the allianced enterprise: breakout strategy for the … enterprise.pdf · peter f. drucker has said...

TRANSCRIPT

The Allianced Enterprise:Breakout Strategy forthe New Millennium

Fifth in a Series of Viewpoints on Alliances

©2000 Booz•Allen & Hamilton Inc.

Executive Summary

Strategic alliances are sweeping through nearly every industry and are becoming an essential driver of superior growth. Within five years, the value of alliances is projected to range between $30 trillion to$50 trillion. Peter F. Drucker has said that there is not just a surge inalliances but “a worldwide restructuring” is occurring in the shape ofalliances and partnerships.

Recent surveys by Booz•Allen have revealed:

• More than 20% of the revenue generated from the top 2,000 U.S.and European companies now comes from alliances, with morepredicted in the near future.

• These same companies earn higher ROIs and ROEs on theiralliances than from their core businesses.

• Leading edge alliance companies are creating a string of interconnected relationships which allows them to overpower the competition.

• The traditional “command and control” organizational model isinadequate to manage the complex set of relationships formingoutside the direct control of the corporation.

Why is a new organizational model called for? What does it look like? How does it work? How does it differ from the traditional“command and control” organizational model, which has worked so well up to now?

This Viewpoint addresses these questions, and covers:

• The Five Driving Forces Behind Alliances

• The Three Alliance Modes— Filling Single and Multiple Gap Deficiencies— Creating Integrated Products and Services— Forming a Breakout Offering

• Four “Pure Tone” Alliance Models— Franchise Model: Deep Bench Strength— Portfolio Model: Hub and Spoke— Cooperative Model: Mutual Benefit— Constellation Model: Integrated Service Offering

Nineteen ninety-eight in Monaco. The magnified image of

Bill Gates beams from a giant screen in front of 200

executives of elite technology firms in Europe during a

live video conference. This leader of the most successful business

start-up of the past century makes a startling admission: “Microsoft

can’t make it alone, but together anything is possible.”

Indeed alliances have become an essential element of every

successful business. They bring higher growth, higher profitability

and higher market valuations. Global companies with successful

alliances get more than 20% of their revenues from alliances today,

and they expect that percentage to increase to 35% by 2004; the

leading European companies are already averaging almost 30%.

Alliance-intensive companies earn 70% higher return on equity

and they are more likely to see higher market valuations. Alliance

announcements routinely cause surges in the stock of both partners.

The Allianced Enterprise:Breakout Strategy for the New Millennium

A Viewpoint by:

John R. Harbison Peter Pekar, Jr.Albert Viscio David Moloney

2

Alliances are becomingpervasive in the very fabric ofhow business is conducted, andcompanies such as Hewlett-Packard and Oracle are decidingthat the ability to form successfulalliances is in itself a core com-petency to be nurtured and devel-oped. But something is missing.Corporations have evolved port-folios of alliances, but too oftenthey are managed discretely, notas an extended enterprise. Yet the fundamental truth is that the predominant “command andcontrol” organizational modelthat we have known for thepast century is inadequate tomanage the complex set ofrelationships where over 50%of the activity of a companyoccurs outside the company.To unleash the power of thisportfolio of relationships, a new model is needed — The Allianced Enterprise.

What is this? How will itwork? This Viewpoint will beginto lay out our blueprint foraddressing the challenge of TheAllianced Enterprise, and howyou can apply the concept toyour company.

Background

As recently as only twodecades ago, competitionwas simpler and compa-

nies did not need to excel in allcapabilities or participate acrossthe globe — one differential capa-bility serving one major marketregion was often enough. Thepace of change in technologiesand markets was modest com-pared with today’s activity, andindustry boundaries were well-defined and generally not global.If you lacked a capability, youeither took the time to develop it or you bought it through anacquisition.

Shareholders were (rela-tively) patient and less demand-ing about profitability andreturns. The hottest ideas of theday for strategic thinkers andplanners were market segmenta-tion, application of portfoliomodels (to categorize the compa-nies’ different businesses anddetermine resource allocation)and competitive strategies. The“command and control” modelwhich had evolved over the lasttwo centuries was still workingsuccessfully.

But there were some disso-nant voices saying that thingswere not what they seemed to be.Individuals such as Gary Hamel(London Business School),Barry Nalebuff (Yale) and AdamBrandenburger (Harvard) noticed

a pattern emerging where compa-nies were voluntarily deciding to cooperate. This cooperationspawned a new type of businessentity —a less discrete enterprisewith clusters of common activi-ties in the midst of a network ofrelationships. The goal of thisnetwork was to share knowledgeand core capabilities in order to rapidly increase the value tocustomers.

These embryonic networksled others such as MichaelHammer (MIT) and SumantraGhoshal (London BusinessSchool) to predict that the tradi-tional concept of managementand control was at the end of its life cycle. And Ben Gomes-Casseres (Brandeis) coined the phrase “constellations” todescribe this new era. BrucePasternack and Albert Viscio at Booz •Allen studied thisemerging trend and came to the conclusion that we are moving toward a “CenterlessCorporation” where competitivestrength will be based more onharnessing capabilities, knowl-edge and the power of people in ways previously unknown (for more details see their bookThe Centerless Corporation).

We are now in the earlyphases of a new era where cooperative business models will become dominant forces in the world economy.

3

The Allianced Enterprise as an Alternative GrowthEngine

Many companies areextending their enter-prises beyond internal

boundaries by teaming withother companies. These relation-ships run from conventional trans-actional sourcing and servicingarrangements at one extreme toacquisitions and mergers at theother. In the middle of the spec-trum are what we call strategicalliances.

We have been studyingstrategic alliances for 15 years.These alliances are not transac-tional (arm’s length) in naturebut are entities where partnersare willing to act in unison andshare core capabilities. Let usshare with you the results of ourmost recent survey of seniorexecutives in the top U.S. andEuropean firms:• In the past two years, morethan 20,000 alliances have beenformed worldwide, and more thanhalf occurred between competi-tors. All our participants said thatalliances are increasing withintheir industry, with over 75% not-ing that alliances are effective.Acquisitions and mergers over thesame period have also remained

strong, with over 15,000 complet-ed; however, a success rate of lessthan 50% is acknowledged.• The percentage of revenuethat the top 1,000 U.S. compa-nies have earned from strategicalliances is now 18% (vs. Europeat almost 30%). By 2004, thesesame companies expect over30% (U.S.) and nearly 40%(Europe) of their revenue tocome from alliances. • The top two reasons stated for forming alliances are (1) to accelerate the growth tra-jectory (75% of survey); and,(2) to gain access to externalcore capabilities (67%). • For the past ten years, strate-gic alliances have consistentlyproduced a return on investment

of nearly 17% among the top2,000 companies in the world.This is 50% more than the aver-age return on investment thatcompanies produced overall. And the 25 Fortune 500 compa-nies most active in alliances earn an average return on equityof 17.2% compared to 10.1% for the 25 least active.

With over 20% of today’srevenue coming from strategicalliances and with more predictedin the near future, is the current“command and control” modelappropriate for managing in theAllianced Enterprise Era?

When we asked this question, nearly two-thirds of our respondents said, “No!”(see Exhibit 1).

Exhibit 1. Today’s Organization Model Is Flawed

Source: 1999 BA&H survey of over 200 U.S. and European firms

NotAppropriate

U.S. & Europeans RateOrganizational Structure

Appropriateness inExtended Enterprise Era

Appropriate

If these battle-testedalliance executives believe theircurrent business model is notappropriate, then what willwork? Where are we headed? Tostart, let’s look at the forces driv-ing this explosion in alliances.

