thai oil public company limited · thai oil public company limited ... thaioil power (tp) 3-on-1...

TRANSCRIPT

Thai Oil Public Company Limited

Presentation to Investors

“PTT Corporate Day”arranged by Deutsche Bank

23-24 January 2006

2CONFIDENTIAL – NOT FOR DISTRIBUTION, NOT AN OFFER OF SECURITIES

Disclaimer:

The information contained in this presentation is intended solely for your personal reference only. Please do not circulate this material. If you are not an intended recipient, you must not read, disclose, copy, retain, distribute or take any action in reliance upon it.

3

Content

I) Highlights

II) Business & Operations Update

III) Consolidated Financial Results

IV) Investment Projects

V) Conclusion

4

I) Highlights

5

9%55%

Thaioil GroupThaioil Group

Thaioil Power Thaioil Power (TP)(TP)

3-on-1 Combined cycleElectricity 118 MWSteam 168 T/hr

Independent Independent Power (Thailand) Power (Thailand)

(IPT)(IPT)PTT 20%

Thaioil 24%

2-on-1 Gas-fired,Combined cycleElectricity 700 MWRelated Business &

Income Stability

Thai Paraxylene Thai Paraxylene (TPX)(TPX)

Thai Lube Base Thai Lube Base (TLB)(TLB)

Capacity: Current: 348 Kt/y (PX)Mid 07: 853 Kt/y total

408 Kt/y (PX)160 Kt/y (Bz)136 Kt/y (To) 149 Kt/y (MX)

Value Enhancement

Capacity: Lube Base oil: 270 Kt/y

Thaioil Marine Thaioil Marine (TM)(TM)

A fleet of 5 oil & petrochemical vessels with int’l classificationsTotal capacity: approx 30,000 DWT

ThapplineThappline

Multi-product Pipeline Capacity: 26,000 mn Litres/Y.

Product Marketing Support

100%

56%

100% 100%

Capacity: Current: 220 KbdMid 07: 270 Kbd

Utility Supply to Group

Thaioil Thaioil (TOP)(TOP)

RefineryRefineryPetrochemPetrochem//

Lube Base Lube Base OIlOIl PowerPower TransportationTransportation

TOP Info:# of shares: 2,040 mnMkt Cap: ~US$ 3.4bn Mkt Cap Ranking: 7

Shareholder structurePTT 49.54%Free float 43.28%Others 7.18%

PTT 26% JPOWER 19%

Core Refining Operations 5

6

(Bt Mn) 9M/05 9M/04 +/- 9M/04 FY04

1. Sales Rev. 182,030 130,317 +40% 184,801

2. EBITDA 24,201 18,364 +32% 25,494

3. Profit Bef. Tax 16,633 11,063 +50% 18,040

4.Tax (3,157) (1,014) +211% (2,967)

5. Net Profit 13,476 10,049 +34% 15,073

6. EPS (Bht/share) 6.61 5.29 +25% 7.82

Financial Highlights

7

1%

Significant Increased Contributions from SubsidiariesSignificant Increased Contributions from Subsidiaries

+40%Sales RevenueSales Revenue

+34%

99%Net ProfitNet Profit

Remark: % is based on total amount

Before deducting inter-company transaction.

Refinery

Power 4% Transportation

95%

9M’04

Refinery

Power 1%

9M’05

* acquired 100% in Oct’04 Transportation

68%

27%

1%

Refinery

TransportationPetrochem/Lube Base*

81%

15%Refinery

Power 4%

Power 4%

Bt. 182 Bt. 182 bnbn..

Bt. 13 Bt. 13 bnbn..

Bt. 130 Bt. 130 bnbn..

Bt. 10 Bt. 10 bnbn..

