the australian conservation foundation submission to...

TRANSCRIPT

1 | P a g e

08 March 2018

The Australian Conservation Foundation

Submission to the Energy Security Board

on the National Energy Guarantee

2 | P a g e

Key ACF Recommendations:

• Ensure that the NEG meets the key policy tests set out in Box 1 below.

• Make the electricity sector play a leading role in climate pollution reduction and set an

electricity emissions target that is genuinely aligned with Australia’s Paris commitment to keep

global warming below 1.5-2 degrees. This requires a trajectory that achieves net zero

greenhouse pollution across the economy before mid-century.

• Ensure that any integrated climate and energy policy encourages investment in new clean,

renewable energy and acts as a floor, not a ceiling on further growth.

• Ensure each successive emissions reduction target is required to be stronger than the last and

no backsliding is allowed.

• Set five-year notice periods with rolling target updates on an annual basis.

• State schemes should be treated as additional to the national electricity emissions reduction

target. At a minimum any NEM-wide emissions or renewable target must meet or exceed the

aggregate of state and territory targets.

• Do not exempt EITE activities from the emissions guarantee obligation.

• Retailers should not be able to use offsets as a flexible option to meet the emissions

requirement.

• Ensure that the design of the mechanism does not add unnecessary complexity and/or cost for

either the administrators or those carrying the obligation. Contract options must not unfairly

burden second and third tier retailers or contribute to further concentration of market power.

• Consider making use of existing reporting structures under the RET and National Greenhouse

and Energy Reporting Scheme.

• Ensure that voluntary actions including GreenPower purchases are treated as additional to the

emissions reduction target.

• Ensure that policies relating to reliability of electricity supply are in the common interest,

clearly meet a demonstrated need, and support a transition away from coal and gas to zero

greenhouse pollution options such as renewable energy, storage and demand response.

3 | P a g e

Introduction

Any climate and energy policy mechanism, whether it be a National Energy Guarantee, Clean Energy

Target, Emissions Intensity Scheme, or other mechanism must at a minimum be effective in reducing

climate pollution, efficient, fair, durable and meet the tests outlined in Box 1: Key Energy Policy Tests

below.

Please note that this Australian Conservation Foundation submission is complemented by a Climate

Action Network Australia (CANA) submission that includes these policy tests, and which ACF has also

signed.

International Context

The Paris Climate Agreement set the world on a path to keep global warming to less than 2°C and to

pursue efforts to limit the increase to 1.5° C. It also set up a long-term goal of achieving net zero carbon

pollution within the second half of the century with an earlier goal to achieve global peaking of

greenhouse gas emissions as soon as possible.

Australia is currently out of sync with these goals. The Australian government’s 26 to 28 per cent carbon

pollution reduction target based on 2005 levels by 2030 is in line with 3°C to 4°C of warming should

other governments commit to similar levels of ambition.1

The most recent quarterly report of Australia’s National Greenhouse Gas Inventory showed that

Australia’s carbon pollution is moving in the wrong direction—carbon emissions are going up. The

government’s Emissions Reduction Fund has not resulted in an overall reduction to Australia’s carbon

emissions, and the current Safeguard Mechanism is not set up to reduce emissions or to impact the

nation’s biggest polluters.

Australia’s increasing carbon pollution is occurring alongside growing indications that global warming is

reaching emergency levels.2 This has been evidenced through record-breaking heat; some of the worst

coral bleaching in history, which has impacted 93 per cent of the Great Barrier Reef; dangerous sea level

rise that is already resulting in climate refugees from low lying Pacific island nations; a growing reduction

1 http://www.climateinstitute.org.au/articles/media-releases/paris-agreement.html 2 http://www.theguardian.com/environment/planet-oz/2016/mar/18/welcome-to-the-climate-emergency-youre-about-20-years-late and http://climatenewsnetwork.net/past-emissions-force-faster-climate-change/

4 | P a g e

in Antarctic icesheets and atmospheric carbon dioxide readings now above 400 parts per million at

Tasmania’s Cape Grim monitoring station—a dangerous threshold that is now a reality.

