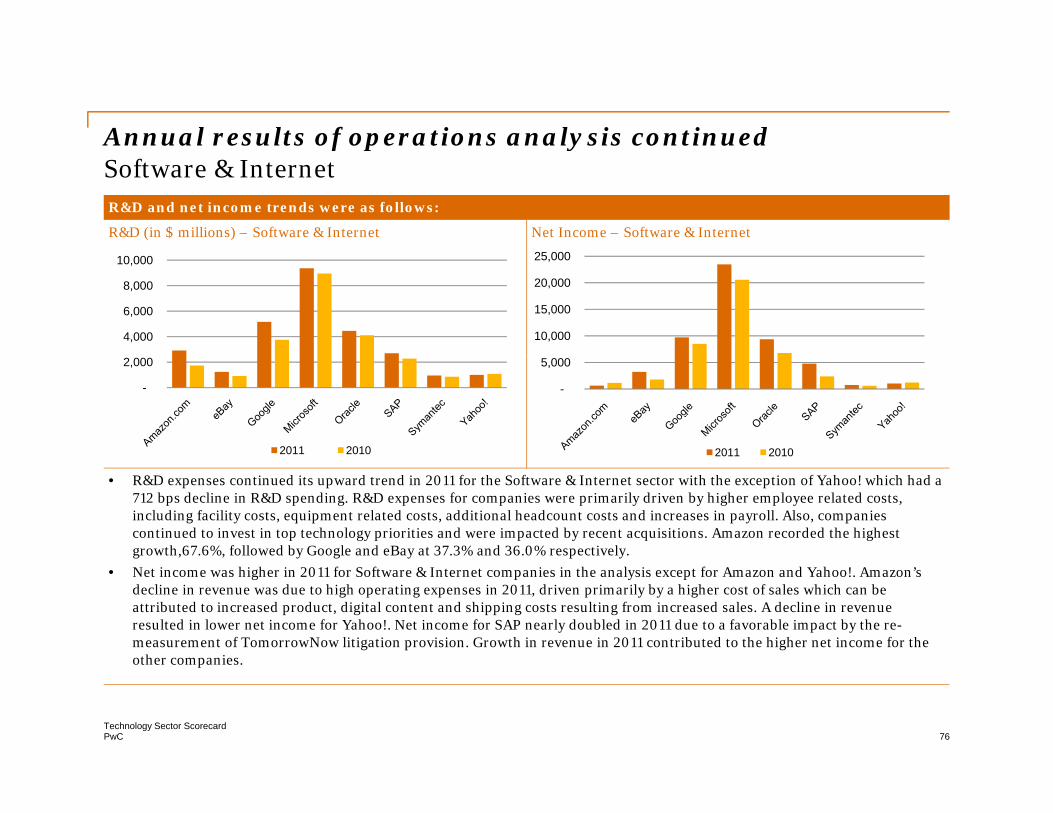

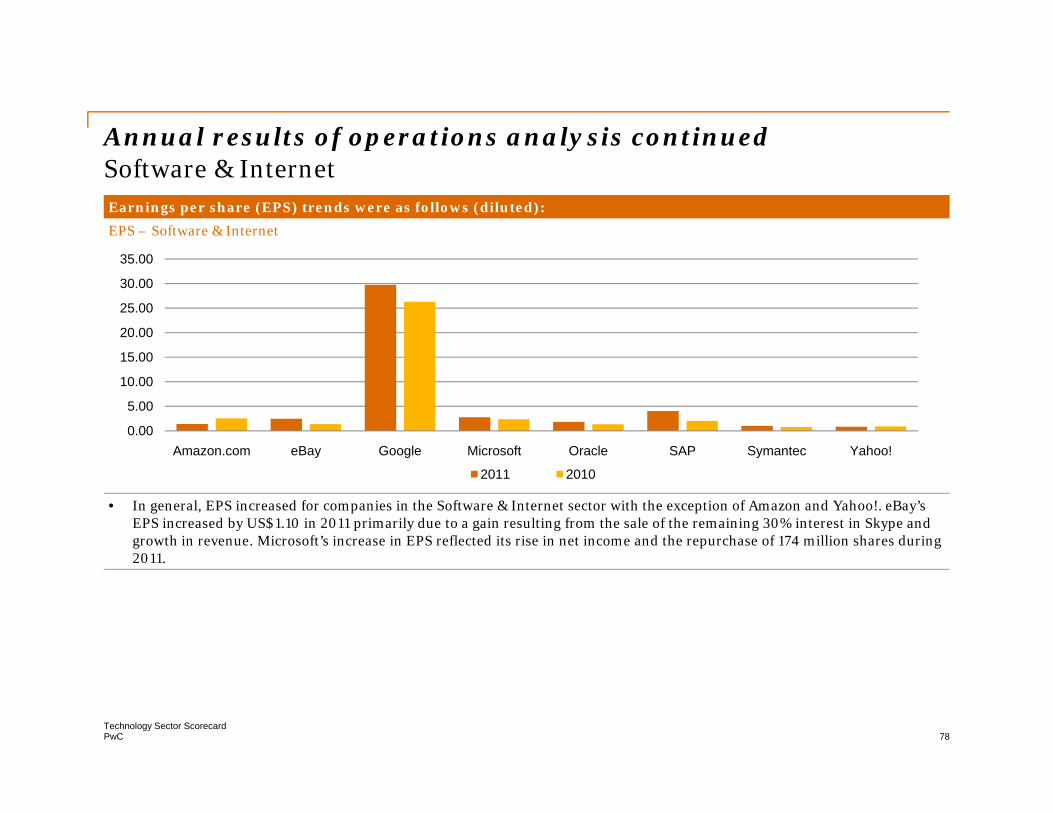

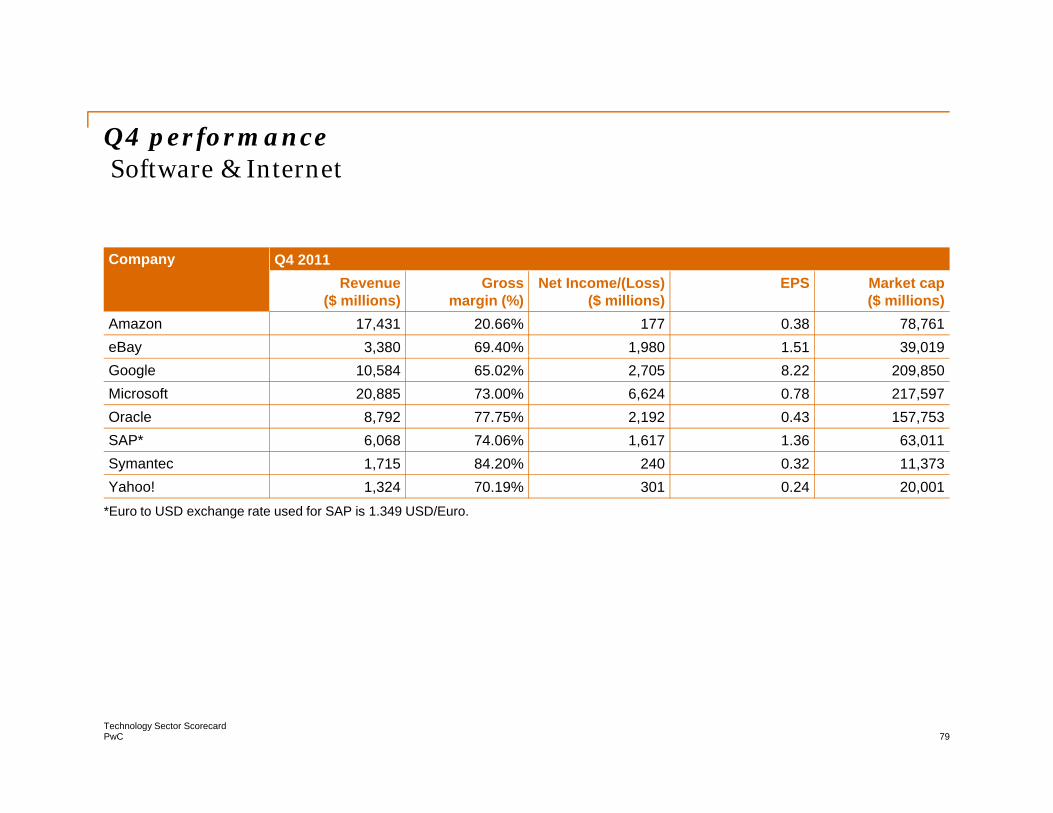

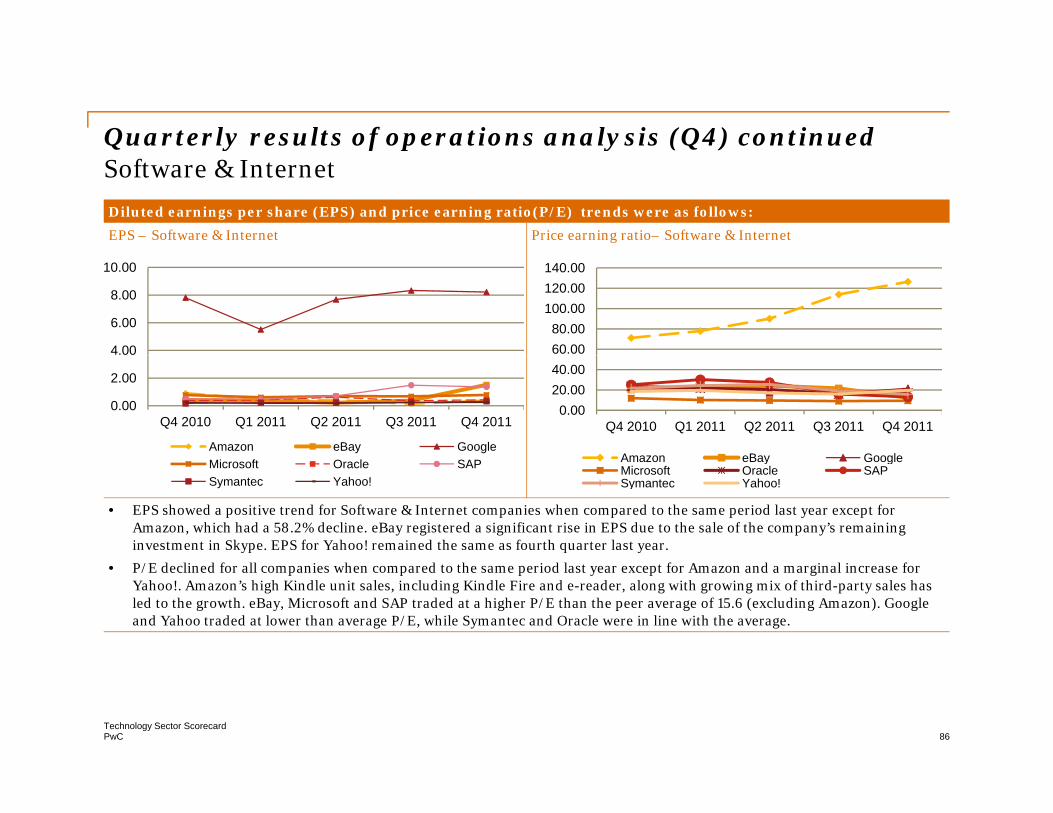

th l technology sector scorecard · •cleantech methodology 87 102 112 pwc ... significantly when...

TRANSCRIPT

T h l

www.pwc.com

Technology Sector ScorecardQ4 d F ll 2011 R iQ4 and Full-year 2011 Review

Introduction

This quarterly global snapshot of activity in the technology sector highlights trends, business h ll d t iti I thi diti i b th Q d th f ll challenges and opportunities. In this edition we review both Q4 and the full-year 2011.

Technology companies weathered a difficult macroeconomic environment and on average posted historically strong profitability in the face of lower top line growth when compared to historical peaks. However, areas of growth in cloud, storage, mobile devices and big data experienced strong growth, in some cases offsetting a difficult environment for desktop PC and semiconductor companiessome cases offsetting a difficult environment for desktop PC and semiconductor companies.

While tech companies have begun 2012 with modest expectations, the second half of 2012 is expected to generate greater excitement with the roll out of several new technology products.

As always, I would like to acknowledge the efforts of Vaibhav Taneja, Stella Su, Dirk Tissera, SameerLadiwala, Steve Mack, Maricel Apuli and Vikram Khosla who contributed greatly in pulling this report together. The observations are the individual views of the authors. Should you have questions or comments, please contact us.

As a reminder, for a richer, interactive experience please visit the online tool: pwc.com/techscorecardd land explore.

Raman Chitkara Global Technology Leader

PwCTechnology Sector Scorecard

2

Contents

Year in review 4

Snapshot by subsector

• Communications

• Consumer Electronics

9

10

25

• EMS/Distributors

• Semiconductors

• Software & Internet

41

54

71

• Systems and PC Hardware

• CleanTech

Methodology

87

102

112

PwC technology territory leaders 113

PwCTechnology Sector Scorecard

3

Year in reviewYear in review

PwCTechnology Sector Scorecard

4

2011 review

Global tech sector posted mixed results Historically high profitability in the face of slower top line growth

• The fourth quarter continued what was a fairly strong year overall despite a host of concerns stemming from the increasingly difficult macroeconomic environment.

• On average, tech companies continued to post historically strong profitability even as top line growth was lower than historical peaks with some notable exceptions: cloud, storage, mobile devices and various software and services categories. These groups experienced strong growth, in some cases offsetting a difficult environment for desktop PC and semiconductor companies.

• On the heels of a slow second half of 2011, calendar 2012 has started with relatively modest expectations.

• The second half of 2012 is expected to generate greater excitement with the roll out of several new technology products.

• Cost focus continues to be a key driver of profitability as business models change. Low cost Cost focus continues to be a key driver of profitability as business models change. Low cost sourcing remains a priority for technology companies. In addition, the natural disasters in Japan and Thailand brought renewed focus to supply chain planning and efficiency as well as risk mitigation.

PwCTechnology Sector Scorecard

5

2011 review continued

• The shift away from traditional IT products to smartphones, tablets and ultrabook PCs is rapidly changing the competitive dynamics in the industry, favoring players with mobile offerings and platforms that connect various devices and applications In the fourth quarter we offerings and platforms that connect various devices and applications. In the fourth quarter we began to see a tiering of the mobile market with clear winners at the top and a second tier niche forming.

• Technology IPOs started the year at a promising note, with 53 IPOs completed during the first half of 2011 However the high volatility of capital markets during the summer significantly half of 2011. However, the high volatility of capital markets during the summer significantly slowed IPO activity. The fourth quarter witnessed a rebound with a 60% jump, but the total number of IPOs completed during the second half of 2011 aggregated to only 33 and fell significantly when compared to 2010 levels.1

• In the scramble for a place at the table in the tech growth markets there has been a host of In the scramble for a place at the table in the tech growth markets, there has been a host of activity in both intellectual property and M&A. Acquisition of IP, market share and innovative technologies has picked up. Coupled with the significant cash reserves on balance sheets, valuations are expected to get higher in 2012.

