temenos romania march 18, 2003 every time a step ahead

TRANSCRIPT

TEMENOS ROMANIA TEMENOS ROMANIA

March 18, 2003March 18, 2003

Every time a step Every time a step ahead ahead

IntroductionIntroduction

Hilde CorbuHilde CorbuCEO, Temenos RomaniaCEO, Temenos Romania

TEMENOS ROMANIA S.A.TEMENOS ROMANIA S.A. Member of the International Temenos GroupMember of the International Temenos Group Distribution, Implementation, Support and Distribution, Implementation, Support and

Training Center for Temenos banking Training Center for Temenos banking products in Romania and Republic of products in Romania and Republic of MoldaviaMoldavia

2003 2003 key business key business challengeschallenges

1/3 – profitability = 1/3 – profitability = extremely challengingextremely challenging

1/3 – customer 1/3 – customer retention = very retention = very

importantimportant

1/4 – cost reduction = 1/4 – cost reduction = extremely challengingextremely challenging

New Channels to New Channels to market & Time to market & Time to

market = importantmarket = important

20032003The importance of IT investmentThe importance of IT investment

Investment in Investment in CRM: CRM:

45%=Critical; 45%=Critical; 51%=Important51%=Important

Investment in Investment in Back Office: Back Office:

37%=Critical; 37%=Critical; 48%=Important48%=Important

Channel Channel Integration=key Integration=key

growth areagrowth area

3/4 – Branch 3/4 – Branch Renewal = Renewal = ImportantImportant

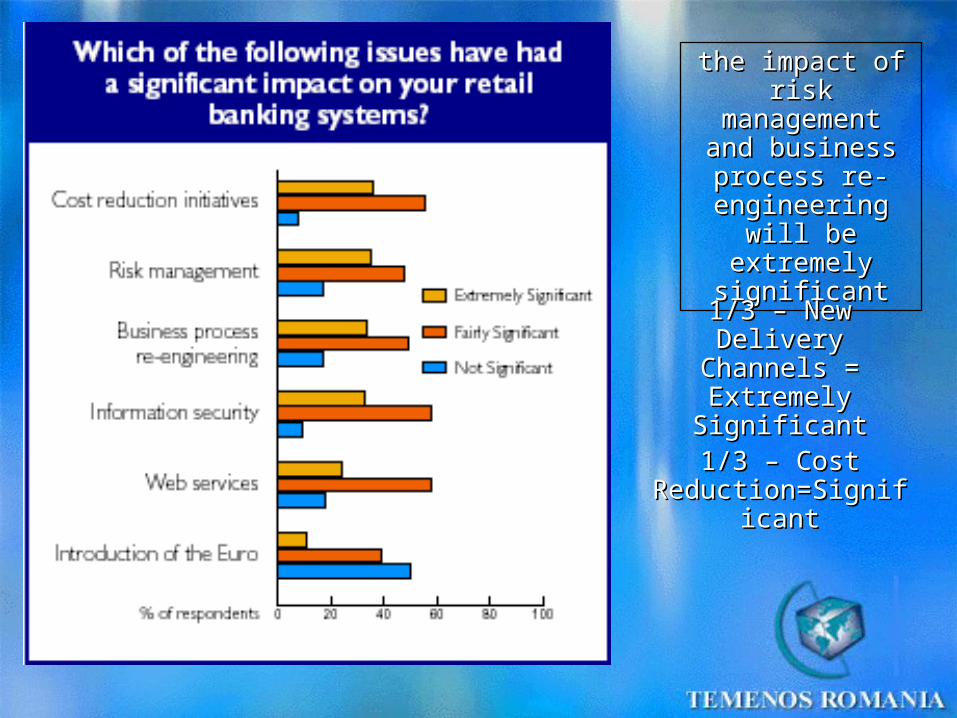

the impact of the impact of risk risk

management management and business and business process re-process re-

engineering will engineering will be extremely be extremely

significantsignificant

1/3 – New Delivery 1/3 – New Delivery Channels = Channels = Extremely Extremely SignificantSignificant

