the budgeting process what is budgeting? what is budgeting? it is the coordinating the combined...

TRANSCRIPT

The Budgeting ProcessThe Budgeting Process

What is budgeting?What is budgeting? It is the coordinating the combined It is the coordinating the combined

intelligence of an entire organization intelligence of an entire organization into a plan of action. Budgets include into a plan of action. Budgets include operating budget and financing operating budget and financing budget.budget.

Budgeting is a formal quantitative Budgeting is a formal quantitative expression of management plan.expression of management plan.

Operating budget is the budget that Operating budget is the budget that focuses on the acquisition and use of focuses on the acquisition and use of scarce resources. scarce resources.

On the other hand financing budget On the other hand financing budget is the budget that focuses on is the budget that focuses on acquiring to obtain resources.acquiring to obtain resources.

Advantages of budgetsAdvantages of budgets Enhance the decision making process Enhance the decision making process

by helping mangers meet by helping mangers meet uncertainties.uncertainties.

Enhance communication between Enhance communication between mangers because in the initial phase mangers because in the initial phase of budgeting mangers are forced to of budgeting mangers are forced to communicate with each other.communicate with each other.

Budgets encourage coordination Budgets encourage coordination among segments. Mangers through among segments. Mangers through budgeting are forced to exchange budgeting are forced to exchange views and hence coordination is views and hence coordination is achieved.achieved.

Budgeting is a formal commitment Budgeting is a formal commitment to take corrective action.to take corrective action.

Provides performance standards Provides performance standards and grantees effective and grantees effective performance.performance.

Difference between actual and Difference between actual and budgeted operations indicates the budgeted operations indicates the areas lacking control and enhances areas lacking control and enhances corrective actions. corrective actions.

Principles of budgetingPrinciples of budgeting Top management support.Top management support. Budgeting must be considered Budgeting must be considered

important by all management levelsimportant by all management levels A budget must not be a scapegoat A budget must not be a scapegoat

to management or company to management or company problems. problems.

Management must consider a Management must consider a budget an excellent means of budget an excellent means of planning so that it can gain planning so that it can gain numerous benefits. numerous benefits.

If there are new external or internal If there are new external or internal conditions that require revision of conditions that require revision of budgets, top management must budgets, top management must make budget revision.make budget revision.

Types of budgetsTypes of budgets Budgets or planning horizon can vary from Budgets or planning horizon can vary from

one year (less) to many years, depending on one year (less) to many years, depending on the objectives and the uncertainties involves.the objectives and the uncertainties involves.

Short term: normally twelve or less months.Short term: normally twelve or less months. Long range: more than a year, normally 5-10 Long range: more than a year, normally 5-10

years. These are prepared for special years. These are prepared for special purposes. Eg equipment purchase, addition purposes. Eg equipment purchase, addition of product lines.of product lines.

Master budget consolidate an Master budget consolidate an organization plan for shorter time organization plan for shorter time span and are usually prepared on an span and are usually prepared on an annual basis. They are sub-divided annual basis. They are sub-divided month to month, monthly basis for month to month, monthly basis for the first quarter and then quarterly the first quarter and then quarterly for the remaining of the year.for the remaining of the year.

Continuous budget these are master Continuous budget these are master budgets that perpetually add a month budgets that perpetually add a month as the month just ended is dropped. as the month just ended is dropped.

Budgets forecast two types of Budgets forecast two types of activitiesactivities

Operating activities are forecasted in Operating activities are forecasted in the operating budget. This include:the operating budget. This include: Sales budgetSales budget Production budget ( units)Production budget ( units) Material useMaterial use Direct laborDirect labor Indirect manufacturing.Indirect manufacturing.

Change in inventory level.Change in inventory level. Cost of goods sold budgetCost of goods sold budget Selling expense budgetSelling expense budget Budgeted income statementBudgeted income statement Financial BudgetFinancial Budget Capital BudgetCapital Budget Administrative expense budget Administrative expense budget

Cash budgetCash budget

Budgeted balance sheetBudgeted balance sheet

Sales budgetSales budget This is the starting point of the This is the starting point of the

budgeting process, because budgeting process, because inventory levels ,purchases, and inventory levels ,purchases, and operating expenses are generally operating expenses are generally geared to the rate of the sales geared to the rate of the sales activity. The sales budget includes activity. The sales budget includes cash sales, credit sales and their cash sales, credit sales and their total.total.

Sample of sales budgetSample of sales budget

Company NameCompany Name Sales BudgetSales Budget

AprilApril May May JuneJune

Credit sales(40%) 160Credit sales(40%) 160 200200 240240 Cash sales(60%) 240Cash sales(60%) 240 300300 360360 Total Total 400400 500500 600600

After the sales budget is prepared, After the sales budget is prepared, the purchase budget can be the purchase budget can be prepared. The total merchandise prepared. The total merchandise needed is the sum of desired ending needed is the sum of desired ending inventory plus the amount needed to inventory plus the amount needed to fulfill the budgeted sales demand. The fulfill the budgeted sales demand. The total needed is partially met by the total needed is partially met by the beginning inventory; the reminder beginning inventory; the reminder must come from planned purchases. must come from planned purchases.

Therefore these purchases are Therefore these purchases are computed as follows:computed as follows:

Purchases= desired ending inventory Purchases= desired ending inventory + Production needs- beginning + Production needs- beginning inventory.inventory.

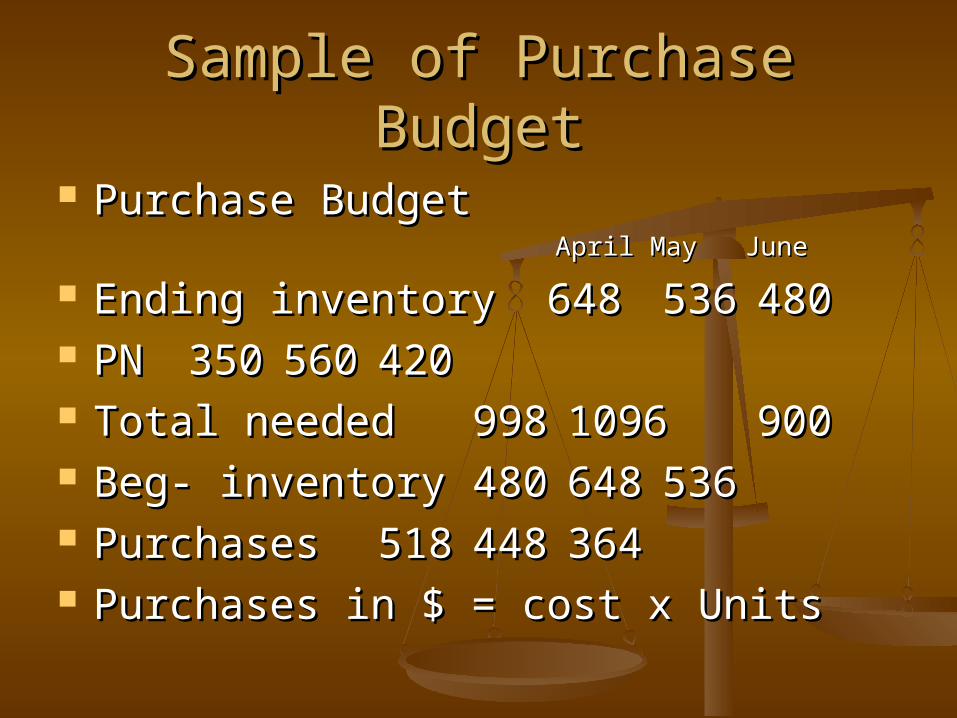

Sample of Purchase BudgetSample of Purchase Budget

Purchase BudgetPurchase Budget AprilApril May May JuneJune

Ending inventory 648Ending inventory 648 536536 480480 PNPN 350350 560560 420420 Total neededTotal needed 998998 10961096

900900 Beg- inventory Beg- inventory 480480 648648 536536 PurchasesPurchases 518518 448448 364364 Purchases in $ = cost x UnitsPurchases in $ = cost x Units

Operating expense budgetOperating expense budget This is dependent on various factors. This is dependent on various factors.

many operating expenses are many operating expenses are directly influenced by month-to-directly influenced by month-to-month fluctuations in sales volume month fluctuations in sales volume (sales commission). Others are not (sales commission). Others are not directly influenced by the volume of directly influenced by the volume of sales( rent, insurance) sales( rent, insurance)

Sample of operating expense Sample of operating expense budgetbudget

Expense budgetExpense budget AprilApril May May JuneJune

WagesWages 250 250 250250 250250 Commission Commission 750750 12001200 900900 Total Total 10001000 14501450 1150 1150 RentRent 250250 250250 250250 Depreciation Depreciation 200200 200200 200200 Other costsOther costs -------- -------- -------- Total O. ExpensesTotal O. Expenses -------- ---- ---- --------

Sample of budgeted P&LSample of budgeted P&L

Budgeted Income StatementBudgeted Income Statement SalesSales -CGS-CGS -Operating expenses-Operating expenses Income from operationsIncome from operations -Interest -Interest Net incomeNet income

At this stage we have completed the At this stage we have completed the operating budget.operating budget.

