testing and extending the capital asset pricing model

TRANSCRIPT

Testing and Extending the Capital Asset

Pricing Model

Gabriel Koh, Diana Kleinknecht, Paolo Parziano, Lei Peng

IB9Y8 Asset Pricing Group 14

MSc Finance

List of Contents

Abstract ................................................................................................................................................... 1

Introduction ............................................................................................................................................. 1

Literature Review .................................................................................................................................... 2

Data Description ...................................................................................................................................... 3

Methodology ........................................................................................................................................... 3

Two-Stage Regression ......................................................................................................................... 3

Rolling Window Regression ................................................................................................................. 4

Jarque-Bera Normality Test ................................................................................................................. 5

Testing of Pricing in Idiosyncratic Risk ................................................................................................ 5

Testing of Linearity in CAPM ............................................................................................................... 6

Wald test ............................................................................................................................................. 6

Gibbons, Ross, and Shanken test ........................................................................................................ 7

Empirical Results ..................................................................................................................................... 8

Testing the Capital Asset Pricing Model (CAPM) ................................................................................. 8

Finding Anomalies in the CAPM .......................................................................................................... 9

Explanatory Power of Risk Factors .................................................................................................... 10

Correlation between Pricing Errors and Firm Characteristics ........................................................... 12

Building and Testing “Factor-Mimicking Portfolios” ......................................................................... 13

Caveats and Limitations ........................................................................................................................ 15

Conclusion ............................................................................................................................................. 16

References ............................................................................................................................................. 17

IB9Y8 Asset Pricing Group 14

MSc Finance 1

Abstract

This paper attempts to prove whether the conventional Capital Asset Pricing Model (CAPM)

holds with respect to a set of asset returns. Starting with the Fama-Macbeth cross-sectional

regression, we prove through the significance of pricing errors that the CAPM does not hold.

Hence, we expand the original CAPM by including risk factors and factor-mimicking portfolios

built on firm-specific characteristics and test for their significance in the model. Ultimately, by

adding significant factors, we find that the model helps to better explain asset returns, but

does still not entirely capture pricing errors.

Introduction

A central economic, but still not completely answered question in the field of finance, is why

different assets earn substantially different returns on average. In this paper, we empirically

examine a given set of data in the context of different aspects of asset pricing theory. Based

on the given data, we first apply a two-stage regression approach (Cochrane, 2001), as well

as the Fama-MacBeth rolling window procedure (1973), to test for the validity of the Capital

Asset Pricing Model (CAPM). We find that assets have an inherent pricing error (𝛼𝑘 ≠ 0) and

that there exists a risk premium which is not explained by the market. Additionally, we find that

idiosyncratic risk is not priced and that the CAPM is indeed linear. In order to improve the

explanatory power of the cross-section of returns and hence reduce pricing errors, we

individually test the significance of two additional risk factors. We then regress the pricing

errors on two anonymous firm characteristics and create a factor-mimicking portfolio for the

significant characteristic.

From our results, we find that although the one risk factor and factor-mimicking portfolio are

significant in explaining pricing errors, the Gibbons, Ross and Shanken (GRS) test shows that

the pricing errors are still jointly not equal to zero.

The paper is organised as follows. First, we conduct a brief literature review with respect to the

development of asset pricing models. In the following, we give a comprehensive description of

the data, methodology, and empirical results. Finally, we evaluate our paper by discussing

some of the caveats and limitations.

IB9Y8 Asset Pricing Group 14

MSc Finance 2

Literature Review

Sharpe (1964) and Lintner (1965) were the first to develop the CAPM, which marks the

beginning of asset pricing theory. The CAPM builds on the model of portfolio choice as

suggested by Markowitz (1959). This model assumes investors to be risk averse and

consequently investors only choose mean-variance-efficient portfolios. Building on this

assumption, Sharpe (1964) states that in equilibrium, if all investors act rationally, assets can

be priced by only considering a market risk factor in the model. The risk premium earned by

an asset is proportional to the asset’s exposure to systematic risk, which is captured by the

asset’s market beta. Idiosyncratic or firm specific risk should not be priced as it can be

eliminated by holding a well-diversified portfolio. However, the literature finds evidence of the

existence of a pricing-error in the model, the so called Jensen’s Alpha (Jensen, 1968). The

pricing error is defined as the difference between the realised return of a stock and its predicted

return according to the CAPM. If the model holds, one would expect the average pricing errors

across assets to be zero, which is often not the case (Harvey, 1988).

Assuming that the market risk premium alone cannot sufficiently capture variations in asset

returns, and acknowledging the presence of anomalies in the CAPM, other researchers

extended the original CAPM model by adding various factors into the model. Basu (1977) finds

evidence that future returns on stocks with high P/E ratio are higher than predicted by the

CAPM, when sorted on their P/E ratio.

Fama and French (1993) accounts for size, book-to-market ratio, leverage and earnings-to-

price ratio in their model. They find that size and book-to-market (B/M) help to better explain

the cross-section of average returns. Banz (1981) also finds that average returns on small

stocks are higher. Furthermore, Rosenberg, Reid and Lanstein (1985), as well as Stattman

(1980) conclude that stocks with high B/M ratio earn higher premiums.

Stemming from the work of Hendricks, Patel & Zeckhauser (1993), Carhart (1997) added a

fourth factor, the so called momentum factor, to the Fama-French three-factor model. The

factor is constructed by forming diversified portfolios that long “winner” and short “loser” stocks.

In their most recent model, Fama and French (2015) extend their three-factor model to a five-

factor model, including a factor that accounts for the profitability and investment level of a firm.

Their results show that high operating profitability and high investments explain excess returns.

Hou, Xue and Zhang (2015) find similar results. According to them, a model which includes

IB9Y8 Asset Pricing Group 14

MSc Finance 3

the market factor, a size factor, a profitability factor, as well as an investment factor improve

the model in capturing anomalies of the CAPM than the Fama-French three-factor model.