• Fourth quarter venture investment was strongest in software, social internet and clean tech. Fourth quarter venture investment was strongest in software, social internet and clean tech. Funding jumped 16% for internet companies in 2011 compared to 2010 and 40% of the dollars went to first time financings.2

PwCTechnology Sector Scorecard

6

1. IPOs with issue size greater than US$40 million2. PricewaterhouseCoopers/National Venture Capital Association MoneyTreeTM - Feb2012

2011 review continued

• The volume of venture-backed deals closed in 2011 in the U.S. was similar to 2010 (429 in 2011 versus 436 in 2010) with deal size increasing only slightly ($150 million versus $145 million).1

• Worldwide IT spending in 2012 is now slated to grow 3.7%, almost a full point decrease from earlier projections. But businesses continue to invest in software tools and applications, storage and network infrastructure, and mobile devices suggesting another year of steady IT market growth.2

PwCTechnology Sector Scorecard

7

1. PricewaterhouseCoopers/National Venture Capital Association MoneyTreeTM - Feb20122. Gartner press release - Jan 2012

U.S. Purchasing Manager’s Index (PMI) trends (2004-2011)60

.858

.656

.655

.353

.1 54.3 56

.055

.153

.92.

60 8 2.

90 .4 54

.6 58.2

56.2

54.4 57

.0 61.0

56.4

0 2.4

55

60

65

g g

49.4

49.5

47.3

45.3

5 5 5251

.50

.8 551

.

51.

51. 5 2

40

45

50

55

32.5 36.4

4

30

35

40

04 04 04 05 05 05 05 06 06 06 06 07 07 07 07 08 08 08 08 09 09 09 09 10 10 10 10 11 11 11 11

Recession Threshold (42.7)

2Q0

3Q0

4Q0

1Q0

2Q0

3Q0

4Q0

1Q0

2Q0

3Q0

4Q0

1Q0

2Q0

3Q0

4Q0

1Q0

2Q0

3Q0

4Q0

1Q0

2Q0

3Q0

4Q0

1Q1

2Q1

3Q1

4Q1

1Q 2Q 3Q 4Q

Quarter

The Purchasing Manager’s Index (PMI) recorded a high in Q1 2011 and then dropped to 51 in Q3. The last quarter saw the PMI recovering again. PMI rose further in January 2012 to 54

Source: ISM. IC Insights

Q3. The last quarter saw the PMI recovering again. PMI rose further in January 2012 to 54 but dropped again in February to 52.4.

PwCTechnology Sector Scorecard

8

Snapshot by subsectorSnapshot by subsector

PwCTechnology Sector Scorecard

9

Snapshot by subsectorSnapshot by subsector

Communications

PwCTechnology Sector Scorecard

10

Market analysisyCommunications

• Global sales of mobile devices increased by approximately 24.6 million units to 427.4 million units in Q4 2011 as compared to Q4 2010. The growth rate was lower compared to prior quarters and was i t d b l b l i f d t l 1impacted by global macroeconomic fundamentals.1

• Nokia lost approximately 8.2% market share, dropping to 26.6% in Q4 2011.1 The company incurred a net loss in the current quarter despite an increase in the average selling price (ASP). Volumes in the Devices and Service segment declined by 10.2 million units to 113.5 million units in Q4 2011 as compared to Q4 2010 Current quarter performance was adversely impacted by lower Smart Devices compared to Q4 2010. Current quarter performance was adversely impacted by lower Smart Devices volumes. This quarter was transformational for the company, owing to the introduction of new mobile and smartphones in the market.2 2012 will continue to be a year of transition, and may be impacted by uncertainties related to consumer demand; the timing and ramp-up related to new products, including Lumia devices; and pressure on margins owing to competition.2

• Cisco continued with its cost-cutting initiatives and reported good Q4 2011 results. The company plans to increase its M&A activity. Cisco reported an across-the-board revenue growth and increase in profit in the current quarter.3

• Motorola Solutions continued with its restructuring plans Q4 2011 results were impacted by the • Motorola Solutions continued with its restructuring plans. Q4 2011 results were impacted by the costs of restructuring its business, legal fees and amortization charges.4

1. Business Wire, IDC – Feb 20122. Nokia press release – Jan 2012

PwCTechnology Sector Scorecard

11

3. Crn.com – Feb 20124. Wirelessweek.com – Jan 2012

Market analysis continuedyCommunications

• Motorola Mobility earned revenue of $3.4 billion and recorded a net loss of $ 80 million in Q4 2011. The company experienced a fall in shipment of devices to 10.5 million units in Q4 2011 from 11.3

illi i i Q S h ib d d illi i i Q 1million units in Q4 2010. Smartphones contributed around 5.3 million units in Q4 2011.1

• Google Inc.'s $12.5 billion acquisition of Motorola Mobility Holdings Inc. received antitrust clearance from the U.S. Justice Department and the European Union, but regulators said they will monitor how Google and others use essential patents in the wireless industry. Google is still

iti tit t l f th t i h M t l d b i l Chi 2awaiting antitrust approval from other countries where Motorola does business, namely China.2

PwCTechnology Sector Scorecard

12

1. Techcrunch.com – Jan 20122. Reuters News – Feb 2012

Annual results of operations analysis f p yCommunications

Revenue and gross margin trends were as follows:

Revenues (in $ millions) – Communications Gross margin % – Communications

35,000

45,000

55,000

40.00%50.00%60.00%70.00%

5,000

15,000

25,000

Cisco Systems Inc Motorola Mobility H ldi I

Motorola S l ti I

Nokia Corp2011

0.00%10.00%20.00%30.00%

Cisco Systems Inc Motorola Mobility H ldi I

Motorola Solutions I

Nokia Corp2011

• Nokia’s total revenues declined by 4.5% from $55.9 billion in 2010 to $53.3 billion in 2011. The decline was primarily attributable to the fall in the net sales of Smart Devices and Mobile Phones. Though there was a significant volume growth in2011, the net sales and profitability of Nokia were adversely impacted by the rising competition from other smartphone platforms Nokia recently transitioned from the Symbian to the Windows platform with the launch of Lumia This coupled

Holdings Inc Solutions Inc

2010Holdings Inc Inc

2011

2010

platforms. Nokia recently transitioned from the Symbian to the Windows platform with the launch of Lumia. This, coupled with pricing actions owing to the competitive environment in both the smartphone and mobile phone markets, and Nokia’s absence in the growing dual-SIM phone market, resulted in the downward pressure on sales and profitability.

• Cisco’s revenues increased by 5.9% in 2011 over 2010, though its gross margin declined by 115 bps during the same period.

• Motorola Solutions witnessed a rise in annual revenue of 9.5%, while its gross margin increased by 30 bps in 2011. Motorola Solutions’ revenues increased due to a rise in demand in all regions for both the Enterprise and Government segments

PwCTechnology Sector Scorecard

13

Solutions revenues increased due to a rise in demand in all regions for both the Enterprise and Government segments.

• Motorola Mobility’s revenue was up by 14.0%, to $13.0 billion from $11.4 billion in 2010. Sales benefited from Motorola RAZR’s positive response in the market and strong performance in the Home business segment.

Annual results of operations analysis continuedf p yCommunications

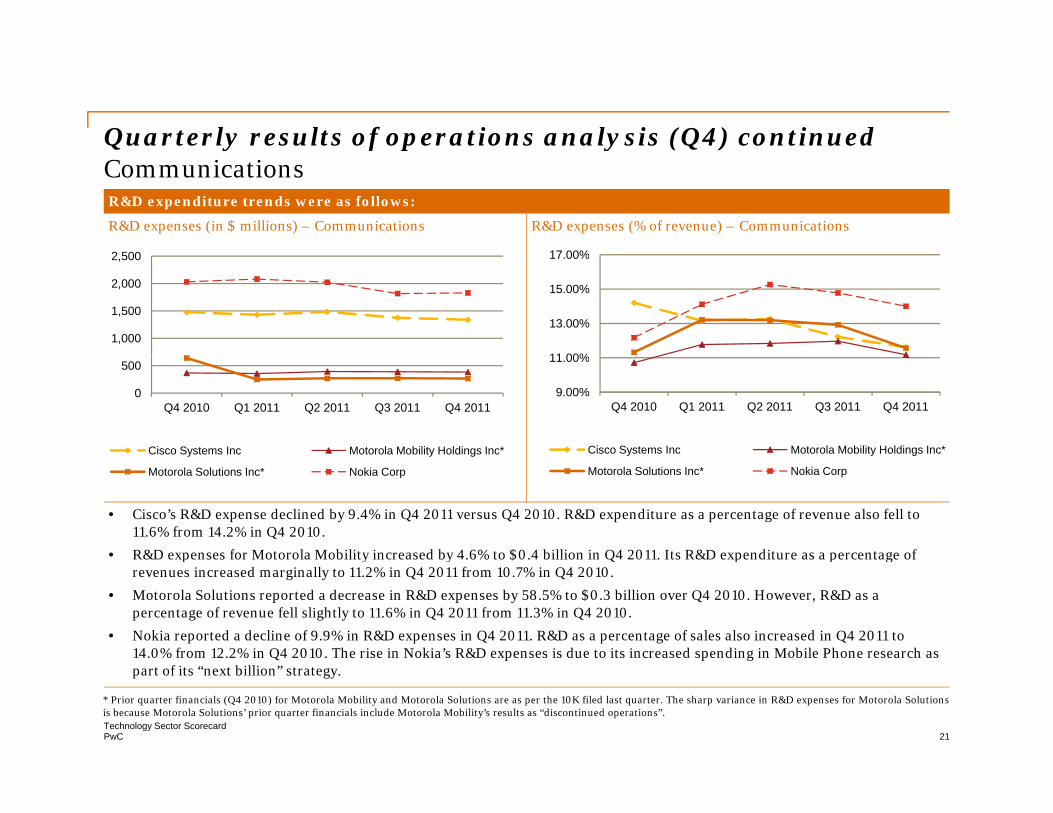

R&D expenditure trends were as follows:

R&D expenses (in $ millions) – Communications R&D expenses (% of revenue) – Communications

4 0005,000 6,000 7,000 8,000

10 00%

15.00%

20.00%

-1,000 2,000 3,000 4,000

Cisco Systems Motorola Mobility Motorola Nokia Corp2011

0.00%

5.00%

10.00%

Cisco Systems I

Motorola Mobility H ldi I

Motorola S l ti I

Nokia Corp2011

• R&D expenditure as a percentage of revenue fell marginally for all companies except Nokia and Motorola Mobility.

• Nokia’s R&D spending increased by 0.6% y-o-y, primarily owing to higher expenditure in mobile phone research and development as a part of Nokia’s “next billion” strategy.

yInc

yHoldings Inc Solutions Inc

p2011

2010

Inc Holdings Inc Solutions Inc2011

2010

• Motorola Mobility’s R&D expenditure also rose by 3.2% in 2011, to $1.5 billion.

• Other companies reduced their R&D expenses primarily as a part of their cost-cutting strategy.

PwCTechnology Sector Scorecard

14

Annual results of operations analysis continued f p yCommunications

Net income trends were as follows:

Net income (in $ millions) – Communications

3 000

4,500

6,000

7,500

(1,500)

-

1,500

3,000

Cisco Systems Inc Motorola Mobility Holdings Inc Motorola Solutions Inc Nokia Corp

• Net income decreased for all the companies analyzed except Motorola Solutions, which grew by 82.9% in 2011 over 2010. The company’s higher annual revenues, coupled with lower interest expenses versus 2010, contributed to the increase in net income.

2011 2010

• Nokia’s net income decreased primarily due to its goodwill impairment of $1.4 billion in 2011.

• Motorola Mobility experienced an increase in operating expenses, especially in its SG&A, R&D expenditures and intangible amortization, which adversely impacted its net income.

PwCTechnology Sector Scorecard

15

Annual results of operations analysis continued f p yCommunications

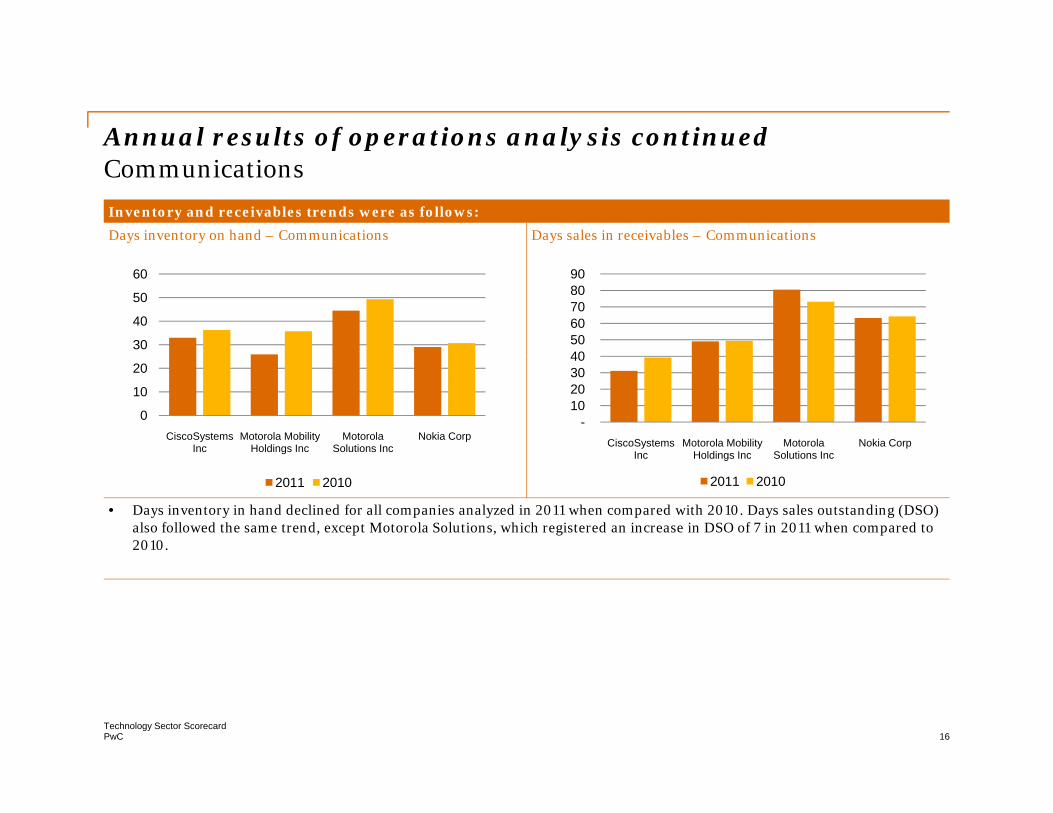

Inventory and receivables trends were as follows:

Days inventory on hand – Communications Days sales in receivables – Communications

30

40

50

60

4050 60 70 80 90

0

10

20

CiscoSystems Inc

Motorola Mobility Holdings Inc

Motorola Solutions Inc

Nokia Corp-

10 20 30 40

CiscoSystems Inc

Motorola Mobility Holdings Inc

Motorola Solutions Inc

Nokia Corp

• Days inventory in hand declined for all companies analyzed in 2011 when compared with 2010. Days sales outstanding (DSO) also followed the same trend, except Motorola Solutions, which registered an increase in DSO of 7 in 2011 when compared to 2010.

