the changing competitive landscape h&m likely to be a

TRANSCRIPT

KEY CONCLUSIONS

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

Equity Research EMEA

Apparel

23 July 2015

South African Apparel Retail INDUSTRY OVERVIEW/ANALYSIS

The Ideas Engine

series showcases

Credit Suisse’s unique

insights and investment ideas.

Please contact your

Sales person to

access the

supplemental

analysis behind this

report.

The changing competitive landscape

Drivers of change

The South African apparel retail market has undergone significant change over the past

five years, and we view most of these changes as structural rather than cyclical. Credit

provided by retailers does not appear to be a meaningful driver of overall apparel sales,

and reduced credit from retailers has been replaced by other credit providers. This

provides consumers with more choice and the ability to take advantage of lower price

points from fast/value fashion, which remains underpenetrated in South Africa. New

entrants are likely to continue to take share from higher-priced domestic players, with

H&M posing a meaningful threat, in our view.

Introducing the Credit Suisse Apparel Price Monitor

We introduce the Credit Suisse Apparel Price Monitor to help assess the relative price

positioning of companies within the industry, track changes in pricing and monitor the

price points of new entrants. Our pricing analysis leaves us with significant concerns over

the sustainability of Truworths' currently world-leading margins as well as the potential

competitive threat from H&M's entry into the South African market later this year.

Key stock calls

In our view, Truworths is most exposed to the structural challenges facing the industry,

and we downgrade our rating to Underperform from Neutral (new TP R65 from R78).

Mr Price (Outperform, new TP R283 from R272) provides the best exposure to global

trends in fast/value fashion and lower consumer reliance on credit provided by retailers.

The Foschini Group's (Neutral, new TP R150 from R165) and Woolworths' (Neutral, new

TP R94 from R86) more diversified income streams and lower price points suggest to us

that they are less at risk than Truworths.

This note replaces the version published earlier in which the company Financial Summaries on pages 6 to 9 showed only historic data. These have now been replaced to include our forecasts.

Figure 1: H&M likely to be a meaningful threat; Mr Price

competitive: Combined men's and women's basket comparison,

Apr-Jun '15, H&M estimated entry point=100

Source: Retailpricewatch.co.za, Credit Suisse research

Figure 2: Truworths' margins in line with TFG's at similar

price points

Source: Company data, Credit Suisse research

RESEARCH ANALYSTS

Pieter Vorster 44 20 7883 2607 [email protected]

Rishay Dhanraj 27 11 012 80 63 [email protected]

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, AND THE STATUS OF NON-U.S ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

183

168

141

122117

106 105 104 100

83

55 52 47 4534

0

20

40

60

80

100

120

140

160

180

200

Dan

iel H

echt

er

Zara

Truw

orth

s

Fosc

hini

/ M

arkh

am

Cot

ton

On

Edga

rs

Iden

tity

Woo

lwor

ths

H&M

est

imat

e

Exac

t!

Acke

rman

s

Legi

t

Jet

Mr P

rice

Pep

Year to Jun 2014 R'm Reported

At Foschini

prices % change

Retail Turnover 10 458 8 715 -16.7

Gross profit 5 841 4 098 -29.8

Gross margin (%) 55.9 47.0

EBITDA 3 273 1 530 -53.3

Operating costs -2 568 -2 568 0.0

Retail profit 3 089 1 346 -56.4

Trade receivable interest income 828 690 -16.7

Debtors cost -916 -763 -16.7

Trading profit 3 236 1 508 -53.4

Trading margin (%) 30.9 17.3

Net profit 2 406 1 167 -51.5

Fully diluted EPS (cents) 568 275 -51.5

IDEAS ENGINE SERIES

IDEAS ENGINE 2

South African Apparel Retail

Key charts

Figure 3: Superior growth should continue at Mr Price; we expect Truworths'

growth to be modest owing to margin pressure

Source: Credit Suisse estimates

Figure 4: Edcon's weakness appears to have shielded other retailers from

structural trends

Source: Company data, Euromonitor, Stats SA, Credit Suisse estimates

Figure 5: Fast/value fashion growing globally, underpenetrated in South Africa

Source: Euromonitor

Figure 6: Other, non-bank, credit providers have filled the gap left by credit

retailers, giving consumers the ability to take advantage of lower prices

elsewhere

Source: NCR

Turnover growth CY15 CY16 CY17 CY18

Mr Price 14.4% 15.0% 15.0% 14.9%

TFG 24.5% 15.1% 10.9% 11.1%

Truworths 9.5% 9.8% 8.8% 8.6%

Woolworths 31.6% 9.1% 9.2% 8.8%

Gross margin (%)

Mr Price 42.9% 43.5% 43.5% 43.5%

TFG (South Africa) 47.3% 47.1% 46.8% 46.6%

Truwroths 54.5% 53.5% 52.2% 50.7%

Woolworths 38.4% 38.4% 38.4% 38.3%

EBIT growth

Mr Price 20.7% 19.1% 18.9% 18.8%

TFG 17.7% 13.4% 11.2% 9.6%

Truworths 5.7% 6.7% 4.7% 3.7%

Woolworths 30.6% 15.7% 14.6% 12.3%

EBIT margin

Mr Price 18.5% 19.1% 19.8% 20.5%

TFG 16.5% 16.3% 16.3% 16.1%

Truworths 29.2% 28.3% 27.3% 26.1%

Woolworths 10.4% 11.0% 11.6% 11.9%

EPS growth

Mr Price 17.8% 17.1% 18.1% 18.0%

TFG 13.6% 12.5% 12.2% 10.6%

Truworths 6.4% 7.6% 5.7% 4.4%

Woolworths 7.7% 15.0% 18.3% 15.3%

% market share 2008 2009 2010 2011 2012 2013 2014 Trend

Edcon 22.3 22.4 21.2 20.9 19.8 18.6 17.7

Edgars 12.5 12.5 12.0 11.8 11.3 10.5 10.0

Discount 9.8 9.9 9.2 9.1 8.4 8.1 7.7

Pepkor 13.9 13.5 13.9 14.3 14.6 14.6 14.5

Mr. Price 6.1 6.8 7.0 7.1 7.2 7.5 8.0

Mr. Price 5.0 5.6 6.0 6.1 6.1 6.5 7.0

Milady's 1.2 1.1 1.1 1.1 1.1 1.1 1.0

Truworths 6.9 7.6 7.8 8.1 8.2 8.1 7.9

Woolworths 8.6 8.5 8.5 8.5 8.7 8.6 8.6

TFG 6.0 6.2 6.5 7.0 7.2 7.2 7.3

Sub-total 63.8 65.0 64.9 65.9 65.8 64.6 64.0

Other 36.2 35.0 35.1 34.1 34.2 35.4 36.0

Total 100.0 100.0 100.0 100.0 100.0 100.0 100.0

0

5

10

15

20

25

30

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

% m

arke

t sha

re

France Germany Italy South Africa

Spain Sweden United Kingdom

0%

2%

4%

6%

8%

10%

12%

2007

Q4

2008

Q1

2008

Q2

2008

Q3

2008

Q4

2009

Q1

2009

Q2

2009

Q3

2009

Q4

2010

Q1

2010

Q2

2010

Q3

2010

Q4

2011

Q1

2011

Q2

2011

Q3

2011

Q4

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2015

Q1

Retailers Other credit providers

IDEAS ENGINE 3

South African Apparel Retail

Investment summary

The South African apparel retail market has undergone significant change over the past five

years and we view most of these changes as structural rather than cyclical. We have

analysed the drivers of these changes and look at how these factors might play out over the

next three-to-five years.

In this report we also introduce the Credit Suisse Apparel Price Monitor to help us assess the

relative price positioning of companies within the industry, track changes in pricing and

monitor the price points of new entrants. Our pricing analysis leaves us with significant

concerns over the sustainability of Truworths' currently world-leading margins as well as the

potential competitive threat from H&M's entry into the South African market later this year.

We highlight four major drivers of change in the market:

− Weak credit sales growth – our analysis shows that although its origin may be cyclical,

its effect is likely lasting and structural.

− Strong cash sales growth – on the face of it, the flipside of weak credit sales growth,

but continued growth in fast/value fashion has a strong global trend underpin and in South

Africa this is likely to be further supported by what we view as structural change in the

credit retail sales market.

− The rising presence of multinational players – we see continued growth in market

share from foreign entrants, which is likely to accelerate significantly with the entry of

H&M in October 2015; this trend will also add downward pressure on margins, particularly

of the credit retailers.

− Edcon as a source of market share – in our view the consistent market share declines

of market leader Edcon have softened the near-term structural negative effects of the

traditional domestic players. The recently announced subordinated debt renegotiation

provides the group with a near-term buffer, while further restructuring could position it

better, potentially making it a more effective competitor.

