th arab bank (switzerland) ltd. · arab bank annual report 2018 arab bank (switzerland) ltd. is an...

TRANSCRIPT

1 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018

57TH ANNUAL REPORT 2018ARAB BANK (SWITZERLAND) LTD.

SUMMARY

Board of Directors 6 CEO Message 10Executive Committee 1 2

CONSOLIDATED FINANCIAL STATEMENTS 2018 Consolidated Financial Highlights 1 8Comments on Consolidated Income Statement and Balance Sheet 1 9Consolidated Balance sheet and Off-Balance sheet Transactions 20Consolidated Income Statement 2 1Consolidated Cash Flow Statement 22Consolidated Statement of Changes in Equity 23

Notes to the Consolidated Financial statements 1 - Business Activities and Personnel 242 - Accounting Policies and Valuation Principles 263 - Information on the Consolidated Balance Sheet 304 - Information on Consolidated Off-Balance Sheet Transactions 425 - Information on the Consolidated Income Statement 436 - Consolidated Capital Adequacy and Liquidity Disclosure 45

Report of the Statutory Auditor on the Consolidated Financial Statements 47

FINANCIAL STATEMENTS 2018

Balance Sheet and Off-Balance sheet Transactions 50Income Statement 5 1Allocation of Earnings 52Statement of Changes in Equity 53

Notes to the Financial statements 1 - Business Activities and Personnel 542 - Accounting Policies and Valuation Principles 563 - Information on the Balance Sheet 604 - Information on Off-Balance Sheet Transactions 665 - Information on the Income Statement 676 - Capital Adequacy and Liquidity Disclosure 69

Report of the Statutory Auditor on the Financial Statements 71

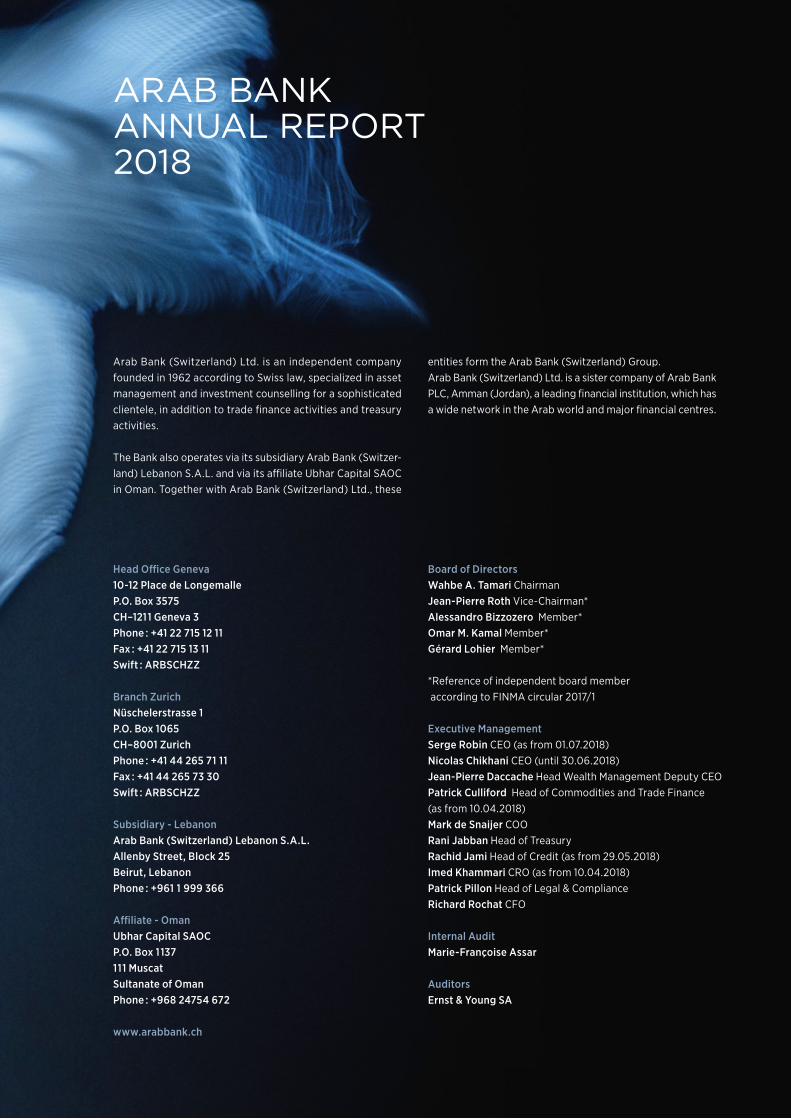

ARAB BANK ANNUAL REPORT 2018

Arab Bank (Switzerland) Ltd. is an independent company founded in 1962 according to Swiss law, specialized in asset management and investment counselling for a sophisticated clientele, in addition to trade finance activities and treasury activities.

The Bank also operates via its subsidiary Arab Bank (Switzer-land) Lebanon S.A.L. and via its affiliate Ubhar Capital SAOC in Oman. Together with Arab Bank (Switzerland) Ltd., these

entities form the Arab Bank (Switzerland) Group.Arab Bank (Switzerland) Ltd. is a sister company of Arab Bank PLC, Amman (Jordan), a leading financial institution, which has a wide network in the Arab world and major financial centres.

Board of DirectorsWahbe A. Tamari Chairman Jean-Pierre Roth Vice-Chairman*Alessandro Bizzozero Member* Omar M. Kamal Member* Gérard Lohier Member*

*Reference of independent board member according to FINMA circular 2017/1

Executive ManagementSerge Robin CEO (as from 01.07.2018)Nicolas Chikhani CEO (until 30.06.2018) Jean-Pierre Daccache Head Wealth Management Deputy CEO Patrick Culliford Head of Commodities and Trade Finance (as from 10.04.2018) Mark de Snaijer COO Rani Jabban Head of Treasury Rachid Jami Head of Credit (as from 29.05.2018)Imed Khammari CRO (as from 10.04.2018)Patrick Pillon Head of Legal & ComplianceRichard Rochat CFO

Internal AuditMarie-Françoise Assar

AuditorsErnst & Young SA

Head Office Geneva10-12 Place de LongemalleP.O. Box 3575CH–1211 Geneva 3Phone : +41 22 715 12 11Fax : +41 22 715 13 11Swift : ARBSCHZZ

Branch ZurichNüschelerstrasse 1 P.O. Box 1065CH–8001 ZurichPhone : +41 44 265 71 11Fax : +41 44 265 73 30Swift : ARBSCHZZ

Subsidiary - LebanonArab Bank (Switzerland) Lebanon S.A.L.Allenby Street, Block 25Beirut, LebanonPhone : +961 1 999 366

Affiliate - OmanUbhar Capital SAOCP.O. Box 1137111 MuscatSultanate of OmanPhone : +968 24754 672

www.arabbank.ch

6 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018

BOARD OF DIRECTORS

THE BOARD OF DIRECTORS IS COMPOSED OF FIVE NON-EXECUTIVE MEMBERS, CHAIRED BY MR WAHBE A. TAMARI.

Dear shareholders and clients,

It is with a great sense of pride that we look back on the achie-vements that have been made over the past year by Arab Bank (Switzerland) Ltd.

In a climate of economic uncertainty, we can reflect on our stead-fast commitment to all our stakeholders and the consistency with which we responsibly curate their wealth. And in a time where walls are as likely to be built as bridges, we can celebrate our vision to connect the Orient and Occident.

Indeed, the metaphor of a bridge is something that resonates profoundly with us at Arab Bank (Switzerland) Ltd.

As the first Arab banking institution in Switzerland and a sister organization of Arab Bank PLC, one of the oldest banks in the Middle East, we are culturally fluent in both markets we serve. This has enabled us to bring effective, customized financial so-lutions, crafted with the integrity and excellence of Swiss private banking culture, to our client base in the diaspora and MENA region.

We look toward 2019 with a strong sense of optimism. The appointment in July last year of industry leader, Monsieur S. Robin, as CEO reaffirms our commitment to the private banking industry and our wish to further develop this business line. But it also reinforces the culture of custodianship, ensuring we stay true to our core values as we seek to consolidate and expand our business.

One of the most exciting avenues is in Fintech. The recently launched Fintech Committee will help guide our program, positioning us at the cutting edge of banking innovation, and enabling us to reach a new, younger generation of investors.

Bridges are also being built by Arab Bank (Switzerland) Ltd. at another level. We believe that our promotion of art and culture is having a small but important role in showing another narrative of the Middle East. We also believe that our continued presence in the region will provide a bridge toward sustainable progress and economic development. We have a rich legacy in this area and are rightly proud of the contribution that Arab Bank PLC Group has made to the economic development of the Middle East over the years.

On behalf of the Board, I want to extend my thanks to you for your continued trust and confidence in Arab Bank (Switzerland) Ltd.

Wahbe A. TamariChairman of the Board of Directors

6 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 7 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018

Wahbe A. Tamari Chairman of the Board of DirectorsChairman of the Remuneration CommitteeMember of the Board Credit Committee

Wahbe A. Tamari is a graduate of Webster University Geneva, with a bachelor’s Degree in Management and is a Harvard Business School Owner/President Management (OPM43) Program Alumni.

Mr Tamari started his career at Sucafina S.A., where he held several positions from trader to CEO and now sits on its board. He is also the founder and Vice-Chairman of W&P S.A. Geneva, a Swiss based asset management firm.

Mr Tamari has a large experience in conducting business in the Middle East. He is a Board Member of the Consolidated Contractors Company (CCC) and Solidere International Ltd. He is also Chairman and Executive General Manager of ATFO SAL, a real estate management and investment company based in Beirut. Currently, he is Chairman of Arab Bank (Switzerland) Ltd., Member of the Board of Arab Bank PLC, Vice Chairman of Oman Arab Bank and of Ubhar Capital SAOC, and Chairman of Arabia Insurance Company SAL.

Mr Tamari sits on the board of the Tamari Foundation and is a member of the Advisory Committee of the Hassib J. Sabbagh Foundation. He belongs to the Board of LIFE (Lebanese Interna-tional Finance Executives) and is a member of the Welfare As-sociation and YPO Gold (Young President Organization Gold).

Jean-Pierre Roth Vice-Chairman of the Board of Directors Vice-Chairman of the Remuneration CommitteeMember of the Board Audit & Risk Committee

Jean-Pierre Roth, completed his doctorate in economics in Geneva at the Graduate Institute of International Studies. In 2009, the University of Neuchâtel awarded him an honorary PhD in economics. He joined the Swiss National Bank in 1979. On 1 May 1996, the Federal Council appointed him Vice-Chair-man of the Governing Board and Chairman (Governor) on 1 January 2001.

Mr Roth represented Switzerland as Governor of the Washing-ton-based International Monetary Fund (IMF). From 1 March 2006 to the end of February 2009, he was Chairman of the Board of Directors of the Bank for International Settlements in Basel. At the end of March 2007, he was designated Swit-zerland’s representative in the Financial Stability Forum. He retired from the SNB on 31 December 2009.

Mr Roth is now member of the Board of Directors of important Swiss companies (Nestlé, Swatch Group, MKS Switzerland) and member of the Board of various Swiss Foundations. He is Vice-chairman of Arab Bank (Switzerland) Ltd and was designated Member of the Board of Directors of Arab Bank Switzerland (Lebanon) in 2018.

8 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018

Alessandro BizzozeroMember of the Board of Directors Chairman of the Board Audit & Risk CommitteeMember of the Board FinTech Committee

Alessandro Bizzozero obtained his Doctorate in Law at the University of Fribourg.

Mr Bizzozero has more than 30 years of experience in the banking and regulatory field. He started his career at the Swiss Federal Banking Commission (today FINMA) where he was deputy Director of the Department of banking authorizations and mutual funds. He then joined one of the big four audit companies as Director in charge of the Regulatory Department. He was also Chief Group Compliance Officer of an important Banking Group in Geneva. Finally, he set up BRP Bizzozero & Partners S.A., one of the worldwide leaders in cross-border financial regulation.