2011 2010

Inc Holdings Inc Solutions Inc

2011 2010

PwCTechnology Sector Scorecard

16

Annual results of operations analysis continuedf p yCommunications

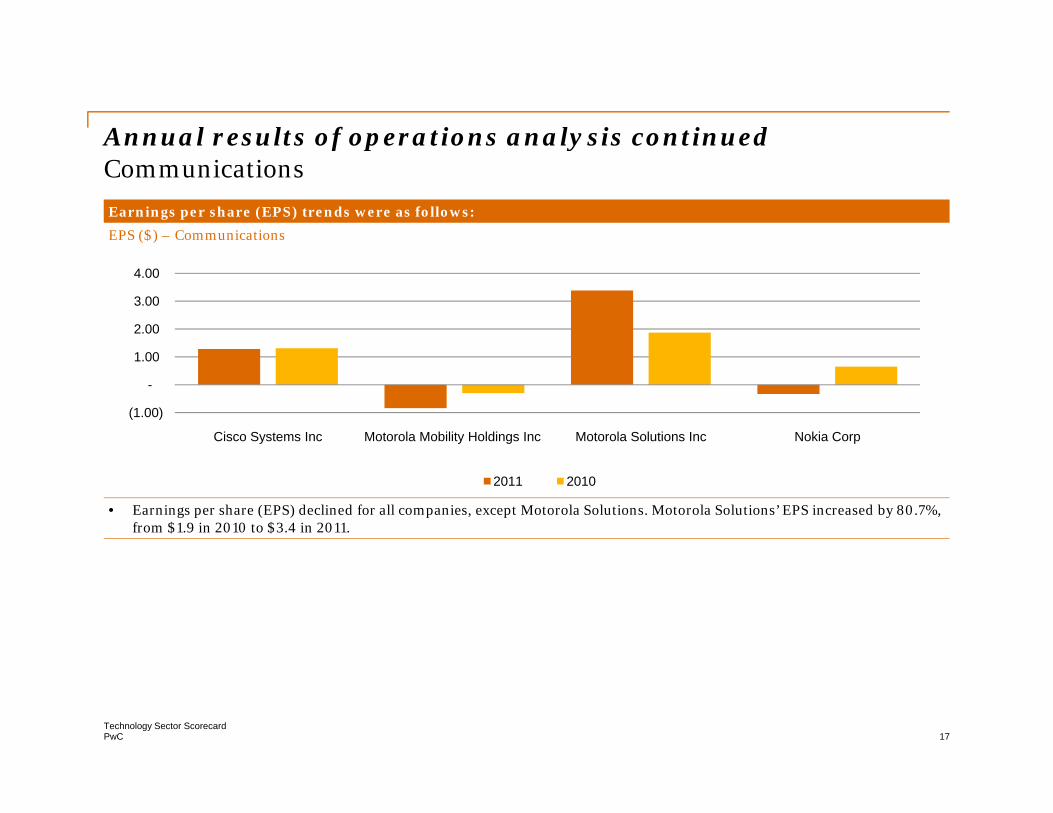

Earnings per share (EPS) trends were as follows:

EPS ($) – Communications

1 00

2.00

3.00

4.00

(1.00)

-

1.00

Cisco Systems Inc Motorola Mobility Holdings Inc Motorola Solutions Inc Nokia Corp

• Earnings per share (EPS) declined for all companies, except Motorola Solutions. Motorola Solutions’ EPS increased by 80.7%, from $1.9 in 2010 to $3.4 in 2011.

2011 2010

PwCTechnology Sector Scorecard

17

Q4 and Q3 performanceQ Q p fCommunications

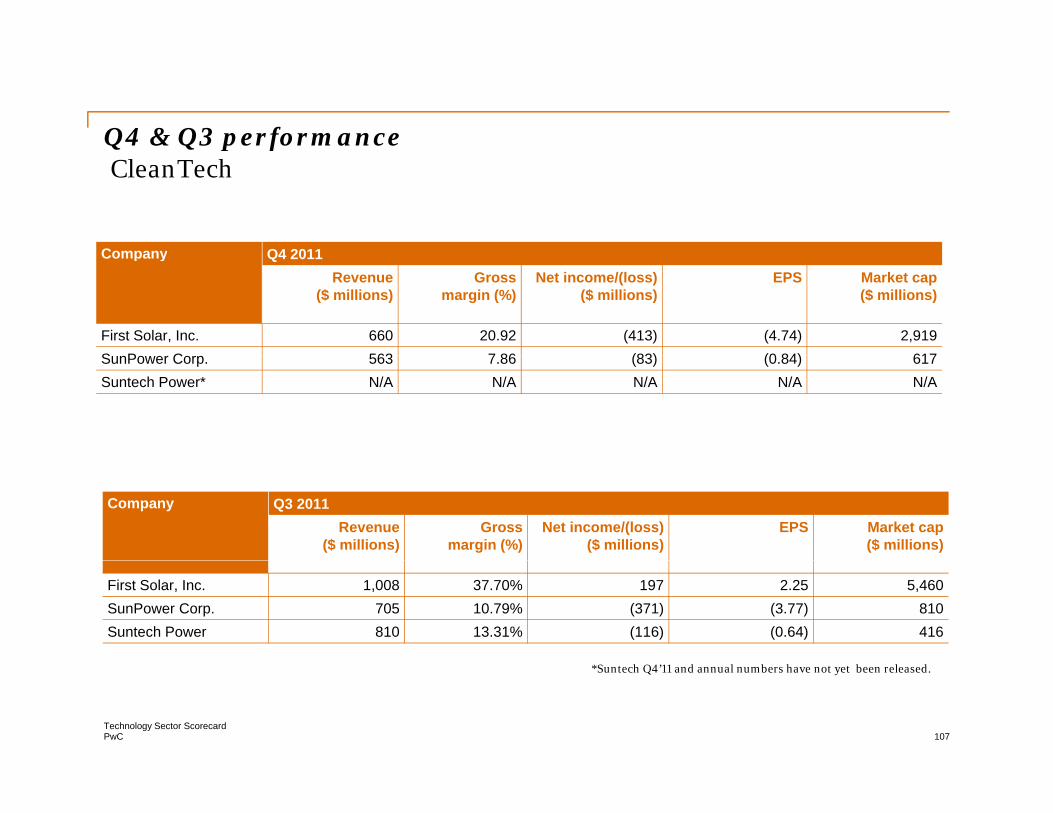

Company Q4 2011Revenue Gross margin (%) Net income/(loss) EPS ($) Market capRevenue

($ millions)Gross margin (%) Net income/(loss)

($ millions)EPS ($) Market cap

($ millions)

Cisco Systems Inc 11,527 61.29% 2,182 0.40 105,037

Motorola Mobility Holdings Inc 3 436 24 85% (80) (0 27) 11 648Holdings Inc 3,436 24.85% (80) (0.27) 11,648

Motorola Solutions Inc 2,300 50.43% 184 0.56 14,757

Nokia Corp* 13,067 29.03% (1,405) (0.29) 17,883

*EUR to USD exchange rate used for Nokia is 1.306 USD/EUR.

Company Q3 2011Revenue

($ millions)Gross margin (%) Net income/(loss)

($ millions)EPS ($) Market cap

($ millions)

Cisco Systems Inc 11,256 61.21% 1,777 0.33 94,478

Motorola Mobility Holdings Inc 3,259 25.90% (32) (0.11) 11,315

Motorola Solutions Inc 2,105 50.36% 128 0.38 13,638

Nokia Corp* 12 303 27 94% (207) (0 03) 20 999

PwCTechnology Sector Scorecard

18

Nokia Corp* 12,303 27.94% (207) (0.03) 20,999

*EUR to USD exchange rate used for Nokia is 1.370 USD/EUR.

Q2 and Q1 performanceQ Q p fCommunications

Company Q2 2011Revenue

($ )Gross margin (%) Net income/(loss)

($ )EPS ($) Market cap

($ )($ millions) ($ millions) ($ millions)

Cisco Systems Inc 11,195 61.29% 1,232 0.22 87,838

Motorola Mobility Holdings Inc 3,337 25.89% (56) (0.19) 6,971

Motorola Solutions Inc 2,055 50.56% 349 1.00 15,954

Nokia Corp* 13,254 30.53% (703) (0.14) 24,709

*EUR to USD exchange rate used for Nokia is 1.429 USD/EUR.

Company Q1 2011Revenue

($ millions)Gross margin (%) Net income/(loss)

($ millions)EPS ($) Market cap

($ millions)

Cisco Systems Inc 10 866 61 28% 1 807 0 33 96 378Cisco Systems Inc 10,866 61.28% 1,807 0.33 96,378

Motorola Mobility Holdings Inc 3,032 24.90% (81) (0.27) 7,198

Motorola Solutions Inc 1,884 50.00% 497 1.44 15,074

Nokia Corp* 14,746 29.56% 328 0.13 61,883

PwCTechnology Sector Scorecard

19

p , ,

*EUR to USD exchange rate used for Nokia is 1.418 USD/EUR.

Quarterly results of operations analysis (Q4) Q y f p y (Q4)Communications

Revenue and gross margin trends were as follows:

Revenue (in $ millions) – Communications Gross margin % – Communications

20 000 70 00%

5 000

10,000

15,000

20,000

20 00%

30.00%

40.00%

50.00%

60.00%

70.00%

0

5,000

Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011

Cisco Systems Inc Motorola Mobility Holdings Inc*

Motorola Solutions Inc* Nokia Corp

0.00%

10.00%

20.00%

Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011

Cisco Systems Inc Motorola Mobility Holdings Inc*

Motorola Solutions Inc* Nokia Corp

• Cisco’s revenue for Q4 2011 increased by 10.8% to $11.5 billion versus $10.4 billion in 2010. The company is currently focused on improving gross margins, which remained flat sequentially in Q4 2011.

• Motorola Mobility’s Q4 2011 revenues were at $3.4 billion, up by 0.3% compared to Q4 2010 owing to higher revenues in the Mobile Devices segment. The company shipped 10.5 million mobile devices, which included 5.3 million smartphones in Q4

Motorola Solutions Inc* Nokia Corp Motorola Solutions Inc Nokia Corp

2011. Gross margins declined to 24.9% in Q4 2011 from 26.7% in Q4 2010.

• Nokia’s revenues in Q4 2011 declined by 21.7% versus Q4 2010. However, its performance on a quarter-over-quarter basis was positive – Q4 2011 revenue was 6.2% higher as compared to Q3 2011. The increase was attributable to the launch of the new phone model Lumia, which sold over 1 million units and to higher seasonal demand. Gross margin increased slightly on a quarter-over-quarter basis due to a margin increase in the Mobile Phones segment, which was offset by the decline in Smart Devices and low IPR royalty income

PwCTechnology Sector Scorecard

20

Devices and low IPR royalty income.

* Prior quarter financials (Q4 2010) for Motorola Mobility and Motorola Solutions are as per the 10K filed last quarter. The sharp variance in the revenues for Motorola Solutions isbecause Motorola Solutions’ prior quarter financials include Motorola Mobility’s results as “discontinued operations”.

Quarterly results of operations analysis (Q4) continuedQ y f p y QCommunicationsR&D expenditure trends were as follows:

R&D expenses (in $ millions) – Communications R&D expenses (% of revenue) – Communications

2 500 17 00%

1,000

1,500

2,000

2,500

11 00%

13.00%

15.00%

17.00%

0

500

Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011

Cisco Systems Inc Motorola Mobility Holdings Inc*

9.00%

11.00%

Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011

Cisco Systems Inc Motorola Mobility Holdings Inc*

• Cisco’s R&D expense declined by 9.4% in Q4 2011 versus Q4 2010. R&D expenditure as a percentage of revenue also fell to 11.6% from 14.2% in Q4 2010.

• R&D expenses for Motorola Mobility increased by 4.6% to $0.4 billion in Q4 2011. Its R&D expenditure as a percentage of

Motorola Solutions Inc* Nokia Corp Motorola Solutions Inc* Nokia Corp

p y y 4 $ 4 Q4 p p grevenues increased marginally to 11.2% in Q4 2011 from 10.7% in Q4 2010.

• Motorola Solutions reported a decrease in R&D expenses by 58.5% to $0.3 billion over Q4 2010. However, R&D as a percentage of revenue fell slightly to 11.6% in Q4 2011 from 11.3% in Q4 2010.

• Nokia reported a decline of 9.9% in R&D expenses in Q4 2011. R&D as a percentage of sales also increased in Q4 2011 to 14.0% from 12.2% in Q4 2010. The rise in Nokia’s R&D expenses is due to its increased spending in Mobile Phone research as

PwCTechnology Sector Scorecard

21

part of its “next billion” strategy.

* Prior quarter financials (Q4 2010) for Motorola Mobility and Motorola Solutions are as per the 10K filed last quarter. The sharp variance in R&D expenses for Motorola Solutionsis because Motorola Solutions’ prior quarter financials include Motorola Mobility’s results as “discontinued operations”.

Quarterly results of operations analysis (Q4) continued Q y f p y QCommunicationsNet income trends were as follows:

Net income (in $ millions) – Communications

0

1,000

2,000

3,000

-2,000

-1,000

0

Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011

Cisco Systems Inc Motorola Mobility Holdings Inc* Motorola Solutions Inc* Nokia Corp

• Cisco reported a robust increase in net income of 43.5% to $2.1 billion in Q4 2011 from $1.5 billion in Q4 2010. The rise wasprimarily attributible to lower operating expenses. Amortization of intangible assets was 52.2% lower than in Q4 2010. Lower R&D expenses and SG&A, along with lower interest expense and higher interest income, favorably contributed to the net income trend.

• Motorola Mobility incurred a a net loss of $80.0 million in Q4 2011 against a net income of $80 million in Q4 2010. Higher y g gcost of goods sold, SG&A and R&D expenses contributed to the decline in net income.

• Motorola Solutions reported a decline in net income of 37.2% to $184 million in Q4 2011 from $0.3 billion in Q4 2010. Lower earnings from discontinued operations and higher income tax expense resulted in the fall in net income.

• Nokia suffered a net loss of $1.4 billion in Q4 2011 from a net income of $0.9 billion in Q4 2010. In spite of an increase inaverage selling price (ASP), the company had an operating loss due to the goodwill impairment of $1.0 billion, which was

b i

PwCTechnology Sector Scorecard

22

absent in Q4 2010.

* Prior quarter financials (Q4 2010) for Motorola Mobility and Motorola Solutions are as per the 10K filed last quarter. The sharp variance in Net Income for Motorola Solutions isbecause Motorola Solutions’ prior quarter financials include Motorola Mobility’s results as “discontinued operations”.

Quarterly results of operations analysis (Q4) continued Q y f p y QCommunicationsInventory and receivables trends were as follows:

Days inventory on hand – Communications Days sales in receivables – Communications

60 80

30

45

60

40

60

80

0

15

Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011

Cisco Systems Inc Motorola Mobility Holdings Inc

0

20

Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011

Cisco Systems Inc Motorola Mobility Holdings Inc

• Cisco’s days inventory on hand decreased to 32 days in Q4 2011 from 35 days in Q4 2010. Receivable days declined to 30 days from 40 days in Q4 2010, as total receivables declined by 16.1% versus a rise in revenue of 10.8% in Q4 2011.

• Motorola Mobility’s inventory decreased to 24 days in Q4 2011 versus 28 days in Q3 2011. Receivable days declined by 2 days

y y g

Motorola Solutions Inc Nokia Corp

y y g

Motorola Solutions Inc Nokia Corp

to 47 days against Q3 2011.

