th annual conference maximise pwc tax panel … · ready format' from either their...

TRANSCRIPT

17th Annual Conference

Maximise Shareholder Value 2016

PwC Tax Panel

27 October 2015

PwC

Agenda

Section one - The Tax Function of the Future

Section two - Tax Life Cycle

Section three - Changes, improvements and updates to laws

227 October 2015 Maximise Shareholder Value 2016

PwC

The Tax Function of the Future

13

27 October 2015 Maximise Shareholder Value 2016

PwC

Our predictions

427 October 2015 Maximise Shareholder Value 2016

PwC

Our predictionsRegulatory

Global tax information reporting requirements (e.g. BEPS and similar transparency initiatives) will grow exponentially and will have a material impact on the operations and related budget allocations within the tax function.

Regulators will demand transparency regarding global taxation, necessitating clear and thoughtful communications with public stakeholders about corporate contributions to the communities in which they do business.

Information sharing will be commonplace among taxing jurisdictions, and taxing authorities will have the capability to mine data and conduct global audits, resulting in increased disputes.

527 October 2015 Maximise Shareholder Value 2016

PwC

Our predictions Risk & Governance

Many jurisdictions will legislatively require the adoption of a tax control framework which follows guidelines similar to Sarbanes-Oxley and COSO (Committee of Sponsoring Organizations of the Treadway Commission).

Enhanced stakeholder scrutiny and reputational risk will force

companies to continuously re-evaluate their tax decisions.

Strategic focus on jurisdictional reporting and documentation of

business activities, including transfer pricing, will be critical to

managing the increased tax controversy resulting from transparency

initiatives.

627 October 2015 Maximise Shareholder Value 2016

PwC

Our predictions Data

The majority of tax functions will receive all information in a 'tax ready format' from either their enterprise-wide financial systems or a dedicated tax data hub.

Dedicated tax data hubs will become mainstream and be developed

internally, licensed from a third-party vendor, and/or accessed

through an accounting firm as part of a co-sourcing arrangement.

Data security will be high on the agenda of tax functions due to

concerns over confidential information being inadvertently released

or shared publicly.

727 October 2015 Maximise Shareholder Value 2016

PwC

Our predictions Technology

More companies will use their enterprise-wide financial systems to prepare tax calculations (e.g. income tax accounting and indirect taxes), thereby replacing spreadsheets and/or traditional tax technology solutions.

The vast majority of tax functions will rely on professional data analysis tools to assist in the decision-making process in areas such as detection of risk, opportunity identification, projections and scenario planning, and overall business support.

827 October 2015 Maximise Shareholder Value 2016

PwC

Our predictions Process

Most global tax preparatory compliance and reporting activities, including data collection and reconciliations, will be performed within the company's shared service centre or will be co-sourced with a third party.

Tax functions will use real-time collaboration tools to automate their workflow, document management, calendaring, and internal controls.

927 October 2015 Maximise Shareholder Value 2016

PwC

Our predictions People

A successful tax professional of the future will be highly proficient in data analysis, statistics, and technology, as well as process improvement and change management.

Tax functions will employ dedicated tax IT, data and project management specialists who will develop, champion, and execute the tax technology and transformation strategies.