Former Director of the CAS in Compliance Management and lecturer at the University of Geneva, Mr Bizzozero also teaches at the HEG ARC of Neuchâtel and at the Centro Studi Bancari of Lugano. He is also the author of several publications, including « Financial cross-border activities into and out of Switzerland ».

Mr Bizzozero is member of the Board of Directors of several Swiss banks (Cornèr Banca SA, Landolt & Cie SA, and GS Banque SA).

Gérard LohierMember of the Board of Directors Chairman of the Board Credit CommitteeMember of the Board Audit & Risk CommitteeMember of the Board FinTech Committee

Gérard Lohier joined in 1960 a French Banking Group which became through successive mergers BNP Paribas. He was gi-ven Commercial assignments in France and French Overseas Territories before being nominated Inspector and then Chief Inspector at Group level (1976).In this position, Mr Lohier acquired the International exposure and banking expertise that lead to further overseas assign-ments:Deputy General Manager, International Division UBA Lagos (1980),Deputy General Manager BNP Switzerland Basel (1982),Managing Director BNP International Financial Services Sin-gapore (1985),General Manager BICI de Côte d’Ivoire Abidjan (1988),Head of Territory BNP Paribas Switzerland Geneva (2000).

In the midst of his International career, Mr Lohier was nomi-nated in Paris, Deputy General Manager of BNP Intercontinental (1992), Secretary General of BNP Investment Banking (1994) and, as Group Head of Corporate Banking (1997), member of the Bank’s Group Executive Committee.Mr Lohier was thus involved operationally and through his various Board positions, in almost all aspects of banking. Currently, he is also member of W&P S.A. Geneva, a Swiss based asset management firm.

8 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 9 | ARAB BANK (SWITZERLAND) LTD.

Dr. Omar KamalMember of the Board of DirectorsChairman of the Board FinTech Committee Member of the Board Credit Committee

Omar Kamal has more than 20 years' experience in the field of financial services. He was first a partner with Ernst & Young on the advisory and consulting side and then one of the initial founders and the CIO of a regional bank in the Middle East. Until August 2015, he was the co-Group CEO of a business group owned by a prominent family with global reach based in Geneva, Switzerland.

Mr Kamal serves now on the board of a number of listed and unlisted companies amongst others, Tharisa mining (FTSE listed), Cambridge Scientific Innovation (CSI) and Cybsafe. In his various positions, he brings always a strategic contribution towards digital innovation and transformation.

Mr Kamal is a member of the Young President Organisation, previously under the Alpine Chapter in Switzerland, and cur-rently serves as the London Stars Chapter Membership Chair in the United Kingdom.

10 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018

CEO MESSAGE

2018 will be remembered as a turning point in economic acti-vity. Sustained growth was replaced by a global downturn, particularly pronounced in Europe and Asia. The Federal Re-serve continued to raise the target rate and the US-China trade war became a major focus in the 4th quarter, which can be indicative of a shift away from globalization. Investors have grown accustomed to the fact that political turbulence – with its strong influence on markets – is the new normal. Brexit, and its still-uncertain outcome, is a perfect illustration of this new paradigm, as is the US government shutdown. Indeed, there are many signs that higher volatility is here to stay across all asset classes. As with every paradigm shift, however, we be-lieve it’s important to look at the positives and, going forward, to seize the many investment opportunities that will emerge. It’s all the more impressive that, despite this challenging macro and market environment, our bank delivered strong and ba-lanced results, with our three pillars – Wealth Management, Commodity Trade Finance (CTF), and Treasury – experiencing consistent growth. Total operating income reached CHF 79,6 million, representing an increase of 20% over 2017. Wealth Management and CTF grew by 17% and 12% as strong forex results enabled Treasury to deliver an increase of 31%. In short, our net profits amounted to CHF 17,1 million, representing growth of 21%.

Behind these excellent results were a range of initiatives and activities. Our Wealth Management business line delivered robust growth thanks to service model enhancements and a more focused approach to improving client service. Our In-vestment Advisory team was strengthened through the addi-tion of seasoned, dedicated specialists, which enabled us to reach out to our clients in a more optimized and structured way. These initiatives have translated into +CHF 250 million net new money bringing our Assets under Management to CHF 3’825 million. We have also restructured our Advisory mandates to better fulfill client needs. Active advisory, classic advisory and ad-hoc advisory mandates have been rolled out

and provide a tailored investment solution to each of our client profiles. In terms of investment solutions, we are now working in a full open architecture framework, which allows our customers to have access to large, best-in-class vehicles for each building block of a balanced portfolio. Large invest-ment menus, translated into focused model portfolios, and a strong franchise in Private Equity and Private Debt, with our Real Estate fund as a flagship offering, lie at the heart of our investment philosophy. Moving forward, we will also launch a Strategic Wealth Allocation Center of Competence in the first quarter of 2019, with a goal of helping our key rela-tionships to optimize their total wealth through customized investment solutions.

Commodities Trade Finance pursued the development of its Energy, Metals and Agri commodities portfolios as per the MENA strategic plans, by expanding its client base and diver-sifying both its geographical scope and product offering. CTF teams have been marketing a wide range of trade finance products and services, optimizing delivery and execution, enabling our bank to keep an edge over competition while simultaneously maintaining a strong risk control framework.

With higher US interest rates, a higher dollar, a number of emerging market currency crises, and a spike in volatility at the end of 2018, the Treasury department has been able to take advantage of fluctuations in currencies to generate more alpha for our portfolios. We have continued to modernize and optimize our service offering, with the launch of our FX plat-form on the Ipad. We also have further strengthened our expertise in complex OTC options structures.

Our bank continued to invest in its IT infrastructure in order to optimize and automate processes while maintaining high IT security standards and improving its technological platform. The digital banking service offering is also an important area in which we decided to invest in 2018 to improve the digital experience as well as the reactiveness and quality of the

10 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 11 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018

services we offer. As an example, a new website was launched in the summer of 2018 and on-line payments are now pro-posed to clients through the e-banking system. Looking forward to 2019, our bank will further focus on improving operational efficiency in support of its strategy and prepare its business to meet upcoming regulatory requirements as well as execute digitalization initiatives and develop electro-nic service channels.

On behalf of our Executive Committee and myself, I would like to thank all our customers for their longstanding trust and business. It has been a privilege and a pleasure for me to have joined the Bank last year. We, as the management team, will continue to make every effort to satisfy our customers in the years ahead through the strategic developments in our pipe-line. Last but not least, I would also like to take this opportunity to thank our shareholders and the Board of Directors for their continuous support as well as all our colleagues for their hard work, dedication, and commitment to delivering results.

Serge Robin

12 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018

EXECUTIVE COMMITTEE

Serge Robin Chief Executive Officer (CEO)

Graduate in Economics and Quantitative analysis, Serge has 35 years’ experience in Asset Management & Research, as well as client facing, and 25 years in management sizeable teams, including at CEO level.

After having spent a year as an auditor, Serge joined Lombard, Odier as a research analyst on the Japanese market. He became Head of Research in 1994 and Head of Asset Management & Research in 1999. He was in charge of more than 200 staffs located in Geneva, Zürich, Amsterdam, London, Montreal and Honk-Kong. His team was managing both institutional and pri-vate money across all type of mandates and asset classes, in-cluding sectorial specialized funds, notably in the life science and technology domains. He also opened the Tokyo office, a marketing hub to develop Private Clients.

Serge then join UBS in 2001 as Managing Director within a team whose mission statement had been to build the « Family Bu-siness Group », a center of competence taking care of UHNW clients worldwide, which was renamed key clients later on.

In 2005, he was appointed CEO of Merrill Lynch Bank (Suisse) S.A. His mandate was to design and implement a growth strate-gy for Institutional and Private Clients with a focus on the Swiss onshore market. He revamped the whole management func-tions, structure and organization to support the growth plans.

In 2010, he joined Gonet, a Swiss Private Bank, as a Managing Partner.

Jean-Pierre Daccache Head of Wealth Management (Deputy CEO)

Prior to joining Arab Bank (Switzerland) Ltd., Jean-Pierre was a Managing Director and Global Sector Head at HSBC Private Bank where he managed the Upper-Gulf, Levant and North Africa region. He served on various regional and local exe-cutive committees.

Prior to HSBC, he was a Principal at Capital E advisors in New York, a boutique private equity firm. Prior to Capital E, he served as co-head of the MENA and Western European wealth management division at The Bank of New York in New York.

Jean-Pierre is the holder of a Juris Doctor degree as well as an active member of the Bar of the State of Texas since 1991. He is currently an active member of LIFE and was previously elected for two terms on its Board of Directors. Jean-pierre is also involved with SEAL, a charitable organization registered as a 501 (C3) in the State of New York.

THE EXECUTIVE COMMITTEE IS COMPOSED OF NINE MEMBERS, CHAIRED BY MR SERGE ROBIN.

12 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 13 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018

Rani Jabban Head of Treasury and Financial Institutions

Rani holds a Msc. in Economics and a graduate from Magis-tère Banque Finance from University Paris 2 Pantheon-Assas (1994).

In 1995, Rani worked as a Forex and Treasury dealer at BFO London (Credit Agricole group) and joined Credit Agricole (Suisse) S.A as senior manager FX advisory in 2000.

Since 2009, he is the Head of Treasury at Arab Bank (Swit-zerland) Ltd. Appointed to the Executive Committee in 2014, he is now in charge of Treasury, Trading, Financial Institutions, and Marketing.

Richard Rochat Chief Financial Officer

Richard holds an economic degree from the University of Geneva and from Swiss Certified Accountant institute. In 1994, Richard started his career as auditor at Ernst & Young. In 2009, he took the role of Head of Finance and Risks, member of the Executive Committee, in a newly implemented foreign bank branch in Switzerland. From 2009 to 2012, he was auditor in charge at KPMG and was authorized banking auditor by the Swiss Financial Market Supervisory Authority FINMA. Richard has been Chief Finan-cial Officer and a member of the Arab Bank (Switzerland) Ltd. Executive Committee since 1 August 2012. Since 2014, he also chairs the Pension Fund of Arab Bank (Switzerland) Ltd.

14 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018

Patrick Culliford Head of Commodities and Trade Finance

Patrick holds a Bachelor of Science in Political Economy de-gree from the University of Geneva.

After starting his career in auditing with renown audit firm PricewaterhouseCoopers in 1992, he moved in 1995 to Banque Indosuez (subsequently Credit Agricole Indosuez) as a member of the Credit and risk Department.

In 1998, he moved to United European Bank which subse-quently became BNP Paribas (Suisse) SA, initially as a member of the Credit and Risk department, then joined in 2001 the front office as Senior Relationship Manager with a focus on soft commodities in the Black Sea and Middle East areas.

End of 2009, he joined Arab Bank (Switzerland) Ltd. to start the Commodities & Trade Finance division which has success-fully developed into a core business of the Bank.

Rachid Jami Head of Credit

Rachid joined Arab Bank (Switzerland) Ltd. in May 2011 as Head of Credit. He was appointed to the Executive Committee in May 2018. Additionally, he serves as Deputy Chairman of the Bank’s Credit Committees and acts as Secretary of the Board of Directors Credit Committee. He was Board Member of Arab Bank Pension Fund from 2014 to 2017 representing the Bank’s employees.

Prior to joining Arab Bank (Switzerland) Ltd., he began his financial career in 2000 in Switzerland at American Express Geneva, followed by Banque Migros SA. He then joined So-ciété Générale Suisse SA and BNP Paribas Suisse SA where he worked as a Senior Credit Analyst.

Rachid holds a MSc. in economics from the Hassan II Univer-sity of Casablanca.

