the 11th annual needham & company growth...

TRANSCRIPT

1

The 11th Annual Needham & Company

GROWTH CONFERENCE January 6, 2009

Jim Green, President & CEO

Analogic Corporation

2

Any statements in this presentation about future expectations, plans, and prospects for the Company, including

statements containing the words “believes,” “anticipates,” “plans,” “expects,” and similar expressions, constitute forward-

looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Actual results may differ

materially from those indicated by such forward-looking statements as a result of various important factors, including risks

relating to product development and commercialization, limited demand for the Company’s products, risks associated

with competition, uncertainties associated with regulatory agency approvals, competitive pricing pressures, downturns in

the economy, the risk of potential intellectual property litigation, and other factors discussed in our most recent quarterly

report filed with the Securities and Exchange Commission. In addition, the forward-looking statements included in this

presentation represent the Company’s views as of January 6, 2009. While the Company anticipates that subsequent

events and developments will cause the Company’s views to change, the Company specifically disclaims any obligation

to update these forward-looking statements. These forward-looking statements should not be relied upon as representing

the Company’s views as of any date subsequent to January 6, 2009.

Safe Harbor Statement

3

This presentation includes non-GAAP financial measures that are not in accordance with, nor an alternative to, generally

accepted accounting principles and may be different from non-GAAP measures used by other companies. In addition,

these non-GAAP measures are not based on any comprehensive set of accounting rules or principles.

Management uses non-GAAP gross margin, non-GAAP operating expenses, non-GAAP other (income) expense, non-

GAAP income before tax, non-GAAP net income and non-GAAP diluted earnings per share to evaluate the Company's

operating performance against past periods and to budget and allocate resources in future periods. These non-GAAP

measures also assist management in understanding and evaluating the underlying baseline operating results and trends

in the Company’s business. The items excluded from the non-GAAP measures were excluded because they are either

non-recurring, non-operating or are of a non-cash nature, which we do not consider when evaluating and managing our

business operations.

Non-GAAP financial measures should not be considered as a substitute for, or superior to, measures of financial

performance prepared in accordance with GAAP. They are limited in value because they exclude charges that have

a material effect on our reported results and, therefore, should not be relied upon as the sole financial measures to

evaluate our financial results. The non-GAAP financial measures are meant to supplement, and to be viewed in

conjunction with, GAAP financial measures. A reconciliation of GAAP to Non-GAAP financial measures can be

found on our website at www.analogic.com.

Use of Non-GAAPFinancial Measures

Global PresenceMore than 35 years of innovation in signal and image processing

4

Canton, MA

Gradient amplifiers for MRI and

precision motion control systems

Copenhagen, Denmark

Specialized Ultrasound scanners

for Urology and Surgery

Montreal, Canada

Direct Digital Selenium flat

panel x-ray detectors for

mammography

State College, PA

Leading developer of Ultrasound probes

and transducers for medical OEMs

Peabody, MA

Worldwide Headquarters

Engineering and manufacturing of medical

imaging subsystems and aviation security

Shanghai, China

Serving the needs of our

customers in China

5

At a Glance

$-

$50

$100

$150

$200

$250

$300

$350

$400

$450

2005 2006 2007 2008

Reven

ue (

Millio

n)

$(10.0)

$(5.0)

$-

$5.0

$10.0

$15.0

$20.0

$25.0

$30.0

Inc

om

e (

Lo

ss

) fr

om

Op

s (

Mil

lio

n)

WW Revenues Income (Loss) from Ops

Analogic (NASDAQ: ALOG)

Peabody, MA. USA

Founded 1967

FY2008 Year End Results• Consolidated revenue of $413.5M• Income from Operations* of $24.3M• GAAP EPS of $1.77• Cash and Equivalents of $186.4M• No Debt

* Excludes non-operating other (income) expense and income taxes

Pioneer in Analog to Digital Conversion for Medical Imaging

6

Revenue and Non-GAAP EPS

FY2005 - FY2008

$-

$50

$100

$150

$200

$250

$300

$350

$400

$450

2005 2006 2007 2008

Reven

ues (

Millio

n)

$-

$0.50

$1.00

$1.50

$2.00

$2.50

No

n-G

AA

P E

PS

Revenues Non-GAAP EPS

• Analogic has demonstrated consistent improvement in Non-GAAP EPS

assisted by Copley acquisition late in FY 2008

• Q1 FY 2009 Revenues and EPS declined as orders for CT systems

used in radiation treatment as well as CT subsystems were delayed

partly as a result of the global financial crisis.

