010-->16 1% 21% 4% 6% 76%

2016-->22 1% 7% 3% 2% 12% 25%SEA 2010-->16 4% 6% 2% 4% 13%

2016-->22 7% -3% 9% 10% 11%

Compounded Annual Growth Rate (CAGR)

No. 4Global Refining & Petrochemicals Congress, Mumbai, 25 May 2017

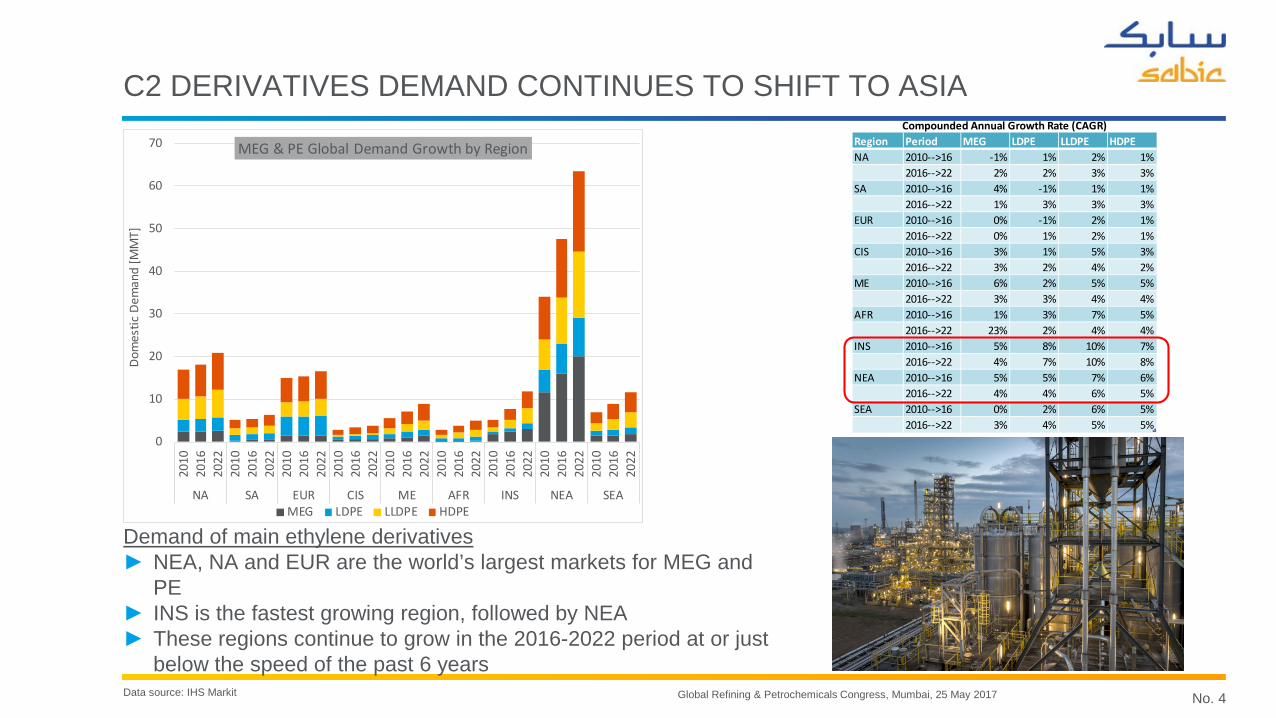

C2 DERIVATIVES DEMAND CONTINUES TO SHIFT TO ASIA

Demand of main ethylene derivatives► NEA, NA and EUR are the world’s largest markets for MEG and

