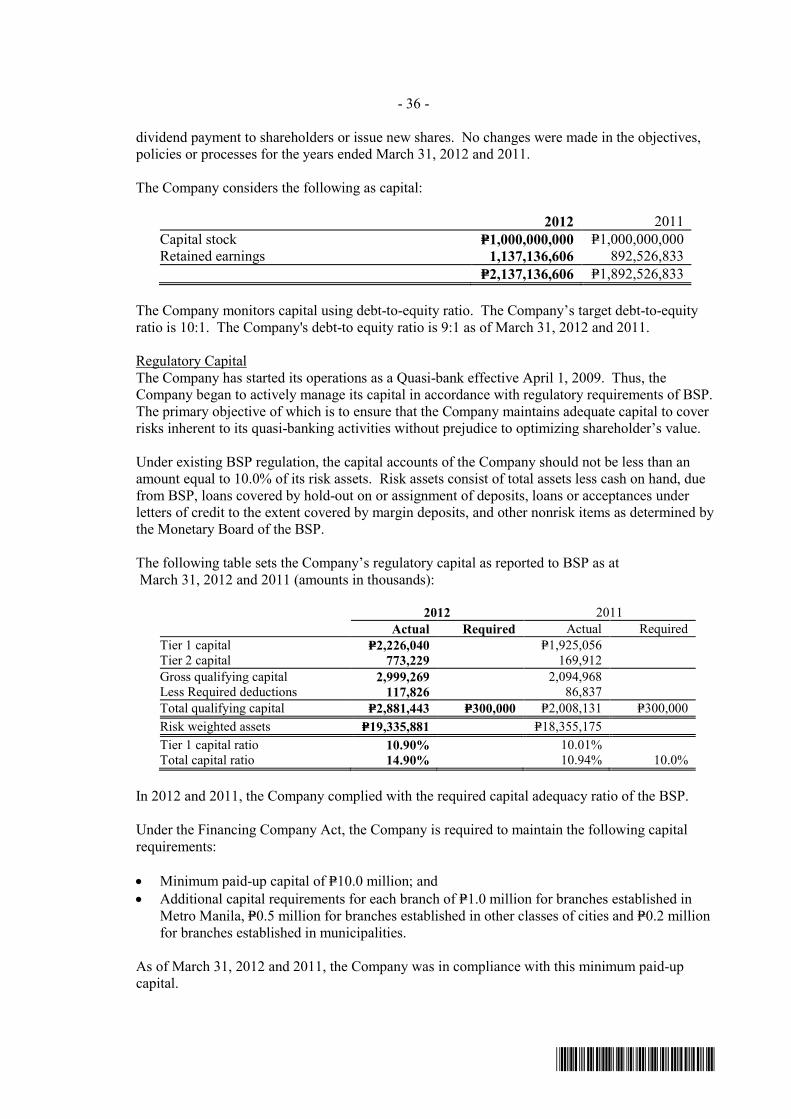

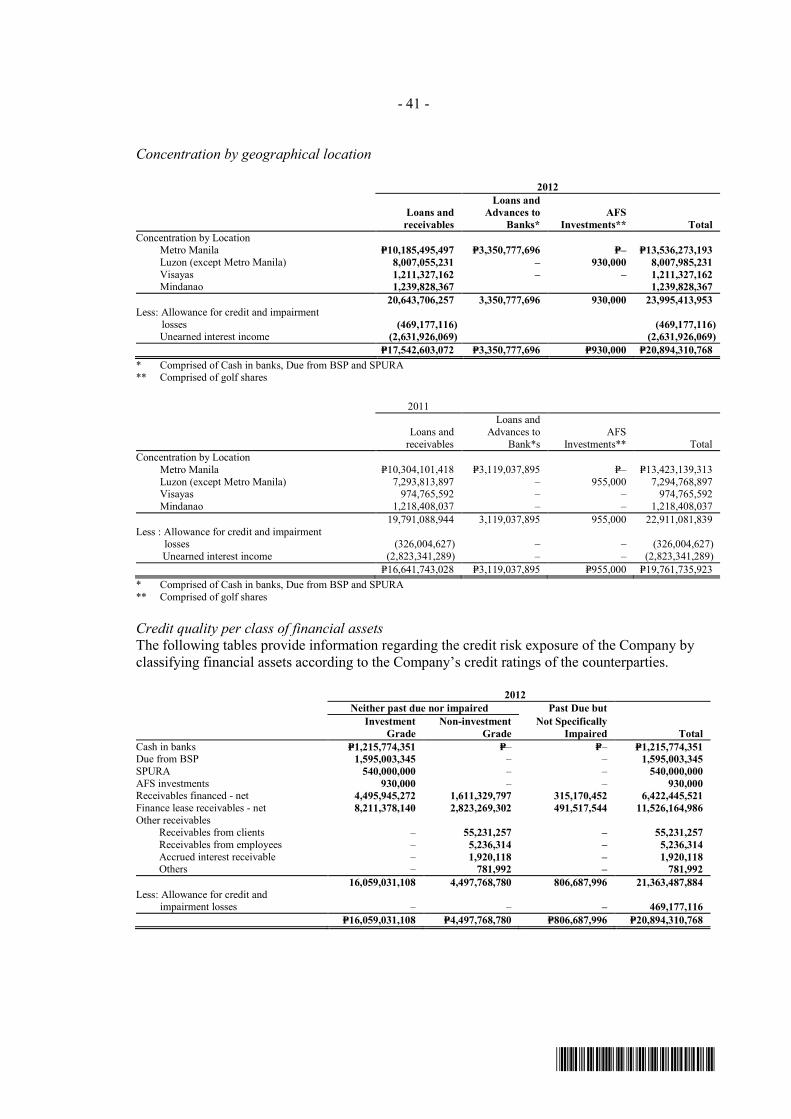

tfspc fs0312 toyota financial services philippines corporation€¦ · toyota financial services...

TRANSCRIPT

Toyota Financial Services Philippines Corporation

Financial Statements March 31, 2012 and 2011 and Independent Auditors’ Report SyCip Gorres Velayo & Co.

*SGVMC118066*

INDEPENDENT AUDITORS’ REPORT The Stockholders and the Board of Directors Toyota Financial Services Philippines Corporation Report on the Financial Statements We have audited the accompanying financial statements of Toyota Financial Services Philippines Corporation, which comprise the statements of financial position as at March 31, 2012 and 2011, and the statements of comprehensive income, statements of changes in equity and statements of cash flows for the years then ended, and a summary of significant accounting policies and other explanatory information. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with Philippine Financial Reporting Standards, and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error. Auditors’ Responsibility Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits in accordance with Philippine Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatements. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

SyCip Gorres Velayo & Co. 6760 Ayala Avenue 1226 Makati City Philippines

Phone: (632) 891 0307 Fax: (632) 819 0872 www.sgv.com.ph BOA/PRC Reg. No. 0001, January 25, 2010, valid until December 31, 2012 SEC Accreditation No. 0012-FR-2 (Group A), February 4, 2010, valid until February 3, 2013

A member firm of Ernst & Young Global Limited

*SGVMC118066*

- 2 - Opinion In our opinion, the financial statements present fairly, in all material respects, the financial position of Toyota Financial Services Philippines Corporation as at March 31, 2012 and 2011, and its financial performance and its cash flows for the years then ended in accordance with Philippine Financial Reporting Standards. Report on the Supplementary Information Required Under Revenue Regulations 19-2011 and 15-2010 Our audits were conducted for the purpose of forming an opinion on the basic financial statements taken as a whole. The supplementary information required under Revenue Regulations 19-2011 and 15-2010 in Note 28 to the financial statements is presented for purposes of filing with the Bureau of Internal Revenue and is not a required part of the basic financial statements. Such information is the responsibility of the management of the Company. The information has been subjected to the auditing procedures applied in our audit of the basic financial statements. In our opinion, the information is fairly stated in all material respects in relation to the basic financial statements taken as whole. SYCIP GORRES VELAYO & CO. Janet A. Paraiso Partner CPA Certificate No. 92305 SEC Accreditation No. 0778-AR-1 (Group A), February 2, 2012, valid until February 1, 2015 Tax Identification No. 193-975-241 BIR Accreditation No. 08-001998-62-2012, April 11, 2012, valid until April 10, 2015 PTR No. 3174578, January 2, 2012, Makati City July 4, 2012

*SGVMC118066*

TOYOTA FINANCIAL SERVICES PHILIPPINES CORPORATION STATEMENTS OF FINANCIAL POSITION March 31 2012 2011

ASSETS

Cash (Notes 4, 22, 23 and 25) P=1,216,209,838 P=1,221,471,063

Due from Bangko Sentral ng Pilipinas (Notes 4, 23 and 25) 1,595,003,345 1,690,041,380

Securities Purchased Under Resale Agreement (Note 5) 540,000,000 208,000,000

Available-for-Sale Investments (Notes 6, 23 and 25) 930,000 955,000

Loans and Receivables (Notes 7, 11, 23 and 25) 17,542,603,072 16,641,743,028

Assets Held for Sale (Note 8) 74,860,784 63,358,174

Property and Equipment (Note 9) 17,337,934 16,380,855

Software Costs (Note 10) 22,647,467 21,670,634

Deferred Tax Assets (Note 20) 113,392,599 88,857,053

Other Assets (Note 10) 21,700,434 11,298,236 P=21,144,685,473 P=19,963,775,423

LIABILITIES AND EQUITY

LIABILITIES

Loans Payable (Notes 12, 22, 23 and 25) P=14,408,406,141 P=15,549,334,873

Derivative Liability (Notes 15 and 23) 34,246,258 70,548,282

Accounts Payable and Other Liabilities (Notes 14, 22, 23, and 25) 550,013,206 411,907,333

Deposits on Lease Contracts (Note 16) 2,921,006,789 1,993,934,583

Subordinated Debt (Note 13) 996,239,534 –

Income Tax Payable 39,940,720 23,512,716 18,949,852,648 18,049,237,787

EQUITY

Capital Stock - P=100 par value Authorized, issued and outstanding - 10,000,000 shares

(Note 24) 1,000,000,000 1,000,000,000

Retained Earnings (Note 24) 1,137,136,606 892,526,833

Net Unrealized Gain on Available-for-Sale

Investments (Note 6) 120,000 45,000

Cash Flow Hedge Reserve (Note 15) 57,576,219 21,965,803 2,194,832,825 1,914,537,636 P=21,144,685,473 P=19,963,775,423 See accompanying Notes to Financial Statements.