1027 October 2015 Maximise Shareholder Value 2016

PwC

Tax function of the future In conclusion

Lots of internal and external changes and influences are impacting

how tax is managed in organizations

The management of tax in the future will be very different to how tax

is managed today

Historic practices and processes will need to be revamped, and fresh,

innovative approaches utilizing technological know-how will be

crucial

1127 October 2015 Maximise Shareholder Value 2016

PwC

Tax Life Cycle

212

27 October 2015 Maximise Shareholder Value 2016

PwC

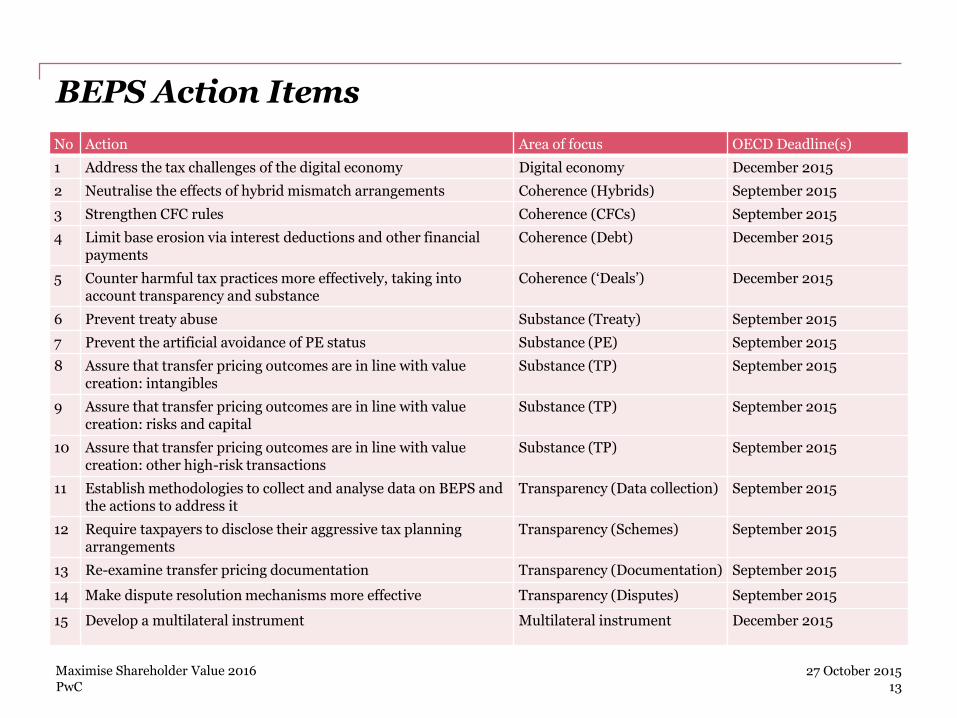

BEPS Action Items

1327 October 2015 Maximise Shareholder Value 2016

No Action Area of focus OECD Deadline(s)

1 Address the tax challenges of the digital economy Digital economy December 2015

2 Neutralise the effects of hybrid mismatch arrangements Coherence (Hybrids) September 2015

3 Strengthen CFC rules Coherence (CFCs) September 2015

4 Limit base erosion via interest deductions and other financial payments

Coherence (Debt) December 2015

5 Counter harmful tax practices more effectively, taking into account transparency and substance

Coherence (‘Deals’) December 2015

6 Prevent treaty abuse Substance (Treaty) September 2015

7 Prevent the artificial avoidance of PE status Substance (PE) September 2015

8 Assure that transfer pricing outcomes are in line with value creation: intangibles

Substance (TP) September 2015

9 Assure that transfer pricing outcomes are in line with value creation: risks and capital

Substance (TP) September 2015

10 Assure that transfer pricing outcomes are in line with value creation: other high-risk transactions

Substance (TP) September 2015

11 Establish methodologies to collect and analyse data on BEPS and the actions to address it

Transparency (Data collection) September 2015

12 Require taxpayers to disclose their aggressive tax planning arrangements

Transparency (Schemes) September 2015

13 Re-examine transfer pricing documentation Transparency (Documentation) September 2015

14 Make dispute resolution mechanisms more effective Transparency (Disputes) September 2015

15 Develop a multilateral instrument Multilateral instrument December 2015

PwC

Tax Life Cycle

1427 October 2015 Maximise Shareholder Value 2016

Tax Policy DesignTax Policy

ImplementationTax

Documentation

Key messages:

• Starting point – establish tax policy (fit for purpose…)

• Tax documentation is the end of the life cycle

• Policy implementation is the ‘glue’ between the policy and the documentation

PwC

Changes, improvements and updates to laws

315

27 October 2015 Maximise Shareholder Value 2016

What you need to know

PwC

Content overview

Maximise Shareholder Value 2016

16

27 October 2015

• New Collateral laws

• BOI

• Licensing Facilitation Act

2 To adjust laws to suit the changing economy

• e-filing1 To improve efficiency and process through technology

• Provident Fund Act (No. 4), B.E. 2558

• Social Security Act (No. 4) B.E. 2558

4 To improve living quality

• Debt Collection Act

• Constitutional Act on the prevention and suppression of corruption (No. 3), B.E. 2558

• Machine Registration Act (No. 3), B.E. 2015

3 To be stricter and tougher in law enforcement

Purpose of law enactment Update on laws

1

234

5

6

7

89

PwC

e-Filing

27 October 2015 Maximise Shareholder Value 2016

17

1

PwC

e-FilingDBD Notification dated 4 September 2015

18

27 October 2015 Maximise Shareholder Value 2016

Duties of account preparer

File audited financial statements, auditor’s report and annual report

• by hand or by

• via e-filing

Closing date

31 Dec April

4 months

May

1 month

June

1 month

AGM Document submission

e-Filing

PwC

1

Registration

2

Preparation

• Apply for user name & password via DBD website

• Submit the following documents via e-filing system by filling in: Balance sheet Profit and loss statement Statement of change of

shareholders’ equity Form SBC. 3 + financial

statements, SBC 3/1 (if any), BOJ. 5 (if any)