Imed Khammari Chief Risk Officer

Imed holds a Master’s Degree in Banking and Finance from the University of Lausanne. Since June 2012, he occupies the position of Chief Risk Officer of Arab Bank (Switzerland) Ltd. and was appointed to the Executive Committee in April 2018. From 2006 to 2012, he occupied the position of deputy Chief Risk Officer at Tradition Group. Before that, he worked for EFG group as senior risk auditor from 2003 to 2006. From 1998 to 2003, he was risk manager at Ernst & Young.

14 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 15 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018

Patrick Pillon Head Legal & Compliance

Patrick holds a law degree from the University of Geneva and was admitted to the Geneva bar in 1997. After working several years as a partner in a law firm in Geneva (Woodtli & Asso-ciés), he joined an international financial institution based in Switzerland (BNP Paribas Suisse SA) in 2000 as member of the Management and senior legal counsel specialized in com-modity trade finance activities. In 2009, he joined Arab Bank (Switzerland) Ltd. where he was appointed to the Executive Committee in May 2012, as responsible for the Legal & Compliance function. In addition, he acts as Secretary of the Board Audit & Risk Committee.

Mark de Snaijer Chief Operating Officer

Mark holds a doctorate in economics, thesis in industrial eco-nomics, University of Berne. In 1992, he worked at the Credit department of Swiss Bank Corporation in Basel.

From 1993 until 2000, he worked as a researcher, first at the University of Berne at the newly founded Department of Eco-nomics, and finalized his doctoral thesis later at Credit Suisse Group in Zurich.

The year after, he worked at the Cantonal Bank of Basel Land in Liestal as Chief of Staff, and joined in 2001 its subsidiary ATAG Asset Management in Berne as Head Business Development for four years.

From 2006 until 2009, he worked for Bank CIC (Suisse) in Basle, first as Head Operations and Deputy COO and from 2007 as COO and member of the Executive Committee. Starting 2010, he joined Arab Bank (Switzerland) Ltd., first as deputy COO and Head Client Services & Logistics, and in 2012 as COO and member of the Executive Committee.

CONSOLIDATED FINANCIAL STATEMENTS 2018

18 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS

CONSOLIDATED FINANCIAL HIGHLIGHTS

CHF MILLION2018 2017 VARIANCE VARIANCE

%

Balance SheetBalance sheet total 3 857 3 454 403 12

Amounts due from customers 1 291 1 059 232 22

Trading portfolio and financial investments 451 436 15 3

Shareholders’ equity (before profit distribution) 560 536 24 4

Income StatementResults from interest operations 17 2 1 - 4 - 19

Results from commissions from business and services 29 28 1 4

Net income from trading operations 33 18 15 83

Other results from ordinary activities - 0.3 - 1 0.7 - 70

Operating expenses - 47 - 49 2 - 4

Gross Profit 32 17 15 88

Depreciation, provisions, value adjustments and losses - 4 9 - 13 - 144

Operating result 28 26 2 8

Net extraordinary results, and change in reserves for general banking risks 2 - 3 5 - 167

Taxes - 13 - 9 - 4 44

Consolidated profit for the period 17 14 3 21

18 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS 19 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS

COMMENTS ON CONSOLIDATED INCOME STATEMENT AND BALANCE SHEET

Consolidated Income StatementThe consolidated net income increased from CHF 14.1 million in 2017 to CHF 17.1 million in 2018 (+21%). Despite the fact that the Bank is facing a challenging global environment and increa-sing competition for MENA clients, the three business lines, Commodity and Trade Finance, Private Banking and Treasury have strongly increased their activity volumes and their pro-fitability over 2018.

The negative interest rates applied by the SNB on deposits held with them had a major impact on our net interest income which ended at CHF 17.4 million in 2018 (CHF 21.1 million in 2017).

The result from commissions and service fees increased by 5 % to reach CHF 29.3 million, mostly attributable to the trade finance and private banking activities.

The results from trading operations increased by 80%.

The heavy extra costs incurred due to new requirements and regulations have been mitigated by very strong cost controls which led to an operating expense total of CHF 47.3 million.

The cost/income ratio dropped from 74% to 59% .

Consolidated Balance Sheet and Off-Balance SheetThe total consolidated Balance Sheet amounted to CHF 3.9 billion at the end of 2018. The consolidated balance sheet is very liquid as the Bank has maintained an average deposit with the Swiss National Bank of around CHF 1.0 billion over the course of the year.

Loans to customers were at CHF 1’291 million and mortgages at CHF 81 million.

Assets under Management amounted to CHF 3.8 billion as of 31st December, 2018.

20 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS

CONSOLIDATED BALANCE SHEET AND OFF-BALANCE SHEETTRANSACTIONSAT DECEMBER 31, 2018

CHF 2018 2017 VARIANCE

AssetsLiquid assets 1 045 382 898 805 832 016 239 550 882

Amounts due from banks 827 781 846 906 31 8 055 - 78 536 209

Amounts due from customers 1 290 923 804 1 058 729 822 232 193 982

Mortgage loans 81 433 21 3 86 581 105 - 5 147 892

Trading portfolio 22 364 155 27 720 280 - 5 356 1 25

Positive replacement values of derivatives 20 158 437 9 747 872 10 410 565

Financial investments 428 203 328 408 280 953 19 922 375

Accrued income and prepaid expenses 53 809 330 48 386 80 1 5 422 529

Participations 50 006 184 65 934 1 56 - 1 5 927 972

Tangible fixed assets 32 097 586 33 784 737 - 1 687 1 5 1

Other assets 5 309 1 1 3 2 296 299 3 012 814

Total assets 3 857 469 894 3 453 612 096 403 857 798

Total subordinated claimsOf which with conversion obligation and / or debt waiver

123 6 13 774 0

1 22 376 679 0

1 237 095 0

LiabilitiesAmounts due to banks 2 139 575 735 1 659 777 878 479 797 857

Amounts due to customers 1 072 306 983 1 1 59 918 379 - 87 6 1 1 396

Negative replacement values of derivatives 22 553 144 1 5 541 065 7 01 2 079

Accrued expenses and deferred income 55 033 707 50 434 223 4 599 484

Other liabilities 1 226 063 772 49 1 453 572

Provisions 6 754 224 3 1 333 337 - 24 579 1 1 3

Reserves for general banking risks 98 6 13 36 1 84 446 048 14 1 67 3 1 3

Share capital 26 700 000 26 700 000 0

Reserves from capital contribution 0 7 309 950 - 7 309 950

Retained earnings 416 772 125 402 632 78 1 14 139 344

Reserves for currency translation 814 939 606 600 208 339

Consolidated profit for the period 17 1 1 9 6 13 14 139 344 2 980 269

Total liabilities 3 857 469 894 3 453 612 096 403 857 798

Off-balance sheet transactions Contingent liabilities 395 855 453 306 476 809 89 378 644

Irrevocable commitments 73 419 744 80 808 094 - 7 388 350

Credit commitments 4 727 624 2 1 7 1 5 658 - 1 6 988 034

20 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS 21 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS

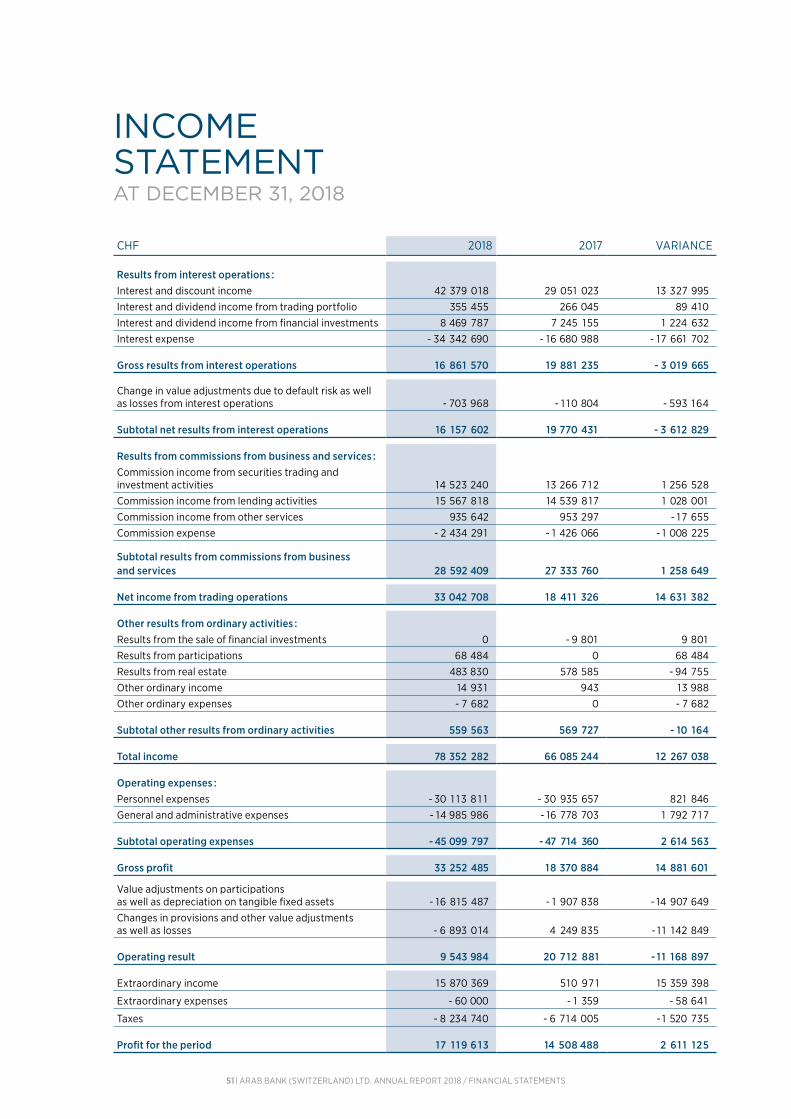

CONSOLIDATEDINCOME STATEMENTAT DECEMBER 31, 2018

CHF 2018 2017 VARIANCE

Results from interest operations :Interest and discount income 43 589 934 30 382 906 13 207 028

Interest and dividend income from trading portfolio 355 455 266 045 89 410

Interest and dividend income from financial investments 8 469 787 7 245 155 1 224 632

Interest expense - 34 342 689 - 16 680 988 - 17 661 70 1

Gross results from interest operations 18 072 487 21 213 1 1 8 - 3 140 631

Change in value adjustments due to default risk as well as lossesfrom interest operations - 703 969 - 1 10 804 - 593 165

Subtotal net results from interest operations 17 368 51 8 21 102 314 - 3 733 796

Results from commissions from business and services :Commission income from securities trading and investment activities 14 523 240 13 266 7 12 1 256 528

Commission income from lending activities 15 567 8 1 7 14 539 81 7 1 028 000

Commission income from other services 952 335 1 002 009 - 49 674

Commission expense - 1 7 1 1 409 - 963 7 1 5 - 747 694

Subtotal results from commissions from business and services 29 331 983 27 844 823 1 487 160

Net income from trading operations 33 229 595 18 503 732 14 725 863

Other results from ordinary activities :

Results from the sale of financial investments 0 - 9 801 9 801

Income from participations - 872 999 - 1 438 889 565 890

of which participations valued according to the equity method - 872 999 - 1 438 889 565 890

Results from real estate 483 830 578 585 - 94 755

Other ordinary income 60 088 1 314 58 774

Other ordinary expenses - 7 681 0 - 7 681

Subtotal other results from ordinary activities - 336 762 - 868 791 532 029

Total income 79 593 334 66 582 078 13 011 256

Operating expenses : Personnel expenses - 31 610 1 33 - 32 1 1 4 925 504 792

General and administrative expenses - 1 5 704 5 1 7 - 1 7 236 272 1 531 755

Subtotal operating expenses - 47 3 14 650 - 49 351 197 2 036 547

Gross profit 32 278 684 17 230 881 15 047 803

Value adjustments on participations as well as depreciation on tangible fixed assets - 16 936 574 - 2 022 035 - 14 9 14 539