As shown above, there exists a great amount of literature which provides evidence that the

original CAPM might not be the best model to explain the cross-section of expected returns,

and factors other than systematic risk might affect asset pricing.

Data Description

The data set used for the analysis in this paper contains monthly returns on the stock prices

of 50 firms for a sample period of 20 years, which adds up to a total of 12,000 observations. In

this paper, we assume that the stock prices are stationary, therefore there should not be any

spurious regression.

The market return for each period is calculated using an equally weighted portfolio of the 50

assets. In addition to the returns for each of the 50 firms, two firm-specific characteristics, are

taken into consideration. These two characteristics vary not only in the cross-section, but they

are also time-varying for each firm. Moreover, the analysis takes monthly observations for two

risk factors into account. These risk factors are considered to be seen as returns on portfolios

or trading strategies.

Methodology

Two-Stage Regression

To effectively estimate the efficiency of the CAPM model, we start running the two-stage

regression to test the CAPM (Fama and Macbeth, 1973), which we will use throughout this

report. Our procedure starts by regressing the returns of assets on market returns to obtain

the individual estimates of each asset.

𝑅𝑒𝑡𝑢𝑟𝑛𝑡,𝑘 − 𝑅𝑖𝑠𝑘𝑓𝑟𝑒𝑒 = 𝛼𝑘 + 𝛽𝑘𝑚(𝑀𝑎𝑟𝑘𝑒𝑡𝑅𝑒𝑡𝑢𝑟𝑛𝑡 − 𝑅𝑖𝑠𝑘𝑓𝑟𝑒𝑒) + 𝜖𝑡,𝑘 (𝐻1)

Where:

𝑅𝑒𝑡𝑢𝑟𝑛𝑡,𝑘 - Return on asset k in period t

𝑅𝑖𝑠𝑘𝑓𝑟𝑒𝑒 - Risk-free rate

𝛼𝑘: - Constant term

𝛽𝑘𝑚: - Factor loading of market portfolio

𝑀𝑎𝑟𝑘𝑒𝑡𝑅𝑒𝑡𝑢𝑟𝑛𝑡 - Market return in period t

𝜖𝑡: - Residual terms in period t

IB9Y8 Asset Pricing Group 14

MSc Finance 4

Given that the risk-free rate is zero in our analysis (as specified in the task), we can modify the

model:

𝑅𝑒𝑡𝑢𝑟𝑛𝑡,𝑘 = 𝛼𝑘 + 𝛽𝑘𝑚𝑀𝑎𝑟𝑘𝑒𝑡𝑅𝑒𝑡𝑢𝑟𝑛𝑡 + 𝜖𝑡,𝑘 (𝐻2)

Furthermore, we assume that residuals are:

1. Uncorrelated across assets and hence, cov(𝜖𝑗, 𝜖𝑘) = 0, for j ≠ k

2. Uncorrelated with factors and hence, 𝑐𝑜𝑣(𝐹𝑗 , 𝜖𝑘) = 0, ∀ j and k.

The first stage of the two-stage regression is a time-series regression. We run the time series

by regressing each of our 50 assets from month 1 to 240 on the market portfolio. From this we

will obtain a set of 50 estimates of alpha (�̂�𝑘) and beta (�̂�𝑘𝑚) which captures the sensitivity of

asset return to monthly changes in the market portfolio.

Next, by regressing the average asset returns (i.e. �̂�𝑘 =1

𝑇∑ 𝑅𝑒𝑡𝑢𝑟𝑛𝑘,𝑡

𝑇𝑡=1 ) on the betas of the

market (H3), we obtain the estimates of the gamma values (𝛾0 & �̂�1) which are the average

pricing error and the market risk premium respectively.

�̂�𝑘 = 𝛾0 + 𝛾1�̂�𝑘𝑚 + 𝜀𝑘 (𝐻3)

We conduct a hypothesis test on 𝛾1 with the following hypotheses:

H0: 𝛾0 = 0, 𝛾1 = 𝑚𝑎𝑟𝑘𝑒𝑡 𝑟𝑖𝑠𝑘 𝑝𝑟𝑒𝑚𝑖𝑢𝑚

H1: 𝑜𝑡ℎ𝑒𝑟𝑤𝑖𝑠𝑒

If we can reject the null hypothesis, it implies that asset returns are not fully explained by

variations in the market and we can conclude that the CAPM does not hold.

Rolling Window Regression

In the two-stage regression as described above, we assume that the betas are constant over

the entire period of estimation. Yet, this assumption is usually violated as the sensitivities of

each asset changes over time. Hence, we implement the rolling window regression which

Fama and MacBeth (1973) as well as Petkova and Zhang (2005) use to improve and account

for the variations in beta.

IB9Y8 Asset Pricing Group 14

MSc Finance 5

We use the first 60 months as the window to estimate the betas for each of the assets and

then roll the window forward for one period, i.e. for one month. In each period we rebalance

the portfolios to account for the variation across time. Following that, we regress the asset

returns on the betas and obtain a set of gammas. We test if �̅�0 is significantly different from

zero using a normal t test. If the null hypothesis can be rejected, we conclude that the CAPM

does not hold.

Jarque-Bera Normality Test

We perform the Jarque-Bera normality test (Jarque and Bera, 1980) to ensure that the errors

follow a normal distribution to successfully perform hypothesis testing.

Hypothesis:

H0: Errors follow a normal distribution

H1: Otherwise

The Jarque-Bera (JB) test statistic:

𝐽𝐵 =𝑛 − 𝑘 + 1

6(𝑆2 +

1

4(𝐶 − 3)2) ~ 𝜒2

2 (𝐻4)

Where:

N - Number of observations

S - Sample skewness

C - Sample kurtosis

K . Number of regressors

Testing of Pricing in Idiosyncratic Risk

Following Fama-MacBeth (1973), we test for anomalies in the CAPM and modify the cross-

section to include the idiosyncratic risk.