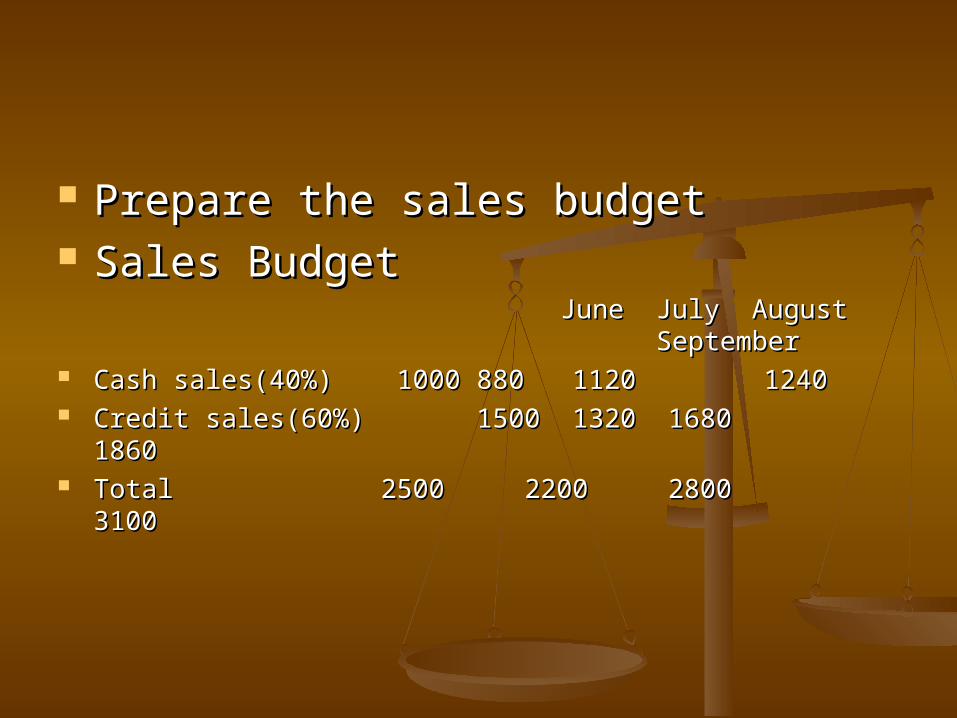

Therefore the steps are as follows:Therefore the steps are as follows: 1. Prepare the sales budget1. Prepare the sales budget 2. Prepare the purchase budget2. Prepare the purchase budget 3. Prepare the operating expenses 3. Prepare the operating expenses

budgetbudget 4. Prepare the income statement 4. Prepare the income statement

budget.budget.

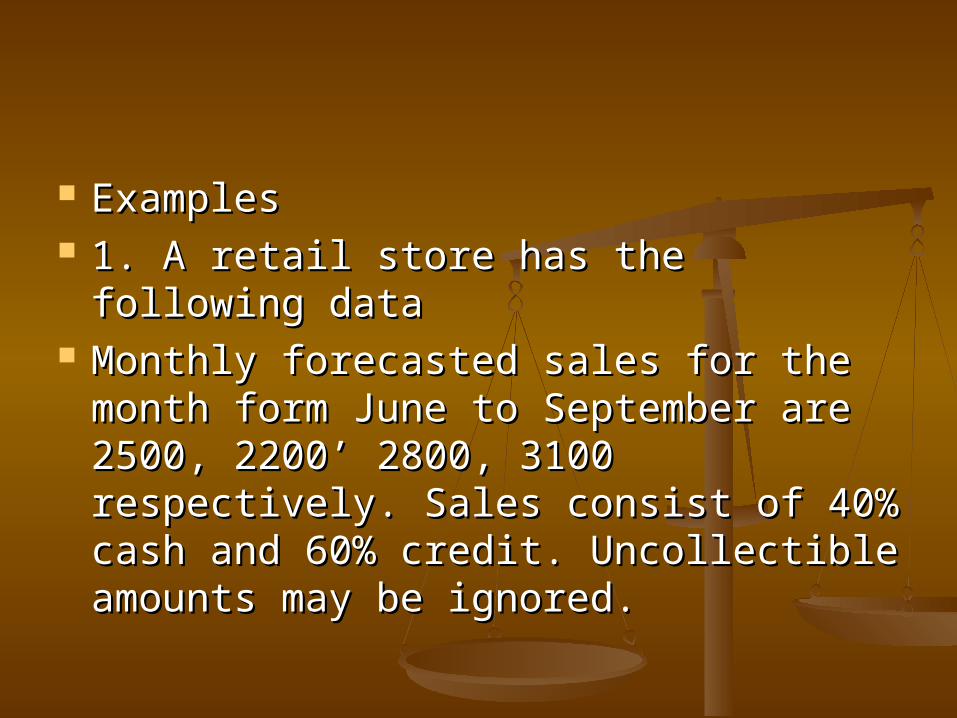

ExamplesExamples 1. A retail store has the following 1. A retail store has the following

datadata Monthly forecasted sales for the Monthly forecasted sales for the

month form June to September are month form June to September are 2500, 22002500, 2200’’ 2800, 3100 respectively. 2800, 3100 respectively. Sales consist of 40% cash and 60% Sales consist of 40% cash and 60% credit. Uncollectible amounts may be credit. Uncollectible amounts may be ignored. ignored.

Prepare the sales budgetPrepare the sales budget Sales BudgetSales Budget

JuneJune July July August August September September

Cash sales(40%)Cash sales(40%) 1000 1000 880880 11201120 12401240 Credit sales(60%) Credit sales(60%) 15001500 13201320 1680 1680 18601860 Total Total 2500 22002500 2200 28002800 31003100

ExampleExample

A retail store has the following dataA retail store has the following data Monthly forecasted inventory levels for the Monthly forecasted inventory levels for the

month from May to August are 170000, month from May to August are 170000, 150000, 190000 and 160000 respectively. 150000, 190000 and 160000 respectively. Sales are expected to be 350000for June, Sales are expected to be 350000for June, 250000 for July and 330000 for August. 250000 for July and 330000 for August. Cost of sales is 60% of sales. Purchases in Cost of sales is 60% of sales. Purchases in April has been 190000, May 160000. April has been 190000, May 160000. Prepare the budget for June, July and Prepare the budget for June, July and August. August.

Purchase BudgetPurchase Budget JuneJune July July August August

End.Inv.End.Inv. 150000150000 190000190000 160000160000 +CGS+CGS 210000210000 150000150000 198000198000 TotalTotal360000360000 340000340000 358000358000- Beg. InvBeg. Inv 170000170000 150000150000 190000190000

190000190000 190000190000 168000 168000

A retail store has the following dataA retail store has the following data Monthly forecasted sales for the month Monthly forecasted sales for the month

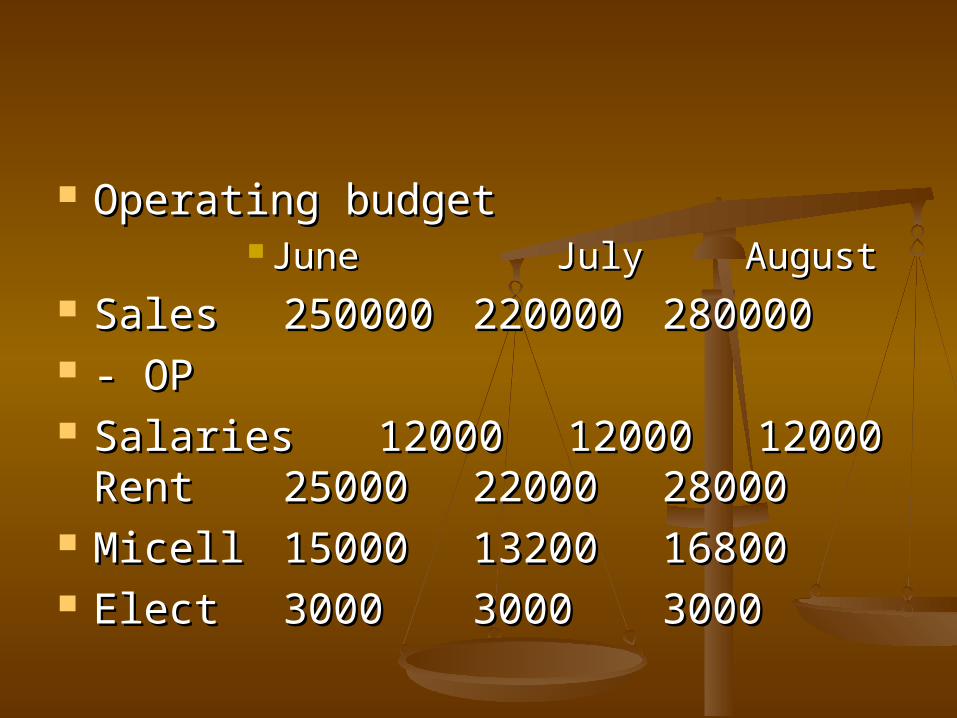

form May to August are 300000, 250000 form May to August are 300000, 250000 220000, 280000 respectively. Salaries 220000, 280000 respectively. Salaries amount to 12000 monthly. Commission is amount to 12000 monthly. Commission is 10% of current sales. Other expenses are 10% of current sales. Other expenses are rent 3000 per month, miscellaneous rent 3000 per month, miscellaneous expenses 6% of sales, depreciation 1900 expenses 6% of sales, depreciation 1900 per month. Prepare the operating budget per month. Prepare the operating budget for the month June, July and August.for the month June, July and August.