Dynamic Forces DrivingStrategic Alliances

Environmental: There are certainenvironmental conditions thatfavor the formation of alliancesand explain the increased coop-eration in the last decade:

1) Competitive boundaries haveblurred as technology advanceshave created crossover opportuni-ties merging formerly distinctindustries

2) Advances in communications(voicemail, e-mail and e-Business)and the trend toward global markets link formerly disparateproducts, markets and geographi-cal regions, and facilitate the

open communication essentialbetween partners

3) Intensifying competition and increasingly demanding customers require advantagedcapabilities across the board,and no company has the time orresources to either develop thesethemselves or acquire them

4) The insatiable drive for tech-nology standards and compatibil-ity in a globally linked worldnecessitates cooperation

5) Growing number of companieshave successfully scaled thealliance learning curve and aglobal body of expertise to ensuresuccessful alliance formulationand execution

Let’s examine some of thefacts behind these influences:• Defending the Ramparts“Retrenchment to the Core ”—Our studies reveal that in 1985only 26% of the revenue of topU.S. companies was coming from their core businesses. Diver-sification was still the standard ofthe day. By 1998, all this had

4

changed. Today we find that thecore generates over 60% (U.S.)and 67% (Europe) of these com-panies’ revenue. It is critical toeffectively identify, protect andenhance one’s core without giv-ing up the key elements of thevalue chain where one’s core isnot positioned. As competitionintensifies, alliances fill in capa-bility gaps to protect the corebusiness.• “Nowhere to Hide—GlobalReach”— Fifteen years ago U.S.companies produced only 14% oftheir revenue overseas. Most U.S.companies saw competition con-fined to U.S. borders. However,today 35% of U.S. revenue (and45% of European revenue) comesfrom international sales — mak-ing all firms vulnerable to threatsfrom global players, especiallyfrom experienced cooperativeinternational partners. • “Holding the High Ground—Turbocharging the Develop-ment Engine”— R&D took aback seat in the early 1980s withonly about 2% of revenue spent

Source: Booz• Allen & Hamilton

Exhibit 2. Growth Drives Performance

* Shareholder returns reflected stock price appreciation plus dividend reinvestment, adjusting for stock split.

Financial Performance 1985 –1994

ANNUAL RATES OF GROWTH TEN-YEAR CUMULATIVE GROWTH

Shareholder Earnings Revenue Shareholder Earnings RevenueReturns* Returns

90th Percentile 23.7% 25.9% 21.1% 841% 997% 678%

80th Percentile 19.1% 17.8% 13.3% 573% 516% 347%

50th Percentile 12.7% 9.6% 8.5% 331% 251% 226%

5

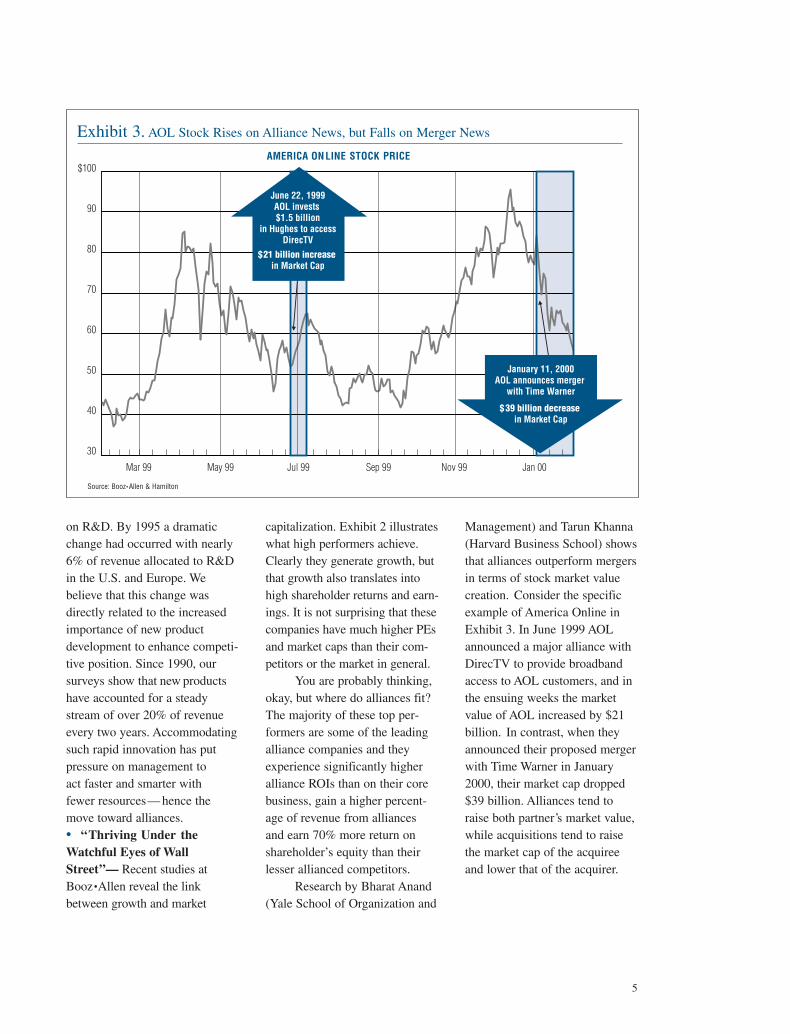

Management) and Tarun Khanna(Harvard Business School) showsthat alliances outperform mergersin terms of stock market valuecreation. Consider the specificexample of America Online inExhibit 3. In June 1999 AOLannounced a major alliance withDirecTV to provide broadbandaccess to AOL customers, and inthe ensuing weeks the marketvalue of AOL increased by $21billion. In contrast, when theyannounced their proposed mergerwith Time Warner in January2000, their market cap dropped$39 billion. Alliances tend toraise both partner’s market value,while acquisitions tend to raisethe market cap of the acquireeand lower that of the acquirer.

on R&D. By 1995 a dramaticchange had occurred with nearly6% of revenue allocated to R&Din the U.S. and Europe. Webelieve that this change wasdirectly related to the increasedimportance of new product development to enhance competi-tive position. Since 1990, our surveys show that new productshave accounted for a steadystream of over 20% of revenueevery two years. Accommodatingsuch rapid innovation has putpressure on management to act faster and smarter with fewer resources— hence the move toward alliances.• “Thriving Under theWatchful Eyes of WallStreet”— Recent studies atBooz•Allen reveal the linkbetween growth and market

capitalization. Exhibit 2 illustrateswhat high performers achieve.Clearly they generate growth, butthat growth also translates intohigh shareholder returns and earn-ings. It is not surprising that thesecompanies have much higher PEsand market caps than their com-petitors or the market in general.

You are probably thinking,okay, but where do alliances fit?The majority of these top per-formers are some of the leadingalliance companies and theyexperience significantly higheralliance ROIs than on their corebusiness, gain a higher percent-age of revenue from alliances and earn 70% more return onshareholder’s equity than theirlesser allianced competitors.

Research by Bharat Anand(Yale School of Organization and

30

Mar 99 May 99 Jul 99 Sep 99 Nov 99 Jan 00

40

50

60

70

80

90

$100

January 11, 2000AOL announces merger

with Time Warner

$39 billion decrease in Market Cap

June 22, 1999AOL invests $1.5 billion

in Hughes to accessDirecTV

$21 billion increase in Market Cap

AMERICA ON LINE STOCK PRICE

Source: Booz• Allen & Hamilton

Exhibit 3. AOL Stock Rises on Alliance News, but Falls on Merger News

ProductInnovation

Process Innovation PotentialProduct

Innovation

R&D

Gain Credibility

Access Capital

Develop Standards

External Value Proposition

Market/Customer Reach

Branding

Co-operation

Stabilize Competition(Constellation Model)