Emissions requirement: Commonwealth Government design elements

Setting the electricity emissions target and review process

Recommendation: Make the electricity sector play a leading role in climate pollution reduction

and set an electricity emissions target that is genuinely aligned with Australia’s Paris commitment

to keep global warming below 1.5-2 degrees. This requires a trajectory that achieves net zero

greenhouse pollution across the economy before mid-century.

Electricity generation is Australia’s largest source of greenhouse pollution. Furthermore, the use of dirty

energy makes a range of other sectors such as transport, industrial processes and agriculture much more

polluting than necessary.

The role of the electricity sector in greenhouse gas reduction targets is crucial, a fact recognised by the

Climate Change Authority when it notes that the sector is “both the largest source of emissions and a

significant source of emissions reduction opportunities”3. It also potentially plays a crucial role in

supporting emissions reduction strategies in other sectors, such as transport, which are likely to be highly

dependent of electricity driven technologies to reduce emissions.

Therefore, reducing the electricity generation sector’s emissions is an essential element of any credible

carbon reduction policy.

The same CCA report recommends the introduction of emissions intensity reduction scheme to reduce

the emissions of the sector to net zero “well before 2050”, a target which is necessary in order meet

Australia’s international commitments and the global target of zero net global emissions by the second

half of the century4.

It is the opinion of ACF that any decisions relating to structure and design of the NEG must be framed by

the longer-term goal of achieving net zero emissions in the electricity sector to enable net zero emissions

from the entire energy sector well before 2050. Australia has made commitments internationally to

pursue a 1.5-2 degree limit on global warming and to be part of a process to ratchet up Australia’s 2030

3 Climate Change Authority, Towards a Climate Policy Toolkit: Special Review on Australia’s Goals and

Policies, August 2016, p.7 4 Climate Change Authority, Towards a Climate Policy Toolkit: Special Review on Australia’s Goals and

Policies, August 2016, p.21

5 | P a g e

pollution reduction target through 5 yearly reviews. Policy decisions and market design must be

informed by that commitment and ultimately the need to achieve zero emissions in the energy sector.

Modelling by the Institute of Sustainable Futures has also verified that a transition to 100 per cent

renewable energy within one generation is technically feasible and economically responsible.5 Similarly

the AEMO itself has confirmed that the National Electricity Market can operate with 100 per cent

renewable energy while meeting the current National Electricity Market reliability requirement.6 In other

words, 100 per cent renewable energy can meet the energy needs of the NEM 99.998 per cent of the time.

There are at least 9 publications that indicate the feasibility of transitioning to 100% renewable energy

(and several provide roadmaps to do so). Three such publications are listed below:

• Energy Networks Australia and CSIRO’s Electricity Network Transformation Roadmap contains a

comprehensive roadmap to 100% renewable energy by 2050

• GetUp And Solar Citizens’ Homegrown Power Plan.

• Beyond Zero Emissions and Melbourne Energy Institute’s Zero Carbon Australia Stationary

Energy Plan.

These publications along with the anecdotal experience of countries aiming for high levels of renewable

energy suggest that a zero-emissions generation sector, providing affordable and reliable energy, is

technically feasible as the costs of renewable energy and storage technology continues to fall, though it is

not necessarily easy and the need for specific policy interventions and market design is clear. The main

barriers have been and are likely to be political rather than technical or financial.

Impact of the proposed NEG on renewable energy

Recommendation: Ensure that any integrated climate and energy policy encourages investment in

new clean, renewable energy and acts as a floor, not a ceiling on further growth.

The proposed NEG is forecast to deliver more carbon pollution and less renewable energy than if the

government did not implement the NEG. Please see Table 1 below. The proposed NEG risks derailing

Australia’s current growth in renewable energy and storage.