*SGVMC118066*

TOYOTA FINANCIAL SERVICES PHILIPPINES CORPORATION STATEMENTS OF COMPREHENSIVE INCOME Years Ended March 31 2012 2011

INTEREST INCOME Loans and receivables (Note 7) P=1,681,753,792 P=1,594,479,822 Cash and cash equivalents (Notes 4 and 22) 69,777,148 96,970,933 1,751,530,940 1,691,450,755

INTEREST EXPENSE (Notes 12, 13 and 22) 871,324,497 926,500,660

NET INTEREST INCOME 880,206,443 764,950,095

SERVICE FEES AND OTHER INCOME (Note 18) 94,012,903 104,229,186

OPERATING EXPENSES Provision for credit and impairment losses (Notes 7, 8 and 11) 269,173,350 147,352,989 Taxes and licenses 108,935,058 110,631,053 Compensation and fringe benefits (Notes 19 and 22) 71,990,427 92,717,359 Occupancy (Note 21) 43,403,873 44,662,006 Sales and marketing 30,988,799 45,431,524 Litigation 28,693,957 23,261,859 Management and professional fees 16,987,702 16,496,025 Depreciation and amortization (Notes 9 and 10) 10,756,533 20,472,814 Entertainment, amusement and recreation (Note 20) 9,161,400 8,356,705 Credit investigation 8,350,866 10,798,807 Transportation and travel 6,087,398 5,370,346 Others 15,266,754 12,559,687 619,796,117 538,111,174

INCOME BEFORE INCOME TAX 354,423,229 331,068,107

PROVISION FOR INCOME TAX (Note 20) 109,813,456 103,433,869

NET INCOME 244,609,773 227,634,238

OTHER COMPREHENSIVE INCOME Net unrealized gain on available-for-sale investments 75,000 45,000 Net movement on cash flow hedges (Note 15) 50,872,023 11,956,004 Income tax effect (Note 20) (15,261,607) (3,586,801) 35,610,416 8,369,203 35,685,416 8,414,203

TOTAL COMPREHENSIVE INCOME P=280,295,189 P=236,048,441 See accompanying Notes to Financial Statements.

*SGVMC118066*

TOYOTA FINANCIAL SERVICES PHILIPPINES CORPORATION STATEMENTS OF CHANGES IN EQUITY

For the Years Ended March 31, 2012 and 2011

Capital Stock

(Note 24)

Retained Earnings (Note 24)

Net Unrealized Gain on

Available-for-Sale

Investments (Note 6)

Cash Flow Hedge Reserve

(Note 15) Total

Balances at April 1, 2011 P=1,000,000,000 P=892,526,833 P=45,000 P=21,965,803 P=1,914,537,636 Net income – 244,609,773 – – 244,609,773 Other comprehensive income – – 75,000 35,610,416 35,685,416 Total comprehensive income – 244,609,773 75,000 35,610,416 280,295,189 Balances at March 31, 2012 P=1,000,000,000 P=1,137,136,606 P=120,000 P=57,576,219 P=2,194,832,825

Balances at April 1, 2010 P=1,000,000,000 P=664,892,595 P=– P=13,596,600 P=1,678,489,195 Net income – 227,634,238 – – 227,634,238 Other comprehensive income – – 45,000 8,369,203 8,414,203 Total comprehensive income – 227,634,238 45,000 8,369,203 236,048,441 Balances at March 31, 2011 P=1,000,000,000 P=892,526,833 P=45,000 P=21,965,803 P=1,914,537,636 See accompanying Notes to Financial Statements.

*SGVMC118066*

TOYOTA FINANCIAL SERVICES PHILIPPINES CORPORATION STATEMENTS OF CASH FLOWS Years Ended March 31 2012 2011

CASH FLOWS FROM OPERATING ACTIVITIES Income before income tax P=354,423,229 P=331,068,107 Adjustments for: Provision for credit and impairment losses (Notes 7, 8 and 11) 269,173,350 147,352,989 Depreciation and amortization (Notes 9 and 10) 10,756,533 20,472,814

Loss (gain) on sale of assets held for sale (Notes 18 and 26) 9,349,983 (9,444,894) Gain on sale of property and equipment (1,005,875) (984,444) Changes in operating assets and liabilities: Decrease (increase) in: Loans and receivables (1,538,076,995) (4,482,338,606) Other assets (10,302,198) 6,884,146 Increase in: Deposits on lease contracts 927,072,206 1,192,524,712 Accounts payable and other liabilities 136,683,642 87,612,922 Net cash generated from (used for) operations 158,073,875 (2,706,852,254) Income taxes paid (131,760,374) (116,527,495) Net cash provided by (used in) operating activities 26,313,501 (2,823,379,749)

CASH FLOWS FROM INVESTING ACTIVITIES Acquisitions of: Property and equipment (Notes 9 and 26) (11,411,842) (2,243,852) Software (Note 10) (7,687,352) (7,572,403) Proceeds from sale of:

Assets held for sale 335,955,565 191,821,279 Property and equipment 18,650,067 5,890,225

Net cash provided by investing activities 335,506,438 187,895,249

CASH FLOWS FROM FINANCING ACTIVITIES Proceeds from availment of loans payable 9,690,385,114 10,502,838,642 Proceeds from issuance of subordinated debt 990,560,879 – Payments of loans payable (10,811,065,192) (7,337,320,093) Net cash provided by (used in) financing activities (130,119,199) 3,165,518,549

NET INCREASE IN CASH AND CASH EQUIVALENTS 231,700,740 530,034,049

CASH AND CASH EQUIVALENTS AT BEGINNING OF YEAR Cash 1,221,471,063 1,231,774,289 Due from Bangko Sentral ng Pilipinas 1,690,041,380 1,357,704,105 Securities Purchased Under Resale Agreement 208,000,000 – 3,119,512,443 2,589,478,394

(Forward)

*SGVMC118066*

- 2 - Years Ended March 31 2012 2011

CASH AND CASH EQUIVALENTS AT END OF YEAR Cash 1,216,209,838 1,221,471,063 Due from Bangko Sentral ng Pilipinas 1,595,003,345 1,690,041,380 Securities Purchased Under Resale Agreement 540,000,000 208,000,000 P=3,351,213,183 P=3,119,512,443 Years Ended March 31 2012 2011 OPERATIONAL CASH FLOWS FROM INTEREST Interest received P=1,560,144,656 P=2,341,358,034 Interest paid 870,976,113 856,109,875 See accompanying Notes to Financial Statements.

*SGVMC118066*

TOYOTA FINANCIAL SERVICES PHILIPPINES CORPORATION NOTES TO FINANCIAL STATEMENTS 1. Corporate Information

Toyota Financial Services Philippines Corporation (the Company) is a domestic corporation registered with the Securities and Exchange Commission (SEC) on August 16, 2002. The Company’s registered address is 32nd Floor, GT Tower International, Ayala Avenue corner H.V. Dela Costa St., Salcedo Village, Makati City.

The Company serves customers of Toyota vehicles through financing and leasing services, as well as Toyota dealers, through inventory stock financing. On May 8, 2008, the Monetary Board of the Bangko Sentral ng Pilipinas (BSP) granted the Company its quasi-banking license, which enables the Company to diversify its sources of funds, as well as offer a wider range of financing products to its growing customers and perform other quasi-banking functions effective April 1, 2009.

The following table sets forth the ownership structure of the Company:

Percentage of ownership Toyota Financial Services Corporation (TFSC) 60% Philippine Savings Bank (PSBank) 25% Metropolitan Bank and Trust Company (MBTC) 15%

The Company’s ultimate parent company is TFSC, a leading financial services company based in Japan.

The accompanying financial statements were approved and authorized for issue by the Board of Directors (BOD) on July 4, 2012.

2. Summary of Significant Accounting Policies

Basis of Preparation The accompanying financial statements of the Company have been prepared using the historical cost basis except for available-for-sale (AFS) investments and derivative financial instruments, which have been measured at fair value.

The accompanying financial statements are presented in Philippine peso (P=), which is also the Company’s functional currency.

All values are rounded to the nearest peso unless otherwise stated.

Statement of Compliance The financial statements of the Company have been prepared in compliance with Philippine Financial Reporting Standards (PFRS).

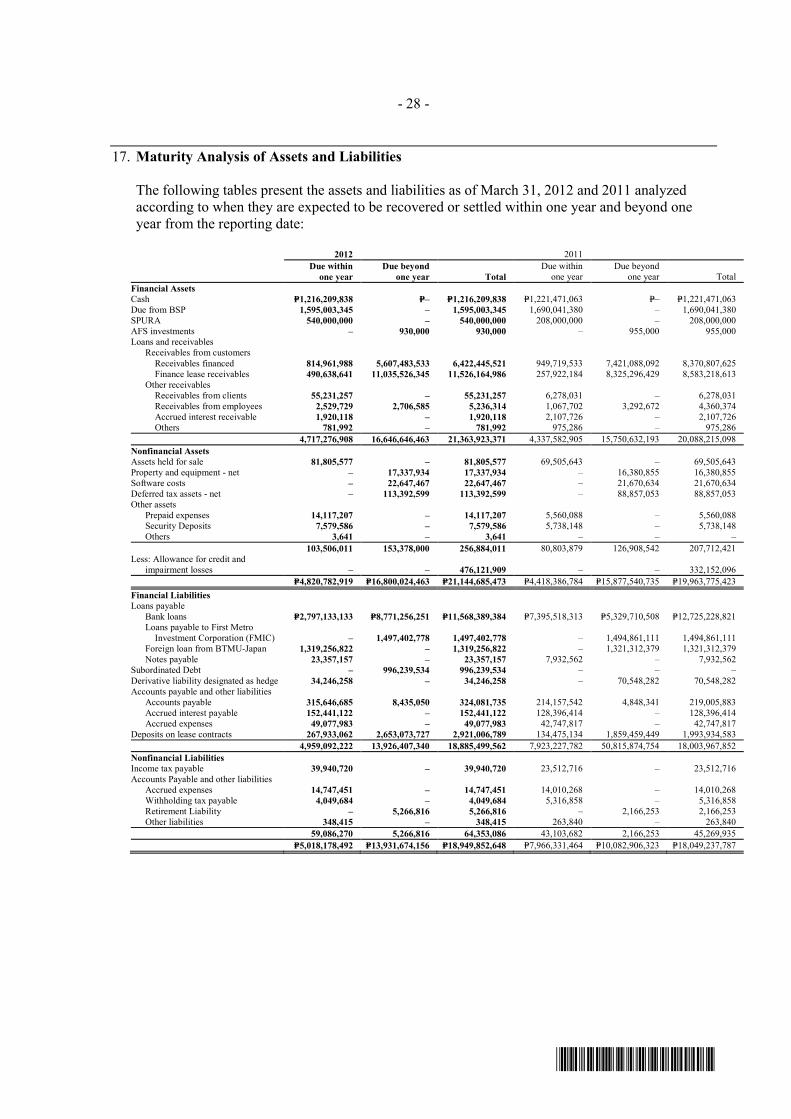

Presentation of Financial Statements The Company presents its statement of financial position broadly in order of liquidity. An analysis regarding recovery or settlement within 12 months after the statement of financial position date (current) and more than 12 months after the statement of financial position date (non-current) is presented in Note 17.