Attachment Report of independent

certified public accountant Notes to the FS

• Print out Form SBC. 3

Prepare information for submission via e-form (Online) or XBRL (Offline)

• Check the status of FS submission via the e-filing system

• Print receipt

Submit application and supporting documents to DBD

Receive activation code from DBD via email

1 – 2 daysWithin

30 days

Activate company’s account

Within 1 month after AGM

4

Status Check

3

Submission

Process overview

Maximise Shareholder Value 2016 27 October 2015

19

PwC

New Collateral laws

20

Written evidence

Contract + Asset’s registration

Handover

• Personal

• Immovable/special movable properties

• Tangible properties

• Guarantee (CCC amendment no 20 and 21)

• Mortgage (CCC amendment no 20 and 21)

• Pledge

Contract registration

• No need to handover

• No need to register the assets

• Intangible assets

• Inventories

• Raw materials

• Intellectual properties

• Rights of claims

• Enterprise

• Business Security Act (Draft version – waiting for publishing in Royal Gazette)

Qualified collateral Requirements Laws

No

w2

Ne

w

Maximise Shareholder Value 2016 27 October 2015

PwC

New Collateral laws

Rights over the collateral

(unless agreed otherwise)

Possession

Transfer Use

Disposal

Mortgage

ExchangePledge

1. Rights of person who gives collateral 2. Collateral enforcement

Assets/Right of claims

• Confiscation

• Auction

• Set-off

• Others

Enterprise

• Enforcement officer

Inquisition

Make decision

21

Maximise Shareholder Value 2016 27 October 2015

PwC

32

22

New Collateral lawsProcess of Mortgage enforcement under amendment of CCC

Pull out of an important statistic goes in this area 14pt Georgia (white)

Old(CCC)

Latest (Amendment No. 21 )

12 February 2015

• Advance notice for mortgage enforcement within reasonable time

• Advance notice for mortgage enforcement Mortgaged by debtor: Notice to debtor not less than 60 days

in advance Mortgaged by third party: Notice to third party mortgagee

within 15 days after notifying the debtor

• One-month advance notice to mortgage transferee for mortgage enforcement

• Extension of notice period to not less than 60 days

• Mortgage enforcement requires exercise of judicial right only

• Not necessary to exercise judicial right to undertake public auction.

Which law will govern?

Maximise Shareholder Value 2016 27 October 2015

PwC

BOI

23

27 October 2015

23

• Merit-based incentives (Decentralization)

• Investment in special economic development zones

• IHQ & ITC

PwC

Update on interesting investment schemes

Maximise Shareholder Value 2016

3

PwC

BOI Merit-based incentives (Decentralization)

24

! Amnatcharoen

@ Buengkan

# Buriram

$ Chaiyaphum

% Kalasin

^ Maehongson

& Mahasarakham

* Mukdahan

( Nakornphanom

) Nan

_ Nongbualamphu

+ Phare

- Roi Et

= Sakaew

{ Sakhonnakhon

} Sisaket

| Sukhothai

[ Surin

] Ubonratchatani

\ Yasothon

• 3 additional years of corporate income tax exemption shall be granted.

• Projects with activities in Group A1 or A2 which are already granted an 8-year corporate income tax exemption shall instead receive a 50% reduction of corporate income tax on net profit derived from promoted activity for 5 years after the corporate income tax exemption period expires.

Maximise Shareholder Value 2016 27 October 2015

PwC

BOI Investment in special economic development zones

25

Tak 1

Sakaew2

Trat3

Songkla 4

Chiang Rai5

Nong Khai 6

Nakhon Panom 7

Kanjanaburi 8

Narathiwas9

Incentives for activities on

BOI General list

Incentives for targeted activities for

Special Economic Development Zones

(13 targeted industries)

3-year additional exemption of CIT, not

exceeding 8 years in total

Exemption of corporate income tax up

to 8 years

Projects with activities in Group A1 or

A2 which are already granted 8-year

CIT shall receive additional 50%

reduction CIT for 5 years.

Additional 50% corporate income tax

exemption for 5 years.

