the 1997 election: can an improving economy secure a fifth tory term?

TRANSCRIPT

The 1997 election: can animprovin g econom y secure afifth Tor y term

Introduction

At the time of writing, the Conservative government entersthe final stages of the parliamentary term with an opinion polldeficit unprecedentedly large for this point of the campaign.In a Gallup poll reported at the end of last year (DailyTelegraph, 5th December), the Labour lead was apparently solarge (59% to the Tories’ 22%), that if those results held in ageneral election, then the models translating polls into seatspredict the Tories would have only 45 MPs. Admittedly, thisis just about the highest gap recorded recently, and in anyevent, such opinion polls should be interpreted with care. It isclear from the polling debacle at the 1992 election that some-thing is awry with the standard opinion poll methodology.One post-mortem was held with pollsters and academics at aconference at Essex University in the aftermath. The conclu-sion was mixed. Yes, methodology needed adjusting, and thepollsters were picking samples that were excessively downmarket; but there was also a genuine last-minute swing to theTories which the final polls did pick up. Since then pollstershave indeed changed their methodology and generally publish‘adjusted’ polls which take account of the apparent tendencyfor Tory voters to understate their support, whereas the figuresjust quoted are unadjusted.

Recently, Gallup has changed its methods in line with theother major organisations and the Labour lead fell; but thelatest lead recorded (in late January) is still a hefty 18 points.Labour at about 51% to the Tories on 33%. The Tory night-mare is the Canadian election of 1993 where the ruling Pro-gressive Conservatives were reduced to only two seats (in one

of which the member subsequently defected to the ReformParty). This is an extreme scenario. The current unadjustedaverage of the polls - the ‘poll of polls’ - is around 28% forthe Conservatives, or 31% adjusted, which would leave theConservatives with about 150 seats (out of a Commons totalof 651).

But the fascinating question from the viewpoint of aneconomic commentator is quite why government popularityis so low when the economic news, on the whole, has been sogood. Inflation (while still above the European average) is ata historically low level; unemployment, still continuing tofall, is the lowest of any major European country (althougheven the government admits the recent figures are distortedby the recent changes to the benefit rules); economic growthis widely forecast to be at least 3% in 1997 ; and interest rates,while still above the European average, are again down tolevels last seen in the 1960s. On the other hand, it is true,despite the evidence that job tenures are generally as long nowas they ever were (see Peter Robinson’s article in the Novem-ber 1996 Economic Outlook), that there is a feeling of eco-nomic insecurity around. In a Gallup survey in December1994 (Daily Telegraph, 12th December 1994) no less than91% of respondents considered that there was ‘a lot of inse-curity ... at the moment’; and 61% admitted that they felt‘insecure’ in relation to their ‘jobs, earnings or homes’. In-come distribution has also widened enormously over the pastdecade-and-a-half (although the latest figures reveal a slightnarrowing). But the main weight of the objective evidence onthe economy points to a solidly successful economic perform-ance in the recent past. And there is a mountain of econometricevidence from democracies all over the world that economic

The current government is in deep electoral trouble. Nothing is certain in politics,but it still seems very likely the Tories will be defeated by New Labour this spring.Yet the economy is in fine shape - inflation and interest rates are at historically lowlevels, economic growth is proceeding at a respectable rate, and unemploymentcontinues to fall. Why won’t the electorate reward the government? In this articleSimon Price argues that the Tories lost their reputation for economic competence in1992 and this has swayed the public’s opinion.

Simon Price is a Professor of Economics at City Univer-sity School of Social Sciences.

Economic Outlook

February 1997 12

conditions matter. In Clinton’s famous phrase, coined duringthe 1992 US Presidential election, ‘It’s the economy, stupid’.