Reduce Cost

R&DExternal Value Proposition

Market/Customer Reach

EARLYGROWTH

GROWTH

ALLIANCEIMPERATIVES

RAPIDGROWTH

CONSOLIDATION INNOVATE/SUSTAIN/DECLINE

STABILITY

Source: Booz • Allen & Hamilton

Exhibit 4. Business Life Cycle Phases Influence Alliance Imperatives

6

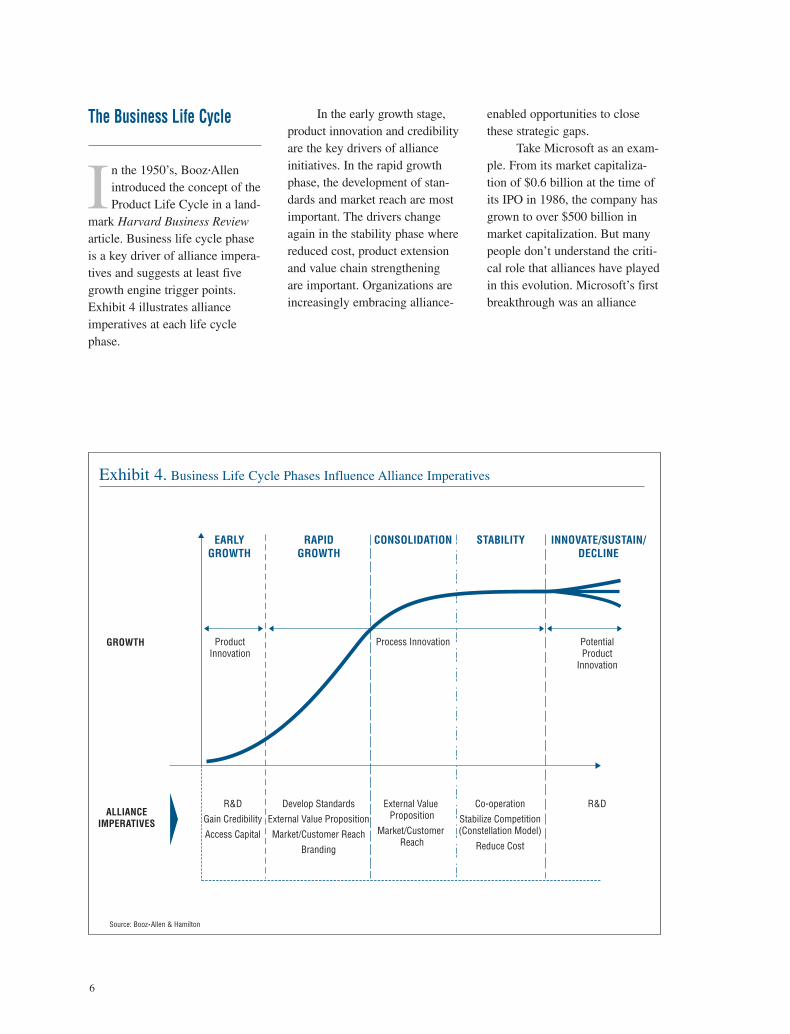

The Business Life Cycle

In the 1950’s, Booz •Allenintroduced the concept of theProduct Life Cycle in a land-

mark Harvard Business Reviewarticle. Business life cycle phaseis a key driver of alliance impera-tives and suggests at least fivegrowth engine trigger points.Exhibit 4 illustrates allianceimperatives at each life cyclephase.

In the early growth stage,product innovation and credibilityare the key drivers of alliance initiatives. In the rapid growthphase, the development of stan-dards and market reach are mostimportant. The drivers changeagain in the stability phase wherereduced cost, product extensionand value chain strengthening are important. Organizations areincreasingly embracing alliance-

enabled opportunities to closethese strategic gaps.

Take Microsoft as an exam-ple. From its market capitaliza-tion of $0.6 billion at the time ofits IPO in 1986, the company hasgrown to over $500 billion inmarket capitalization. But manypeople don’t understand the criti-cal role that alliances have playedin this evolution. Microsoft’s firstbreakthrough was an alliance

POTE

NTI

AL P

ARTN

ERS

FOR

A R

ETAI

L FU

ND

S M

ANAG

ER

LIFE CYCLE EVENT ANALYSIS — INDIVIDUAL INVESTMENT LIFE CYCLE

• Financial institutionswithout investmentoffering (e.g.,credit unions,small banks)

• Employers

• Professionalassociations/affinity groups

• Real estateagents

• HR consultants

• Accountants

• Independentfinancialadvisers

• Investment magazines

• Investment clubs

• Financialplanningsoftware

• FinancialplanningInternet sites

• Independentfinancialadvisers

• Investment magazines

• Investment clubs

• InvestmentInternet sites

• Stockbrokers

• Credit unions/small banks

• Financialmanagementsoftware (e.g.,Quicken, MSMoney)

• Utilities

• Credit cardcompanies

• Investment magazines/finance papers

• Financialmanagementsoftware (e.g.,Quicken, MSMoney)

• InvestmenttrackingInternet sites

• Accountants

• Tax returnpreparationagents

• Independentfinancialadvisers

• Stockbrokers

Acquire Funds to Invest

Identify Investment Needs

InvestigateAvailableProducts

EffectTransaction

MonitorInvestment Performance

Manage Tax

SellInvestment

EXAMPLES

7

with IBM to develop DOS. It fol-lowed this alliance with its sec-ond breakthrough, the emergingdominance in operating systemsthrough Windows and its “Wintel”alliance with Intel. The pace hasnever slackened. In the past twoyears, the company announced on average two alliances per day. Microsoft’s investments inthese partnerships have paid huge

dividends; for example, theirequity investment in Apple hasrisen over 800% in just twoyears.

Business life cycle phase isthe key driver of alliance strategyimperatives. Once the linkagebetween these imperatives andthe corporate and business strate-gies and objectives is clear, thenext step is determining wherealliances can be effective in meeting these objectives and

strategies. Processes for identify-ing alliance opportunities encom-pass traditional industry analysis,brainstorming and a new breed of opportunity identifying toolswe call “Forcing Techniques.”Exhibit 5 illustrates a forcingtechnique designed to identifyalliance opportunities for a retail funds manager looking to grow distribution.

Exhibit 5. Forcing Techniques to Surface Alliance Options—Example

Source: Booz • Allen & Hamilton

alliances, but from using a groupof alliances in a concentratedmanner, i.e., creating a string or class of interconnectedalliances to rapidly overpower the competition.

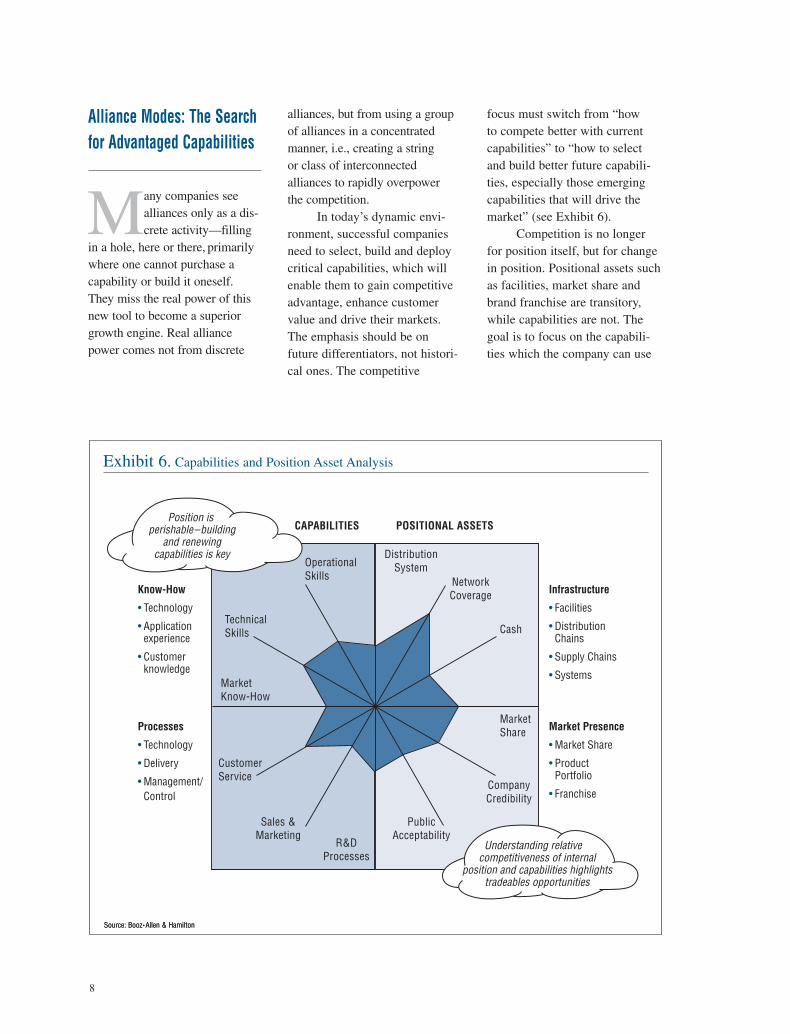

In today’s dynamic envi-ronment, successful companiesneed to select, build and deploycritical capabilities, which willenable them to gain competitiveadvantage, enhance customervalue and drive their markets.The emphasis should be onfuture differentiators, not histori-cal ones. The competitive

focus must switch from “how to compete better with currentcapabilities” to “how to selectand build better future capabili-ties, especially those emergingcapabilities that will drive themarket” (see Exhibit 6).