Changes in provisions and other value adjustments as well as losses 12 91 1 440 1 1 148 032 1 763 408

Operating result 28 253 550 26 356 878 1 896 672

Extraordinary income 15 870 369 510 971 15 359 398

Extraordinary expenses - 60 000 - 1 358 - 58 642

Change in reserves for general banking risks - 14 1 67 3 1 3 - 4 064 414 - 10 102 899

Taxes - 12 776 993 - 8 662 733 - 4 1 1 4 260

Consolidated profit for the period 17 1 1 9 613 14 139 344 2 980 269

22 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS

CONSOLIDATED CASH FLOWSTATEMENT

2018 2017

CHF 1 000SOURCE OF

FUNDSAPPLICATION

OF FUNDSSOURCE OF

FUNDSAPPLICATION

OF FUNDS

Cash flow from operating businessProfit for the period 17 120 14 139

Reserves for general banking risks 14 1 67 4 064

Value adjustments on participations as well as depreciation on tangible fixed assets 16 937 4 143

Provisions and other value adjustments 24 579 1 1 502

Accrued income and prepaid expenses 5 423 9 995

Accrued expenses and deferred income 4 599 6 603

Previous year dividend 7 310 7 310

Balance 15 5 1 1 142

Cash flow from transactions in participations and tangible fixed assetsParticipations 928 2 459

Reserves for currency translation 208 388

Real estate 584 584

Other tangible fixed assets 335 1 96

Balance 887 3 627

Cash flow from the banking businessMedium to long-term business (>1 year)Other liabilities 454 64

Amounts due from customers 3 033

Mortgages loans 5 148 8 140

Financial investments 30 131 47 545

Other receivables 3 013 124

Short-term businessAmounts due to banks 479 798 1 77 168

Liabilities from securities financing transactions 64 265

Amounts due to customers 87 61 1 310 25 1

Negative replacement values of derivatives 7 012 2 575

Amounts due from banks 78 536 92 7 1 1

Amounts due from customers 229 1 61 81 61 8

Amounts due arising from trading transactions 5 356 23 358

Positive replacement values of derivatives 10 4 1 1 229

Financial investments 10 209

LiquidityLiquid assets 239 551 38 545

Balance 16 398 3 485

Total source of funds 16 398 3 627

Total application of funds 16 398 3 627

22 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS 23 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS

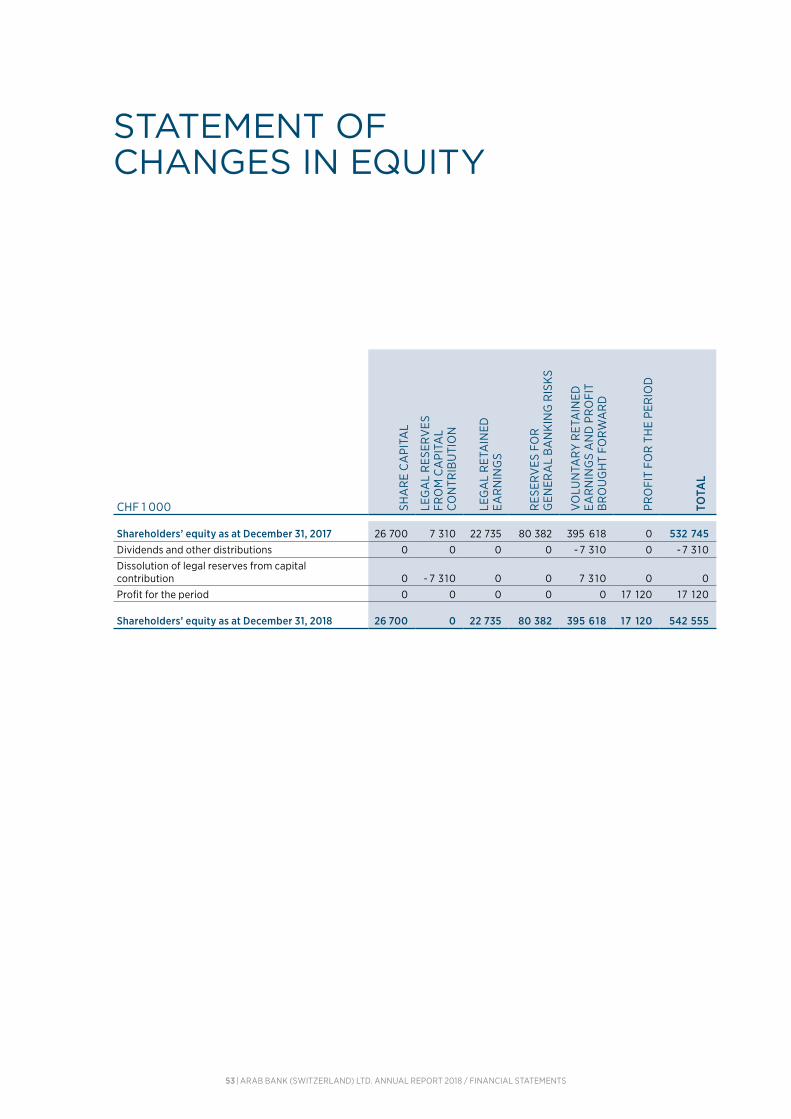

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

CHF 1 000 SHA

RE

CA

PITA

L

RES

ERV

ES F

ROM

C

API

TAL

CON

TRIB

UTI

ON

RES

ERV

ES F

OR

GEN

ERA

L BA

NKI

NG

RIS

KS

RET

AIN

ED E

AR

NIN

GS

RES

ERV

ES F

OR

CUR

REN

CY

TR

AN

SLAT

ION

CON

SOLI

DAT

ED P

ROFI

TFO

R TH

E PE

RIO

D

TOTA

L

Shareholders’ equity as at December 31, 2017 26 700 7 31 0 84 446 41 6 772 607 0 535 835Dividends and other distributions 0 0 0 - 7 310 0 0 - 7 31 0

Dissolution of reserves from capital contribution 0 - 7 31 0 0 7 31 0 0 0 0

Allocation to the reserves for general banking risks 0 0 14 1 67 0 0 0 14 1 67

Translation differences 0 0 0 0 208 0 208

Consolidated profit for the period 0 0 0 0 0 17 120 17 120

Shareholders’ equity as at December 31, 2018 26 700 0 98 613 41 6 772 815 17 120 560 020

24 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS

Arab Bank (Switzerland) Ltd. (“Bank”) is the main and parent company of Arab Bank (Switzerland) Group (“ABS Group”). Arab Bank (Switzerland) Ltd. is constituted according to Swiss law as an independent company. It started operations in 1962 in Zug, then moved its operations to Zurich soon afterwards. It opened a branch in Geneva in June 1964. The Bank head-quarters were located in Zurich until their transfer to Geneva in 2012. The Bank has a branch in Zurich.

The focus of ABS Group services is on providing asset mana-gement and investment advisory as well as financial planning services for private and institutional clients, in addition to Commodity Trade Finance and other credit-related products and services for commercial and corporate clients.

ABS Group also operates via its subsidiary Arab Bank (Swit-zerland) Lebanon S.A.L., Lebanon and its associate company Ubhar Capital SAOC, Oman.

ABS Group employed 120 people, of which 14 people abroad, on a full-time equivalent basis at the end of 2018 (previous year: 120 people, of which 13 people abroad).

FINMA’s regime for banks of category 4 and 5 In 2018, the Swiss Financial Market Supervisory Authority FINMA has defined a new regime for banks of category 4 and 5 that have high levels of capital and liquidity. Participating institutions will be subject to a substantially less complex regu-latory regime. The regulatory requirements regarding the risk-weighted assets, the net stable funding ratio and disclosure are reduced to a minimum. FINMA, in its July 12th, 2018 letter, has accepted Arab Bank (Switzerland) Ltd in this new regime.

BUSINESS ACTIVITIES

Wealth Management Wealth Management caters and responds to the private banking needs of its predominantly Middle-Eastern cliente-le, providing it with tailor-made solutions and access to an open platform covering the full range of wealth management products, services, mainly investment management, such as advisory services and discretionary portfolio management as well as market research.

Commodities Trade FinanceThe Commodities Trade Finance division ABS Group created at the end of 2009 has become a reference name in the com-modities trade finance sector. ABS Group offers tailored made solutions to finance predominantly Commodities Trading com-panies active in the Soft Commodities, Ferrous and non-Fer-rous Metals and Energy fields with a particular focus on flows going to or originating from the MENA region.

Credit / Financing products and servicesABS Group provides a comprehensive range of credit ins-truments (various types of loans such as Lombard loans, mortgages and guarantees) to its private banking clients en-abling them to fund their commercial business or leverage their private portfolios. ABS Group also offers credit solutions including a comprehensive range of commercial loans and do-cumentary products to its Commodities Trade Finance clients base of commodities trading companies, local exporters and large corporates.

Treasury and Foreign ExchangeABS Group provides its clients with a wide range of products and services in Money Market, Foreign Exchange, Precious Metals and Securities Trading.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

1 - BUSINESS ACTIVITIESAND PERSONNEL

24 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS 25 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS

RISK MANAGEMENT & CONTROL

GeneralABS Group has established and implemented a comprehen-sive set of internal policies and procedures in order to manage and monitor the key risks to which it is exposed, and to ensure that Swiss laws and all the relevant guidelines and regulations issued by FINMA and Swiss Bankers Association, as well as the internal rules of ABS Group, are adhered to. Whenever risks are taken, they are identified, measured, monitored and mitigated accordingly.

In conformity with the Swiss Code of Obligations, the Board of Directors formally reviews annually the bank’s key risks and, whenever deemed necessary, takes appropriate measures.

Credit RisksCredits and loans are granted according to clear rules, regula-tions and competencies approved by the Board of Directors. Lending ratios for all categories of collateral have been de-fined. Credit risks are mitigated by strict monitoring of limits (counterparty, group, country) and quality collaterals are as-sessed and reviewed on a regular basis.

Market risksABS Group defines various limits regarding the nature, quality, currency and duration of investments for the Banking and the Trading Book. Beside the daily management of the market risks by Treasury, ABS Group’s Asset & Liability Committee monitors these risks and adherence to the limits on a conti-nuous basis.

As a rule, interest rate risk is minimized by funding loans with matching maturities. ABS Group optimizes asset and liability management in accordance with the anticipated interest rate variation and the limits granted. ABS Group defines limits for refinancing gaps for the Net Economic Value and monitors adherence to these limits on a regular basis.

Liquidity RisksABS Group monitors its liquidity in a way to ensure adequate levels at all times, in line with the regulatory requirements per-taining to the liquidity ratios. Operational RisksABS Group has clear policies, regulations and procedures in place, and maintains an overall control infrastructure that is re-gularly amended to factor-in changes occurring in ABS Group. The assessment of the control framework is reviewed and va-lidated on a regular basis by the Board of Directors upon the Audit Committee recommendation.

Legal & Compliance RisksABS Group implements comprehensive measures to ensure compliance with laws and regulations in order to mitigate legal and reputational risks. The Legal & Compliance department is responsible for supervising these aspects. AML-related risk is subject to Compliance’s continuous focus. Regulatory changes are followed-up upon and are duly and regularly reflected in the Group’s policies.

Compliance ensures appropriate training of the Group’s em-ployees on all relevant subjects.

26 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS

General PrinciplesAccounting and valuation principles are governed by the Swiss Code of Obligations, the Federal Law on banks and savings banks, its ordinance and its execution by the Articles of Asso-ciation and the directives issued by the Swiss Financial Markets Supervisory Authority (FINMA).

The consolidated financial statements are presented in confor-mity with the FINMA circular 2015/1 – Accounting - Banks.

The consolidated financial statements are prepared in accor-dance with the rules applicable in Switzerland to consolidated financial statements, using the true and fair view principle.