• Motorola Solutions experienced a decline in inventory days to 40 days in Q4 2011 from 47 days in Q3 2011.

• Nokia’s days inventory increased by 5 days to 30 days in Q4 2011 as compared to Q4 2010.

PwCTechnology Sector Scorecard

23

Quarterly results of operations analysis (Q4) continuedQ y f p y QCommunicationsEPS (earnings per share) and P/E trends were as follows:

EPS ($) – Communications P/E – Communications

2 00

0.50

1.00

1.50

2.00

10 00

20.00

30.00

-0.50

0.00

Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011Cisco Systems Inc Motorola Mobility Holdings Inc*

Motorola Solutions Inc* Nokia Corp

0.00

10.00

Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011

Cisco Systems Inc Motorola Mobility Holdings Inc*

Motorola Solutions Inc* Nokia Corp

• Cisco’s EPS increased from $0.33 in Q3 2011 to $0.40 in Q4 2011 owing to a rise in net income by 22.8% against last quarter. Its price-earning (P/E) multiple decreased slightly to 15.2 in Q4 2011 from 15.3 in Q3 2011.

• A rise of 43.8% in net income over Q3 2011 contributed to an increase in EPS to $0.56 in Q4 2011 from$0.38 in Q3 2011 for Motorola Solutions The P/E multiple increased in Q4 2011 to 13 7 from 11 4 in Q3 2011

Motorola Solutions Inc Nokia Corp Motorola Solutions Inc Nokia Corp

Motorola Solutions. The P/E multiple increased in Q4 2011 to 13.7 from 11.4 in Q3 2011.

• Nokia had a negative EPS, which deteriorated as compared to Q3 2011 owing to a higher net loss in Q4 2011.

PwCTechnology Sector Scorecard

24

* Prior quarter financials (Q4 2010) for Motorola Mobility and Motorola Solutions are as per the 10K filed last quarter. The sharp variance in EPS for Motorola Solutions is becauseMotorola Solutions’ prior quarter financials include Motorola Mobility results as “discontinued operations”.

Snapshot by subsectorSnapshot by subsector

Consumer Electronics

PwCTechnology Sector Scorecard

25

Market analysisyConsumer Electronics• Lack of improvement in the employment and housing problems in the US, along with the sovereign

debt crisis in Europe, impacted the Consumer Electronics sector as a whole in 2011.

• Japanese Consumer Electronics companies, namely Canon, Sony and Toshiba, were hit due to the sharp appreciation of the yen, the earthquake in Japan and massive floods in Thailand, resulting in a slowdown of the economy.

• Apple Inc.’s net sales during this quarter increased $19.6 billion compared to the same quarter in 2011. This increase in net sales was driven by the launch of iPhone 4S, expanded distribution of the iPhone with new carriers, strong demand for iPad and higher sales from the iTunes store, partially offset by decreased sales of iPod.

• Analysts believe that Apple is well positioned to maintain momentum across key product lines driven by innovation in hardware, software and its services ecosystem. Analysts also think that for the iPhone business with continued backlog, as well as additional carrier expansion, share gains in the fast-growing smartphone segment will continue. In the case of the iPad, growth should be driven by a product refresh and a possible price cut.1

i hi h i i l h h i l i d b l h• Within the Consumer Business Unit, although Canon was negatively impacted by supply shortages caused by the earthquake and floods, efforts to ramp up production and boost sales in response to robust demand resulted in significant increases in year-on-year sales volumes for digital SLR cameras. With respect to inkjet printers, unit sales increased year on year, largely owing to growth in emerging markets.2

PwCTechnology Sector Scorecard

26

in emerging markets.

1. Credit Suisse - Jan 20122. Canon Inc.’s earnings release - Jan 2012

Market analysis continued

• In 2012, despite concerns over negative effects arising from stagnant economies mainly in Europe, Canon expects demands for products such as network digital MFDs and laser printers to realize solid growth While solid demand for digital SLR cameras is expected in all regions around the

yConsumer Electronics

solid growth. While solid demand for digital SLR cameras is expected in all regions around the globe, demand for compact digital cameras is projected to remain relatively unchanged in developed countries.1

• Philips’ fourth quarter results were impacted by weak European sales, postponement in deliveries of existing orders in the Healthcare sector and inventory correction actions and other operational existing orders in the Healthcare sector, and inventory correction actions and other operational issues in the Lighting business. These issues were partially offset by strong results in the Consumer Lifestyle growth businesses, which benefited from the early adoption of the Accelerate! change and performance improvement program.2

• Philips expects 2012 results to be affected by restructuring charges and one-time investments aimed Philips expects 2012 results to be affected by restructuring charges and one time investments aimed at improving their business performance trajectory as a part of the multi-year Accelerate! program. Excluding these additional charges, the company expects the underlying operating margins and capital efficiency in the sectors to improve in the latter part of 2012.2

• Sony Corporation’s operating profit was sharply down year on year mainly due to widening losses in Sony Corporation s operating profit was sharply down year on year mainly due to widening losses in the TV business, plus margin erosion in the digital camera, PC, component and professional solutions businesses owing to yen appreciation and the floods in Thailand.3

PwCTechnology Sector Scorecard

27

1. Canon Inc.’s earnings release - Jan 20122. Philips press release3. JP Morgan - Feb 2012

Market analysis continued

• Sony expects consolidated sales for the fiscal year ending March 31, 2012 to be ¥6,400 billion, slightly below their November forecast. This change is due to lower expected sales, mainly in the Consumer Electronics and Services segment resulting primarily from deterioration in the operating

yConsumer Electronics

Consumer Electronics and Services segment, resulting primarily from deterioration in the operating environment in developed countries.

• The consolidated sales of Toshiba Group were ¥4,353.9 billion, a year on year decrease of ¥315.7 billion. This was largely due to lower sales in the Digital Products and Electronic Devices segment.

• Toshiba’s Visual Product business, which includes LCD TVs, recorded a significant decrease in sales in Japan. The business saw the completion of the transition to terrestrial digital broadcasting, expiration of the eco-point stimulus program and price declines. The Storage Products business saw sales rise mainly due to a healthy performance by hard disk drives for mobile applications. However, the Semiconductor business saw a decrease in sales due to sharp yen appreciation the floods in the Semiconductor business saw a decrease in sales due to sharp yen appreciation, the floods in Thailand, price declines and a fall in demand for discrete semiconductors and system LSI.

PwCTechnology Sector Scorecard

28

Annual results of operations analysisf p yConsumer Electronics

Revenue and gross margin trends were as follows:

Revenues (in $ millions) – Consumer Electronics Gross margin % – Consumer Electronics

50 00%

60 000

80,000

100,000

120,000

30.00%

40.00%

50.00%

-

20,000

40,000

60,000

Apple Canon Inc Philips Sony Corp Toshiba0.00%

10.00%

20.00%

Apple Canon Inc Philips Sony Corp Toshiba

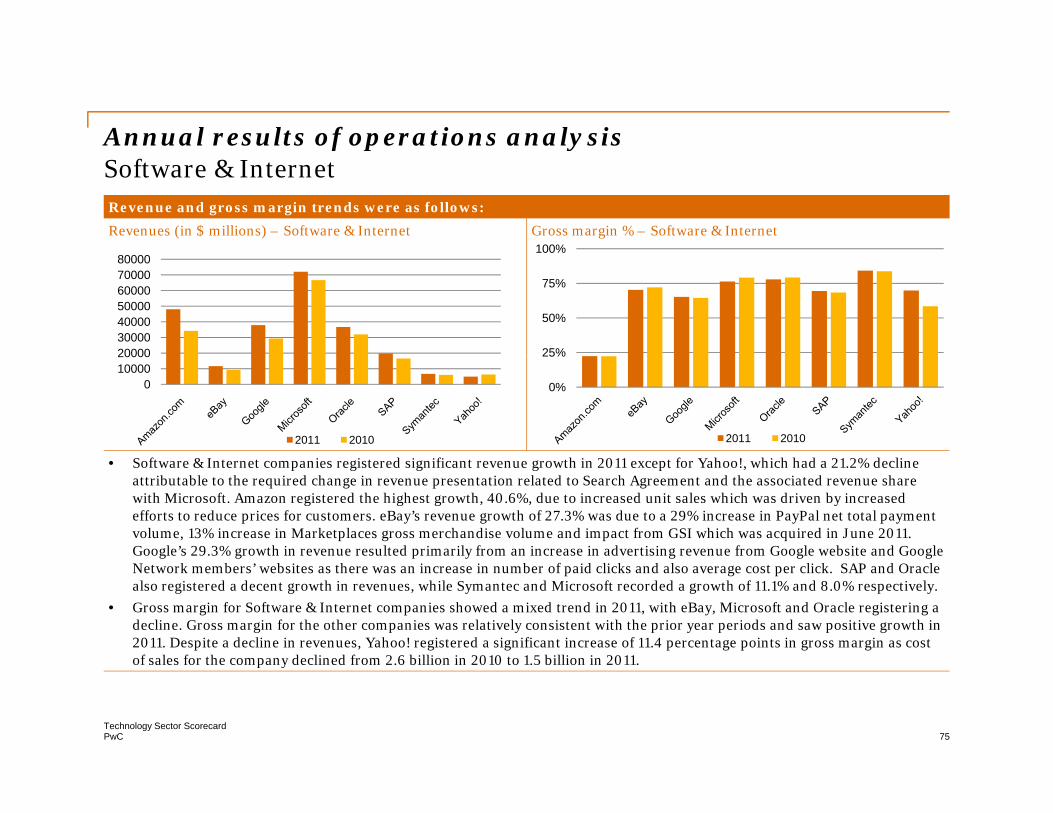

• Revenues for Consumer Electronics companies in 2011 exhibited a mixed trend when compared to 2010. Apple’s rise in revenue is directly attributable to the increased sales of iPhones, iPads and Mac computers. Canon’s revenue in the current year was lower by 4.0% in local currency (¥3,557.43 in 2011 vs. ¥3,706.90 in 2010), impacted by strong yen appreciation, earthquake and floods. Sales growth for Philips was lower when compared to last year due to weakness in European markets.

Apple Canon Inc Philips Sony Corp Toshiba2011 2010 2011 2010

q g p p y pRevenue for Sony decreased due to lower sales in Consumer Electronics & Services and Professional Device & Solutions segments. Toshiba’s revenue in 2011 was almost flat when compared to 2010.

• Gross margins for Consumer Electronics companies were largely consistent with the prior year, except for Apple whose gross margin increased by 365 bps. Apple’s increase in gross margin was largely driven by lower commodity and a mix of other product costs.

PwCTechnology Sector Scorecard

29

Annual results of operations analysis continuedf p yConsumer Electronics

R&D expenditure trends were as follows:

R&D expenses (in $ millions) – Consumer Electronics* R&D expenses (% of revenue) – Consumer Electronics*10 00%

2,000.00 2,500.00 3,000.00 3,500.00 4,000.00

4 00%

6.00%

8.00%

10.00%

-500.00

1,000.00 1,500.00

Apple Canon Inc Philips0.00%

2.00%

4.00%

Apple Canon Inc Philips

*Sony and Toshiba do not report R&D expense separately in public filings

• Research & Development (R&D) expenses for Consumer Electronics companies showed an upward trend when compared to last year. Apple showed the highest growth at 33.3% primarily due to an increase in headcount. R&D expenditure improved by 5.4% and 6.4% for Canon and Philips respectively. R&D as a percentage of revenue declined for Apple, due to a significant growth in the company’s net sales when compared to prior year while it remained consistent for Canon

2011 2010 2011 2010

growth in the company s net sales when compared to prior year, while it remained consistent for Canon.

PwCTechnology Sector Scorecard

30

Annual results of operations analysis continuedf p yConsumer Electronics

Net income trends were as follows:

Net income (in $ millions) – Consumer Electronics

20,000.00

30,000.00

40,000.00

(10,000.00)

-

10,000.00

Apple Canon Inc Philips Sony Corp Toshiba

• Net income for Consumer Electronics companies showed a mixed trend, as some were negatively impacted by the economic downturns in the US and Europe. Higher net income for Apple is directly attributable to higher net sales. Canon’s net income in local currency was in line with the prior year (¥248.63 in 2011 vs. ¥246.60). Lower net income for Philips was primarily due to lower sales in 2011 Sony’s net income declined due to decreased sales significant deterioration in the net income of

Apple Canon Inc Philips Sony Corp Toshiba

2011 2010

due to lower sales in 2011. Sony s net income declined due to decreased sales, significant deterioration in the net income ofaffiliated companies and a smaller benefit from foreign exchange gains. Toshiba recorded an increase of 8.3% in its net income compared to prior year.

PwCTechnology Sector Scorecard

31

Annual results of operations analysis continuedf p yConsumer Electronics

Inventory and receivables trends were as follows:

Days inventory on hand – Consumer Electronics Days sales in receivables – Consumer Electronics

50 60 70 80 90

100

40 50 60 70 80

-10 20 30 40

Apple Inc Canon Inc Philips Sony Corp Toshiba-

10 20 30

Apple Inc Canon Inc Philips Sony Corp Toshiba

• Days inventory on hand increased for Canon, Philips and Toshiba, while it declined for Apple and Sony. Despite an increase ininventories, Apple’s significant growth in sales in 2011 contributed to the decline in days inventory. Canon optimized its inventory levels to meet the growing demand and recorded the highest increase (20 days) in days inventory on hand.

Apple Inc Canon Inc Philips Sony Corp Toshiba

2011 2010

Apple Inc Canon Inc Philips Sony Corp Toshiba2011 2010

• Days sales in receivables also followed a mixed trend in 2011, with Philips and Toshiba registering an increase while Apple, Canon and Sony recorded declines. The largest increase was for Philips, whose DSO increased from 63 days in 2010 to 68 days in 2011.

PwCTechnology Sector Scorecard

32

Annual results of operations analysis continuedf p yConsumer Electronics

Earnings per share (EPS) trends were as follows:

EPS($) – Consumer Electronics

15.00 20.00 25.00 30.00 35.00 40.00

(10.00)(5.00)

-5.00

10.00

Apple Inc Canon Inc Philips Sony Corp Toshiba

• EPS increased for Consumer Electronics companies except for Philips and Sony which recorded negative EPS in 2011. Apple’s EPS grew from $ 17.91 in 2010 to $ 35.11 in 2011 on the back of strong demand for iPhones, iPads and Macs. Philips recorded negative EPS as a result of goodwill impairment charges, lower earnings and a loss from discontinued operations mainly related to disentanglement costs for the Television business Sony’s EPS was impacted by natural disasters in 2011 and hence

2011 2010

related to disentanglement costs for the Television business. Sony s EPS was impacted by natural disasters in 2011 and, hence, the company recorded negative EPS in all the four quarters. Canon and Toshiba registered a positive growth in EPS in 2011.

PwCTechnology Sector Scorecard

33

Q4 and Q3 performanceQ Q p fConsumer Electronics

Company Q4 2011

Revenue Gross Net income/(loss) EPS Market cap ($ millions) margin (%)

( )($ millions)

p($ millions)

Apple Inc 46,333 44.68% 13,064 13.87 377,547

Canon Inc 12,369 47.63% 788 0.70 529,155

Philips* 9 054 35 92% (219) (0 23) 19 402Philips* 9,054 35.92% (219) (0.23) 19,402

Sony Corp 23,370 30.74% (2038) (2.03) 18,105

Toshiba Corporation 18,479 22.10% (136) (0.03) 17,152

*EUR to USD exchange rate used for Philips is 1.349 USD/EUR.