• 10–year double deductions from the

costs of transportation, electricity,

and water supply

• 25% deduction of the cost of

installation or construction of

facilities (apart from normal

depreciation deduction)

• Exemption of import duties on

machinery

• Exemption of import duty on raw

materials imported, used in

production for export.

• Non-tax incentives i.e. permission to

own land and permission to bring in

experts to work.

Same incentives

Maximise Shareholder Value 2016 27 October 2015

PwC

What is IHQ & ITCMilestone

• IHQ regimes were developed from the ROH regimes

• ITC regime was developed from IPC and IPO regimes

26

July 20, 2015

IHQ/ITC Timeline

IPO

ROH Regime 1

2002

IHQ & ITC

1999

2015

ROH Regime 2

2010

IPC

2011

Maximise Shareholder Value 2016 27 October 2015 26

PwC

Scope of Activities

27

Maximise Shareholder Value 2016 27 October 2015

PwC

PwC

Discrepancy of activities under IHQ

28

Supporting, Managerial &

Technical BOI RD FBA

Sourcing services Goods (RM and parts) RM and parts Services only (no trading

activities)

Other activities` `

Excluding services under

the list three attached to the

FBA e.g. accounting, legal,

architectural, engineering

TC Services BOI BOT RD

1) Treasury Centre under the Exchange

Control Law governed by BOT ` ` `2) Lending and borrowing of Thai

currency (“Baht”) in the following

cases:`

(a) Funds borrowed from Thai financial

institutions or associated enterprise

in Thailand; and`

(b) Funds obtained from TC operations`

Maximise Shareholder Value 2016 27 October 2015

PwC

Discrepancy of activities under ITC

29

ITC Services BOI RD FBA

Trading transactions

1) Out - Out ` `2) Out – In ` `3) In-In ` `4) In – Out `

Services relating to ITC

1) Procurement of goods ` `2) Storage of goods prior to delivery ` `3) Packaging services ` `4) Transportation of goods ` `5) Insurance of goods ` `6) Advisory, technical and training services

relating to goods` `

Maximise Shareholder Value 2016 27 October 2015

PwC

21 September 2015

Criteria and Condition for Operation and tax Maximising under IHQ and ITC

29

THB 10 million paid-up registered capital

Having the paid-up registered capital on the last day of each accounting period from

THB 10 million upwards

THB 15 million operating expenses

Having operating expenses paid to the receivers in Thailand not less than THB 15

million in each accounting period.

1 foreign associated enterprise

Providing services to at least 1 foreign associated enterprise.

ITC ITCIHQ IHQIHQ

BOI condition for investment promotion

RD conditions for tax maximizing

THB 1 million investment amount for each IHQ & ITC

Must have a new investment amount investing in fixed assets at least THB 1 million

per each.

Maximise Shareholder Value 2016 27 October 2015

30

PwC

Licensing Facilitation Act

31

27 October 2015 Maximise Shareholder Value 2016

21 July 2015came into effect

Enforcement:licensing, registration and any prior notification required by law

Every 5 years• A review to repeal licensing or replace licensing with other measures

• A review report to be submitted to the Cabinet for approval

Licensing Manuals

Prepare licensing manual for the public within 180 days from the date of announcement in Government Gazette. The manual must include:

Rules, procedures and conditions

Work flow and period of time for granting the license

Required documents to be attached to the application (no additional documents/evidence to be called)

1

3

2

Authority’s responsibilities

Review completeness of the application and documents /evidence

1

a) Advise the applicant if:

b) Write a memo of any deficiency and additional documents required, specify time period, give the memo to the applicant if there is no submission of requested documents by the deadline:

additional documents are required correction is needed; or

i. return application with written reason for the return; or

ii. the applicant may appeal

Consider the application within the specified period of time

2

a) After completion, notify the applicant within 7 days

b) If consideration is delayed, update the applicant every 7 days on reason of delaying until completion

Transitional provisions are not applicable to previously filed applications.