- 2 -

*SGVMC118066*

Changes in Accounting Policies and Disclosures The accounting policies adopted are consistent with those of the previous year except for the following new and amended standards, interpretations and improvements to PFRS adopted as of April 1, 2011. These new and amended standards and improvements to PFRS did not have any impact on the accounting policies, financial position or performance of the Company.

New and Amended Standards and Interpretations • Philippine Accounting Standard (PAS) 24, Related Party Disclosures (Amendment) • PAS 32, Financial Instruments: Presentation (Amendment) • Philippine Interpretation of International Financial Reporting Interpretation Committee

(IFRIC) 14, Prepayments of a Minimum Funding Requirement (Amendment) • Philippines Interpretation IFRIC 19, Extinguishing Financial Liabilities with Equity

Instruments • Philippine Interpretation IFRIC 13, Customer Loyalty Programmes (determining the fair value

of award credits)

Improvements to PFRS in 2010 • PFRS 3, Business Combinations • PFRS 7, Financial Instruments: Disclosures • PAS 1, Presentation of Financial Statements • PAS 27, Consolidated and Separate Financial Statements • PAS 34, Interim Financial Reporting

New standards and interpretations that have been issued but are not yet effective Standards or interpretations issued but are not effective as of March 31, 2012 are listed below. The Company intends to adopt these standards and interpretations when they become effective. Except as otherwise stated, the Company does not expect the adoption of these new standards and interpretations to have a significant impact on its financial statements.

• PAS 1, Financial Statement Presentation - Presentation of Items of Other Comprehensive

Income (Amendment), effective for annual periods beginning on or after July 1, 2012. The amendments to PAS 1 change the grouping of items presented in other comprehensive income (OCI). Items that could be reclassified (or “recycled”) to profit or loss at a future point in time (for example, upon derecognition or settlement) would be presented separately from items that will never be reclassified.

• PAS 12, Income Taxes - Recovery of Underlying Assets (Amendment), effective for annual

periods beginning on or after January 1, 2012. It clarified the determination of deferred tax on investment property measured at fair value. The amendment introduces a rebuttable presumption that deferred tax on investment property measured using the fair value model in PAS 40, Investment Property, should be determined on the basis that its carrying amount will be recovered through sale. Furthermore, it introduces the requirement that deferred tax on non-depreciable assets that are measured using the revaluation model in PAS 16, Property, Plant and Equipment, always be measured on a sale basis of the asset.

• PAS 19, Employee Benefits (Amendment), effective for annual periods beginning on or after

January 1, 2013. Amendments to PAS 19 range from fundamental changes such as removing the corridor mechanism and the concept of expected returns on plan assets to simple clarifications and rewording. The Company is currently assessing the impact of the amendment to PAS 19.

- 3 -

*SGVMC118066*

• PAS 27, Separate Financial Statements (as revised in 2011), effective for annual periods

beginning on or after January 1, 2013. As a consequence of the new PFRS 10, Consolidated Financial Statements, and PFRS 12, Disclosure of Interests in Other Entities, what remains of PAS 27 is limited to accounting for subsidiaries, jointly controlled entities, and associates in separate financial statements.

• PAS 28, Investments in Associates and Joint Ventures (as revised in 2011), effective for

annual periods beginning on or after January 1, 2012. As a consequence of the new PFRS 11, Joint Arrangements, and PFRS 12, PAS 28 has been renamed PAS 28, Investments in Associates and Joint Ventures, and describes the application of the equity method to investments in joint ventures in addition to associates.

• PFRS 7, Financial Instruments: Disclosures - Enhanced Derecognition Disclosure

Requirements, effective for annual periods beginning on or after January 1, 2012. The amendment requires additional disclosure about financial assets that have been transferred but not derecognized to enable the user of the Company’s financial statements to understand the relationship with those assets that have not been derecognized and their associated liabilities. In addition, the amendment requires disclosures about continuing involvement in derecognized assets to enable the user to evaluate the nature of, and risks associated with, the entity’s continuing involvement in those derecognized assets.

• PFRS 7, Financial Instruments: Disclosures - Offsetting Financial Assets and Financial

Liabilities. These amendments require an entity to disclose information about rights of set-off and related arrangements (such as collateral agreements). The new disclosures are required for all recognized financial instruments that are set off in accordance with PAS 32. These disclosures also apply to recognized financial instruments that are subject to an enforceable master netting arrangement or ‘similar agreement’, irrespective of whether they are set-off in accordance with PAS 32. The amendments require entities to disclose, in a tabular format unless another format is more appropriate, the following minimum quantitative information. This is presented separately for financial assets and financial liabilities recognized at the end of the reporting period:

a. The gross amounts of those recognized financial assets and recognized financial

liabilities; b. The amounts that are set off in accordance with the criteria in PAS 32 when determining

the net amounts presented in the statement of financial position; c. The net amounts presented in the statement of financial position; d. The amounts subject to an enforceable master netting arrangement or similar agreement

that are not otherwise included in (b) above, including: i. Amounts related to recognized financial instruments that do not meet some or all of

the offsetting criteria in PAS 32; and ii. Amounts related to financial collateral (including cash collateral); and

e. The net amount after deducting the amounts in (d) from the amounts in (c) above.

The amendments to PFRS 7 are to be retrospectively applied for annual periods beginning on or after January 1, 2013.

- 4 -

*SGVMC118066*

• PFRS 10, Consolidated Financial Statements, effective for annual periods beginning on or

after January 1, 2013. PFRS 10 replaces the portion of PAS 27, Consolidated and Separate Financial Statements, that addresses the accounting for consolidated financial statements. It also includes the issues raised in SIC-12, Consolidation - Special Purpose Entities. PFRS 10 establishes a single control model that applies to all entities including special purpose entities. The changes introduced by PFRS 10 will require management to exercise significant judgment to determine which entities are controlled, and therefore, are required to be consolidated by a parent, compared with the requirements that were in PAS 27.

• PFRS 11, Joint Arrangements, effective for annual periods beginning on or after

January 1, 2012. PFRS 11 replaces PAS 31, Interests in Joint Ventures, and SIC-13, Jointly-controlled Entities - Non-monetary Contributions by Venturers. PFRS 11 removes the option to account for jointly controlled entities (JCEs) using proportionate consolidation. Instead, JCEs that meet the definition of a joint venture must be accounted for using the equity method. This standard becomes effective for annual periods beginning on or after January 1, 2013.

• PFRS 12, Disclosure of Interests in Other Entities, effective for annual periods beginning on

or after January 1, 2013. PFRS 12 includes all of the disclosures that were previously in PAS 27 related to consolidated financial statements, as well as all of the disclosures that were previously included in PAS 31 and PAS 28. These disclosures relate to an entity’s interests in subsidiaries, joint arrangements, associates and structured entities. A number of new disclosures are also required.

• PFRS 13, Fair Value Measurement, effective for annual periods beginning on or after

January 1, 2013. PFRS 13 establishes a single source of guidance under PFRS for all fair value measurements. PFRS 13 does not change when an entity is required to use fair value, but rather provides guidance on how to measure fair value under PFRS when fair value is required or permitted.

• PFRS 9, Financial Instruments: Classification and Measurement, effective for annual periods

beginning on or after January 1, 2015. PFRS 9, as issued in 2010, reflects the first phase of the work on the replacement of PAS 39 and applies to classification and measurement of financial assets and financial liabilities as defined in PAS 39. In subsequent phases, hedge accounting and impairment of financial assets will be addressed with the completion of this project expected on the first half of 2012.

• PAS 32, Financial Instruments: Presentation - Offsetting Financial Assets and Financial

Liabilities. These amendments to PAS 32 clarify the meaning of ‘currently has a legally enforceable right to set-off’ and also clarify the application of the PAS 32 offsetting criteria to settlement systems (such as central clearing house systems) which apply gross settlement mechanisms that are not simultaneous. The amendments to PAS 32 are to be retrospectively applied for annual periods beginning on or after January 1, 2014.

• Philippine Interpretation IFRIC 15, Agreements for the Construction of Real Estate. This

interpretation covers accounting for revenue and associated expenses by entities that undertake the construction of real estate directly or through subcontractors. The interpretation requires that revenue on construction of real estate be recognized only upon completion, except when such contract qualifies as construction contract to be accounted for under

- 5 -

*SGVMC118066*

PAS 11, Construction Contracts, or involves rendering of services in which case revenue is recognized based on stage of completion. Contracts involving provision of services with the construction materials and where the risks and reward of ownership are transferred to the buyer on a continuous basis will also be accounted for based on stage of completion. SEC and the Financial Reporting Standards Council have deferred the effectivity of this interpretation until the final Revenue standard is issued by International Accounting and Standards Board and an evaluation of the requirements of the final revenue standard against the practices of the Philippine real estate industry is completed.

• Philippine Interpretation IFRIC 20, Stripping Costs in the Production Phase of a Surface

Mine, effective for annual periods beginning on or after January 1, 2013. This interpretation applies to waste removal costs that are incurred in surface mining activity during the production phase of the mine (‘production stripping costs’) and provides guidance on the recognition of production stripping costs as an asset and measurement of the stripping activity asset.

Significant Accounting Policies

Foreign Currency Translations Transactions denominated in foreign currencies are recorded using the applicable exchange rate at the date of the transaction. Foreign currency-denominated assets and liabilities are translated to Philippine peso using the Philippine Dealing System (PDS) closing rate prevailing at the reporting date. Foreign exchange gains or losses arising from foreign currency transactions and revaluation of foreign currency-denominated assets and liabilities are credited to or charged to profit or loss in the year in which the rates change.

