the basicsfile/brgaap_vs... · and errors, cpc 26 presentation of financial statements 13 • cpc...

TRANSCRIPT

BRAZILIAN GAAPvs. IFRS

The BasicsSeptember 2010

Table of Contents

Introduction 04

Converged Standards

• Framework for the Preparation and Presentation of Financial Statements 06

• Accounting Standard for Small and Medium-sized Entities (CPCs for PMEs) 06

• CPC 01 (R1)- Impairment of Assets 07

• CPC 02 - Changes in Foreign Exchange Rates and Financial Statements Conversion 07

• CPC 03 - Statement of Cash Flows 08

• CPC 04 - Intangible Assets 08

• CPC 05 - Related Party Disclosures 08

• CPC 06 - Leases 08

• CPC 07 - Government Grants 08

• CPC 08 - Transaction Costs and Premium on the Issuance of Debt and Equity Instruments, CPC 38 Financial Instruments: Recognition and Measurement (supersedes CPC 14), CPC 39 Financial Instruments: Presentation, CPC 40 Financial Instruments: Disclosure 09

• CPC 10 - Share Based Payment 09

• CPC 11 - Insurance Contracts 09

• CPC 13 - First Time Adoption of Law 11,638, CPC 37 First Time Adoption of IFRS, CPC 43 Initial Adoption of Technical Pronouncements CPC 15 and 40 10

• CPC 15 - Business Combinations 11

• CPC 16 (R1) - Inventory 11

• CPC 17 - Construction Contracts, CPC 30 Revenue Recognition and CPC 01 Concession Contracts 11

BRAZILIAN GAAP vs. IFRS | Ernst & Young Terco2

• CPC 18 - Investments in Associates, CPC 19 Interests in Joint Ventures, CPC 35 Separate Financial Statements, CPC 36 (R1)Consolidated Financial Statements; ICPC 09 Individual Financial Statements, Separate Financial Statements and Consolidated Financial Statements and Equity Method 12

• CPC 20 - Borrowing Costs 12

• CPC 21 - Interim Reporting, CPC 22 Operating Segments, CPC 23 Accounting Policies, Changes in Accounting Estimates and Errors, CPC 26 Presentation of Financial Statements 13

• CPC 24 - Subsequent Events; ICPC 08 Accounting for the Payment of Proposed Dividends 13

• CPC 25 - Provisions, Contingent Liabilities and Contingent Assets 14

• CPC 27 - Property, Plant & Equipment, CPC 28 Investment Property, CPC 31 Non-Current Assets Held for Sale and Discontinued Operations, ICPC 01 Concession Contracts 14

• CPC 29 - Biological Assets 14

• CPC 32 - Income Taxes 15

• CPC 33 - Employee Benefits 15

• CPC 41 - Earnings per Share 16

Standards without a direct IFRS equivalent

• CPC 09 - Value Added Statement 17

• CPC 12 - Adjustments to Present Value 17

Areas for Future Consideration by the CPC

• CPC 34 - Exploration for and Evaluation of Mineral Resources 18

• CPC 42 Financial Reporting in Hyperinflationary Economies 18

• CPC 44 Combined Financial Statements 19

BRAZILIAN GAAP vs. IFRS | Ernst & Young Terco 3

BRAZILIAN GAAP vs. IFRS | Ernst & Young Terco4 BRAZILIAN GAAP vs. IFRS | Ernst & Young Terco

It is of no surprise today that many people who follow the development of worldwide accounting standards may well be confused. GAAP convergence is a high priority on the agendas of several countries and “convergence” is a term that suggests the elimination or coming together of differences.

In Brazil, a number of steps have been taken towards the use of International Financial Reporting Standards (IFRS), with two distinct but related paths to IFRS adoption being taken.

First, the Brazilian securities regulator, the Comissão de Valores Mobiliários (locally CVM) and the Brazilian Central Bank (locally BACON) have determined that IFRS should be used for consolidated financial statements of public companies

and companies regulated by BACON from 2010 onwards, with early adoption being permitted. Similar decisions will most likely be taken by the insurance regulator (locally SUSEP), meaning that insurance companies will also have IFRS reporting requirements from this date.

Secondly, a new corporate Law 11,638, which was enacted in 2007 and took effect in 2008, requires all Brazilian companies to prepare their financial statements in accordance with a new set of local standards which are currently being issued and are based on IFRS. This means that all Brazilian companies, both public and non-public, are currently required to use local standards which are identical to IFRS.