Consolidation methodThe entities directly or indirectly controlled by ABS Group are consolidated using the global integration method. The share capital is consolidated using the purchase method.

The entities held between 20% and 50% are accounted for un-der the equity method. The net assets and net profit of those entities are reflecting in the consolidated financial statements in proportion to the Group’s percentage stake.

ABS Group’s internal transactions, as well as the intercompany profits, are reported as elimination entries when establishing the consolidated financial statements.

Holdings less than 20% are recognized in non-consolidated participations and are reported in the balance sheet at acqui-sition value, after deduction of any impairment required by the circumstances.

Scope of Consolidation The scope of the consolidation includes, as of 31 December 2018, the following entities :• Arab Bank (Switzerland) Ltd. (ABS), the parent company, • Arab Bank (Switzerland) Lebanon S.A.L., Lebanon, wholly owned by ABS, which activity is Private Banking. Share Capital is LBP 15’000 million.• Ubhar Capital SAOC, Oman, 34% owned by ABS, which provides investment services. Share Capital is OMR 14 million.

Recording of transactionsAll operations executed at the date of the balance sheet were accounted for and evaluated according to recognized prin-ciples. The results of all operations executed are included in the income statement. Recording in the balance sheet of spot transactions, concluded but not yet settled, is done following the trade date accounting principles.

Timeliness of recognitionIncome and expenses are booked as soon as they are acquired or accrued, or as they are incurred, and booked in the related year, and not on the date they are received or paid.

The most important valuation principles can be summarized as follows :

Foreign currency translationsAssets and liabilities denominated in foreign currencies are translated into Swiss francs at the exchange rates on the balance sheet closing date, except the participations which are translated at the historical rate. Income and expenses are converted at the exchange rate in force on the transaction date. Exchange gains and losses resulting from conversion into Swiss Francs of positions and operations denominated in foreign currencies are booked to Income from trading.

Translation of foreign currencies in ABS Group financial statementsFor consolidation purposes, in order to convert into CHF the annual financial statements denominated in foreign curren-cies, the following methods have been applied.

For the balance sheet, the closing rate has been used, except for equity which has been converted using historical rates.

For the income statement, the average rate has been applied.

The resulting foreign exchange differences have been ac-counted for in the reserves for currency translation (equity), without impacting the income statement.

2- ACCOUNTING POLICIES AND VALUATION PRINCIPLES

26 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS 27 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS

The rates applied for the conversion of the main currencies into Swiss francs are the following :

CLOSING AVERAGE 31.12.2018 2018USD 0.9843 0.9767EUR 1 . 1 266 1 . 15 19GBP 1.2545 1 .3006CAD 0.7266 0.7533

Liquid assets and amounts due to / from banks These balances are shown on the balance sheet at the nominal value after deduction of individual bad debt provisions, if any are required.

Claims and liabilities in respect of customers and mortgage loansThese amounts are recorded at their nominal value. Valuation adjustments are made for identifiable risks. General provisions exist for contingent risks. Lending against collateral is made within the generally accepted lending principles. These are stipulated in the internal rules and regulations. The valuation of real estate is based on market value, which is determined according to generally accepted valuation methods.

Impaired customer loans are subject to individual valuation and, should the case arise, to an individual value adjustment, directly deducted from this caption, equivalent to the part of the amount which is not secured by collateral, as soon as the loan is reported impaired.

Interest and commission income, which is overdue for more than 90 days, will only be booked after payment. Trading positions in securities and precious metalsTrading positions are valued at market prices on the balance sheet date.

Profits and losses on prices are booked to result from trading operations.

Replacement values of derivative financial instrumentsReplacement values of derivative financial instruments are calculated and accounted for in order to take into account the cost or the gain resulting from a potential counterparty delivery failure.

The positive replacement values are accounted for in the ba-lance sheet on the asset side, and the negative replacement values on the liability side, for all the derivative financial ins-truments outstanding at balance sheet date which would re-sult from own account or customer transactions, irrespective of the accounting treatment in the income statement.

Financial investmentsFinancial investments, acquired with the intent to be held un-til maturity, are carried in the balance sheet under “financial investments”. The difference between the nominal value and the acquisition cost is spread over the period remaining to maturity (accrual method) and booked to the “interest and dividend income on financial investments”.

Tangible Fixed AssetsFixed assets are stated in the balance sheet at their cost price and depreciated using the straight-line method over a period corresponding to the useful economic life of the different types of assets. The depreciation rates used are as follows::

• Bank building : maximum 50 years• Building improvement costs : maximum 10 years• Furniture and fixtures : maximum 5 years• Vehicles : maximum 5 years• Software : maximum 5 years• IT hardware : maximum 3 years

28 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS

Intangible assetsAny goodwill or acquisition difference resulting from the pur-chase of activities or firms is reported in the balance sheet under intangible assets. ABS Group depreciates any goodwill over its estimated useful life using the straight line method.

Valuation Adjustments and ProvisionsValuation adjustments and specific provisions are made for all identifiable risks existing at the balance sheet date.

Reserves for general banking risksReserves for general banking risks are reserves constituted out of prudence with the objective to cover unforeseen and non-recurrent banking risks. The underlying tax charge is posted to deferred tax provisions and is determined on the basis of tax rates in force. CHF 80,381,634 are net of tax.

TaxesTaxes are calculated in accordance with relevant tax laws and are either paid or provisioned for.

The caption taxes in the consolidated income statement in-cludes current income taxes of ABS Group companies as well as deferred taxes. Deferred taxes are recorded in accordance with requirements. The tax effects arising from temporary differences between the carrying value and tax value of assets and liabilities are recorded as deferred taxes.

Current taxes are accrued for in the liability side of the balance sheet under accrued expenses, and deferred tax liabilities are reported under provisions. Deferred taxes are calculated based on the expected tax rates.

Policy applicable in respect of derivative financial instrumentsThe derivative financial instruments are mainly used in opera-tions for the account of customers. To avoid any exposure, ABS Group concludes back-to-back transactions on the financial markets.

ABS Group uses financial derivative instruments when dee-med adequate in order to hedge the foreign currency exposure on its revenues, an important proportion of which derives from underlying assets denominated in foreign currencies, particu-larly in USD and EUR.

Premiums paid or received in relation to these operations are recognized in the balance sheet within the lines positive and negative replacement values. They are reported prorata tem-poris in the income statement item which is subject to the hedge transaction until maturity.

The positive or negative replacement values are recognized in the balance sheet. Should a hedge transaction exceed the underlying amount to be covered (inefficiency), the amount resulting from the excess of hedge would be accounted for in the trading results. Definition Client Assets & Net Increase / (Decrease) of Client AssetsClient assets are asset values of clients, for which ABS Group renders investment and advisory services. Custody portfolios and asset values, which are held exclusively for transaction and custodian purposes, are not included in the client assets. The same applies for loans and purely commercial clients. The net increase / (decrease) of client assets consists of the sum of all individual money deposits and payments as well as security incoming and outgoing deliveries, whereby new loans and loan repayments are accounted for. Interest and dividends credited to clients as well as debit interest, commissions and charges debited for bank services, are excluded from the calculation of the net increase/(decrease) of client assets, as they form part of the client performance – the same is valid for variations in client assets due to market currency and security prices.

28 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS

Pension PlanABS Group only operates pension plan for its employees in Switzerland.

Arab Bank (Switzerland) Ltd. maintains legally separated welfare schemes for its 104 active insured parties at the date of the balance sheet (2017 : 108) and 50 retired (2017 : 48). The pension plan is based on the Swiss defined contribution system (defined contribution plans in accordance with “Swiss GAAP FER 26”). The Bank carries approximately two thirds of the pension cost. The cost carried by the bank is shown under the information on the balance sheet (note “Information on payables to own employee pension fund”).The pension fund liabilities as well as the plan assets are le-gally separated from the Bank in fully funded independent foundations. Organization, management and financing of the pension plan are subject to Swiss Federal regulations and to the constitution of the foundations (trust deed) as well as the currently valid regulations of the pension plan.

Subsequent eventsThe participation Turkland Bank A.S. has been sold at the be-ginning of 2019. No further gain or loss raised from this tran-saction. This transaction is subject to the Turkish authorities’ approval.

30 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS

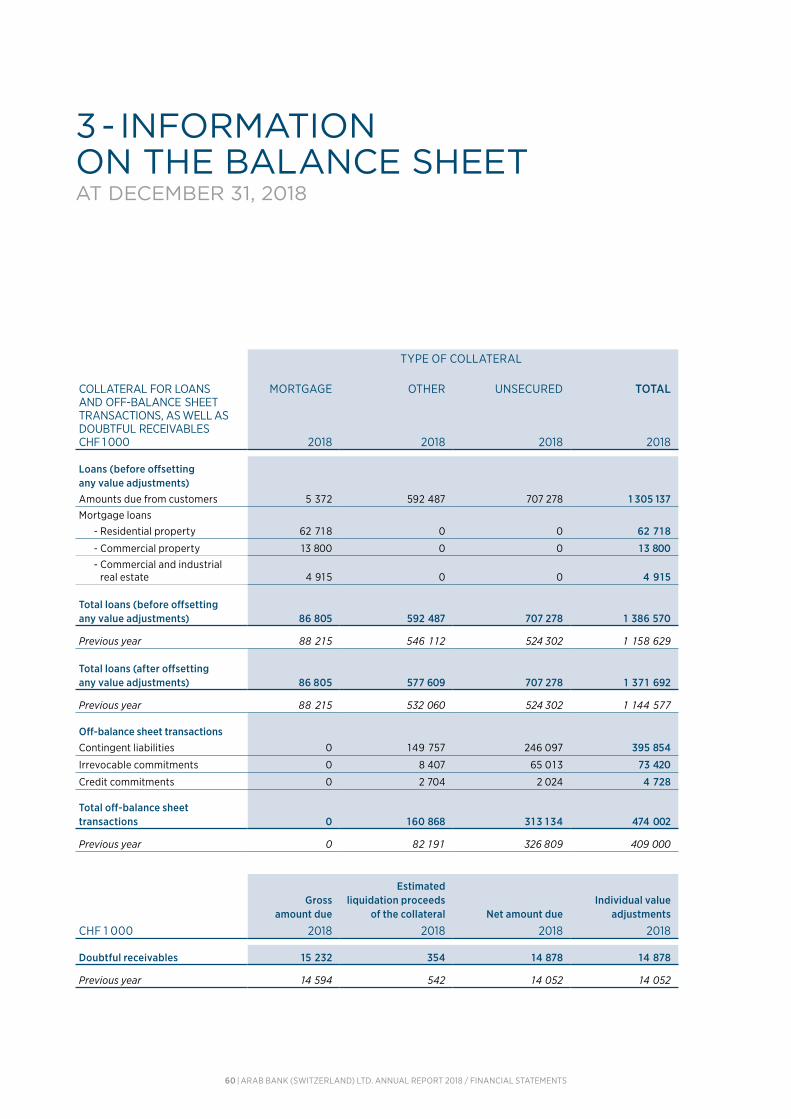

3 - INFORMATION ON THECONSOLIDATED BALANCE SHEETAT DECEMBER 31, 2018

TYPE OF COLLATERALCOLLATERAL FOR LOANSAND OFF-BALANCE SHEETTRANSACTIONS, AS WELL ASDOUBTFUL RECEIVABLESCHF 1 000

MORTGAGE

2018

OTHER

2018

UNSECURED

2018

TOTAL

2018

Loans (before offsetting any value adjustments)

Amounts due from customers 5 372 593 158 707 278 1 305 808Mortgage loans

- Residential property 62 7 1 8 0 0 62 7 1 8

- Commercial property 13 800 0 0 13 800 - Commercial and industrial real estate 4 9 15 0 0 4 915