Petrochem/Lube Base*

0%

8

II) Business & Operations Update

9

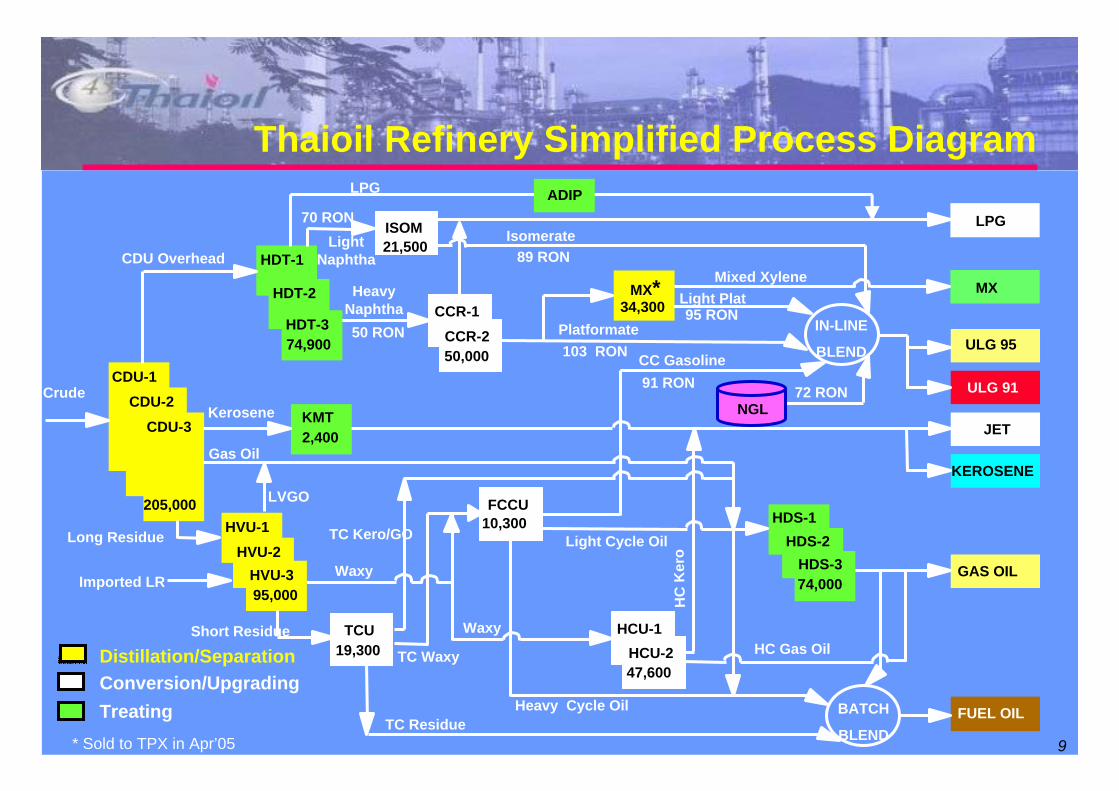

CDU-1CDU-2

CDU-3

TCU19,300

HCU-1

FCCU10,300

CCR-1

HDT-1

KMT2,400

HDS-1

LPG

ULG 95

JET

KEROSENE

GAS OIL

ULG 91

HCU-247,600

CCR-250,000

HVU-1HVU-2

HVU-395,000

HDT-2

HDT-374,900

205,000

FUEL OIL

HDS-2HDS-374,000

MXMX*34,300

Thaioil Refinery Simplified Process Diagram

Crude

Distillation/SeparationConversion/UpgradingTreating

Long Residue

LVGO

Gas Oil

Kerosene

CDU Overhead

Short Residue

TC Residue

TC Waxy

Heavy Cycle Oil

HC Gas Oil

HeavyNaphtha

Platformate

LPG

Light Plat

Light Cycle Oil

HC

Ker

o

Waxy

CC Gasoline

ADIP

Isomerate

NGL72 RON

Mixed Xylene

50 RON

70 RONISOM21,500

Waxy

IN-LINE

BLEND

BATCH

BLEND

LightNaphtha

Imported LR

TC Kero/GO

95 RON

103 RON

89 RON

91 RON

* Sold to TPX in Apr’05 9

10

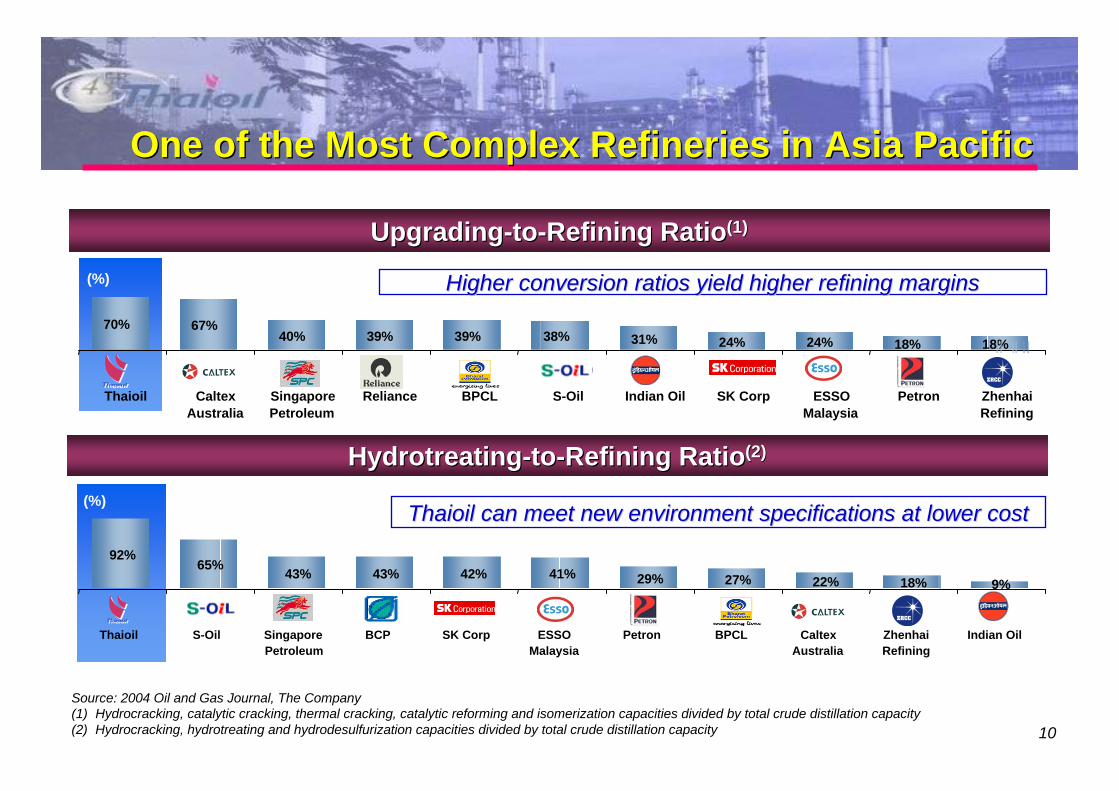

70% 67%40% 39% 39% 38% 31% 24% 24% 18% 18%

Thaioil CaltexAustralia

SingaporePetroleum

Reliance BPCL S-Oil Indian Oil SK Corp ESSOMalaysia

Petron ZhenhaiRefining

One of the Most Complex Refineries in Asia PacificOne of the Most Complex Refineries in Asia Pacific

(%)

Thaioil can meet new environment specifications at lower costThaioil can meet new environment specifications at lower cost

UpgradingUpgrading--toto--Refining RatioRefining Ratio(1)(1)

Source: 2004 Oil and Gas Journal, The Company(1) Hydrocracking, catalytic cracking, thermal cracking, catalytic reforming and isomerization capacities divided by total crude distillation capacity(2) Hydrocracking, hydrotreating and hydrodesulfurization capacities divided by total crude distillation capacity

HydrotreatingHydrotreating--toto--Refining RatioRefining Ratio(2)(2)

(%)

Higher conversion ratios yield higher refining marginsHigher conversion ratios yield higher refining margins(%)

92%65% 43% 43% 42% 41% 29% 27% 22% 18% 9%

Thaioil S-Oil SingaporePetroleum

BCP SK Corp ESSOMalaysia

Petron BPCL CaltexAustralia

ZhenhaiRefining

Indian Oil

11

Operating Cost Index

AnnualizedMaintenance

Costs

Maintenance Effort(Based on Headcounts)

Avg. Personnel Cost

Shell Personnel Index (Based on Headcounts)

CEL

Corrected Energy Loss

Utilization

OperationalAvailability

2003 2004

One of the Best Performing Refineries in the WorldShell Worldwide Annual Benchmarking

High maintenance effort and Personnel Index is offset by

low labor costs.

11

12

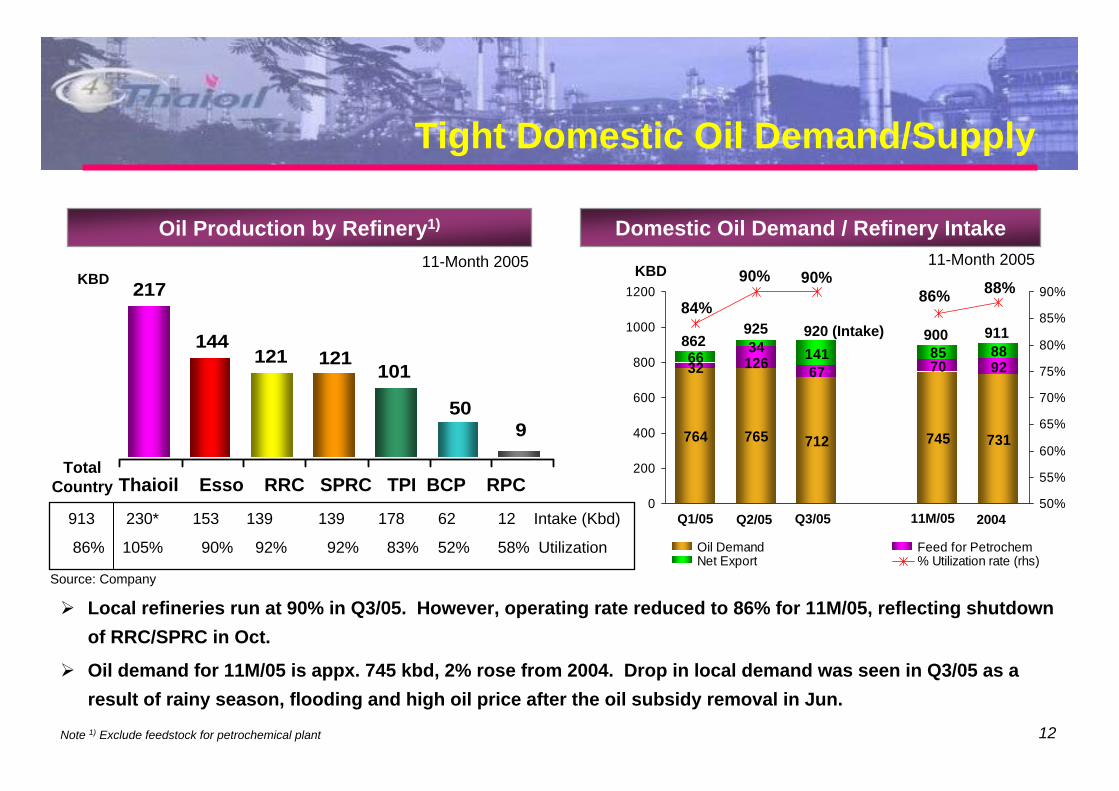

913 230* 153 139 139 178 62 12 Intake (Kbd)

86% 105% 90% 92% 92% 83% 52% 58% Utilization

950

101121121

144

217KBD

Oil Production by Refinery1)

Local refineries run at 90% in Q3/05. However, operating rate reduced to 86% for 11M/05, reflecting shutdown of RRC/SPRC in Oct.

Oil demand for 11M/05 is appx. 745 kbd, 2% rose from 2004. Drop in local demand was seen in Q3/05 as a result of rainy season, flooding and high oil price after the oil subsidy removal in Jun.