Economic influences on governmentpopularity

The current author and Professor David Sanders of EssexUniversity have themselves added a small pile to this moun-tain. We examined the relationship between governmentpopularity and economic variables, over a very long (40 year)period up to 1989 (Price and Sanders (1995)). It is part of theconventional wisdom that this kind of relationship is veryunstable, but we found the opposite. As one would expect,extraordinary political factors matter a great deal. For in-stance, the three day week cost Edward Heath’s government20% of its popularity; the Falklands war boosted MrsThatcher’s by no less than 30%. The Brighton bombing of theGovernment cabinet at the party conference perpetrated in1984 also led to a boost in support, contrary, no doubt, to theIRA’s intentions. And the - substantial - unexplained variationin the data must conceal a plethora of political factors wecannot put a precise label on. But economic factors also count.Government popularity is boosted by low interest rates, lowinflation and falling unemployment. Interestingly, the level ofunemployment turns out to have no impact on popularity,which helps to explain how government popularity was main-tained at respectable levels through most of the high unem-ployment years of the 1980s. This relationship is very stable.It works as well for the 1980s - after the Thatcher revolution- as it does for the 1960s.

Given this evidence, it seems that on the face of it thegovernment has got the economic situation exactly right! Thecomplicated dynamics of the process make it hard to say whatthe equation should now be predicting, six years after it wasestimated. However, we can easily work out what the steady-state prediction is (the long-run value after the dynamics havesettled down). Even if we ignore the beneficial effect of fallingunemployment which will boost support, the predicted long-run level of popularity (given the current inflation rate andinterest rate of roughly 3% and 6% respectively) is about37.5%. The actual figure, as we just saw, is nearer 30%. Thisis all the more puzzling in the light of another key indicatorthat political forecasters have found useful in the past, the‘feelgood factor’, nearly always referred to as ‘elusive’ overthe past three years. This variable is thought to be measuredby the difference between those reporting their financial situ-ation will improve and those thinking it will worsen, assurveyed in the regular Gallup poll. It is no longer elusive, andis now firmly back in the black. A recent Gallup survey(Sunday Telegraph, 4th January 1997) puts it at a high 11%,a dramatic rise since the last quarter, when it hovered aroundzero. House prices, often thought to be related to the subjec-tive well-being of home-owners, are also on the rise; the

Halifax house price index is now rising at around 8% perannum and there is a widespread belief that the housingmarket is on the move again.

So what did the Tories do wrong? The answer seems to bethat the Government has lost its traditional reputation forcompetent economic management, always the Tories’ trumpcard. Since 1992, this has been blown away. Voters nowappear not to credit the government with the evident economicsuccess of the UK. The causes of this disillusionment are tobe found in the period after the 1992 election, when taxes roseand Britain left the ERM. The government’s reputation foreconomic competence took a crushing blow; and it is possibleto argue that, after these events, it became much more difficultto rescue a poor political situation with a tax-slashing pre-election budget than it had been in the period prior to the 1992election.

Policy, politics and business cycles

The situation described above highlights the fact that therelationship between the state of the economy and electoralsupport is a good deal more complex than the naive ‘politicalbusiness cycle’ view suggests.

In fact, there has been a profound shift since the early1970s in thinking about the limits of government power withregard to macroeconomic management and the electoral cy-cle. In 1975, the view associated with William Nordhaus - thatgovernments cynically manipulate the economy to increasetheir chances of re-election - was the conventional wisdom.But by the early 1980s, this consensus had been entirelyoverturned. After the rational expectations ‘revolution’,which captured the macroeconomic profession in the mid1970s, it was simply not thinkable that governments could actin this calculating way without the electorate realising whatthe game was, and the political business cycle was consideredto be a dead duck. But belief in this simple view of the waygovernments manipulate the economy persists in populardebate. For example, Victor Keegan wrote recently that ‘wehave become quite accustomed to an‘‘official’’ boom beforean election’ (The Guardian, 18th March 1996, p.13). Econo-mists are more skeptical - recalling the impossibility of therebeing dollar bills on the sidewalk that no-one had picked up.Economic research has yielded a more measured view ofelectoral cycles and the possible irresponsibility of policymakers: there is something going on out there, but it ishappening rather intermittently and weakly. For example,Alberto Alesina, who was the pioneering researcher in thisarea, concludes (Alesina and Perotti (1995), p 235);

"The theory suggests that electoral budget cycles(i.e. loose policies in election years) should beobserved only occasionally and should not be verylarge."