�̂�𝑘 = 𝛾0 + 𝛾1𝛽𝑘𝑚 + 𝛾2𝜎2(𝜖𝑘) + 𝜀𝑘 (𝐻5)

We perform a standard t test on 𝛾2. If 𝛾2 is not equal to zero, we can conclude that idiosyncratic

risk is priced i.e. idiosyncratic risk carries risk premium.

IB9Y8 Asset Pricing Group 14

MSc Finance 6

Testing of Linearity in CAPM

Fama-MacBeth (1973), also check if the CAPM is indeed linear. Hence, we add the beta

squared term into the cross section to account for non-linearity.

�̂�𝑘 = 𝛾0 + 𝛾1𝛽𝑘𝑚 + 𝛾2𝛽𝑘

𝑚2+ 𝜀𝑘 (𝐻6)

As above, we perform a standard t test. If 𝛾2 is not equal to zero, we can conclude that the

relationship between risk premium and beta is not linear.

Wald test

In order to test if CAPM works, we use the Wald test (MacBeth, 1975) to determine whether

all pricing errors (𝛼𝑘) are jointly equal to zero. The Wald test statistic is valid asymptotically

and does not require the errors to be normal, instead it relies on the central limit theorem so

that �̂�𝑘 is normally distributed. The test assumes no autocorrelation or heteroskedasticity. We

test the following hypotheses:

H0: 𝛼1 = 𝛼2 = ⋯ = 𝛼𝑘 = 0

H1: Otherwise

Wald test statistic

𝑇 [1 + (𝐸(𝛼)

�̂�(𝛼))

2

]

−1

�̂�′(∑̂)−1

�̂� ~ 𝜒𝑁2 (𝐻7)

Where:

𝐸(𝛼) - Sample mean

�̂�(𝛼) - Sample variance

�̂� - Vector of estimated intercepts

∑̂ - Residual covariance matrix i.e. the sample estimate of 𝐸(𝜖𝑡𝜖𝑡′) = ∑

IB9Y8 Asset Pricing Group 14

MSc Finance 7

Gibbons, Ross, and Shanken test

Given the assumptions in the Wald test, we use the Gibbons, Ross, and Shanken test to test

if pricing errors (𝛼𝑘) are jointly equal to zero (Gibbons, Ross, and Shanken, 1989). The

Gibbons, Ross, and Shanken (GRS) test statistic follows a F distribution.

The F distribution recognises sampling variations in the residual covariance matrix, which was

not accounted for in H6 (see Cochrane, 2001).

Hypothesis:

H0: 𝛼1 = 𝛼2 = ⋯ = 𝛼𝑘 = 0

H1: Otherwise

GRS test statistics

(𝑇

𝑁) (

𝑇 − 𝑁 − 1

𝑇 − 𝐿 − 1) [

�̂�′(∑̂)−1

�̂�

1 + �̅�′(Ω̂)−1

�̅�] ~ 𝐹𝑁,𝑇−𝑁−1 (𝐻8)

Where,

�̂� is a 𝑁 𝑥 1 vector of estimated intercepts

∑̂ is an unbiased estimate of the residual covariance matrix

�̅� is a 𝐿 𝑥 1 vector of the factor portfolios’ sample means

Ω̂ is an unbiased estimate of the factor portfolios’ covariance matrix

The GRS test requires the errors to be normally distributed as well as uncorrelated and

homoscedastic. This distribution is exact in a finite sample.

IB9Y8 Asset Pricing Group 14

MSc Finance 8

Empirical Results Testing the Capital Asset Pricing Model (CAPM)

Two-Stage Regression

𝑅𝑒𝑡𝑢𝑟𝑛𝑡,𝑘 = 𝛼𝑘 + 𝛽𝑘𝑚𝑀𝑎𝑟𝑘𝑒𝑡𝑅𝑒𝑡𝑢𝑟𝑛𝑡 + 𝜖𝑡,𝑘 (𝑀1)

�̂�𝑘 = 𝛾0 + 𝛾1𝛽𝑘𝑚 + 𝜀𝑘 (𝑀2)

Wald test

H0: 𝛼𝑘 is jointly equal to zero

H1: otherwise

Test statistic: 𝑇 [1 + (𝐸(𝛼)

�̂�(𝛼))

2

]−1

�̂�′(∑̂)−1

�̂� ~ 𝜒𝑁2

The Wald test statistic gives us a value of 0.1613 with a p-value of 0.000. Hence, we can reject

our null hypothesis that the alphas are jointly equal to zero and conclude that the CAPM does

not hold.

We then go one step further and analyse the significance of 𝛾0 in Table 1 below.

Table 1: Regression results for M2

Model 𝜸𝟎 𝜸𝟏 R2

M2 0.0021** (0.0230)

0.0065*** (0.0000)

0.6804

*** - 1%, ** - 5%, * - 10% significance level

We also test the error terms for normality using the Jarque-Bera (JB) test to ensure that we

can do hypothesis testing on the results. The JB test fails to reject the null hypothesis at the

5% significance level and thus we conclude that the error terms are normally distributed at the

5% significance level. Visually, this can be seen in Figure G1.

IB9Y8 Asset Pricing Group 14

MSc Finance 9

Our results show that 𝛾0 is significant at the 5% level which should not be the case if indeed

we do expect the CAPM to hold. Hence, we reject the null hypothesis H0: 𝛾0 = 0 and conclude

the CAPM does not hold.

Rolling window regression

In the above regression, we assumed that betas do not vary over time. Yet betas may change

and we must account for these variations. Hence, we use the rolling window to estimate the

beta for each firm at each period. We then regress these betas and obtain a set of 𝛾0 and 𝛾1.