Financial Instruments - Initial Recognition and Measurement Date of recognition Purchases or sales of financial assets that require delivery of assets within the time frame established by regulation or convention in the marketplace are recognized on the settlement date, the date that an asset is delivered to or by the Company. Deposits on finance lease, amounts due to banks and loans are recognized when cash is received by the Company or advanced to the borrowers.

Initial recognition of financial instruments All financial instruments are initially recognized at fair value. Except for financial assets and financial liabilities at fair value through profit or loss (FVPL), the initial measurement of financial assets includes transaction costs. The Company classifies its financial assets in the following categories: financial assets at FVPL, AFS investments, held-to-maturity (HTM) investments and loans and receivables. Financial liabilities are classified as financial liabilities at FVPL and other financial liabilities carried at amortized cost. Financial assets or financial liabilities at FVPL include financial assets or liabilities held for trading purposes and financial assets or liabilities designated upon initial recognition as at FVPL. The classification depends on the purpose for which the investments were acquired and whether they are quoted in an active market. Management determines the classification of its investments at initial recognition and, where allowed and appropriate, reevaluates such designation at every reporting date.

As of March 31, 2012 and 2011, the Company has no financial assets at FVPL and HTM investments.

- 6 -

*SGVMC118066*

Determination of fair value The fair value for financial instruments traded in active markets at the reporting date is based on their quoted market prices or dealer price quotations (bid price for long positions and ask price for short positions), without any deduction for transaction costs. When current bid and asking prices are not available, the price of the most recent transaction is used since it provides evidence of the current fair value as long as there has not been a significant change in economic circumstances since the time of the transaction.

For all other financial instruments not listed in an active market, the fair value is determined by using appropriate valuation techniques. Valuation techniques include net present value techniques, comparison to similar instruments for which market observable prices exist, and other relevant valuation models.

‘Day 1’ difference Where the transaction price in a non-active market is different from the fair value of other observable current market transactions in the same instrument or based on a valuation technique whose variables include only data from observable market, the Company recognizes the difference between the transaction price and fair value (a ‘Day 1’ difference) in profit or loss unless it qualifies for recognition as some other type of asset. In cases where use is made of data which is not observable, the difference between the transaction price and model value is only recognized in profit or loss when the inputs become observable or when the instrument is derecognized. For each transaction, the Company determines the appropriate method of recognizing the ‘Day 1’ difference amount.

AFS investments AFS investments are those which are designated as such or do not qualify to be classified as financial assets held for trading, designated at FVPL, HTM investments or loans and receivables. These are purchased and held indefinitely, and may be sold in response to liquidity requirements or changes in market conditions.

After initial measurement, AFS investments are subsequently measured at fair value. The unrealized gains and losses arising from the fair valuation of AFS investments are excluded, net of tax, from reported earnings and are reported as other comprehensive income in the statement of comprehensive income as ‘Net unrealized gain (loss) on available-for-sale investments,’ until the investment is derecognized or determined to be impaired at which time the cumulative gains or losses previously reported as other comprehensive income is included in profit or loss.

The Company’s AFS investments consist of golf club shares.

Loans and receivables Loans and receivables are non-derivative financial assets with fixed or determinable payments and fixed maturities that are not quoted in an active market. These are not entered into with the intention of immediate or short-term resale and as such are not classified as financial assets at FVPL and AFS investments. They also do not include those for which the company may not recover substantially as its initial investments, other than because of credit deterioration.

After initial measurement, loans and receivables are subsequently measured at amortized cost using the effective interest method less allowance for credit losses. Amortized cost is calculated by taking into account any discount or premium on acquisition cost and fees that are an integral

- 7 -

*SGVMC118066*

part of the effective interest rate (EIR). The amortization is included in profit or loss under “Interest income.” The losses arising from impairment are recognized in profit or loss under “Provision for credit and impairment losses.”

The Company’s loans and receivables consist of cash, due from BSP, SPURA, receivables from customers and other receivables.

Other financial liabilities Issued financial instruments or their components, which are not designated at FVPL, are classified as loans payable, accounts payable and other liabilities, deposits on lease contracts and subordinated debt where the substance of the contractual arrangement results in the Company having an obligation either to deliver cash or another financial assets to the holder, or to satisfy the obligation other than by the exchange of a fixed amount of cash or another financial asset for a fixed number of own equity shares.

After initial measurement, these financial liabilities not qualified as and not designated at FVPL are subsequently measured at amortized cost using the effective interest method.

Derivative Financial Instrument and Hedge Accounting The Company uses derivative financial instruments such as cross currency interest rate swap to hedge its foreign currency and interest rate risks. Such derivative financial instruments are initially recognized at fair value on the date in which a derivative transaction is entered into and are subsequently re-measured at fair value. Derivatives are carried as assets when the fair value is positive and as liabilities when the fair value is negative.

Any gains or losses arising from the changes in fair value of derivatives are taken directly to profit or loss, except for the effective portion of cash flow hedges, which is recognized as OCI.

For the purpose of hedge accounting, hedges are classified as:

• Fair value hedges when hedging the exposure to changes in the fair value of a recognized asset

or liability or an unrecognized firm commitment (except for foreign currency risk); • Cash flow hedges when hedging exposure to variability in cash flows that is either attributable

to a particular risk associated with a recognized asset or liability or a highly probable forecast transaction or the foreign currency risk in an unrecognized firm commitment; or

• Hedges of a net investment in a foreign operation.

At the inception of a hedge relationship, the Company formally designates and documents the hedge relationship to which the Company wishes to apply hedge accounting and the risk management objective and strategy for undertaking the hedge. The documentation includes identification of the hedging instrument, the hedged item or transaction, the nature of the risk being hedged and how the entity will assess the hedging instrument’s effectiveness in offsetting the exposure to changes in the hedge item’s fair value or cash flows attributable to the hedged risk. Such hedges are expected to be highly effective in achieving offsetting changes in fair value or cash flows and are assessed on an on-going basis to determine that they actually have been highly effective throughout the financial reporting periods for which they were designated.

Cash flow hedges The effective portion of the gain or loss on the hedging instrument is recognized directly as other comprehensive income in the cash flow hedge reserve, while the ineffective portion is recognized directly in profit or loss.

- 8 -

*SGVMC118066*

Amounts recognized as other comprehensive income are transferred to profit or loss, such as when the hedged financial income or financial expense is recognized or when a forecast sale occurs. Where the hedged item is the cost of a non-financial asset or non-financial liability, the amounts recognized as other comprehensive income are transferred to the initial carrying amount of the non-financial asset or liability.

If the forecast transaction or firm commitment is no longer expected to occur, the cumulative gain or loss previously recognized in other comprehensive income are transferred to profit or loss. If the hedging instrument expires or is sold, terminated or exercised without replacement or rollover or if its designation as a hedge is revoked, any cumulative gain or loss previously recognized in other comprehensive income remains in OCI until the forecast transaction or firm commitment affects profit or loss. If the related transaction is not expected to occur, the amount is taken to profit or loss.

The Company designates its cross currency interest rate swaps as cash flow hedges of the foreign currency and interest rate risks arising from floating interest rate foreign currency-denominated liabilities.

Derecognition of Financial Assets and Liabilities Financial asset A financial asset (or, where applicable a part of a financial asset or part of a group of similar financial assets) is derecognized when:

• the rights to receive cash flows from the asset have expired; • the Company retains the right to receive cash flows from the asset, but has assumed an

obligation to pay them in full without material delay to a third party under a ‘pass-through’ arrangement, or;

• the Company has transferred its rights to receive cash flows from the asset and either (a) has transferred substantially all the risks and rewards of the asset, or (b) has neither transferred nor retained substantially all the risks and rewards of the asset, but has transferred control of the asset.

Where the Company has transferred its rights to receive cash flows from an asset or has entered into a ‘pass-through’ arrangement, and has neither transferred nor retained substantially all the risks and rewards of the asset nor transferred control over the asset, the asset is recognized to the extent of the Company’s continuing involvement in the asset. Continuing involvement that takes the form of a guarantee over the transferred asset is measured at the lower of original carrying amount of the asset and the maximum amount of consideration that the Company could be required to repay.

Financial liability A financial liability is derecognized when the obligation under the liability, is discharged, cancelled or has expired. Where an existing financial liability is replaced by another from the same lender on substantially different terms, or the terms of an existing liability are substantially modified, such an exchange or modification is treated as a derecognition of the original liability and the recognition of a new liability, and the difference in the respective carrying amounts is recognized in profit or loss.

- 9 -

*SGVMC118066*

Securities Purchased Under Resale Agreement Conversely, securities purchased under resale agreements (SPURA) to resell at a specified future date (‘reverse repos’) are not recognized on the statement of financial position. The corresponding cash paid, including accrued interest, is recognized in the statement of financial position as SPURA, and is considered a loan to the counterparty. The difference between the purchase price and resale price is treated as interest income and is accrued over the life of the agreement using the effective interest method.

Cash and Cash Equivalents For purposes of reporting cash flows, cash and cash equivalents include cash on hand, cash in banks, due from BSP and SPURA with original maturities of three months or less from dates of placements and that are subject to insignificant risks of changes in value.

Offsetting Financial Instruments Financial assets and financial liabilities are offset and the net amount is reported in the statement of financial position if, and only if, there is a currently enforceable legal right to offset the recognized amounts and there is an intention to settle on a net basis, or to realize the asset and settle the liability simultaneously. This is not generally the case with master netting agreements, and the related assets and liabilities are presented gross in the statement of financial position.

Impairment of Financial Assets The Company assesses at each reporting date whether there is objective evidence that a financial asset or a group of financial assets is impaired. A financial asset or a group of financial assets is deemed to be impaired if, and only if, there is objective evidence of impairment as a result of one or more events that has occurred after the initial recognition of the asset (an incurred ‘loss event’) and that loss event (or events) has an impact on the estimated future cash flows of the financial asset or the group of financial assets that can be reliably estimated. Evidence of impairment may include indications that the borrower or a group of borrowers is experiencing significant financial difficulty, default or delinquency in interest or principal payments, the probability that they will enter bankruptcy or other financial reorganization and where observable data indicate that there is measurable decrease in the estimated future cash flows, such as changes in arrears or economic conditions that correlate with defaults.