The local standards are being issued by Comitê de Pronunciamentos Contábeis (locally CPC), a newly established Brazilian

Introduction

BRAZILIAN GAAP vs. IFRS | Ernst & Young Terco BRAZILIAN GAAP vs. IFRS | Ernst & Young Terco 5

accounting standard setter. These new standards replace the existing accounting standards (Normas Profissionais de Contabilidade or NPCs issued by Instituto dos Auditores Independentes do Brasil – IBRACON) and other guidance issued by regulators. As of December 31, 2008, a total of fourteen CPC standards and 1 technical orientation (OCPC) had been issued and most of these were required to be applied to calendar year 2008. Since then, an additional 27 CPCs have been issued along with 14 interpretations (ICPC) and 2 technical orientations (OCPC). There are also 2 additional standards relating to the framework for preparing and presenting financial information and specific to small and medium sized entities. These new standards are required to be applied to calendar year 2010 and can be found online at www.cpc.org.br.

In this guide, “Brazilian GAAP vs. IFRS: The Basics”, we take a high level look into existing GAAP differences and provide an overview of where the standards are similar and where they diverge.

No publication that compares two sets of accounting standards can include all differences that could arise in light of the huge variety of business transactions that could possibly occur. The existence of any differences – and their materiality to an entity’s financial statements – depends on a variety of specific factors. This guide focuses on those differences most commonly found in present practices and, where applicable, provides an overview of how and when those differences are expected to converge.

We hope you find this guide a useful tool for that purpose.

Ernst & Young Terco September 2010

BRAZILIAN GAAP vs. IFRS | Ernst & Young Terco6 BRAZILIAN GAAP vs. IFRS | Ernst & Young Terco

As of September 2010, the CPC has issued forty-three accounting standards of which thirty-eight are essentially translations of the

equivalent IFRS standard. However, there are some subtle differences, usually due to addi-tional guidance or clarification being inserted

BR GAAP Standard IFRS Standard Significant Differences BR GAAP prior to CPC

Basic Concepts Framework for the Preparation and Presentation of Financial Statements

Framework for the Preparation and Presentation of Financial Statements

The Framework under BR GAAP contains differences from the IFRS Framework as it relates to items that are not allowed by Brazilian Corporate Law such as the revaluation of assets.

Prior to the framework, BR GAAP did not have a specific framework relating to financial statements. The framework formalizes certain items such as the definition of assets, liabilities, revenues and expenses and the concept of substance over form.

CPC PME Accounting Standard for Small and Medium-sized Entities (CPCs for PMEs)

The International Financial Reporting Standard for Small and Medium-sized Entities (IFRS for SMEs)

Both standards include criteria that entities must meet in order to utilize the pronouncement such as no public debt or equity and no fiduciary responsibilities, but the BR GAAP standard also includes specific size requirements which are consistent with Brazilian Corporate Law in order for an entity to qualify as an SME. In Brazil, an entity is qualified to use this standard as long as the specific criteria in the standard are met and its revenues are not greater than R$300 million and its total assets are not greater than R$240 million.

Prior to the accounting standard for SMEs, BR GAAP did not have a specific standard for small and medium-sized entities. This standard simplifies the requirements for entities that qualify as SMEs by omitting certain topics such as EPS and operating segments, removes and simplifies, options contained in the complete set of CPCs, simplifies recognition and measurement principles and reduces disclosure requirements.

Converged Standards

BRAZILIAN GAAP vs. IFRS | Ernst & Young Terco BRAZILIAN GAAP vs. IFRS | Ernst & Young Terco 7

BR GAAP Standard IFRS Standard Significant Differences BR GAAP prior to CPC

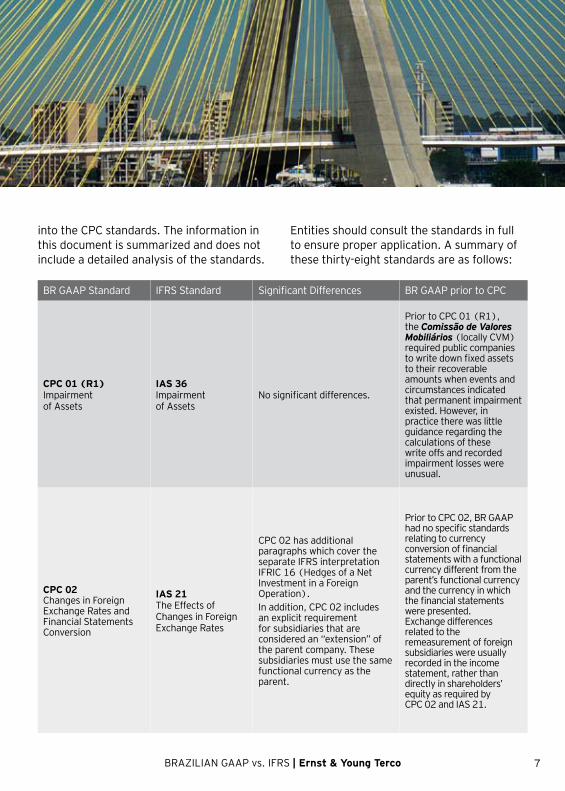

CPC 01 (R1) Impairment of Assets

IAS 36Impairment of Assets

No significant differences.