Total loans (before offsetting any value adjustments) 86 805 593 158 707 278 1 387 241

Previous year 88 215 546 852 524 302 1 159 369

Total loans (after offsetting any value adjustments) 86 805 578 274 707 278 1 372 357

Previous year 88 215 532 794 524 302 1 145 3 1 1

Off-balance sheet transactionsContingent liabilities 0 149 757 246 098 395 855Irrevocable commitments 0 8 407 65 0 13 73 420Credit commitments 0 2 704 2 024 4 728

Total off-balance sheet transactions 0 160 868 313 135 474 003

Previous year 0 82 1 9 1 326 810 409 001

Gross amount due

Estimated liquidation proceeds

of the collateral Net amount dueIndividual value

adjustments

CHF 1 000 2018 2018 2018 2018

Doubtful receivables 15 232 348 14 884 14 884

Previous year 14 484 426 14 058 14 058

30 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS 31 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS

TRADING PORTFOLIOCHF 1 000 2018 2017

Assets - Trading portfolio

Debt instruments, money-market instruments, money-market transactions 0 0

- of which listed 0 0

Equity securities 22 364 27 720

Total assets - Trading portfolio 22 364 27 720

- of which securities allowed for repos as per liquidity provisions 0 0

- of which determined using a valuation model 0 0

32 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS

TRADING INSTRUMENTS

DERIVATIVE FINANCIAL INSTRUMENTS (ASSETS AND LIABILITIES) PO

SITI

VE

REP

LACE

MEN

T VA

LUE

NEG

ATIV

E R

EPLA

CEM

ENT

VALU

E

CON

TRA

CT

VOLU

ME

CHF 1 000 2018 2018 2018

Interest rate instruments

- Swaps 0 0 0

Foreign exchange / precious metal

- Forward contracts 13 276 15 548 2 002 259

- Options (OTC) 1 890 1 880 180 269

Participations / indices

- Options (exchange-traded) 4 992 4 993 659 354

Total before netting agreements 20 1 58 22 421 2 841 882

Previous year 9 748 15 394 2 1 85 487

CHF 1 000

Positive replacement

value(cumulative)

2018

Negative replacement

value (cumulative)

2018

Total after netting agreements 20 158 22 553

Previous year 9 748 15 541

HEDGING INSTRUMENTS

POSI

TIV

E R

EPLA

CEM

ENT

VALU

E

NEG

ATIV

E R

EPLA

CEM

ENT

VALU

E

CON

TRA

CT

VOLU

ME

2018 2018 2018

0 132 3 764

0 0 0

0 0 0

0 0 0

0 132 3 764

0 147 3 955

BREAKDOWN ACCORDING TO COUNTERPARTIES CE

NTR

AL

CLEA

RIN

G P

ART

IES

BAN

KS A

ND

SE

CURI

TIES

DEA

LERS

OTH

ER C

LIEN

TS

TOTA

L

CHF 1 000 2018 2018 2018 2018

Positive replacement values (after netting agreements) 0 10 550 9 608 20 158

32 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS 33 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS

BOOK VALUE FAIR VALUEFINANCIAL INVESTMENTSCHF 1 000 2018 2017 2018 2017

Debt instruments 428 168 408 246 426 898 410 099

- of which held until maturity 428 168 408 246 426 898 410 099

Participations 35 35 40 37

Total 428 203 408 281 426 938 410 136

- of which securities allowed for repos as per liquidity provisions 264 1 53 1 10 291 262 246 1 1 1 204

2018

BREAKDOWN OF THE COUNTERPARTY ACCORDING TO RATING CHF 1 000

AAA TO AA-

A+ TO A-

BBB+ TOBBB-

BB+ TO B-

LOWER THAN

B- UNRATED TOTAL

Debt instruments : book value 172 374 90 769 20 321 1 325 0 143 379 428 168

The above mentioned ratings have been issued by Standard & Poor’s.

34 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS

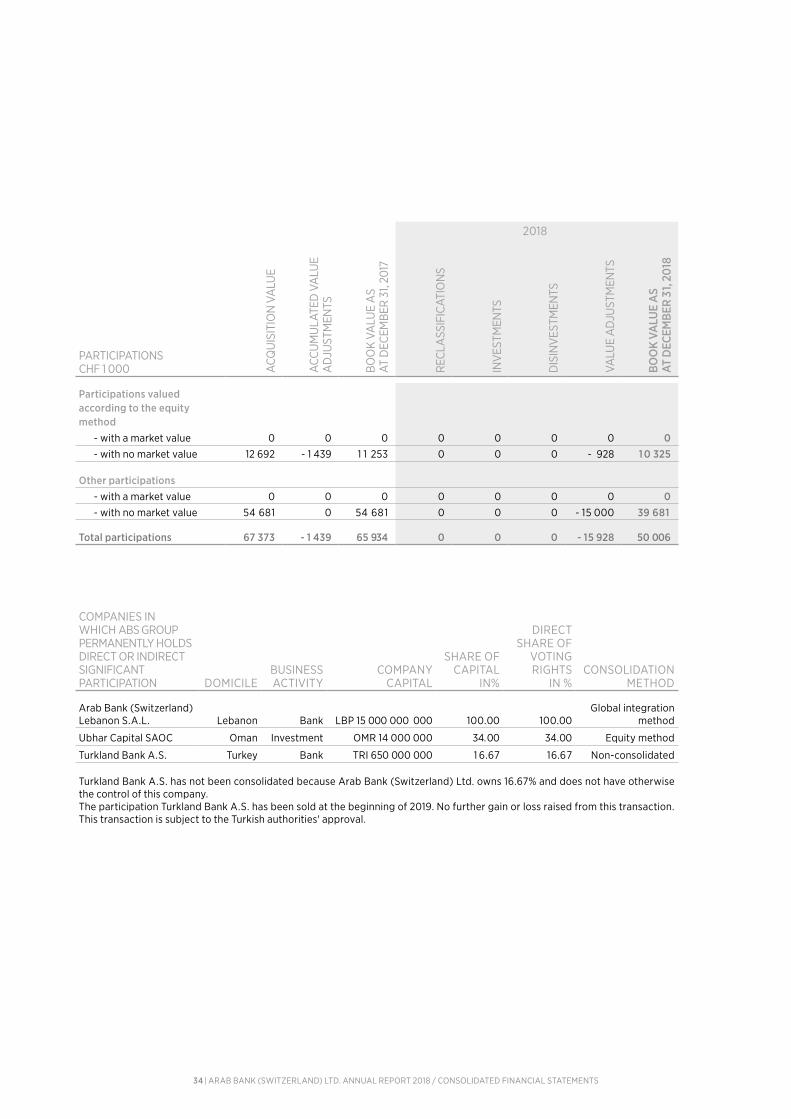

2018

PARTICIPATIONSCHF 1 000 A

CQU

ISIT

ION

VA

LUE

ACC

UM

ULA

TED

VA

LUE

AD

JUST

MEN

TS

BOO

K VA

LUE

AS

AT D

ECEM

BER

31,

2017

REC

LASS

IFIC

ATIO

NS

INV

ESTM

ENTS

DIS

INV

ESTM

ENTS

VALU

E A

DJU

STM

ENTS

BOO

K VA

LUE

AS

AT D

ECEM

BER

31, 2

018

Participations valued according to the equity method - with a market value 0 0 0 0 0 0 0 0 - with no market value 12 692 - 1 439 1 1 253 0 0 0 - 928 1 0 325

Other participations - with a market value 0 0 0 0 0 0 0 0 - with no market value 54 681 0 54 681 0 0 0 - 15 000 39 681

Total participations 67 373 - 1 439 65 934 0 0 0 - 15 928 50 006

COMPANIES IN WHICH ABS GROUP PERMANENTLY HOLDS DIRECT OR INDIRECT SIGNIFICANT PARTICIPATION DOMICILE

BUSINESS ACTIVITY

COMPANY CAPITAL

SHARE OF CAPITAL

IN%

DIRECT SHARE OF

VOTING RIGHTS

IN %CONSOLIDATION

METHOD

Arab Bank (Switzerland) Lebanon S.A.L. Lebanon Bank LBP 15 000 000 000 100.00 100.00

Global integration method

Ubhar Capital SAOC Oman Investment OMR 14 000 000 34.00 34.00 Equity method

Turkland Bank A.S. Turkey Bank TRI 650 000 000 1 6.67 16.67 Non-consolidated

Turkland Bank A.S. has not been consolidated because Arab Bank (Switzerland) Ltd. owns 16.67% and does not have otherwise the control of this company.The participation Turkland Bank A.S. has been sold at the beginning of 2019. No further gain or loss raised from this transaction. This transaction is subject to the Turkish authorities' approval.

34 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS 35 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS

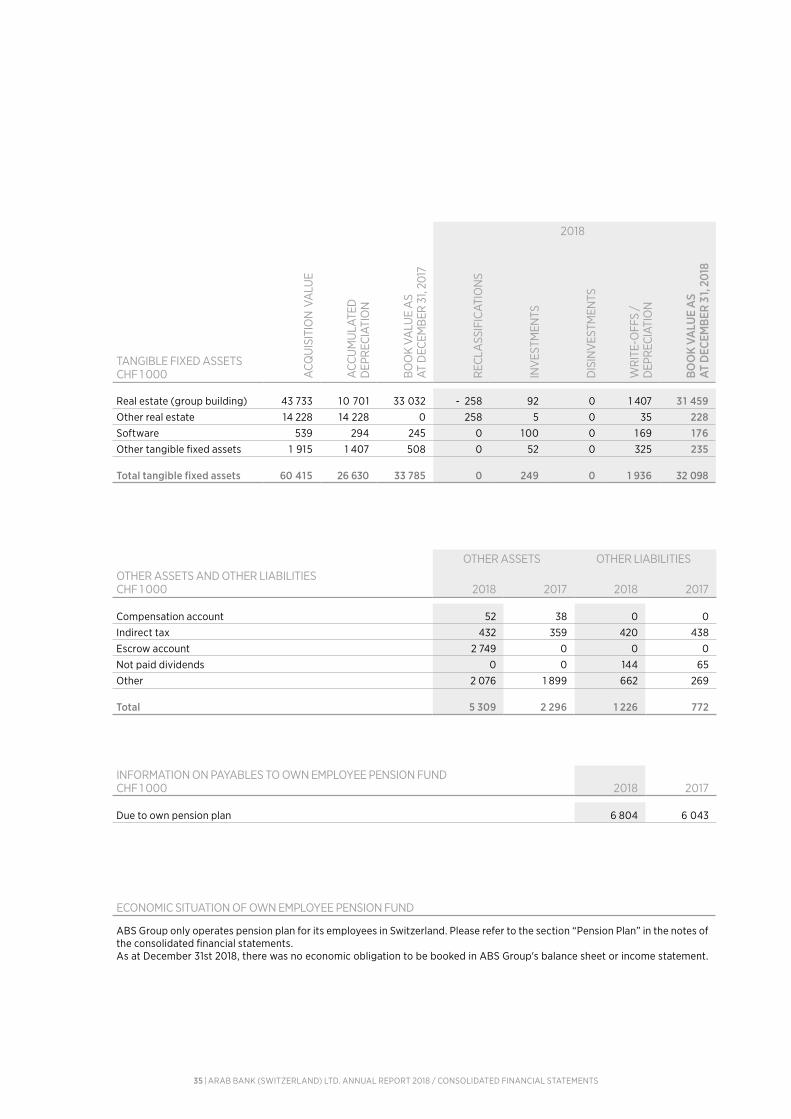

2018

TANGIBLE FIXED ASSETSCHF 1 000 A

CQU

ISIT

ION

VA

LUE

ACC

UM

ULA

TED

D

EPR

ECIA

TIO

N

BOO

K VA

LUE

AS

AT D

ECEM

BER

31,

2017

REC

LASS

IFIC

ATIO

NS

INV

ESTM

ENTS

DIS

INV

ESTM

ENTS

WRI

TE-O

FFS

/ D

EPR

ECIA

TIO

N

BOO

K VA

LUE

AS

AT D

ECEM

BER

31, 2

018

Real estate (group building) 43 733 10 701 33 032 - 258 92 0 1 407 31 459Other real estate 14 228 14 228 0 258 5 0 35 228Software 539 294 245 0 100 0 1 69 176Other tangible fixed assets 1 915 1 407 508 0 52 0 325 235

Total tangible fixed assets 60 415 26 630 33 785 0 249 0 1 936 32 098

OTHER ASSETS OTHER LIABILITIESOTHER ASSETS AND OTHER LIABILITIESCHF 1 000 2018 2017 2018 2017

Compensation account 52 38 0 0

Indirect tax 432 359 420 438

Escrow account 2 749 0 0 0

Not paid dividends 0 0 144 65

Other 2 076 1 899 662 269

Total 5 309 2 296 1 226 772

INFORMATION ON PAYABLES TO OWN EMPLOYEE PENSION FUNDCHF 1 000 2018 2017

Due to own pension plan 6 804 6 043

ECONOMIC SITUATION OF OWN EMPLOYEE PENSION FUND

ABS Group only operates pension plan for its employees in Switzerland. Please refer to the section “Pension Plan” in the notes of the consolidated financial statements. As at December 31st 2018, there was no economic obligation to be booked in ABS Group's balance sheet or income statement.