Q1 FY 2008 - Q1 FY 2009

$50

$60

$70

$80

$90

$100

$110

$120

$130

Q1 FY08 Q2 FY08 Q3 FY08 Q4 FY08 Q1 FY09

Re

ve

nu

es

(M

illi

on

s)

$-

$0.10

$0.20

$0.30

$0.40

$0.50

$0.60

$0.70

No

n-G

AA

P E

PS

Revenue Non-GAAP EPS

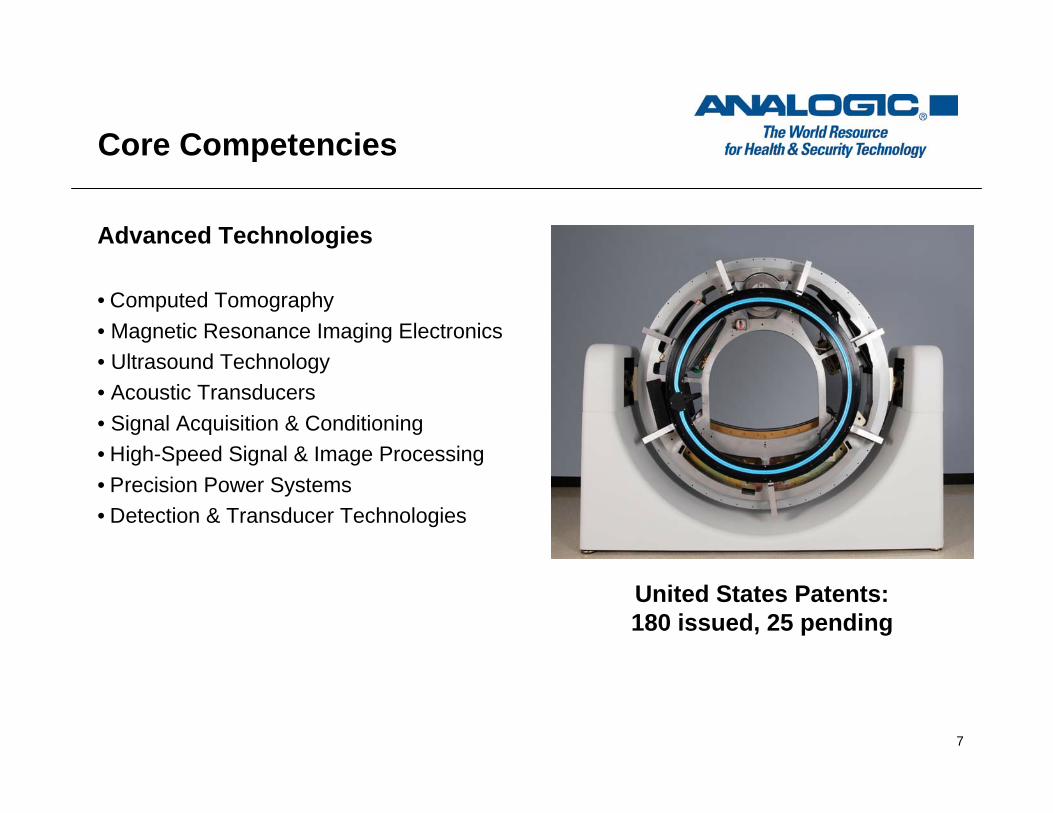

Core Competencies

7

• Computed Tomography

• Magnetic Resonance Imaging Electronics

• Ultrasound Technology

• Acoustic Transducers

• Signal Acquisition & Conditioning

• High-Speed Signal & Image Processing

• Precision Power Systems

• Detection & Transducer Technologies

United States Patents:180 issued, 25 pending

Advanced Technologies

8

Revenue by Segments

Medical Technology – 85%

Security Technology, 12%

Medical Imaging, 56%

Digital Radiography, 7%

BK Medical, 22%

Other, 3%

9

Aging Population Drives Demand

0

500

1000

1500

2000

2500

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

2020

2025

2030

2035

2040

2045

2050

Wo

rld

Po

pu

lati

on

Ov

er

65

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Pe