Operating budgetOperating budget JuneJune July July August August

SalesSales 250000250000 220000220000 280000280000 - OP- OP SalariesSalaries 1200012000 1200012000 12000 12000

RentRent 2500025000 2200022000 2800028000 MicellMicell 1500015000 1320013200 1680016800 ElectElect 30003000 30003000 30003000

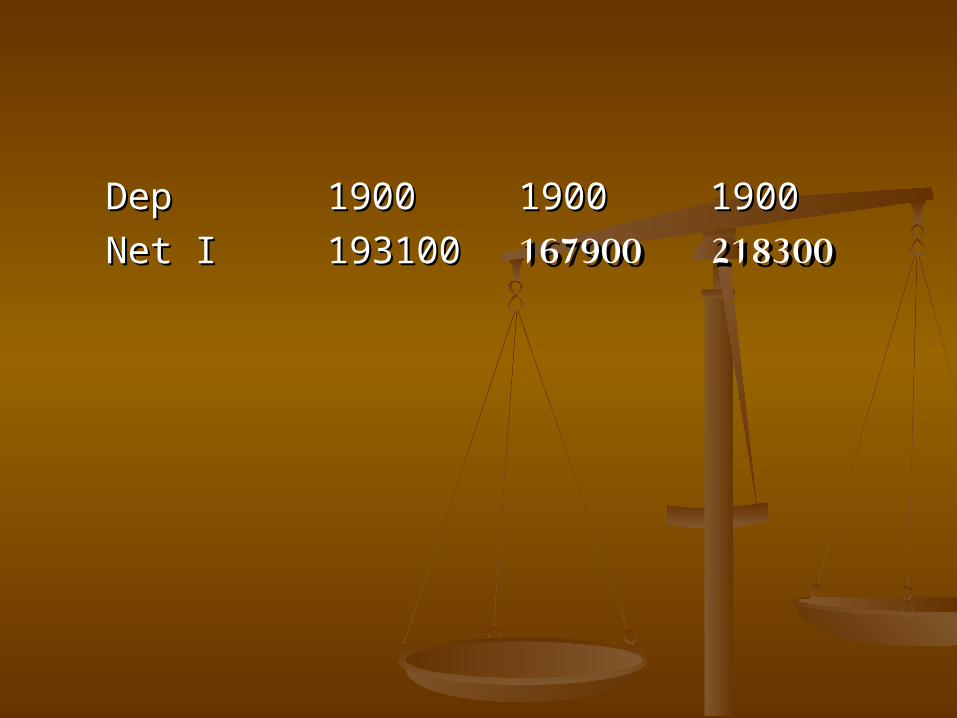

DepDep 19001900 19001900 19001900

Net INet I 193100193100 167900167900 218300218300

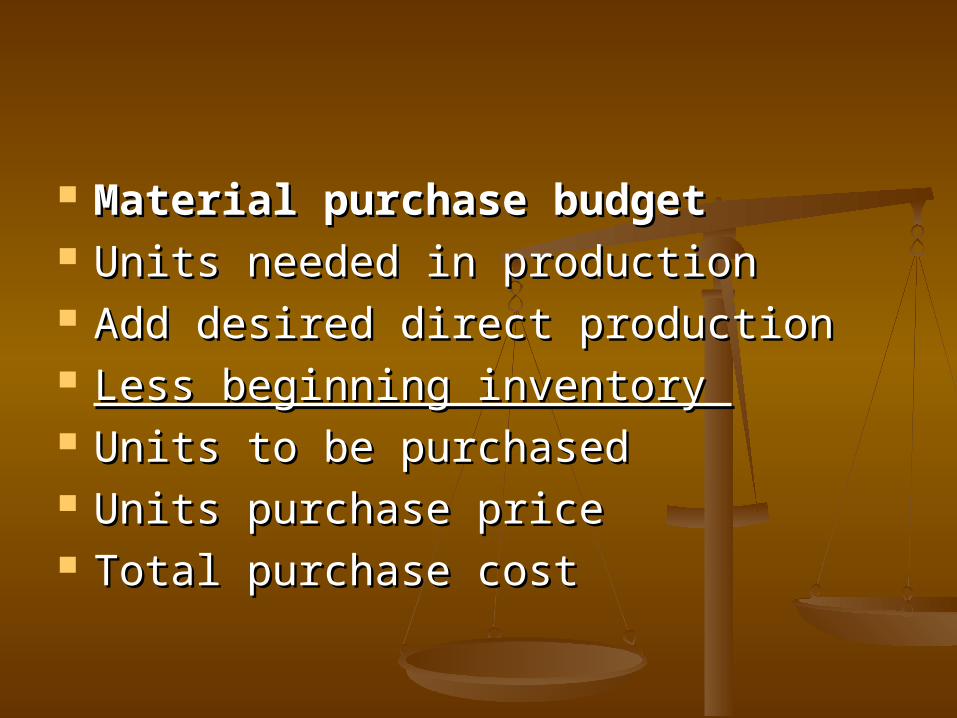

Material purchase budgetMaterial purchase budget Units needed in production Units needed in production Add desired direct production Add desired direct production Less beginning inventory Less beginning inventory Units to be purchasedUnits to be purchased Units purchase priceUnits purchase price Total purchase costTotal purchase cost

Problem 1. Problem 1. Alex Company manufactures Alex Company manufactures

products X, Y and Z. each product products X, Y and Z. each product required different quantities of input. required different quantities of input. Planned unit production of each Planned unit production of each product in 1991 is 10000 units for X, product in 1991 is 10000 units for X, 40000 for Y and 30000 for Z. the 40000 for Y and 30000 for Z. the direct material for each product aredirect material for each product are

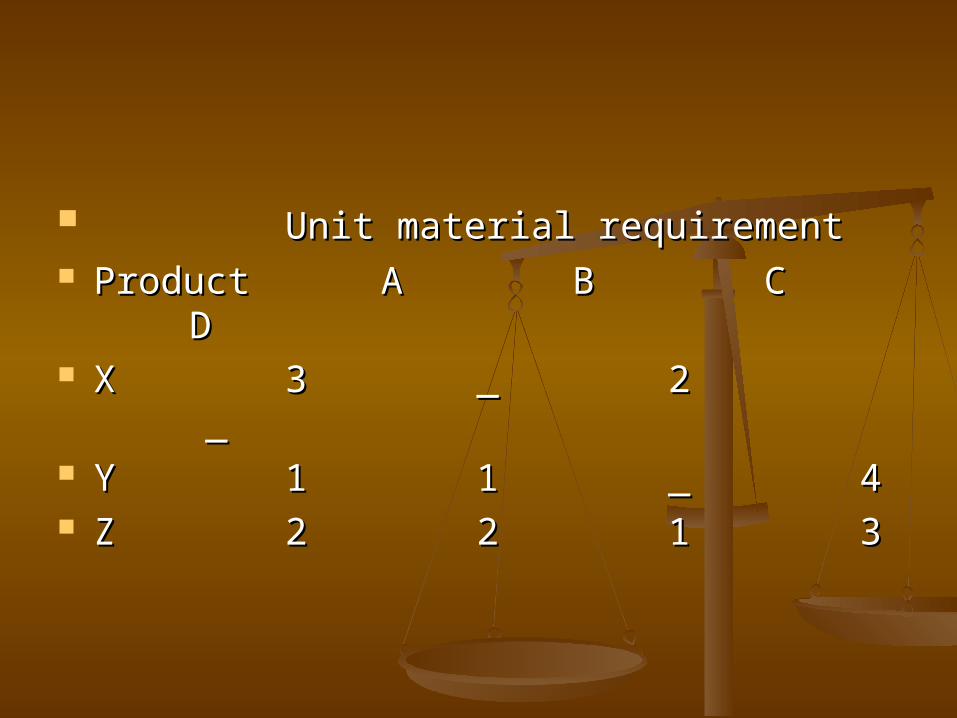

Unit material requirementUnit material requirement Product Product AA BB CC DD XX 33 __ 2 _2 _ YY 11 11 __ 44 ZZ 22 22 11 33