Table 1: Renewable energy projections for 2030

Source Projection Renewables in 2030

5 The Climate Institute, A Switch in Time: Enabling the electricity sector’s transition to net zero emissions, April

2016 6 Australian Energy Market Operation 2013, 100 per cent Renewable Study: Modelling Outcomes, July 2013

6 | P a g e

Energy Security Board (ESB) Forecast levels of renewables

under the NEG

28-36% renewables

Finkel Review Modelling of business-as-

usual

35% renewables

Finkel Review Modelling of the

Commonwealth Government’s

climate targets (26-28%

below 2005 levels by 2030)

applied equally across all

sectors

42% renewables

RepuTex, Jacobs Applying a least-cost

approach to meeting

Commonwealth Government’s

climate targets i.e., reducing

electricity sector emissions by

40-55% on 2005 levels

66-75% renewables

For the forecast under the NEG to be correct, the growth of renewable energy in Australia would have to

slow rapidly relative to current trends - according to Kane Thornton from the Clean Energy Council,

perhaps by more than half.

This curb on renewable energy would be impacted by the government’s extremely low emissions

reduction target. Beyond that, a policy mechanism such as the NEG that avoids a carbon price, and is

likely to have a negative effect on competition in wholesale and retail markets also runs the risk of

reducing investment efficiency and hence delivering less renewables capacity per quantum of investment.

Because the emissions guarantee is more indirect and inefficient than for example other versions of an

Emissions Intensity Scheme (EIS), increased emissions targets would be likely to be costlier than a similar

increase under a different mechanism. As an example, the Clean Energy Target (CET) made higher targets

more affordable because it placed greater downward pressure on wholesale prices.

7 | P a g e

Timing and process for setting electricity emissions targets

Recommendations:

• Ensure each successive emissions reduction target is required to be stronger than the last

and no backsliding is allowed.

• Set five-year notice periods with rolling target updates on an annual basis.

The goal of ensuring investment certainty through a durable mechanism and predictable targets is

important. But, the target proposed is unreasonably and unacceptably low. Without a credible target that

genuinely lines up with Australia’s 1.5-2-degree commitment, a high risk remains that the current target

will need to be changed prior to 2030. The ACF does not support locking in the current, unreasonably

low target for a 10-year period (2021 to 2030).

There must be flexibility to increase ambition while still maintaining sufficient certainty for investors.

Therefore, the ACF supports five-year notice periods. However, the ACF prefers rolling target updates

that maintain a five-year notice period but allow annual updates to provide flexibility. This would allow

for increased ambition to take advantage of constantly evolving clean energy technologies and new

innovative solutions.

Consistent with the Paris Agreement and the need to rapidly cut carbon pollution, it must be a

requirement that each successive target is stronger than the last, and there is no tolerance for backsliding.

Geographic neutrality (and Jurisdictional considerations)

Recommendation: State schemes should be treated as additional to the national electricity

emissions reduction target. At a minimum any NEM-wide emissions or renewable target must

meet or exceed the aggregate of state and territory targets.

Any effort to achieve a nationally coordinated and consistent approach to reducing emissions in the

electricity sector must not reduce state and territory ambition to the lowest common denominator. This

lowest common denominator is currently the national electricity emissions reduction target. State

governments that have chosen to act responsibly to reduce climate pollution and to grow the contribution

of renewable energy investment in their jurisdiction should not have their ability to take stronger climate

action reduced, nor should their ability to meet their renewable energy targets be negatively impacted by

national policy.

8 | P a g e

Treatment of EITE activities

Recommendation: Do not exempt EITE activities from the emissions guarantee obligation.

EITE industries should not be exempt from the emissions requirement of the NEG. An exemption would

not be fair, it would not ensure EITE industry competitiveness, and it would not be in the best interest of

Australia’s energy transition.

EITE industries have previously been successful in making the case that because they compete in

international markets, they would be disadvantaged if emissions-related policy mechanisms such as the

carbon price or the RET were applied to them. They were given exemptions in both cases. As a result,

some of our most polluting industries have been free to pollute without penalty or incentive to find

cleaner solutions. They have been relieved of carrying their fair share of Australia’s pollution reduction

burden, and that burden has instead been increased for others. This is inherently unfair. Other businesses

and households carry a higher burden and this includes Australia’s most vulnerable households.