We perform a t test on the average of these estimates 𝛾0̂ to test if it is statistically different from

zero.

The results show a t statistic of -3590 which we reject at the 1% significance level. Hence, we

conclude that even if we account for the variations in beta, the CAPM does not hold.

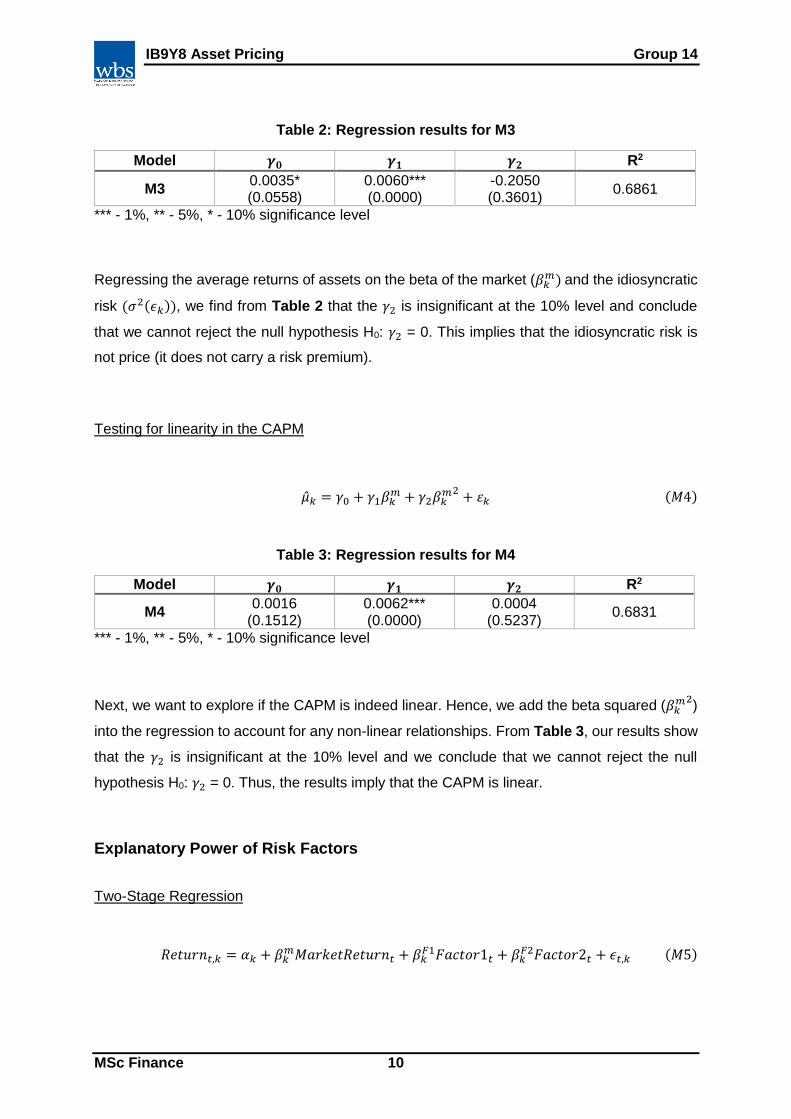

Finding Anomalies in the CAPM

Testing correlation between asset returns and idiosyncratic risk

�̂�𝑘 = 𝛾0 + 𝛾1𝛽𝑘𝑚 + 𝛾2𝜎2(𝜖𝑘) + 𝜀𝑘 (𝑀3)

IB9Y8 Asset Pricing Group 14

MSc Finance 10

Table 2: Regression results for M3

Model 𝜸𝟎 𝜸𝟏 𝜸𝟐 R2

M3 0.0035* (0.0558)

0.0060*** (0.0000)

-0.2050 (0.3601)

0.6861

*** - 1%, ** - 5%, * - 10% significance level

Regressing the average returns of assets on the beta of the market (𝛽𝑘𝑚) and the idiosyncratic

risk (𝜎2(𝜖𝑘)), we find from Table 2 that the 𝛾2 is insignificant at the 10% level and conclude

that we cannot reject the null hypothesis H0: 𝛾2 = 0. This implies that the idiosyncratic risk is

not price (it does not carry a risk premium).

Testing for linearity in the CAPM

�̂�𝑘 = 𝛾0 + 𝛾1𝛽𝑘𝑚 + 𝛾2𝛽𝑘

𝑚2+ 𝜀𝑘 (𝑀4)

Table 3: Regression results for M4

Model 𝜸𝟎 𝜸𝟏 𝜸𝟐 R2

M4 0.0016

(0.1512) 0.0062*** (0.0000)

0.0004 (0.5237)

0.6831

*** - 1%, ** - 5%, * - 10% significance level

Next, we want to explore if the CAPM is indeed linear. Hence, we add the beta squared (𝛽𝑘𝑚2

)

into the regression to account for any non-linear relationships. From Table 3, our results show

that the 𝛾2 is insignificant at the 10% level and we conclude that we cannot reject the null

hypothesis H0: 𝛾2 = 0. Thus, the results imply that the CAPM is linear.