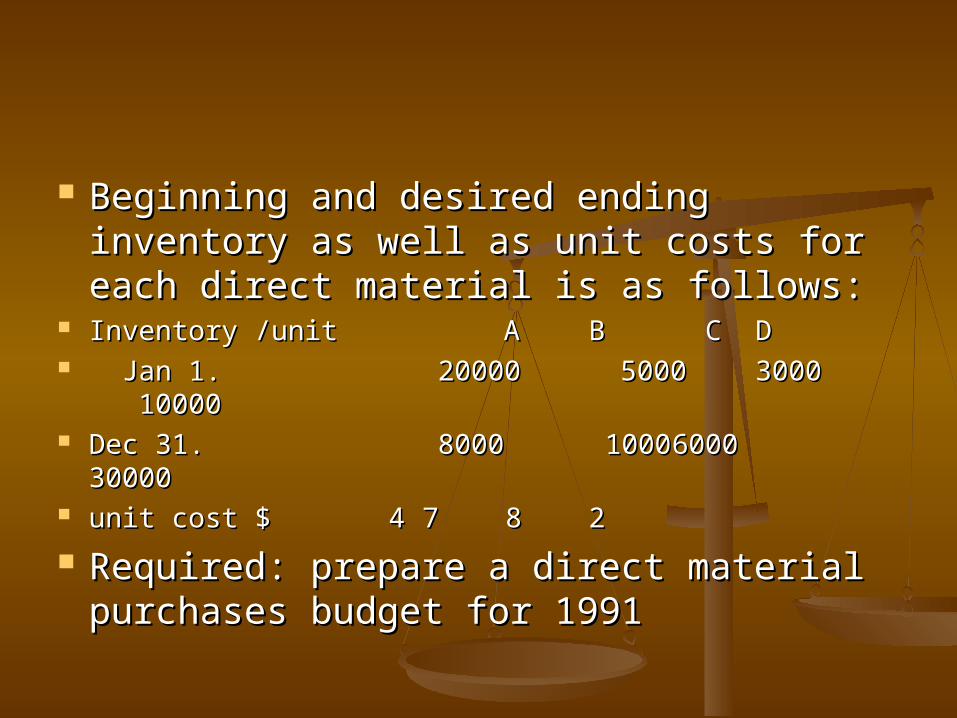

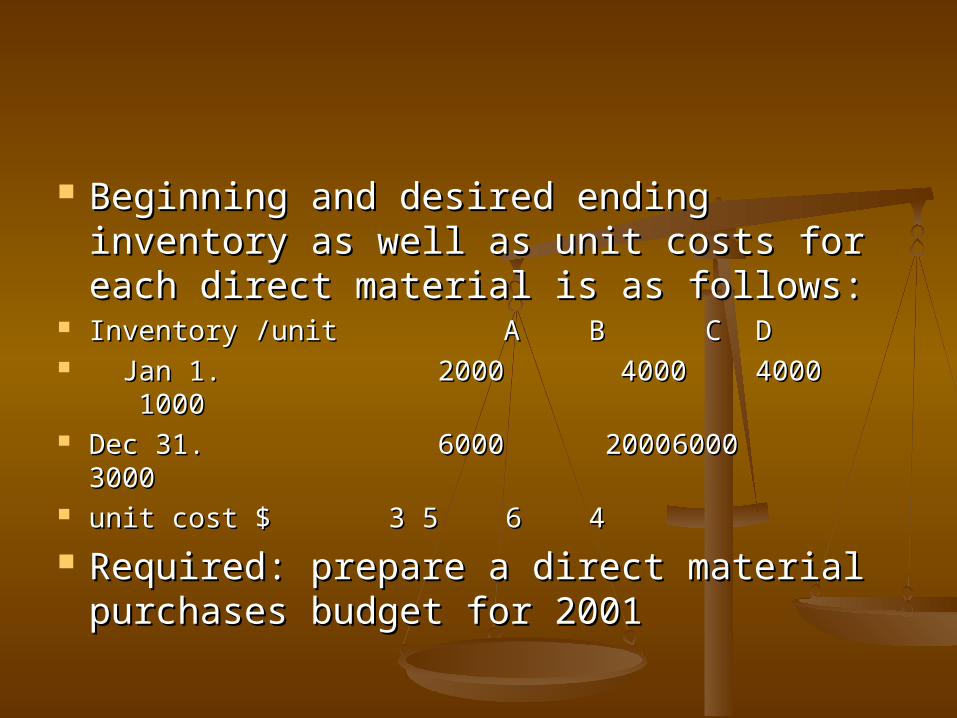

Beginning and desired ending Beginning and desired ending inventory as well as unit costs for each inventory as well as unit costs for each direct material is as follows:direct material is as follows:

Inventory /unit AInventory /unit A BB C C DD Jan 1. Jan 1. 20000 5000 20000 5000 3000 100003000 10000 Dec 31. Dec 31. 8000 8000 1000 1000 60006000

3000030000 unit cost $unit cost $ 4 4 77 88 22

Required: prepare a direct material Required: prepare a direct material purchases budget for 1991purchases budget for 1991

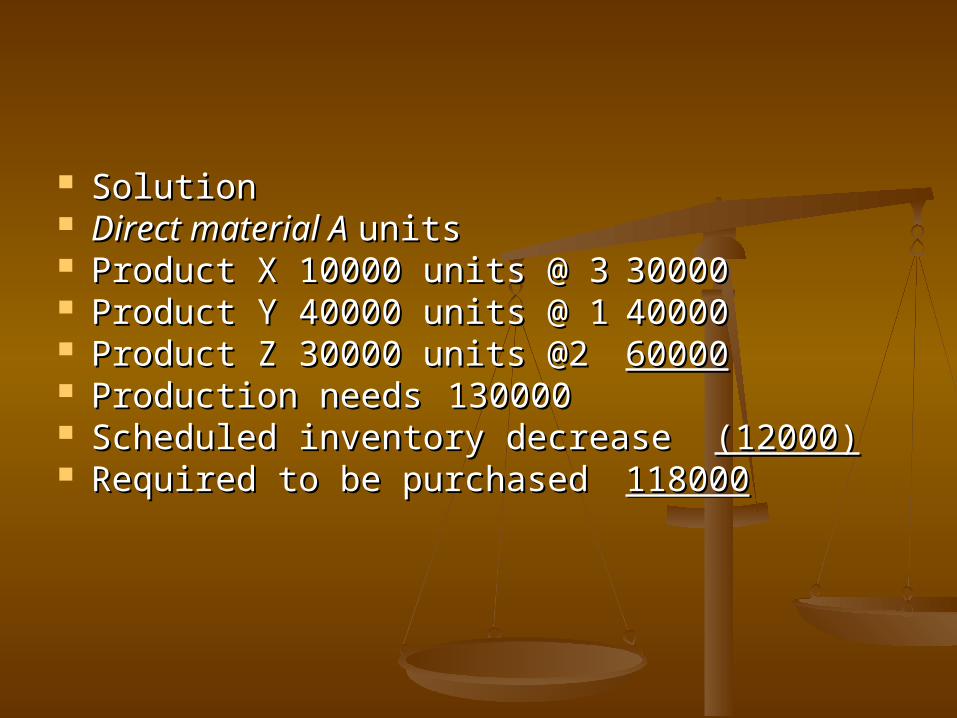

Solution Solution Direct material ADirect material A units units Product X 10000 units @ 3Product X 10000 units @ 3 3000030000 Product Y 40000 units @ 1Product Y 40000 units @ 1 4000040000 Product Z 30000 units @2Product Z 30000 units @2 6000060000 Production needs Production needs 130000130000 Scheduled inventory decreaseScheduled inventory decrease (12000)(12000) Required to be purchasedRequired to be purchased

118000118000

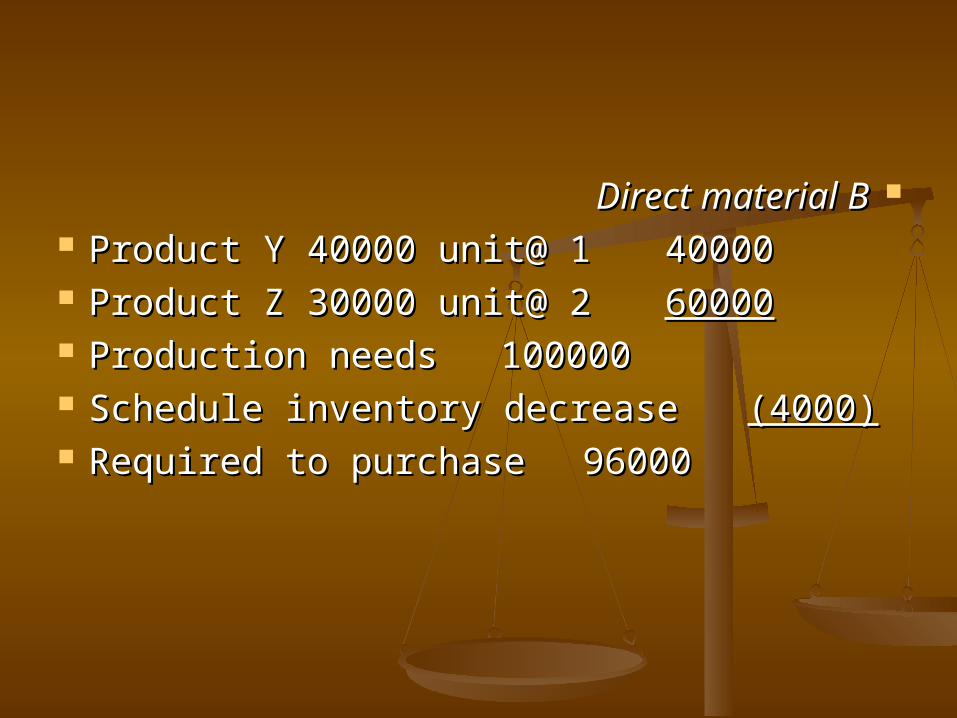

Direct material BDirect material B Product Y 40000 unit@ 1Product Y 40000 unit@ 1 4000040000 Product Z 30000 unit@ 2Product Z 30000 unit@ 2 6000060000 Production needs Production needs

100000100000 Schedule inventory decreaseSchedule inventory decrease

(4000)(4000) Required to purchaseRequired to purchase 9600096000

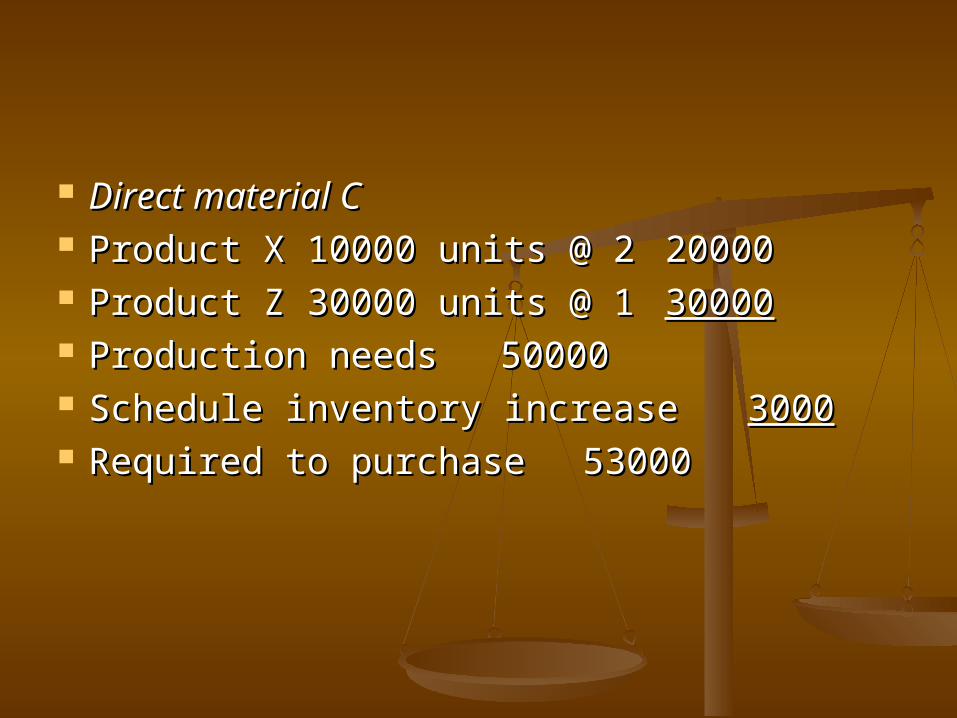

Direct material C Direct material C Product X 10000 units @ 2Product X 10000 units @ 2 2000020000 Product Z 30000 units @ 1Product Z 30000 units @ 1 3000030000 Production needs Production needs