PE► INS is the fastest growing region, followed by NEA► These regions continue to grow in the 2016-2022 period at or just

below the speed of the past 6 yearsData source: IHS Markit

0

10

20

30

40

50

60

70

2010

2016

2022

2010

2016

2022

2010

2016

2022

2010

2016

2022

2010

2016

2022

2010

2016

2022

2010

2016

2022

2010

2016

2022

2010

2016

2022

NA SA EUR CIS ME AFR INS NEA SEA

Dom

estic

Dem

and

[MM

T]MEG & PE Global Demand Growth by Region

MEG LDPE LLDPE HDPE

Region Period MEG LDPE LLDPE HDPENA 2010-->16 -1% 1% 2% 1%

2016-->22 2% 2% 3% 3%SA 2010-->16 4% -1% 1% 1%

2016-->22 1% 3% 3% 3%EUR 2010-->16 0% -1% 2% 1%

2016-->22 0% 1% 2% 1%CIS 2010-->16 3% 1% 5% 3%

2016-->22 3% 2% 4% 2%ME 2010-->16 6% 2% 5% 5%

2016-->22 3% 3% 4% 4%AFR 2010-->16 1% 3% 7% 5%

2016-->22 23% 2% 4% 4%INS 2010-->16 5% 8% 10% 7%

2016-->22 4% 7% 10% 8%NEA 2010-->16 5% 5% 7% 6%

2016-->22 4% 4% 6% 5%SEA 2010-->16 0% 2% 6% 5%

2016-->22 3% 4% 5% 5%

Compounded Annual Growth Rate (CAGR)

No. 5Global Refining & Petrochemicals Congress, Mumbai, 25 May 2017

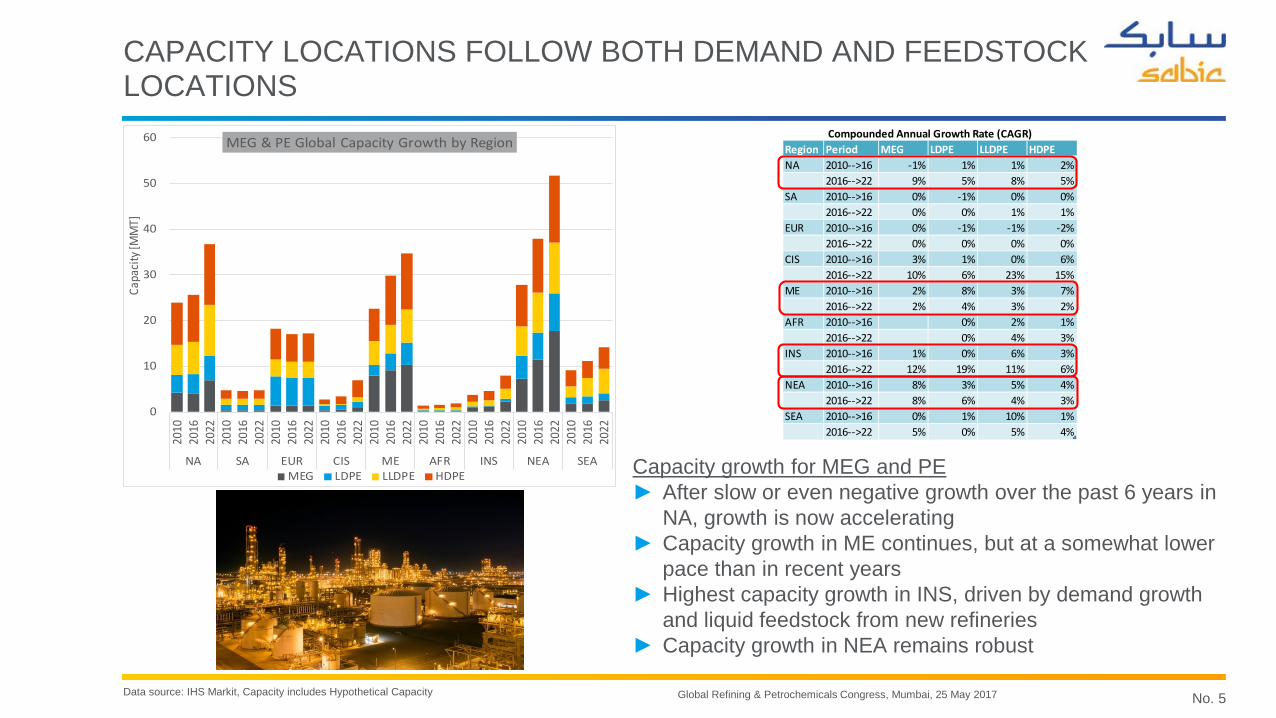

CAPACITY LOCATIONS FOLLOW BOTH DEMAND AND FEEDSTOCK LOCATIONS

Capacity growth for MEG and PE► After slow or even negative growth over the past 6 years in