Explanatory Power of Risk Factors

Two-Stage Regression

𝑅𝑒𝑡𝑢𝑟𝑛𝑡,𝑘 = 𝛼𝑘 + 𝛽𝑘𝑚𝑀𝑎𝑟𝑘𝑒𝑡𝑅𝑒𝑡𝑢𝑟𝑛𝑡 + 𝛽𝑘

𝐹1𝐹𝑎𝑐𝑡𝑜𝑟1𝑡 + 𝛽𝑘𝐹2𝐹𝑎𝑐𝑡𝑜𝑟2𝑡 + 𝜖𝑡,𝑘 (𝑀5)

IB9Y8 Asset Pricing Group 14

MSc Finance 11

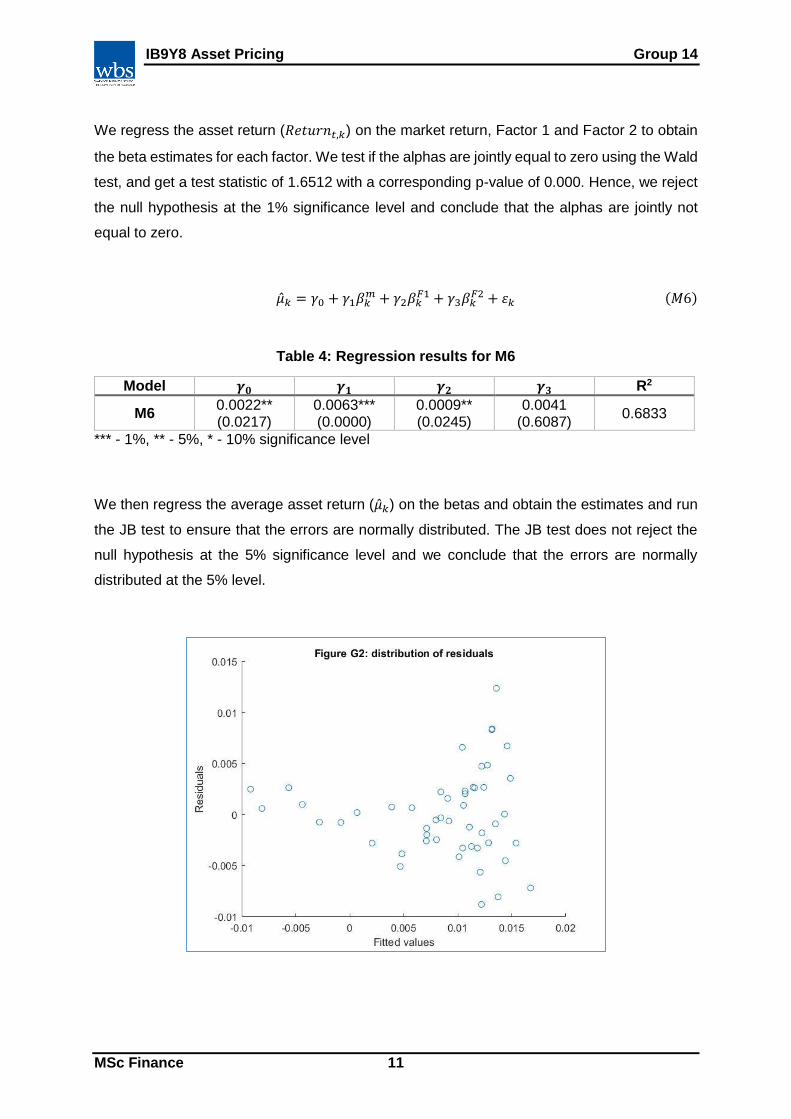

We regress the asset return (𝑅𝑒𝑡𝑢𝑟𝑛𝑡,𝑘) on the market return, Factor 1 and Factor 2 to obtain

the beta estimates for each factor. We test if the alphas are jointly equal to zero using the Wald

test, and get a test statistic of 1.6512 with a corresponding p-value of 0.000. Hence, we reject

the null hypothesis at the 1% significance level and conclude that the alphas are jointly not

equal to zero.

�̂�𝑘 = 𝛾0 + 𝛾1𝛽𝑘𝑚 + 𝛾2𝛽𝑘

𝐹1 + 𝛾3𝛽𝑘𝐹2 + 𝜀𝑘 (𝑀6)

Table 4: Regression results for M6

Model 𝜸𝟎 𝜸𝟏 𝜸𝟐 𝜸𝟑 R2

M6 0.0022** (0.0217)

0.0063*** (0.0000)

0.0009** (0.0245)

0.0041 (0.6087)

0.6833

*** - 1%, ** - 5%, * - 10% significance level

We then regress the average asset return (�̂�𝑘) on the betas and obtain the estimates and run

the JB test to ensure that the errors are normally distributed. The JB test does not reject the

null hypothesis at the 5% significance level and we conclude that the errors are normally

distributed at the 5% level.