5000050000 Schedule inventory increase Schedule inventory increase 30003000 Required to purchaseRequired to purchase 5300053000

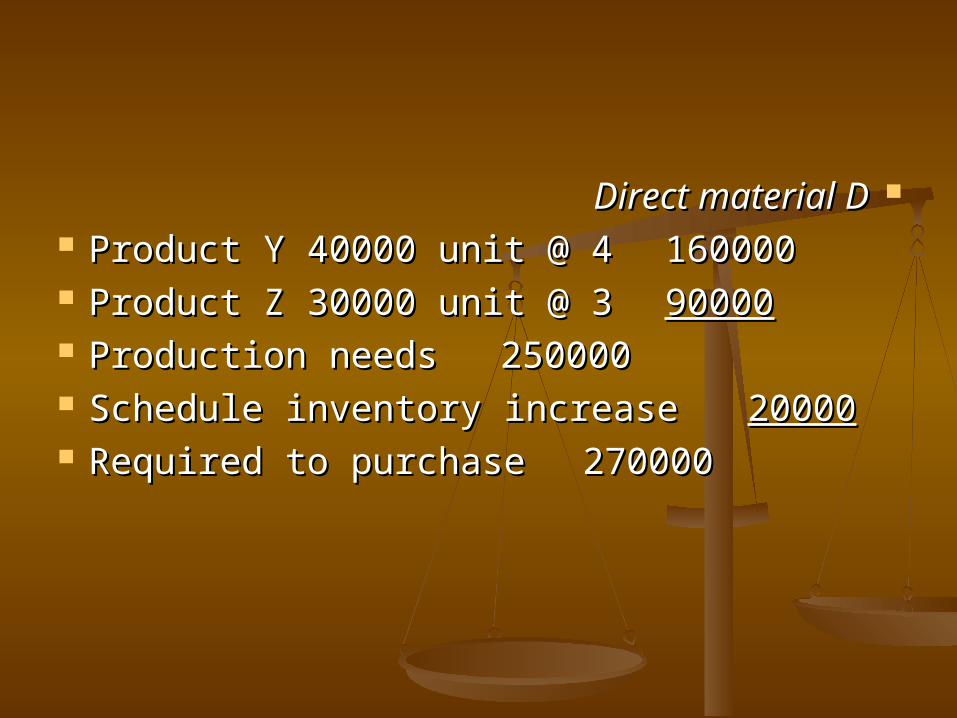

Direct material DDirect material D Product Y 40000 unit @ 4Product Y 40000 unit @ 4 160000160000 Product Z 30000 unit @ 3Product Z 30000 unit @ 3 9000090000 Production needsProduction needs 250000250000 Schedule inventory increaseSchedule inventory increase

2000020000 Required to purchaseRequired to purchase 270000270000

material Qmaterial Q Price Price Totat Totat purchase purchase priceprice

AA 118000118000 4 4 $472000 $472000 BB 96000 796000 7 672000 672000 CC 5300053000 8 8 424000 424000 D D 270000270000 2 2 540000540000 TotalTotal

$2108000$2108000

Direct labor budgetDirect labor budget It reflects the number of units to be It reflects the number of units to be

produced according to the production produced according to the production budget. Labor budget includes only direct budget. Labor budget includes only direct labor as indirect labor is included in the labor as indirect labor is included in the overhead budget. In this budget the direct overhead budget. In this budget the direct labor hours have to be specified so that labor hours have to be specified so that management has to translate this into management has to translate this into dollars by applying the appropriate labor dollars by applying the appropriate labor rate.rate.

SampleSample ABC Co.ABC Co. Direct labor budgetDirect labor budget DateDate UnitsUnits HoursHours Total hourTotal hour’’ss

Total Total budget@ budget@ raterate

Product A 1650Product A 1650 33 495049505940059400

Product B 16130Product B 16130 55 8065080650 967800967800

Product C 9400Product C 9400 1010 9400094000 11280001128000

179600179600 2155200 2155200

Practice 1. Practice 1. Emilio and Sons Company Emilio and Sons Company

manufactures products 1,2 and 3. manufactures products 1,2 and 3. each product required different each product required different quantities of input. Planned unit quantities of input. Planned unit production of each product in 2001 is production of each product in 2001 is 20000 units for 1, 30000 for 2 and 20000 units for 1, 30000 for 2 and 40000 for 3. The direct material for 40000 for 3. The direct material for each product areeach product are

Unit material requirementUnit material requirement Product AProduct A BB CC DD 11 -- 33 2 12 1 22 11 11 33 22 33 55 22 -- 44

Beginning and desired ending Beginning and desired ending inventory as well as unit costs for each inventory as well as unit costs for each direct material is as follows:direct material is as follows:

Inventory /unit AInventory /unit A BB C C DD Jan 1. Jan 1. 2000 4000 2000 4000 4000 10004000 1000 Dec 31. Dec 31. 6000 6000 2000 2000 60006000

30003000 unit cost $unit cost $ 3 3 55 66 44

Required: prepare a direct material Required: prepare a direct material purchases budget for 2001purchases budget for 2001

Practice 2. Practice 2. Mohd and Sons Company Mohd and Sons Company

manufactures products 1,2 and 3. manufactures products 1,2 and 3. Each product required different Each product required different quantities of input. Planned unit quantities of input. Planned unit production of each product in 2003 is production of each product in 2003 is 10000 units for 1, 15000 for 2 and 10000 units for 1, 15000 for 2 and 20000 for 3. The direct material for 20000 for 3. The direct material for each product areeach product are

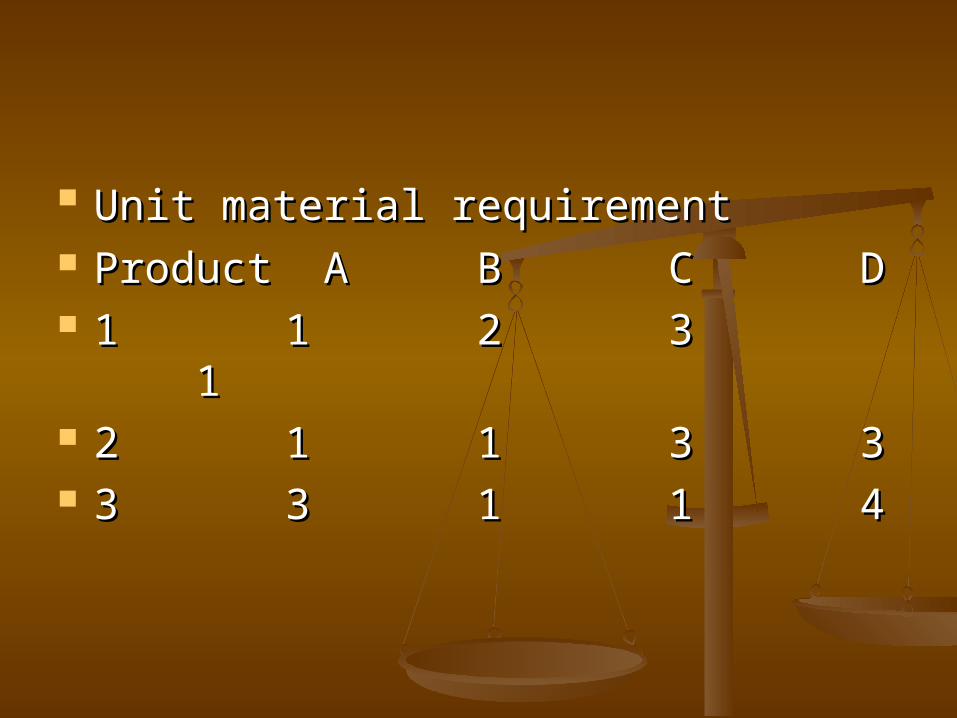

Unit material requirementUnit material requirement Product AProduct A BB CC DD 11 11 22 3 13 1 22 11 11 33 33 33 33 11 11 44

Beginning and desired ending Beginning and desired ending inventory as well as unit costs for each inventory as well as unit costs for each direct material is as follows:direct material is as follows:

Inventory /unit AInventory /unit A BB C C DD Jan 1. Jan 1. 2000 4000 2000 4000 4000 10004000 1000 Dec 31. Dec 31. 5000 5000 2000 2000 30003000

30003000 unit cost $unit cost $ 3 3 55 66 44

Required: prepare a direct material Required: prepare a direct material purchases budget for 2003purchases budget for 2003