The vast majority of countries around the world, including competing economies and trading partners,

are Parties to the Paris Climate Change Agreement. As such, they have also committed to keep global

warming to 1.5-2 degrees and are on a path to emissions reduction. Their EITE industries are subject to

pollution reduction policies.

It is no longer a reasonable argument that some sectors should be exempt because they will be at a

competitive disadvantage. If anything, industries actively preparing for a lower emissions future will be

more competitive. In addition, emissions intensive industries are big energy users and have an important

role to play in providing on-site and decentralised clean electricity generation and storage as well as

demand management.

External Offsets

Recommendation: Retailers should not be able to use offsets as a flexible option to meet the

emissions requirement.

Retailers should not be able to use offsets external to the electricity sector as a flexible option to meet the

emissions requirement.

Solar PV and wind energy with firming capacity are now cheaper for new build generation than coal or

gas. Battery storage technology costs are dropping rapidly. There are enough pumped hydro sites around

the country to couple with. wind and solar PV to manage a full transition to 100% clean energy7. Both

energy efficiency and demand response are largely untapped opportunities for low cost, readily available

7 Andrew Blakers, 100% Renewable Electricity in Australia, February 2017

9 | P a g e

solutions to reduce emissions in the electricity sector. There is no need to provide offsets when excellent

zero emission options are readily available in the electricity sector and it is a sector that must be

decarbonised to enable additional emissions reduction through electrification. Reliance on offsets would

unnecessarily reduce the growth of renewable energy and that is the opposite of what’s needed.

Emissions requirement: Energy Security Board design elements

Applying the emissions requirement

The fundamental design of the NEG is a concern, as it places the obligation on retailers to ensure that the

average emissions intensity of the electricity they sell does not exceed a target level. The proposed

system appears impractical and hard to administer.

The following extract from A description and critique of the National Energy Guarantee prepared for the

Australian Conservation Foundation by Bruce Mountain of CME outlines some key issues.

The NEG was introduced after the Government rejected the key recommendation of the Finkel Review

to establish a Clean Energy Target. In its place, the NEG imposes an obligation on retailers to ensure

that the average emission intensity of the electricity they sell does not exceed a target level. It also

obliges retailers to procure “dispatchable” power.

We have many concerns with this approach:

• Firstly, a critical issue hiding in plain sight and not yet widely understood is that establishing

retailers’ emission intensity will require that they are able to identify which generators produce the

electricity that they sell. This means that the existing mandatory spot market – which does not

identify which generators are used to supply the electricity that retailers buy from the spot market

– will need to be disbanded. Disbanding the spot market and its settlement systems and also

terminating financial contracts that are struck relative to the prices in this mandatory spot market

will require many years to complete and will result in transition costs in the hundreds of millions of

dollars.

• Second we do not believe that the NEG will establish an effective market in emission reduction. The

stated purpose of the policy is to not establish a price on emissions. The absence of an emission price,

makes it harder for buyers and sellers to find each other and to find prices that they are willing to

trade at. The resulting transaction costs and illiquidity undermines operational and investment

efficiency. This makes the task of emission reduction more costly than it would be if mechanisms

were designed with the intention of ensuring an efficient and transparent market. While customers

are the common losers from this approach, it does nonetheless provide a relative advantage for

incumbent vertically integrated producers relative to smaller new entrant generators and

10 | P a g e

retailers.

• Third the implementation of emission intensity obligations on retailers will require a large

bureaucracy to account for all electricity produced by generators and sold by retailers and to

account for the contracts between generators and retailers, between generators and generators,

and between retailers and retailers. It is only with such accounting that the retailers’ emission

intensity claims can be verified.