Company Q3 2011

Revenue($ millions)

Grossmargin (%)

Net income/(loss)($ millions)

EPS Market cap ($ millions)

Apple Inc 28,270 40.25% 6,623 7.05 370,327pp , , ,

Canon Inc 11,908 49.35% 1,011 0.84 54,380

Philips* 7,633 38.30% 105 0.11 16,865

Sony Corp 20,454 33.84% (350) (0.35) 19,068

Toshiba Corporation 20,602 24.66% 288 0.07 17,448

PwCTechnology Sector Scorecard

34

*EUR to USD exchange rate used for Philips is 1.415 USD/EUR.

Q2 and Q1 performanceQ Q p fConsumer Electronics

Company Q2 2011

Revenue Gross Net income/(loss) EPS Market cap ($ millions) margin (%) ($ millions) ($ millions)

Apple Inc 28,571 41.73% 7,308 7.79 307,769

Canon Inc 10,328 50.03% 665 0.54 57,849

Philips* 7 496 39 19% (1 933) (2 00) 24 710Philips 7,496 39.19% (1,933) (2.00) 24,710

Sony Corp 18,456 34.88% (191) (0.19) 26,484

Toshiba Corporation 16,372 23.44% 5,802 - 22,361

*EUR to USD exchange rate used for Philips is 1.438 USD/EUR.

Company Q1 2011

Revenue($ millions)

Grossmargin (%)

Net income/(loss)($ millions)

EPS Market cap ($ millions)

Apple Inc 24,667 41.42% 5,987 6.40 324,043

Canon Inc 10,111 48.41% 668 0.54 53,254

Philips* 7,186 40.42% 187 0.19 30,477

Sony Corp 19,046 30.28% (4,684 ) (4.67) 31,944

Toshiba Corporation 20,830 23.51% 1,177 0.28 20,921

*EUR t USD h t d f Phili i 1 367 USD/EUR

PwCTechnology Sector Scorecard

35

*EUR to USD exchange rate used for Philips is 1.367 USD/EUR.

Quarterly results of operations analysis (Q4)Q y f p y QConsumer ElectronicsRevenue and gross margin trends were as follows:

Revenues (in $ millions) – Consumer Electronics Gross margin % – Consumer Electronics

20,000

30,000

40,000

50,000

40.00%

60.00%

80.00%

0

10,000

Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011

Apple Inc Canon IncPhilips Sony Corp

0.00%

20.00%

Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011

Apple Inc Canon IncPhilips Sony Corp

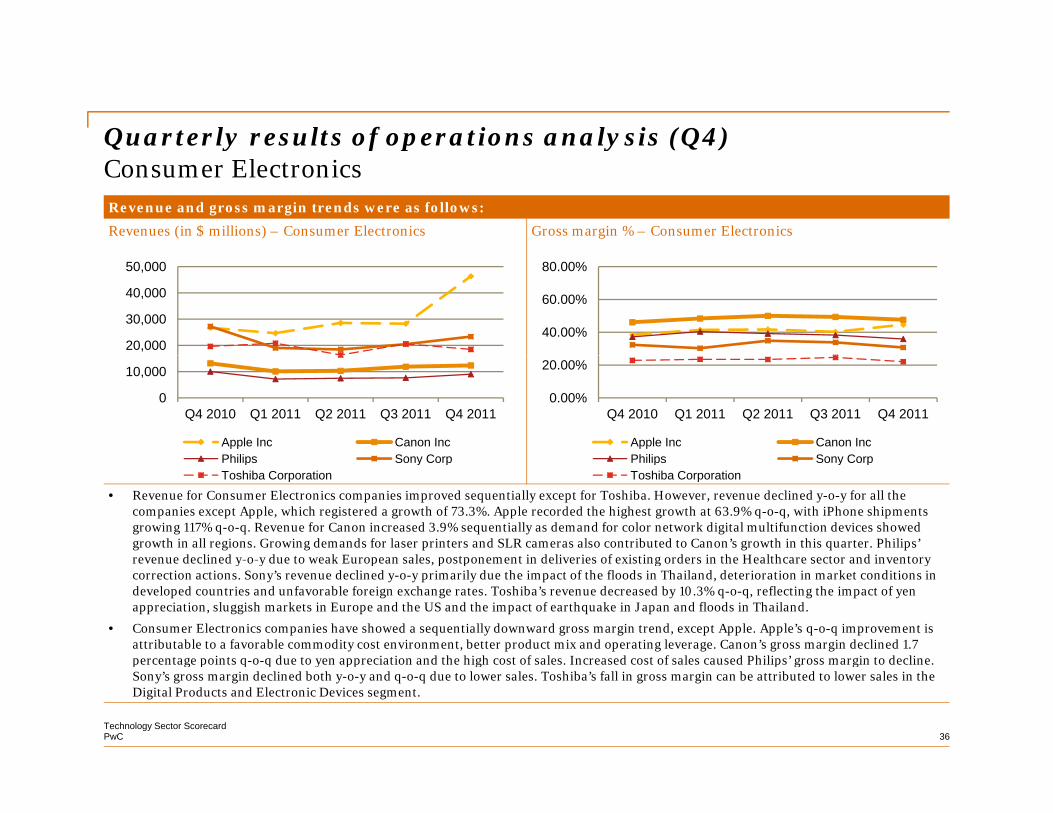

• Revenue for Consumer Electronics companies improved sequentially except for Toshiba. However, revenue declined y-o-y for all thecompanies except Apple, which registered a growth of 73.3%. Apple recorded the highest growth at 63.9% q-o-q, with iPhone shipments growing 117% q-o-q. Revenue for Canon increased 3.9% sequentially as demand for color network digital multifunction devices showed growth in all regions. Growing demands for laser printers and SLR cameras also contributed to Canon’s growth in this quarter. Philips’ revenue declined y-o-y due to weak European sales postponement in deliveries of existing orders in the Healthcare sector and inventory

Philips Sony CorpToshiba Corporation

Philips Sony CorpToshiba Corporation

revenue declined y o y due to weak European sales, postponement in deliveries of existing orders in the Healthcare sector and inventory correction actions. Sony’s revenue declined y-o-y primarily due the impact of the floods in Thailand, deterioration in market conditions in developed countries and unfavorable foreign exchange rates. Toshiba’s revenue decreased by 10.3% q-o-q, reflecting the impact of yen appreciation, sluggish markets in Europe and the US and the impact of earthquake in Japan and floods in Thailand.

• Consumer Electronics companies have showed a sequentially downward gross margin trend, except Apple. Apple’s q-o-q improvement is attributable to a favorable commodity cost environment, better product mix and operating leverage. Canon’s gross margin declined 1.7 percentage points q-o-q due to yen appreciation and the high cost of sales. Increased cost of sales caused Philips’ gross margin to decline.

PwCTechnology Sector Scorecard

36

percentage points q o q due to yen appreciation and the high cost of sales. Increased cost of sales caused Philips gross margin to decline. Sony’s gross margin declined both y-o-y and q-o-q due to lower sales. Toshiba’s fall in gross margin can be attributed to lower sales in the Digital Products and Electronic Devices segment.

Quarterly results of operations analysis (Q4) continuedQ y f p y QConsumer Electronics

R&D expenditure trends were as follows:

R&D expenses (in $ millions) – Consumer Electronics* R&D expenses (% of revenue) – Consumer Electronics*

400600800

1,0001,200

6.00%

9.00%

12.00%

15.00%

0200400

Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011

Apple Inc Canon Inc Philips

0.00%

3.00%

Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011

Apple Inc Canon Inc Philips

*Sony and Toshiba do not report R&D expense separately in public filings.

• R&D expenses for Consumer Electronics companies improved both q-o-q and y-o-y. Apple’s R&D expenses increased y-o-y primarily due to an increase in headcount and related expenses to support R&D activities. Canon’s R&D expense improved sequentially due to acceleration of production innovation activities. Philips’ R&D expenses improved by 10.0% this quarter due to increased investments in new product innovation and sales channels and increased headcount due to acquisitions

Apple Inc Canon Inc Philips Apple Inc Canon Inc Philips

due to increased investments in new product innovation and sales channels and increased headcount due to acquisitions.

• In this quarter R&D as a percentage of income declined by 65 bps for Apple, by 52 bps for Philips and remained almost flat for Canon. Apple’s R&D expenses as a percentage of revenue decreased due to the 63.9% y-o-y increase in net sales.

PwCTechnology Sector Scorecard

37

Quarterly results of operations analysis (Q4) continuedQ y f p y QConsumer Electronics

Net income trends were as follows:

Net income (in $ millions) – Consumer Electronics

4000

9000

14000

-6000

-1000

4000

Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011

• Net income for Consumer Electronics companies in the analysis showed a negative trend in this quarter except for Apple which exhibited a significant rise of 97.3% q-o-q. Apple’s net income improved y-o-y due to 133%, 99% and 22% higher sales of iPhones, iPads and Mac computers respectively. Canon’s net income increased by 18.3% y-o-y due to a lower effective income tax rate

Apple Inc Canon Inc Philips Sony Corp Toshiba Corporation

income tax rate.

• Philips’ net income declined significantly y-o-y, largely attributable to lower earnings and a higher loss from discontinued operations. Sony’s y-o-y decline in net income resulted from lower sales of LCD televisions due to deteriorating market conditions in Japan, Europe and North America. Net income for Toshiba decreased compared to the same period last year due to lower sales of Digital Products and Electronic Devices, reflecting the impact of sharp yen appreciation, the March earthquake, the floods in Thailand and demand deterioration.

PwCTechnology Sector Scorecard

38

q

Quarterly results of operations analysis (Q4) continuedQ y f p y QConsumer Electronics

Inventory and receivables trends were as follows:

Days inventory on hand – Consumer Electronics Days sales in receivables – Consumer Electronics

406080

100120

406080

100120140

02040

Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011

Apple Inc Canon IncPhilips Sony Corp

02040

Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011

Apple Inc Canon IncPhilips Sony Corp

• Days inventory on hand declined significantly for Canon, Philips and Sony when compared to the previous quarter. The decline is directly attributable to lower inventories in the current quarter. Inventory for Philips declined across all sectors and Sony registered lower inventories due to valuation loss in its unprofitable TV business. Apple’s days inventory was in line withthe previous quarters while Toshiba had a sequential increase of six days

Philips Sony CorpToshiba Corporation

Philips Sony CorpToshiba Corporation

the previous quarters, while Toshiba had a sequential increase of six days.

• Days sales in receivables (DSO) increased sequentially for all companies except for Philips which registered a decline of 10 days. DSOs for Apple and Sony were in line with the previous quarter. Toshiba had the highest growth as its DSO increased from 57 days in the previous quarter to 64 days in the current quarter.

PwCTechnology Sector Scorecard

39

Quarterly results of operations analysis (Q4) continuedQ y f p y QConsumer Electronics

EPS and P/E trends were as follows:

EPS($) – Consumer Electronics P/E – Consumer Electronics

2.505.007.50

10.0012.5015.00

16

24

32

40

-5.00-2.500.00

Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011

Apple Inc Canon IncPhili S C

0

8

Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011

Apple Inc Canon IncPhilips Sony Corp

• EPS for Consumer Electronics companies registered significant movements, with Philips, Sony and Toshiba recording negative EPS of $0.23, $2.03 and $0.03 respectively. Philips’ negative EPS was due to its lower earnings and a higher loss from discontinued operations which included an after-tax loss related to the Television business. Sony’s EPS was impacted by the floods in Thailand which negatively affected digital cameras and camcorders Also the company recorded valuation losses

Philips Sony CorpToshiba Corporation

Philips Sony CorpToshiba Corporation

the floods in Thailand which negatively affected digital cameras and camcorders. Also, the company recorded valuation losses on S-LCD shares and an appraisal loss allowance for Sony Ericsson. Apple’s EPS almost doubled due to increased holiday sales and an additional week in the December quarter. EPS for Canon and Toshiba declined sequentially.

• Consumer Electronics companies recorded lower P/E this quarter, except for Toshiba, as stock prices did not show any significant upward trend. Analysts believe that the new iPad 3 and iPhone 5 will help maintain sales momentum for Apple in 2012 and lead to higher P/E in the coming quarters. Canon is expected to benefit from the growth potential of the SLR

PwCTechnology Sector Scorecard

40

g / g q p g pbusiness. Overall, P/E for the sector is expected to rise.

Snapshot by subsectorSnapshot by subsector

EMS/Distributors

PwCTechnology Sector Scorecard

41

Market analysis yEMS/Distributors

• EMS companies, in general, seem to have recovered from their low stock prices in November, but p g pstill remain significantly below their highs of the last year. With the US breaking away from the woes of Europe and the effects of the Thai floods abating somewhat, it is possible that EMS stocks could offer significant value in 2012 and for long-term investors.1

• Arrow Electronics’ sales in 2011 were driven by increased demand for the company’s products in EMEA and America, as well as by the impact of acquisitions. In the global Enterprise Computing Solutions (ECS) business segment, the sales in 2011 increased due to growth in storage, software, services, industry standard servers and proprietary servers.

• Approximately 55% of Arrow’s sales in 2011 came from its operations outside the US. As a result, its operations are subject to a variety of risks that are specific to international operations, such as import and export regulations that could erode profit margins or restrict exports, the burden and cost of compliance with international laws, potential restrictions on transfers of funds, etc.

PwCTechnology Sector Scorecard

42

1. Market Watch - Jan 2012

Market analysis continued yEMS/Distributors

• Although Avnet’s revenue declined, the company’s continuing focus on profitability helped improve g p y g p y p pits gross profit margin and operating income margin from the prior year same quarter. The improved profitability at Technology Solutions (TS), which had an operating income margin within management’s target range for the first time in eight quarters, combined with the improvement in Electronic Marketing (EM), due primarily to higher prices for hard disk drives and a reduction in share count resulted in higher-than-expected diluted earnings per share for the quartershare count, resulted in higher-than-expected diluted earnings per share for the quarter.

• Flextronics International Ltd reported mixed results during the quarter as the exit from PC ODM (original design manufacturing) impacted both its sales and profitability. According to the analysts, Flextronics will continue to see sluggish but stable demand in the next quarter. With the PC ODM business now gone management sees higher operating margins and lower variability in sales in the business now gone, management sees higher operating margins and lower variability in sales in the future.1

PwCTechnology Sector Scorecard

43

1. Deutsche Bank - Jan 2012

Annual results of operations analysis f p yEMS/Distributors

Revenue and gross margin trends were as follows:

Revenues (in $ millions) – EMS/Distributors Gross margin % – EMS/Distributors

15,000 20,000 25,000 30,000 35,000

9.00%

12.00%

15.00%

-5,000

10,000 ,

Arrow Electronics Inc

Avnet Inc Flextronics International

0.00%

3.00%

6.00%

Arrow Electronics I

Avnet Inc Flextronics I t ti l

• Revenue for EMS companies improved in 2011 compared to 2010. The 14.1% increase in sales for Arrow was driven by an increase of 12.8% in the global components business segment sales and an increase of 17.2% in global ECS business segment sales, compared to last year. Avnet registered a 16.5% growth this year compared to last year due to the combination of acquisitions and organic growth Flextronics recorded revenue growth of 7 9% due to increased sales across all markets

Limited2011 2010

Inc International Limited2011 2010

acquisitions and organic growth. Flextronics recorded revenue growth of 7.9% due to increased sales across all markets.