Weak credit sales – a structural change in the way consumers fund their spending

Whilst the state of the consumer credit market may be an important revenue driver for those

retailers whose sales are predominantly on credit, it does not appear to have a meaningful

impact on the overall level of Apparel and Footwear sales in South Africa. Furthermore,

consumers now have access to a larger variety of credit sources and have become less reliant

on store credit, in our view. This has enabled traditional store credit customers to access still

aspirational, but substantially lower-priced, retailers such as Mr Price. We believe that consumer

behaviour has changed and that, even when credit conditions ease, we are unlikely to see the

same uptick in credit sales as one might have expected based on previous cycles.

Cash sales – the new credit sales, supported by global trends in fast/value fashion

Although Mr Price's strong performance over the past five years could be attributed to a

combination of weak sales at competitor Edcon and its value for money offering resonating with

a consumer under pressure on multiple fronts, including restricted availability of credit, we

believe the development is structural and in line with global trends which has seen significant

growth in the fast/value fashion segment of the market.

Multinationals – a rising threat to domestic players

In 2011, both Cotton On and Inditex entered the South African market and H&M is set to open

its first store in the country in October 2015. In addition, Edcon has introduced Topshop into

its Edgars stores in 2012 and opened its first standalone Topshop store in 2013.

We expect Cotton On to continue to grow from its current base of 118 stores and view H&M as

a major risk to the likes of Truworths and Foschini and, to some extent, Edgars and

Woolworths, given its likely price points, whereas we expect Zara's relatively high price points to

keep it a relatively small, albeit growing participant.

Both Inditex and H&M have shown that they can operate successfully in southern hemisphere

markets and we believe their success in Australia is of particular relevance in South Africa.

H&M stands out, capturing c.1.7% of the Australian market after only one year. We are not

forecasting the same rate of market share capture in South Africa given differences in the

geographic distribution of retail sales, but nonetheless view it as a meaningful threat to

domestic players, particularly with respect to pricing and margins.

Assuming H&M positions its price points in South Africa relative to Zara in line with where it is

in the UK, we think this would place it at the low end of fashion retailers in South Africa, with

Woolworths' and Edgars' price points at a premium to H&M of 4% and 6%, respectively,

Cotton On at a 17% premium, Foschini at 22% and Truworths 41% more expensive. Mr Price

would be at a 55% discount to H&M, which is not dissimilar to the relative price positioning of

Primark to H&M in the UK.

Our key stock calls

In our view, Truworths is most exposed to the structural challenges facing the industry, and we

downgrade our rating to Underperform from Neutral (new TP R65 from R78). Mr Price

(Outperform, new TP R283 from R272) provides the best exposure to global trends in

fast/value fashion, in our view, as well as lower consumer reliance on credit provided by

retailers. TFG's (Neutral, new TP R150 from R165) and Woolworths' (Neutral, new TP R94

from R86) more diversified income streams and lower price points suggest to us that they are

less at risk than Truworths.

Truworths International – Downgrade to Underperform, reducing target price by 15%

We downgrade our rating on Truworths to Underperform from Neutral and reduce our DCF-

based target price by 15% to R65 (from R78), indicating potential downside of 26%. We cut

our FY16-18 fully diluted adjusted EPS estimates by 5-16%, leaving us 11% below

I/B/E/S consensus in FY18.

Truworths currently generates the highest operating margin in our global apparel coverage

universe. Our analysis shows that, relative to its closest domestic peer, TFG, this is largely a

function of higher and, in our view, unsustainable price points.

IDEAS ENGINE 4

South African Apparel Retail

While Truworths' CY16E PE multiple appears to offer value, we show that on a pro forma

basis, at TFG's price points, it would generate operating margins in line with TFG and EPS

some 50% below current levels.

With some 70% of group sales on credit, Truworths has by far the highest exposure to the

changing credit market dynamics outlined in this report. Not only does it potentially restrict

sales growth, but as alternative sources of consumer credit provide credit customers with the

ability to make cash purchases and more choice, the high price premiums charged by

Truworths look increasingly unsustainable.

We believe Truworths also faces the largest threat from international competition. Although

its average price points are currently below those of Zara, it is likely to lose higher-end

customers to it. Cotton On's average pricing is c.17% lower than Truworths', with an

offering that appears to be resonating well with the under 25-year-old, mid-to-high LSM

segment. We view H&M as a key risk for Truworths.

Excluding acquisitions, we expect revenue growth to remain below 9% p.a. with like-for-like

growth at 4% p.a. (1.3% in FY15) over the next five reporting years and forecast gross

margins to decline from 55.9% in FY14 to 50.0% in FY19 owing to pricing pressure. This

margin would still be higher than the 47.3% achieved by TFG in FY15E and the 46.5% we

forecast for TFG in FY19.

At the EPS level, we forecast growth of only 5.5% per annum over the next five years, with

improved bad debts more than offset by gross margin and other cost pressures.

Although Truworths' recent trading statement surprised positively, we believe the implied

margin reductions may signal a change in the company's long-standing philosophy of not

sacrificing margin for growth and we expect this trend to accelerate under new management.

In its trading statement covering the period to 28 June 2015, Truworths announced that it

expects growth in HEPS of 2-4%, in line with our estimate of 3.8%, but ahead of consensus

growth of 1.9%. However, its revenue growth of 8.2% exceeded our estimate of 6.7%.

Excluding the recently acquired Naartjie and Earthchild brands, growth amounted to 7.2%.

Owing to the stable cash flow growth of the retail industry, we believe it is appropriate to

value Truworths using the discounted cash flow (DCF) methodology. We forecast explicit

cash flows for five years, after which the growth rate free cash flow return in invested capital

is faded to the final year growth rate and WACC respectively over the competitive advantage

period (CAP). Our DCF fair value is adjusted by the WACC to determine our 12-month

target price of R65. For Truworths, we use a 13.25% WACC, 10-year CAP and a final year

growth rate of 6%. Our target price change largely reflects our lower earnings estimates (our

FY19 earnings estimates are 23% below our previous forecast).

Mr Price Group Limited – Retain Outperform, raise target price

We retain our recently upgraded rating at Outperform (Mr Price Group Limited - Upgrade

to Outperform) and increase our DCF-based target price to R283 from R272.

Mr Price has shown strong growth in market share over the past five years, rising from 5.6%

in 2009 to 7.0% in 2014. In our view, this growth has resulted from a combination of global

trends favouring fast/value fashion, supported by structural change in the South African retail

credit market and attractive price points that are currently only about one third of Truworths'.

Our analysis shows that the South African fast/value segment remains underpenetrated and

we expect Mr Price, the leading player in this segment, to continue to gain share.

With Mr Price's average basket currently at 27% of Zara, 38% of Cotton On and 45% of

where we estimate H&M will likely enter the market, we do not view increased participation

by multinational players as a meaningful threat to Mr Price's growth prospects in the apparel

segment.

With its full-year results, Mr Price has announced that it intends to enter the Australian

market with two trial stores and indicated that it would have pricing relative to Cotton On

similar to its position in South Africa, i.e. some 60% below. We have not factored in any

contribution from Australia, but estimate that it can contribute between 5% and 10% of

group earnings over the next 3-5 years.

Over the next five years, we expect Mr Price to deliver diluted EPS growth of 17.6% p.a.,

which is the highest in our coverage universe by some margin.

Owing to the stable cash flow growth of the retail industry, we believe it is appropriate to

value Mr Price using the discounted cash flow (DCF) methodology. We forecast explicit cash

flows for five years, after which the growth rate free cash flow return in invested capital is

faded to the final year growth rate and WACC respective over the competitive advantage

period (CAP). Our DCF fair value is adjusted by the WACC to determine our 12-month

target price of R283. For Mr Price, we use a 12.02% WACC, 23-year CAP and a final year

growth rate of 7.5%. Our target price increase reflects a one-year increase in our CAP

assumption owing to our increased confidence in the sustainability of Mr Price's growth and

returns, partly offset by an increase in the number of shares issued under the group's share

incentive schemes.

The Foschini Group – Retain Neutral, reduce estimates and target price

We reduce our DCF-based target price by 9% from R165 to R150 and retain our Neutral

rating and cut our FY16-18 diluted HEPS estimates 2-7%, leaving us 7% below consensus

in FY18.

TFG's credit fashion apparel businesses, Foschini and Markham, face the same competitive

pressures as Truworths, except that TFG's average basket is priced 13-17% below that of

Truworths'. These two divisions made up 42% of TFG's FY14 revenue, with this likely to fall

to below 35% in FY16 when the Phase Eight acquisition is included for a full year.

For the South African Clothing division (56% of FY16E group turnover), we forecast growth

of 10% p.a. over the next five years, with LFL growth of 5% in FY16, rising to 6% in

subsequent years. This is ahead of the 4% we forecast for Truworths partly because we

expect less price pressure at TFG's fashion apparel businesses given lower price points, and

partly because we expect higher growth from its sports businesses that make up around

30% of divisional revenue.

From FY16-20 we expect group gross margins in South Africa to decline by some 100bps,

which implies a reduction at Foschini and Markham of around 250bps, which is less than half

the decline we are forecasting at Truworths owing to its lower relative price points.