Note 1) Exclude feedstock for petrochemical plant

Tight Domestic Oil Demand/Supply

Domestic Oil Demand / Refinery Intake

Thaioil Esso RRC SPRC TPI BCP RPC

Source: Company

764 765 712 745 731

67 70 92141 85 88

32 1266634

86%90%

84%88%90%

0

200

400

600

800

1000

1200

50%

55%

60%

65%

70%

75%

80%

85%

90%

Oil Demand Feed for PetrochemNet Export % Utilization rate (rhs)

KBD

Q1/05 Q2/05 Q3/05 200411M/05

862 900925 920 (Intake) 911

11-Month 2005 11-Month 2005

TotalCountry

13

30

40

50

60

J200

4 M M J S N

J'05 M M J S N

With multiple cracking and treating facilities, Thaioil has flexibility to select most economical crude capitalizing on the favorable sweet and sour differential to optimize refinery operation. 2005 Average Oil Prices

Upto 80% of crude from Middle East (whose prices are more attractive than Far East sweet grade) are normally processed.

LR purchased from BCP during the first 9 months was about 9 kbd on average.

Thaioil could process higher Far East and local crude due to better quality when price differential between M/E-F/E became narrow (i.e. in Q3/05).

Middle distillate was produced to meet local demand (represents about 50% of Country's demand).

Refinery Intake and Production

ThaioilThaioil’’ss Crude Mix and Product YieldCrude Mix and Product Yield

US$/bblTapis

Dubai

8.588.58

TPTP--DBDB

40.3140.3164.0364.0362.1062.1057.9057.9049.3249.32

Fuel OilFuel OilDieselDieselULG 95ULG 95TapisTapisDubaiDubai

80% 75%

6%6%

14% 19%

16%

53%56%

56%

38%28%

9% 11%

33%

ThaioilThaioil’’ss Crude Mix and Product YieldCrude Mix and Product Yield

Middle East

Far East

Heavy

Light

Distillate

Middle

2005

Others

2004

Crude Mix Product Yield Domestic Demand

11M05

14

BCP 4%

TPX 11%

Shell/Caltex,14%

PTT, 49%

Export, 14%

OtherIndependent

domestic,15%

39

49

59

69

79

Jul'0

4 A S O N D

J'05 F M A M J J A S

Refinery Customers BreakdownRefinery Customers Breakdown

FY 05

Including 7% export of PTT

Appx 49% of products was sold to PTT at the market prices. (Domestic 42% and Export 7%).

About 14% of products was sold to Shell and Caltex (Marketing). While Sales to other customers was 15%.

Although the export in Q3/05 increased due to rainy season and slow domestic demand growth, overall export for 2005 was only 14% (compared with country export of 17%).

When export, Thaioil switched to produce more Jet fuel at the expense of diesel due to its more favorable price.

Jet

Diesel

US$/bbl

15

20

30

40

50

60

70

80

Jan' 0

4 M M J S NJa

n' 05 M M J S N

Oil Prices Movement and GRMOil Prices Movement

Strong demand and tight supply supported high oil prices during the first 9M.

Hurricanes in US and slow recoveries of US refineries fueled gasoline, diesel and other oil prices in Q3.

Delayed and warmer winter in The States, coupled with high stock pile post Katrina weakened prices in Q4/05.

Dipped in Thaioil’s GRM in Q2/05 was due to softening product price in May (high US inventory).

GRM in Q3/05 rebounded as a result of Katrina.

Regional GRM was pressured In Q4/04, due to warmer weather, stock up in US, prompt high VLCC freight as well as lackluster demand from high oil price (after subsidy reduction/removal in certain countries).

Thaioil’s GRM (incl. MX)

* Transfer MX to TPX as from April 1 2005* Transfer MX to TPX as from April 1 2005

US$/bbl

Diesel

Gasoline

Tapis

OmanFuel Oil

US$/bbl

0

2

4

6

8

10

Q1/05 Q2/05 Q3/05 FY/04 9M05

8.756.55+1

8.52+1

7.50

7.9+0.7

16

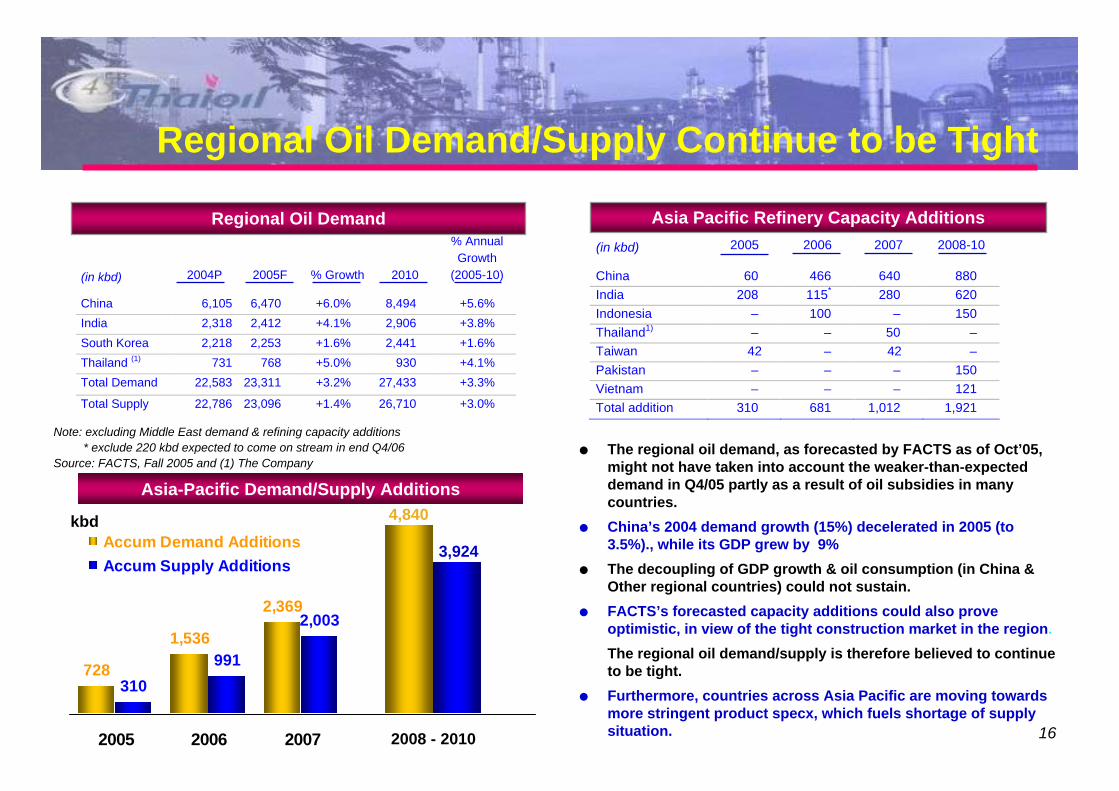

(in kbd) 2005 2006 2007 2008-10

China 60 466 640 880 India 208 115* 280 620 Indonesia – 100 – 150 Thailand1) – – 50 – Taiwan 42 – 42 – Pakistan – – – 150 Vietnam – – – 121 Total addition 310 681 1,012 1,921

(in kbd) 2004P 2005F % Growth 2010

% Annual Growth

(2005-10)

China 6,105 6,470 +6.0% 8,494 +5.6% India 2,318 2,412 +4.1% 2,906 +3.8% South Korea 2,218 2,253 +1.6% 2,441 +1.6% Thailand (1) 731 768 +5.0% 930 +4.1% Total Demand 22,583 23,311 +3.2% 27,433 +3.3%

Total Supply 22,786 23,096 +1.4% 26,710 +3.0%

Regional Oil Demand/Supply Continue to be Tight

Note: excluding Middle East demand & refining capacity additions* exclude 220 kbd expected to come on stream in end Q4/06