Prior to CPC 01 (R1), the Comissão de Valores Mobiliários (locally CVM) required public companies to write down fixed assets to their recoverable amounts when events and circumstances indicated that permanent impairment existed. However, in practice there was little guidance regarding the calculations of these write offs and recorded impairment losses were unusual.

CPC 02 Changes in Foreign Exchange Rates and Financial Statements Conversion

IAS 21 The Effects of Changes in Foreign Exchange Rates

CPC 02 has additional paragraphs which cover the separate IFRS interpretation IFRIC 16 (Hedges of a Net Investment in a Foreign Operation).In addition, CPC 02 includes an explicit requirement for subsidiaries that are considered an “extension” of the parent company. These subsidiaries must use the same functional currency as the parent.

Prior to CPC 02, BR GAAP had no specific standards relating to currency conversion of financial statements with a functional currency different from the parent’s functional currency and the currency in which the financial statements were presented. Exchange differences related to the remeasurement of foreign subsidiaries were usually recorded in the income statement, rather than directly in shareholders’ equity as required by CPC 02 and IAS 21.

into the CPC standards. The information in this document is summarized and does not include a detailed analysis of the standards.

Entities should consult the standards in full to ensure proper application. A summary of these thirty-eight standards are as follows:

BRAZILIAN GAAP vs. IFRS | Ernst & Young Terco8 BRAZILIAN GAAP vs. IFRS | Ernst & Young Terco

BR GAAP Standard IFRS Standard Significant Differences BR GAAP prior to CPC

CPC 03 Statement of Cash Flows

IAS 7 Statement of Cash Flows

No significant differences.

Prior to CPC 03, BR GAAP required a Statement of Changes of Financial Position (locally DOAR). Although not mandatory, the Statement of Cash Flows was considered supplemental information and was usually disclosed by public companies.

CPC 04 Intangible Assets

IAS 38 Intangible Assets

No significant differences.

Prior to CPC 04, there were no specific standards relating to intangible assets in Brazil. However, the concept of deferred assets under BR GAAP allowed entities to capitalize pre-operating expenses and research and development costs. Under CPC 04, many of these amounts can no longer be capitalized.

CPC 05 Related Party Disclosures

IAS 24 Related Party Disclosures

No significant differences.

Prior to CPC 05, certain related parties disclosures were required for public companies.

CPC 06 Leases

IAS 17 Leases

No significant differences.

Prior to CPC 06, all leases were normally treated for accounting purposes as operating leases and the expense was recognized at the time that each lease installment fell due. Disclosure regarding leases was limited.

CPC 07 Government Grants

IAS 20 Accounting for Government Grants and Disclosure of Government Assistance

CPC 07 includes examples specific to the Brazilian environment, as government grants are common in Brazil and take many forms.

Prior to CPC 07, government grants were usually recorded as a credit in shareholders’ equity rather than being recorded in the income statement immediately or over time, as appropriate.

Converged Standards

BRAZILIAN GAAP vs. IFRS | Ernst & Young Terco BRAZILIAN GAAP vs. IFRS | Ernst & Young Terco 9

BR GAAP Standard IFRS Standard Significant Differences BR GAAP prior to CPC

CPC 08 Transaction Costs and Premium on the Issuance of Debt and Equity Instruments;

CPC 38 Financial Instruments: Recognition and Measurement (replaces CPC 14);

CPC 39 Financial Instruments: Presentation;

CPC 40 Financial Instruments: Disclosure

IAS 32 Financial Instruments: Presentation;

IAS 39 Financial Instruments: Recognition and Measurement;

IFRS 7 Financial Instruments: Disclosures

No significant differences.

Prior to CPC 38, 39 and 40, certain financial instruments were classified as trading without considering whether or not they should be classified for available-for-sale or held-to-maturity.

There were no specific rules in regard to preference shares with debt characteristics, convertible debt, or puts and calls.

CPC 10 Share Based Payment

IFRS 2 Share Based Payment

No significant differences.

Prior to CPC 10, no amounts relating to share options were recognized. Certain disclosures were, however, required for public companies.

CPC 11 Insurance Contracts

IFRS 4 Insurance Contracts

No significant differences.

Prior to CPC 11, there was no specific guidance for embedded derivatives in insurance contracts. CPC 11 is effective for periods beginning on or after January 1, 2010, for consolidated financial statements rather than for calendar 2008.