• Fourth with respect to the dispatchability obligation, this inserts retailers between the producers

of power system services (the generators, flexible load and storage providers) and the consumer of

these services (the Australian Energy Market Operator). Contrary to the stated purpose of this

obligation, it will undermine power system security by introducing needless complexity and

bureaucracy.

We conclude that the NEG is likely to deliver outcomes that will protect coal generators from

competition provided by renewables and batteries and will undermine the efficiency of investment in

renewable generation capacity. It can be no surprise that there is no evidence in Australia or

internationally of an approach similar to the NEG having ever been implemented or even proposed.

What are stakeholders’ views on how a retailer’s emissions should be determined?

Recommendation:

• Ensure that the design of the mechanism does not add unnecessary complexity and/or cost

for either the administrators or those carrying the obligation. Contract options must not

unfairly burden second and third tier retailers or contribute to further concentration of

market power.

• Consider making use of existing reporting structures under the RET and National

Greenhouse and Energy Reporting Scheme.

The possible methods for calculating retailers’ emissions as outlined in section 3.2.3 of the consultation

paper appear fraught with complexity and raise serious concerns about the accuracy with which

emissions intensity can be determined for retailers, transparency and the burden of tracking, managing

and enforcing the obligation. The fundamental design of the emissions guarantee—with the obligation

based on retailers that buy from the market—makes emissions intensity difficult to track efficiently and

effectively.

Three types of contracts are outlined in section 3.3 that retailers could potentially use to achieve

compliance with the emission requirement. Contracts that specify a generation source appear the most

straightforward, but even these contracts are not standardised or a fully reliable means of accounting for

11 | P a g e

emissions intensity. The other two options are not straightforward at all. As acknowledged, contracts that

specify the emissions per MWh but not a generation source do not currently exist. It’s unclear how

emissions intensity could be reliably determined through contracts that pool together several generators

with similar emissions within a region. The record keeping obligation required to track emissions

associated with each MWh generated by each relevant plant appears very significant and resource

intensive.

Even more concerning is the scenario outlined in section 3.3.3 where contracts that specify neither

emissions per MWh nor a generation source might be used to determine retailers’ emissions. In this

scenario, the potential is raised for all types of contracts sold in a particular region to be ‘deemed’ to have

the same emissions level based on the previous year’s levels. This raises serious concerns about achieving

accurate reporting, the ability to adjust to specific changes in emissions intensity (if regionally based and

blended), and a potential lack of transparency.

The complexity and burden that the emissions guarantee would impose broadly on retailers is a

particular concern for smaller retailers and for market competition. Complexity would also add cost to

the overall administration of the policy.

The complexity of the most direct option (contracts that specify a generation source) is shown in a short

case study by Bruce Mountains, inserted as Box 1 below, which highlights these issues.

Box 1: Short case study: Contracts that specify a generation source (extracted from case

study by Bruce Mountain, CME)

When figuring out policy it’s good to get down to brass tacks. So for the purpose of trying to understand how the NEG might actually work (or not) let’s explore one of the contract options described in the latest NEG document, that purports to explain how retailers can contract to meet their emission reduction obligations. Specifically, let’s take the case that a retailer enters into a contract for production from a specified source with known emission intensity. For argument’s sake, let’s say a contract between AGL and Origin for the sale of 300 MW from unit 1 of Loy Yang A for the 8784 hours in the year 2020. For argument’s sake, let’s say the emission intensity of this unit is 1.3 tonnes of CO2-equivalent per MWh, and Origin agrees to pay AGL $60/MWh for the electricity produced by unit 1 of Loy Yang A. Now of course Loy Yang A like other generating units is very unlikely to be able to produce 300 MW for every hour in 2020 as it contracted to. Let’s say it only produced for 85% of those hours: it lost 5% for forced outages, 5% for planned outages and 5% because it offered its production in to the NEM at a price that was higher than the clearing price and so AEMO did not dispatch it.