NA, growth is now accelerating► Capacity growth in ME continues, but at a somewhat lower

pace than in recent years► Highest capacity growth in INS, driven by demand growth

and liquid feedstock from new refineries► Capacity growth in NEA remains robust

Data source: IHS Markit, Capacity includes Hypothetical Capacity

0

10

20

30

40

50

60

2010

2016

2022

2010

2016

2022

2010

2016

2022

2010

2016

2022

2010

2016

2022

2010

2016

2022

2010

2016

2022

2010

2016

2022

2010

2016

2022

NA SA EUR CIS ME AFR INS NEA SEA

Capa

city

[MM

T]MEG & PE Global Capacity Growth by Region

MEG LDPE LLDPE HDPE

Region Period MEG LDPE LLDPE HDPENA 2010-->16 -1% 1% 1% 2%

2016-->22 9% 5% 8% 5%SA 2010-->16 0% -1% 0% 0%

2016-->22 0% 0% 1% 1%EUR 2010-->16 0% -1% -1% -2%

2016-->22 0% 0% 0% 0%CIS 2010-->16 3% 1% 0% 6%

2016-->22 10% 6% 23% 15%ME 2010-->16 2% 8% 3% 7%

2016-->22 2% 4% 3% 2%AFR 2010-->16 0% 2% 1%

2016-->22 0% 4% 3%INS 2010-->16 1% 0% 6% 3%

2016-->22 12% 19% 11% 6%NEA 2010-->16 8% 3% 5% 4%

2016-->22 8% 6% 4% 3%SEA 2010-->16 0% 1% 10% 1%

2016-->22 5% 0% 5% 4%

Compounded Annual Growth Rate (CAGR)