At the EPS level, we forecast growth of 12% p.a. over the next five years, which is more

than double the rate we expect at Truworths.

IDEAS ENGINE 5

South African Apparel Retail

Owing to the stable cash flow growth of the retail industry, we believe it is appropriate to

value TFG using the discounted cash flow (DCF) methodology. We forecast explicit cash

flows for five years, after which the growth rate free cash flow return in invested capital is

faded to the final year growth rate and WACC respective over the competitive advantage

period (CAP). Our DCF fair value is adjusted by the WACC to determine our 12-month

target price of R150. For TFG, we use a 12.1% WACC, 11-year CAP and a final year

growth rate of 6.% Our target price reduction is largely a function of our lower earnings

estimates.

Woolworths Holdings Limited – Retain Neutral, raise target price

We retain our Neutral rating on Woolworths and raise our DCF-based target price to R94

from R86.

Although Woolworths' South African apparel business is not immune to the threat of

international competition and fast/value fashion trends, it operates at lower price points than

the credit retailers.

Furthermore, Clothing and General Merchandise accounts for only 20% of FY16E group

revenue and 34% of operating profit. We are cautious on this division and forecast turnover

growth of around 9% p.a. over the next five years, modestly above Truworths'. We are not

forecasting margin declines, but believe the group's FY17 margin target of 19% for this

division is at risk – we forecast 18.25%.

Offsetting this is continued good, albeit slowing growth in Food—at 13.5% in FY15E to slow

moderately to 13.1% by FY17E and restructuring benefits from David Jones in Australia.

Over the next five years we expect EPS growth of 14.5% p.a., which is second only to

Mr Price in our South African Apparel retail universe.

Owing to the stable cash flow growth of the retail industry, we believe it is appropriate to

value Woolworths using the discounted cash flow (DCF) methodology. We forecast explicit

cash flows for five years, after which the growth rate free cash flow return in invested capital

is faded to the final year growth rate and WACC respectively over the competitive advantage

period (CAP). Our DCF fair value is adjusted by the WACC to determine our 12-month target

price of R94. For Woolworths, we use a 12.25% WACC, 15-year CAP and a final year

growth rate of 5%. Our target price increase reflects an increase in invested capital used for

our terminal value to incorporate the David Jones acquisition, partly offset by a lower CAP

assumption.

IDEAS ENGINE 6

South African Apparel Retail

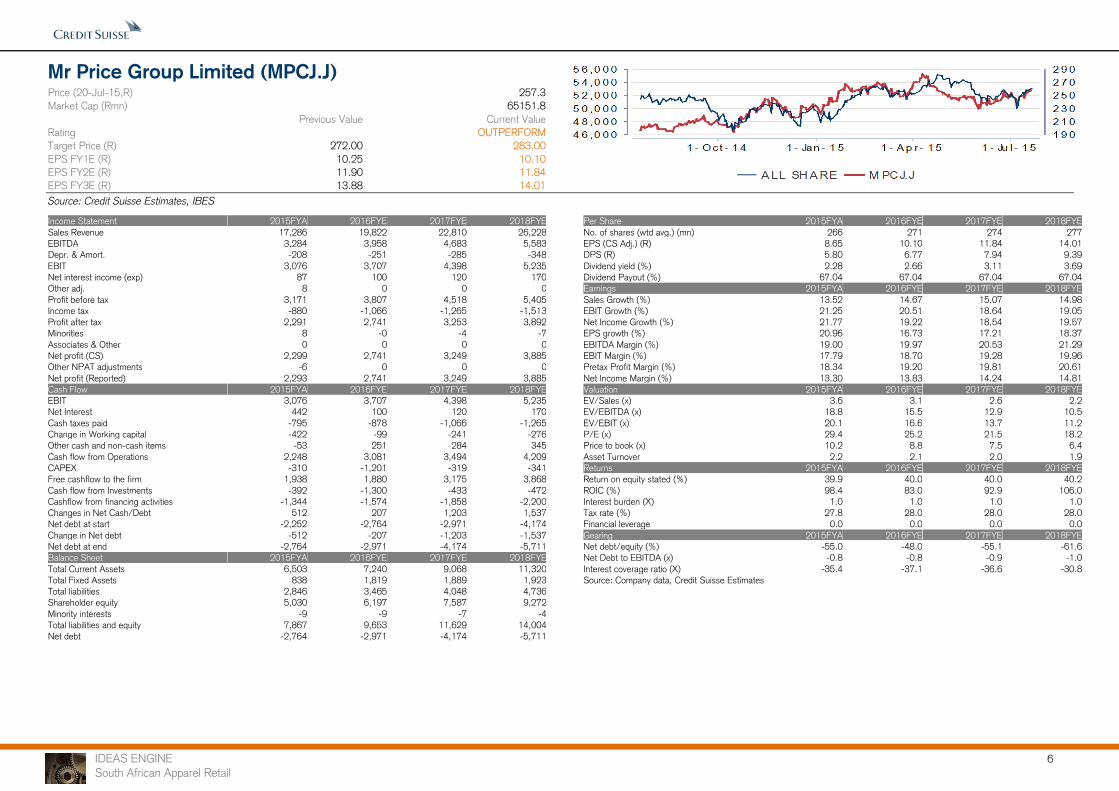

Mr Price Group Limited (MPCJ.J)

Price (20-Jul-15,R) 257.3

Market Cap (Rmn) 65151.8

Previous Value Current Value

Rating OUTPERFORM

Target Price (R) 272.00 283.00

EPS FY1E (R) 10.25 10.10

EPS FY2E (R) 11.90 11.84

EPS FY3E (R) 13.88 14.01

Source: Credit Suisse Estimates, IBES

Income Statement 2015FYA 2016FYE 2017FYE 2018FYE

Sales Revenue 17,286 19,822 22,810 26,228

EBITDA 3,284 3,958 4,683 5,583

Depr. & Amort. -208 -251 -285 -348

EBIT 3,076 3,707 4,398 5,235

Net interest income (exp) 87 100 120 170

Other adj. 8 0 0 0

Profit before tax 3,171 3,807 4,518 5,405

Income tax -880 -1,066 -1,265 -1,513

Profit after tax 2,291 2,741 3,253 3,892

Minorities 8 -0 -4 -7

Associates & Other 0 0 0 0

Net profit (CS) 2,299 2,741 3,249 3,885

Other NPAT adjustments -6 0 0 0

Net profit (Reported) 2,293 2,741 3,249 3,885

Cash Flow 2015FYA 2016FYE 2017FYE 2018FYE

EBIT 3,076 3,707 4,398 5,235

Net Interest 442 100 120 170

Cash taxes paid -795 -878 -1,066 -1,265

Change in Working capital -422 -99 -241 -276

Other cash and non-cash items -53 251 284 345

Cash flow from Operations 2,248 3,081 3,494 4,209

CAPEX -310 -1,201 -319 -341

Free cashflow to the firm 1,938 1,880 3,175 3,868

Cash flow from Investments -392 -1,300 -433 -472

Cashflow from financing activities -1,344 -1,574 -1,858 -2,200

Changes in Net Cash/Debt 512 207 1,203 1,537

Net debt at start -2,252 -2,764 -2,971 -4,174

Change in Net debt -512 -207 -1,203 -1,537

Net debt at end -2,764 -2,971 -4,174 -5,711

Balance Sheet 2015FYA 2016FYE 2017FYE 2018FYE

Total Current Assets 6,503 7,240 9,068 11,320

Total Fixed Assets 838 1,819 1,889 1,923

Total liabilities 2,846 3,465 4,048 4,736

Shareholder equity 5,030 6,197 7,587 9,272

Minority interests -9 -9 -7 -4

Total liabilities and equity 7,867 9,653 11,629 14,004

Net debt -2,764 -2,971 -4,174 -5,711

Per Share 2015FYA 2016FYE 2017FYE 2018FYE

No. of shares (wtd avg.) (mn) 266 271 274 277

EPS (CS Adj.) (R) 8.65 10.10 11.84 14.01

DPS (R) 5.80 6.77 7.94 9.39

Dividend yield (%) 2.28 2.66 3.11 3.69

Dividend Payout (%) 67.04 67.04 67.04 67.04

Earnings 2015FYA 2016FYE 2017FYE 2018FYE

Sales Growth (%) 13.52 14.67 15.07 14.98

EBIT Growth (%) 21.25 20.51 18.64 19.05

Net Income Growth (%) 21.77 19.22 18.54 19.57

EPS growth (%) 20.96 16.73 17.21 18.37

EBITDA Margin (%) 19.00 19.97 20.53 21.29

EBIT Margin (%) 17.79 18.70 19.28 19.96

Pretax Profit Margin (%) 18.34 19.20 19.81 20.61

Net Income Margin (%) 13.30 13.83 14.24 14.81

Valuation 2015FYA 2016FYE 2017FYE 2018FYE

EV/Sales (x) 3.6 3.1 2.6 2.2

EV/EBITDA (x) 18.8 15.5 12.9 10.5

EV/EBIT (x) 20.1 16.6 13.7 11.2

P/E (x) 29.4 25.2 21.5 18.2

Price to book (x) 10.2 8.8 7.5 6.4

Asset Turnover 2.2 2.1 2.0 1.9

Returns 2015FYA 2016FYE 2017FYE 2018FYE

Return on equity stated (%) 39.9 40.0 40.0 40.2

ROIC (%) 98.4 83.0 92.9 106.0

Interest burden (X) 1.0 1.0 1.0 1.0

Tax rate (%) 27.8 28.0 28.0 28.0

Financial leverage 0.0 0.0 0.0 0.0

Gearing 2015FYA 2016FYE 2017FYE 2018FYE

Net debt/equity (%) -55.0 -48.0 -55.1 -61.6

Net Debt to EBITDA (x) -0.8 -0.8 -0.9 -1.0

Interest coverage ratio (X) -35.4 -37.1 -36.6 -30.8

Source: Company data, Credit Suisse Estimates

IDEAS ENGINE 7

South African Apparel Retail

The Foschini Group (TFGJ.J)