• Gross margin increased for Arrow in 2011, but declined for Avnet and Flextronics. The increase in margin for Arrow was mainly due to improved pricing and a favorable mix towards higher-profit margin products in both global components and global ECS businesses. The gross margin of Flextronics decreased by 41 bps due to a higher mix of low-margin products and unfavorable manufacturing costs.

PwCTechnology Sector Scorecard

44

Annual results of operations analysis continued f p yEMS/Distributors

Net income trends were as follows:

Net income (in $ millions) – EMS/Distributors

300.00 400.00 500.00 600.00 700.00

-100.00 200.00

Arrow Electronics Inc Avnet Inc Flextronics International Limited

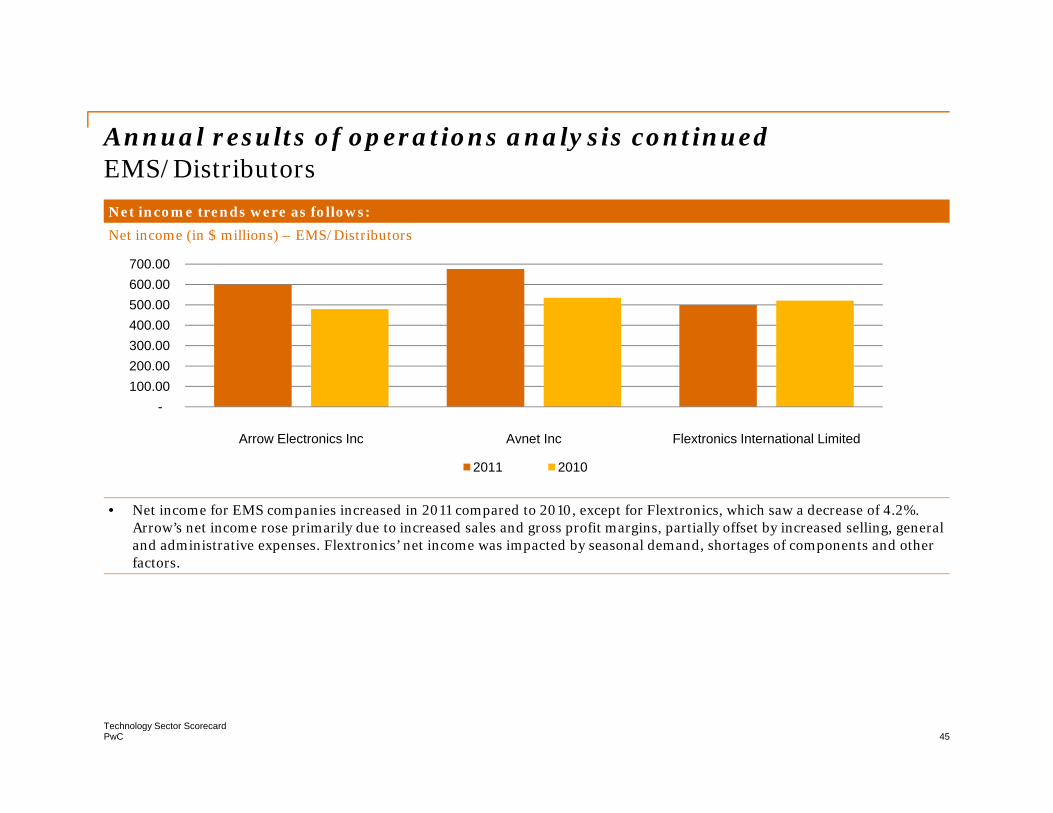

• Net income for EMS companies increased in 2011 compared to 2010, except for Flextronics, which saw a decrease of 4.2%. Arrow’s net income rose primarily due to increased sales and gross profit margins, partially offset by increased selling, general and administrative expenses. Flextronics’ net income was impacted by seasonal demand, shortages of components and other factors

2011 2010

factors.

PwCTechnology Sector Scorecard

45

Annual results of operations analysis continued f p yEMS/Distributors

Inventory and receivables trends were as follows:

Days inventory on hand – EMS/Distributors Days sales in receivables – EMS/Distributors

30.00

40.00

50.00

60.00

40.00 50.00 60.00 70.00 80.00 90.00

-

10.00

20.00

Arrow Electronics Inc

Avnet Inc Flextronics International

-10.00 20.00 30.00

Arrow Electronics Inc

Avnet Inc Flextronics International

• Days inventory on hand declined for EMS companies in 2011 compared to last year.

• Receivables also decreased for EMS companies in 2011.

Limited2011 2010

Limited2011 2010

PwCTechnology Sector Scorecard

46

Annual results of operations analysis continued f p yEMS/Distributors

Earnings per share (EPS) and market capitalization trends were as follows:

EPS – EMS/Distributors Market cap (in $ millions) – EMS/Distributors

4

5

6

4 000 00

5,000.00

6,000.00

7,000.00

0

1

2

3

1,000.00

2,000.00

3,000.00

4,000.00

Arrow Electronics Avnet Inc Flextronics

• EPS increased by 28.9% and 26.4% for Arrow and Avnet respectively, primarily due to higher net income and lower shares outstanding in 2011. EPS for Flextronics remained flat compared to last year, with lower income being offset by lower shares

Arrow Electronics Inc Avnet Inc Flextronics International Limited

2011 2010

Inc International Limited

2011 2010

outstanding.

• Market cap for Avnet and Flextronics showed a negative trend this year due to lower share prices compared to last year and the lower shares outstanding, while Arrow recorded a marginal increase of 6.4%.

PwCTechnology Sector Scorecard

47

Q4 and Q3 performanceQ Q p fEMS/Distributors

Company Q4 2011Company Q4 2011Revenue

($ millions)Gross

margin (%)Net income/(loss)

($ millions)EPS($) Market cap

($ millions)

Arrow Electronics Inc 5,440 13.69% 174 1.53 4,183

A t I 6 694 11 71% 147 0 98 4 506Avnet Inc 6,694 11.71% 147 0.98 4,506

Flextronics International Ltd 7,493 5.10% 102 0.14 4,037

Company Q3 2011Revenue

($ millions)Gross

margin (%)Net income/(loss)

($ millions)EPS($) Market cap

($ millions)

Arrow Electronics Inc 5,187 13.71% 132 1.15 3,104

Avnet Inc 6,426 11.73% 139 0.90 3,901

Flextronics International Ltd 8,044 4.67% 130 0.18 4,118

PwCTechnology Sector Scorecard

48

Q2 and Q1 performanceQ Q p fEMS/Distributors

Company Q2 2011Company Q2 2011Revenue

($ millions)Gross

margin (%)Net income/(loss)

($ millions)EPS($) Market cap

($ millions)

Arrow Electronics Inc 5,540 13.90% 156 1.33 5,252

A t I 6 912 11 93% 239 1 54 4 975Avnet Inc 6,912 11.93% 239 1.54 4,975

Flextronics International Ltd 7,548 5.30% 132 0.17 4,823

Company Q1 2011Revenue

($ millions)Gross

margin (%)Net income/(loss)

($ millions)EPS($) Market cap

($ millions)

Arrow Electronics Inc 5,223 13.83% 136 1.16 4,862

Avnet Inc 6,672 11.79% 151 0.98 5,201

Flextronics International Ltd 6,859 5.58% 135 0.17 5,797

PwCTechnology Sector Scorecard

49

Quarterly results of operations analysis (Q4) Q y f p y QEMS/DistributorsRevenue and gross margin trends were as follows:

Revenues (in $ millions) – EMS/Distributors Gross margin % – EMS/Distributors

4,000

6,000

8,000

10,000

5%

10%

15%

0

2,000

Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011

Arrow Electronics IncAvnet Inc

0%

5%

Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011

Arrow Electronics IncAvnet Inc

• Revenue increased for EMS companies, with Arrow and Avnet recording sequential growth of 4.8% and 4.2% respectively, while Flextronics’ revenue declined by 6.9% sequentially. Arrow Electronics’ revenue increased primarily due to increased sales in both the global components business segment and the global ECS business segment. Avnet’s revenue improved due to a rise in Electronic Marketing sales driven by growth in the American region Flextronics’ net sales declined due to decreased

Avnet IncFlextronics International Limited

Avnet IncFlextronics International Limited

a rise in Electronic Marketing sales, driven by growth in the American region. Flextronics net sales declined due to decreased sales in the High Velocity Solutions market, as a result of the exit from the ODM personal computing business in the current quarter.

• Gross margin remained almost flat sequentially for Arrow and Avnet. Flextronics’ gross margin improved due to lower cost of sales in this quarter.

PwCTechnology Sector Scorecard

50

Quarterly results of operations analysis (Q4) continued Q y f p y QEMS/DistributorsNet income trends were as follows:

Net income (in $ millions) – EMS/Distributors

100

150

200

250

0

50

100

Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011

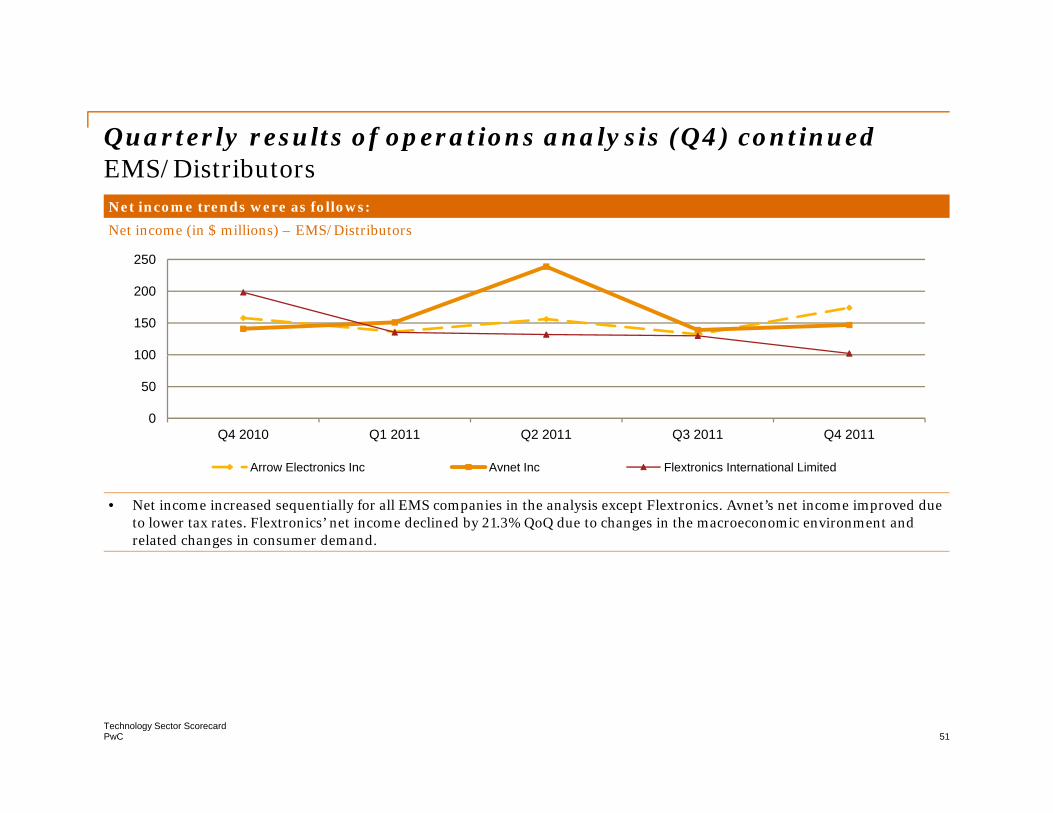

• Net income increased sequentially for all EMS companies in the analysis except Flextronics. Avnet’s net income improved due to lower tax rates. Flextronics’ net income declined by 21.3% QoQ due to changes in the macroeconomic environment and related changes in consumer demand.

Arrow Electronics Inc Avnet Inc Flextronics International Limited

PwCTechnology Sector Scorecard

51

Quarterly results of operations analysis (Q4) continued Q y f p y QEMS/DistributorsInventory and receivables trends were as follows:

Days inventory on hand – EMS/Distributors Days sales in receivables – EMS/Distributors

15

30

45

60

20

40

60

80

0

15

Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011

Arrow Electronics IncAvnet Inc

0

20

Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011

Arrow Electronics IncAvnet Inc

• Days inventory on hand decreased sequentially for Arrow Electronics from 44 days to 38 days and for Avnet from 42 days to 38 days. Days inventory on hand remained flat sequentially for Flextronics.

• Days sales in receivables (DSO) for EMS companies in the analysis almost remained flat QoQ for Avnet and Flextronics. Arro registered a marginal increase in DSO from 72 da s in the pre io s q arter to 74 da s in the c rrent q arter d e to

Flextronics International Limited Flextronics International Limited

Arrow registered a marginal increase in DSO, from 72 days in the previous quarter to 74 days in the current quarter, due to higher sales.

PwCTechnology Sector Scorecard

52

Quarterly results of operations analysis (Q4) continued Q y f p y QEMS/Distributors Earnings per share (EPS) and market capitalization trends were as follows:

EPS($) – EMS/Distributors Market cap (in $ millions) – EMS/Distributors

1.00

1.50

2.00

3 000

4,500

6,000

7,500

0.00

0.50

Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011

Arrow Electronics Inc

0

1,500

3,000

Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011

Arrow Electronics Inc

• EPS for Arrow increased sequentially by 33.0%, primarily due to higher revenues and lower operating expenses. Improved profitability at Technology Solutions, higher prices for hard disk drives and a lower share count were the factors behind A t’ hi h EPS i thi q t Fl t i ’ EPS d li d b 22 2% d t l t i

Avnet IncFlextronics International Limited

Avnet IncFlextronics International Limited

Avnet’s higher EPS in this quarter. Flextronics’ EPS declined by 22.2% due to lower net income.

• Avnet and Arrow registered increased market share in this quarter due to higher share prices.