BRAZILIAN GAAP vs. IFRS | Ernst & Young Terco10 BRAZILIAN GAAP vs. IFRS | Ernst & Young Terco

Converged Standards

Description BR GAAP prior to CPC

CPC 13 First Time Adoption of Law 11,638;

CPC 37 First Time Adoption of IFRS;

CPC 43 Initial Adoption of Technical Pronouncements CPC 15 and 40

These CPCs were issued in order to help companies apply the changes brought by Law 11.638 and the CPCs. They are broadly equivalent to IFRS 1 but there are differences eliminating alternatives and requiring items primarily due to CPC or Corporate Law constraints or requirements such as the revaluation of assets (not allowed under Corporate Law), presentation of the income statement (under the CPC, entities must present an income statement separate from comprehensive income but the IFRS allows a choice between one statement and 2 statements), and the effective date of when businesses combinations must be revalued (under the CPC, business combinations can only be revalued back to January 1, 2009 but the IFRS allows companies to go back further than this so companies in Brazil should be following the CPC requirements).

We expect CPC 37 and 43 to be revised to be aligned with IFRS 1.

Under BR GAAP, NPC 12 – Accounting Policies, Changes in Accounting Estimates and Errors was used, with the CPC providing an additional option on the adoption of Law 11,638. NPC 12 is similar to IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors. CPC 23 – Accounting policies, changes in estimates and errors, is effective in 2010.

BRAZILIAN GAAP vs. IFRS | Ernst & Young Terco BRAZILIAN GAAP vs. IFRS | Ernst & Young Terco 11

BR GAAP Standard IFRS Standard Significant Differences BR GAAP prior to CPC

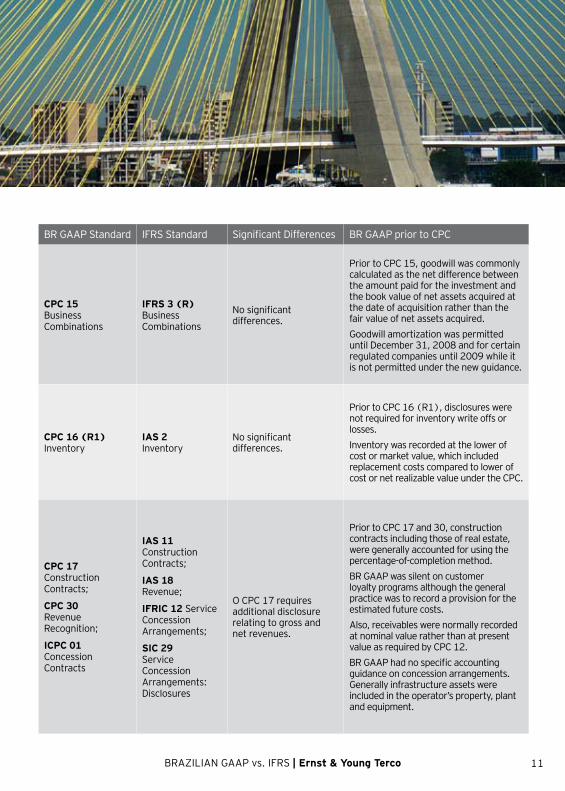

CPC 15 Business Combinations

IFRS 3 (R) Business Combinations

No significant differences.

Prior to CPC 15, goodwill was commonly calculated as the net difference between the amount paid for the investment and the book value of net assets acquired at the date of acquisition rather than the fair value of net assets acquired.

Goodwill amortization was permitted until December 31, 2008 and for certain regulated companies until 2009 while it is not permitted under the new guidance.

CPC 16 (R1) Inventory

IAS 2 Inventory

No significant differences.

Prior to CPC 16 (R1), disclosures were not required for inventory write offs or losses.

Inventory was recorded at the lower of cost or market value, which included replacement costs compared to lower of cost or net realizable value under the CPC.

CPC 17 Construction Contracts;

CPC 30 Revenue Recognition;

ICPC 01 Concession Contracts

IAS 11 Construction Contracts;

IAS 18 Revenue;

IFRIC 12 Service Concession Arrangements;

SIC 29 Service Concession Arrangements: Disclosures

O CPC 17 requires additional disclosure relating to gross and net revenues.

Prior to CPC 17 and 30, construction contracts including those of real estate, were generally accounted for using the percentage-of-completion method.

BR GAAP was silent on customer loyalty programs although the general practice was to record a provision for the estimated future costs.

Also, receivables were normally recorded at nominal value rather than at present value as required by CPC 12.

BR GAAP had no specific accounting guidance on concession arrangements. Generally infrastructure assets were included in the operator’s property, plant and equipment.