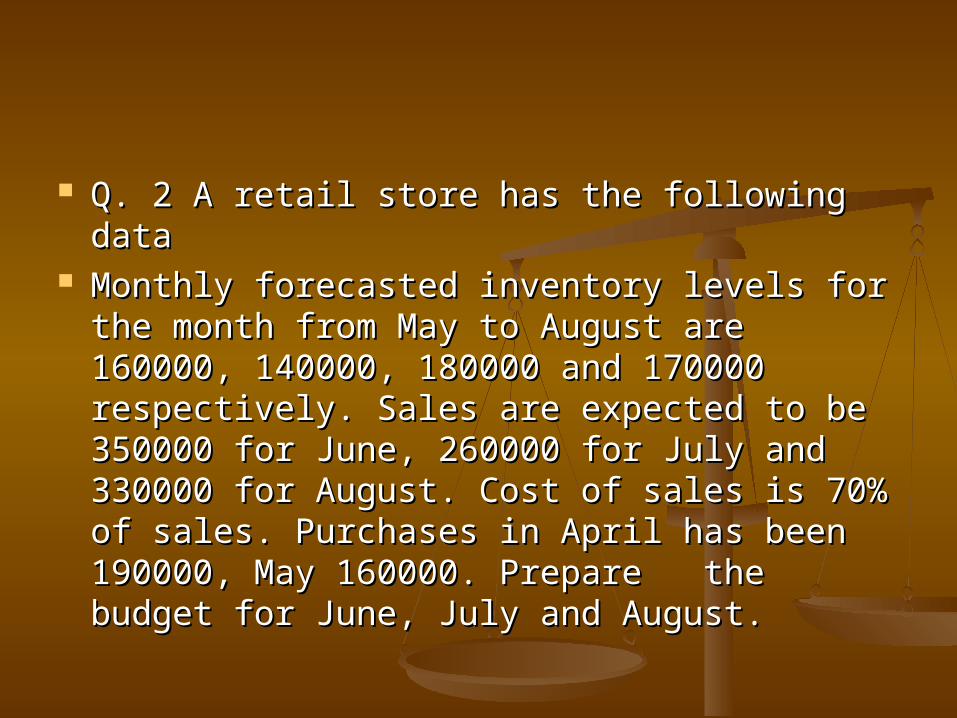

Q. 2 A retail store has the following dataQ. 2 A retail store has the following data Monthly forecasted inventory levels for the Monthly forecasted inventory levels for the

month from May to August are 160000, month from May to August are 160000, 140000, 180000 and 170000 respectively. 140000, 180000 and 170000 respectively. Sales are expected to be 350000 for June, Sales are expected to be 350000 for June, 260000 for July and 330000 for August. 260000 for July and 330000 for August. Cost of sales is 70% of sales. Purchases in Cost of sales is 70% of sales. Purchases in April has been 190000, May 160000. April has been 190000, May 160000. Prepare the budget for June, July and Prepare the budget for June, July and August. August.

CGS BudgetCGS Budget

Company NameCompany NameCost of Goods Sold BudgetCost of Goods Sold BudgetDateDateDirect materials Inventory1.1Direct materials Inventory1.1Add: net material purchaseAdd: net material purchaseDirect material available for useDirect material available for useLess direct material inventory 31.12Less direct material inventory 31.12Direct material usedDirect material used

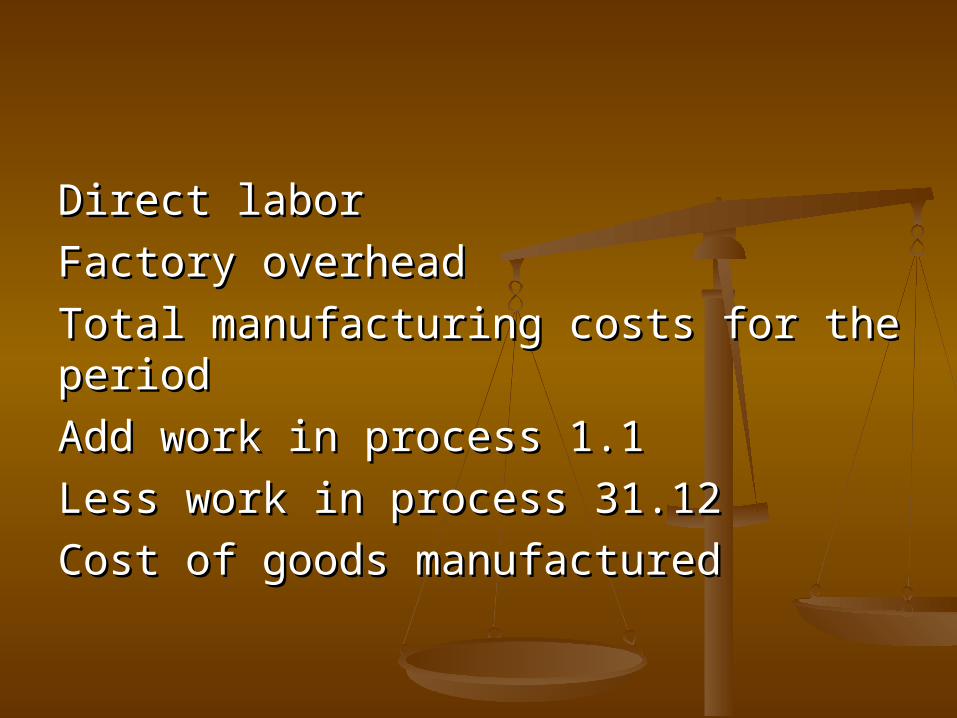

Direct laborDirect labor

Factory overheadFactory overhead

Total manufacturing costs for the Total manufacturing costs for the periodperiod

Add work in process 1.1Add work in process 1.1

Less work in process 31.12Less work in process 31.12

Cost of goods manufacturedCost of goods manufactured

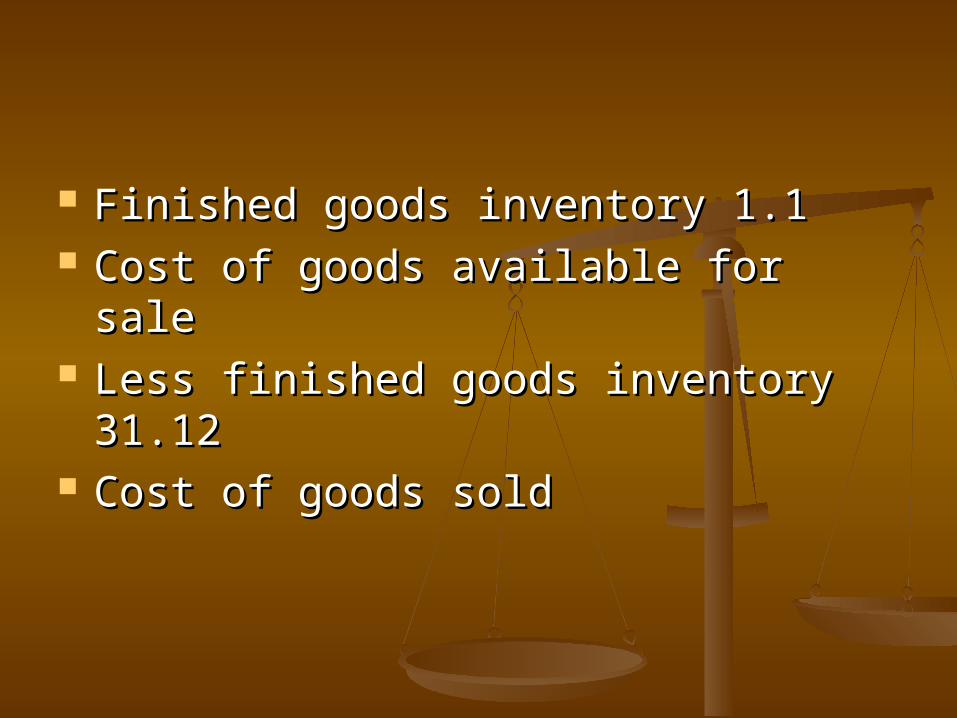

Finished goods inventory 1.1Finished goods inventory 1.1 Cost of goods available for saleCost of goods available for sale Less finished goods inventory 31.12Less finished goods inventory 31.12 Cost of goods soldCost of goods sold

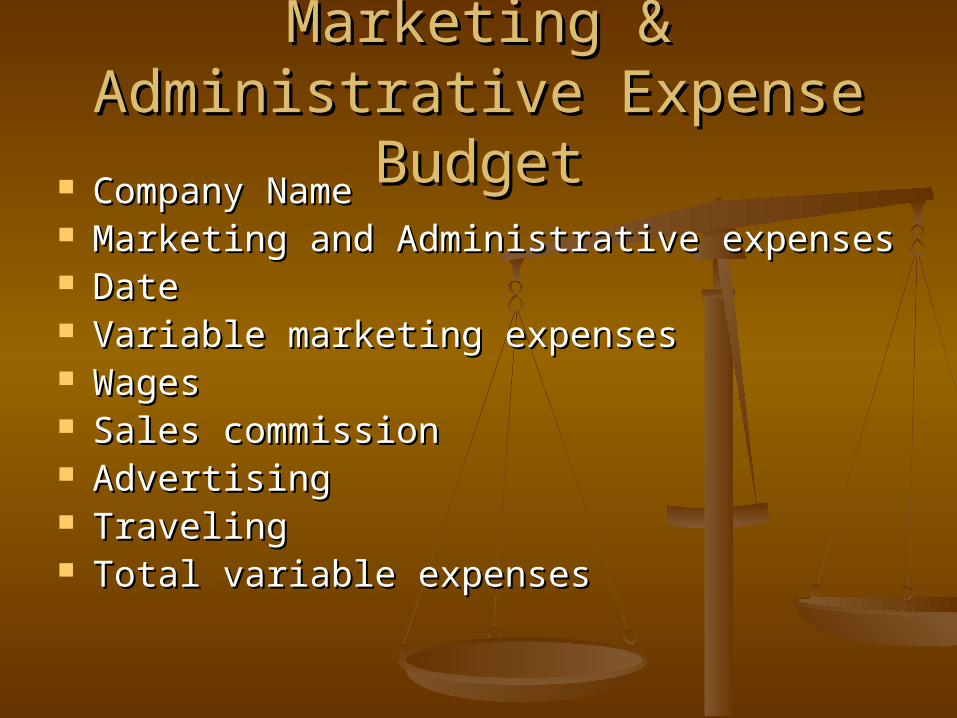

Marketing & Administrative Marketing & Administrative Expense BudgetExpense Budget