No. 6Global Refining & Petrochemicals Congress, Mumbai, 25 May 2017

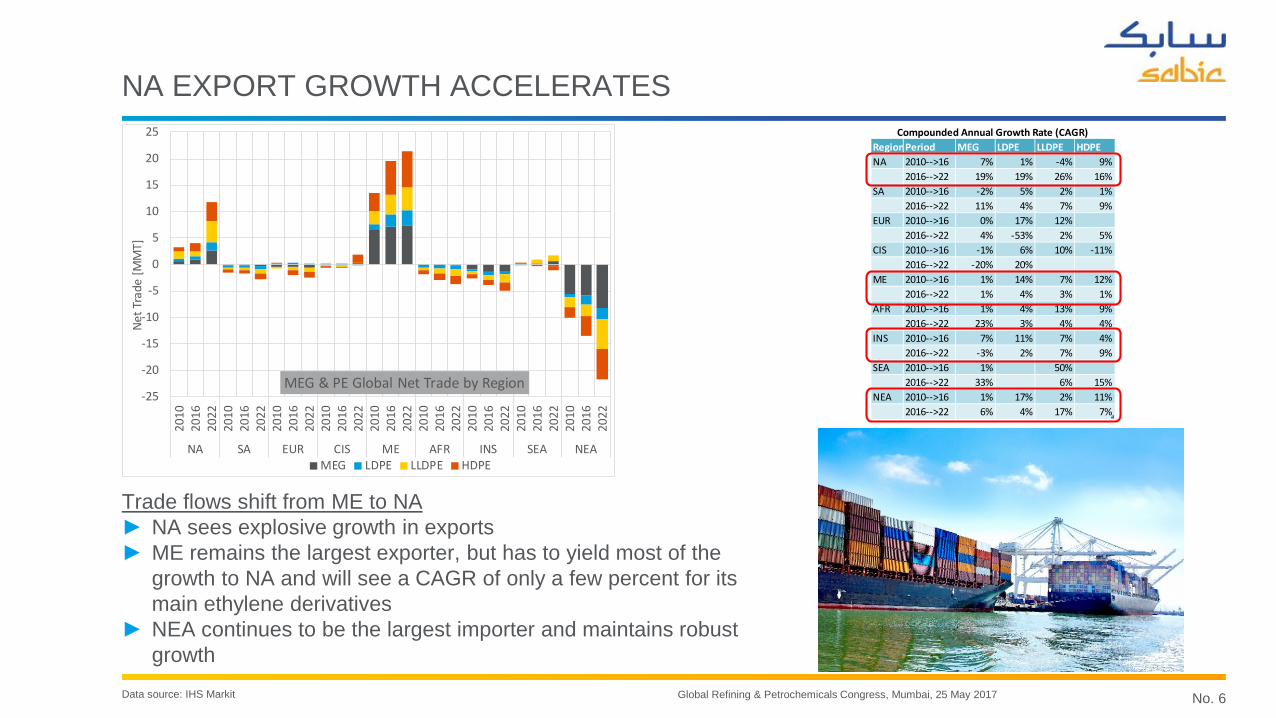

NA EXPORT GROWTH ACCELERATES

Trade flows shift from ME to NA► NA sees explosive growth in exports► ME remains the largest exporter, but has to yield most of the

growth to NA and will see a CAGR of only a few percent for its main ethylene derivatives

► NEA continues to be the largest importer and maintains robust growth

Data source: IHS Markit

-25

-20

-15

-10

-5

0

5

10

15

20

25

2010

2016

2022

2010

2016

2022

2010

2016

2022

2010

2016

2022

2010

2016

2022

2010

2016

2022

2010

2016

2022

2010

2016

2022

2010

2016

2022

NA SA EUR CIS ME AFR INS SEA NEA

Net T

rade

[MM

T]

MEG & PE Global Net Trade by Region

MEG LDPE LLDPE HDPE

RegionPeriod MEG LDPE LLDPE HDPENA 2010-->16 7% 1% -4% 9%

2016-->22 19% 19% 26% 16%SA 2010-->16 -2% 5% 2% 1%

2016-->22 11% 4% 7% 9%EUR 2010-->16 0% 17% 12%

2016-->22 4% -53% 2% 5%CIS 2010-->16 -1% 6% 10% -11%

2016-->22 -20% 20%ME 2010-->16 1% 14% 7% 12%

2016-->22 1% 4% 3% 1%AFR 2010-->16 1% 4% 13% 9%

2016-->22 23% 3% 4% 4%INS 2010-->16 7% 11% 7% 4%

2016-->22 -3% 2% 7% 9%SEA 2010-->16 1% 50%

2016-->22 33% 6% 15%NEA 2010-->16 1% 17% 2% 11%

2016-->22 6% 4% 17% 7%

Compounded Annual Growth Rate (CAGR)