Price (20-Jul-15,R) 155.0

Market Cap (Rmn) 32705.8

Previous Value Current Value

Rating NEUTRAL

Target Price (R) 165.00 150.00

EPS FY1E (R) 10.44 10.26

EPS FY2E (R) 12.01 11.47

EPS FY3E (R) 13.84 12.89

Source: Credit Suisse Estimates, IBES

Income Statement 2015FYA 2016FYE 2017FYE 2018FYE

Sales Revenue 16,086 20,616 22,850 25,349

EBITDA 2,913 3,993 4,448 4,950

Depr. & Amort. -428 -650 -727 -815

EBIT 2,786 3,343 3,721 4,135

Net interest income (exp) -198 -300 -267 -252

Other adj. 302 0 0 0

Profit before tax 2,890 3,043 3,454 3,883

Income tax -754 -855 -971 -1,091

Profit after tax 2,137 2,188 2,484 2,792

Minorities -0 -31 -37 -44

Associates & Other -292 0 0 0

Net profit (CS) 1,844 2,157 2,446 2,748

Other NPAT adjustments 24 0 0 0

Net profit (Reported) 1,867 2,157 2,446 2,748

Cash Flow 2015FYA 2016FYE 2017FYE 2018FYE

EBIT 2,786 3,343 3,721 4,135

Net Interest -228 -320 -290 -280

Cash taxes paid -766 -749 -855 -971

Change in Working capital -998 -560 -521 -560

Other cash and non-cash items 300 654 731 821

Cash flow from Operations 1,095 2,368 2,786 3,146

CAPEX -670 -660 -663 -760

Free cashflow to the firm 425 1,709 2,123 2,386

Cash flow from Investments -1,780 -660 -663 -760

Cashflow from financing activities -2,898 -609 -1,809 -2,018

Changes in Net Cash/Debt -3,583 1,100 314 367

Net debt at start 2,659 6,242 5,142 4,828

Change in Net debt 3,583 -1,100 -314 -367

Net debt at end 6,242 5,142 4,828 4,461

Balance Sheet 2015FYA 2016FYE 2017FYE 2018FYE

Total Current Assets 11,608 12,488 13,521 14,629

Total Fixed Assets 2,197 2,331 2,409 2,516

Total liabilities 10,400 9,726 10,039 10,340

Shareholder equity 8,131 9,679 10,316 11,046

Minority interests 3 18 37 59

Total liabilities and equity 18,533 19,423 20,392 21,445

Net debt 6,242 5,142 4,828 4,461

Per Share 2015FYA 2016FYE 2017FYE 2018FYE

No. of shares (wtd avg.) (mn) 206 210 213 213

EPS (CS Adj.) (R) 8.95 10.26 11.47 12.89

DPS (R) 5.88 6.78 7.58 8.51

Dividend yield (%) 3.87 4.46 4.99 5.61

Dividend Payout (%) 65.71 66.04 66.04 66.04

Earnings 2015FYA 2016FYE 2017FYE 2018FYE

Sales Growth (%) 13.61 28.16 10.83 10.94

EBIT Growth (%) 10.62 19.98 11.30 11.12

Net Income Growth (%) 9.57 16.97 13.43 12.33

EPS growth (%) 10.31 14.67 11.81 12.33

EBITDA Margin (%) 18.11 19.37 19.47 19.53

EBIT Margin (%) 17.32 16.22 16.29 16.31

Pretax Profit Margin (%) 17.97 14.76 15.12 15.32

Net Income Margin (%) 11.46 10.46 10.71 10.84

Valuation 2015FYA 2016FYE 2017FYE 2018FYE

EV/Sales (x) 2.4 1.8 1.6 1.4

EV/EBITDA (x) 13.1 9.3 8.3 7.4

EV/EBIT (x) 13.7 11.1 9.9 8.8

P/E (x) 17.0 14.8 13.2 11.8

Price to book (x) 3.8 3.3 3.1 2.9

Asset Turnover 0.9 1.1 1.1 1.2

Returns 2015FYA 2016FYE 2017FYE 2018FYE

Return on equity stated (%) 24.3 24.2 24.5 25.7

ROIC (%) 13.0 16.2 17.6 19.1

Interest burden (X) 1.0 0.9 0.9 0.9

Tax rate (%) 32.8 28.1 28.1 28.1

Financial leverage 0.9 0.6 0.6 0.5

Gearing 2015FYA 2016FYE 2017FYE 2018FYE

Net debt/equity (%) 76.7 53.0 46.6 40.2

Net Debt to EBITDA (x) 2.1 1.3 1.1 0.9

Interest coverage ratio (X) 14.1 11.1 13.9 16.4

Source: Company data, Credit Suisse Estimates

IDEAS ENGINE 8

South African Apparel Retail

Truworths International Limited (TRUJ.J)