Economic Outlook

13 February 1997

The authors are able to back this up with evidence from anumber of countries.

Recent experience in the UK and US supports this assess-ment. After all, if Keegan (quoted above) is correct, why wasKenneth Clarke’s November budget, for all the headline talkof a penny off the income tax, so fiscally prudent? And whywas taxation never an issue in the 1996 US Presidentialcampaign, despite Dole’s best efforts to introduce it? Both ofthe major Presidential candidates promised tax cuts, but Presi-dent Clinton, the incumbent, offered a largely cosmetic pack-age that was fiscally responsible and left the budgetary ad-vances his administration achieved intact. One plausible ex-planation is that Clinton, unlike Major, was comfortablyahead of his opponent in the polls and had very little incentiveto massage opinion with imprudent tax cuts that would createproblems in his next term. The explanation of Clarke’s for-bearance is somewhat different, and lies in the fact thatexpansionary fiscal policy had been tried before, in 1992. Thepolicy (spend more, tax less, and pick up the deficit tab afterthe election) worked then; but Clarke and Major were onlytoo aware they could not use the same powder twice. The issueis one of reputation, or credibility.

The importance of credibility

These ideas stem from a hugely influential paper publishedby Finn Kydland and Edward Prescott in 1977, on the ‘timeinconsistency’ of optimal plans, including macroeconomicpolicy. The key idea that emerges is the credibility of policy.The insight is that although the government might sincerelypromise to do something - e.g. achieve lower inflation - beforethe election, things might look very different afterwards, whenbygones are bygones and the election victory is in the bag.This has very general applications across a whole range ofpolicies, from patent law to the optimal structure of govern-ment debt. The tools of the trade come from game theory. Inan ‘inflation game’, the private sector forms expectations ofinflation based on what policy is expected to be before thepolicy is actually implemented. So when the governmentactually does finalise the policy - say, set the money supplyor the PSBR - those expectations are already fixed and peopleare locked into existing wage and other contracts. The gov-ernment is now free to renege on its promises - and it will oftenhave a strong incentive to do so.

Because people can see this coming, low inflation prom-ises are simply unbelievable - or not credible, to use thejargon. In ‘non-cooperative’ policy games of this type lowinflation becomes hard to achieve. If it were possible for thegovernment to somehow credibly ‘precommit’ itself to lowinflation, the game would become cooperative and every onewould become better off; but it is hard to devise such means.A large part of the macroeconomic policy debate over the pastdecade has been an attempt to find these credible commitmentdevices. For instance, many believe that the most significant

argument in favour of EMU is not the avoidance of currencytransactions costs; it is the anti-inflation credibility it delivers(at least in countries with a poor inflation record, such as theUK). The same is true of the ERM (when it was working), orthe fashionable notion of central bank independence. The ideahere is that if the opportunity to affect inflation is removedfrom the government, for example by giving control overmonetary policy to an independent Bank, or a EuropeanCentral Bank, then the whole problem of credibility is neatlyside-stepped.

At the heart of all such policy games is an incentive for thepolicy maker to deviate from the optimal policy (e.g. lowinflation). The most obvious incentive is that created by theelectoral process. A pre-election boost helps the governmentto win power at the expense of more inflation later. So - it isargued - the simple existence of the democratic, electoralsystem tends to induce an inflationary bias. Of course, evenin the absence of institutional fixes, a policy can be credible.It seems pretty clear that Mrs Thatcher developed a strongreputation for being prepared to take unpopular decisions inthe fight against inflation. But such credibility has to beearned. As far as electoral success is concerned, a partypursuing an incredible policy will not be supported (unless thepublic can temporarily be persuaded the policy is, in fact,credible). Thus an intriguing test of the credibility of a gov-ernment’s anti-inflation policy is to look for shifts in popularsupport, after allowing for the effect of past observed eco-nomic variables.