4

PwC

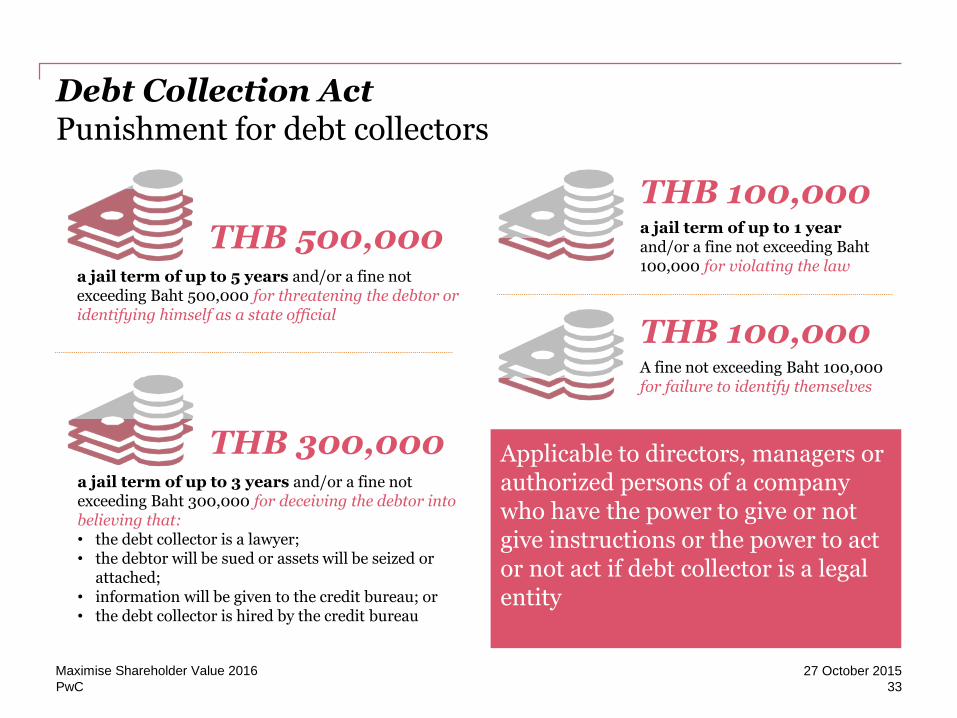

Debt Collection Act

32

27 October 2015 Maximise Shareholder Value 2016

Who are debtors?

a) Individualsb) Individual debt

guarantors

Who are debt collectors?a) A creditor who makes loans to debtorsb) A business operator under the law on

consumer protectionc) A person arranging gamblingd) Creditors in the ordinary course of businesse) Creditors’ authorized attorneys

Persons delegated by the attorneys to take charge of debt collection

f) Debt collection agency Debt collection agency’s authorized

attorneys Evidence must be presented for e) and f)

Communication with debtors• Debt collectors must:

Law enforcement

• Allow debtors to lodge complaints to the Committee

• Took effect on 2 September 2015)

Debt collector cannot do the following:

a) Threaten the debtor, use violence, use insulting language

b) Disclose a debt of the debtor to unrelated partiesc) Use false information to deceive the debtor, e.g.

falsely claiming to be a state official and threatening to sue the debtor or seize the debtor’s assets

d) Collect fees or expenses or force the debtor to write cheques, knowing that the debtor cannot pay.

e) Show information, symbol, mark or business name on any correspondence suggesting that the communication is about debt collection

f) Contact debtor via open letter, fax or “non-discreet” method

g) Contact other persons who are not debtors

5

a) Register themselves with the authority within 90 days from the end of 180 days of announcement

a) Notify debtor/identify themselves to debtor

b) Contact debtor by:

i. written notice to the address provided by debtor/ debtor’s domicile

ii. Hours of communication via all media; e.g. telephone, online media:

o From 8.00 a.m. – 8.00 p.m. on business days or 8.00 a.m. – 6.00 p.m. on public holidays

PwC

PwC

Debt Collection ActPunishment for debt collectors

33

27 October 2015 Maximise Shareholder Value 2016

THB 100,000A fine not exceeding Baht 100,000 for failure to identify themselves

THB 100,000a jail term of up to 1 yearand/or a fine not exceeding Baht 100,000 for violating the law

Applicable to directors, managers or authorized persons of a company who have the power to give or not give instructions or the power to act or not act if debt collector is a legal entity

THB 300,000a jail term of up to 3 years and/or a fine not exceeding Baht 300,000 for deceiving the debtor into believing that:• the debt collector is a lawyer;• the debtor will be sued or assets will be seized or

attached;• information will be given to the credit bureau; or• the debt collector is hired by the credit bureau

THB 500,000a jail term of up to 5 years and/or a fine not exceeding Baht 500,000 for threatening the debtor or identifying himself as a state official