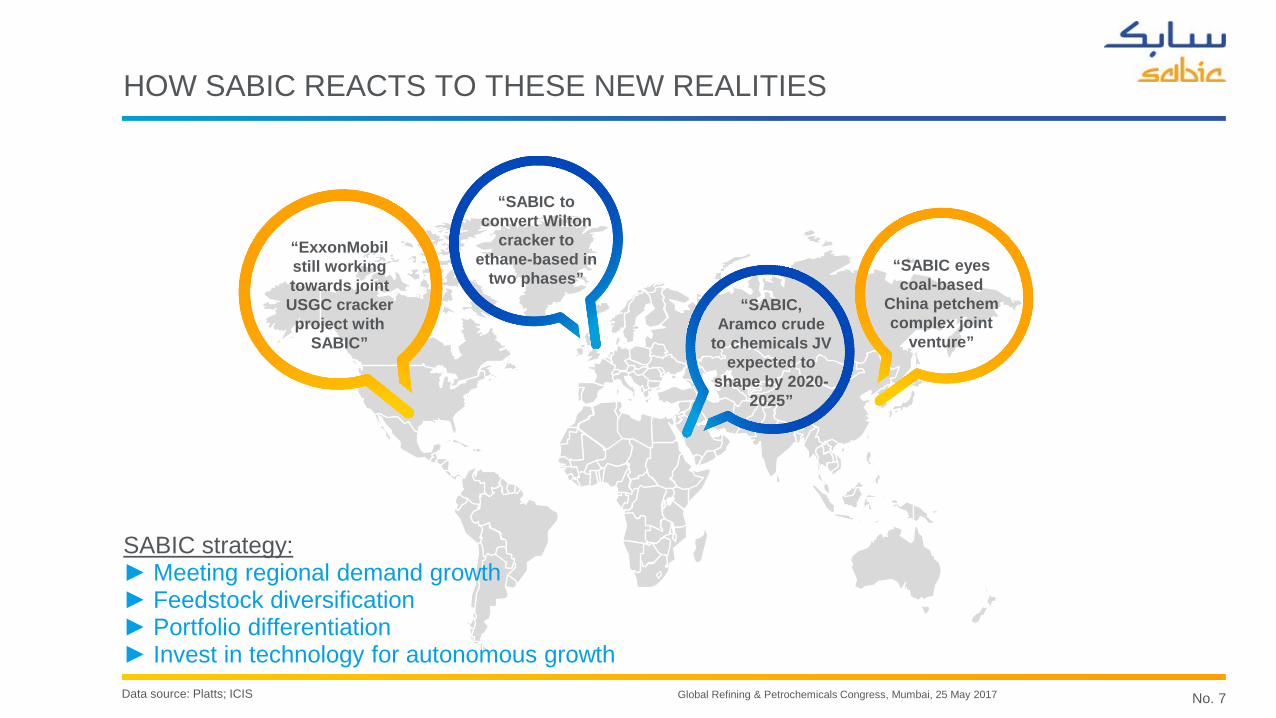

No. 7Global Refining & Petrochemicals Congress, Mumbai, 25 May 2017Data source: Platts; ICIS

“SABIC eyes coal-based

China petchemcomplex joint

venture”

“ExxonMobil still working towards joint USGC cracker project with

SABIC”

“SABIC to convert Wilton

cracker to ethane-based in

two phases” “SABIC,

Aramco crude to chemicals JV

expected to shape by 2020-

2025”

HOW SABIC REACTS TO THESE NEW REALITIES

SABIC strategy:► Meeting regional demand growth► Feedstock diversification► Portfolio differentiation► Invest in technology for autonomous growth

No. 8Global Refining & Petrochemicals Congress, Mumbai, 25 May 2017

TECHNOLOGY & INNOVATION FOCUS

Sustained efforts in► New and improved technology► Differentiated products within a commodity portfolio

World-class infrastructure and know-how Five key geographies with innovation hubs in USA, Europe, Middle East, Indian Subcontinent, North East Asia

Practical innovation Application development with key customers at the heart of our strategy More than 150 new products created every year Backed by 10,960 global patent filings