However, though the need to maintain credibility hasreduced the scope for electoral cycles, it has not eliminatedthem altogether. In practice, there is always room for someuncertainty on the part of the public, which, in principle, canallow cyclical effects. For example, Rogoff and Sibert (1988)have suggested a model based on ‘rational opportunism’where there is uncertainty about the competence of the incum-bent government. Nobody can actually observe competence,so it has to be inferred by the electorate, by observing policyoutcomes. This leaves room for parties to show, or ‘signal’,competence by (for example) cutting taxes; all things beingequal, competent governments can cut taxes most. This ap-proach is particularly useful in the attempt to understand thecurrent UK situation. The benefit of signaling is that theincumbent is re-elected. However, there is also a cost to givingthis signal, which is that policy is driven from the “ ideal”point with the possibility that economic problems (e.g. highdeficits or inflation) will emerge in the future.

Depending on the relative costs and benefits, the modelpredicts either separating1 or pooling equilibria, both of whichgenerate pre-election cycles, but with different characteristics.

1 A separating signalling equilibrium results in different behav-iour of competent and incompetent governments, so they can bedistinguished. A pooling equilibrium results in identical behav-iour.

Economic Outlook

February 1997 14

In the latter case, the signal is misleading half the time. Thismakes the model difficult - possibly, impossible - to test. Butwe might expect to observe pre-electoral cycles in inflationand Alberto Alesina and others have indeed found such evi-dence for some countries.

For our purposes, the point of this rational opportunisticapproach is that the perceived competence of the governmentis a crucial variable. Promising tax cuts can provide a signalthat the government is competent - but this strategy carriedrisks. The message we take from the more general politicalbusiness cycle and policy game literature is that competenceand credibility are closely connected. A government judgedcompetent is likely to be judged to have a credible economicpolicy. Thus, from either perspective, a credible governmenthas an electoral advantage.

Tax cuts and the 1992 election

So what does this tell us about the UK and the prospects forthe next election? Why did Clarke not relax the fiscal stance,as Lamont did in the run-up to 1992? Part of the answer liesin the poor fiscal position that the current Chancellor inher-ited. Soon after the last election it became clear that the loosefiscal stance created by the pre-electoral softeners had led toa dramatic deterioration in the public finances. The 1993Budget forecast for the deficit (excluding privatisation re-ceipts) was a massively unstable 9% of GDP for 1993/94. Ifthis level of deficit were sustained, then (assuming the gov-ernment achieved the respectable levels of 3% inflation and2.5% growth) the debt to GDP ratio would have risen fromabout 55% in 1992 to almost 125% by 2010. Consequently,the government just elected on a tax-cutting programme em-barked on the largest peace-time increase in taxes ever, raisingthe tax yield by £17.2bn over two years. Inevitably, thisepisode damaged the government’s credibility, in the sensethat official pronouncement were now greeted with greatscepticism, by markets and voters.