Loans and receivables For loans and receivables, carried at amortized cost, the Company first assesses whether objective evidence of impairment exists individually for financial assets that are individually significant, or collectively, for financial assets that are not individually significant. If the Company determines that no objective evidence of impairment exists for individually assessed financial asset, whether significant or not, it includes the asset in a group of financial assets with similar credit risk characteristics and collectively assesses for impairment. Those characteristics are relevant to the estimation of future cash flows for groups of such assets by being indicative of the debtors’ ability to pay all amounts due according to the contractual terms of the assets being evaluated. Assets that are individually assessed for impairment and for which an impairment loss is, or continues to be, recognized are not included in a collective assessment for impairment.

If there is objective evidence that an impairment loss has been incurred, the amount of the loss is measured as the difference between the asset’s carrying amount and the present value of the estimated future cash flows (excluding future credit losses that have not been incurred). The carrying amount of the asset is reduced through use of an allowance account and the amount of loss is charged to profit or loss. Interest income continues to be recognized based on the original

- 10 -

*SGVMC118066*

EIR of the asset. The financial assets, together with the associated allowance accounts, are written off when there is no realistic prospect of future recovery and all collateral has been realized. If, in a subsequent year, the amount of the estimated impairment loss decreases because of an event occurring after the impairment was recognized, the previously recognized impairment loss is reduced by adjusting the allowance account. If a future write-off is later recovered, any amounts formerly charged are credited to “Other income” in profit or loss.

AFS investments For equity investments classified as AFS investments, impairment indicators would include a significant or prolonged decline in the fair value of the investments below its cost. Where there is evidence of impairment, the cumulative loss measured as the difference between the acquisition cost and the current fair value, less any impairment loss on that financial asset previously recognized as OCI is removed and recognized in profit or loss. Impairment losses on equity instruments are not reversed through profit or loss. Increases in fair value after impairment are recognized directly in other comprehensive income.

Finance Lease Receivables When assets are held subject to finance leases, the present value of the lease payments is

recognized as finance lease receivables. Finance lease receivables are stated at the outstanding balance, reduced by unearned lease income and allowance for credit losses.

Residual Value of Leased Assets and Deposits on Lease Contracts The residual value of leased assets is the estimated proceeds from the disposal of the leased asset at the end of the lease term which approximates the amount of guaranty deposit paid by the lessee at the inception of the lease. At the end of the lease term, the residual value is generally applied against the guaranty deposit of the lessee.

Property and Equipment Property and equipment are carried at cost less accumulated depreciation and amortization and impairment loss, if any.

The initial cost of property and equipment consists of its purchase price, any directly attributable costs of bringing the asset to its working condition and location for its intended use and the initial estimate of the costs of dismantling and removing the item and restoring the site on which it is located to the extent it had recognized an obligation for that cost.

Expenditures incurred after an item of property and equipment has been put into operation, such as repairs and maintenance, are normally charged to operations in the year in which the costs are incurred. In situations where it can be clearly demonstrated that the expenditures have resulted in an increase in the future economic benefits expected to be obtained from the use of an item of property and equipment beyond its originally assessed standard of performance, the expenditures are capitalized as an additional cost of property and equipment. When the property and equipment are retired or otherwise disposed of, the cost and the related accumulated depreciation and amortization are removed from the accounts and any resulting gain or loss is reflected in profit or loss.

- 11 -

*SGVMC118066*

Depreciation and amortization is computed using the straight-line method over the estimated useful lives of the property and equipment as follows:

Leasehold improvements 5 years or the lease term,

whichever is shorter Furniture, fixtures and equipment 3-5 years Transportation equipment 3-5 years

The useful life and the depreciation and amortization method are reviewed periodically to ensure that the period and method of depreciation and amortization are consistent with the expected pattern of economic benefits from items of property and equipment.

An item of property and equipment is derecognized upon disposal or when no future economic benefits are expected from its use or disposal. Any gain or loss arising on derecognition of the assets, which is calculated as the difference between the net disposal proceeds and the carrying amount of the asset, is included in profit or loss in the year the asset is derecognized.

Assets Held for Sale An asset is classified as held for sale if its carrying amount will be recovered principally through a sale transaction rather than through continuing use, available for immediate sale and its sale is highly probable. An asset classified as held for sale is measured at the lower of fair value less costs to sell and its carrying amount.

Any impairment loss on write-down of the asset to fair value less costs to sell is recognized in profit or loss. Any gain on subsequent increase in fair value less costs to sell is also recognized in profit or loss, but not in excess of the cumulative impairment loss already recognized on the asset.

Assets held for sale of the Company consists mainly of motor vehicles foreclosed from borrowers or lessees who have defaulted on their installment or lease payments.

Intangible Assets This consists of software costs, stated at acquisition cost and is amortized on a straight-line basis over estimated useful life of five (5) years.

An intangible asset is recognised only when its cost can be measured reliably and it is probable that the expected future economic benefits that are attributable to it will flow to the Company.

Impairment of Nonfinancial Assets The carrying values of non-financial assets (i.e. property and equipment, assets held for sale, software cost) are reviewed for impairment when events or changes in circumstances indicate that the carrying values may not be recoverable. If any such indication exists and where the carrying values exceed the estimated recoverable amounts, the assets or cash-generating units are written down to their recoverable amounts. The recoverable amount of an asset is the greater of its net selling price and value in use. In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessment of the time value of money and the risks specific to the asset. For an asset that does not generate largely independent cash inflows, the recoverable amount is determined for the cash-generating unit to which the asset belongs. Impairment loss is recognized under ‘Provision for credit and impairment losses’ in profit or loss.

- 12 -

*SGVMC118066*

An assessment is made at each reporting date as to whether there is any indication that previously recognized impairment losses may no longer exist or may have decreased. If such indication exists, the recoverable amount is estimated. A previously recognized impairment loss is reversed only if there has been a change in the estimates used to determine the asset’s recoverable amount since the last impairment loss was recognized. If that is the case, the carrying amount of the asset is increased to its recoverable amount. That increased amount cannot exceed the carrying amount that would have been determined, net of depreciation and amortization, had no impairment loss been recognized for the asset in prior years. Such reversal is recognized in profit or loss. After such a reversal, depreciation and amortization expense is adjusted in future years to allocate the asset’s revised carrying amount, less any residual value, on a systematic basis over its remaining life.

Retirement Cost The Company has a defined benefit pension plan (the Plan), which requires contributions to be made to a separately administered fund. The retirement cost of the Company is determined using the projected unit credit method. Under this method, the current service cost is the present value of retirement benefits payable in the future with respect to services rendered in the current period. The liability recognized in the statement of financial position with respect to defined benefit pension plans is the present value of the defined benefit obligation at the reporting date less the fair value of plan assets, together with adjustments for unrecognized actuarial gains or losses and past service costs. In case the fair value of the plan assets exceed the present value of the defined benefit obligation, the recognition of the net plan assets should not exceed the total of (a) any cumulative unrecognized net actuarial losses and past service cost and (b) the present value of any economic benefits available in the form of refunds from the Plan or reductions in future contributions to the Plan.

The defined benefit obligation is calculated annually by an independent actuary. The present value of the defined benefit obligation is determined by discounting the estimated future cash outflows using interest rate on government bonds that have terms to maturity approximating the terms of the related retirement liability. Actuarial gains and losses arising from experience adjustments and changes in actuarial assumptions are charged or credited to income when the net cumulative unrecognized actuarial gains and losses at the end of the previous period exceeded 10.0% of the higher of the defined benefit obligation and the fair value of plan assets at that date. These gains or losses are recognized over the expected average remaining working life of the employees participating in the Plan.

Past service costs, if any, are recognized immediately in profit or loss, unless the changes to the pension plan are conditional on the employees remaining in service for a specified period of time (the vesting period). In this case, the past service costs are amortized on a straight-line basis over the vesting period.

Leases The determination of whether an arrangement is, or contains a lease is based on the substance of the arrangement at inception date whether the fulfillment of the arrangement is dependent on the use of a specific asset or assets or the arrangement conveys a right to use the asset.

Company as lessor The Company recognizes assets held under a finance lease in its statement of financial position as a receivable at an amount equal to the net investment in the lease. The lease payments received from the lessee are treated as repayments of principal and finance income. Initial direct costs that

- 13 -

*SGVMC118066*

are incremental and directly attributable to negotiating and arranging the lease, are included in the measurement of the net investment in the lease at inception and reflected in the calculation of the implicit interest rate.

Company as lessee Lease of assets under which the lessor effectively retains all the risks and rewards of ownership is classified as operating lease. Lease payments under an operating lease are recognized as an expense on a straight-line basis over the lease term.

Revenue Recognition Revenue is recognized to the extent that it is probable that the economic benefits will flow to the Company and the income can be reliably measured. The following specific recognition criteria must also be met before revenue is recognized:

Interest income Interest and financing fees on finance leases and loans and receivables (including dealers’ and manufacturers’ subsidy) are initially credited to unearned interest income and amortized over the term using effective interest method. Any direct costs to acquire finance leases and loans and receivables are capitalized and amortized using the effective interest method.

Interest income on impaired receivables is recognized based on the rate used to discount future cash flows to their net present value. Interest income from cash in bank is accrued as earned.

Service fees Service fees earned for the provision of transaction services such as processing fees are recognized upon completion of the underlying transaction.

Recoveries of accounts written off Recoveries of accounts written off are recognized as income upon actual collection.

Borrowing Costs Borrowing costs directly attributable to the acquisition, construction or production of an asset that necessarily takes a substantial period of time to get ready for its intended use are capitalized. All other borrowing costs are recognized as expense in the year which they are incurred.

Income Taxes Current taxes Current tax assets and liabilities are measured at the amount expected to be recovered from or paid to the taxation authorities. The tax rates and tax laws used to compute the amount are those that are enacted or substantively enacted at the reporting date.

Deferred taxes Deferred tax is provided on all temporary differences at the reporting date between the tax bases of assets and liabilities and their carrying amounts for financial reporting purposes.

Deferred tax liabilities are recognized for all taxable temporary differences. Deferred tax assets are recognized for all deductible temporary differences, carryforward benefit of the excess of minimum corporate income tax (MCIT) over regular corporate income tax (RCIT) and unused net operating loss carryover (NOLCO), to the extent that it is probable that taxable profit will be available against which the deductible temporary differences and carryforward of MCIT and unused NOLCO can be utilized.

- 14 -

*SGVMC118066*

The carrying amount of deferred tax assets is reviewed at each reporting date and reduced to the extent that it is no longer probable that sufficient taxable profit will be available to allow all or part of the deferred tax assets to be utilized. Unrecognized deferred tax assets are reassessed at each reporting date and are recognized to the extent that it has become probable that future taxable profit will allow all or part of the deferred tax assets to be recovered. Deferred tax, however, is not recognized on temporary differences that arise from the initial recognition of an asset or liability in a transaction that is not a business combination and, at the time of the transaction, affects neither the accounting income nor taxable income or loss.