No. 9Global Refining & Petrochemicals Congress, Mumbai, 25 May 2017

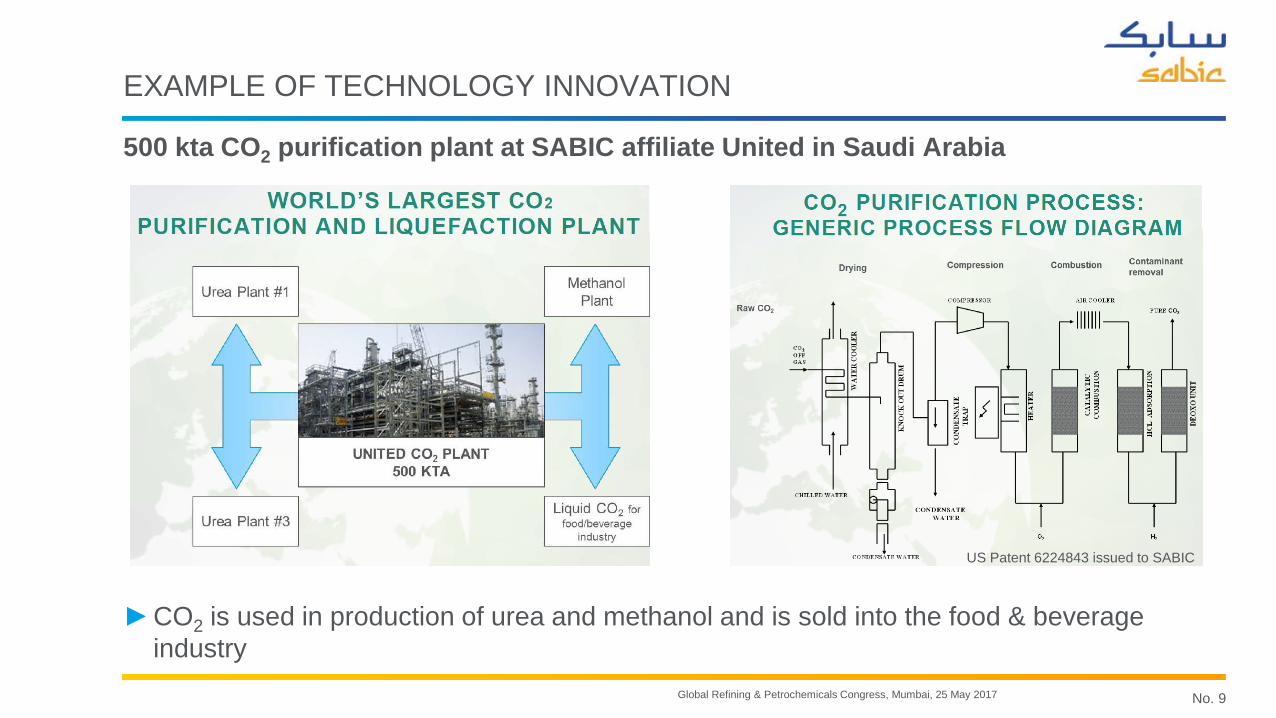

EXAMPLE OF TECHNOLOGY INNOVATION

►CO2 is used in production of urea and methanol and is sold into the food & beverage industry

500 kta CO2 purification plant at SABIC affiliate United in Saudi Arabia

US Patent 6224843 issued to SABIC

No. 10Global Refining & Petrochemicals Congress, Mumbai, 25 May 2017

PRODUCT INNOVATION IN FOOD PACKAGING

2. New SABIC® LDPE film grade produced in CTR® process Excellent draw-down ability as low as 12 μm Higher production line speed Can be used in both mono and co-extruded film Provides full compliance with stringent food contact regulations for

both fatty and non-fatty foods

RESIN PRODUCER

EXTRUSIONCOATER FILLER CONSUMER

1. Extrusion coating grade from CTR® tubular LDPE technology production

UNIQUE MWD DISTRIBUTION MADEIN CTR® PROCESS

PROCESSABILLITY:• High line speeds• Thin coating layers• Improved adhesion

BETTER HOTTACK& SEALING

COMPLIANT TO REGULATIONS • ADDITIVE FREE

CTR®=Clean Tubular Reactor

No. 11Global Refining & Petrochemicals Congress, Mumbai, 25 May 2017

PROCESS & PRODUCT TECHNOLOGY STRATEGY IS KEY

SABIC is revisiting its technology strategy:

Main Drivers:1. Maximise use of proprietary technology in new projects, leveraging:

CAPEX/OPEX improvements for chemicals Enhanced product development on selected polymer technology platforms

2. Monetise SABIC’s proven technology portfolio, through: Active licensing of SABIC technology to 3rd parties, combined with: R&D efforts and Technical Service Sharing of Operational Excellence (where applicable) Catalyst sales

3. Explore opportunities to license non-proven technologies and patents

From traditionally licensing technologies from others SABIC is now moving towards proprietary developments and licensing technologies out to 3rd parties