Competence

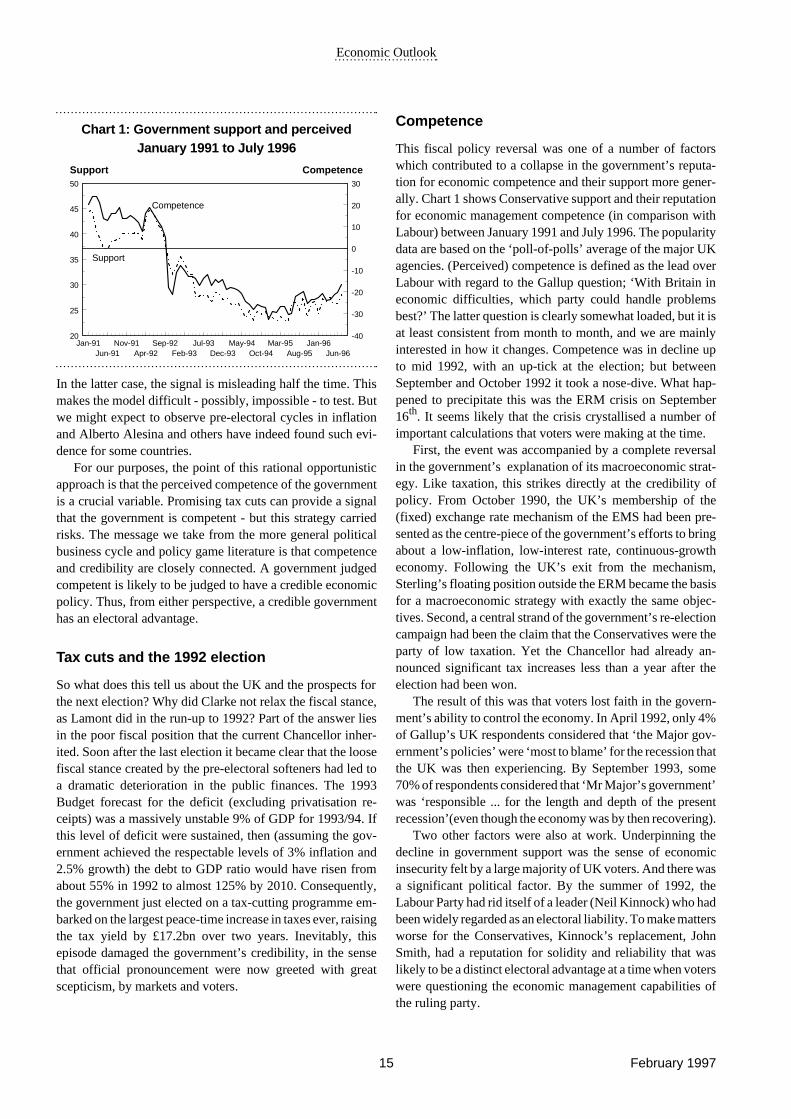

This fiscal policy reversal was one of a number of factorswhich contributed to a collapse in the government’s reputa-tion for economic competence and their support more gener-ally. Chart 1 shows Conservative support and their reputationfor economic management competence (in comparison withLabour) between January 1991 and July 1996. The popularitydata are based on the ‘poll-of-polls’ average of the major UKagencies. (Perceived) competence is defined as the lead overLabour with regard to the Gallup question; ‘With Britain ineconomic difficulties, which party could handle problemsbest?’ The latter question is clearly somewhat loaded, but it isat least consistent from month to month, and we are mainlyinterested in how it changes. Competence was in decline upto mid 1992, with an up-tick at the election; but betweenSeptember and October 1992 it took a nose-dive. What hap-pened to precipitate this was the ERM crisis on September16th. It seems likely that the crisis crystallised a number ofimportant calculations that voters were making at the time.

First, the event was accompanied by a complete reversalin the government’s explanation of its macroeconomic strat-egy. Like taxation, this strikes directly at the credibility ofpolicy. From October 1990, the UK’s membership of the(fixed) exchange rate mechanism of the EMS had been pre-sented as the centre-piece of the government’s efforts to bringabout a low-inflation, low-interest rate, continuous-growtheconomy. Following the UK’s exit from the mechanism,Sterling’s floating position outside the ERM became the basisfor a macroeconomic strategy with exactly the same objec-tives. Second, a central strand of the government’s re-electioncampaign had been the claim that the Conservatives were theparty of low taxation. Yet the Chancellor had already an-nounced significant tax increases less than a year after theelection had been won.

The result of this was that voters lost faith in the govern-ment’s ability to control the economy. In April 1992, only 4%of Gallup’s UK respondents considered that ‘the Major gov-ernment’s policies’ were ‘most to blame’ for the recession thatthe UK was then experiencing. By September 1993, some70% of respondents considered that ‘Mr Major’s government’was ‘responsible ... for the length and depth of the presentrecession’(even though the economy was by then recovering).