1/3 – Cost 1/3 – Cost Reduction=SignificReduction=Signific

antant

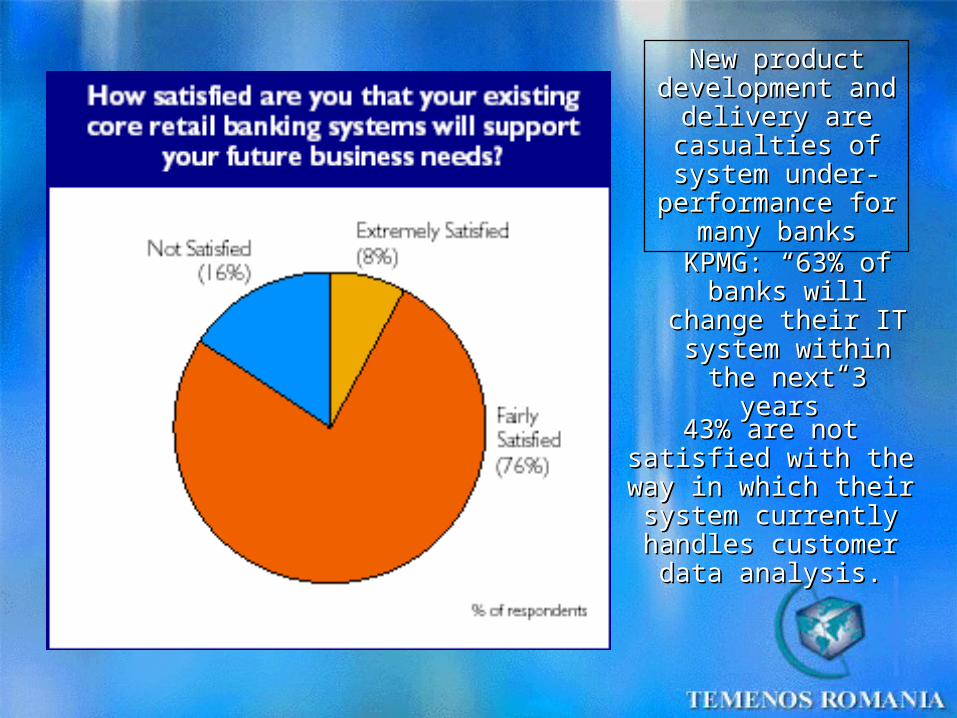

New product New product development and development and

delivery are delivery are casualties of casualties of

system under-system under-performance for performance for

many banksmany banksKPMG: “63% of KPMG: “63% of

banks will change banks will change their IT system their IT system

within the next 3 within the next 3 years”years”

43% are not satisfied 43% are not satisfied with the way in which with the way in which their system currently their system currently

handles customer handles customer data analysis.data analysis.

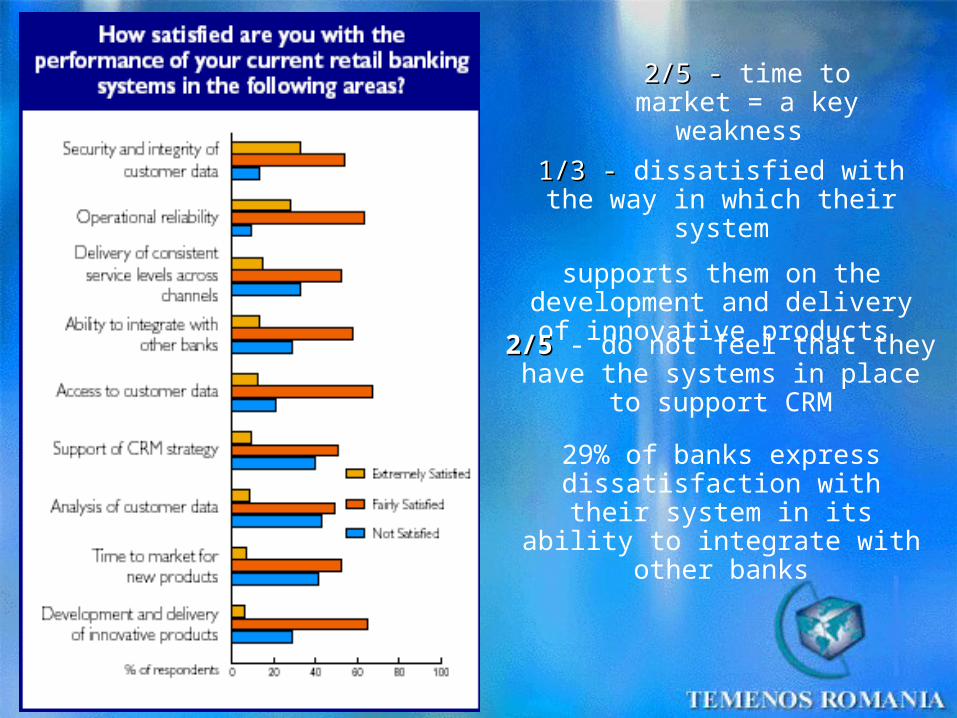

2/5 - 2/5 - time to market = a key weakness

1/3 - 1/3 - dissatisfied with the way in which their system

supports them on the development and delivery of

innovative products

2/52/5 - do not feel that they have the systems in place to support

CRM

29% of banks express dissatisfaction with their system in its ability to

integrate with other banks

Characteristics of the Retail Business Characteristics of the Retail Business MarketMarket

Banks in order to attract retail customers, and at the same time be successful in this business, need:

To be competitive in terms or interest rates and charges

To provide service quality

To be innovative in offering new products and services

To find alternative channels to promote and sell retail products in a controlled and secure way.