No. 12Global Refining & Petrochemicals Congress, Mumbai, 25 May 2017

COMPREHENSIVE PORTFOLIO OF PROVEN TECHNOLOGIES

Jointly owned Others

Styrene

EO/EG

PET

PC

BPA

EPS

Phenol

CV

PTA

Cumene

CTR LDPE

Butadiene

Acetic Acid

HRG

Ethylene cracker

LAO 1-Butene1-Hexene

C8-C20

MMA

Ethane

Benzene

UHMWPE

LDPE

UHMWPE

LLDPE/HDPE

STARTEC Styrene

DMC DPCMethane Methanol

CO

O2

BPA

Paraxylene

Chlorine PhosgeneChlorine

Naphtha crackerNaphtha

Ethylene Production

Acetone

HDPE

LLDPE

PC

SAN

PBLABSAcrylonitrile

LLDPE

PS

ABS

1-butene

HDPE

LLDPE

Butane

PC

NaOH

Propylene

Vinyl AcetateAcetic Anhydride

PET Tape line

Technology owners

PET Tape

AA

EO/EG

SABICPolymer

PP PPCO2

SABICChemical

No. 13Global Refining & Petrochemicals Congress, Mumbai, 25 May 2017

A WIDE RANGE OF TECHNOLOGIES FOR 3rd PARTY LICENSING

Butadiene α-Sablin LAO1 EO/EG2

Butene-1 CO2 BPA

Phenol Acetic Acid

State of art technologies supported withworld class engineering and licensing partners

Polymers TechnologiesChemicals Technologies

CTR® LDPE LLDPE/HDPE UHMWPE*

PP ABS-Emulsion ABS-Mass

PC*

* Only captive licensing1 Technology jointly owned with Linde2 Marketed by Scientific Design, a SABIC/Clariant JV