Competition is no longerfor position itself, but for changein position. Positional assets suchas facilities, market share andbrand franchise are transitory,while capabilities are not. Thegoal is to focus on the capabili-ties which the company can use

8

Alliance Modes: The Searchfor Advantaged Capabilities

Many companies seealliances only as a dis-crete activity—filling

in a hole, here or there, primarilywhere one cannot purchase acapability or build it oneself.They miss the real power of thisnew tool to become a superiorgrowth engine. Real alliancepower comes not from discrete

OperationalSkills

TechnicalSkills

MarketKnow-How

CustomerService

MarketShare

Cash

CompanyCredibility

NetworkCoverage

DistributionSystem

Sales &Marketing

PublicAcceptability

R&DProcesses

CAPABILITIES POSITIONAL ASSETS

Know-How

• Technology

• Applicationexperience

• Customerknowledge

Infrastructure

• Facilities

• DistributionChains

• Supply Chains

• Systems

Processes

• Technology

• Delivery

• Management/Control

Market Presence

• Market Share

• ProductPortfolio

• Franchise

Position is perishable–building

and renewingcapabilities is key

Understanding relative competitiveness of internal

position and capabilities highlightstradeables opportunities

Exhibit 6. Capabilities and Position Asset Analysis

Source: Booz • Allen & HamiltonSource: Booz • Allen & Hamilton

9

to constantly renew and extendits position. We find alliances are being used in the followingways. (We will later discuss howthese modes can be grouped into classes of interconnectedalliances, thus leveraging a vastarray of capabilities to increasevalue to the consumer and tooverwhelm the competition.)

1) Filling Single and MultipleGap Deficiencies: Capabilitiesare know-how leveraged by cost-effective, responsive businessprocesses and systems for inno-vation and delivery of enhancedcustomer value. Capabilities areintrinsically cross-functional;they are based on horizontally

organized teams working according to well-designed,pre-engineered processes andempowered by policy to makedecisions within an establishedframework of rules.

Competitive advantage incapabilities comes from preci-sion tailoring and sharp focus —no company can afford to buildadvantaged capabilities againstall aspects of the value-addedstream.

Alliances are an excellentsolution for filling critical gapswhere the company lacks theresources and/or time to build its own capability to world-classlevels. Alliances also should notbe viewed as static events. Thestrategy linkage is particularlyimportant when thinking about

the changing “know-how” needsand emerging critical processesthat will impact the company in the future. At a minimum,alliances should be seen as away to fill key single or multiplegaps in a company’s value-addedchain.

2) Creating IntegratedProducts and Services: Thealliance approach also can beused to build integrated productsor services. A team of partnerscan significantly raise the com-petitive bar whereby a singlecompetitor will be outflanked or be forced to respond and thus place a severe strain on its internal resources.

integration. We expect that thewinning alliance(s) will findways of acting more effectivelyas one, potentially leveragingregional JVs and other mecha-nisms to combine revenue man-agement fully, while integratingoperations more effectively overtime. The group that is most suc-cessful with these initiatives willnot only further stimulate travel,but will gain share of high-yieldtraffic over time at the expenseof other groupings.

Beyond this, airlines aredeveloping additional alliancesand relationships in related busi-nesses such as maintenance, and

effectively on their own—providing more competitiveofferings between medium-sizedcities that were not aggressivelymarketed and sold with the more traditional interline rela-tionships. Member airlines arealso rewarded with richer yields,attracting a higher proportion of frequent travelers.

However, significant oppor-tunities remain untapped in thelargest (new) alliances. The lackof effective cross-company compensation schemes, lack of antitrust immunity in someinstances and a natural reluc-tance to violate corporate sover-eignty may be inhibiting further

Global airline alliances areperhaps the most obvious exam-ple of initiatives to provide anintegrated product or serviceoffering (see Exhibit 7). Memberairlines coordinate schedules forrapid, more hassle-free connec-tions; frequent travelers are pro-vided recognition and specialservices even when far fromhome; and customers can earnand redeem miles essentiallywherever they go. Alliance mem-bers have been especially suc-cessful at stimulating marketsthat neither carrier could serve

10

Revenue

100%

100%

100%

Cost

DEGREE OF INTEGRATION IN AIRLINE ALLIANCES

New Code-ShareWorld

RegionalJVS

Combined Revenue

Management

Integrated Operating Company

Simple Win-WinActions MaintainCorp. Sovereignty

Full Integration

Combine FFP,code-sharing,schedules, new routes

Shared Atlanticprofit center &

coordinated yield management

Treat revenuemanagement

as onenetwork

FULL(One Brand)

Coordinatedsales, handling,

purchasing,spares, rotables,

new AC

Coordinatedgauge/crew/

routing, sales & fleetrationalization

All but crewand aspects

of MROconsolidated

FULL(One Operation)

Exhibit 7. The Future of Global Airline Alliances

Source: Booz • Allen & HamiltonSource: Booz • Allen & Hamilton

goal has been to create a broadband alternative to AOL(America Online) by marrying a leading graphics-intensive portal/search engine (Excite) to@Home’s exclusive distributionarrangement with the cable TVcompanies. The service offeringto customers is integrated (e.g.,Cox@home, Comcast@home,etc.), and the customer is proba-bly not aware that there are multiple companies behind theservice offering.

In the breakout offering,successful partners select, buildand deploy critical capabilities,which will enable them to gaincompetitive advantage, enhancecustomer value and drive theirmarkets, thus putting their com-petitors on the defensive.

Controlling the Battlefield—Emergence of AllianceModels

“The Command and ControlModel of Organization IsDead. Long Live the AlliancedEnterprise!”

The exploding number andscope of alliances is cre-ating challenges for exec-

utives trying to manage this complex activity — which isincreasingly outside the directcontrol of the corporation.Companies are forming vastarrays of alliances that on the surface seem to be a collection of unconnected arrangements.

the airlines are beginning toexplore potential “breakout”strategies by leveraging their keycapabilities and market positionsin the e-commerce and loyaltymanagement businesses.

3) Forming a BreakoutOffering: Some companies areusing alliances to develop abreakout strategy to leap over the competition and grab the high ground before the competi-tion can react. Consider Exhibit 8which shows how a constellationhas been developed in theExcite@Home cable broadbandInternet access market.

Since its founding in 1995,@Home has reached affiliateagreements with 23 leading cablecompanies worldwide. Their

11

ExciteHigh GraphicsPortal/Search

Engine

$7 Billion Acquisition

HIGHBANDWIDTH

INTERNETACCESS Cable

ModemSuppliers

MicrosoftWindows CE

Web TV

@HomeCable Modem

Service

AT&TCable Systems

and PhoneServices

OtherCable

Systems

Exhibit 8. Excite@Home Cable Modems “Constellation”

Source: Booz • Allen & HamiltonSource: Booz • Allen & Hamilton

However, these alliances areincreasingly becoming an inter-related tapestry of activities,linked in ways to gain competi-tive advantage and control thebattlefield, rather than a series ofdiscrete transactions. The need toadapt the organizational model iscompelling.

Leading-edge companiesare beginning to use alliancearchitecture models that aredefined in terms of the rolestrategic alliances can play andtheir leadership structure. Thekey issue is how should these

alliances be governed, controlledand managed? Consider this:many of these alliances coulddwarf the size of any one partner.Yet today, many of these highlydynamic and competitivelystrong entities have no definablebusiness model of their own.

These models cannot use a“command and control” businessmodel to span multiple partners.Rather, they require somethingmore flexible and dynamic toreflect the market environmentand the partnership structure. We see four models emerging

for companies with multiplealliances: franchise, portfolio,cooperative and constellation,and each of these “pure tones”will have a different set of impli-cations in terms of the appropri-ate governance model.

These pure tone models are shown in Exhibit 9, anddescribed on the following pages.

Need for AdditionalCapabilities

Need toInvolve Peers

POSITIONAL ASSETS

PORTFOLIO(e.g., Time Warner, AT&T)

CONSTELLATION(e.g., Mondex, Excite@Home)

FRANCHISE(e.g., McDonald's, Nintendo)

COOPERATIVE(e.g., VISA, TriStar)

NUMBER OFALLIANCE

ROLES

SEVERAL(Multiple

Gaps)

ONE(Single

Gap)

SINGLE ENTITY COALITION

Multiple classalliances managed

as portfolio by one firm

Alliances between many

comparably sized peers

STRUCTURE OF LEADERSHIP

Multiple interdependentalliances led by

two or morecomparably sized peers

Alliance betweenfirm and one discrete

class of partners

Exhibit 9. Alliance Architecture Models

12

Source: Booz • Allen & Hamilton

13

contains far too many elementsfor it to command all the capa-bilities necessary to compete.However, instead of forming a number of single discretearrangements to fill each gap(thus making itself vulnerableshould a partner experience diffi-culty or if the market changesrapidly), the company decides to create multiple class alliancesmanaged as a portfolio. Thesecompanies are still in the center,but they are weaving together aportfolio of distinct and oftenunrelated partnerships. Theexternal partners have little rela-tionship to each other, but inter-act only with the company at the center.

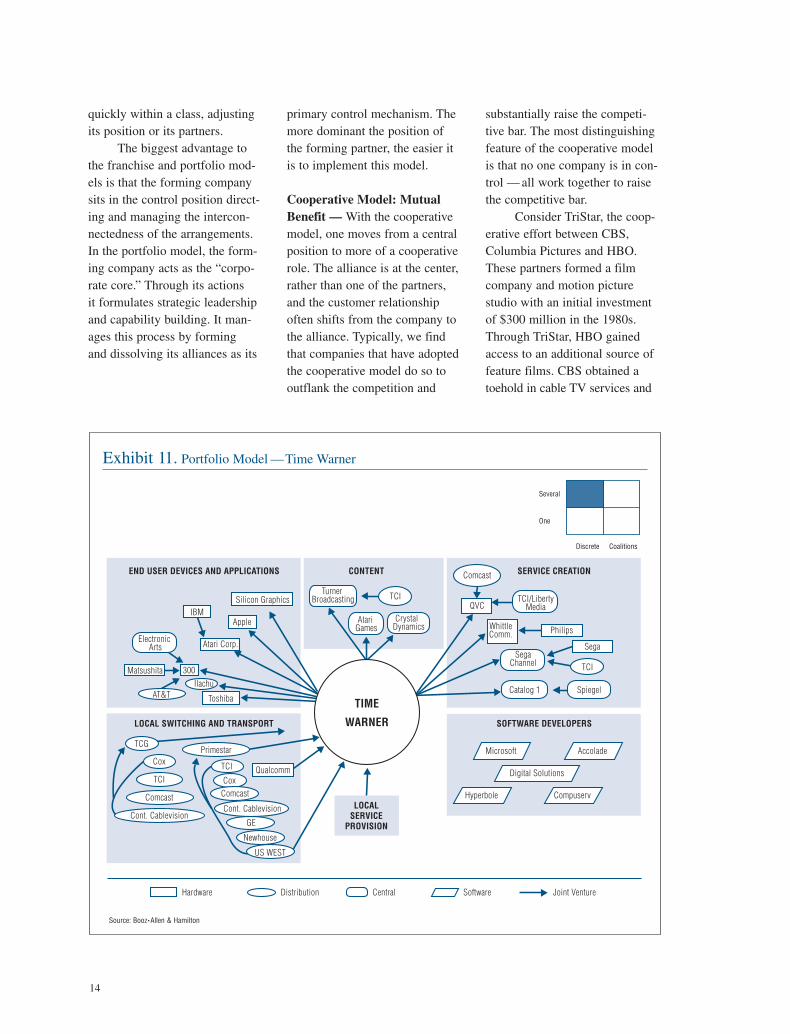

For example, Time Warneris trying to cover multiple gapsin the key elements of the valuechain—including content, appli-cations, distribution, softwareand service (see Exhibit 11). Ineach of these areas, it has formedalliances with a variety of part-ners, although generally a similarclass of companies. It managesthese classes as a portfolio,thus directing the arrangementsto meet its strategic needs.Although Time Warner acts inconsort with its portfolio part-ners, it never loses its sense ofdirection or co-ops its control of its future. By adopting theportfolio approach, it can move

Franchise Model: Deep BenchStrength — This model is usedby companies to fill a single crit-ical gap in its value chain. Butthe needs in that gap area aregreater than any one partner canfill. So the company develops areplicable alliance model for aclass of partnerships.

For example, Nintendo isusing this franchise model to fillin a key capability need— thedevelopment of games for itsconsoles. Nintendo is positionedin the center, closely controllingthe activities of its alliance partners (see Exhibit 10). Thefranchise model develops a single alliance role that can berefined and quickly replicated tocreate scale, thereby producingan alliance growth corridor forthe alliance initiator. Thisalliance architecture is a signifi-cant part of the business modelof e-Business companies that use the franchise architecture to develop and manage referralaffiliates (e.g., Next Card),content partners (AOL) or distri-bution partners (FirstUSA).

Portfolio Model: Hub andSpoke — The portfolio model isa major step up from the fran-chise approach. Companies thatadopt this approach are findingthat the value-added chain

Acclaim Entertainment Inc./LJN Toys Ltd.

Accolade, Inc.Activision, Inc.Advanced GravisAdvanced Productions, Inc.American Sammy Corp.American Softworks Corp.American Technos, Inc.Ascii Entertainment Inc./NexoftAtlus Software, Inc.Bandai America, Inc./ShinseiBMG EntertainmentCapcomDisney InteractiveEidos IneractiveElectro Brain Corp.Electronic Arts/EA SportsFox InteractiveGametek, Inc./Cybersoft, Inc.GT Interactive SoftwareGTE Interactive MediaHot-B USA Inc.

I MotionIMNInteract Accessories Inc.Interplay ProductionsJaleco USA, Inc.JVC Musical Industries, Inc.Kemco of America, Inc.Koei CorporationKonami Inc./Ultra SoftLaral GroupLeft Field EntertainmentLife FitnessLight Wave TechnologiesMajesco Sales, Inc.Microprose Software, Inc.Midway Home EntertainmentMilton BradleyMindscape/Software ToolworksNamco Hometek, Inc.Natsume Inc.Nuby/CurtisOcean of America, Inc.Parker BrothersPhilips Media

Playmates Interactive Ent.Psygnosis, LimitedRare Ltd.Raya Systems, Inc.Seta USA, Inc.Sharp Electronics Corp.Sports Sciences, Inc.Sun Corporation of America

(Sunsoft)Take-Two Interactive

Software, Inc.TecMagik, Inc.Tecmo Inc.T*HQ/Malibu Games/Black

Pearl SoftwareTitus Software Corp.Toho Co., Ltd.TycoUbi Soft Inc.Viacom New MediaVic Tokai Inc.Video SystemVirgin Interactive

Entertainment, Inc.

Nintendo

Several

Discrete Coalitions

One

Exhibit 10. Franchise Model —Nintendo

Source: Booz • Allen & Hamilton

quickly within a class, adjustingits position or its partners.

The biggest advantage tothe franchise and portfolio mod-els is that the forming companysits in the control position direct-ing and managing the intercon-nectedness of the arrangements.In the portfolio model, the form-ing company acts as the “corpo-rate core.” Through its actions it formulates strategic leadershipand capability building. It man-ages this process by forming and dissolving its alliances as its

primary control mechanism. Themore dominant the position ofthe forming partner, the easier itis to implement this model.

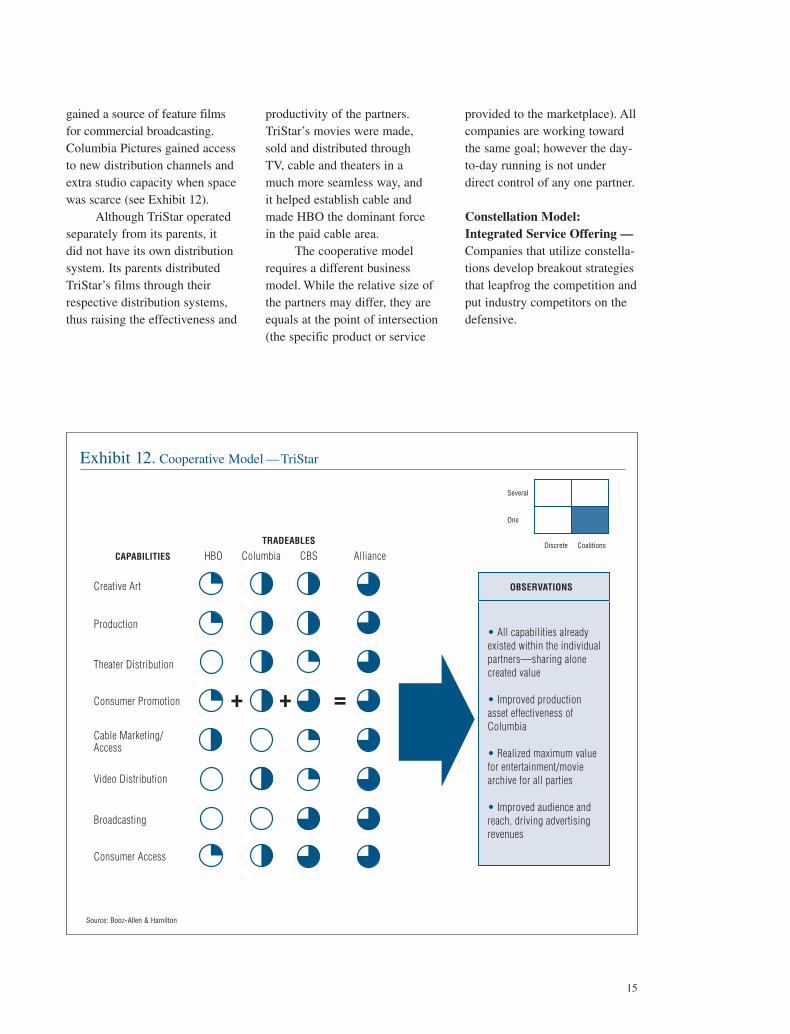

Cooperative Model: MutualBenefit — With the cooperativemodel, one moves from a centralposition to more of a cooperativerole. The alliance is at the center,rather than one of the partners,and the customer relationshipoften shifts from the company tothe alliance. Typically, we findthat companies that have adoptedthe cooperative model do so tooutflank the competition and

Comcast

Cox

TCI

AT&T

Comcast

Cont. Cablevision

Cox

TCI

Comcast

GE

Newhouse

Cont. Cablevision

QVC

SegaChannel

Catalog 1

Microsoft Accolade

Digital Solutions

Hyperbole Compuserv

DistributionHardware Central Software Joint Venture

Spiegel

Atari Games

Toshiba

IlachuMatsushita

Atari Corp.

Apple

Silicon Graphics

300

WhittleComm.

Sega

Philips

SERVICE CREATION

SOFTWARE DEVELOPERS

LOCALSERVICE

PROVISION

END USER DEVICES AND APPLICATIONS CONTENT

LOCAL SWITCHING AND TRANSPORT

TCI

IBM

TIME WARNER

Several

Discrete Coalitions

One

Turner Broadcasting

Crystal Dynamics

TCI/LibertyMedia

TCI

US WEST

Qualcomm

Primestar

Electronic Arts

TCG

Source: Booz • Allen & Hamilton

substantially raise the competi-tive bar. The most distinguishingfeature of the cooperative modelis that no one company is in con-trol — all work together to raisethe competitive bar.

Consider TriStar, the coop-erative effort between CBS,Columbia Pictures and HBO.These partners formed a filmcompany and motion picture studio with an initial investmentof $300 million in the 1980s.Through TriStar, HBO gainedaccess to an additional source offeature films. CBS obtained atoehold in cable TV services and

14

Exhibit 11. Portfolio Model —Time Warner

gained a source of feature filmsfor commercial broadcasting.Columbia Pictures gained accessto new distribution channels andextra studio capacity when spacewas scarce (see Exhibit 12).

Although TriStar operatedseparately from its parents, it did not have its own distributionsystem. Its parents distributedTriStar’s films through theirrespective distribution systems,thus raising the effectiveness and

TRADEABLES

CAPABILITIES HBO

Creative Art

Production

Theater Distribution

Consumer Promotion

Cable Marketing/Access

Video Distribution

Broadcasting

Consumer Access

Columbia CBS Alliance

Several

Discrete Coalitions

One

OBSERVATIONS

• All capabilities already existed within the individualpartners—sharing alone created value

• Improved production asset effectiveness of Columbia

• Realized maximum valuefor entertainment/movie archive for all parties

• Improved audience and reach, driving advertising revenues

+ + =

Exhibit 12. Cooperative Model —TriStar

Source: Booz • Allen & Hamilton

15

productivity of the partners.TriStar’s movies were made,sold and distributed through TV, cable and theaters in a much more seamless way, and it helped establish cable andmade HBO the dominant force in the paid cable area.

The cooperative modelrequires a different businessmodel. While the relative size ofthe partners may differ, they areequals at the point of intersection(the specific product or service

provided to the marketplace). Allcompanies are working towardthe same goal; however the day-to-day running is not underdirect control of any one partner.

Constellation Model:Integrated Service Offering —Companies that utilize constella-tions develop breakout strategiesthat leapfrog the competition andput industry competitors on thedefensive.

E-Procurement is a goodexample of an industry withemerging alliance constellations.Entering this industry requires a very substantial set of partnersplaying multiple alliance roles(portfolio model). However,requirements for global scale,standardization and substantialcapital injections are forcingearly players to share leadershipand equity with selected partnersthrough migration to a constella-tion model (see Exhibit 13).These constellations will mature

as constellation partners discovernew ways to work together tochange the rules of the game.

These constellations are initially comprised of a set ofequity joint ventures and shouldnaturally evolve into independentcompanies. They will have all the“organization” required and beself-contained. They will be gov-erned through board processesand create their own identity inthe marketplace.

Managing Alliance Models:Art of Virtual Coherence

Each alliance model has adifferent set of character-istics, governance issues

and strategic focus (see Exhibit14), and this is one key reasonthat a new organizational modelis necessary. Trying to managethese models under the old “com-mand and control” structureinhibits the formation and man-agement of these models. It hasbeen our experience that compa-nies which form and manage

16

Oracle

Oracle

OracleOracle

BAAN

BAAN

BAAN

SAP

SAP

SAP

Staples

HP Intel

PwC

ADP

ADP

Deloitte

Deloitte ArisArthur Andersen

Eggrock

PRT GrpRaymond James

PeopleSoft

PeopleSoft

PeopleSoft

PeopleSoft

PeopleSoft

SAP

SAP

SAPSAP

SAP

SAP

SAPDG

DG

DG

Unisys

Unisys

Unisys

Unisys

Peachtree

Peachtree

TRADEexMacola

Nova Is

SAP

JD Edwards

JD Edwards

Oracle

Oracle

OraclePeopleSoft

Oracle

SAP

GERS RetailGERS Retail

MCI/W

MCI/W

MCI/WMS

MS

MS

MS

MS

BSG

BSG

PwC

Cambridge

Sabre

Sabre

Sabre

Oracle

Oracle

Oracle

Oracle

SabreIndus

WalkerBrit Telecom

FileNET

TanData

Ernst & Young

Levi, Ray&ShoupRainier Tech

SARCOM

Info BuildersSymix

Solutions

SupplyChain

InfoAccess

Symix

CTP

MS

MS

MSMarket FirstCommerce 1

HPHP

MS

HP

OpenMarket

TopTierExtricity

iCat

HP IntelAMEX Velfore

Open MarketSterling VISA

ADP

FedEx

AMEX

Oracle

MSimagex.comAMEX

Oracle

MS

AMEX

Competitor

Learning & Innovation

Core Component Supplier

Implementation Services

Resellers

Industry Influencers

Harbinger

Sterling

BAANNetscape

ROLES

AT&T

SAPCommerce 1

GEISAriba ConcurClarus

Several

One

Discrete Coalitions

Exhibit 13. E-Procurement Alliance Portfolios —Ripe for Evolution to Constellations

Source: Booz • Allen & Hamilton

these successfully do not want toteam up with companies thathave not learned this lesson.

Successful companies inthe next decade will be the onesthat harness the full potential ofthe alliance models and tailortheir organizational structures totake full advantage of the “puretone” alliance situation whichmost appropriately fits their

strategic needs. The world will be difficult to navigate and competitors too ingenious ascompanies are shaken loose fromtraditional ways of doing busi-ness. Companies must develop“coherence” among the manyseemingly disparate and far-flungpieces of the business, establish apotent binding force and sense ofdirection where all the pieces

mutually reinforce each other, aswell as provide a platform forgrowth. Coherence is what allowsthe company to de-emphasize a rigid organizational structure.One of the staggering failures of the old and dysfunctional“command and control” businessmodel is that it “chokes” thepotential of the company.

17

Governance

Franchise Easiest (Operationally Managed)

Little(Fill Single Gap)

Single(Concentrate on Current

Customer/Market Segments)

Easier – Internal(Oversight Committee

Crosses Various Areas)

Little(Multiple Gap Focus)

Single(Concentrate on Current

Customer/Market Segments)

Intricate – External(Shared LeadershipShared Governance)

High(Create New Value

PropositionWithin Industry)

Multiple(Concentrate on Creating

New Value Position to Extend Reach into

Customer/Market Segments)

Difficult – External (Shared Governance

Crosses Industry Boundaries)

High(Leapfrogs Current

CompetitiveStructure)

Multiple(Rapid Expansion

into New High Growthand High Value Market

Areas Unobtainable Before)

Portfolio

Cooperative

Constellation

Integrated Offerings Industry Focus

Exhibit 14. Each “Pure Tone” Alliance Class Has a Unique Set of Characteristics

Source: Booz • Allen & Hamilton

The successful company of tomorrow will develop coher-ence between the control modeland the cooperative model ofalliances (see Exhibit 15). Sohow does one establish coherencein an alliance? How should these alliances interact with thepartners? The answers differ bykind of alliance.

Franchise alliances areoperational in nature, an exten-sion of a specific part of a com-pany and that’s where and how it should be managed.

The portfolio model is,de facto, a new business model.Since it usually involves morethan one primary part of the dom-inant partner, it is managed not byan operations group but by a busi-ness center. That center acts as the “corporate center” for thealliances. It must treat its partnersas a business unit within aCenterless Corporation — addingvalue only where the businessescannot (see Exhibit 16). It mustfocus on knowledge and peopleand work diligently to build coher-ence internally and externally.

The cooperative model is ashared business model that needsits own leadership, but with few“owners,” they need to workthrough some cooperative gover-nance structure. The challengewith these models is to establisha set of operating/performanceparameters. This model is verysimilar to what firms do whenthey establish a shared servicesorganization within the corpora-tion, or rely on an outsourcingagreement.

Major Customers

GovernmentRegulators

Stockholders

COOPERATIVE MODEL

Unions

DebtProviders

Public

Boardof

DirectorsCorporate Strategy

Operations

Governance Strategic Sourcing

EnhancingOperationalCapabilities

SharedResources

ExtendingAssetReach

JointEquity

SharedFunding

JointPartnership

Boards

Constellations

Pilots and R&D Projects

Finance

LegalAudit

BU Optimization

PortfolioMaximization

Integration andImplementations

Major Increasein Value

ParadigmShift

Mergers andAcquisitions

CEO

CONTROL MODEL

Exhibit 15. Emerging New Business Model Contains Elements of Control and Cooperation

Source: Booz • Allen & Hamilton

18

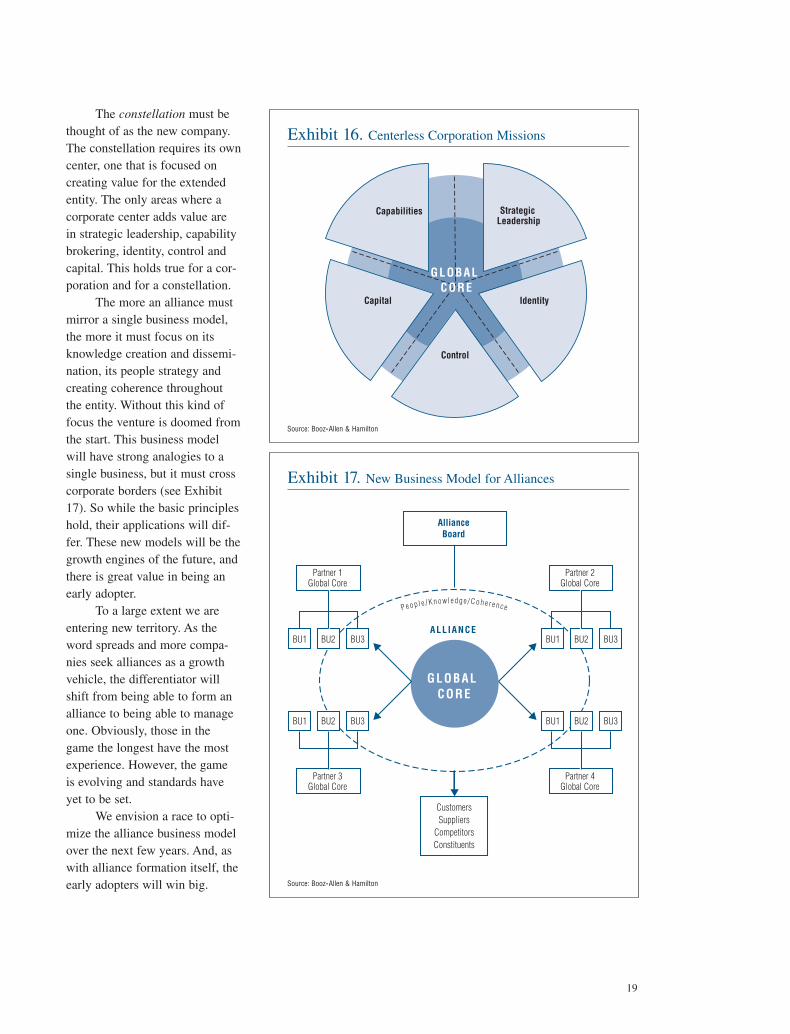

The constellation must bethought of as the new company.The constellation requires its owncenter, one that is focused on creating value for the extendedentity. The only areas where acorporate center adds value are in strategic leadership, capabilitybrokering, identity, control andcapital. This holds true for a cor-poration and for a constellation.

The more an alliance mustmirror a single business model,the more it must focus on itsknowledge creation and dissemi-nation, its people strategy andcreating coherence throughoutthe entity. Without this kind offocus the venture is doomed fromthe start. This business modelwill have strong analogies to asingle business, but it must crosscorporate borders (see Exhibit17). So while the basic principleshold, their applications will dif-fer. These new models will be thegrowth engines of the future, andthere is great value in being anearly adopter.

To a large extent we areentering new territory. As theword spreads and more compa-nies seek alliances as a growthvehicle, the differentiator willshift from being able to form analliance to being able to manageone. Obviously, those in thegame the longest have the mostexperience. However, the game is evolving and standards haveyet to be set.

We envision a race to opti-mize the alliance business modelover the next few years. And, aswith alliance formation itself, theearly adopters will win big.

GLOBAL CORE

GLOBAL CORE

ALLIANCE

AllianceBoard

CustomersSuppliers

CompetitorsConstituents

P e o p l e / K n o w l e d g e / C o h e r e n c e

BU1

Partner 2Global Core

Partner 1Global Core

BU2 BU3

BU1 BU2 BU3

BU1 BU2 BU3

BU1 BU2 BU3

Partner 4Global Core

Partner 3Global Core

Exhibit 17. New Business Model for Alliances

Source: Booz • Allen & Hamilton

GLOBAL CORE

GLOBAL CORE

Capabilities Strategic Leadership

Capital

Control

Identity

Exhibit 16. Centerless Corporation Missions

Source: Booz • Allen & Hamilton

19

Alliances as a CoreCompetency

Regardless of which ofthe four “pure tones” isappropriate for your

company, you will no doubt becompelled to form multiple kindsof alliances. You will need tohave a disciplined process thathelps you decide what type ofalliance is optimal in a particularsituation, and then adapt theprocess to the particular type of alliance.

Pragmatic executives areoften suspicious, and rightly so,about simple formulas. Some

executives even maintain that“seat-of-the-pants” managementand pure luck play an importantrole in any alliance. We agree thatluck always helps a businessalliance succeed. However, ourstudies show, and experiencedalliance practitioners will tell you,that the chances of alliance suc-cess without experience, learningand best practice adoption are, atbest, only one out of five.

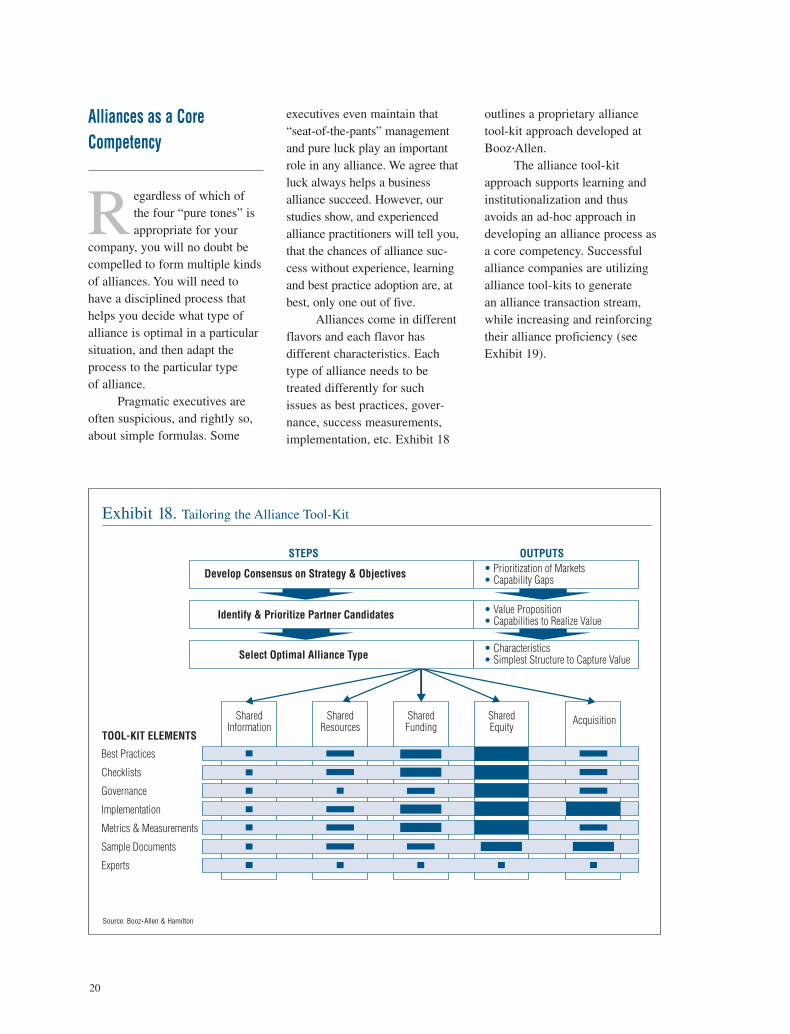

Alliances come in differentflavors and each flavor has different characteristics. Eachtype of alliance needs to be treated differently for such issues as best practices, gover-nance, success measurements,implementation, etc. Exhibit 18

outlines a proprietary alliancetool-kit approach developed atBooz •Allen.