12 | P a g e

Now, what happens for the 15% of the time (1137 hours) that Loy Yang A unit 1 did not meet the contractual commitment to sell 300 MW to Origin? In the NEM, Origin will still be supplied by the NEM (the shortfall will come from some other source). But the contract between Origin and AGL will mean that there will be a side payment between and Origin and AGL so that the $60/MWh price is honoured for that shortfall. So far, so good. But what about the emission intensity of that 15% shortfall? Origin (and AGL) has to know which generating units actually supplied the shortfall when unit 1 did not produce. It could be a bunch of wind farms with zero emissions. In this case in recording the emission intensity of the electricity that Origin got from AGL it would be 85% of Loy Yang A’s emission intensity plus 15% of zero (for the wind). But if instead it was Yallourn that made up the shortfall then Origin’s emission position would look much worse (85% of Loy Yang A plus 15 % of 1.5 tonnes CO2-e /MWh from Yallourn). Now Origin has powerful incentives to argue that it was wind farms that made up the shortfall (since this would reduce the emissions counted in their name). But it can not just be left to Origin to say this – all the retailers have an incentive to argue that they got their electricity from the lowest emission source. Obviously this can not be settled on the basis of some argument: there has to be a verifiable basis of figuring out the emission intensity of the electricity that made up for Loy Yang A’s shortfall. Now this is the crux of the matter: How can you possibly work out the emission intensity of that shortfall? The answer is that some entity (the AER according to the NEG) must be in a position to know the emissions of all generators that produced during every five minute trading interval that Loy Yang did not produce (that's the easy bit). But the AER must also know all contracts entered into by all generators and all retailers for each five minute interval (so that it can allocate the generation contracted in each 5 minute trading interval to the retailers that contracted for it). Once the AER has done that accounting, they will be able to figure out which uncontracted generators were effectively selling the electricity that Origin bought when Loy Yang A failed. Now in any five minute trading interval you can expect there to be many contracts (probably counted in the thousands) between various generators and various retailers. This reconciliation will need to be done for every generator and every retailer in every five minute interval so that the AER can reconcile the emission intensity of the electricity sold by every retailer. The retailers can not do this reconciliation: it has to be a central agency that collects all the dispatch and contract information and continually does this giant reconciliation (and did I mention the complexities presented by distributed generation and inter-regional trade?). Now while writing this I can sense your hands starting to wave about: but surely the AER can just use some sort of average regional emission intensity? No it can’t! If a retailer contracts to buy electricity from a specific generator, the emissions (and production) of that generator has to be accounted for specifically by the parties to that contract, and it has to be netted off to work out the emission intensity of the remaining production in every 5 minute trading interval. And retailers will have to enter into such bi-lateral contracts if they are to have an aggregate emission intensity that reduces below the average of the market (as it must for emissions to decrease in aggregate across the industry).

13 | P a g e

And if you think contracts in this new world are sacred to the parties, forget it: all contracts will have to be supplied to the AER. Lawyers’ picnic anyone? Now this is just the easy case of a contract for the purchase of production from a specific generating unit. The picture gets a whole lot more complex to work out the emission intensity to apply to financial contracts when a specific generating unit is not identified. This is not my nightmare: luckily I am not in the market. But if I was I would be getting mighty petrified – after all the Government promises to legislate on this in two month’s time.

Bruce Mountain, 15 February 2018

Interaction with voluntary ‘green’ programs

Recommendation: Ensure that voluntary actions including GreenPower purchases are treated as

additional to the emissions reduction target.

Many businesses, households and individual consumers choose to make a voluntary contribution to

reduce the greenhouse pollution related to their electricity use. This contribution, including GreenPower

purchases, must be additional to the government’s emissions requirements. The NEG design should not

allow voluntary GreenPower purchases to replace any amount of pollution reduction under the

government’s international commitments.

Reliability requirement

Recommendation: Ensure that policies relating to reliability of electricity supply are in the

common interest, clearly meet a demonstrated need, and support a transition away from coal and

gas to zero greenhouse pollution options such as renewable energy, storage and demand

response.