IB9Y8 Asset Pricing Group 14

MSc Finance 12

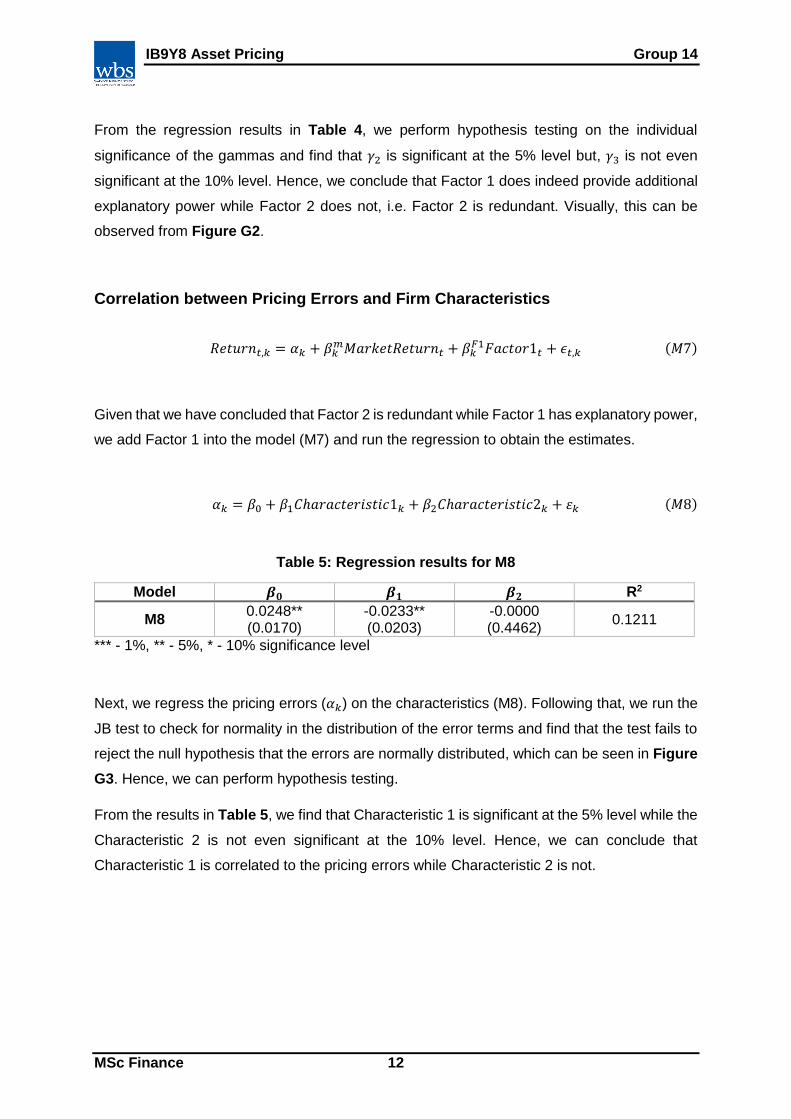

From the regression results in Table 4, we perform hypothesis testing on the individual

significance of the gammas and find that 𝛾2 is significant at the 5% level but, 𝛾3 is not even

significant at the 10% level. Hence, we conclude that Factor 1 does indeed provide additional

explanatory power while Factor 2 does not, i.e. Factor 2 is redundant. Visually, this can be

observed from Figure G2.

Correlation between Pricing Errors and Firm Characteristics

𝑅𝑒𝑡𝑢𝑟𝑛𝑡,𝑘 = 𝛼𝑘 + 𝛽𝑘𝑚𝑀𝑎𝑟𝑘𝑒𝑡𝑅𝑒𝑡𝑢𝑟𝑛𝑡 + 𝛽𝑘

𝐹1𝐹𝑎𝑐𝑡𝑜𝑟1𝑡 + 𝜖𝑡,𝑘 (𝑀7)

Given that we have concluded that Factor 2 is redundant while Factor 1 has explanatory power,

we add Factor 1 into the model (M7) and run the regression to obtain the estimates.

𝛼𝑘 = 𝛽0 + 𝛽1𝐶ℎ𝑎𝑟𝑎𝑐𝑡𝑒𝑟𝑖𝑠𝑡𝑖𝑐1𝑘 + 𝛽2𝐶ℎ𝑎𝑟𝑎𝑐𝑡𝑒𝑟𝑖𝑠𝑡𝑖𝑐2𝑘 + 𝜀𝑘 (𝑀8)

Table 5: Regression results for M8

Model 𝜷𝟎 𝜷𝟏 𝜷𝟐 R2

M8 0.0248** (0.0170)

-0.0233** (0.0203)

-0.0000 (0.4462)

0.1211

*** - 1%, ** - 5%, * - 10% significance level

Next, we regress the pricing errors (𝛼𝑘) on the characteristics (M8). Following that, we run the

JB test to check for normality in the distribution of the error terms and find that the test fails to

reject the null hypothesis that the errors are normally distributed, which can be seen in Figure

G3. Hence, we can perform hypothesis testing.

From the results in Table 5, we find that Characteristic 1 is significant at the 5% level while the

Characteristic 2 is not even significant at the 10% level. Hence, we can conclude that

Characteristic 1 is correlated to the pricing errors while Characteristic 2 is not.

IB9Y8 Asset Pricing Group 14

MSc Finance 13

Building and Testing “Factor-Mimicking Portfolios”

𝑅𝑒𝑡𝑢𝑟𝑛𝑡,𝑘 = 𝛼𝑘 + 𝛽𝑘𝑚𝑀𝑎𝑟𝑘𝑒𝑡𝑅𝑒𝑡𝑢𝑟𝑛𝑡 + 𝛽𝑘

𝐹𝑀𝐹𝑎𝑐𝑡𝑜𝑟𝑀𝑖𝑚𝑖𝑐𝑘𝑖𝑛𝑔𝑡 + 𝜖𝑡,𝑘 (𝑀9)

�̂�𝑘 = 𝛾0 + 𝛾1𝛽𝑘𝑚 + 𝛾2𝛽𝑘

𝐹𝑀 + 𝜀𝑘 (𝑀10)

𝑅𝑒𝑡𝑢𝑟𝑛𝑡,𝑘 = 𝛼𝑘 + 𝛽𝑘𝑚𝑀𝑎𝑟𝑘𝑒𝑡𝑅𝑒𝑡𝑢𝑟𝑛𝑡 + 𝛽𝑘

𝐹1𝐹𝑎𝑐𝑡𝑜𝑟1𝑡 + 𝛽𝑘𝐹𝑀𝐹𝑎𝑐𝑡𝑜𝑟𝑀𝑖𝑚𝑖𝑐𝑘𝑖𝑛𝑔𝑡 + 𝜖𝑡,𝑘 (𝑀11)

�̂�𝑘 = 𝛾0 + 𝛾1𝛽𝑘𝑚 + 𝛾2𝛽𝑘

𝐹1 + 𝛾3𝛽𝑘𝐹𝑀 + 𝜀𝑘 (𝑀12)