36 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS

2018

VALUE ADJUSTMENTS AND PROVISIONS AS WELL AS RESERVES FOR GENERAL BANKING RISKSCHF 1 000 BA

LAN

CE A

S AT

DEC

EMB

ER 3

1, 20

17

USE

IN C

ON

FOR

MIT

Y

WIT

H D

ESIG

NAT

ED

PUR

POSE

REC

LASS

IFIC

ATIO

NS

FOR

EIG

N E

XCH

AN

GE

DIF

FER

ENCE

S

OV

ERD

UE

INTE

RES

T,R

ECO

VER

IES

NEW

AD

JUST

MEN

TS

DEB

ITED

TO

INCO

ME

REL

EASE

S CR

EDIT

ED

TO IN

COM

E

BALA

NCE

AS

AT D

ECEM

BER

31, 2

018

Provisions for deferred taxes 1 869 0 0 0 0 4 463 0 6 332

Provisions for other business risks 10 0 0 0 0 0 0 10

Other provisions 29 454 0 0 8 0 4 1 -29 091* 41 2

Total provisions 31 333 0 0 8 0 4 504 -29 091 6 754

Reserves for general banking risks 84 446 0 0 0 0 14 1 67 0 98 61 3

Value adjustments for default risks and country risks 14 058 0 0 1 19 - 176 883 0 14 884

- of which value adjustments for default risks due to doubtful receivables 14 058 0 0 1 19 - 176 883 0 14 884

The amount of CHF 80'381'634 of reserves for general banking risks are free of taxes.* The releases credited to income of CHF 29.1 million mainly comprised the release of CHF 15.0 million in relation with a permanent participation accounted for under “Extraordinary income”, and the release of a prior year general provision to cover latent credit risk, which is not eligible to be considered as economically justified anymore. An allocation to the reserve for general banking risks has been created during the year.

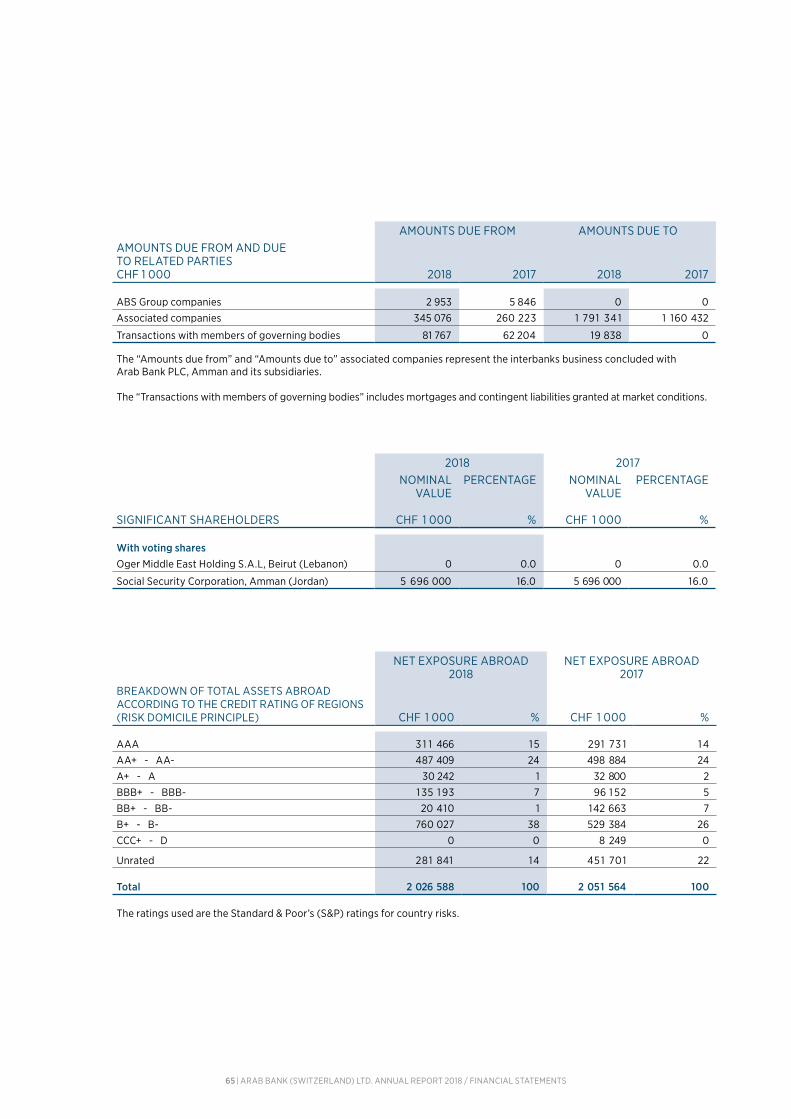

AMOUNTS DUE FROM AMOUNTS DUE TO

AMOUNTS DUE FROM AND DUE TO RELATED PARTIESCHF 1 000 2018 2017 2018 2017

Associated companies 353 279 268 712 1 791 341 1 160 432

Transactions with members of governing bodies 8 1 767 62 204 19 838 0

The "Amounts due from" and "Amounts due to" associated companies represent the interbanks business concluded with Arab Bank PLC., Amman and its subsidiaries.The "Transactions with members of governing bodies" includes mortgages and contingent liabilities granted at market conditions.

36 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS 37 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS

2018

MATURITY STRUCTURE OF FINANCIAL INSTRUMENTSCHF 1 000 AT

SIG

HT

RED

EEM

AB

LE B

YN

OTI

CE

DU

E W

ITH

IN3

MO

NTH

S

DU

E W

ITH

IN

3 TO

12 M

ON

THS

DU

E W

ITH

IN

1 TO

5 Y

EARS

DU

E A

FTER

5 YE

ARS

TOTA

L

Asset / financial instrumentsLiquid assets 1 045 383 0 0 0 0 0 1 045 383Amounts due from banks 325 484 0 353 910 148 388 0 0 827 782Amounts due from customers 0 589 050 604 822 93 399 3 142 5 1 1 1 290 924Mortgages loans 0 46 595 1 223 0 7 569 26 046 81 433Trading portfolio 22 364 0 0 0 0 0 22 364Positive replacement values of derivatives 0 0 1 2 91 3 7 1 84 6 1 0 20 158Financial investments 0 0 16 858 42 980 1 27 1 1 9 241 246 428 203

Total reporting year 1 393 231 635 645 989 726 291 951 137 891 267 803 3 716 247

Previous year 1 227 596 437 628 972 355 292 878 164 446 208 307 3 303 210

Liabilities / financial instruments

Amounts due to banks 31 6 430 1 363 1 94 459 952 0 0 0 2 139 576Amounts due to customers 1 01 3 3 1 1 27 797 29 21 6 1 983 0 0 1 072 307

Negative replacement values of derivatives 0 0 15 278 7 082 193 0 22 553

Total reporting year 1 329 741 1 390 991 504 446 9 065 193 0 3 234 436

Previous year 1 454 1 1 5 100 237 1 201 078 79 660 147 0 2 835 237

38 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS

2018 2017ASSETS AND LIABILITIES BY DOMESTIC AND FOREIGN ORIGINCHF 1 000 DOMESTIC FOREIGN DOMESTIC FOREIGN

AssetsLiquid assets 1 043 765 1 61 8 804 668 1 1 64

Amounts due from banks 228 453 599 329 204 622 701 696

Amounts due from customers 342 626 948 298 23 1 457 827 273

Mortgages loans 49 1 5 1 32 282 37 203 49 378

Trading portfolio 4 1 5 1 18 2 1 3 4 270 23 450

Positive replacement values of derivatives 5 759 14 399 3 575 6 1 73

Financial investments 76 343 351 861 39 883 368 398

Accrued income and prepaid expenses 48 067 5 742 43 324 5 063

Participations 0 50 006 0 65 934

Tangible fixed assets 31 773 325 33 380 405

Other assets 3 351 1 958 369 1 927

Total assets 1 833 439 2 024 031 1 402 751 2 050 861

Liabilities Amounts due to banks 90 102 2 049 474 74 139 1 585 639

Amounts due to customers 76 208 996 099 85 920 1 073 998

Negative replacement values of derivatives 10 955 1 1 598 9 996 5 545

Accrued expenses and deferred income 53 224 1 810 45 648 4 786

Other liabilities 1 123 103 685 88

Provisions 6 642 1 1 2 3 1 264 69

Reserves for general banking risks 98 6 13 0 84 446 0

Share capital 26 700 0 26 700 0

Reserves from capital contribution 0 0 7 3 10 0

Retained earnings 416 772 0 402 633 0

Reserves for currency translation 8 1 5 0 607 0

Consolidated profit for the period 17 120 0 14 1 39 0

Total liabilities 798 274 3 059 196 783 487 2 670 1 25

38 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS 39 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS

