terms and conditions in insurance contracts · terms and conditions in insurance contracts rob...

TRANSCRIPT

TERMS AND CONDITIONS

IN INSURANCE CONTRACTS Rob Merkin

University of Exeter

DLA Phillips Fox

SUBJECT MATTER OF TERMS

• Pre-policy or pre-inception terms – Premium

– Inspection/survey/improvements

• Pre-loss terms – Reasonable care

– Specific obligations, alarms, sprinklers

• Post-loss terms – Notice of loss and co-operation

–Mitigation

CONDITIONS

• Conditions precedent to risk: no attachment

• Conditions precedent to claim: no liability irrespective of prejudice • Milton Furniture Ltd v Brit Insurance Ltd [2014] EWHC

965 (QB)

• Bare conditions: liability unless policy repudiated, but insurer entitled to damages for breach • Friends Provident v Sirius International Insurance

Corporation [2006] Lloyd’s Rep IR 45

• Nulty v Milton Keynes Borough Council [2013] EWCA Civ 13

WARRANTIES

• Construction of warranties: strict interpretation

• Pratt v Aigaion Insurance [2008] EWCA Civ 2359

• Breach of warranty

• The Good Luck [1991] 3 All ER 1 • J A Chapman Co v Kadirga Denizcilik Ve Ticaret

[1998] Lloyd’s Rep IR 377

• Provincial Insurance Co v Morgan [1933] AC 240

• Present, future and implied marine warranties

• Waiver and estoppel • HIH v Axa Corporate [2003] Lloyd’s Rep IR 1

UK REFORMS TO DATE

• General control of unfair terms by Unfair Terms Regulations 1999 (now Consumer Rights Bill 2014)

• Present warranties: Consumer Insurance Act 2012

• Insurance Conduct of Business Rules • Insurers not to reject claims unreasonably

• Enforcement by Financial Ombudsman Service

• Breach of statutory duty (FSMA 2000)

PROPOSED UK REFORMS: INSURANCE REFORM BILL 2014

• No control over notice provisions

• Present warranties in business policies to be banned – treated as representations

• Future warranties suspensory only

• Increased risk clauses to be subject to causation test

ABOLITION OF CONTINUING WARRANTIES (UK)

(1) Any rule of law that breach of a warranty (express or implied) in a contract of insurance results in the discharge of the insurer’s liability under the contract is abolished.

(2) An insurer has no liability under a contract of insurance in respect of any loss occurring, or attributable to something happening, after a warranty (express or implied) in the contract has been breached but before the breach has been remedied (if it can be remedied).

DEFENCES TO BREACH OF WARRANTY (UK)

(3) But subsection (2) does not apply if—

(a) because of a change of circumstances, the warranty ceases to be applicable to the circumstances of the contract,

(b) compliance with the warranty is rendered unlawful by any subsequent law,

(c) the insurer waives the breach of warranty.

(4) Subsection (2) does not affect the liability of the insurer in respect of losses occurring, or attributable to something happening—

(a) before the breach of warranty, or

(b) if the breach can be remedied, after it has been remedied

FIXED DATE WARRANTIES (UK)

(5) Subsection (6) applies in the case of breach of a warranty requiring that by an ascertainable time—

(a) something is to be done, or not done,

(b) a condition is to be fulfilled, or

(c) something is, or is not, to be the case.

(6) For the purposes of this section, the breach is to be taken as remedied if at a later time the risk to which the warranty relates becomes essentially the same as that originally contemplated by the parties.

RISK CLAUSES (WHETHER OR NOT WARRANTIES) (UK)

(1) This section applies to any term (express or implied) of a contract of insurance compliance with which would tend to reduce the risk of one or both of the following—

(a) loss of a particular kind,

(b) loss at a particular location or time.

(2) Breach of such a term may not be relied upon by the insurer to exclude, limit or discharge its liability for, respectively—

(a) loss of a different kind,

(b) loss at a different location or time.

INSURANCE LAW REFORM ACT 1977. SECTION 11 (NZ)

(a) the policy excludes or limits the liability of the insurers to provide an indemnity

(b) the exclusion or limitation applies on the happening of certain events or on the existence of certain circumstances;

(c) the clause was present because, in the view of the insurer, the events or circumstances were likely to increase the risk of loss;

(d) the assured proves on the balance of probabilities that the loss was not caused or contributed to by the happening of those events or the existence of such circumstances

SECTION 11: GENERAL POINTS

• Post-contractual only

• Post-loss only where it can affect loss, eg, negotiating liability settlements with third parties

• Doesn’t override MIA 1908

• Events or circumstances needn’t be the acts or omissions of the assured, but in practice every case has been

SECTION 11 IN OPERATION

• Subjective and objective limbs in (c) and (d) – NZI v Harris (1990). Is (c) significant?