BRAZILIAN GAAP vs. IFRS | Ernst & Young Terco12 BRAZILIAN GAAP vs. IFRS | Ernst & Young Terco

Converged Standards

BR GAAP Standard IFRS Standard Significant Differences BR GAAP prior to CPC

CPC 18 Investments in Associates;

CPC 19 Interests in Joint Ventures;

CPC 35 Separate Financial Statements;

CPC 36 (R1) Consolidated Financial Statements;

ICPC 09 Individual Financial Statements, Separate Financial Statements and Consolidated Financial Statements and Equity Method

IAS 28 Investments in Associates;

IAS 31 Interests in Joint Ventures;

IAS 27 Consolidated and Separate Financial Statements

CPC’s 35 and 36 (R1)have a third type of financial statements called individual financial statements. These are parent company financial statements in which subsidiaries and joint ventures are presented using the equity method.

Joint ventures must use proportionate consolidation under CPC 19 while they have the option of proportionate or equity method consolidation under IFRS.

Under IFRS, an entity can include results of an investment in associate with a different reporting period as long as it is within 3 months of the entity’s reporting date. CPC18 only allows a difference of 2 months.

CPC 18 has an additional paragraph (22A) which says that profit cannot be recorded on individual financial statements on intercompany transactions that remain within the group of related parties.

Prior to CPC 36 (R1), non-controlling minority interests were presented outside of equity as a separate line item in the balance sheet rather than as a separate component in equity.

CPC 20 Borrowing Costs

IAS 23 Borrowing Costs

IFRS is silent as to whether or not exchange differences should actually create a credit to the asset due to favorable exchange rates while the CPC indicates that exchange rate differences should be captured in the capitalization.

Prior to CPC 20, only interest related to debt was capitalized by public companies.

BRAZILIAN GAAP vs. IFRS | Ernst & Young Terco BRAZILIAN GAAP vs. IFRS | Ernst & Young Terco 13

BR GAAP Standard IFRS Standard Significant Differences BR GAAP prior to CPC

CPC 21 Interim Reporting;

CPC 22 Operating Segments;

CPC 23 Accounting Policies, Changes in Accounting Estimates and Errors;

CPC 26 Presentation of Financial Statements

IAS 34 Interim Financial Reporting;

IFRS 8 Operating Segments;

IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors;

IAS 1 Presentation of Financial Statements

IAS 1 does not require the Value Added (locally DVA) statement that is required by CPC 26, it would only be required if there was a legal requirement or a requirement by a regulator.

Prior to CPC 22, public companies had an option to disclose segments based on IAS 14. IAS 14 was superseded by IFRS 8 and the criteria for defining segments are now different.

Prior to CPC 26, assets and liabilities were presented in the descending order of liquidity rather than by using current and non-current classifications. Minority interests were included in a separate line from equity. A statement of comprehensive income was not required.

CPC 24 Subsequent Events;

ICPC 08 Accounting for the Payment of Proposed Dividends

IAS 10 Events after the Reporting Period

ICPC 08 explains how dividends are recorded and explicitly states that mandatory dividends under Law 6.404/76 must be recorded as a liability. The same conclusion would be reached under IFRS but there is no interpretation in IFRS similar to ICPC 08.

Prior to CPC 24 and ICPC 08, entities were required to record dividends proposed by management which were normally subject to approval by shareholders in the subsequent year.

Debt for which there was a covenant violation was presented as non-current if a lender agreement existed prior to the issuance of the financial statements. Also, short-term loans were reclassified as long-term if the entity intended to refinance the loan on a long-term basis and, if prior to issuing the financial statements, the entity presented formal documents that supported the reclassification of the loan.

BRAZILIAN GAAP vs. IFRS | Ernst & Young Terco14 BRAZILIAN GAAP vs. IFRS | Ernst & Young Terco

Converged Standards

BR GAAP Standard IFRS Standard Significant Differences BR GAAP prior to CPC

CPC 25 Provisions, Contingent Liabilities and Contingent Assets

IAS 37 Provisions, Contingent Liabilities and Contingent Assets

No significant differences.

Prior to CPC 25, provisions for legal obligations were sometimes recorded regardless of the probability of the eventual settlement. Provisions for onerous contracts and constructive obligations were uncommon.

CPC 27 Property, Plant & Equipment;

CPC 28 Investment Property;

CPC 31 Non-current Assets Held for Sale and Discontinued Operations;

ICPC 01 Concession Contracts

IAS 16 Property, Plant & Equipment;

IAS 40 Investment Property;

IFRS 5 Non-current Assets Held for Sale and Discontinued Operations;

IFRIC 12 Service Concession Arrangements

Revaluation of assets is not permitted under Law 11,638 while revaluation may be applied (as a policy choice) to an entire class of assets which are then required to be revalued to fair value on a regular basis under IFRS.