PwC

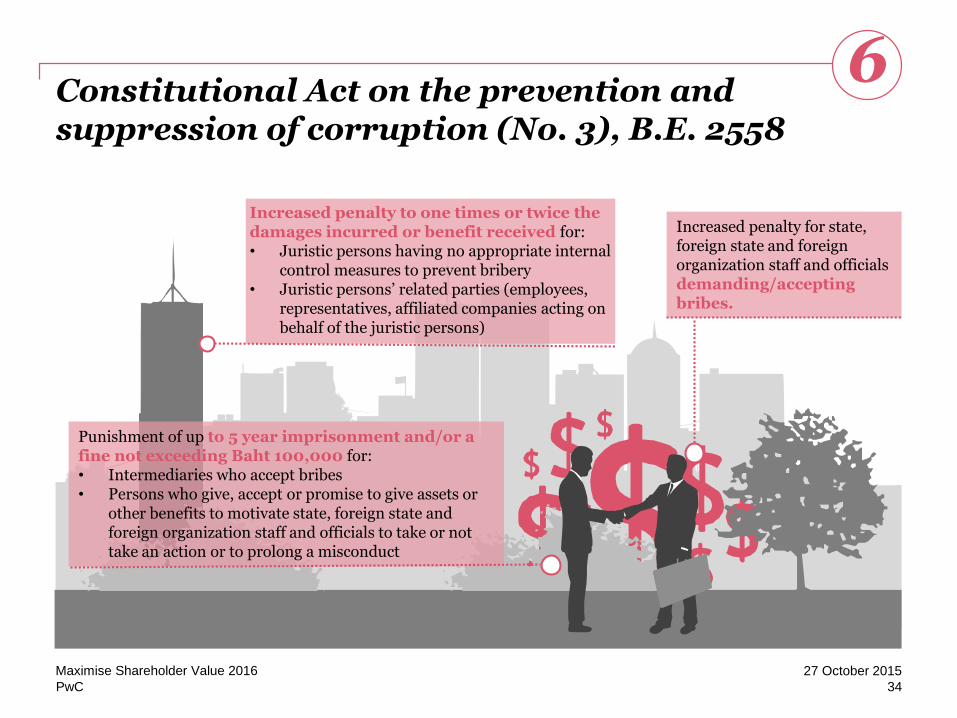

Constitutional Act on the prevention and suppression of corruption (No. 3), B.E. 2558

34

27 October 2015 Maximise Shareholder Value 2016

6

Increased penalty for state, foreign state and foreign organization staff and officials demanding/accepting bribes.

Punishment of up to 5 year imprisonment and/or a fine not exceeding Baht 100,000 for:• Intermediaries who accept bribes• Persons who give, accept or promise to give assets or

other benefits to motivate state, foreign state and foreign organization staff and officials to take or not take an action or to prolong a misconduct

Increased penalty to one times or twice the damages incurred or benefit received for:• Juristic persons having no appropriate internal

control measures to prevent bribery• Juristic persons’ related parties (employees,

representatives, affiliated companies acting on behalf of the juristic persons)

PwC

Machine Registration Act (No. 3), B.E. 2015

35

27 October 2015 Maximise Shareholder Value 2016

724 August 2015came into effect

MachineryMachine must pass inspection by the government official or a certified private machine inspection agency

Punishment

Submission of false report: imprisonment for a term up to one year and/or a fine not exceeding Baht 20,000

1

2

No ministerial regulations have yet been issued.

Relocation of mortgaged machinery out of the production line

for:

3 Violation by a juristic entity:

• Managing Director• Manager• Other persons

with authority to give instruction or not give instruction to take or not take actions

PwC

Provident Fund Act (No. 4), B.E. 2558

36

27 October 2015 Maximise Shareholder Value 2016

9

15%

Employees can choose to contribute at a max rate of 15%

Investment of provident fund Employees can choose

investment policy.

Options to receive provident fund payment

• Resign at the age of 55 Instalment payment

one lump sum payment

!

@

#

Social Security Act (No. 4) B.E. 2558

Employer or employee’s contribution payment can be

suspended or postpone if severely and economically affected by disaster

$

Benefits must not prejudice the rights and benefits that the insured or beneficiary is entitled to under other laws.

Additional benefits for the insured

Reduction of employer contribution if severely and economically affected by disaster.

!

@

#

8

Thank you

© 2015 PricewaterhouseCoopers Legal & Tax Consultants Ltd. All rights reserved. ‘PricewaterhouseCoopers’ and/or ‘PwC’ refers to the individual members of the PricewaterhouseCoopers organisation in Thailand, each of which is a separate and independent legal entity. Please see www.pwc.com/structure for further details.