• Insurers to prove breach, assured to prove lack of causation – obligation on assured to show that loss would have happened anyway

• Norwich Winterthur v Hammond (1985): worn tyres unconnected to loss by flood

• Hing v Security (1986): unauthorised method of moving building did not contribute to loss

SECTION 11 AND RISK DEFINITION

• Barnaby v South British (1980): wall collapsed due to fault in design, policy not covering faults, s 11 not applicable to collapse

• Nelson v Three Tuis (2011): farm converted to B&B, s 11 not applicable to fire

• Hall v North (2010): PI policy excluding insolvency claims, s 11 not applicable

• Culham v Lumley (2000): unauthorised modification of premises within s 11

PROPOSALS FOR REFORM 1998: NEW S 11(1) • (1) An insured is not bound by an increased risk

exclusion if the insured proves on the balance of probability that the loss in respect of which the insured seeks to be indemnified was not caused or contributed to by the happening of an event or the existence of a circumstance referred to in the increased risk exclusion.

PROPOSALS FOR REFORM: NEW SECTION 11(2) (2) For the purposes of this section, an increased risk

exclusion is a provision in a contract of insurance that (a) defines the circumstances in which the insurer is

bound to indemnify the insured against loss so as to exclude or limit the liability of the insurer to indemnify the insured on the happening of certain events or on the existence of certain circumstances; and

(b) so defined the liability of the insurer, in the view of the court or arbitrator determining the claim of the insured, because the happening of such events or the existence of such circumstances was in the view of the insurer likely to increase the risk of loss occurring.

PROPOSALS FOR REFORM: NEW SECTION 11(3) (3) A provision is not an increased risk exclusion for the

purposes of this section that

(a) defines the age, identity, qualifications or experience of a driver of a vehicle, a pilot of an aircraft, or an operator of a chattel; or

(b) defines the geographical area in which a loss must occur if the insurer is to be liable to indemnify the insured; or

(c) excludes loss that occurs while a vehicle, aircraft, or other chattel is being used for commercial purposes other than those permitted by the contract of insurance.

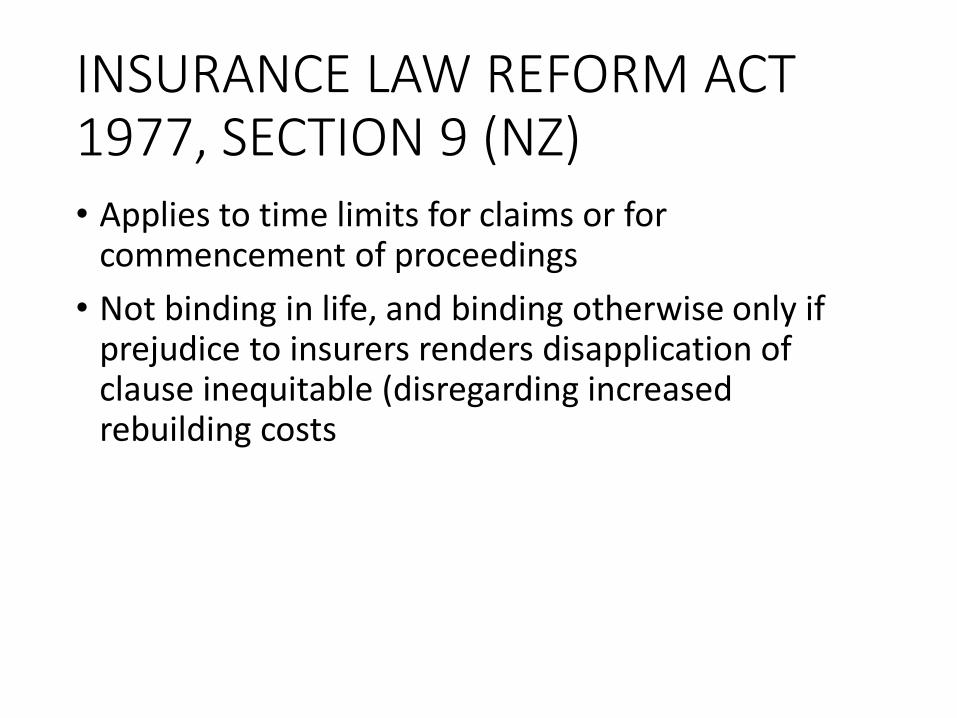

INSURANCE LAW REFORM ACT 1977, SECTION 9 (NZ) • Applies to time limits for claims or for

commencement of proceedings

• Not binding in life, and binding otherwise only if prejudice to insurers renders disapplication of clause inequitable (disregarding increased rebuilding costs