Under CPC 31, the CPC has an additional category of assets called assets held to be distributed to owners.

Prior to CPC 27, costs of major overhauls were normally expensed. It was common for entities to apply useful lives which were determined by tax legislation. Component depreciation was permitted but not commonly applied.

Prior to CPC 28, investment property was not separately defined and was, therefore, accounted for as held for use or held for sale.

Prior to ICPC 01, BR GAAP had no specific accounting guidance on concession arrangements. Generally, infrastructure assets were included in the operator’s property, plant and equipment.

CPC 29 Biological Assets

IAS 41 Agriculture

No significant differences.

Prior to CPC 29, entities normally used cost to measure these assets although they could be measured at fair value subject to certain conditions.

BRAZILIAN GAAP vs. IFRS | Ernst & Young Terco BRAZILIAN GAAP vs. IFRS | Ernst & Young Terco 15

BR GAAP Standard

IFRS Standard

Significant Differences

BR GAAP prior to CPC

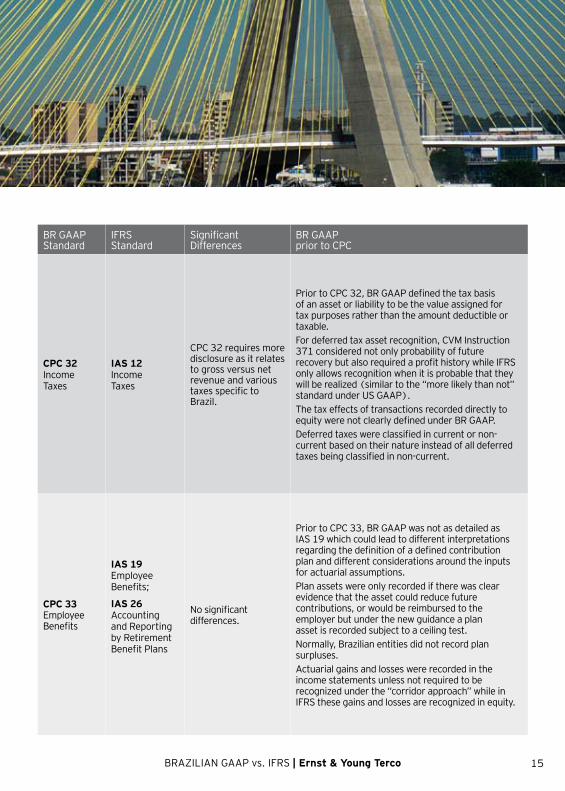

CPC 32 Income Taxes

IAS 12 Income Taxes

CPC 32 requires more disclosure as it relates to gross versus net revenue and various taxes specific to Brazil.

Prior to CPC 32, BR GAAP defined the tax basis of an asset or liability to be the value assigned for tax purposes rather than the amount deductible or taxable.

For deferred tax asset recognition, CVM Instruction 371 considered not only probability of future recovery but also required a profit history while IFRS only allows recognition when it is probable that they will be realized (similar to the “more likely than not” standard under US GAAP).

The tax effects of transactions recorded directly to equity were not clearly defined under BR GAAP.

Deferred taxes were classified in current or non-current based on their nature instead of all deferred taxes being classified in non-current.

CPC 33 Employee Benefits

IAS 19 Employee Benefits;

IAS 26 Accounting and Reporting by Retirement Benefit Plans

No significant differences.

Prior to CPC 33, BR GAAP was not as detailed as IAS 19 which could lead to different interpretations regarding the definition of a defined contribution plan and different considerations around the inputs for actuarial assumptions.

Plan assets were only recorded if there was clear evidence that the asset could reduce future contributions, or would be reimbursed to the employer but under the new guidance a plan asset is recorded subject to a ceiling test.

Normally, Brazilian entities did not record plan surpluses.

Actuarial gains and losses were recorded in the income statements unless not required to be recognized under the “corridor approach” while in IFRS these gains and losses are recognized in equity.

BRAZILIAN GAAP vs. IFRS | Ernst & Young Terco16 BRAZILIAN GAAP vs. IFRS | Ernst & Young Terco