Two other factors were also at work. Underpinning thedecline in government support was the sense of economicinsecurity felt by a large majority of UK voters. And there wasa significant political factor. By the summer of 1992, theLabour Party had rid itself of a leader (Neil Kinnock) who hadbeen widely regarded as an electoral liability. To make mattersworse for the Conservatives, Kinnock’s replacement, JohnSmith, had a reputation for solidity and reliability that waslikely to be a distinct electoral advantage at a time when voterswere questioning the economic management capabilities ofthe ruling party.

Competence

Support

Jan-91Jun-91

Nov-91Apr-92

Sep-92Feb-93

Jul-93Dec-93

May-94Oct-94

Mar-95Aug-95

Jan-96Jun-96

20

25

30

35

40

45

50

-40

-30

-20

-10

0

10

20

30

Support Competence

Chart 1: Government support and perceivedJanuary 1991 to July 1996

Economic Outlook

15 February 1997

As Chart 1 shows, the government’s reputation for com-petence and popularity are closely linked. Econometric re-search in Sanders and Price (1997) confirms this. The paperfocusses on two big ‘credibility’ issues - competence andtaxes. Using cointegration techniques on monthly data be-tween 1991 and 1995, we find that competence and tax mattergreatly in determining popularity, as well as special politicalfactors and events. The econometric techniques used alsoenable us to say something about the causality underpinningthis relationship. It could be argued that popular governmentsare seen as competent; popularity causes competence. But wecan safely conclude that is not the case. Governments are notjudged competent because they are popular; but the contraryposition is true. On this interpretation, the best the Chancellorcan do for his party is to restore its reputation for competenteconomic management. So the 1996 Budget can be seen asone step in this long process.

Elections and budgets

But we can dig a little deeper than this by considering thequestion: When is the best time for a government to lose itsreputation? One answer is: when you need it most. The pointis that irresponsible economic policy may win elections ifused infrequently, but has a cost. Two costs, in fact - a loss ofreputation which will come home to roost in the future; and acost in terms of economic disruption (typically higher infla-tion). So a popular government, having little to gain from apre-electoral boom, has little incentive to act like this. On theother hand, less popular governments do. But there is a furthertwist. Extremely unpopular governments cannot gain either -the damage is too large to undo. So they may as well actresponsibly.

These ideas are set out formally in some recent researchreported in Price (1996). The paper sets out a model in whichgovernment would like to do as well as they can with theeconomy - achieve low inflation and so on. But they also wantto remain in office. As Rogoff and Sibert argued, as well as

Victor Keegan and many others, they can increase theirchances of doing so by manipulating the economy. This yieldsa benefit in terms of a higher chance of re-election; the cost isthat to do so, they shift views away from the ideal set ofpolicies. But if the government is sure to be elected, they donot need to incur this cost! Popular parties have less need tomanipulate the economy, and therefore act in a more respon-sible manner. As popularity changes with the natural courseof events, the incentive to generate electoral cycles alsochanges. The somewhat less obvious conclusion of the model,however, is that very unpopular governments should alsopursue responsible economic policies. The reason is that thecost of restoring popularity is very high for unpopular gov-ernments, as it is simply hard to regain a lot of popularity.Thus we might expect there to be an inverted U shape discern-ible between government support and economic policychanges in the run-up to elections.

However, while this is a persuasive argument, it is onlypart of the story. Other effects might pull us in the oppositedirection. For example, party leaders often fail to (politically)survive lost elections. So the prospect of election defeat mayconcentrate the mind wonderfully. The point is that, for theparty leader (acting as the ‘agent’ for the party or electorate),the consequences of defeat far outweigh the cost to the partyor electorate (the ‘principals’) of pursuing the ‘wrong’ eco-nomic policy. This may lead to low popularity levels inducingextreme economic behaviour. Another explanation that mayapply in some cases is that an unpopular government can planto leave a ‘poisoned fiscal chalice’. For example, dislikingpublic expenditure, a right wing government might lowertaxes or raise transfers to increase the deficit and prevent anynew government from increasing spending. This idea wasintroduced by Alesina and Tabellini (1990). In case it seemedtoo fanciful, in an early version of their paper, the authorsquote the New York Times (January 25, 1987), which makesthe point very clearly;

“The deficit is not a despised orphan. It is PresidentReagan’s child, and secretly he loves it, as DavidStockman has explained: the deficit rigorously dis-courages any idea of spending another dime onsocial welfare.”