Deferred tax assets and liabilities are measured at the tax rate that is expected to apply to the year when the asset is realized or the liability is settled, based on tax rates (and tax laws) that have been enacted or substantively enacted at the reporting date.

Current tax and deferred tax relating to items recognized directly in equity is also recognized in equity and not in profit or loss.

Deferred tax assets and tax liabilities are offset, if a legally enforceable right exists to set off current tax assets against current tax liabilities and the deferred taxes relate to the same taxable entity and the same taxation authority.

Provisions Provisions are recognized when the Company has a present obligation (legal or constructive) where, as a result of a past event, it is probable that an outflow of resources embodying economic benefits will be required to settle the obligation and a reliable estimate can be made of the amount of the obligation.

Contingencies Contingent liabilities are not recognized but are disclosed in the notes to the financial statements unless the possibility of an outflow of resources embodying economic benefits is remote. Contingent assets are not recognized but are disclosed in the notes to the financial statements when the inflow of economic benefits is probable.

Equity Capital stock is measured at par value for all shares issued. When the Company issues more than one class of stock, a separate account is maintained for each class of stock and the number of shares issued.

When the shares are sold at premium, the difference between the proceeds and the par value is credited to “Additional paid-in capital” account. When shares are issued for a consideration other than cash, the proceeds are measured by the fair value of the consideration received. In case the shares are issued to extinguish or settle the liability of the Company, the shares shall be measured either at the fair value of the shares issued or fair value of the liability settled, whichever is more reliably determinable.

Direct cost incurred related to the equity issuance, such as underwriting, accounting and legal fees, printing costs and taxes are chargeable to “Additional paid-in capital” account. If additional paid-in capital is not sufficient, the excess is charged against retained earnings.

Retained earnings represent accumulated net income of the Company, net of dividends paid.

- 15 -

*SGVMC118066*

Dividends Dividends are recognized as a liability and deducted from equity when declared and approved by the Board of Directors of the Company and of the BSP. Dividends for the year that are declared and approved after the reporting date, if any, are dealt with as an event after the reporting date and disclosed accordingly.

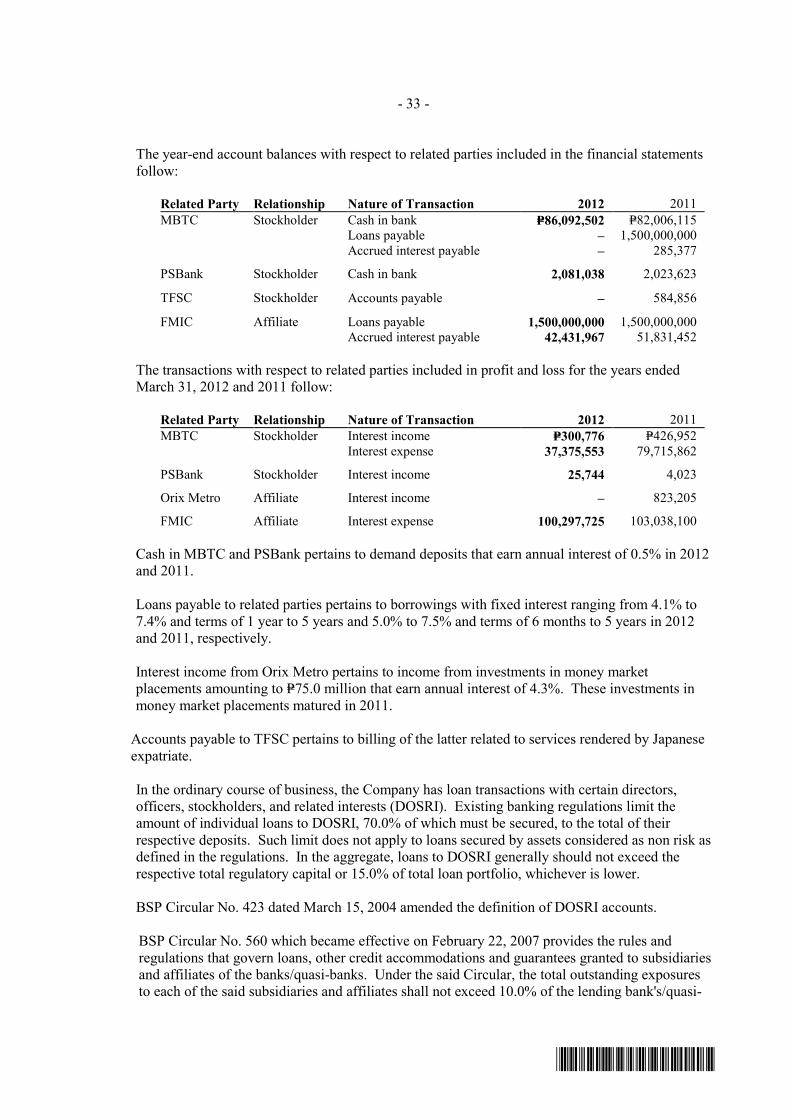

Related Party Transactions Parties are considered to be related if one party has the ability, directly or indirectly, to control the other party or exercise significant influence over the other party in making financial and operating decisions or if they are subjected to common control or common significant influence. Related parties may be individuals or corporate entities. Transactions between related parties are based on terms similar to those offered to non-related parties.

Expense Recognition Expenses are recognized in profit or loss when decrease in future economic benefit related to a decrease in an asset or an increase in a liability has arisen that can be measured reliably. Expenses are recognized in profit or loss: on the basis of a direct association between the costs incurred and the earning of specific items of income; on the basis of systematic and rational allocation procedures when economic benefits are expected to arise over several accounting periods and the association with income can only be broadly or indirectly determined; or immediately when an expenditure produces no future economic benefits or when, and to the extent that, future economic benefits do not qualify or cease to qualify, for recognition in the statements of financial position as an asset.

Events after the Reporting Period Post year-end events that provide additional information about the Company’s financial position at the reporting date (adjusting events) are reflected in the financial statements. Post year-end events that are not adjusting events are disclosed in the notes to the financial statements when material.

3. Significant Accounting Judgments and Estimates

The preparation of the accompanying financial statements in conformity with PFRS requires management to make judgments, estimates and assumptions that affect the reported amounts in the financial statements and accompanying notes. The judgments, estimates and assumptions used in the accompanying financial statements are based upon management’s evaluation of relevant facts and circumstances as of the date of the financial statements. Actual results could differ from such estimates.

Judgments and estimates are continually evaluated and are based on historical experience and other factors, including expectations of future events that are believed to be reasonable under the circumstances.

Judgments In the process of applying the Company’s accounting policies, management has made the following judgments, apart from those involving estimates and assumptions, which have the most significant effect on the amounts recognized in the financial statements.

- 16 -

*SGVMC118066*

Finance leases The Company, as a lessor, has entered into finance leases of vehicles with its customers. The Company has determined that it transfers all the significant risks and rewards of ownership as the lease terms are for the major part of the economic life of these properties which are leased out on finance leases.

Operating leases The Company has entered into a lease commitment for its occupied office premises. The Company has determined based on its evaluation of the terms and conditions of the lease arrangements (i.e., the lease does not transfer ownership of the asset to the lessee by the end of the lease term, the lessee has no option to purchase the asset at a price that is expected to be sufficiently lower than the fair value at the date the option is exercisable and the lease term is not for the major part of the asset’s economic life) that all significant risks and rewards of ownership are retained by the respective lessors. Operating lease payments are recognized as an expense in the statement of income on a straight-line basis over the lease term.

Estimates The key assumptions concerning the future and other key sources of estimation uncertainty at the reporting date, that have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities within the next financial year are discussed in the following paragraphs.

a. Estimation of allowance for credit losses

The Company reviews impairment of receivables on a monthly basis. Impairment loss on receivables is determined on a collective basis using the net flow rate methodology.

In determining whether an impairment loss should be recorded in profit or loss, the Company makes judgments as to whether there is any observable data indicating that there is a measurable decrease in the estimated future cash flows from a portfolio of receivables financed and lease contract receivables before the decrease can be identified with an individual account in that portfolio. This observable data may include adverse changes in the payment status of borrowers in a group, or national or local economic conditions that correlate with defaults on assets in the portfolio.

The amount and timing of recorded expenses for any period would differ if the Company made different estimates. An increase in allowance for credit losses would increase the recorded expenses and decrease the related asset account.

As of March 31, 2012 and 2011, the carrying value of loans and receivables amounted to P=17.5 billion and P=16.6 billion, respectively (see Note 7).

As of March 31, 2012 and 2011, allowance for credit losses on loans and receivables amounted to P=469.2 million and P=326.0 million, respectively (see Note 7).

b. Fair value of derivatives

The fair values of derivatives that are not quoted in active markets are determined using valuation techniques. Where valuation techniques are used to determine fair values, they are validated and periodically reviewed by qualified personnel independent of the area that created them. All models are reviewed before they are used, and models are calibrated to ensure that outputs reflect actual data and comparative market prices. To the extent practical, models use

- 17 -

*SGVMC118066*

only observable data, however areas such as credit risk (both own and counterparty), volatilities and correlations require management to make estimates. Changes in assumptions about these factors could affect reported fair value of financial instruments.

As of March 31, 2012 and 2011, derivative liabilities designated as hedge amounted to P=34.2 million and P=70.5 million, respectively (see Note 15).

c. Valuation of assets held for sale

The Company’s assets held for sale are carried at the lower of its carrying amount and fair value less costs to sell. Fair value is based on the valuation performed by the internal appraiser. Valuation of assets held for sale is ascertained using the market data approach, wherein current sales prices of identical vehicles, together with the valuation opinions of conversant appraisers are accumulated, compared and thoroughly analyzed. As of March 31, 2012 and 2011, assets held for sale amounted to P=74.9 million and P=63.4 million, respectively (see Note 8).

d. Present value of retirement obligation

The present value of the obligation depends on certain factors that are determined on an actuarial basis using a number of assumptions. These include, among others, discount rates, expected rate of return on plan assets, future salary increases, mortality rates, and future pension increases. Due to long term nature of this plan, such estimates are subject to significant uncertainty.