BR GAAP Standard

IFRS Standard

Significant Differences

BR GAAP prior to CPC

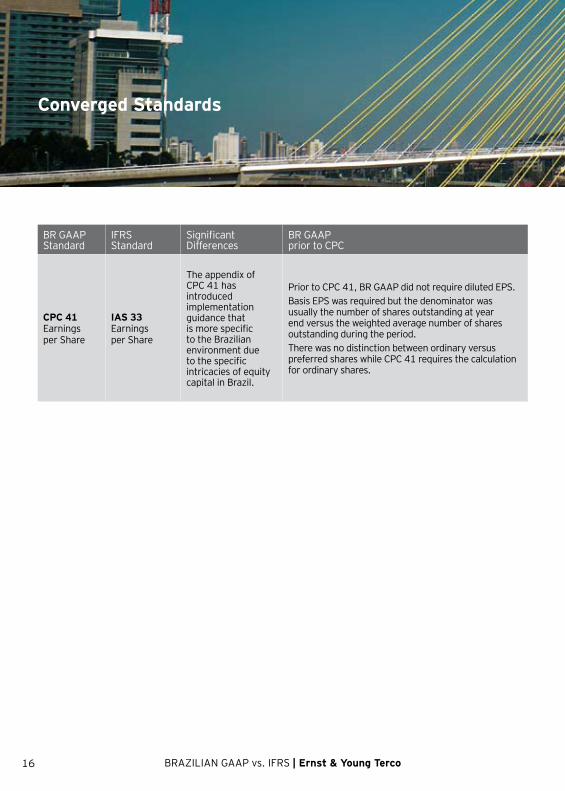

CPC 41 Earnings per Share

IAS 33 Earnings per Share

The appendix of CPC 41 has introduced implementation guidance that is more specific to the Brazilian environment due to the specific intricacies of equity capital in Brazil.

Prior to CPC 41, BR GAAP did not require diluted EPS.

Basis EPS was required but the denominator was usually the number of shares outstanding at year end versus the weighted average number of shares outstanding during the period.

There was no distinction between ordinary versus preferred shares while CPC 41 requires the calculation for ordinary shares.

Converged Standards

BRAZILIAN GAAP vs. IFRS | Ernst & Young Terco BRAZILIAN GAAP vs. IFRS | Ernst & Young Terco 17

Description BR GAAP prior to CPC

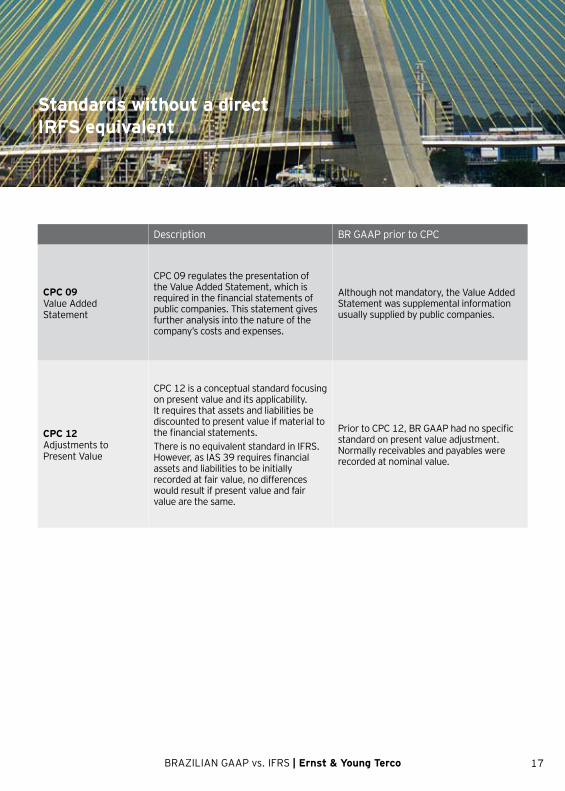

CPC 09 Value Added Statement

CPC 09 regulates the presentation of the Value Added Statement, which is required in the financial statements of public companies. This statement gives further analysis into the nature of the company’s costs and expenses.

Although not mandatory, the Value Added Statement was supplemental information usually supplied by public companies.

CPC 12 Adjustments to Present Value

CPC 12 is a conceptual standard focusing on present value and its applicability. It requires that assets and liabilities be discounted to present value if material to the financial statements.

There is no equivalent standard in IFRS. However, as IAS 39 requires financial assets and liabilities to be initially recorded at fair value, no differences would result if present value and fair value are the same.

Prior to CPC 12, BR GAAP had no specific standard on present value adjustment. Normally receivables and payables were recorded at nominal value.

Standards without a direct IRFS equivalent

BRAZILIAN GAAP vs. IFRS | Ernst & Young Terco18 BRAZILIAN GAAP vs. IFRS | Ernst & Young Terco

Areas for Future Consideration by the CPC

Exploration for and Evaluation of Mineral Resources

Convergence

The Brazilian CPC has not yet issued a standard relating to mineral resources. A standard on mineral resources (CPC 34)is expected to be issued and based on the IFRS 6.