Source: FACTS, Fall 2005 and (1) The Company

Asia Pacific Refinery Capacity AdditionsRegional Oil Demand

Asia-Pacific Demand/Supply Additions

728

1,536

2,369

310991

2,003

2005 2006 2007

kbdAccum Demand AdditionsAccum Supply Additions

4,840

3,924

2008 - 2010

The regional oil demand, as forecasted by FACTS as of Oct’05, might not have taken into account the weaker-than-expected demand in Q4/05 partly as a result of oil subsidies in many countries.China’s 2004 demand growth (15%) decelerated in 2005 (to 3.5%)., while its GDP grew by 9%The decoupling of GDP growth & oil consumption (in China & Other regional countries) could not sustain.FACTS’s forecasted capacity additions could also prove optimistic, in view of the tight construction market in the region.The regional oil demand/supply is therefore believed to continueto be tight.Furthermore, countries across Asia Pacific are moving towards more stringent product specx, which fuels shortage of supply situation.

kbd

17

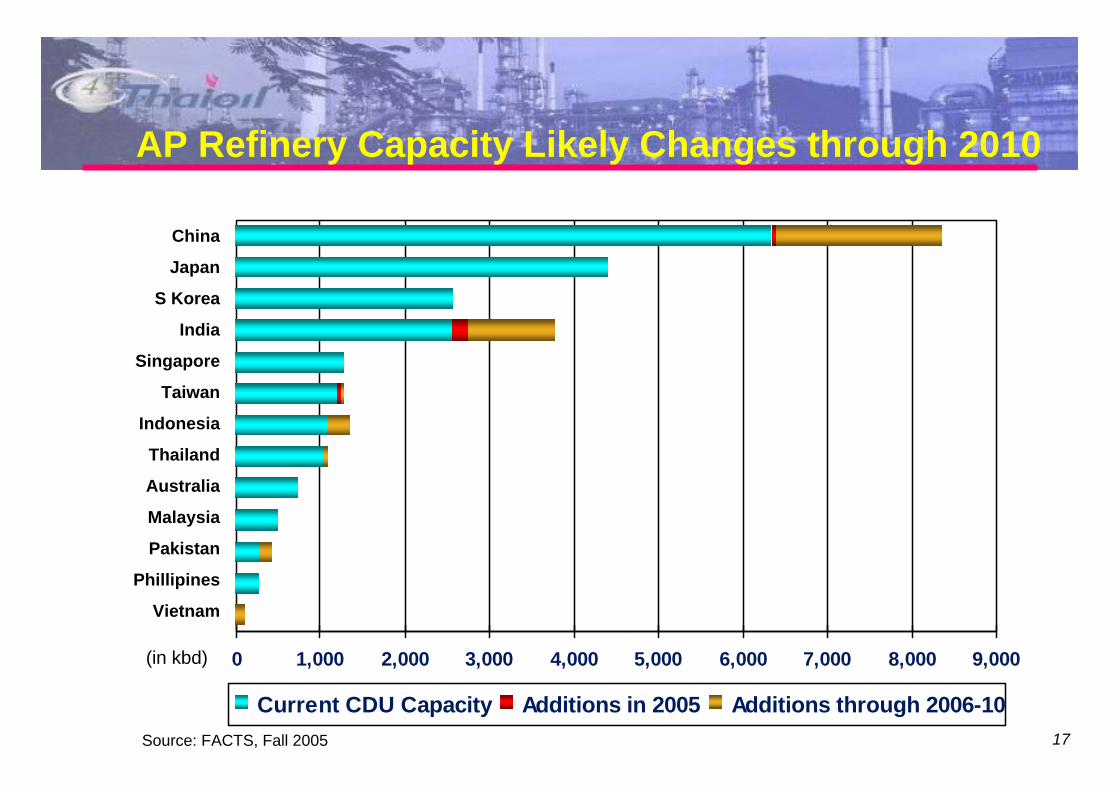

AP Refinery Capacity Likely Changes through 2010

0 1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000 9,000

Current CDU Capacity Additions in 2005 Additions through 2006-10

China

Japan

S Korea

India

Singapore

Taiwan

Indonesia

Thailand

Australia

Malaysia

Pakistan

Phillipines

Vietnam

(in kbd)

Source: FACTS, Fall 2005 17

18

TPX’s Business

Jan04 M M J S N

Jan' 0

5 M M J S NPlat

PX, MX and Platformate Spot Prices

PX

MX

US$/Ton

* Transfer MX to TPX as from April 1 2005

PX-PlatPX-MX

BackgroundAfter years of liquidity and profitability problems, TOP acquired 100% shares in Oct’04.In Jan’05, TPX invested US$ 5 M. to change catalyst and effectively increase PX output to 348 KTA (a 21% increase).In Apr’05, transfer MX unit was transfer to TPX.

2004 9M05Gross Margin (US$ M.) 20 80(Equivalent to $/bbl) 0.25 1.00

Net Profit (Baht M.) 115 2,371

PX Market

Other

S.E.Asia

N.E.Asia

Europe

North America

Utilization (rhs)Capacity (rhs)

South America

Source Company

World Production by Region

1,000

800

600

400

200

0

A utilization rate of more than 80% would trigger investment in new capacity. Regional PX demand grows at 6%, outpacing the supply growth of 2%, mainly driven by China.Thailand PX market 2005 2006

Demand - Tuntex 295 362- SMPC 714 965- Indorama -0- 429

Supply - ATC 495 455- Exxon 445 485- TPX 340 340

Surplus / (Deficit)

1,009

1,280

1,756

1,387

271 (476)

19

TLB’s Business

Background

Strong lube base oil price is supported by growing regional demand, tight supply (after closures of plants in Asia) and strong diesel price.

Lube base - HSFO spread widened from 280 US$/Ton in 2004 and 380 US$/ton in 2005.

9M/05 saw a 83% (full capacity utilization of lube base production unit). Net profit has gone up by 186%, as compared to 2004, to 1,352 Baht M.

Prior to TOP acquisition, TLB had experienced financial problems as a result of Baht devaluation and depressed lube base oil market.In Oct 04, TOP acquired 100% shares of TLB and fully integrated it with the refinery.TOP has commissioned a team to study and has identified 15 synergy projects with the refinery.TLB LT debt was reduced to zero.

Higher MPU’s Utilization / Profitability

Lube Base Market

Jan/04 M M J S N

Jan'0

5 M M J S N

US$/Ton

HSFO

500SN

20370 331

1,4351,352

-422

83%70%

60%

-500

0

500

1000

1500

2000

2003 2004 9M05-20%-10%0%10%20%30%40%50%60%70%80%90%

EBITDA Net Profit % MPU Utilization (Lube Production Unit)

Baht M.

Lube Base - HSFO800

600

400

200

0

% Utilization

20

IPT BusinessIPT Business

Plant Availability Improved Financial Performance

IPP IndustryBackground• Established in 1995 as a JV of TOP, Westinghouse and

Unocal. • During first IPP bidding in 1995, IPT won the mandate to

build the power plant to EGAT as the first ranked bid proposal among 32 bidders.

• IPT experienced technical problems with Westinghouse GTs which were later replaced with Siemens GTs in 2003 and 2005, respectively, at Siemens and Insurance expenses.

• With the new 2 GTs, IPT declared full availability of 700 MW as from Jun’05.

• Steady revenue nature, as PPA allow IPP to pass through variable cost to EGAT. IPP will get availability payment (AP) which covers fixed cost, debt service and return.

• Thailand electricity demand grows inline with GDP. Therefore EGAT plan to announce new round IPP in end 2006 / H107.

• TOP is ready for the 2nd IPP bidding (700-1400 MW),

(Baht M.) 9M/05 9M/04 +/(-)

• EBITDA 1,099 577 522

• Profit bef. FX/Extra Exp. 613 (200) 813

• FX/Extra. Expense (444) (269) (175)

• Net Profit 169 (469) 638

77%70%78%

57%48%

41%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000 2001 2002 2003 2004 2005

700 MW from Jun’05

* In year 2001, IPT report net profit of 813 Baht M.