Price (20-Jul-15,R) 88.2

Market Cap (Rmn) 37866.7

Previous Value Current Value

Rating NEUTRAL UNDERPERFORM

Target Price (R) 78.00 65.00

EPS FY1E (R) 5.91 5.90

EPS FY2E (R) 6.76 6.41

EPS FY3E (R) 7.63 6.83

Source: Credit Suisse Estimates, IBES

Income Statement 2014FYA 2015FYE 2016FYE 2017FYE

Sales Revenue 10,458 11,314 12,526 13,642

EBITDA 3,424 3,566 3,868 4,103

Depr. & Amort. -203 -241 -277 -316

EBIT 3,240 3,344 3,610 3,807

Net interest income (exp) 89 110 147 195

Other adj. 36 0 0 0

Profit before tax 3,365 3,454 3,757 4,002

Income tax -952 -978 -1,064 -1,134

Profit after tax 2,413 2,475 2,693 2,868

Minorities -0 -0 -0 -0

Associates & Other -4 0 0 0

Net profit (CS) 2,409 2,475 2,693 2,868

Other NPAT adjustments -3 0 0 0

Net profit (Reported) 2,406 2,475 2,693 2,868

Cash Flow 2014FYA 2015FYE 2016FYE 2017FYE

EBIT 3,240 3,344 3,610 3,807

Net Interest 917 1,104 1,235 1,326

Cash taxes paid -984 -951 -978 -1,064

Change in Working capital -105 -264 -170 -180

Other cash and non-cash items -527 -772 -830 -834

Cash flow from Operations 2,541 2,461 2,867 3,054

CAPEX -275 -430 -376 -409

Free cashflow to the firm 2,266 2,031 2,491 2,645

Cash flow from Investments -287 -445 -393 -428

Cashflow from financing activities -1,991 -1,616 -1,677 -1,824

Changes in Net Cash/Debt 263 400 797 803

Net debt at start -1,325 -1,588 -1,988 -2,785

Change in Net debt -263 -400 -797 -803

Net debt at end -1,588 -1,988 -2,785 -3,587

Balance Sheet 2014FYA 2015FYE 2016FYE 2017FYE

Total Current Assets 6,716 7,472 8,571 9,674

Total Fixed Assets 934 1,151 1,279 1,403

Total liabilities 1,434 1,554 1,771 1,962

Shareholder equity 6,642 7,501 8,517 9,561

Minority interests 0 0 0 0

Total liabilities and equity 8,076 9,056 10,288 11,522

Net debt -1,588 -1,988 -2,785 -3,587

Per Share 2014FYA 2015FYE 2016FYE 2017FYE

No. of shares (wtd avg.) (mn) 424 420 420 420

EPS (CS Adj.) (R) 5.68 5.90 6.41 6.83

DPS (R) 3.85 4.00 4.35 4.63

Dividend yield (%) 4.39 4.56 4.95 5.28

Dividend Payout (%) 67.75 67.75 67.75 67.75

Earnings 2014FYA 2015FYE 2016FYE 2017FYE

Sales Growth (%) 7.10 8.18 10.72 8.91

EBIT Growth (%) -0.98 3.21 7.95 5.45

Net Income Growth (%) 0.04 2.76 8.77 6.52

EPS growth (%) 1.36 3.77 8.77 6.52

EBITDA Margin (%) 32.74 31.52 30.88 30.08

EBIT Margin (%) 30.98 29.56 28.82 27.90

Pretax Profit Margin (%) 32.18 30.53 29.99 29.33

Net Income Margin (%) 23.03 21.88 21.50 21.02

Valuation 2014FYA 2015FYE 2016FYE 2017FYE

EV/Sales (x) 3.4 3.2 2.8 2.5

EV/EBITDA (x) 10.5 10.0 9.0 8.3

EV/EBIT (x) 11.1 10.7 9.7 8.9

P/E (x) 15.4 14.9 13.7 12.8

Price to book (x) 5.0 4.5 4.0 3.6

Asset Turnover 1.3 1.2 1.2 1.2

Returns 2014FYA 2015FYE 2016FYE 2017FYE

Return on equity stated (%) 31.0 32.0 31.1 29.6

ROIC (%) 45.9 43.5 45.1 45.7

Interest burden (X) 1.0 1.0 1.0 1.1

Tax rate (%) 28.4 28.3 28.3 28.3

Financial leverage 0.0 0.0 0.0 0.0

Gearing 2014FYA 2015FYE 2016FYE 2017FYE

Net debt/equity (%) -23.9 -26.5 -32.7 -37.5

Net Debt to EBITDA (x) -0.5 -0.6 -0.7 -0.9

Interest coverage ratio (X) -36.4 -30.4 -24.6 -19.5

Source: Company data, Credit Suisse Estimates

IDEAS ENGINE 9

South African Apparel Retail

Woolworths Holdings Limited (WHLJ.J)

Price (20-Jul-15,R) 98.6

Market Cap (Rmn) 100234.5

Previous Value Current Value

Rating NEUTRAL

Target Price (R) 86.00 94.00

EPS FY1E (R) 3.96 3.96

EPS FY2E (R) 4.76 4.66

EPS FY3E (R) 5.70 5.58

Source: Credit Suisse Estimates, IBES

Income Statement 2014FYA 2015FYE 2016FYE 2017FYE

Sales Revenue 39,707 61,521 66,758 73,200

EBITDA 5,117 7,741 8,924 10,256

Depr. & Amort. -872 -1,559 -1,772 -1,977

EBIT 4,245 6,183 7,152 8,279

Net interest income (exp) -24 -1,210 -1,090 -990

Other adj. 185 204 224 246

Profit before tax 4,406 5,177 6,286 7,535

Income tax -1,114 -1,450 -1,810 -2,170

Profit after tax 3,292 3,727 4,476 5,365

Minorities -102 -0 -0 -0

Associates & Other -172 -149 0 0

Net profit (CS) 3,018 3,578 4,476 5,365

Other NPAT adjustments -233 -512 0 0

Net profit (Reported) 2,785 3,066 4,476 5,365

Cash Flow 2014FYA 2015FYE 2016FYE 2017FYE

EBIT 4,245 6,183 7,152 8,279

Net Interest -2 -1,220 -1,100 -1,000

Cash taxes paid -1,047 -1,114 -1,450 -1,810

Change in Working capital -407 13 102 126

Other cash and non-cash items 1,287 1,016 1,782 1,987

Cash flow from Operations 4,076 4,878 6,487 7,582

CAPEX -1,314 -2,615 -2,670 -2,562

Free cashflow to the firm 2,762 2,263 3,817 5,020

Cash flow from Investments -1,710 -26,162 -2,670 -2,562

Cashflow from financing activities -1,936 5,966 -2,744 -3,228

Changes in Net Cash/Debt 130 -15,426 1,072 1,792

Net debt at start -750 -880 14,546 13,474

Change in Net debt -130 15,426 -1,072 -1,792

Net debt at end -880 14,546 13,474 11,682

Balance Sheet 2014FYA 2015FYE 2016FYE 2017FYE

Total Current Assets 14,077 8,095 8,683 9,406

Total Fixed Assets 3,404 14,665 15,563 16,147

Total liabilities 15,317 27,909 27,888 27,304

Shareholder equity 6,629 14,906 16,637 18,774

Minority interests 323 107 107 107

Total liabilities and equity 22,269 42,922 44,632 46,186

Net debt -880 14,546 13,474 11,682

Per Share 2014FYA 2015FYE 2016FYE 2017FYE

No. of shares (wtd avg.) (mn) 801 903 961 961

EPS (CS Adj.) (R) 3.77 3.96 4.66 5.58

DPS (R) 2.72 2.86 3.36 4.03

Dividend yield (%) 2.80 2.94 3.46 4.15

Dividend Payout (%) 72.11 72.11 72.11 72.11

Earnings 2014FYA 2015FYE 2016FYE 2017FYE

Sales Growth (%) 12.72 54.94 8.51 9.65

EBIT Growth (%) 19.61 45.64 15.68 15.75

Net Income Growth (%) 16.44 18.54 25.10 19.86

EPS growth (%) 21.20 5.14 17.61 19.86

EBITDA Margin (%) 12.89 12.58 13.37 14.01

EBIT Margin (%) 10.69 10.05 10.71 11.31

Pretax Profit Margin (%) 11.10 8.41 9.42 10.29

Net Income Margin (%) 7.60 5.82 6.70 7.33

Valuation 2014FYA 2015FYE 2016FYE 2017FYE

EV/Sales (x) 2.5 1.8 1.7 1.5

EV/EBITDA (x) 19.1 14.6 12.6 10.8

EV/EBIT (x) 23.0 18.3 15.7 13.3

P/E (x) 25.8 24.5 20.8 17.4

Price to book (x) 9.7 5.3 5.1 4.6

Asset Turnover 1.8 1.4 1.5 1.6

Returns 2014FYA 2015FYE 2016FYE 2017FYE

Return on equity stated (%) 37.2 25.4 26.2 28.2

ROIC (%) 50.9 14.4 16.9 19.3

Interest burden (X) 1.0 0.8 0.9 0.9

Tax rate (%) 27.1 31.4 28.8 28.8

Financial leverage 1.1 0.9 0.8 0.6

Gearing 2014FYA 2015FYE 2016FYE 2017FYE

Net debt/equity (%) -12.7 96.9 80.5 61.9

Net Debt to EBITDA (x) -0.2 1.9 1.5 1.1

Interest coverage ratio (X) 176.9 5.1 6.6 8.4

Source: Company data, Credit Suisse Estimates

IDEAS ENGINE 10

South African Apparel Retail

Figure 7: Global apparel retail valuation comparison

Source: Company data, Credit Suisse estimates, IBES estimates for Not Covered stocks, Priced as at 21 July 2014

Rating Ticker CCYShare price

Target

price

Upside /

(Downside) CY2015E CY2016E CY2015E CY2016E CY2015E CY2016E CY2015E CY2016E CY2015E CY2016E

South Africa

Mr Price Group Limited OUTPERFORM MPCJ.J ZAR 260.7 283.0 9% 26.8x 22.9x 24.8x 20.73x 16.7x 14.0x 2.9% 4.3% 2.5% 2.9%

The Foschini Group NEUTRAL TFGJ.J ZAR 156.2 150.0 -4% 15.7x 14.0x 16.9x 14.71x 10.3x 8.8x 4.2% 6.1% 4.2% 4.7%

Truworths International Limited UNDERPERFORM TRUJ.J ZAR 89.7 65.0 -28% 14.5x 13.5x 14.7x 13.57x 9.9x 9.0x 5.9% 6.7% 4.7% 5.0%

Woolworths Holdings Limited NEUTRAL WHLJ.J ZAR 99.3 94.0 -5% 23.0x 19.4x 23.1x 20.9x 12.9x 12.0x 3.0% 4.4% 3.1% 3.7%

Average 20.0x 17.4x 19.9x 17.5x 12.4x 11.0x 4.0% 5.4% 3.6% 4.1%

Latam

Marisa S.A. UNDERPERFORM AMAR3 BRL 9.1 17.0 88% 8.3x 5.6x 8.4x 6.00x 4.0x 3.5x 10.0% 9.0% 2.1% 3.0%

Arezzo Industria e Comercio SA NEUTRAL ARZZ3 BRL 22.2 33.0 49% 13.5x 11.1x 12.8x 10.9x 8.5x 7.2x -4.5% -5.6% 3.7% 4.3%

CIA Hering S.A. NEUTRAL HGTX3 BRL 11.9 25.0 110% 6.0x 5.2x 5.9x 5.0x 3.8x 3.2x 13.9% 13.3% 11.8% 13.4%

Restoque Comércio e Confecções de NEUTRAL LLIS3 BRL 5.6 7.0 25% 25.7x 19.1x 26.4x 24.6x 11.4x 9.9x 5.7% 6.2% 0.6% 1.0%

Lojas Renner S.A. OUTPERFORM LREN3 BRL 111.6 100.0 -10% 24.9x 20.6x 24.2x 20.2x 12.7x 10.7x 3.8% 6.3% 1.3% 2.0%