To manage the relations with their customers in a cost efficient and sales efficient way

To measure their exposure and manage their risks

Manage delinquencies

Control their costs due to the volumes of this business

Modern IT solutions supports the Bank Modern IT solutions supports the Bank to gain competitive advantageto gain competitive advantage

1) Processing (credit scoring)(credit scoring) of the profile of the customer and all his “risk related” data, in order to

define:

The “worthiness” of the customer,

The credit limit the Bank is willing to grant to this customer for all consumer lending related products (i.e. credit cards, consumer loans, mortgages, overdrafts e.t.c.).

The brake down of the credit limit to the several retail lending products,

“ “Personalization” of the product depending on the creditability of the client.

2) Credit Card productsCredit Card products should be supported and ideally allow the customer to be given the possibility to switch between credit card debt (revolving credit line which is normally more expensive) to term loans, which are normally less expensive, and vice versa

Modern IT solutions supports the Bank Modern IT solutions supports the Bank to gain competitive advantageto gain competitive advantage

3) FlexibilityFlexibility to define Loan Product characteristics, the terms and conditions, which will be automatically applied on every loan product depending on the commodity.

4) Processing and evaluation of customer’s Processing and evaluation of customer’s applicationsapplications in order to grant a loan or a credit card and support the operational workflows in order to process the request

Modern IT solutions supports the Bank Modern IT solutions supports the Bank to gain competitive advantageto gain competitive advantage5) Checking for the presence of all required documentsChecking for the presence of all required documents,

which are a prerequisite for granting a consumer loan or any other facility

6) Production of all related documentationProduction of all related documentation including all “agreements”, which need to be signed at the time of granting the loan

7) Functionality, that can be introduced, to improve the improve the relationship with cooperating merchantsrelationship with cooperating merchants and allow settlement of commissions to be paid to them.

8) Monitoring of payments due Monitoring of payments due, and if a payment is not done on time, then a past due payment record should be automatically created for which the Bank should apply its policy in terms of grace periods, penalty interest, hierarchy of payments, accruing of interest, transferring of the record to “Non Accrual basis” so that interest will not be booked in the P&L but in memo accounts etc.

Automation = Automation = Cost reductionCost reduction

Possibility to serve the retail Possibility to serve the retail customer through “direct customer through “direct banking channels” = banking channels” = Cost Cost

reductionreduction

Modern IT solutions supports the Bank Modern IT solutions supports the Bank to gain competitive advantageto gain competitive advantage

Modern IT solutions supports the Bank Modern IT solutions supports the Bank to gain competitive advantageto gain competitive advantageBy using such channels customers will not have to visit the

branches, as often as they do today, and will be in a position to perform, by themselves, the majority of the banking

transactions needed:

If there is the need for cash withdrawal the customer could use the ATM network

If there is a need to know an account balance, a credit card balance, a loan balance, or a need to receive a statement, the customer could use the ATM, or internet banking or phone banking

Similarly, if there is a need for a fund transfer, the ATM or the phone banking could be used (for simple transfers) and the Internet Banking or Mobile phone banking could be used (for more demanding fund transfers). International payments could also be served through these channels, as well as, buying or selling foreign currency.

Placing orders to buy or sell securities can also be served by the direct banking channels