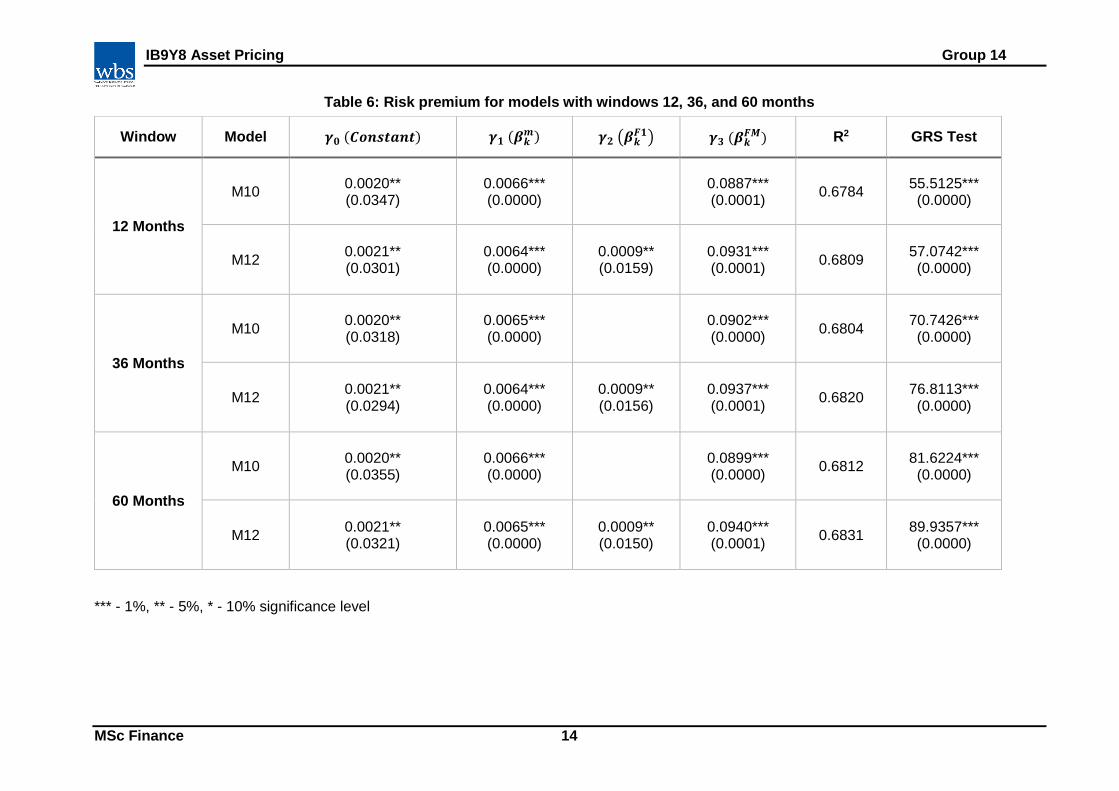

We estimate the betas for both model M9 and M11, using a window of 12, 36, and 60 months

while rebalancing the portfolio every month. Secondly, we regress the average returns on the

beta of the market and these betas to arrive at the models, M10 and M12. From Table 6, our

results show that for all six models we obtained significant results for all 𝛾’s at the 5% level and

1% level. This implies that the model is robust even though the window of estimating betas

change. Furthermore, we also show that the risk factor 1 is significant individually and jointly.

When we examine the R2 of these models, the R2 increases as our window increases from 12

months to 60 months for model M12, which has a value of 0.6809 and 0.6831 respectively.

This suggests that the rolling window estimation is better over 60 months instead of just 12

months.

Lastly, we assume that the error terms follow a normal distribution and conduct the GRS test

for alphas in M9 and M11. The GRS test show that we cannot conclude that the alphas in

these models are jointly equal to zero. Hence, this implies that pricing errors still exist in the

models and we need to add in relevant variables to explain the pricing errors.

IB9Y8 Asset Pricing Group 14

MSc Finance 14

Table 6: Risk premium for models with windows 12, 36, and 60 months

*** - 1%, ** - 5%, * - 10% significance level

Window Model 𝜸𝟎 (𝑪𝒐𝒏𝒔𝒕𝒂𝒏𝒕) 𝜸𝟏 (𝜷𝒌𝒎) 𝜸𝟐 (𝜷𝒌

𝑭𝟏) 𝜸𝟑 (𝜷𝒌𝑭𝑴) R2 GRS Test

12 Months

M10 0.0020** (0.0347)

0.0066*** (0.0000)

0.0887*** (0.0001)

0.6784 55.5125*** (0.0000)

M12 0.0021** (0.0301)

0.0064*** (0.0000)

0.0009** (0.0159)

0.0931*** (0.0001)

0.6809 57.0742*** (0.0000)

36 Months

M10 0.0020** (0.0318)

0.0065*** (0.0000)

0.0902*** (0.0000)

0.6804 70.7426*** (0.0000)

M12 0.0021** (0.0294)

0.0064*** (0.0000)

0.0009** (0.0156)

0.0937*** (0.0001)

0.6820 76.8113*** (0.0000)

60 Months

M10 0.0020** (0.0355)

0.0066*** (0.0000)

0.0899*** (0.0000)

0.6812 81.6224*** (0.0000)

M12 0.0021** (0.0321)

0.0065*** (0.0000)

0.0009** (0.0150)

0.0940*** (0.0001)

0.6831 89.9357*** (0.0000)

IB9Y8 Asset Pricing Group 14

MSc Finance 15

Caveats and Limitations

Earlier, we established two assumptions; error terms are not autocorrelated and no

heteroskedasticity exists. While we do perform the Jarque-Bera test for normality and ensure

that all error terms are normally distributed, i.e. implying that they are not autocorrelated, we

assumed that heteroskedasticity was not present. However, if the assumption was violated,

we would obtain inefficient estimators which may result in the increase in standard errors and

ultimately resulting in the t and F test being invalid.

Secondly, we assume that the stock prices in our data are stationary. However, if these are

indeed nonstationary, this may result in the problem of spurious regression where we

mistakenly fail to reject the factor risk premiums.