GRUPO SANBORNS, S.A.B. DE CV OUTPERFORM GSNBRB1.MX MXN 25.6 31.0 21% 18.7x 16.5x 15.5x 14.1x 9.6x 8.7x 4.0% 5.8% 4.1% 4.1%

El Puerto de Liverpool, S.A.B. de C.V. OUTPERFORM LIVEPOLC1.MX MXN 193.0 175.0 -9% 30.1x 25.5x 30.0x 25.9x 18.3x 15.9x 0.8% 0.7% 0.2% 0.5%

S.A.C.I. FALABELLA NEUTRAL FALAB CLP 4400.0 4500.0 2% 20.1x 18.1x 20.1x 18.1x 12.2x 10.9x 1.1% 1.8% 1.3% 1.5%

Average 18.4x 15.2x 17.9x 15.6x 10.1x 8.8x 4.4% 4.7% 3.1% 3.7%

Europe

Hennes & Mauritz NEUTRAL HMb.ST SEK 339.4 360.0 6% 26.0x 24.0x 22.4x 20.7x 14.1x 13.0x 3.4% 3.5% 3.1% 3.4%

Inditex UNDERPERFORM ITX.MC EUR 31.0 20.0 -35% 34.6x 31.4x 33.6x 30.2x 20.1x 18.1x 3.1% 3.4% 1.5% 1.6%

Marks & Spencer UNDERPERFORM MKS.L GBp 531.5 500.0 -6% 15.5x 15.2x 18.8x 18.3x 7.7x 7.6x 7.5% 7.7% 3.5% 3.5%

Next NEUTRAL NXT.L GBp 7665.0 7450.0 -3% 18.0x 17.3x 18.2x 17.5x 12.7x 12.2x 5.6% 5.9% 2.0% 2.1%

OVS Spa NEUTRAL OVS.MI EUR 6.0 5.0 -16% 22.1x 19.6x 18.2x 17.5x 10.3x 9.6x 2.4% 5.8% 0.9% 1.5%

XXL ASA NEUTRAL XXLA.OL NOK 89.8 81.0 -10% 26.2x 20.3x 18.2x 17.5x 17.9x 14.2x 2.1% 3.3% 2.5% 3.0%

Average 23.7x 21.3x 21.6x 20.3x 13.8x 12.5x 4.0% 5.0% 2.2% 2.5%

US

Francesca's Not Covered FRAN.OQ USD 12.4 14.8x 13.0x 1.4x 1.5x 6.6x 5.8x

Ralph Lauren OUTPERFORM RL.N USD 130.3 146.0 12% 18.1x 17.1x 16.1x 15.8x 8.4x 8.2x 4.6% 4.8% 1.5% 1.7%

The Gap, Inc. UNDERPERFORM GPS.N USD 36.9 35.0 -5% 13.3x 12.5x 13.7x 13.1x 6.5x 6.2x 12.5% 12.3% 2.5% 2.5%

Abercrombie & Fitch Co. UNDERPERFORM ANF.N USD 21.0 15.0 -28% 24.2x 25.0x 18.4x 18.5x 3.8x 3.9x 17.9% 7.1% 4.7% 5.2%

Amer Eagle Out Not Covered AEO.N USD 18.0 19.2x 17.1x 1.3x 1.4x 7.0x 6.5x

Phillips-Van Heusen OUTPERFORM PVH.N USD 114.3 131.0 15% 16.4x 15.4x 18.6x 17.3x 11.4x 10.7x 5.9% 6.2% 0.2% 0.3%

Average 17.6x 16.7x 11.6x 11.3x 7.3x 6.9x 10.2% 7.6% 2.2% 2.4%

Asia

Fast Retailing NEUTRAL 9983.T JPY 58790.0 45000.0 -23% 43.3x 42.2x 40.9x 37.2x 23.3x 22.1x 2.0% 1.8% 0.8% 0.8%

PE EV/EBITDA FCF YieldEV/NOPAT Dividend Yield

IDEAS ENGINE 11

South African Apparel Retail

Figure 8: Global apparel growth and margin comparison

Source: Company data, Credit Suisse estimates, IBES estimates for Not Covered stocks indicated with *

FY1e FY2e FY3e 3yr CAGR FY1e FY2e FY3e 3yr CAGR FY1e FY2e FY3e 3yr CAGR FY1e FY2e FY3e 3yr CAGRLast

ActualFY1e FY2e FY3e

South Africa

Mr Price Group Limited 14.7% 15.1% 15.0% 14.9% 20.5% 18.3% 19.2% 19.4% 20.5% 18.6% 19.0% 19.4% 16.7% 17.2% 18.4% 17.4% 17.8% 18.7% 19.3% 20.0%

The Foschini Group 28.2% 10.8% 10.9% 16.4% 37.1% 11.4% 11.3% 19.3% 20.0% 11.3% 11.1% 14.1% 14.7% 11.8% 12.3% 12.9% 17.3% 16.2% 16.3% 16.3%

Truworths International Limited 8.2% 10.7% 8.9% 9.3% 4.1% 8.5% 6.1% 6.2% 3.2% 8.0% 5.5% 5.5% 3.8% 8.8% 6.5% 6.3% 31.0% 29.6% 28.8% 27.9%

Woolworths Holdings Limited 54.9% 8.5% 9.6% 22.6% 51.3% 15.3% 14.9% 26.1% 45.6% 15.7% 15.8% 24.9% 5.1% 17.6% 19.9% 14.0% 10.7% 10.0% 10.7% 11.3%

Latam

Marisa S.A. 9.1% 8.4% 8.4% 8.7% 31.7% 16.1% 11.1% 19.3% 42.7% 22.0% 35.7% 33.2% 61.3% 47.6% 48.6% 52.4% 6.7% 8.7% 9.8% 12.3%

Arezzo Industria e Comercio SA 11.3% 9.6% 9.8% 10.2% 15.7% 14.7% 16.1% 15.5% 17.7% 14.0% 15.6% 15.7% 15.0% 15.0% 21.5% 17.1% 15.4% 16.2% 16.9% 17.8%

Restoque Comércio e Confecções de

Roupas S.A. 12.1% 8.1% 8.1% 9.4% 12.2% 10.8% 12.0% 11.7% 17.8% 14.3% 16.5% 16.2% 317.6% 59.7% 29.6% 105.2% 10.8% 11.3% 12.0% 12.9%

Lojas Renner S.A. 13.5% 13.5% 10.8% 12.6% 14.6% 19.0% 18.2% 17.3% 12.7% 18.6% 24.0% 18.3% 21.1% 20.7% 30.2% 23.9% 15.4% 15.3% 16.0% 17.9%

GRUPO SANBORNS, S.A.B. DE CV 7.9% 9.0% 9.1% 8.7% 11.2% 12.7% 12.7% 12.2% 8.7% 13.0% 13.0% 11.6% 9.6% 12.9% 13.7% 12.0% 10.7% 10.8% 11.2% 11.6%

El Puerto de Liverpool, S.A.B. de C.V. 10.9% 12.5% 12.5% 12.0% 10.6% 16.7% 14.4% 13.9% 10.8% 17.7% 15.0% 14.4% 11.0% 17.8% 15.6% 14.8% 13.7% 13.7% 14.3% 14.6%

S.A.C.I. FALABELLA 9.3% 9.4% 9.3% 9.3% 9.0% 11.4% 11.0% 10.5% 9.9% 11.6% 11.3% 11.0% 14.7% 11.0% 11.7% 12.4% 10.7% 10.8% 11.0% 11.2%

Europe

Hennes & Mauritz 20.5% 11.3% 9.7% 13.7% 9.8% 7.9% 15.1% 10.9% 7.4% 7.7% 16.0% 10.3% 7.5% 7.7% 16.0% 10.3% 16.9% 15.1% 14.6% 15.4%

Inditex 12.7% 8.7% 8.2% 9.9% 13.5% 9.5% 8.8% 10.6% 14.2% 10.0% 9.5% 11.2% 13.3% 10.0% 9.5% 10.9% 17.7% 17.9% 18.1% 18.3%

Marks & Spencer 2.9% 3.0% 1.7% 2.5% 5.5% 0.6% 1.9% 2.6% 5.5% 1.1% 3.2% 3.3% 5.9% 0.2% 5.0% 3.7% 7.4% 7.6% 7.4% 7.6%

Next 6.2% 4.1% 3.7% 4.7% 4.5% 3.7% 3.0% 3.7% 4.8% 3.9% 3.1% 3.9% 2.1% 4.1% 3.3% 3.2% 20.3% 20.0% 20.0% 19.9%

OVS Spa 6.3% 7.2% 7.1% 6.9% 6.4% 3.5% 19.8% 9.7% 8.6% 3.7% 29.2% 13.3% 220.3% 6.4% 29.5% 64.0% 7.7% 7.8% 7.6% 9.2%

XXL ASA 25.9% 18.6% 18.0% 20.8% 17.0% 26.9% 22.2% 22.0% 17.0% 27.8% 22.8% 22.4% 52.3% 28.9% 22.9% 34.1% 10.7% 9.9% 10.7% 11.1%