The assumed discount rates were determined using average market yields on Philippine government bonds with terms consistent with the expected employee benefit payout as of reporting date. The expected rate of return on plan assets of 7.0% as of March 31, 2012 and 2011 was based on market prices prevailing on the date of valuation, applicable to the period over which the obligation is to be settled. Refer to Note 19 for the details of assumptions used in the calculation.

As of March 31, 2012 and 2011, the present value of the defined benefit obligation of the Company amounted to P=15.9 million and P=17.9 million, respectively. As of March 31, 2012 and 2011, the Company has net plan liability amounting to P=5.3 million and P=2.2 million, respectively (see Note 19).

e. Recognition of deferred tax assets

Deferred tax assets are recognized for all deductible temporary differences to the extent that it is probable that taxable income will be available against which the losses can be utilized. Significant management judgment is required to determine the amount of deferred tax assets that can be recognized, based upon the likely timing and level of future taxable income together with future tax planning strategies.

The Company has been in a taxable income position over the past several years. The Company believes, based on its expected future taxable income, that it is highly probable for temporary differences to be realized in the future.

As of March 31, 2012 and 2011, the carrying value of the recognized net deferred tax assets amounted to P=113.4 million and P=88.9 million, respectively (see Note 20).

- 18 -

*SGVMC118066*

4. Cash and Due from Bangko Sentral ng Pilipinas

Cash This account consists of:

2012 2011 Cash on hand P=435,487 P=474,548 Cash in banks 1,215,774,351 1,220,996,515 P=1,216,209,838 P=1,221,471,063

Cash in bank earns annual interest ranging from 2.9% to 3.0% in 2012 and 2011.

Due from BSP As of March 31, 2012 and 2011, due from BSP consists of demand deposits and savings and reserve deposits accounts with placement term not exceeding three months and interest rates ranging from 0.4% to 4.0% and 0.3% to 4.3%, respectively.

5. Securities Purchased Under Resale Agreement (SPURA)

This account consists of government securities purchased under reverse repurchase agreement with the BSP as counterparty. As of March 31, 2012 and 2011, these government securities with face value amounting to P=540.0 million and P=208.0 million respectively, and fair value of P=582.0 million and P=212.0 million, respectively, were pledged in favor of the Company as collateral for SPURA equivalent to the face value of the government securities.

6. Available-for-Sale Investments

AFS investments include quoted equity shares. The carrying value of the AFS investments amounted to P=0.93 million and P=0.96 million as of March 31, 2012 and 2011. The changes in fair value recognized in other comprehensive income amounted to P=0.08 million in 2012 and P=0.05 million in 2011. In 2012, the Company recognized impairment loss on AFS investments amounting to P=0.10 million directly to profit or loss.

The movements in unrealized gain on AFS investments follow:

2012 2011 Balance at beginning of year P=955,000 P=910,000 Impairment loss (100,000) – Changes in fair value 75,000 45,000 Balance at end of year P=930,000 P=955,000

- 19 -

*SGVMC118066*

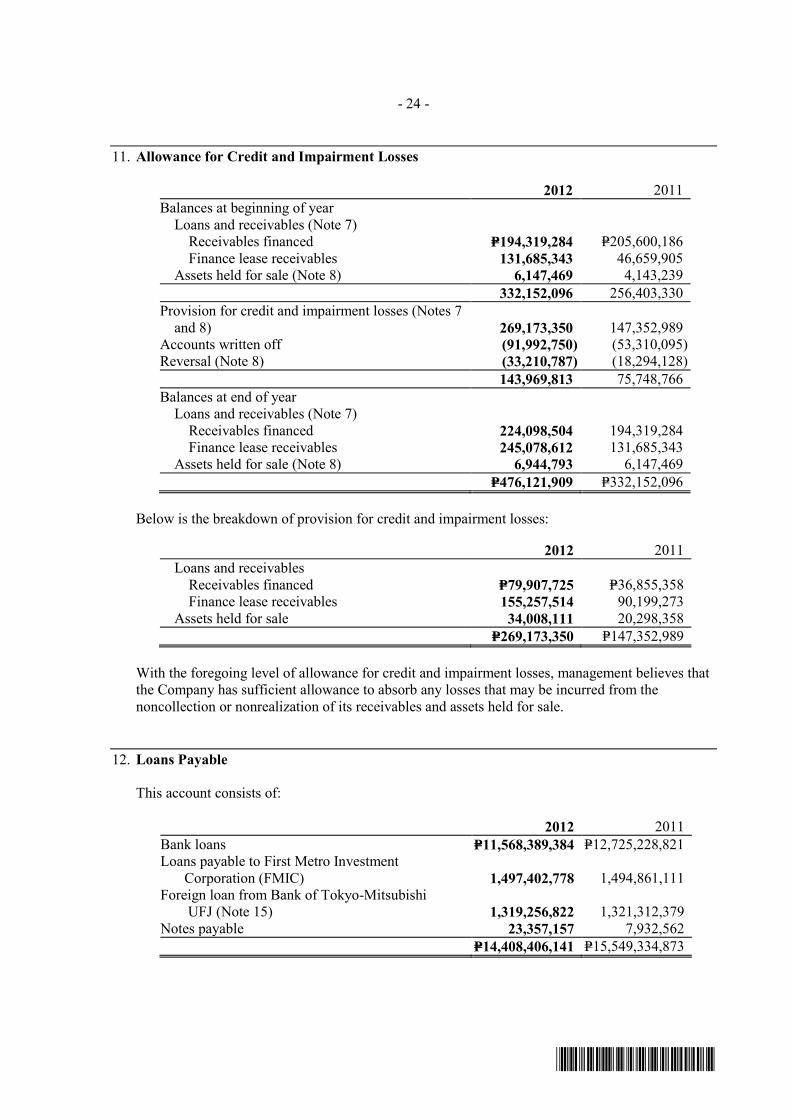

7. Loans and Receivables

This account consists of:

2012 2011 Receivables from customers Receivables financed P=7,369,528,572 P=9,724,745,596 Unearned finance income (947,083,051) (1,353,937,971) 6,422,445,521 8,370,807,625 Finance lease receivables Finance lease receivables 10,276,562,416 8,040,180,950 Residual value of leased assets 2,934,445,588 2,012,440,981 13,211,008,004 10,052,621,931 Unearned lease income (1,684,843,018) (1,469,403,318) 11,526,164,986 8,583,218,613 17,948,610,507 16,954,026,238 Other receivables Receivables from clients 55,231,257 6,278,031 Receivables from employees 5,236,314 4,360,374 Accrued interest receivable 1,920,118 2,107,726 Others 781,992 975,286 63,169,681 13,721,417 Allowance for credit losses (Note 11) (469,177,116) (326,004,627) P=17,542,603,072 P=16,641,743,028

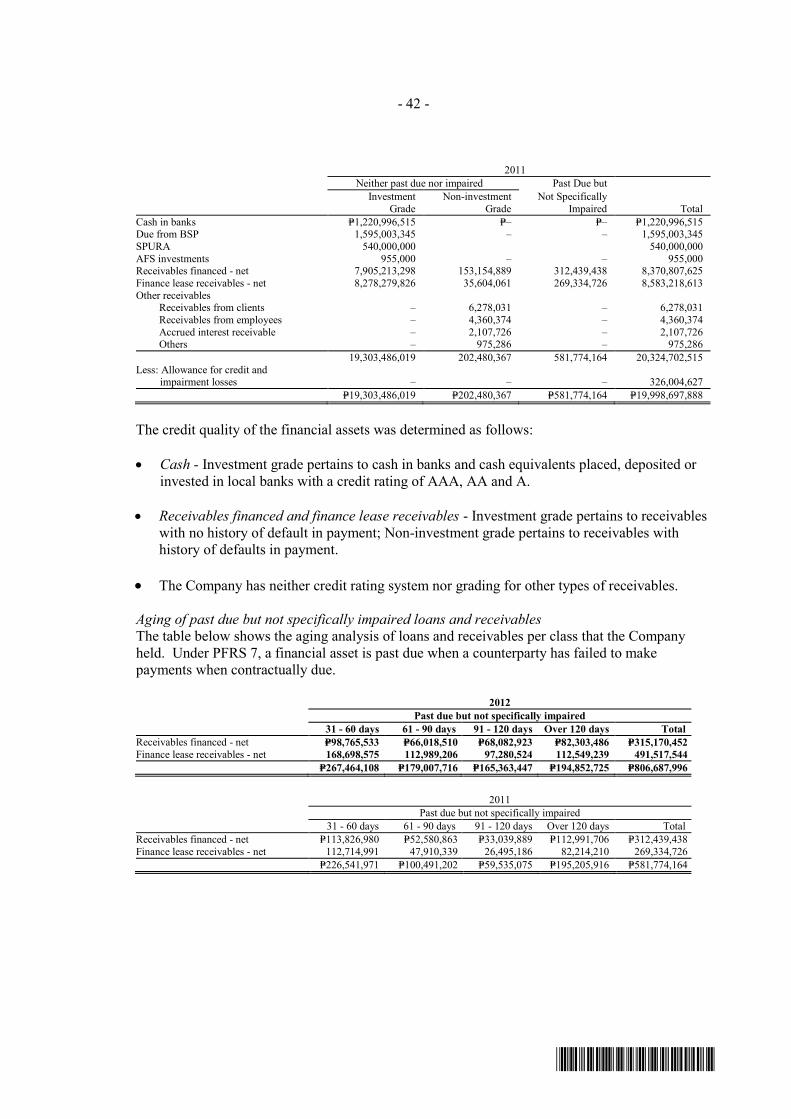

Receivables financed earn fixed interest ranging from 6.6% to 38.0% in 2012 and from 7.8% to 24.3% in 2011 while finance lease receivables earn fixed interest ranging from 7.5% to 19.2% in 2012 and from 8.8% to 20.6% in 2011. An account shall be considered past due when after the arrival of a payment due date, the client failed to settle the amount within a reasonable period of time. If the account remains unpaid for 30 days from the last due date, the account shall be considered past due.