Banks are seeking partnerships with external solutions

providers who can transfer their

expert skills and

experience to internal staff

TEMENOS ROMANIA TEMENOS ROMANIA

Software Applications Software Applications

to address theto address the

Banking Industry Banking Industry

Every time a step Every time a step ahead ahead

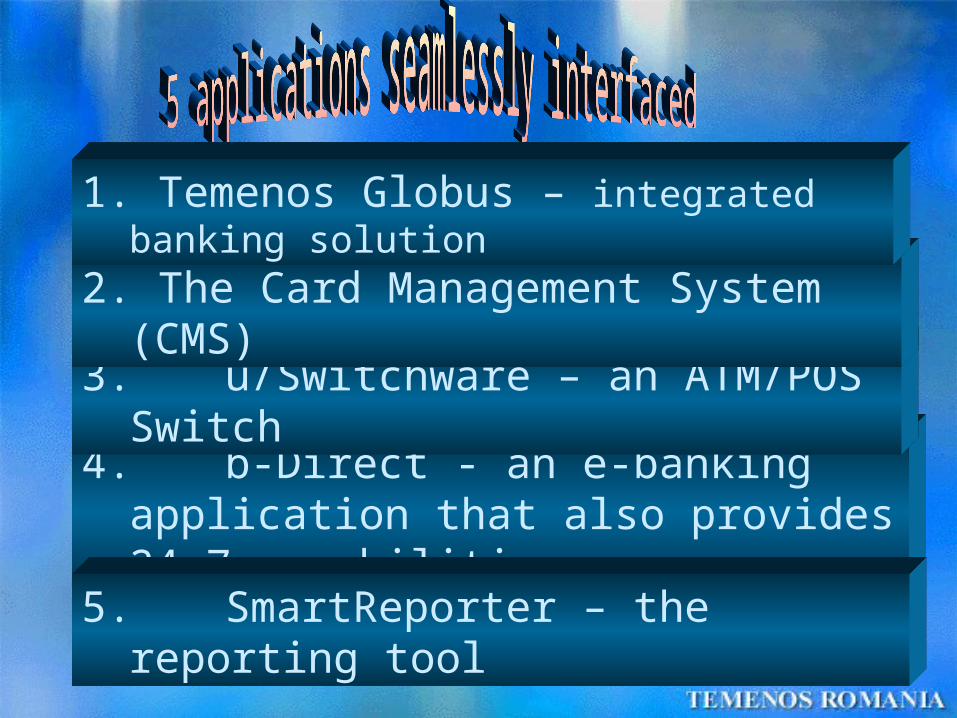

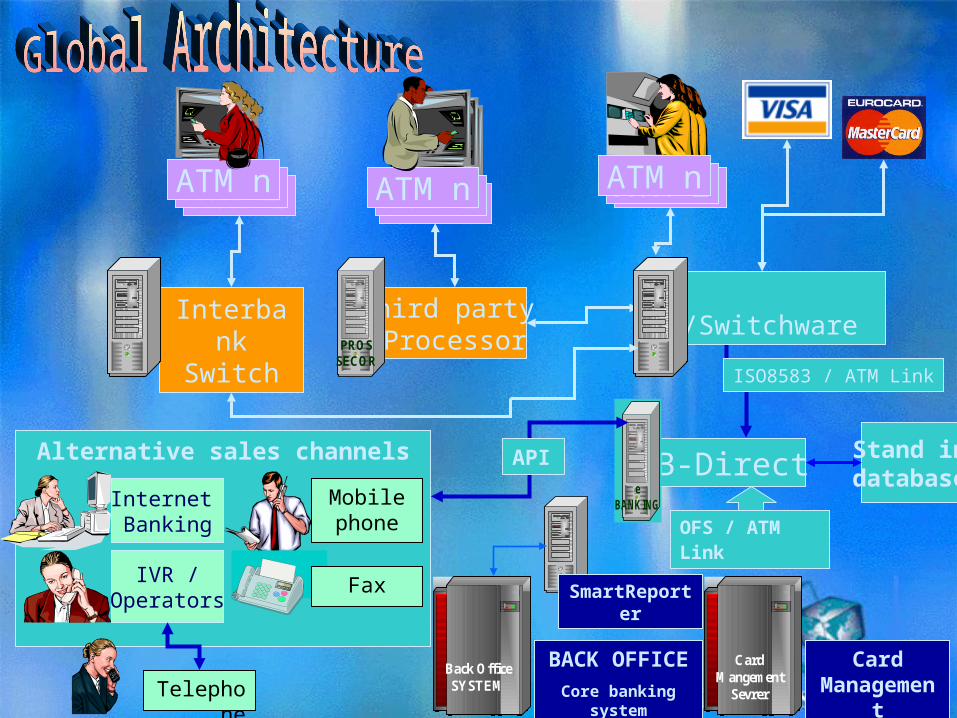

4. b-Direct - an e-banking application that also provides 24x7 capabilities

3. u/Switchware – an ATM/POS Switch

2. The Card Management System (CMS)

5. SmartReporter – the reporting tool

1. Temenos Globus – integrated banking solution

OFS / ATM Link

B-Directe

BANKING

ISO8583 / ATM Link

u/SwitchwareThird party ProcessorPROS

SECOR

ATM 1 ATM 1 ATM 1

InterbankSwitch

ATM 2ATM nATM 2ATM nATM 2ATM n

Stand indatabase

Alternative sales channels

Internet Banking

IVR /Operators

Telephone

Mobile phone

Fax

API

BACK OFFICE

Core banking system

Back OfficeSYSTEM

Card Management

CardMangement

Sevrer

SmartReporter

www.temenos.rowww.temenos.ro