21

III) Consolidated Financial Results

22

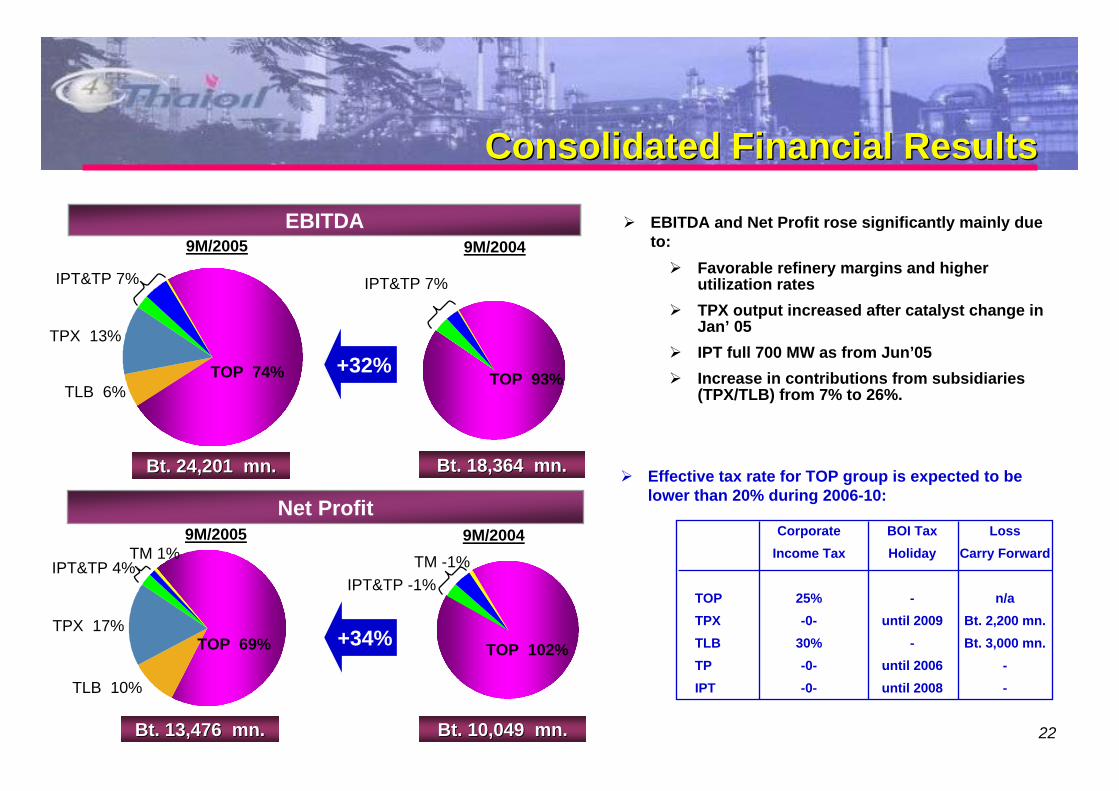

Consolidated Financial ResultsConsolidated Financial Results

EBITDA

TOP 74%TLB 6%

TPX 13%

IPT&TP 7%

EBITDA

TOP 69%

TLB 10%

TPX 17%

IPT&TP 4%

Net Profit

TM 1%

TOP 93%

IPT&TP 7%

TOP 102%

IPT&TP -1%TM -1%

Bt. 24,201 Bt. 24,201 mnmn.. Bt. 18,364 Bt. 18,364 mnmn..

Bt. 13,476 Bt. 13,476 mnmn.. Bt. 10,049 Bt. 10,049 mnmn..

9M/2005 9M/2004

9M/2005 9M/2004

EBITDA and Net Profit rose significantly mainly due to:

Favorable refinery margins and higher utilization ratesTPX output increased after catalyst change in Jan’ 05 IPT full 700 MW as from Jun’05 Increase in contributions from subsidiaries (TPX/TLB) from 7% to 26%.

Effective tax rate for TOP group is expected to be lower than 20% during 2006-10:

Corporate BOI Tax LossIncome Tax Holiday Carry Forward

TOP 25% - n/aTPX -0- until 2009 Bt. 2,200 mn.TLB 30% - Bt. 3,000 mn.TP -0- until 2006 -IPT -0- until 2008 -

+32%

+34%

23

Financial Strength

Balance Sheet

2,486

2,957

Dec ’02 Dec ’04

Current Assets

Fixed Assets

OtherLiabilities

TotalEquities

US$ mn 2,816

Sep ’05

2,462

Dec ’03

Long-term Debts

1,564 1,279

982 874

Note: Convert by 41 Baht/US$

Since 2002,- Total Assets: up ~Bt 20 bn (+20%)- Total Debt: down ~Bt 28 bn (-44%)- Total Equities: up ~Bt 26 bn (+70%)

Key Financial Ratios

3.04.8

11.2

15.06.5

2.2

1.4 0.7 0.6

3.5

1.31.0

0.01.02.03.04.05.06.07.0

2002 2003 2004 20050.02.04.06.08.010.012.014.016.0

ICR LT Debt/Equity Debt/EBITDA

Interest Coverage

LT Debt / Equity

Net Debt/EBITDA

24

Group Debt Structure

Dividend policy is at least 25% of net profit after legal reserve. (pay at Bt1.80/share in May’05 (3.27% dividend yield or 13.09% annualized).

Dividend Policy

Consolidated Repayment ProfileConsolidated Repayment Profile10-Year Bullet Bond US$ 350 M. @ coupon 5.1%. (Moody’s Baa1 / S&P’s BBB)

5-Year revolving US$ Loan: US$ 200 M.

6-Year syndicated onshore loan (US$ 65 M. + THB 2,600 M.)

Consolidated Long Term Debt Profile

• Total LT Loan is 83% in USD to match with USD-linked revenue.

• Total fixed interest is appx. 50% of total borrowing.

• Average cost of debt is appx. 6% p.a. (before corporate tax)

TOP 72%

($629M)

TLB & TM 0%

IPT 18% ($156M)

TP 3% ($27M)

TPX 7% ($62M)

112

324 377

59

0

100

200

300

400

1 Yr 2-4 Yr 5-7 Yr 8-10 Yr

US$ M.

25

IV) Investment Projects

26

Updated CAPEX Requirements

US$ Mn 2005 F 2006 F 2007 F Total In 2005-07

CDU-3 Debottlenecking1) 54 110 54 218

Mercury Removal Units 6 2 0 8

SBM Expansion 20 75 55 150

Power Projects2) 11 21 11 43

Maintenance Projects 15 15 15 45

TPX (Expansion) 10 50 55 115

TLB (Synergy Project) 5 5 0 10

Thaioil Marine 6 6 0 12

Total 127 284 190 601

US$ Mn

27

US$ Mn Total In 2005-07

CDU-3 Debottlenecking 218

Mercury Removal Units 8

SBM Expansion 150

Power Projects 43

Maintenance Projects 45

TPX (Expansion) 115

TLB (Synergy Projects) 10

Thaioil Marine 12

Total 601

Updated CAPEX Requirements

Size: 50 kbd (additional 23%)EPC: ABB PMC: Foster WheelerInvestment Cost: US$ 4,000 /bblExpected C.O.D : Mid 2007IRR: ~ 20% based on 4.5 US$/bbl GRM

Size: 52”diameter * 14.5 km long pipelineEPC: SAIPEM PMC: Bechtel Expected C.O.D : Mid 2007Benefit: Freight saving

Size: 500,000 T/Yr (additional)Cost: US$ 115 M. est. Expected C.O.D : Mid 2007Benefit: Margin base on aromatics (BTX) over

ULG95 and able to supply oil product

For example, TLB/TOP Hot Oil ExchangeCost: US$ 3 mnBenefit: Enhance CDU-1 feed by 5 kbdExpected C.O.D : Mid 2006