The following points outlined in The Climate Council’s recent report: Clean, Reliable Power: Roadmap to a

Renewable Future summarise shared concerns and recommendations that ACF supports related to the

reliability requirement.

The NEG has misdiagnosed a reliability problem for the national energy grid [as] Australia’s power supply is highly reliable.

• The NEG’s proposed solution is to continue dependence on centralised coal and gas power plants, when the recent track record of these fossil fuel plants is anything but reliable.

• The Australian Energy Market Operator already has measures in place to ensure there is sufficient electricity supply to meet demand, and more reliability measures are on the way as adopted from the Finkel Review.

• Future reliability of supply requires forward planning to replace ageing, inflexible coal and gas plants with distributed renewable power and storage.

14 | P a g e

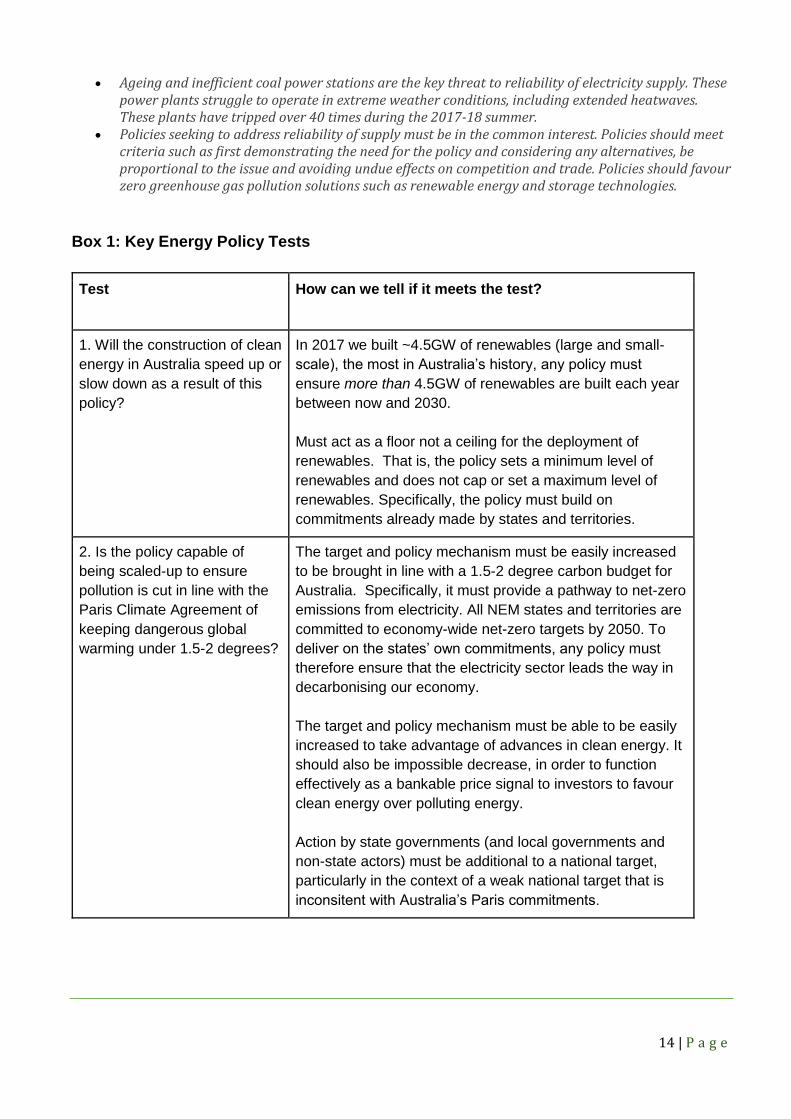

• Ageing and inefficient coal power stations are the key threat to reliability of electricity supply. These power plants struggle to operate in extreme weather conditions, including extended heatwaves. These plants have tripped over 40 times during the 2017-18 summer.