Company NameCompany Name Marketing and Administrative expensesMarketing and Administrative expenses DateDate Variable marketing expensesVariable marketing expenses WagesWages Sales commission Sales commission AdvertisingAdvertising TravelingTraveling Total variable expenses Total variable expenses

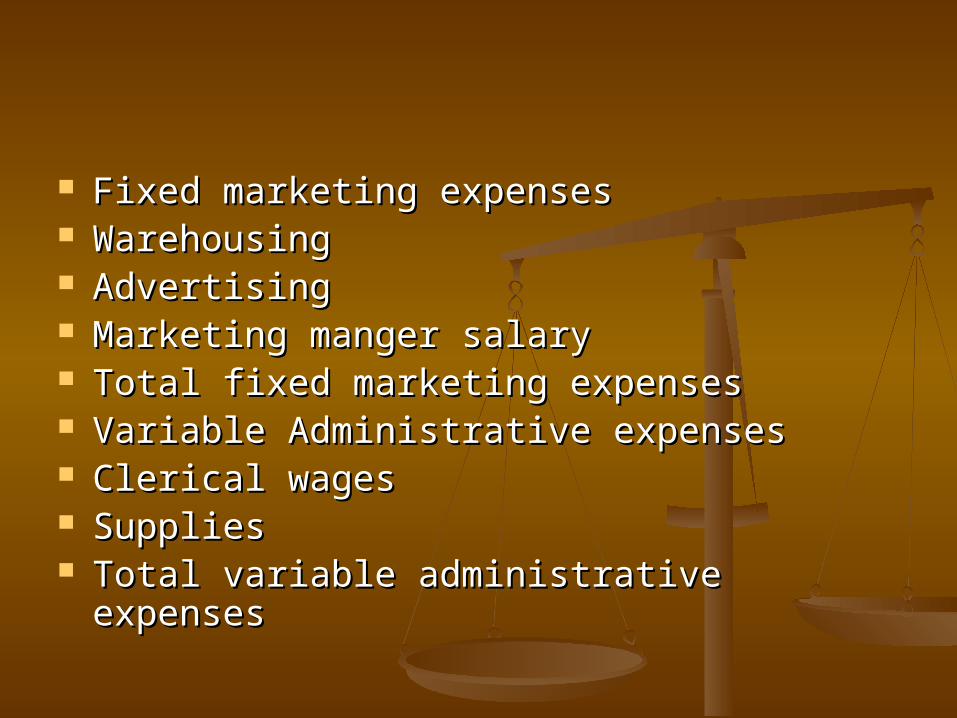

Fixed marketing expensesFixed marketing expenses WarehousingWarehousing Advertising Advertising Marketing manger salary Marketing manger salary Total fixed marketing expensesTotal fixed marketing expenses Variable Administrative expensesVariable Administrative expenses Clerical wagesClerical wages Supplies Supplies Total variable administrative expensesTotal variable administrative expenses

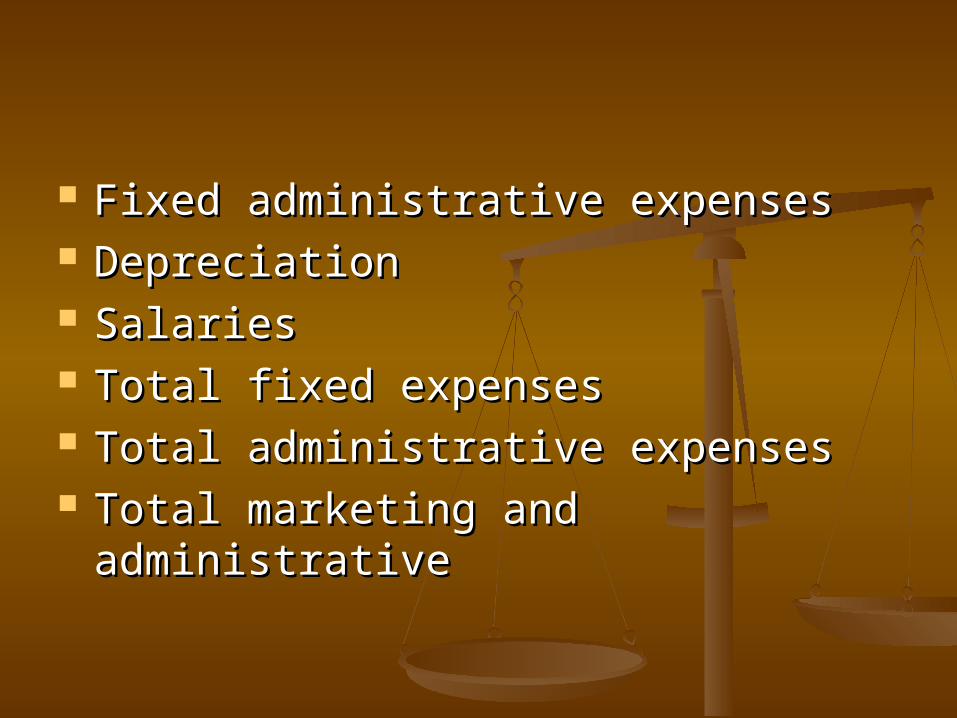

Fixed administrative expensesFixed administrative expenses Depreciation Depreciation Salaries Salaries Total fixed expensesTotal fixed expenses Total administrative expensesTotal administrative expenses Total marketing and administrative Total marketing and administrative

Budget for a new product Budget for a new product PhasePhase Planning Planning Production PromotionProduction Promotion

Expenses Expenses xxxx xxxx xxxx Direct MaterialDirect Material xxxx xxxx

xxxx Labor costLabor cost Consulting feesConsulting fees Indirect Labor Indirect Labor

Supplies Supplies Equipment Equipment OverheadOverhead Total Total xxxx xxxx

xxxx

Estimated machine hours Estimated machine hours Completion date Completion date

ABC is a manufacturing company. ABC is a manufacturing company. Actual sales for the first quarter of Actual sales for the first quarter of 2001 and projects sales from April 2001 and projects sales from April and may are as follows:and may are as follows:

Jan (actual sales)Jan (actual sales)……………… 300000 300000 Feb (actual)Feb (actual)…………………………. 308000. 308000 March (actual)March (actual)…………………… 312000 312000 April projected April projected ………………... 316000... 316000 May projectedMay projected……………………..322000..322000

The company collects 60% of its sales The company collects 60% of its sales during the month in which the sale is during the month in which the sale is made, 25% during the following month and made, 25% during the following month and 15% in the second month. ABC pays for 15% in the second month. ABC pays for purchases the same amounts it pays for purchases the same amounts it pays for sales but their payment policy is as follows: sales but their payment policy is as follows: 40% are paid during the month of purchase 40% are paid during the month of purchase and 60% during the following month. and 60% during the following month. Merchandise is purchased in the month Merchandise is purchased in the month proceeding the sale. The company plans to proceeding the sale. The company plans to maintain the current level of inventory.maintain the current level of inventory.

To meet loan obligations there must be a To meet loan obligations there must be a cash balance of $25000 on hand at the end cash balance of $25000 on hand at the end of April. Other cash payments anticipated of April. Other cash payments anticipated during April are salaries 58000, other during April are salaries 58000, other expenses 12000 and equipment purchase expenses 12000 and equipment purchase 15000. the cash balance at 1. April id 1800.15000. the cash balance at 1. April id 1800.

Required : prepare a cash budget for April. Required : prepare a cash budget for April. Will the company need additional financing Will the company need additional financing for to maintain the required ending cash for to maintain the required ending cash balance?balance?