Receivables from customers are due in monthly installments with terms ranging from one (1) to six (6) years. The receivables financed, net of unearned finance income, by contractual maturity dates is analyzed as follows:

2012 2011 Due within 1 year P=814,961,988 P=949,719,533 Due beyond 1 year but not beyond 5 years 5,607,483,533 7,415,413,214 Due beyond 5 years – 5,674,878 P=6,422,445,521 P=8,370,807,625

- 20 -

*SGVMC118066*

The breakdown of the Company’s gross investment in finance lease receivables by contractual maturity dates is analyzed as follows:

2012 2011 Gross investment in finance lease receivables Due within 1 year P=228,998,133 P=125,570,152 Due beyond 1 year but not beyond 5 years 10,047,564,283 7,886,619,765 Due beyond 5 years – 27,991,033 10,276,562,416 8,040,180,950 Residual value of leased assets Due within 1 year 270,670,112 137,919,733 Due beyond 1 year but not beyond 5 years 2,663,775,476 1,870,221,198 Due beyond 5 years – 4,300,050 2,934,445,588 2,012,440,981 Unearned lease income Due within 1 year (9,029,604) (5,567,701) Due beyond 1 year but not beyond 5 years (1,675,813,414) (1,456,642,878) Due beyond 5 years – (7,192,739) (1,684,843,018) (1,469,403,318) Net investment in finance lease receivables P=11,526,164,986 P=8,583,218,613

The net investment in finance lease receivables is analyzed as follows:

2012 2011 Due within 1 year P=490,638,641 P=257,922,184Due beyond 1 year but not beyond 5 years 11,035,526,345 8,300,198,085Due beyond 5 years – 25,098,344 P=11,526,164,986 P=8,583,218,613

Interest income on loans and receivables consists of:

2012 2011 Receivables financed P=829,294,069 P=1,049,130,562 Finance lease receivables 852,459,723 545,349,260 P=1,681,753,792 P=1,594,479,822

A reconciliation of the allowance for credit losses by class of receivables from customers follows (see Note 11):

2012

Receivables

financed Finance lease

receivables Total

Balances at beginning of year P=194,319,284

P=131,685,343 P=326,004,627 Provisions 79,907,725 155,257,514 235,165,239 Accounts written off (50,128,505) (41,864,245) (91,992,750) Balances at end of year P=224,098,504 P=245,078,612 P=469,177,116

- 21 -

*SGVMC118066*

2011

Receivables

financed Finance lease

receivables Total Balances at beginning of year P=205,600,186 P=46,659,905 P=252,260,091 Provisions 36,855,358 90,199,273 127,054,631 Accounts written off (48,136,260) (5,173,835) (53,310,095) Balances at end of year P=194,319,284 P=131,685,343 P=326,004,627

All accounts not identified as specifically impaired are subjected to collective testing. Collective testing of impairment loss is assessed using net flow rate methodology.

BSP reporting As of March 31, 2012 and 2011, information on concentration of receivables from customers as to economic activity of the Company follows:

2012 2011 Amount % Amount % Real estate, renting and business activities P=4,142,682,610 27.6 P=4,374,986,094 29.2 Wholesale and retail trade 2,839,040,371 18.9 3,018,223,283 20.2 Manufacturing 2,089,825,349 13.9 2,052,134,612 13.7 Financial intermediaries 1,570,651,395 10.5 1,937,236,591 13.0 Transportation, storage and communication 1,482,045,847 9.9 1,306,007,992 8.7 Other community, social and personal activities 1,121,414,636 7.5 605,213,760 4.1 Education 577,990,217 3.8 527,685,802 3.5 Construction 338,693,330 2.3 288,054,633 1.9 Agricultural, hunting and forestry 326,776,252 2.1 279,295,921 1.9 Hotels and restaurants 292,401,096 1.9 321,547,543 2.2 Electricity, gas and water 149,542,707 1.0 144,502,918 1.0 Mining and quarrying 72,170,901 0.5 78,900,862 0.5 Fishing 10,930,208 0.1 7,795,246 0.1 P=15,014,164,919 100.0 P=14,941,585,257 100.0

The BSP considers that concentration of credit exists when total loan exposure to a particular industry or economic sector exceeds 30% of total loan portfolio.

As of March 31, 2012 and 2011, nonperforming loans (NPLs) not fully covered by allowance for credit losses of the Company, as reported to BSP, follow:

2012 2011 Total NPLs P=317,110,732 P=234,645,120 NPLs fully covered by allowance for credit losses (158,012,014) (124,790,902) P=159,098,718 P=109,854,218

Generally, NPLs refer to loans whose principal and/or interest is unpaid for ninety (90) days or more after due date or after they have become past due in accordance with existing BSP rules and regulations. This shall apply to loans payable in lump sum and loans payable in quarterly, semi-annual, or annual installments, in which case, the total outstanding balance thereof shall be considered nonperforming.

- 22 -

*SGVMC118066*

In the case of receivables that are payable in monthly installments, the total outstanding balance thereof shall be considered nonperforming when three (3) or more installments are in arrears. In the case of receivables that are payable in weekly, or semi-monthly installments, the total outstanding balance thereof shall be considered nonperforming at the same time that they become past due in accordance with existing BSP regulations, i.e., the entire outstanding balance of the receivable shall be considered as past due when the total amount of arrearages reaches more than 10.0% of the total receivable balance.

8. Assets Held for Sale

The rollforward analysis of this account follows:

2012 2011 Cost Balance at beginning of year P=69,505,643 P=46,043,345 Additions 402,051,712 237,030,282 Disposals (389,751,778) (213,567,984) Balance at end of year 81,805,577 69,505,643 Allowance for impairment losses (Note 11) Balance at beginning of year 6,147,469 4,143,239 Additions 34,008,111 20,298,358 Disposals (33,210,787) (18,294,128) Balance at end of year 6,944,793 6,147,469 Net book value P=74,860,784 P=63,358,174

The Company’s assets held for sale consist of repossessed collaterals from customers who have defaulted in their respective loan accounts. These are actively marketed for sale and are expected to be sold within one year from the date of its classification as assets held for sale.

Gain (loss) on assets held for sale included under “Service fees and other income” in the statements of comprehensive income amounted to (P=9.3) million and P=9.4 million in 2012 and 2011, respectively (see Note 18).

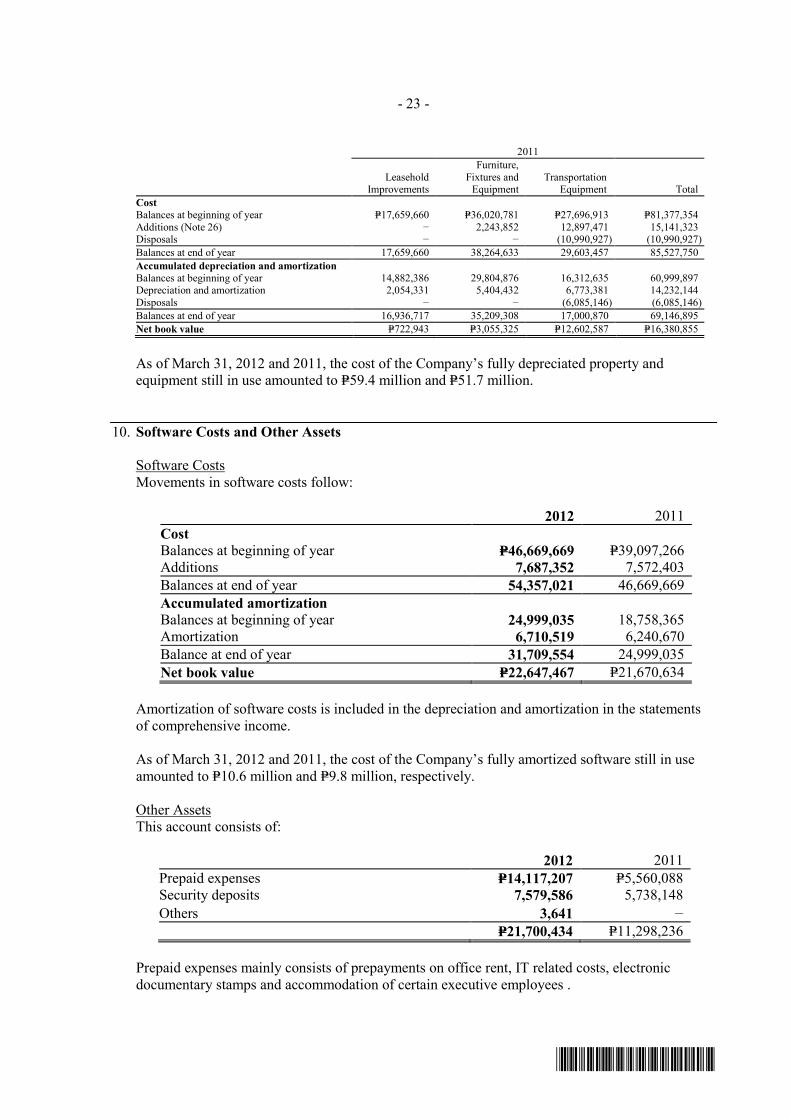

9. Property and Equipment

The composition and movements in this account follow:

2012

Leasehold

Improvements

Furniture, Fixtures and

Equipment Transportation

Equipment Total Cost Balances at beginning of year P=17,659,660 P=38,264,633 P=29,603,457 P=85,527,750 Additions (Note 26) 5,017,196 3,081,360 14,548,729 22,647,285 Disposals - - (20,749,222) (20,749,222) Balances at end of year 22,676,856 41,345,993 23,402,964 87,425,813 Accumulated depreciation and amortization Balances at beginning of year 16,936,717 35,209,308 17,000,870 69,146,895 Depreciation and amortization 675,659 3,354,808 15,547 4,046,014 Disposals (12,766) - (3,092,264) (3,105,030) Balances at end of year 17,599,610 38,564,116 13,924,153 70,087,879 Net book value P=5,077,246 P=2,781,877 P=9,478,811 P=17,337,934

- 23 -

*SGVMC118066*

2011

Leasehold

Improvements

Furniture, Fixtures and

Equipment Transportation

Equipment Total Cost Balances at beginning of year P=17,659,660 P=36,020,781 P=27,696,913 P=81,377,354 Additions (Note 26) − 2,243,852 12,897,471 15,141,323 Disposals − − (10,990,927) (10,990,927) Balances at end of year 17,659,660 38,264,633 29,603,457 85,527,750 Accumulated depreciation and amortization Balances at beginning of year 14,882,386 29,804,876 16,312,635 60,999,897 Depreciation and amortization 2,054,331 5,404,432 6,773,381 14,232,144 Disposals − − (6,085,146) (6,085,146) Balances at end of year 16,936,717 35,209,308 17,000,870 69,146,895 Net book value P=722,943 P=3,055,325 P=12,602,587 P=16,380,855

As of March 31, 2012 and 2011, the cost of the Company’s fully depreciated property and equipment still in use amounted to P=59.4 million and P=51.7 million.

10. Software Costs and Other Assets

Software Costs Movements in software costs follow: