the antebellum financial system november 13, 2007

TRANSCRIPT

The Antebellum Financial System

November 13, 2007

Origins of US Money and Banking: Why do we have bank?

• Supply credit

• Keep assets safe

Origins of US Money and Banking: Forms of Money

• Specie – precious metals such as gold and silver

• Paper money – banknotes supplied by banks

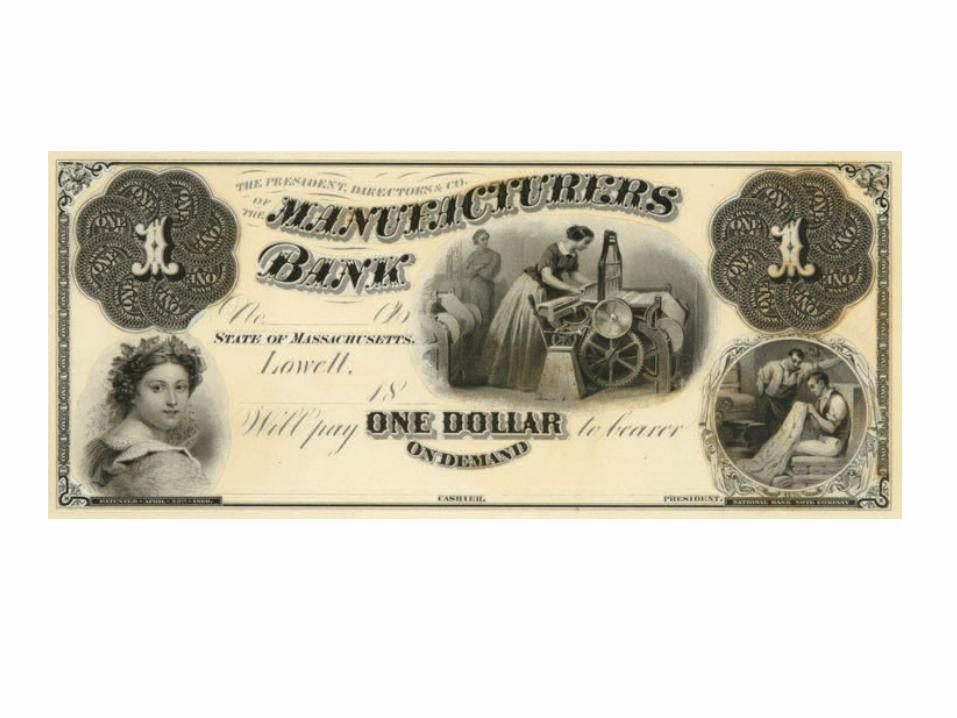

Origins of US Money and Banking: Origins of paper money

• Example: Suppose you are a shopkeeper and you want to stock a six month supply of pots and pans in your store.

• You give a $500 promissory note to a local banker

• The banker charges you a 3% interest rate for 6 months (6% per annum) and gives you $485 in banknotes

Origins of US Money and Banking: Origins of paper money

• You travel to the city to buy $485 worth of pots and pans from the wholesaler

• You return to your retail shop and sell the pots and pans over the next 6 months

• After the 6 months you pay $500 to the banker

Origins of US Money and Banking: Origins of paper money

• The wholesaler pays himself, his workers, and his suppliers with the banknotes.

• The banknotes circulate in the economy as money

• At some point the banknotes return to the original banker for redemption

Origins of US Money and Banking: Origins of paper money

• Why did the shopkeeper use banknotes instead of specie to buy his pots?

• Why did the wholesaler accept the banknotes?

Origins of US Money and Banking: Skepticism of Early Banks

• Do you think the bank backed up his banknotes one-for-one with specie in his bank?

• Bankers only held enough specie to cover the expected redemption of banknotes

• This fractional reserve system allows bankers to generate more profits through extending credit

Origins of US Money and Banking: Skepticism of Early Banks

• The perception was that bankers were greedy and were increasing the money supply and causing rapid inflation by printing too many bank notes

• This is not credible because most bankers self-regulated. Their business depended on their ability to convert!

Origins of US Money and Banking: Price Levels in the Antebellum Period

• Four periods of inflation• 1790s – very few banks; probably due to

high demand of American exports• War of 1812 – still very few banks; war

financing• 1830s – large imports of silver from

Mexico, i.e. increase in the monetary base• 1850s – large increases in the specie

stock, this time from California

The First and Second Banks of the United States

• First attempts at Central Banking

• First Bank of the United States: 1791 – 1811

• Second Bank of the United States: 1816 - 1836

The First and Second Banks of the United States

• Functions:

• Receive payments to the government

• Kept monetary base in check

The First and Second Banks of the United States: Why did they fail?

• Perceived as anti-business – no cheap credit

• Possibly unconstitutional

• “privileged monopoly”

• Banks were distrusted in general

Institutional Innovation in Absence of Central Bank

• Suffolk Bank of Boston served as regional bank in New England

• Controlled New England money supply

• Required smaller out-of-town banks to keep deposits in order to keep their banknotes convertible in Boston

• New England never needed to suspend convertibility

Institutional Innovation in Absence of Central Bank

• New York – deposit insurance scheme

• New York Free Banking Act of 1838

Institutional Origins of Savings Banks

• Two purposes of banks: provide credit and provide safe place to store assets

• Prior to banks, where did people keep their money?

• Before the Industrial Revolution, was there a pressing need for banks to deposit cash wages?

Institutional Origins of Savings Banks

• “Philanthropic” banks for the poor and working class

• First bank chartered in Boston in 1816

• Trustees volunteered their time to run bank and make investment decisions

• Poor and working class depositors earned dividends on deposits

Savings Banks: Why start a savings bank? Who benefits?

• Savers benefit

• Savings banks provided a relatively safe place to deposit wages

• Savers earned substantial dividends from investments

Savings Banks: Why start a savings bank? Who benefits?

• Do the bank trustees benefit?• Philanthropic motive?• Philanthropy is a poor economic reason to run a

bank• Personal gain?• Trustees could not profit directly from

investments, but…• Trustees could direct investments into projects

that benefit them directly or indirectly

Savings Banks: Why start a savings bank? Who benefits?

• Example: New York savings banks

• New York government restricted savings bank investments to state bonds

• Bonds were used to finance large infrastructure projects, i.e. Erie Canal

• Result: savings banks located along Erie Canal

New York Savings Banks, 1819 - 1834

- One Savings Bank

- Multiple Savings Banks4

4New York City

Rochester Area Albany Area

New York Savings Banks, 1819 - 1834

- One Savings Bank

- Multiple Savings Banks

- Erie Canal

4

4New York City

Rochester Area Albany Area

Savings Banks: Legacy

• Opened up formal financial intermediation to the working class

• Freed up new sources of financial capital for investments

• Provided investment funds for important public infrastructure projects