US

Francesca's * 10.9% 11.4% 11.7% 11.3% -18.1% 4.6% 10.2% -1.9% -24.5% 1.7% 13.1% -4.6% -21.0% 1.6% 14.9% -2.6% 22.4% 15.2% 13.9% 14.1%

Ralph Lauren 0.4% 4.5% 5.8% 3.6% -9.3% 7.3% 9.2% 2.0% -14.3% 8.0% 10.7% 0.8% -11.1% 11.4% 13.6% 4.0% 13.6% 11.6% 12.0% 12.5%

The Gap, Inc. -0.4% 3.9% 5.6% 3.0% -3.4% 5.6% 5.6% 2.5% -6.0% 6.1% 5.7% 1.8% 1.1% 6.8% 6.4% 4.7% 12.4% 11.7% 12.0% 12.0%

Abercrombie & Fitch Co. -0.5% -0.5% -0.5% -0.5% -2.6% -2.7% -2.7% -2.6% -4.7% -5.0% -5.0% -4.9% -5.2% -5.5% -5.6% -5.5% 4.2% 4.0% 3.8% 3.6%

Amer Eagle Out * -0.7% 5.4% 1.9% 2.2% -1.6% 30.1% 8.3% 11.5% -11.4% 47.7% 12.0% 13.6% -14.9% 53.7% 9.5% 12.7% 7.1% 6.3% 8.8% 9.7%

Phillips-Van Heusen -3.5% 3.4% 4.4% 1.3% -5.2% 4.1% 6.8% 1.8% -6.7% 4.9% 8.3% 2.0% -4.9% 7.7% 12.2% 4.7% 11.2% 10.8% 11.0% 11.4%

Asia

Fast Retailing 19.7% 15.0% 9.9% 14.8% 51.3% 3.6% 4.4% 17.9% 60.3% 3.3% 4.2% 19.9% 85.5% 0.1% 7.9% 26.1% 9.4% 12.6% 11.3% 10.8%

EBIT marginSales growth EBITDA growth EBIT growth EPS growth

IDEAS ENGINE 12

South African Apparel Retail

Companies Mentioned (Price as of 20-Jul-2015)

Abercrombie & Fitch Co. (ANF.N, $21.54) Amer Eagle Out (AEO.N, $18.01) American Apparel (APP.A, $0.3) Arezzo Industria e Comercio SA (ARZZ3.SA, R$22.55) Associated British Foods (ABF.L, 3202.0p) CIA Hering S.A. (HGTX3.SA, R$12.2) El Puerto de Liverpool, S.A.B. de C.V. (LIVEPOLC1.MX, MXN193.02) Etam Develop (TAM.PA, €53.0) Fast Retailing (9983.T, ¥57,220) Francesca's (FRAN.OQ, $12.52) GRUPO SANBORNS, S.A.B. DE CV (GSNBRB1.MX, MXN25.03) Hennes & Mauritz (HMb.ST, Skr341.8) Inditex (ITX.MC, €31.14) Lojas Renner S.A. (LREN3.SA, R$112.4) Marisa S.A. (AMAR3.SA, R$9.02) Marks & Spencer (MKS.L, 534.0p) Mr Price Group Limited (MPCJ.J, R257.33, OUTPERFORM, TP R283.0) Next (NXT.L, 7640.0p) OVS Spa (OVS.MI, €5.91) Phillips-Van Heusen (PVH.N, $114.43) Ralph Lauren (RL.N, $130.51) Restoque Comércio e Confecções de Roupas S.A. (LLIS3.SA, R$5.75) S.A.C.I. FALABELLA (FAL.SN, CLP$4400.0) The Foschini Group (TFGJ.J, R155.0, NEUTRAL, TP R150.0) The Gap, Inc. (GPS.N, $37.61) Tom Tailor Hldg (TTIGn.DE, €9.679) Truworths International Limited (TRUJ.J, R88.2, UNDERPERFORM, TP R65.0) Woolworths Holdings Limited (WHLJ.J, R98.6, NEUTRAL, TP R94.0) XXL ASA (XXLA.OL, Nkr90.25)

Disclosure Appendix

Important Global Disclosures

The analysts identified in this report each certify, with respect to the companies or securities that the individual analyzes, that (1) the views expressed in this report accurately reflect his or her personal views about all of the subject companies and securities and (2) no part of his or her compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this report.

3-Year Price and Rating History for Mr Price Group Limited (MPCJ.J)

MPCJ.J Closing Price Target Price

Date (R) (R) Rating

13-Aug-12 129.29 116.00 N

04-Dec-12 132.80 136.00

20-Feb-13 121.00 NR

28-Aug-13 119.98 129.00 N *

29-Nov-13 155.00 147.50

02-Jun-14 169.20 165.00

19-Nov-14 238.84 235.00

23-Feb-15 265.00 259.00

11-Jun-15 244.50 272.00 O

* Asterisk signifies initiation or assumption of coverage.

N EU T RA L

N O T RA T ED

O U T PERFO RM

IDEAS ENGINE 13

South African Apparel Retail

3-Year Price and Rating History for The Foschini Group (TFGJ.J)

TFGJ.J Closing Price Target Price

Date (R) (R) Rating

13-Aug-12 139.90 154.00 O

04-Dec-12 132.60 158.00

20-Feb-13 114.60 NR

28-Aug-13 95.31 88.50 U *

29-Nov-13 101.50 90.50

03-Jun-14 108.10 105.00 N

12-Nov-14 132.00 145.00 O

23-Feb-15 171.00 162.00 N

01-Jun-15 157.00 165.00

* Asterisk signifies initiation or assumption of coverage.

O U T PERFO RM

N O T RA T ED

U N D ERPERFO RM

N EU T RA L

3-Year Price and Rating History for Truworths International Limited (TRUJ.J)

TRUJ.J Closing Price Target Price

Date (R) (R) Rating

13-Aug-12 104.00 102.00 N

04-Dec-12 97.99 109.00

20-Feb-13 99.80 NR

28-Aug-13 80.00 96.50 O *

29-Nov-13 81.01 92.50

25-Feb-14 69.95 84.00

12-Nov-14 68.86 73.00 N

23-Feb-15 94.35 78.00

* Asterisk signifies initiation or assumption of coverage. N EU T RA L

N O T RA T ED

O U T PERFO RM

IDEAS ENGINE 14

South African Apparel Retail

3-Year Price and Rating History for Woolworths Holdings Limited (WHLJ.J)

WHLJ.J Closing Price Target Price

Date (R) (R) Rating

01-Aug-12 50.94 57.13 O

03-Sep-12 57.79 63.79

04-Dec-12 67.60 69.03 N

20-Feb-13 63.02 NR

28-Aug-13 56.98 72.36 O *

28-Nov-13 70.42 NR

02-Dec-13 70.16 83.31 O *

20-Feb-14 59.03 76.17

18-Jul-14 78.08 80.00 N

03-Sep-14 76.58 81.00

16-Feb-15 92.25 85.00

23-Feb-15 94.00 86.00

* Asterisk signifies initiation or assumption of coverage.

O U T PERFO RM

N EU T RA L

N O T RA T ED

The analyst(s) responsible for preparing this research report received Compensation that is based upon various factors including Credit Suisse's total revenues, a portion of which are generated by Credit Suisse's investment banking activities

As of December 10, 2012 Analysts’ stock rating are defined as follows:

Outperform (O) : The stock’s total return is expected to outperform the relevant benchmark*over the next 12 months.

Neutral (N) : The stock’s total return is expected to be in line with the relevant benchmark* over the next 12 months.

Underperform (U) : The stock’s total return is expected to underperform the relevant benchmark* over the next 12 months.

*Relevant benchmark by region: As of 10th December 2012, Japanese ratings are based on a stock’s total return relative to the analyst's coverage universe which consists of all companies covered by the analyst within the relevant sector, with Outperforms representing the most attractive, Neutrals the less attractive, and Underperforms the least attractive investment opportunities. As of 2nd October 2012, U.S. and Canadian as well as European ratings are based on a stock’s total return relative to the analyst's coverage universe which consists of all companies covered by the analyst within the relevant sector , with Outperforms representing the most attractive, Neutrals the less attractive, and Underperforms the least attractive investment opportunities. For Latin American and non-Japan Asia stocks, ratings are based on a stock’s total return relative to the average total return of the relevant country o r regional benchmark; prior to 2nd October 2012 U.S. and Canadian ratings were based on (1) a stock’s absolute total return potential to its current share price and (2) the relative attractiveness of a stock’s total return potential within an analyst’s coverage universe. For Australian and New Zealand s tocks, the expected total return (ETR) calculation includes 12-month rolling dividend yield. An Outperform rating is assigned where an ETR is greater than or equal to 7.5%; Underperform wh ere an ETR less than or equal to 5%. A Neutral may be assigned where the ETR is between -5% and 15%. The overlapping rating range allows analysts to assign a rating that puts ETR in the context of associated risks. Prior to 18 May 2015, ETR ranges for Outperform and Underperform ratings did not overlap with Neutral thresholds between 15% and 7.5%, which was in operation from 7 July 2011.