rce

nta

ge

of

Wo

rld

Po

pu

lati

on

60+

Percent of World

Source: Espicom 2008

10

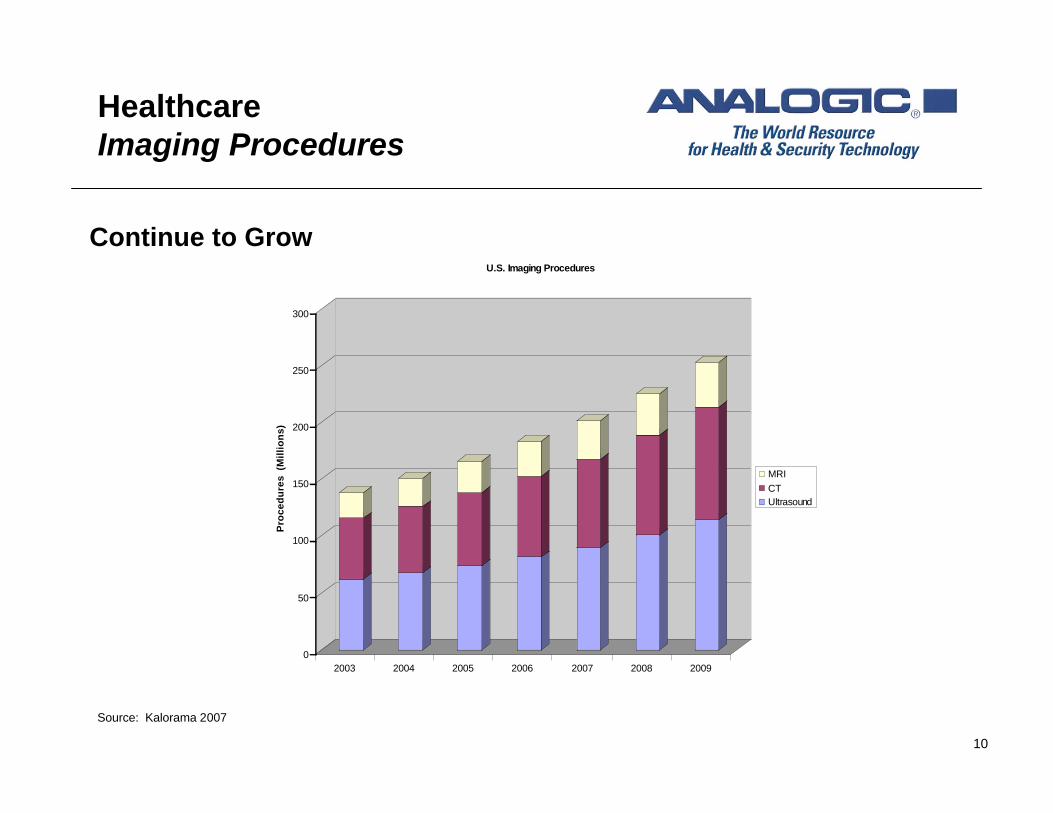

0

50

100

150

200

250

300

Pro

ce

du

res

(M

illi

on

s)

2003 2004 2005 2006 2007 2008 2009

U.S. Imaging Procedures

MRI

CT

Ultrasound

Source: Kalorama 2007

HealthcareImaging Procedures

Continue to Grow

11

HealthcareMedical Technology Applications

• Magnetic Resonance Power Systems

- RF Amplifiers

- Gradient Amplifiers

• Computed Tomography

- Data Acquisition and Data Management

Systems

- PowerLink™ Non-contact Power System

• Digital Mammography Detectors

• Clinical Ultrasound Scanners & Transducers

• Radiation Treatment

- CT Guided Gantry Systems

Leading OEM Supplier Subsystems for:

12

HealthcareDigital Mammography Detectors

Analogic’s Proprietary AmorphousSelenium Technology

Digital Mammography Market ~ $600M (10+% CAGR)*

Leading Customers:

• Siemens’ “MAMMOMAT Inspiration”

• Philips’ “MammoDiagnost DR”

• Toshiba’s “Peruru”