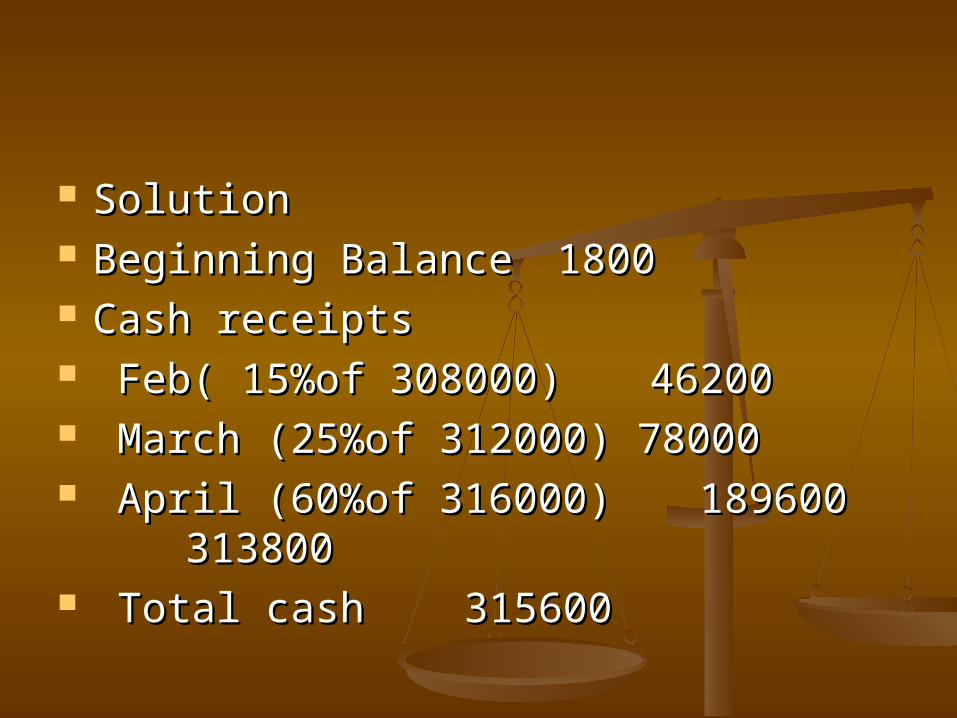

Solution Solution Beginning BalanceBeginning Balance 18001800 Cash receiptsCash receipts Feb( 15%of 308000)Feb( 15%of 308000) 4620046200 March (25%of 312000) 78000March (25%of 312000) 78000 April (60%of 316000)April (60%of 316000) 189600 189600313800313800 Total cash Total cash 315600315600

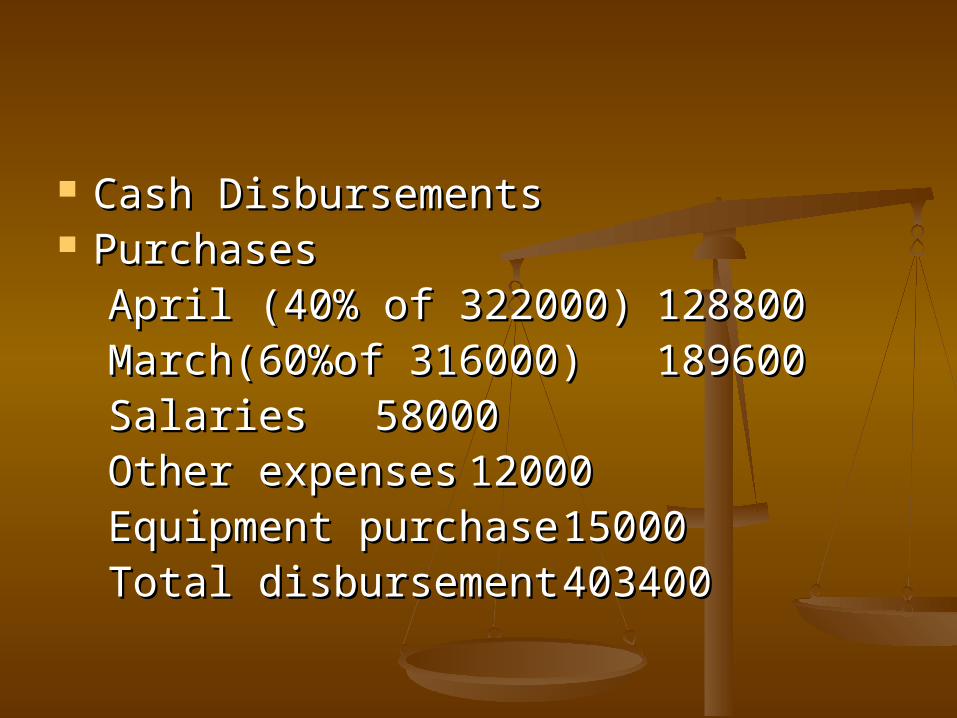

Cash DisbursementsCash Disbursements PurchasesPurchases April (40% of 322000)April (40% of 322000) 128800128800 March(60%of 316000)March(60%of 316000) 189600189600 SalariesSalaries 5800058000 Other expensesOther expenses 1200012000 Equipment purchaseEquipment purchase 1500015000 Total disbursementTotal disbursement 403400403400

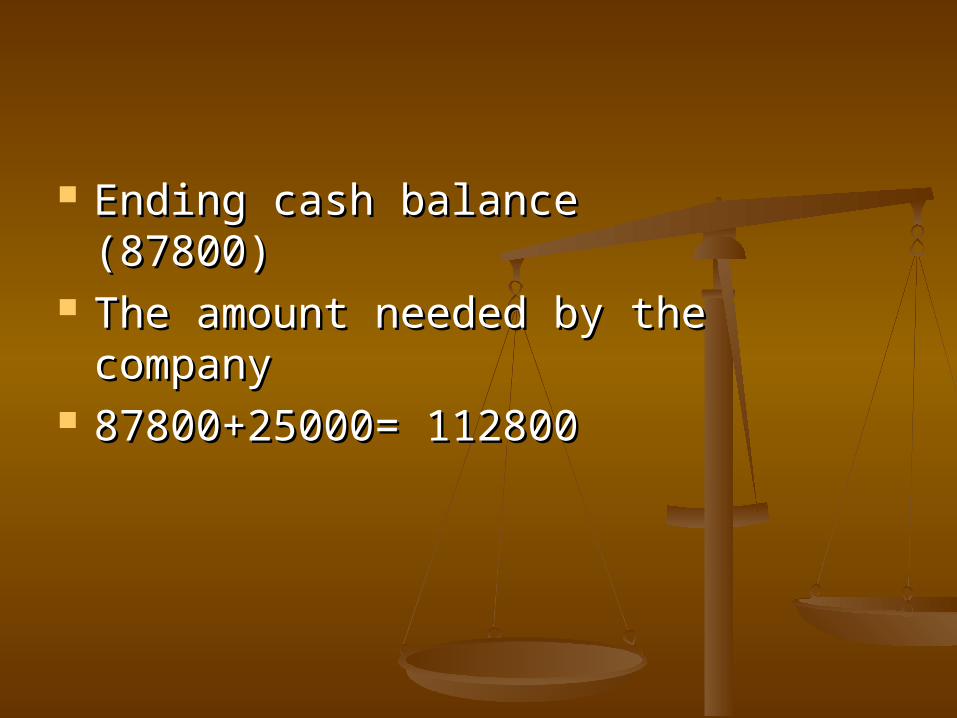

Ending cash balanceEnding cash balance (87800)(87800) The amount needed by the company The amount needed by the company 87800+25000= 11280087800+25000= 112800

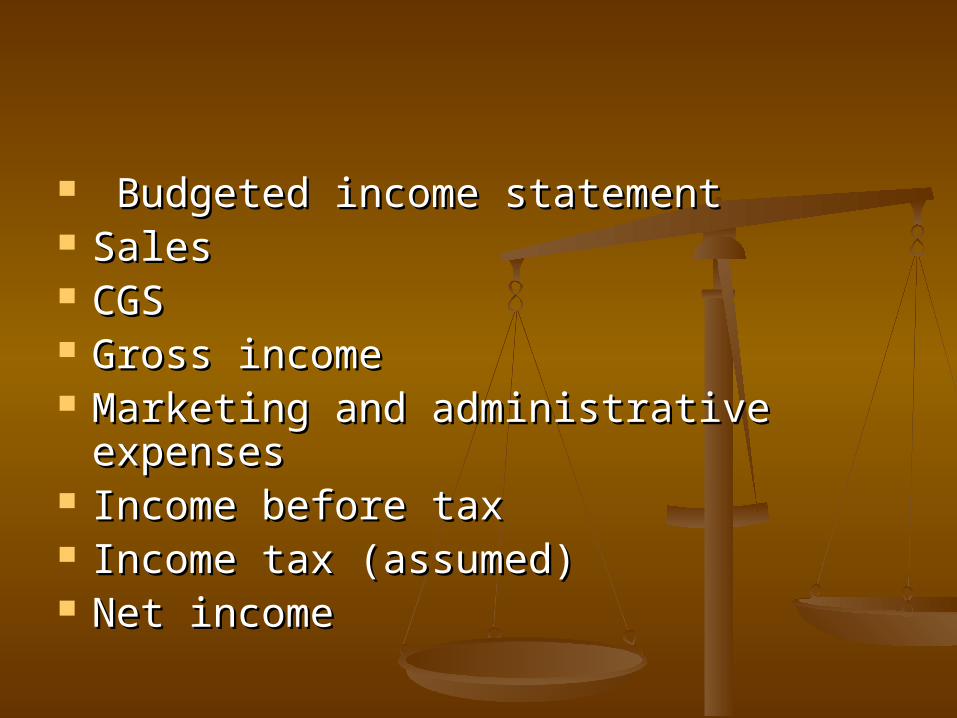

Budgeted income statementBudgeted income statement SalesSales CGSCGS Gross incomeGross income Marketing and administrative Marketing and administrative

expensesexpenses Income before taxIncome before tax Income tax (assumed)Income tax (assumed) Net incomeNet income

Budgeted statement of financial Budgeted statement of financial PositionPosition

CashCash Accounts receivableAccounts receivable Direct material inventoryDirect material inventory Work in process inventory Work in process inventory Finished goods inventory Finished goods inventory Total current AssetsTotal current Assets Plant assetsPlant assets

Plant assetsPlant assets LandLand Building Building Less accumulated depreciationLess accumulated depreciation EquipmentsEquipments Less Accumulated depreciationLess Accumulated depreciation Total plant assetsTotal plant assets

Current liabilitiesCurrent liabilities Accounts payableAccounts payable Income tax payableIncome tax payable Total current liabilitiesTotal current liabilities Owners Equity Owners Equity Common stock Common stock Retained earnings( income Retained earnings( income –– dividends) dividends) Total owners equityTotal owners equity Total liabilities and owners equityTotal liabilities and owners equity