28

0

0.5

1

1.5

2

2.5

3

3.5

2011 2012 2013 2014 2015

'000 MW

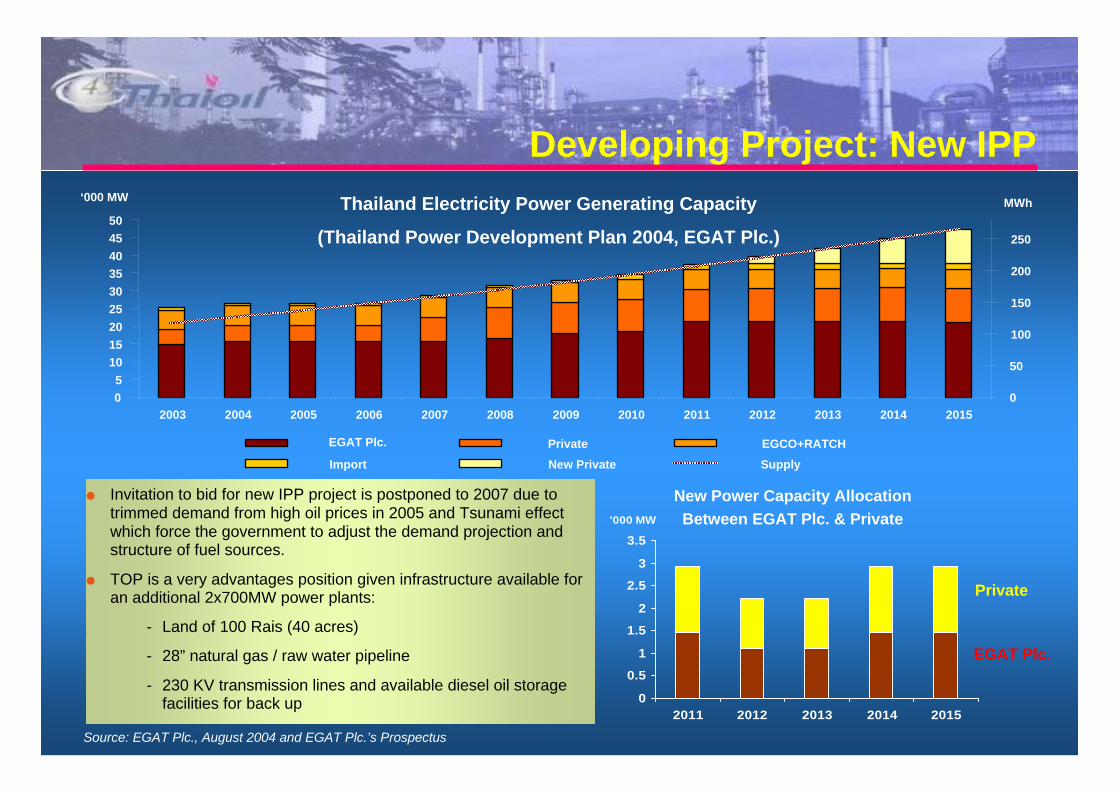

Developing Project: New IPP

Invitation to bid for new IPP project is postponed to 2007 due to trimmed demand from high oil prices in 2005 and Tsunami effect which force the government to adjust the demand projection and structure of fuel sources.

TOP is a very advantages position given infrastructure available for an additional 2x700MW power plants:

- Land of 100 Rais (40 acres)

- 28” natural gas / raw water pipeline

- 230 KV transmission lines and available diesel oil storage facilities for back up

Thailand Electricity Power Generating Capacity

(Thailand Power Development Plan 2004, EGAT Plc.)

Source: EGAT Plc., August 2004 and EGAT Plc.’s Prospectus

New Power Capacity AllocationBetween EGAT Plc. & Private

EGAT Plc.

Private

05

101520253035404550

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

‘000 MW

0

50

100

150

200

250

MWh

EGAT Plc. Private EGCO+RATCHImport New Private Supply

29

V) Conclusion

30

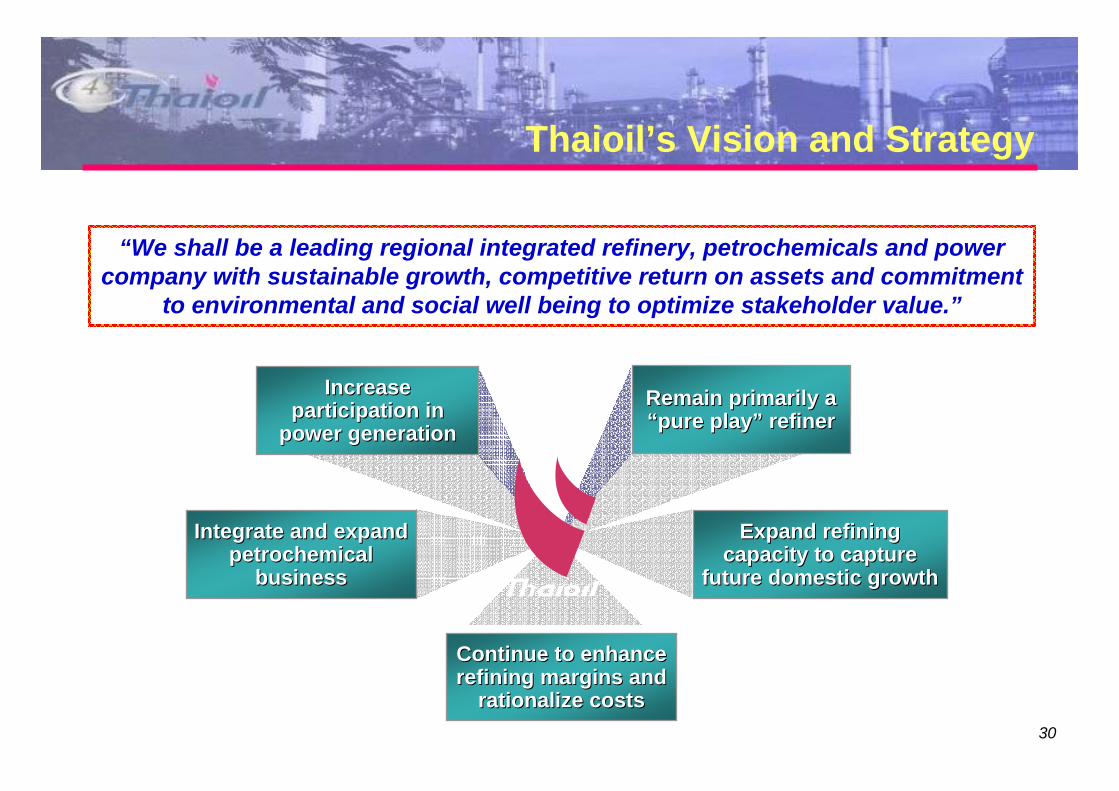

Thaioil’s Vision and Strategy

Remain primarily a Remain primarily a ““pure playpure play”” refinerrefiner

Increase Increase participation in participation in

power generationpower generation

Expand refining Expand refining capacity to capture capacity to capture

future domestic growthfuture domestic growth

Integrate and expand Integrate and expand petrochemical petrochemical

businessbusiness

Continue to enhance Continue to enhance refining margins and refining margins and

rationalize costsrationalize costs

“We shall be a leading regional integrated refinery, petrochemicals and power company with sustainable growth, competitive return on assets and commitment

to environmental and social well being to optimize stakeholder value.”

31

Conclusion

One of the most complex, cost-efficientand modern refinery in the region;

Favorable oil & petrochemical industries - inability of supply to keep up with continuously growing demand;

Investment strengths: High barrier to entry due to investment cost, limited new supplied, prospect demand and captive market.

Significant increased contributions from subsidiaries, as a result of business restructuring & synergy within the group;

Strong financial position post-completion of the refinancing exercise;

Effective project development enhances investment returns & ensures growth;

One of the most complex, cost-efficientand modern refinery in the region;

Favorable oil & petrochemical industries - inability of supply to keep up with continuously growing demand;

Investment strengths: High barrier to entry due to investment cost, limited new supplied, prospect demand and captive market.