IFRS 6

The Brazilian CPC has not issued a draft of this pronouncement yet because it doesn’t cover all types of exploration and evaluation (i.e. petroleum exploration).The IFRS 6 states that expenditures related to exploration for and evaluation of mineral resources, incurred after an entity has the legal right to explore the location and before an entity has technical feasibility and commercial viability relating to extracting the mineral resource, should be accounted for as either tangible or intangible assets depending on their nature. It further states that expenditures related to development of mineral resources should not be recognized as exploration and evaluation assets and should instead be considered under the

Framework and IAS 38 - Intangible Assets.

Impairment analysis of these assets are

required when facts and circumstances

suggest the carrying amount is greater

than the recoverable amount and just

before the asset is reclassified because

the technical feasibility and commercial

viability of extracting a mineral resource

are demonstrable.

Current Practice

There is not a specific pronouncement

related to mineral resources in current

BR GAAP, so companies have historically

used the guidance under the accounting

framework and tangible and intangible

assets to determine which costs are

capitalizable relating to these activities.

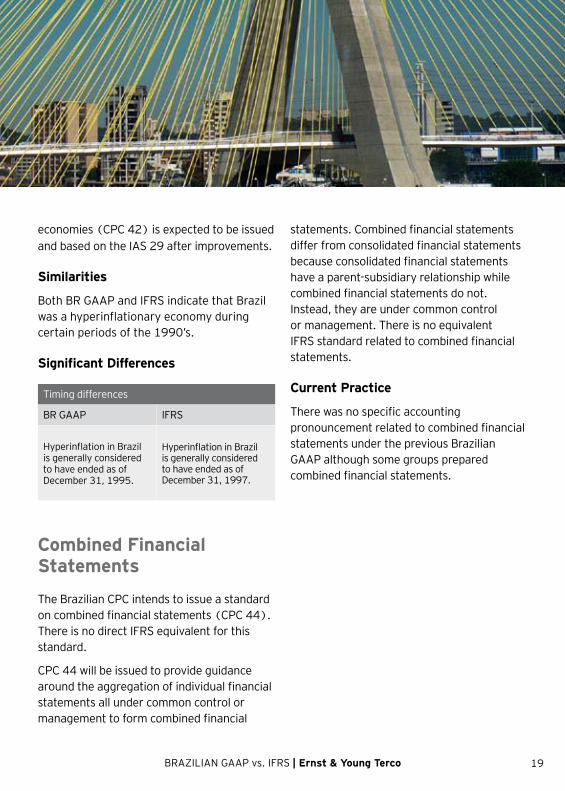

Financial Reporting in Hyperinflationary Economies

Convergence

The Brazilian CPC has not yet issued a

standard relating to hyperinflationary

economies because they are waiting for

improvements to be made to IAS 29 by

the IASB. A standard on hyperinflationary

BRAZILIAN GAAP vs. IFRS | Ernst & Young Terco BRAZILIAN GAAP vs. IFRS | Ernst & Young Terco 19

economies (CPC 42) is expected to be issued

and based on the IAS 29 after improvements.

Similarities

Both BR GAAP and IFRS indicate that Brazil was a hyperinflationary economy during certain periods of the 1990’s.

Significant Differences

Timing differences

BR GAAP IFRS

Hyperinflation in Brazil is generally considered to have ended as of December 31, 1995.

Hyperinflation in Brazil is generally considered to have ended as of December 31, 1997.

Combined Financial Statements

The Brazilian CPC intends to issue a standard on combined financial statements (CPC 44). There is no direct IFRS equivalent for this standard.

CPC 44 will be issued to provide guidance around the aggregation of individual financial statements all under common control or management to form combined financial

statements. Combined financial statements differ from consolidated financial statements because consolidated financial statements have a parent-subsidiary relationship while combined financial statements do not. Instead, they are under common control or management. There is no equivalent IFRS standard related to combined financial statements.

Current Practice

There was no specific accounting pronouncement related to combined financial statements under the previous Brazilian GAAP although some groups prepared combined financial statements.

Ernst & Young Terco

Assurance | Tax | Transactions | Advisory Services | Middle Market | Government | Financial Services

About Ernst & Young • Ernst & Young is a global leader in assurance, tax, transaction and advisory services. Worldwide, our 144,000 people are united by our shared values and an unwavering commitment to quality. We make a difference by helping our people, our clients and our wider communities achieve their potential. In Brazil, Ernst & Young Terco is the most complete company for advisory and assurance services in Brazil, boasting 3,500 professionals that support and serve over 3,400 large-, medium- and small-sized companies, 111 of which are listed on BM&FBovespa (in June 2010) and are part of the special portfolio of the assurance team.

www.ey.com.br

© 2010 EYGM Limited. All rights reserved.

This is a publication of the Branding and Communication Department. The full or partial reproduction of the contents of this publication is allowed provided the source is quoted.