• Early adopters: IMS & Planmed

*InMedica 2007

13

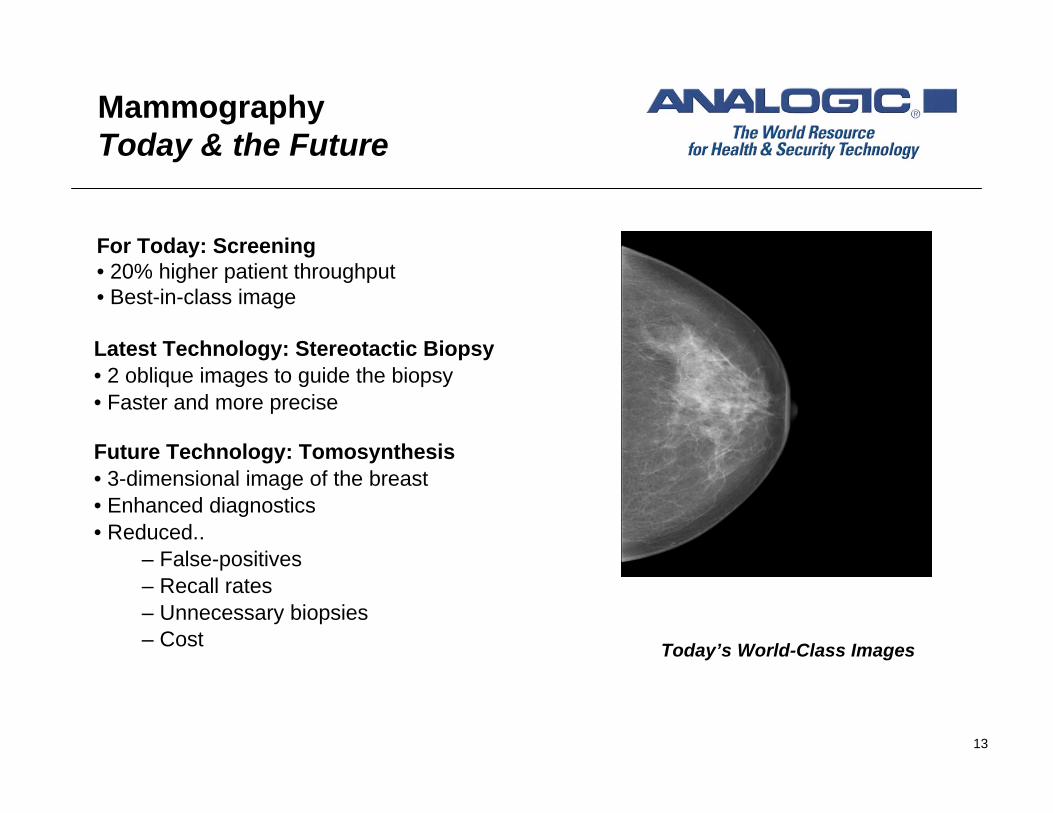

MammographyToday & the Future

Today’s World-Class Images

Latest Technology: Stereotactic Biopsy

• 2 oblique images to guide the biopsy

• Faster and more precise

Future Technology: Tomosynthesis

• 3-dimensional image of the breast

• Enhanced diagnostics

• Reduced..

– False-positives

– Recall rates

– Unnecessary biopsies

– Cost

For Today: Screening• 20% higher patient throughput

• Best-in-class image

14

MammographyToday & the Future

Tomosynthesis Image

Latest Technology: Stereotactic Biopsy

• 2 oblique images to guide the biopsy

• Faster and more precise

Future Technology: Tomosynthesis

• 3-dimensional image of the breast

• Enhanced diagnostics

• Reduced..

– False-positives

– Recall rates

– Unnecessary biopsies

– Cost

For Today: Screening• 20% higher patient throughput

• Best-in-class image

15

HealthcareUltrasound

BK MedicalNew Product Family Introductions:

• Pro Focus UltraView Scanner launched at RSNA last month

• Flex Focus Scanner to launch next quarter

World market leader in:

• Colorectal Ultrasound

• Surgical Ultrasound, including Brachytherapy

New market opportunities:

– Pelvic Floor

– Interventional Radiology

– Highly mobile acute care

16

Aviation SecurityAdvanced 3-D Imaging Technology

2D Projection Displays

Interactive, 3D Threat Display

Interactive, 3D Display

17

Aviation Security Systems

eXaminer™ XLB - Ultra-high throughput next

generation EDS

- In certification testing, Fall 09 shipments

- Up to 1100 bags per hour

New eXaminer™ SX - Multi use

applications in small to mid size airports

-Completed certification testing

- Up to 360 bags per hour

EXACT™ AN6000 - First and only

CT based, full volumetric scanner

-850 units installed worldwide

-550 bags per hour

18

Growth Drivers

17

Medical Imaging Business

• The Copley acquisition strengthens our business while expanding new

customer opportunities in MR

• Our Selenium based direct digital mammography plates will drive growth

as our customers penetrate new markets

• New multi-slice CT data management systems to launch this summer

expected to grow share

End User B-K Ultrasound

• Hospital sales of surgical ultrasound products are poised to grow with the introduction

of the new generation UltraView™ and Flex Focus™ product families

Security

• Growth opportunities in checked baggage driven by expanded product offering

of the eXaminer SX into the mid-tier airports and the upcoming ultra-high speed

eXaminer XLB for large airports

19

Summary

• The global financial credit crisis impacted our Q1 results

• We’re accelerating efforts to optimize our operating cost structure

• Our cash and balance sheet remain strong

• New product platforms in Medical and Security position us for share growth

• Our considerable technological strength, the continuing growth of medical

imaging procedures, and the opportunities for new baggage screening systems

position Analogic for both the short and long term

20

Thank You

21