This story may also tell us something about the UK; seeLockwood, Philippopolous and Snell (1996).

So what can we tell from the past pattern of economicpolicy before UK elections? To test these ideas against theevidence, we look at the behaviour of three policy variablesover ten elections: real transfers (mainly social security pay-ments), interest rates and a measure of the ‘inflation surprise’.Real transfers are the National Accounts variable‘currentgrants and subsidies’ (deflated by the Retail Price Index),about 37% of total government expenditure in 1993. This is agood variable to choose as it fluctuates quite a lot in the short

30 35 40 45 50 55-0.15

-0.1

-0.05

0

0.05

0.1

0.15

0.2

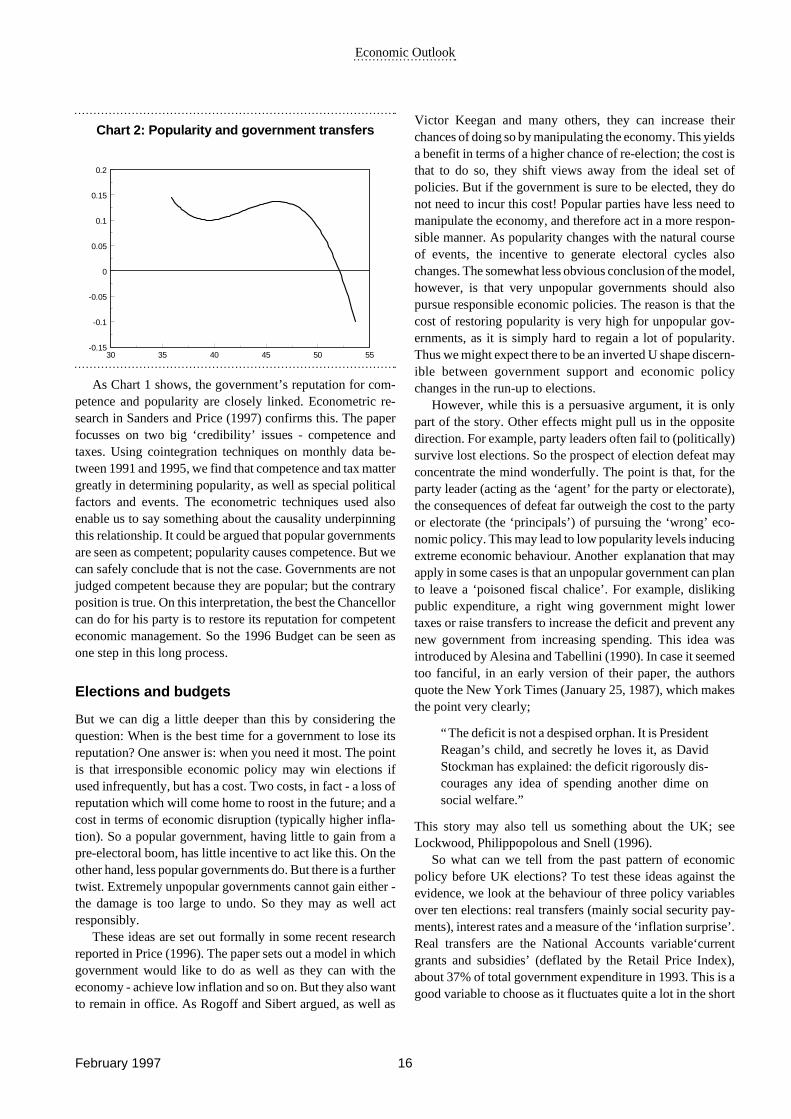

Chart 2: Popularity and government transfers

Economic Outlook

February 1997 16

run and has a very direct impact on voters. Interest rates arethree-month Treasury Bill rates. Inflation surprises are theone-step ahead forecast errors from a 40-period rolling regres-sion 6th order auto regressive process on inflation. Whathappens is that in all cases popular governments behaveresponsibly. As they get less popular, they (for example) boostspending. The relationship starts to dip as popularity declines- but then rises again as popularity dips further. Very unpopu-lar governments go for broke in a spectacular manner. The keyresults are summarised in Charts 2 to 4, which show the‘steady state’ effect, abstracting from the short-run dynamics.In essence, the figures show the amount by which the policyinstruments in question deviate from their long-run levels(vertical scale) at different levels of popularity (shown onhorizontal axis). The zero line is the long-run average, al-though this does not imply it is the ‘best’ level. Low valuesare ‘responsible’ - that is, they are low in relation to thelong-run average. High values indicate an electoral ‘bribe’.What is most remarkable is that the same effect appears tohold for all three variables and is particularly strong forinterest rates - the instrument most easy to manipulate. (Ashigher interest rates are ‘bad’ for electoral support the scale isnegative to enable comparisons.) Not only is the shape thesame, but also the turning points. We may have come acrossa new law of the electoral cycle.

Conclusion