Significant increased contributions from subsidiaries, as a result of business restructuring & synergy within the group;

Strong financial position post-completion of the refinancing exercise;

Effective project development enhances investment returns & ensures growth;

2004

Best Equity Deal, Best IPO, BestPrivatization and Best Thailand Deal for the Year 2004

Best Deal of the Year for IPO inThailand in 2004

Thai Capital Market Deal in 2004

Asia’s Best Equity Deal in 2004

Best IPO Deals in 2004

Best Newly Listed Companyof the Year 2004

2005

Best Newly Listed Company in Asia

Most Improved Companies in Asia

32

THANK YOU

Any further questions, please contact Investor Relations Dept. Tel: (662) 299-0124Fax: (662) 617-8295

email: [email protected]: www.thaioil.co.th

33

Appendix

34

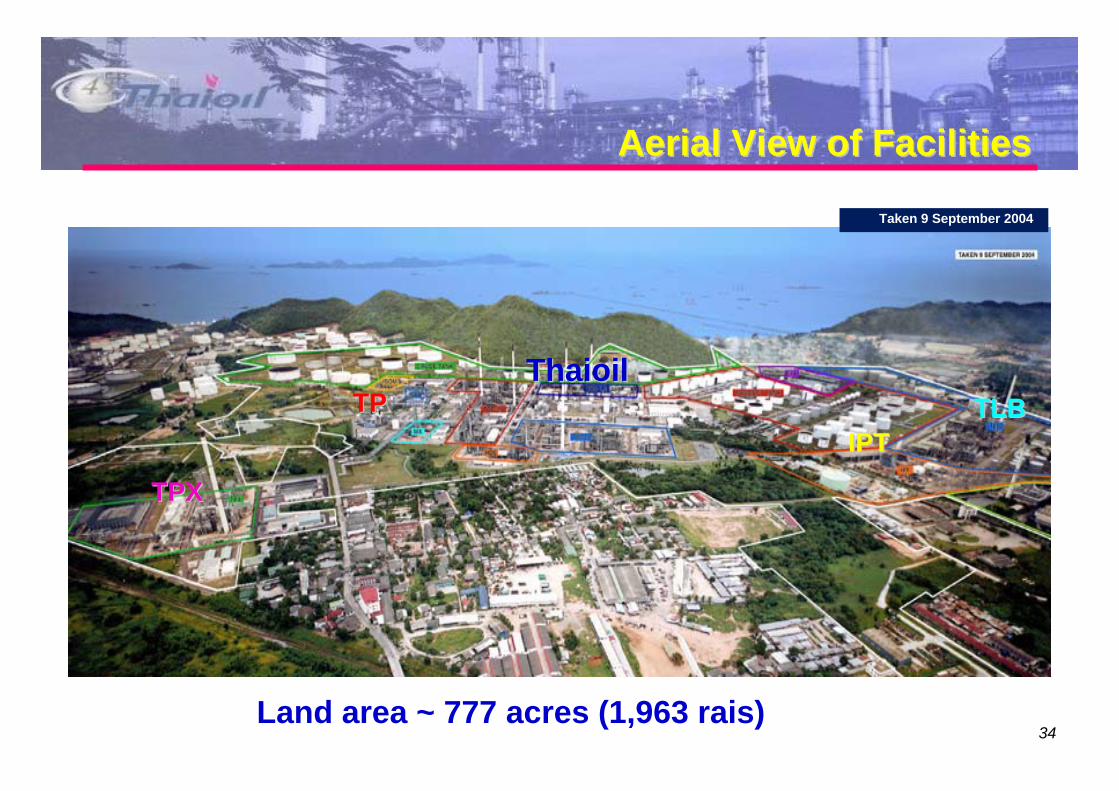

Aerial View of FacilitiesAerial View of FacilitiesAerial View of Facilities

Land area ~ 777 acres (1,963 rais)

TPXTPX

IPTIPTTLBTLBTPTP

Taken 9 September 2004

ThaioilThaioil

35

Strategic LocationStrategic LocationStrategic Location

The site is in the Eastern region, 124 km from BangkokHas 2 mooring facilities for crude receiving and product exportClose to market by connecting to multi-product pipelineHas space available for future expansion

Source: Ministry of Energy 2003

9%

10%

59%11%

11%

SARABURI

LUMLUKKADONMUANG

SUVARNABHUMI

Esso

GULF OF THAILAND

Shell (RRC)Caltex (SPRC)

MAP TA PHUT

SRIRACHA

Ø24”, 134 km

Ø18”, 38 km

Ø10”, 29 km

Ø18”, 92 km

Main Line Expansion Pipeline

SBM Facility

Domestic demand

distribution THAIOIL

Bangchak

TPI

SBM

36

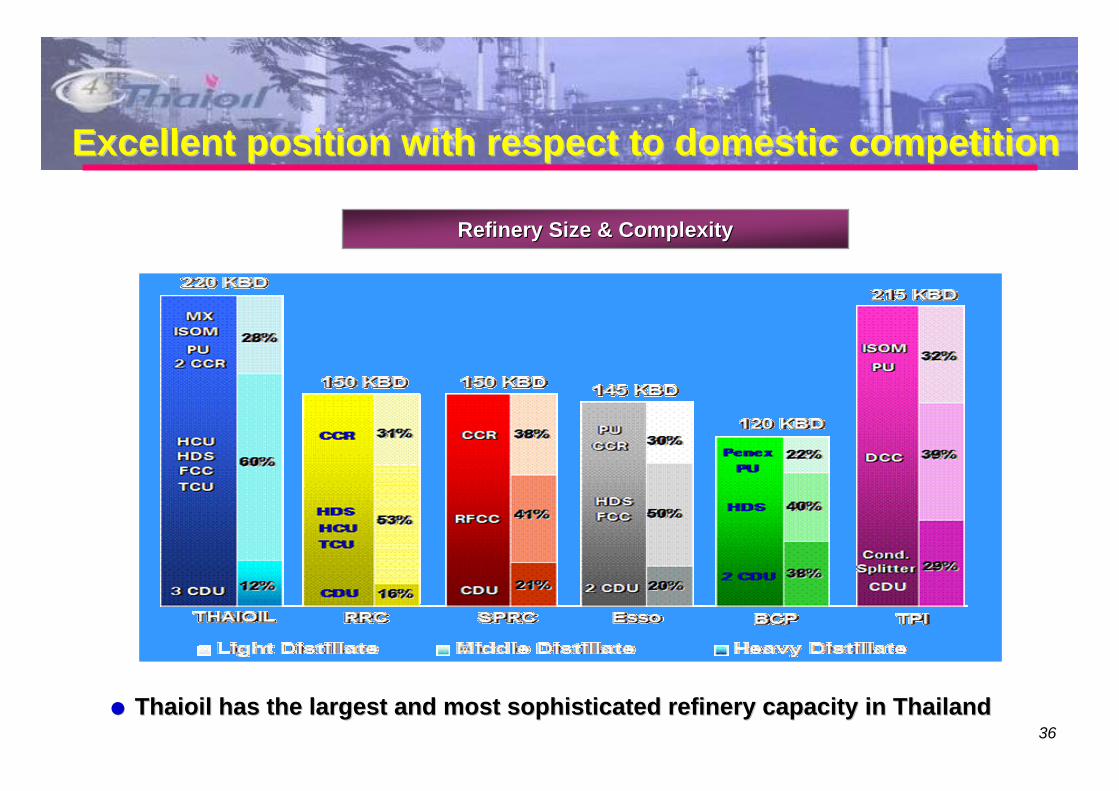

Excellent position with respect to domestic competitionExcellent position with respect to domestic competitionExcellent position with respect to domestic competition

Refinery Size & ComplexityRefinery Size & Complexity

Thaioil has the largest and most sophisticated refinery capacityThaioil has the largest and most sophisticated refinery capacity in Thailandin Thailand