Thirdly, a salient limitation in our analysis of the two-stage regression is that the cross-section

regression implicitly assumes that betas do not vary in time. Fama-MacBeth (1973) argues

that by using a rolling window regression we can circumvent this issue. However, the main

drawback of the rolling window regression is that by rebalancing the portfolio we inevitably

overfit the model. This may result in the factor being significant even though it may not actually

be relevant in explaining returns.

Next, when using the rolling window to estimate the factor mimicking portfolio, we rebalance

the portfolio every month and estimate the beta i.e. moving average. However, this may affect

our estimation of betas because we subject our estimation to changes in assets at every period

in our data. Additionally, we choose arbitrary windows (12, 36, and 60 months) to estimate our

betas. While this may account for the variations in beta, it has no economic meaning and is

just taken to represent 1, 3, and 5 years of asset prices.

Moreover, given that the factor-mimicking portfolios are pre-sorted based on their values, it

comes as no surprise that the risk premiums on these factors are significant. This may be

observed by a marginal increase in the R2, even when the factors are added into the model.

With respect to the Wald test, the distribution is assumed to be asymptotically valid. Yet, with

only 50 assets it is arguable that we do not have enough data to make the conjecture about

the validity of the assumptions. Hence, we should use a finite sample test, i.e. GRS test.

Lastly, in conducting the GRS test, we assume that the error terms are normally distributed.

However, this assumption may not hold and the hypothesis test may be invalid if error terms

do not follow a normal distribution.

IB9Y8 Asset Pricing Group 14

MSc Finance 16

Conclusion

In this paper, we have tested the validity of the CAPM using the two-stage regression and the

rolling window regression approach. We use the Wald test to jointly test the null hypothesis

that the pricing errors are equal to zero and show that the CAPM does not hold. Following

Fama-MacBeth (1973), we show that the idiosyncratic risk is not priced and that the CAPM is

linear. We regress the asset returns on the market returns and risk factors and find that only

the risk premia of Factor 1 is significant. Next, we regress pricing errors on the characteristics

and find that only Characteristic 1 is significant in explaining variations in the pricing errors.

We create the factor-mimicking portfolio and obtain the relevant betas and risk premiums.

Finally, we use the GRS test and observe that Factor 1 and the factor-mimicking portfolio do

not fully explain the pricing errors. Hence, we conclude that additional factors are required to

better explain the pricing errors.

IB9Y8 Asset Pricing Group 14

MSc Finance 17

References

Banz, R.W. (1981), “The Relationship between Return and Market Value of Common

Stocks”, Journal of Financial Economics, Vol. 9 No. 1, pp. 3–18.

Basu, S. (1977), “Investment Performance of Common Stocks in Relation to their Price‐

Earnings Ratios: A test of the efficient Market Hypothesis”, Journal of Finance, Vol. 32

No. 3, pp. 663–682.

Carhart, M.M. (1997), “On Persistence in Mutual Fund Performance”, Journal of Finance,

Vol. 52 No. 1, pp. 57–82.

Cochrane, J.H. (2001), Asset Pricing, Princeton, NJ: Princeton University Press.

Fama, E. and MacBeth, J. (1973), “Risk, Return, and Equilibrium: Empirical Tests”, Journal

of Political Economy, Vol. 81 No. 3, p. 607.

Fama, E.F. and French, K.R. (2015), “A Five-Factor Asset Pricing Model”, Journal of

Financial Economics, Vol. 116, pp. 1–22.

Gibbons, M., Ross, S.A. and Shanken, J., “A Test of the Efficiency of a given Portfolio”,

Econometrica: Journal of the Econometric Society, pp. 1121–1152.

Harvey, C.R. (1988), “The Real Term Structure and Consumption Growth”, Journal of

Financial Economics, Vol. 22 No. 2, pp. 305–333.

Hendricks, D., Patel, J. and Zeckhauser, R. (1993), “Hot Hands in Mutual Funds: Short‐Run

Persistence of Relative Performance, 1974–1988”, Journal of Finance, Vol. 48 No. 1, pp.

93–130.

Jarque, C.M. and Bera, A.K. (1980), “Efficient Tests for Normality, Homoscedasticity and

Serial Independence of Regression Residuals”, Economic letters, Vol. 6 No. 3, pp. 225–

259.

Jensen, M.C. (1968), “The Perfomance of Mutual Funds in the Period 1945-1964”, Journal of

Finance, Vol. 23, pp. 389–416.

IB9Y8 Asset Pricing Group 14

MSc Finance 18

Lintner, J. (1965), “The Valuation of Risk Assets and the Selection of Risky Investments in

Stock Portfolios and Capital Budgets”, Review of Economics & Statistics, Vol. 47 No. 1, p.

13.

MacBeth, J.D. (1975), Tests of the two parameter model of capital market equilibrium,

University of Chicago, Graduate School of Business.

Markowitz, H. (1959), “Portfolio Selection: Efficient Diversification of Investments”, Cowles

Foundation Monograph No. 16. New York: John Wiley & Sons, Inc.

Petkova, R. and Zhang, L. (2005), “Is Value riskier than Growth?”, Journal of Financial

Economics, Vol. 78 No. 1, pp. 187–202.

Rosenberg, B., Reid, K. and Lanstein, R. (1985), “Persuasive Evidence of Market

Inefficiency”, The Journal of Portfolio Management, Vol. 11 No. 3, pp. 9–16.

Sharpe, W.F. (1964), “Capital Asset Prices: A Theory of Market Equilibrium under Conditions

of Risk”, Journal of Finance, Vol. 19 No. 3, pp. 425–442.

Stattman, D. (1980), “Book Values and Stock Returns”, The Chicago MBA: A Journal of

Selected Papers, Vol. 4, pp. 25–45.