PwCTechnology Sector Scorecard

53

Snapshot by subsectorSnapshot by subsector

Semiconductors

PwCTechnology Sector Scorecard

54

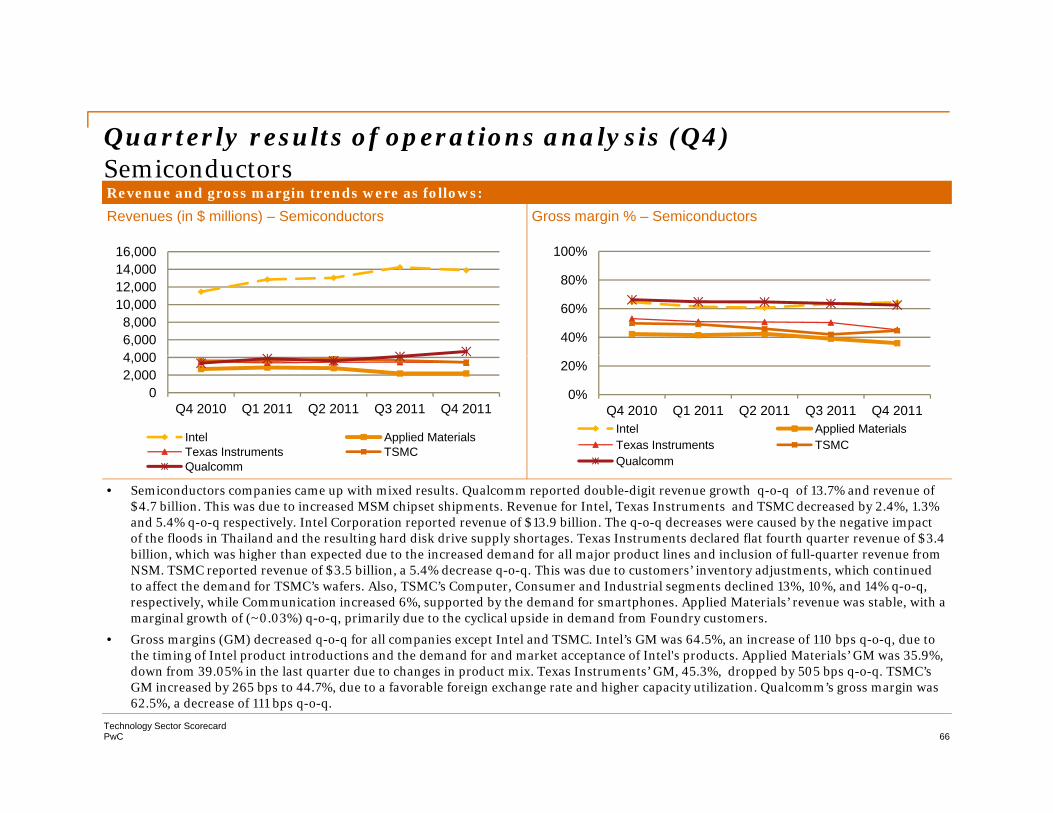

Market analysisySemiconductors

• Worldwide semiconductor sales for 2011 reached a record $299.5 billion, a year-on-year increase of 0.4% from the $298.3 billion recorded in 2010. In 2011, the industry saw strong d d i l ifi ll th t l t i d t t d demand in several areas; specifically the optoelectronic, sensor and actuator, and microprocessor markets showed strong y-o-y growth.1

• Worldwide semiconductor revenue is forecast to reach $309 billion in 2012, a 2.2% increase from 2011, according to Gartner, Inc. With continuing concern over the future of the euro zone

ff ti th l b l th i hi h d f t i t G t id th t th fl d affecting the global economy, there is a high degree of uncertainty. Gartner said that the floods that hit Thailand this year resulted in a hard-disk drive (HDD) shortage that has slowed the PC market even further and estimates that the supply chain disruption meant that the PC production will be limited by HDD availability over the next few quarters until the HDD industry can resume full production.2y p

• Worldwide semiconductor capital equipment spending is expected to total $51.7 billion in 2012, a 19.5% decline from projected 2011 spending of $64.2 billion, according to Gartner, Inc. The impact of the sluggish macro economy, high inventories and a slowing PC industry — due to both weak demand and the flooding in Thailand — will temper the outlook for 2012.2

PwCTechnology Sector Scorecard

55

1. Semiconductor Industry Association - Dec 20112. Gartner - Dec 2011

Market analysis continuedySemiconductors

• 2011 was by far Intel’s most profitable year. Revenue of $54.0 billion was up 24% from a year ago and was their second year in a row with revenue growing over 20%. PC Client Group grew 17% y-o-y and was their second year in a row with revenue growing over 20%. PC Client Group grew 17% y o y on continued strength in emerging markets, as rising incomes increased the affordability of personal computers, and on strength from the enterprise market segment. The server market segment was particularly strong, with Intel’s Data Center Group growing 17% year over year. The strength of the product portfolio drove a richer mix of products, resulting in an increase in average selling prices in I t l’ li t d b iIntel’s client and server businesses.

• Applied Materials generated orders of $2.01 billion and net sales of $2.19 billion during the quarter ended January 2012. Applied completed the acquisition of Varian Semiconductor Equipment Associates, Inc. during the quarter. Global demand for mobile devices has driven a third consecutive

f t it l i t t b i d t t l di t lid d t year of strong capital investment by semiconductor customers, leading to solid order momentum and an improved outlook overall for Applied’s second quarter. The company also returned substantial capital to stockholders, paying $104 million in cash dividends and using $200 million to repurchase common stock.

TSMC announced consolidated revenue of US$14 54 billion and net income of US$4 6 billion for • TSMC announced consolidated revenue of US$14.54 billion and net income of US$4.6 billion for full-year 2011. Compared to the previous year, the results represent a 9% increase in revenue, but an 11% decrease in net income. 28-nanometer process technology accounted for 2% of total wafer revenues, 40-nanometer was 27%, and 65-nanometer accounted for 30%. These advanced technologies accounted for 59% of total wafer revenues. Although the outlook of the global economy

PwCTechnology Sector Scorecard

56

remains uncertain, TSMC expects the demand for wafers to be stronger than seasonal for the first quarter.

Market analysis continuedySemiconductors

• Texas Instruments (TI) reported a revenue was $13.73 billion, net income of $2.24 billion and earnings per share (EPS) of $1.88 for the full year ended 2011. The company strengthened the core earnings per share (EPS) of $1.88 for the full year ended 2011. The company strengthened the core businesses of Analog, Embedded Processing and Wireless. Although the year started strong, global economic uncertainty and the earthquake in Japan impacted TI. Despite these challenges, it successfully completed the acquisition of National, gaining share in the Analog and Embedded Processing markets. TI continued to wind down their baseband operations. It announced fourth-

t f $3 42 billi d t i f $298 illi R i th t t quarter revenue of $3.42 billion and net income of $298 million. Revenue in the current quarter was higher than expected across all major product lines, reinforcing the belief that the economy is at the bottom of this downturn. The company has stated that in 2012 it will exit from the baseband market, and thus further focus on Analog, Embedded Processing and Wireless. TI closed its acquisition of National Semiconductor on September 23, 2011, and it began to consolidate the q p gresults of the acquired operations into TI's Analog segment under the name Silicon Valley Analog.

• Qualcomm reported another record quarter, with revenues of $4.68 billion, up 40% y-o-y and 14% sequentially. Earnings and MSM shipments reached all-time highs, driven by an industry-leading chipset portfolio and the continued strong demand for smartphones around the world. Broad licensing partnerships and an extensive chipset road map, led by integrated Snapdragon processors, position the company well for strong growth in fiscal 2012. It continues to invest in innovative wireless technologies, products and services.

PwCTechnology Sector Scorecard

57

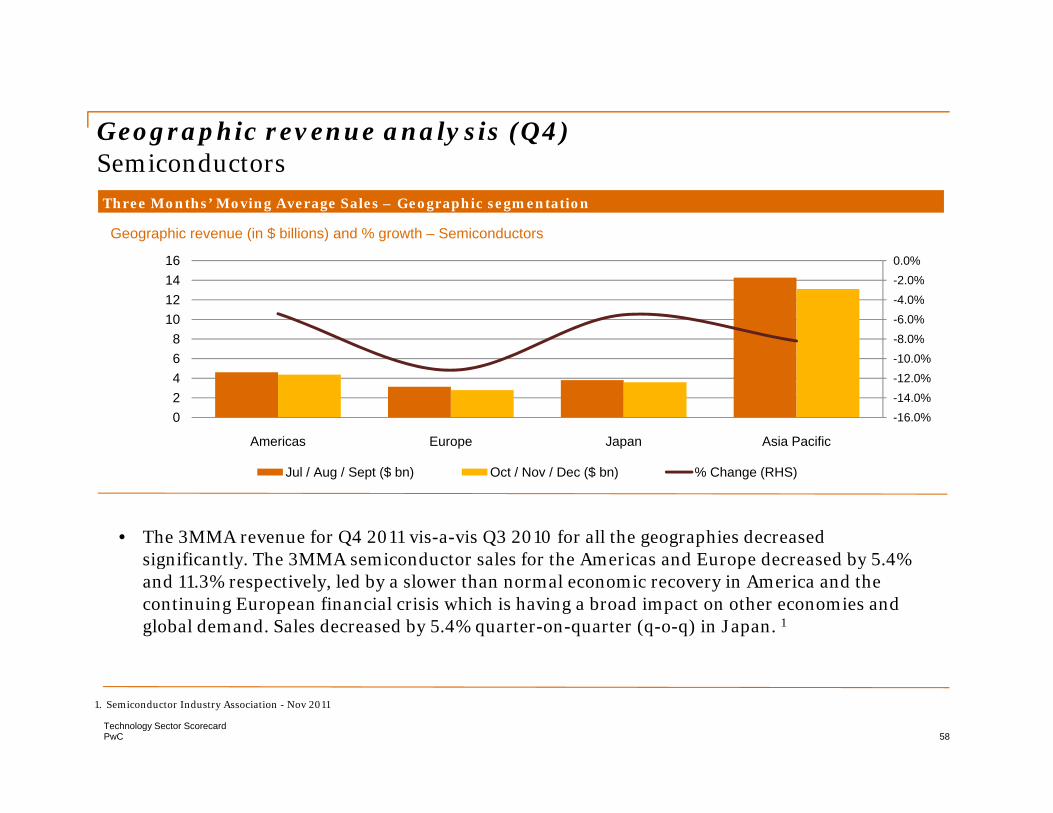

Geographic revenue analysis (Q4)

Three Months’ Moving Average Sales – Geographic segmentation

Geographic revenue (in $ billions) and % growth – Semiconductors

Semiconductors

10 0%-8.0%-6.0%-4.0%-2.0%0.0%

68

10121416

-16.0%-14.0%-12.0%-10.0%

0246

Americas Europe Japan Asia Pacific

Jul / Aug / Sept ($ bn) Oct / Nov / Dec ($ bn) % Change (RHS)

• The 3MMA revenue for Q4 2011 vis-a-vis Q3 2010 for all the geographies decreased significantly The 3MMA semiconductor sales for the Americas and Europe decreased by 5 4% significantly. The 3MMA semiconductor sales for the Americas and Europe decreased by 5.4% and 11.3% respectively, led by a slower than normal economic recovery in America and the continuing European financial crisis which is having a broad impact on other economies and global demand. Sales decreased by 5.4% quarter-on-quarter (q-o-q) in Japan. 1

PwCTechnology Sector Scorecard

58

1. Semiconductor Industry Association - Nov 2011

Annual results of operations analysis f p ySemiconductors

Revenue and gross margin trends were as follows:

Revenues (in $ millions) – Semiconductors Gross margin % – Semiconductors

25 00030,000 35,000 40,000 45,000 50,000 55,000 60,000

30 00%

40.00%

50.00%

60.00%

70.00%

-5,000

10,000 15,000 20,000 25,000

Intel Applied M t i l

TI TSMC Qualcomm

0.00%

10.00%

20.00%

30.00%

Intel Applied M t i l

TI TSMC Qualcomm

• Revenue for Semiconductor companies was higher in 2011 when compared to 2010 except Applied Materials and Texas Instruments (TI). Qualcomm’s annual revenue increased sharply by 39.7%, driven by an increased chipset portfolio and the continued strong demand for smartphones. Intel’s net revenue for 2011 increased to $54 billion, a rise of 23.8%, compared to 2010 led by 64% higher demand reported by Other Intel Architecture segment TSMC’s revenue increased by 9 2% led by

Materials

2011 2010 20102

Materials

2011 2010

2010, led by 64% higher demand reported by Other Intel Architecture segment. TSMC s revenue increased by 9.2%, led by higher demand in the communications segment. Applied Materials’ and TI’s revenues decreased by 3.5% and 1.6% respectively.

• All companies within the industry, except Applied Materials, witnessed lower gross margin percentages in 2011 compared with 2010 as cost of sales increased due to supply-chain issues impacting the industry. Raw materials costs increased in 2011 due to the natural disasters which impacted supplier companies.

PwCTechnology Sector Scorecard

59

p pp p

Annual results of operations analysis continuedf p ySemiconductors

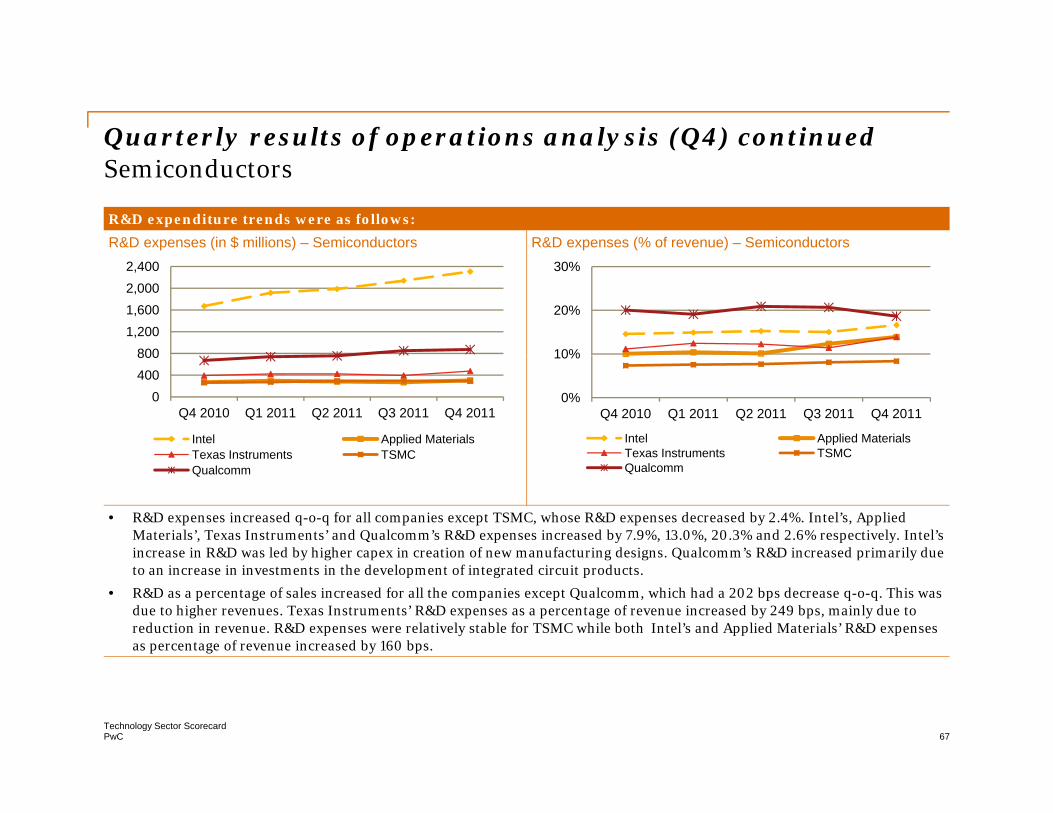

R&D expenditure trends were as follows:

R&D expenses (in $ millions) – Semiconductors R&D expenses (% of revenue) – Semiconductors9 000

4,0005,000 6,000 7,000 8,000 9,000

9.00%

12.00%

15.00%

18.00%

-1,000 2,000 3,000 4,000

Intel Applied M t i l

TI TSMC Qualcomm

0.00%

3.00%

6.00%

Intel Applied Materials

TI TSMC Qualcomm

• R&D expenses increased for all the companies in the sector compared to last year as companies increased their spending for newer technologies. Intel’s and Qualcomm’s R&D spending increased by 26.9% and 33.5% respectively in 2011 compared to 2010 This was led by increased spending on R&D for new products and also by acquisition-related increases in R&D

Materials2011 2010 2011 2010

2010. This was led by increased spending on R&D for new products and also by acquisition-related increases in R&D expenditure. The R&D expenditure for TSMC and TI increased y-o-y by 21.8% and 9.2% respectively. Applied Materials’ R&D expenditure was relatively flat y-o-y.