What we learn from this analysis is that popularity, reputationand competence are closely linked. It looks like an unpopularadministration attempted to cash in its hard-won reputationfor competent behaviour in 1992 - with some success. But thiscard could not be played again. After large tax increases anda complete reversal in exchange rate policy after 1992, popu-larity slumped to record lows. Since then, first Lamont andthen Clarke painstakingly worked to reacquire a reputation forcompetence with cautious fiscal policy. But as Clarke himselfacknowledged in the run-up to the November budget, tax cuts

are now subjected to a stringent fiscal condition, more so thanever before. John Major’s only hope is that the stream of goodeconomic news continues. On past evidence, this will eventu-ally filter through to restore the government’s lost reputation.On this view, Major is therefore right to wait until the lastminute to hold the election - although as his majority hasdwindled, the government has increasingly appeared a victim,rather than a shaper, of events. This is not an image guaranteedto restore confidence. But in any event, it seems likely that thepit into which the government fell, partly dug by its ownhands, is still too deep to climb out of before May. �

References

Alesina, A and R Perotti (1995) ‘Fiscal adjustments; fiscalexpansion and adjustment in OECD countries’, EconomicPolicy 21 pp 205-40.

Alesina, A and G Tabellini (1990)‘A positive theory of fiscaldeficits and government debt’ Review of EconomicStudies Vol. 57 pp 403-14.

Kydland, F and E Prescott (1977) ‘Rules rather thandiscretion; the inconsistency of optimal plans’ Journal ofPolitical Economy Vol. 85 pp 473-91.

Lockwood, B, Philippopoulos, A and A Snell (1996) ‘Fiscalpolicy, public debt stabilisation and politics: theory andUK evidence’ Economic Journal Vol. 106 pp 894-911.

Price, S (1996) ‘Government popularity and the politicalbusiness cycle’ City University Economics DepartmentDiscussion Paper.

Price S and D Sanders (1995) ‘Economic competence,government popularity and rational expectations’Manchester School Vol 62 pp 296-312.

Rogoff, K and A Sibert (1988) ‘Equilibrium political businesscycles’ Review of Economic Studies Vol 55 pp 1-16.

Sanders, D and S Price (1997) ‘Government popularity,competence and credibility in the UK, 1991 to 1995’mimeo.

30 35 40 45 50 55-5

-4

-3

-2

-1

0

1

2

3

Chart 4: Popularity and inflation surprises

36 40 44 48 52-0.5

-0.4

-0.3

-0.2

-0.1

0

0.1

0.2

Chart 3: Popularity and interest rates

(Interest rate scale negative for comparison)

Economic Outlook

17 February 1997