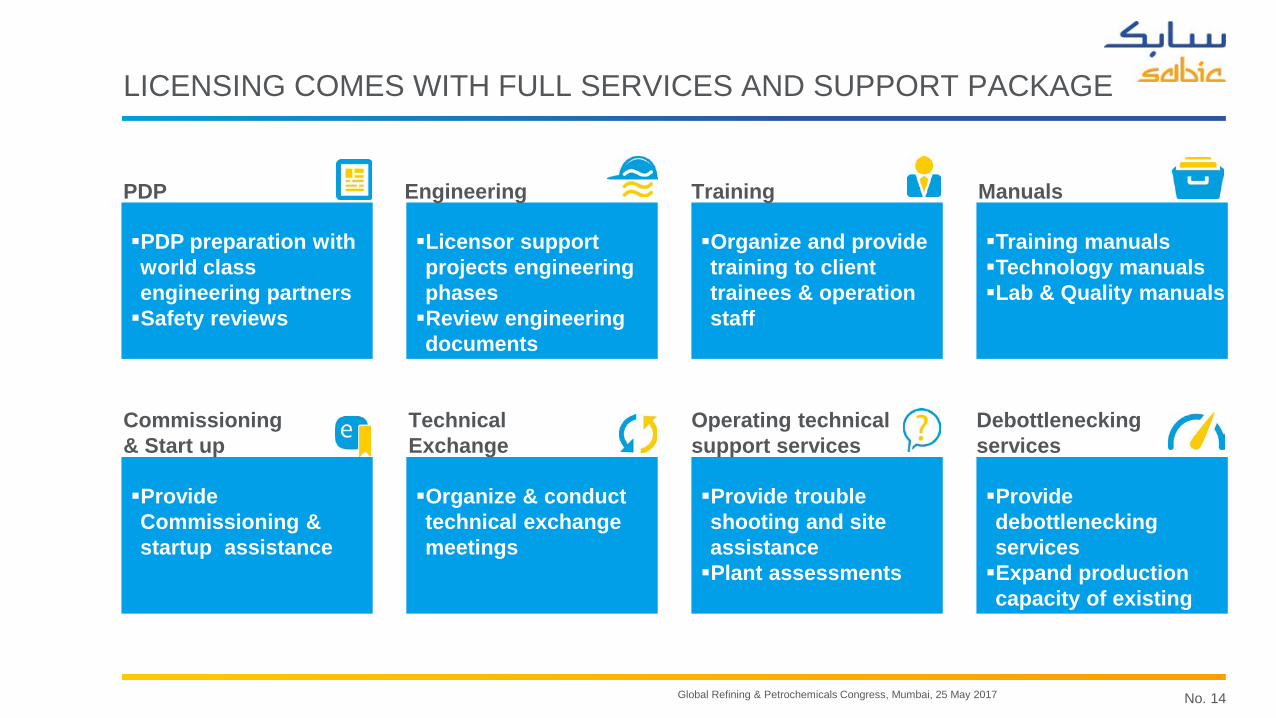

No. 14Global Refining & Petrochemicals Congress, Mumbai, 25 May 2017

PDP preparation with world class engineering partnersSafety reviews

Licensor support projects engineering phasesReview engineering documents

Organize and provide training to client trainees & operation staff

Training manualsTechnology manualsLab & Quality manuals

Provide Commissioning & startup assistance

Organize & conduct technical exchange meetings

Provide trouble shooting and site assistance Plant assessments

Provide debottlenecking servicesExpand production capacity of existing facilities

PDP Engineering Training Manuals

Commissioning & Start up

Technical Exchange

Operating technical support services

Debottleneckingservices

LICENSING COMES WITH FULL SERVICES AND SUPPORT PACKAGE

No. 15Global Refining & Petrochemicals Congress, Mumbai, 25 May 2017

SUMMARY

►Significant changes in ethylene value chain: demand, supply and trade flows

►In response, SABIC is globalising its asset footprint and investing in alternative feedstock for ethylene

►Increased focus on developing proprietary technologies

►Active marketing of SABIC’s proven technologies

Contact:Martijn VogelzangDirector [email protected]+31 6 3192 9952

Guido CrevecoeurLicensing Marketing [email protected]+31 6 4691 0261

No. 16Global Refining & Petrochemicals Congress, Mumbai, 25 May 2017

No. 17Global Refining & Petrochemicals Congress, Mumbai, 25 May 2017

DISCLAIMER

DISCLAIMER: THE MATERIALS, PRODUCTS AND SERVICES OF SAUDI BASIC INDUSTRIES CORPORATION (SABIC) OR ITS SUBSIDIARIES OR AFFILIATES (“SELLER”) ARE SOLD SUBJECT TO SELLER’S STANDARD CONDITIONS OF SALE, WHICH ARE AVAILABLE UPON REQUEST. INFORMATION AND RECOMMENDATIONS CONTAINED IN THIS DOCUMENT ARE GIVEN IN GOOD FAITH. HOWEVER, SELLER MAKES NO EXPRESS OR IMPLIED REPRESENTATION, WARRANTY OR GUARANTEE (i) THAT ANY RESULTS DESCRIBED IN THIS DOCUMENT WILL BE OBTAINED UNDER END-USE CONDITIONS, OR (ii) AS TO THE EFFECTIVENESS OR SAFETY OF ANY DESIGN OR APPLICATION INCORPORATING SELLER’S MATERIALS, PRODUCTS, SERVICES OR RECOMMENDATIONS. UNLESS OTHERWISE PROVIDED IN SELLER’S STANDARD CONDITIONS OF SALE, SELLER SHALL NOT BE RESPONSIBLE FOR ANY LOSS RESULTING FROM ANY USE OF ITS MATERIALS, PRODUCTS, SERVICES OR RECOMMENDATIONS DESCRIBED IN THIS DOCUMENT. Each user is responsible for making its own determination as to the suitability of Seller’s materials, products, services or recommendations for the user’s particular use through appropriate end-use and other testing and analysis. Nothing in any document or oral statement shall be deemed to alter or waive any provision of Seller’s Standard Conditions of Sale or this Disclaimer, unless it is specifically agreed to in a writing signed by Seller. Statements by Seller concerning a possible use of any material, product, service or design do not, are not intended to, and should not be construed to grant any license under any patent or other intellectual property right of Seller or as a recommendation for the use of any material, product, service or design in a manner that infringes any patent or other intellectual property right.

SABIC and brands marked with ™ are trademarks of SABIC or its subsidiaries or affiliates.© 2017 Saudi Basic Industries Corporation (SABIC). All Rights Reserved.

† Any brands, products or services of other companies referenced in this document are the trademarks, service marks and/or trade names of their respective holders.