SECTION 9 AND LIABILITY

• Late notification of claim not protected if insurers lose right to defend: Nupin v Harlick (1988) – motor

• Claims made: late notification of circumstance within s 9 – Sinclair Horder v O’Malley (1995)

• Claims made and notified: late notification of circumstance within s 9 – Bradley v Keeman (1997)

INSURANCE CONTRACTS ACT 1984 (AUS)

(1) Subject to this section, where the effect of a contract of insurance would, but for this section, be that the insurer may refuse to pay a claim, either in whole or in part, by reason of some act [or omission] of the insured or of some other person, being an act that occurred after the contract was entered into but not being an act in respect of which subsection (2) applies, the insurer may not refuse to pay the claim by reason only of that act [or omission] but the insurer's liability in respect of the claim is reduced by the amount that fairly represents the extent to which the insurer's interests were prejudiced as a result of that act.

(2) Subject to the succeeding provisions of this section, where the act could reasonably be regarded as being capable of causing or contributing to a loss in respect of which insurance cover is provided by the contract, the insurer may refuse to pay the claim.

EFFECT OF BREACH (AUS)

(3) Where the insured proves that no part of the loss that gave rise to the claim was caused by the act, the insurer may not refuse to pay the claim by reason only of the act.

(4) Where the insured proves that some part of the loss that gave rise to the claim was not caused by the act, the insurer may not refuse to pay the claim, so far as it concerns that part of the loss, by reason only of the act.

(5) Where:

(a) the act was necessary to protect the safety of a person or to preserve property; or

(b) it was not reasonably possible for the insured or other person not to do the act;

the insurer may not refuse to pay the claim by reason only of the act.

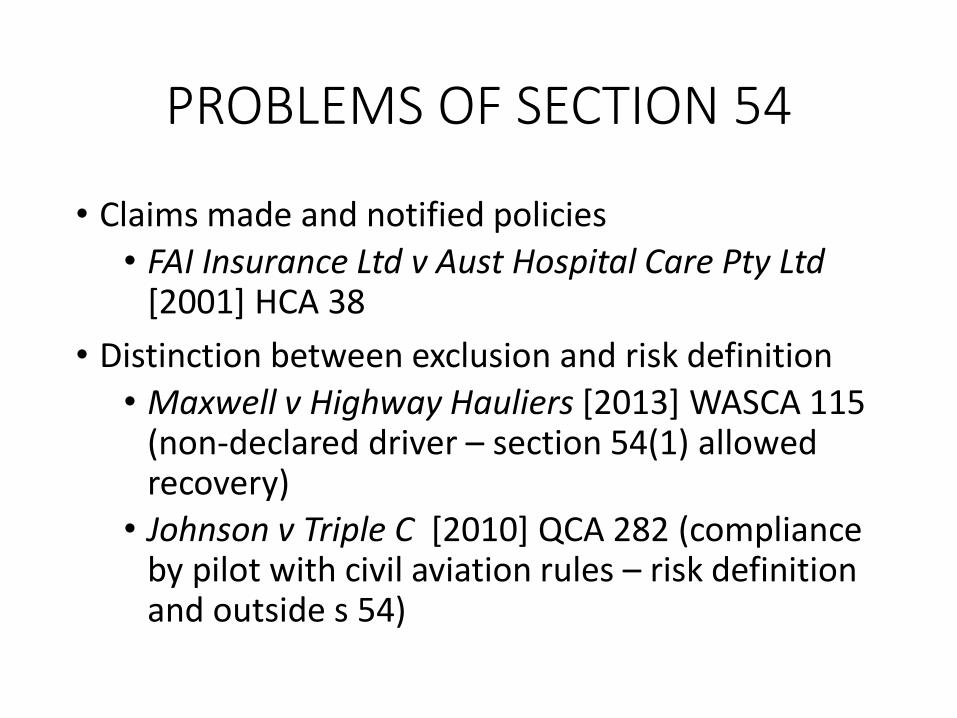

PROBLEMS OF SECTION 54

• Claims made and notified policies

• FAI Insurance Ltd v Aust Hospital Care Pty Ltd [2001] HCA 38

• Distinction between exclusion and risk definition

• Maxwell v Highway Hauliers [2013] WASCA 115 (non-declared driver – section 54(1) allowed recovery)

• Johnson v Triple C [2010] QCA 282 (compliance by pilot with civil aviation rules – risk definition and outside s 54)