• Policies seeking to address reliability of supply must be in the common interest. Policies should meet criteria such as first demonstrating the need for the policy and considering any alternatives, be proportional to the issue and avoiding undue effects on competition and trade. Policies should favour zero greenhouse gas pollution solutions such as renewable energy and storage technologies.

Box 1: Key Energy Policy Tests

Test How can we tell if it meets the test?

1. Will the construction of clean

energy in Australia speed up or

slow down as a result of this

policy?

In 2017 we built ~4.5GW of renewables (large and small-

scale), the most in Australia’s history, any policy must

ensure more than 4.5GW of renewables are built each year

between now and 2030.

Must act as a floor not a ceiling for the deployment of

renewables. That is, the policy sets a minimum level of

renewables and does not cap or set a maximum level of

renewables. Specifically, the policy must build on

commitments already made by states and territories.

2. Is the policy capable of

being scaled-up to ensure

pollution is cut in line with the

Paris Climate Agreement of

keeping dangerous global

warming under 1.5-2 degrees?

The target and policy mechanism must be easily increased

to be brought in line with a 1.5-2 degree carbon budget for

Australia. Specifically, it must provide a pathway to net-zero

emissions from electricity. All NEM states and territories are

committed to economy-wide net-zero targets by 2050. To

deliver on the states’ own commitments, any policy must

therefore ensure that the electricity sector leads the way in

decarbonising our economy.

The target and policy mechanism must be able to be easily

increased to take advantage of advances in clean energy. It

should also be impossible decrease, in order to function

effectively as a bankable price signal to investors to favour

clean energy over polluting energy.

Action by state governments (and local governments and

non-state actors) must be additional to a national target,

particularly in the context of a weak national target that is

inconsitent with Australia’s Paris commitments.

15 | P a g e

3. Will it make everyday

Australians pay to keep

polluting power stations open

for longer?

The policy should not result in any subsidy to the owners of

coal and gas plants nor create an incentive to keep coal in

the mix longer.

The policy should bring on enough renewables, energy

efficiency and storage to ensure coal power stations can

shut down in a timeframe consistent with Australia’s Paris

commitments.

4. Will it concentrate market

power, or will it enable cleaner

competitors to enter the

market?

The policy should ensure that the majority of financial

benefit associated with the policies flows through to

consumers not the big gentailers.

The policy should lead to more competition in the retail and

generation market. This includes ensuring that small

renewable generators are easily able to secure a contract to

sell their electricity and small retailers are easily able to

meet their obligations to purchase clean power.

The public should be able to easily assess whether or not

the liable party (retailer or generator) are meeting their

obligations.

5. Does the policy lead to

emissions reductions in

Australia’s electricity sector?

The policy should not allow for offsets to replace emissions

reduction in the electricity sector. Doing so would slow

down the modernisation and decarbonisation of Australia’s

electricity sector.

6. Is the policy practical and

able to be implemented

efficiently?

The policy should not create unnecessary burdensome,

expensive, complexity when simpler solutions exist.

16 | P a g e

Will it concentrate market

power, or will it enable cleaner

competitors to enter the

market?

The policy should ensure that the majority of financial

benefit associated with the policies flows through to

consumers not the big gentailers.

The policy should lead to more competition in the retail

and generation market. This includes ensuring that small

renewable generators are easily able to secure a

contract to sell their electricity and small retailers are

easily able to meet their obligations to purchase clean

power.

The public should be able to easily assess whether or

not the liable party (retailer or generator) are meeting

their obligations.

Does the policy lead to

emissions reductions in

Australia’s electricity sector?

The policy should not allow for offsets to replace

emissions reduction in the electricity sector. Doing so

would slow down the modernisation and decarbonisation

of Australia’s electricity sector.

Is the policy practical and able

to be implemented efficiently?

The policy should not create unnecessary burdensome,

expensive, complexity when simpler solutions exist.

For more information:

Suzanne Harter | Climate Change and Clean Energy Campaigner | P: 03 9345 1208 | E:

The ACF community speaks out for a healthy environment, Australia's special places, climate action and for lasting

social and economic change.