37

16% 14% 19% 19%34%

56%57% 41%

47% 47%

47%

28%45%

34% 34%18%

11%10%

75%

14%33%

ThaiDemand

Thaioil Esso RRC SPRC TPI Bangchak

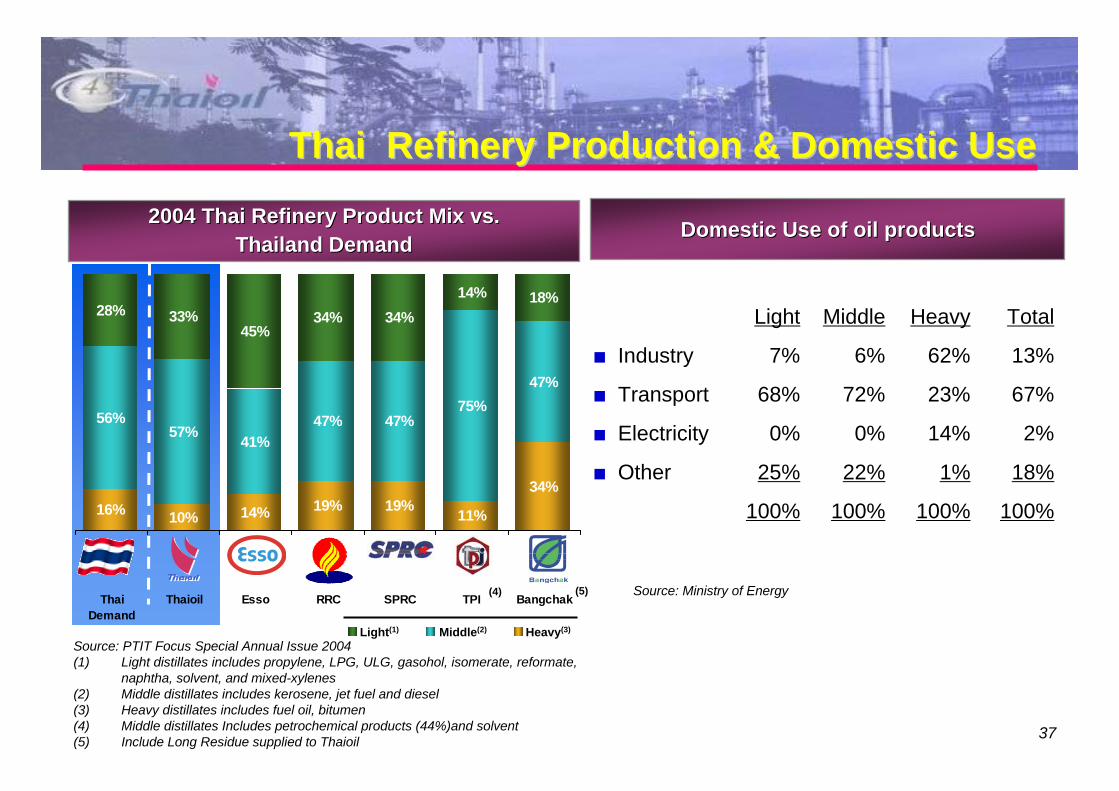

Thai Refinery Production & Domestic UseThai Refinery Production & Domestic UseThai Refinery Production & Domestic Use

2004 Thai Refinery Product Mix vs.2004 Thai Refinery Product Mix vs.Thailand DemandThailand Demand

Source: PTIT Focus Special Annual Issue 2004(1) Light distillates includes propylene, LPG, ULG, gasohol, isomerate, reformate,

naphtha, solvent, and mixed-xylenes(2) Middle distillates includes kerosene, jet fuel and diesel(3) Heavy distillates includes fuel oil, bitumen(4) Middle distillates Includes petrochemical products (44%)and solvent (5) Include Long Residue supplied to Thaioil

Middle(2) Heavy(3)Light(1)

(4) (5)

Light Middle Heavy Total

Industry 7% 6% 62% 13%

Transport 68% 72% 23% 67%

Electricity 0% 0% 14% 2%

Other 25% 22% 1% 18%

100% 100% 100% 100%

Source: Ministry of Energy

Domestic Use of oil productsDomestic Use of oil products

38

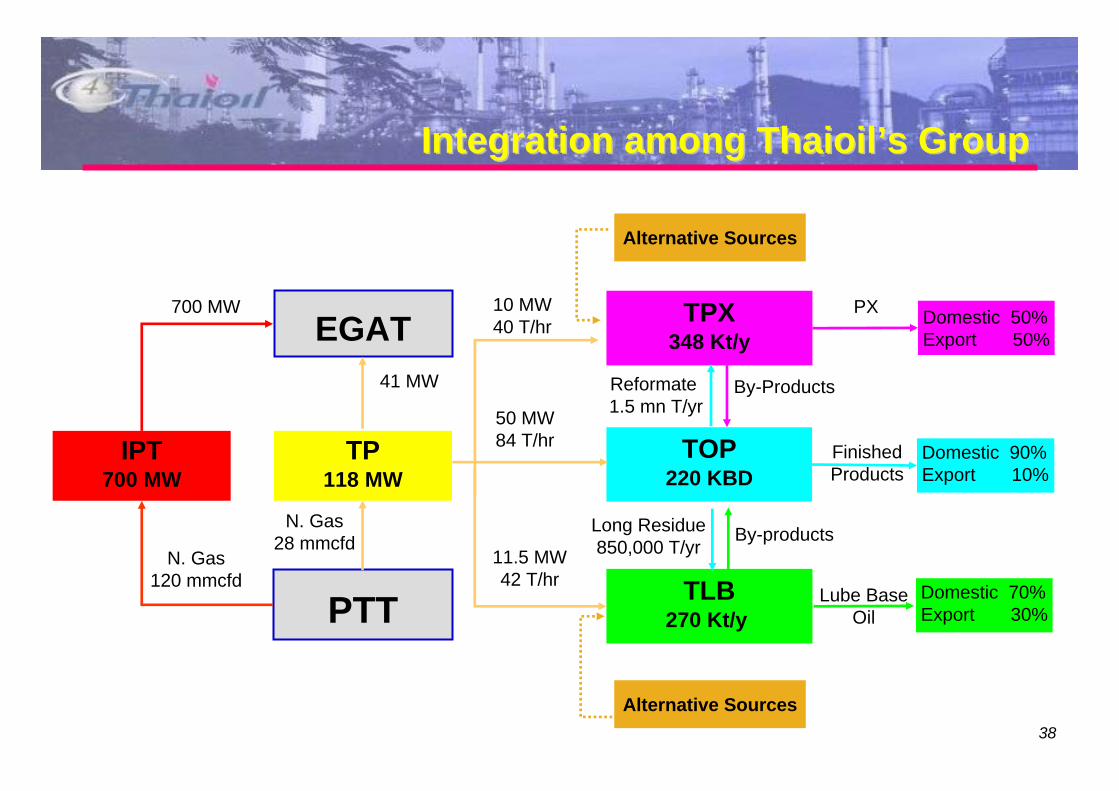

PTT

TOP220 KBD

EGAT

IPT700 MW

TPX348 Kt/y

TLB270 Kt/y

Integration among Thaioil’s GroupInIntetegrationgration amongamong ThaioilThaioil’’ss GroupGroup

Alternative Sources

Alternative Sources

Long Residue 850,000 T/yr

By-products

TP118 MW

N. Gas28 mmcfd

N. Gas120 mmcfd

Reformate1.5 mn T/yr

By-Products

Domestic 90%Export 10%

Domestic 70%Export 30%

Lube Base Oil

41 MW

50 MW84 T/hr

10 MW40 T/hr

11.5 MW42 T/hr

Domestic 50%Export 50%

700 MW

Finished Products

PX

39

Rationales

Ethanol ProjectBackground

• Government plans to phase out MTBE by 2007 and use Ethanol as high octane component instead for environmental concern/import reduction/agricultural support.

• There is insufficient domestic ethanol supply as only 3 licensees (from 24 licensees) is currently in operation for 300,000 L/Day.

• Abundant feedstock as Thailand exports Tapioca chips more than 3 mn Tons/Yr (1 mnL/Day of Ethanol requires about 0.9 mn Ton/Yr of Tapioca Chips).

New Developing Project: Ethanol

• Ethanol Plant Capacity 1 – 2 Mn L/Day

• Feedstocks: Tapioca Chips 1 – 2 Mn T/Yr

• Estimated Investment Cost 150 – 250 Mn USD

• Site Location under consideration

Economy of Scale

• Government promotion• Supply of raw material is abundant because Thailand is largest exporter• Raw material price and availability is less volatile, compared with Molasses• Low cost produces due to economy of scale