• R&D as a percentage of revenue was stable for all the companies, with a marginal increase y-o-y with the exception of Qualcomm.

PwCTechnology Sector Scorecard

60

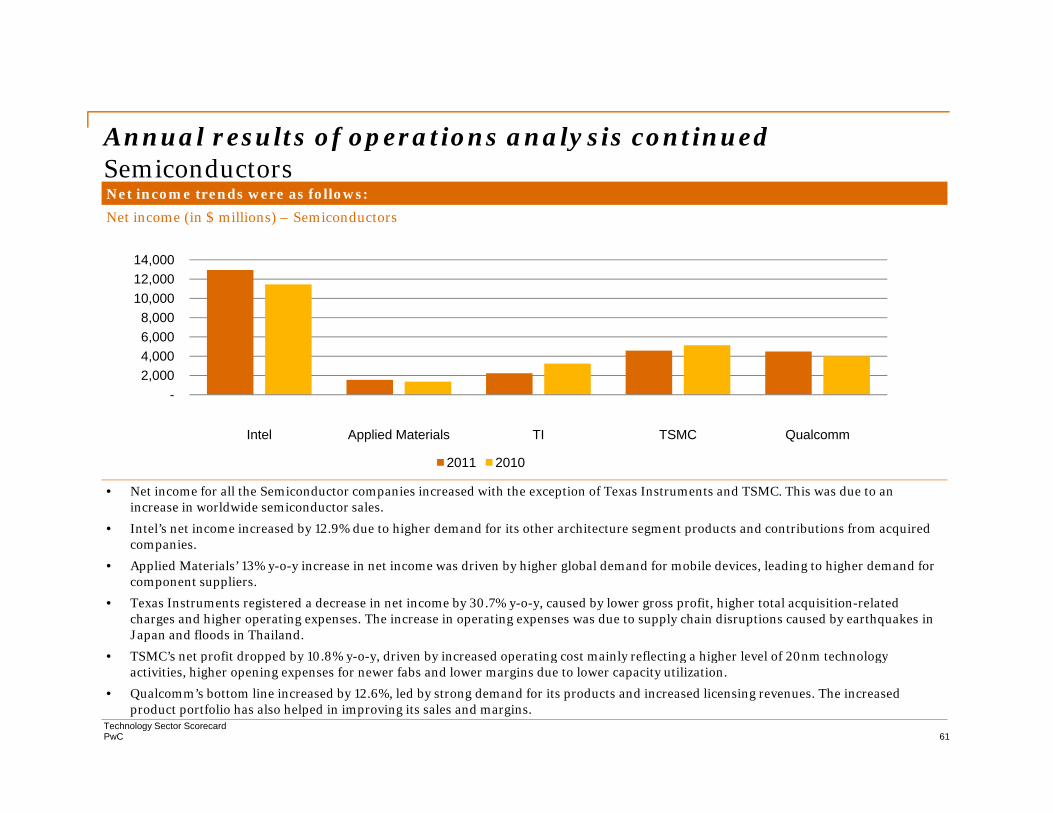

Annual results of operations analysis continued f p ySemiconductorsNet income trends were as follows:

Net income (in $ millions) – Semiconductors

4 0006,000 8,000

10,000 12,000 14,000

-2,000 4,000

Intel Applied Materials TI TSMC Qualcomm

2011 2010

• Net income for all the Semiconductor companies increased with the exception of Texas Instruments and TSMC. This was due to anincrease in worldwide semiconductor sales.

• Intel’s net income increased by 12.9% due to higher demand for its other architecture segment products and contributions from acquired companies.

li d i l ’ i i i d i b hi h l b l d d f bil d i l di hi h d d f

2011 2010

• Applied Materials’ 13% y-o-y increase in net income was driven by higher global demand for mobile devices, leading to higher demand for component suppliers.

• Texas Instruments registered a decrease in net income by 30.7% y-o-y, caused by lower gross profit, higher total acquisition-related charges and higher operating expenses. The increase in operating expenses was due to supply chain disruptions caused by earthquakes in Japan and floods in Thailand.

• TSMC’s net profit dropped by 10.8% y-o-y, driven by increased operating cost mainly reflecting a higher level of 20nm technology

PwCTechnology Sector Scorecard

61

p pp y y y y p g y g g gyactivities, higher opening expenses for newer fabs and lower margins due to lower capacity utilization.

• Qualcomm’s bottom line increased by 12.6%, led by strong demand for its products and increased licensing revenues. The increasedproduct portfolio has also helped in improving its sales and margins.

Annual results of operations analysis continued f p ySemiconductors

Inventory and receivables trends were as follows:

Days inventory on hand – Semiconductors Days sales in receivables – Semiconductors

60.00

90.00

120.00

40.00 50.00 60.00 70.00 80.00

-

30.00

Intel Applied TI TSMC Qualcomm

-10.00 20.00 30.00

Intel Applied TI TSMC Qualcomm

• Days inventory on hand declined for all companies except Applied Materials and Texas Instruments. The increase in DOI for Applied Materials and TI was due to slower demand as companies in the supply chain decided to clear off their inventory pileup.

ppMaterials

Q

2011 2010

ppMaterials

2011 2010

• DSO increased marginally for all companies except Applied Materials and TSMC, which had declines of 11 and 5 days respectively.

PwCTechnology Sector Scorecard

62

Annual results of operations analysis continued f p ySemiconductors

Earnings per share (EPS) trends were as follows:

EPS – Semiconductors

2.00

3.00

-

1.00

I t l A li d M t i l TI TSMC Q l

• EPS increased for all Semiconductor companies in 2011 as compared to 2010 except Texas Instruments and TSMC whose EPS declined by 29% and 10% respectively. Intel’s, Applied Materials’ and Qualcomm’s EPS increased by 19%, 14% and 9% respectively EPS was impacted by the same factors as net income as discussed two slides previously Other than net income

Intel Applied Materials TI TSMC Qualcomm2011 2010

respectively. EPS was impacted by the same factors as net income, as discussed two slides previously. Other than net income,the increase in EPS was also due to aggressive repurchasing activities by Intel, Applied Materials and Qualcomm.

PwCTechnology Sector Scorecard

63

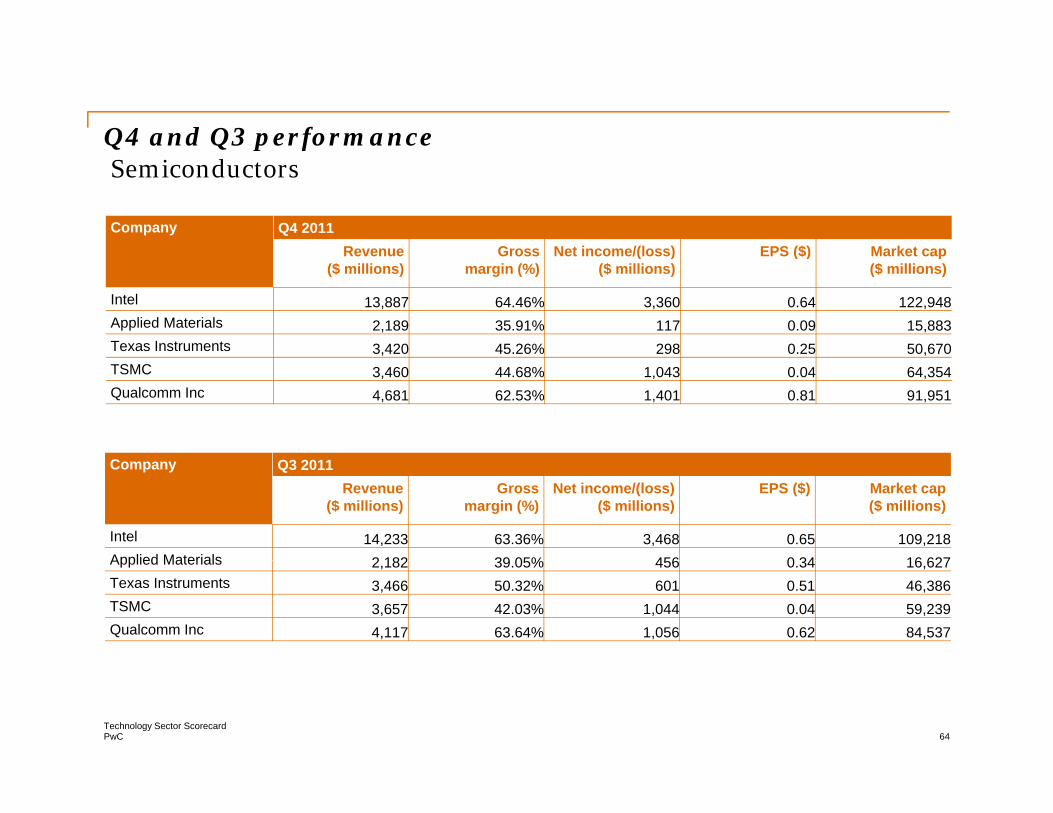

Q4 and Q3 performance Q Q p fSemiconductors

Company Q4 2011Revenue Gross Net income/(loss) EPS ($) Market capRevenue

($ millions)Gross

margin (%)Net income/(loss)

($ millions)EPS ($) Market cap

($ millions)

Intel 13,887 64.46% 3,360 0.64 122,948 Applied Materials 2,189 35.91% 117 0.09 15,883Texas Instruments 3,420 45.26% 298 0.25 50,670, ,TSMC 3,460 44.68% 1,043 0.04 64,354 Qualcomm Inc 4,681 62.53% 1,401 0.81 91,951

Company Q3 2011Revenue

($ millions)Gross

margin (%)Net income/(loss)

($ millions)EPS ($) Market cap

($ millions)

Intel 14,233 63.36% 3,468 0.65 109,218 Applied Materials 2 182 39 05% 456 0 34 16 627Applied Materials 2,182 39.05% 456 0.34 16,627 Texas Instruments 3,466 50.32% 601 0.51 46,386 TSMC 3,657 42.03% 1,044 0.04 59,239 Qualcomm Inc 4,117 63.64% 1,056 0.62 84,537

PwCTechnology Sector Scorecard

64

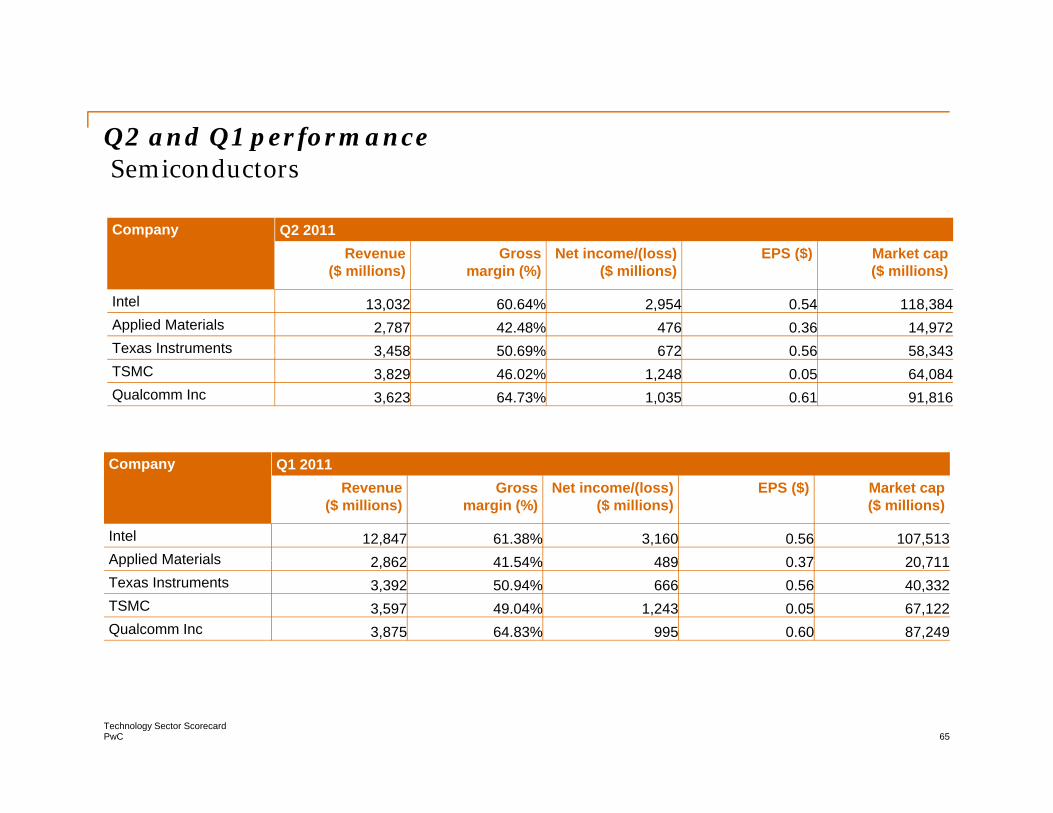

Q2 and Q1 performanceQ Q p fSemiconductors

Company Q2 2011Revenue Gross Net income/(loss) EPS ($) Market capRevenue

($ millions)Gross

margin (%)Net income/(loss)

($ millions)EPS ($) Market cap

($ millions)

Intel 13,032 60.64% 2,954 0.54 118,384Applied Materials 2,787 42.48% 476 0.36 14,972Texas Instruments 3,458 50.69% 672 0.56 58,3433,458 50.69% 672 0.56 58,343TSMC 3,829 46.02% 1,248 0.05 64,084Qualcomm Inc 3,623 64.73% 1,035 0.61 91,816

Company Q1 2011Revenue

($ millions)Gross

margin (%)Net income/(loss)

($ millions)EPS ($) Market cap

($ millions)

Intel 12,847 61.38% 3,160 0.56 107,513Applied Materials 2 862 41 54% 489 0 37 20 711Applied Materials 2,862 41.54% 489 0.37 20,711Texas Instruments 3,392 50.94% 666 0.56 40,332TSMC 3,597 49.04% 1,243 0.05 67,122Qualcomm Inc 3,875 64.83% 995 0.60 87,249

PwCTechnology Sector Scorecard

65

Quarterly results of operations analysis (Q4) Q y f p y QSemiconductorsRevenue and gross margin trends were as follows:

Revenues (in $ millions) – Semiconductors Gross margin % – Semiconductors

100%16 000

40%

60%

80%

100%

4 0006,0008,000

10,00012,00014,00016,000

0%

20%

Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011Intel Applied MaterialsTexas Instruments TSMCQ l

02,0004,000

Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011

Intel Applied MaterialsTexas Instruments TSMC