The alliance tool-kitapproach supports learning andinstitutionalization and thusavoids an ad-hoc approach indeveloping an alliance process asa core competency. Successfulalliance companies are utilizingalliance tool-kits to generate an alliance transaction stream,while increasing and reinforcingtheir alliance proficiency (seeExhibit 19).

20

STEPS OUTPUTS

SharedInformation

Best Practices

Checklists

Governance

Implementation

Metrics & Measurements

Sample Documents

Experts

SharedResources

SharedFunding

SharedEquity

Acquisition

Develop Consensus on Strategy & Objectives • Prioritization of Markets• Capability Gaps

• Value Proposition• Capabilities to Realize Value

• Characteristics• Simplest Structure to Capture Value

Identify & Prioritize Partner Candidates

Select Optimal Alliance Type

TOOL-KIT ELEMENTS

Exhibit 18. Tailoring the Alliance Tool-Kit

Source: Booz • Allen & Hamilton

Summary

Global industry hasentered an unprece-dented era of structural

change. Not since the industrialrevolution have new technologydevelopment and adoption, rapidmarket expansion and revolution-ary business processes invadedmanagerial space with such viru-lence. The old “command andcontrol” model that has worked

successfully for nearly two cen-turies is now challenged by “TheAllianced Enterprise.” This neworganizational ecosystem is morerobust than what it replaces. Thisecosystem places a high premiumon growth, market leadership andcapability absorption — and itdelivers results. Leading edgecompanies are transforming theirorganizations and are reaping the benefits of this new businessmodel, and so should you.

21

PerformInventory

Diagnostic &Benchmark

AllianceCapabilityBuilding—

Ongoing

BuildAlliance

Processes andCapabilities

IncorporateLearningsA

LL

IAN

CE

TO

OL

-KIT Strategy and

ObjectivesAlliance

ImperativesAlliance

Growth Engine

AlliancePortfolio/

Constellation

Portfolio/Constellation

Renewal

Alliance Transaction

Stream

Examplesfor

Training

EXECUTION

C A P A B I L I T Y R E N E W A L

Exhibit 19. Building an Alliance Capability

Source: Booz • Allen & Hamilton

What Booz•Allen Brings

Booz •Allen & Hamilton isa global management andtechnology consulting

firm, owned by its partners, all ofwhom are officers in the firm andactively engaged in client service.As world markets mature, andcompetition on an internationalscale quickens, our global per-spective on business issues growsincreasingly critical. In more than90 countries, our 9,000 profes-sionals serve the world’s leadingindustrial, service and govern-ment organizations. Each mem-ber of our multinational team hasa single, common goal— to helpevery client achieve and sustainsuccess.

Our broad experienceincludes the world’s major busi-ness and industrial sectors: aero-space, agriculture, airlines, auto-motive, banking, basic metals,chemicals, construction, con-sumer goods, defense, electron-ics, energy, engineering, foodservice, health care, heavy indus-try, insurance, oil and gas, phar-maceuticals, publishing, railways,steel, telecommunications, tex-tiles, tourism, transportation andutilities.

With our in-depth under-standing of industry issues andour expertise in strategy, systems,operation and technology, we

assist our clients in developingthe capabilities they need to compete and thrive in the globalmarketplace.

We judge the quality of our work just as our clients do — by the results. Their confi-dence in our abilities is reflectedin the fact that more than 85% of the work we do is for clientswe have served before. Since our founding in 1914, we havealways considered client satisfac-tion our most important measureof success.

Booz•Allen & Hamilton hasextensive experience assistingclients throughout the process ofstrategic alliance formulation,including vision definition, iden-tification of critical capabilities,screening for partners, evaluatingpriority partners, negotiating andimplementing alliances. We worktogether with our clients in fourways to help them improve theirperformance in alliances:• Strategy (explicit alliancestrategy formulation): Assistingclients to identify the alliancepotential of their business,exploring traditional and non-traditional alliances, as well asthreats posed by pre-emptivealliance plays.• Alliance Formulation (transactions): Working togetherwith a client on specific alliances,at individual stages in the processor throughout the process.

• Process (institutionalizingalliance capabilities): Assistingclients to build and improve theirunderlying capabilities in identi-fying, evaluating, negotiating,implementing and managingalliances — based on our bestpractices frameworks andmethodology.• Alliance Portfolio Renewal:Revitalizing a client’s portfolio ofexisting alliances by involvingthe client’s current partners in aneffort to improve performance ofthose alliances — by tuning themup and reinvigorating them.

We couple the understand-ing from our industry practiceswith our functional expertise inalliances and our geographicalfootprint to help our clientsachieve superior results in theiralliance efforts.

We work with the full rangeof clients in terms of theiralliance sophistication. We helpcurrent alliance leaders advanceto the next level, as well as helpcompanies inexperienced inalliances get established in build-ing core capability.

Our book, Smart Alliances,is the top-selling alliance book,and we host the leading websiteon the topic (www.smartalliances.com), as well as the leading annual conference on allianceswhich we co-sponsor with TheConference Board.

22

23

John R. Harbison, Vice Presidentof Booz •Allen based in LosAngeles, leads the firm’s StrategicAlliances practice, and special-izes in strategic alliances, acqui-sitions and post-merger integration. He is co-author,with Peter Pekar, of SmartAlliances: A Practical Guide toRepeatable Success, which is thebestseller of the 110 books onalliances sold by Amazon.com.

Peter Pekar, Jr., Ph.D., VisitingAssociate Professor at the LondonBusiness School, is a recognizedexpert in the area of strategicalliances, with 30 years of busi-ness experience in forming andmanaging alliances. He has writ-ten more than 40 articles onalliances and related subjects andis a Senior Advisor to Booz •Allen.

Albert Viscio, Vice President of Booz •Allen based in SanFrancisco, specializes in organization and leadership,and is co-author of the book The Centerless Corporation.

David Moloney, Principal ofBooz •Allen and based in Sydney,specializes in alliance-enabledstrategy formulation and e-Business.

Other titles in Booz •Allen’sStrategic Alliances Viewpointseries:

1) A Practical Guide toAlliances: Leapfrogging theLearning Curve (1993)

2) Cross-Border Alliances in theAge of Collaboration (1997)

• An Asian Perspective on Cross-Border Alliances:Different Dreams (1997)

• Betting on Stability andGrowth: Strategic Alliances in Latin America (1997)

3) Institutionalizing AllianceSkills: Secrets of RepeatableSuccess (1997)

4) Making Acquisitions Work:Capturing Value After the Deal(1999)

For more information, contact:

John R. HarbisonVice PresidentBooz •Allen & Hamilton Inc. 5220 Pacific Concourse DriveSuite 390Los Angeles, CA 90045310-348-1900E-mail: [email protected]

Web site: www.smartalliances.com

Worldwide Offices

Abu DhabiAmsterdam

AtlantaAucklandBangkok

BeirutBogotáBoston

Buenos AiresCaracasChicago

ClevelandDallas

DüsseldorfFrankfurt

Hong KongHoustonJakartaLima

LondonLos Angeles

MadridMcLean

MelbourneMexico City

MilanMunich

New YorkParis

PhiladelphiaRio de Janeiro

RomeSan Diego

San FranciscoSantiago

São PauloSeoul

SingaporeSt. Louis

StockholmSydneyTokyoViennaWarsaw

Washington, D.C.Wellington

Zürich

CORP 215 5M:3/00 PRINTED IN USA