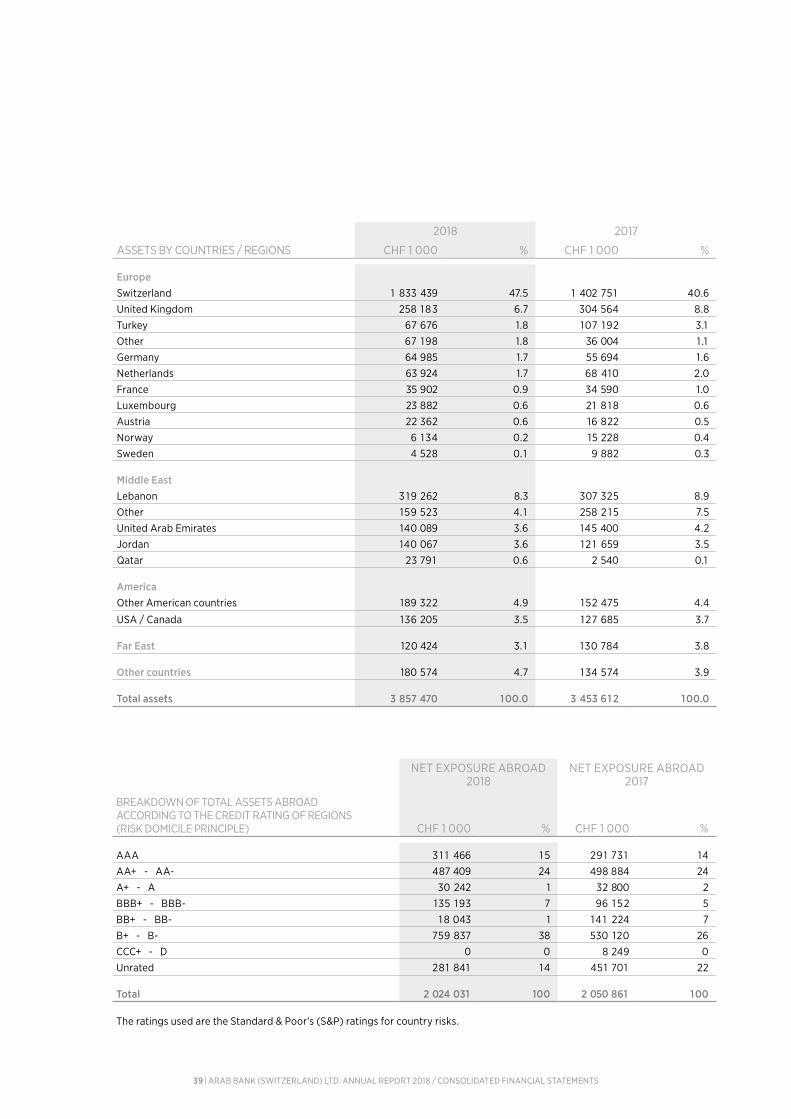

2018 2017

ASSETS BY COUNTRIES / REGIONS CHF 1 000 % CHF 1 000 %

EuropeSwitzerland 1 833 439 47.5 1 402 751 40.6

United Kingdom 258 1 83 6.7 304 564 8.8

Turkey 67 676 1.8 107 1 92 3.1

Other 67 1 98 1.8 36 004 1 .1

Germany 64 985 1.7 55 694 1.6

Netherlands 63 924 1.7 68 410 2.0

France 35 902 0.9 34 590 1.0

Luxembourg 23 882 0.6 21 8 1 8 0.6

Austria 22 362 0.6 16 822 0.5

Norway 6 1 34 0.2 15 228 0.4

Sweden 4 528 0.1 9 882 0.3

Middle EastLebanon 3 1 9 262 8.3 307 325 8.9

Other 159 523 4. 1 258 2 1 5 7.5

United Arab Emirates 140 089 3.6 145 400 4.2

Jordan 140 067 3.6 1 2 1 659 3.5

Qatar 23 791 0.6 2 540 0.1

AmericaOther American countries 189 322 4.9 1 52 475 4.4

USA / Canada 136 205 3.5 1 27 685 3.7

Far East 120 424 3.1 130 784 3.8

Other countries 180 574 4.7 1 34 574 3.9

Total assets 3 857 470 100.0 3 453 61 2 100.0

NET EXPOSURE ABROAD2018

NET EXPOSURE ABROAD2017

BREAKDOWN OF TOTAL ASSETS ABROADACCORDING TO THE CREDIT RATING OF REGIONS(RISK DOMICILE PRINCIPLE) CHF 1 000 % CHF 1 000 %

AAA 3 1 1 466 1 5 291 73 1 14

AA+ - AA- 487 409 24 498 884 24

A+ - A 30 242 1 32 800 2

BBB+ - BBB- 135 193 7 96 1 52 5

BB+ - BB- 1 8 043 1 14 1 224 7

B+ - B- 759 837 38 530 120 26

CCC+ - D 0 0 8 249 0

Unrated 281 841 14 451 701 22

Total 2 024 031 100 2 050 861 100

The ratings used are the Standard & Poor’s (S&P) ratings for country risks.

40 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2017 / CONSOLIDATED FINANCIAL STATEMENTS

2018ASSETS AND LIABILITIES BY CURRENCIESCHF 1 000 CHF USD EUR OTHER

AssetsLiquid assets 1 043 375 7 1 7 1 250 4 1

Amounts due from banks 246 726 334 229 1 74 953 7 1 874

Amounts due from customers 1 53 97 1 1 081 054 47 351 8 548

Mortgages loans 49 558 0 0 3 1 875

Trading portfolio 0 1 5 293 6 578 493

Positive replacement values of derivatives 13 555 5 648 1 97 759

Financial investments 199 735 221 145 3 348 3 975

Accrued income and prepaid expenses 48 462 5 081 57 209

Participations 50 006 0 0 0

Tangible fixed assets 3 1 773 0 0 325

Other assets 824 2 834 1 46 1 505

Total on-balance sheet assets 1 837 985 1 666 001 233 880 1 1 9 604

Delivery claims from spot exchange deals, forward exchange deals and currency options transactions 225 734 1 754 237 1 60 094 698 7 1 7

Total assets 2 063 719 3 420 238 393 974 8 1 8 321

LiabilitiesAmounts due to banks 246 096 1 776 566 41 809 75 105

Amounts due to customers 65 220 646 097 21 8 932 142 058

Negative replacement values of derivatives 15 827 5 639 1 96 891

Accrued expenses and deferred income 52 865 1 331 - 8 846

Other liabilities 1 104 34 1 5 73

Provisions 6 597 45 0 1 1 2

Reserves for general banking risks 98 6 13 0 0 0

Share capital 26 700 0 0 0

Reserves from capital contribution 0 0 0 0

Retained earnings 416 772 0 0 0

Reserves for currency translation 0 0 0 8 1 5

Consolidated profit for the period 17 120 0 0 0

Total on-balance sheet liabilities 946 914 2 429 71 2 260 944 21 9 900

Delivery claims from spot exchange deals, forward exchange deals and currency options transactions 1 1 33 1 97 97 1 952 143 753 589 880

Total liabilities 2 080 1 1 1 3 401 664 404 697 809 780

Net positions - 1 6 392 18 574 - 10 723 8 541

41 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS

42 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS

4 - INFORMATION ON CONSOLIDATED OFF-BALANCE SHEET TRANSACTIONS

CONTINGENT LIABILITIESCHF 1 000 2018 2017

Credit guarantees and similar 41 440 43 666

Performance-related guarantees and similar 36 908 53 1 24

Irrevocable commitments due to documentary credits 3 17 507 209 687

Total contingent liabilities 395 855 306 477

FIDUCIARY TRANSACTIONSCHF 1 000 2018 2017

Fiduciary placements with third party companies 998 972 7 1 6 695

Fiduciary placements with Arab Bank PLC Amman and its subsidiaries as well as affiliated companies 186 8 1 7 234 678

Total fiduciary transactions 1 185 789 951 373

ASSETS UNDER MANAGEMENTCHF 1 000 2018 2017

Type of assets under managementAssets in collective investment schemes managed by ABS Group 136 554 86 372

Assets with administrations’ mandate 168 914 188 530

Other client assets 3 5 1 9 959 3 1 77 562

Total assets under management (including double-counting) 1) 3 825 427 3 452 464

- of which double counts 136 554 86 372

Total assets under management (excluding double-counting) 1) 3 688 873 3 366 092

Development of assets under managementTotal assets under management (including double-counting) at the beginning 3 452 464 3 769 779

+ / - Net new money inflows or outflows 2) 250 446 - 67 573

+ / - Market price trend, dividends and currency development 1 22 5 1 7 - 249 742

Total assets under management (including double-counting) at the end 3 825 427 3 452 464

1) Client Assets are asset values of clients, for which ABS Group renders investment and consulting services, but without loans.2) Sum of all individual money deposits and payments as well as security incoming and outgoing deliveries, whereby new loans and loan repayments are accounted for.

CREDIT COMMITMENTSCHF 1 000 2018 2017

Commitments arising from deferred payments 4 728 21 71 6

Total credit commitments 4 728 21 716

42 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS 43 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS

5 - INFORMATION ON THE CONSOLIDATED INCOME STATEMENT

RESULTS FROM TRADING OPERATIONSCHF 1 000 2018 2017

Equities shares (including funds) -483 766

Foreign exchange 33 713 17 738

Total trading results 33 230 18 504

INFORMATION ON SIGNIFICANT NEGATIVE INTERESTS

In 2015, the Swiss National Bank (SNB) introduced negative interest rates of -0.75% on sight deposit account balances with SNB. The paid and accrued SNB negative interests for the year of 2018 amounted to CHF 7.3 million (2017: CHF 6.5 million).

PERSONNEL EXPENSESCHF 1 000 2018 2017

Salaries 25 883 26 745

Social insurance obligations 1 822 1 7 51

Pension fund 3 202 3 180

Other personnel expenses 703 439

Total personnel expenses 31 610 32 1 15

GENERAL AND ADMINISTRATIVE EXPENSESCHF 1 000 2018 2017

Office space expenses 1 086 946

Expenses for information technology and telecommunications 3 059 2 936

Outsourcing expenses 3 546 5 672

Expenses for motor vehicles, machinery, furniture and other equipment and operating lease expenses 300 422

Audit fees 542 5 1 1

- of which for financial and regulatory audits 492 465

- of which for other services 49 46

Other operating expenses 7 172 6 749

Total general and administrative expenses 15 705 17 236

44 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS

OPERATING RESULTS, BROKEN DOWN ACCORDING TO DOMESTIC AND FOREIGN ORIGIN, ACCORDING TO THE PRINCIPLE OF PERMANENT ESTABLISHMENT CHF 1 000

2018 2017

DOMESTIC FOREIGN TOTAL DOMESTIC FOREIGN TOTAL

Net results from interest operations 1 6 158 1 2 1 1 17 369 1 9 770 1 332 2 1 102 Results from commissions from business and services 28 592 740 29 332 27 334 5 1 1 27 845 Net income from trading 33 043 1 87 33 230 18 4 1 1 92 18 503 Other results from ordinary activities 560 - 897 - 337 570 - 1 438 - 868 Operating expenses - 45 100 - 2 21 5 - 47 315 - 47 7 14 - 1 637 - 49 35 1 Value adjustments on participations as well as depreciation on tangible fixed assets - 16 815 - 1 22 - 1 6 937 - 1 908 - 1 1 4 - 2 022

Changes in provisions and other value adjustments as well as losses 12 953 - 4 1 1 2 91 2 1 1 1 83 - 35 1 1 148

Operating result 29 391 - 1 137 28 254 27 646 - 1 289 26 357

CURRENT AND DEFERRED TAXESCHF 1 000 2018 2017

Current taxes 8 314 6 794

Total current taxes 8 314 6 794

The average tax rate was 32.7% of the results for the period before taxes in the current year (previous year : 32.5%).

Deferred taxes 4 463 1 869

Total deferred taxes 4 463 1 869

Deferred tax were calculated using actual expected tax rates.

MATERIAL LOSSES, EXTRAORDINARY INCOME AND EXPENSES AS WELL AS RELEASE OF SIGNIFICANT HIDDEN RESERVES, RESERVES FOR GENERAL BANKING RISKS AND VALUE ADJUSTMENTS AND PROVISIONS NO LONGER NECESSARYCHF 1 000 2018 2017

Extraordinary incomeRelease of provisions* 1 5 545 0

Other extraordinary income 325 5 1 1

Total extraordinary income 15 870 5 1 1

Extraordinary expensesOther extraordinary expenses 60 1

Total extraordinary expenses 60 1

* Of which release of a provision of CHF 15 million created in 2016 in relation with increased risks relating to a permanent participation, instead of recording a valuation adjustment whose economic necessity was not clear at that time.

44 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS 45 | ARAB BANK (SWITZERLAND) LTD. ANNUAL REPORT 2018 / CONSOLIDATED FINANCIAL STATEMENTS

6 - CONSOLIDATED CAPITAL ADEQUACY AND LIQUIDITY DISCLOSURE

CHF 1 000 2018 2017

Eligible capitalCommon Equity Tier 1 Capital (CET1) 538 282 514 081

Total eligible capital 538 282 514 081

Required capitalCredit risks 122 654 120 036

Non-counterparty-related risks 2 554 2 686

Market risks 14 792 11 469

Operational risks 9 873 9 249

Other capital requirement * 7 936 10 341

Total required capital 157 809 153 781