Restricted (R) : In certain circumstances, Credit Suisse policy and/or applicable law and regulations preclude certain types of communications, including an investment recommendation, during the course of Credit Suisse's engagement in an investment banking transaction and in certain other circumstances.

Volatility Indicator [V] : A stock is defined as volatile if the stock price has moved up or down by 20% or more in a month in at least 8 of the past 24 months or the analyst expects significant volatility going forward.

Analysts’ sector weightings are distinct from analysts’ stock ratings and are based on the analyst’s expectations for the fundamentals and/or valuation of the sector* relative to the group’s historic fundamentals and/or valuation:

Overweight : The analyst’s expectation for the sector’s fundamentals and/or valuation is favorable over the next 12 months.

Market Weight : The analyst’s expectation for the sector’s fundamentals and/or valuation is neutral over the next 12 months.

Underweight : The analyst’s expectation for the sector’s fundamentals and/or valuation is cautious over the next 12 months.

*An analyst’s coverage sector consists of all companies covered by the analyst within the relevant sector. An analyst may cover multiple sectors.

IDEAS ENGINE 15

South African Apparel Retail

Credit Suisse's distribution of stock ratings (and banking clients) is:

Global Ratings Distribution

Rating Versus universe (%) Of which banking clients (%)

Outperform/Buy* 48% (25% banking clients)

Neutral/Hold* 36% (44% banking clients)

Underperform/Sell* 13% (38% banking clients)

Restricted 3%

*For purposes of the NYSE and NASD ratings distribution disclosure requirements, our stock ratings of Outperform, Neutral, an d Underperform most closely correspond to Buy, Hold, and Sell, respectively; however, the meanings are not the same, as our stock ratings are determined on a relative basis. (Please refer to definitions above.) An investor's decision to buy o r sell a security should be based on investment objectives, current holdings, and other individual factors.

Credit Suisse’s policy is to update research reports as it deems appropriate, based on developments with the subject company, the sector or the market that may have a material impact on the research views or opinions stated herein.

Credit Suisse's policy is only to publish investment research that is impartial, independent, clear, fair and not misleading. For more detail please refer to Credit Suisse's Policies for Managing Conflicts of Interest in connection with Investment Research: http://www.csfb.com/research-and-analytics/disclaimer/managing_conflicts_disclaimer.html

Credit Suisse does not provide any tax advice. Any statement herein regarding any US federal tax is not intended or written to be used, and cannot be used, by any taxpayer for the purposes of avoiding any penalties.

Price Target: (12 months) for Mr Price Group Limited (MPCJ.J)

Method: Owing to the stable cash flow growth of the retail industry, we believe it is appropriate to value it using the discounted cash flow (DCF) methodology. We forecast explicit cash flows for five years, after

which the growth rate free cash flow return in invested capital is faded to the final year growth rate and WACC respectively over the competitive advantage period (CAP). Our DCF fair value is adjusted by the WACC to determine our 12-month target price of R283. For Mr Price, we use a 12.02% WACC, 23-year CAP and a final year growth rate of 7.5%.

Risk: Risks to our target price include: (i) Cotton price volatility in (ii) Competition from foreign entrants with similar value proposition; (iii) Brand perception; (iv) Chinese supply chain pressures; and (v) Rand exchange

rate weakness / volatility.

Price Target: (12 months) for The Foschini Group (TFGJ.J)

Method: Owing to the stable cash flow growth of the retail industry, we believe it is appropriate to value it using the discounted cash flow (DCF) methodology. We forecast explicit cash flows for five years, after

which the growth rate free cash flow return in invested capital is faded to the final year growth rate and WACC respectively over the competitive advantage period (CAP). Our DCF fair value is adjusted by the WACC to determine our 12-month target price of R150. For TFG, we use a 12.1% WACC, 11-year CAP and a final year growth rate of 6%.

Risk: Risks to our target price include: (i) bad debts (ii) exposure to credit sales (iii) Competition from foreign entrants (iv) imported inflation on the back of currency fluctuations (v) fashion trends

Price Target: (12 months) for Truworths International Limited (TRUJ.J)

Method: Owing to the stable cash flow growth of the retail industry, we believe it is appropriate to value it using the discounted cash flow (DCF) methodology. We forecast explicit cash flows for five years, after

which the growth rate free cash flow return in invested capital is faded to the final year growth rate and WACC respectively over the competitive advantage period (CAP). Our DCF fair value is adjusted by the WACC to determine our 12-month target price of R65. For Truworths, we use a 13.25% WACC, 10-year CAP and a final year growth rate of 6%.

Risk: Risks to our target price include: (i) bad debts (ii) high exposure to credit sales (iii) competition from foreign entrants (iv) imported inflation on the back of currency fluctuations (v) new management strategy (vi)

excess cash on balance sheet (vii) fashion trends

IDEAS ENGINE 16

South African Apparel Retail

Price Target: (12 months) for Woolworths Holdings Limited (WHLJ.J)

Method: Owing to the stable cash flow growth of the retail industry, we believe it is appropriate to value it using the discounted cash flow (DCF) methodology. We forecast explicit cash flows for five years, after

which the growth rate free cash flow return in invested capital is faded to the final year growth rate and WACC respectively over the competitive advantage period (CAP). Our DCF fair value is adjusted by the WACC to determine our 12-month target price of R94. For Woolworths, we use a 12.25% WACC, 15-year CAP and a final year growth rate of 5%.

Risk: Risks include (i) execution risk in Australia, (ii) significant currency movements, (iii) poor fashion calls, (iv) increased competition from foreign entrants, (v) weak macro economic environment.

Please refer to the firm's disclosure website at https://rave.credit-suisse.com/disclosures for the definitions of abbreviations typically used in the target price method and risk sections.

See the Companies Mentioned section for full company names

The subject company (ABF.L, GSNBRB1.MX, LIVEPOLC1.MX) currently is, or was during the 12-month period preceding the date of distribution of this report, a client of Credit Suisse.

Credit Suisse provided investment banking services to the subject company (ABF.L) within the past 12 months.

Credit Suisse has received investment banking related compensation from the subject company (ABF.L) within the past 12 months

Credit Suisse expects to receive or intends to seek investment banking related compensation from the subject company (ABF.L, 9983.T, ANF.N, GPS.N, GSNBRB1.MX, MKS.L, FAL.SN) within the next 3 months.

As of the date of this report, Credit Suisse makes a market in the following subject companies (ANF.N, GPS.N, PVH.N, RL.N).

As of the end of the preceding month, Credit Suisse beneficially own 1% or more of a class of common equity securities of (OVS.MI).

For other important disclosures concerning companies featured in this report, including price charts, please visit the website at https://rave.credit-suisse.com/disclosures or call +1 (877) 291-2683.

Important Regional Disclosures

Singapore recipients should contact Credit Suisse AG, Singapore Branch for any matters arising from this research report.

The analyst(s) involved in the preparation of this report have not visited the material operations of the subject company (MPCJ.J, TFGJ.J, TRUJ.J, WHLJ.J, HMb.ST, ITX.MC, ABF.L, 9983.T, AMAR3.SA, ANF.N, ARZZ3.SA, GPS.N, GSNBRB1.MX, HGTX3.SA, LIVEPOLC1.MX, LLIS3.SA, LREN3.SA, MKS.L, NXT.L, OVS.MI, PVH.N, RL.N, FAL.SN) within the past 12 months

Restrictions on certain Canadian securities are indicated by the following abbreviations: NVS--Non-Voting shares; RVS--Restricted Voting Shares; SVS--Subordinate Voting Shares.

Individuals receiving this report from a Canadian investment dealer that is not affiliated with Credit Suisse should be advised that this report may not contain regulatory disclosures the non-affiliated Canadian investment dealer would be required to make if this were its own report.

For Credit Suisse Securities (Canada), Inc.'s policies and procedures regarding the dissemination of equity research, please visit https://www.credit-suisse.com/sites/disclaimers-ib/en/canada-research-policy.html.

Credit Suisse Securities (Europe) Limited (Credit Suisse) acts as broker to (ABF.L).

The following disclosed European company/ies have estimates that comply with IFRS: (HMb.ST, ITX.MC, ABF.L, MKS.L, NXT.L).

Credit Suisse has acted as lead manager or syndicate member in a public offering of securities for the subject company (GSNBRB1.MX, PVH.N) within the past 3 years.

As of the date of this report, Credit Suisse acts as a market maker or liquidity provider in the equities securities that are the subject of this report.

Principal is not guaranteed in the case of equities because equity prices are variable.

Commission is the commission rate or the amount agreed with a customer when setting up an account or at any time after that.

To the extent this is a report authored in whole or in part by a non-U.S. analyst and is made available in the U.S., the following are important disclosures regarding any non-U.S. analyst contributors: The non-U.S. research analysts listed below (if any) are not registered/qualified as research analysts with FINRA. The non-U.S. research analysts listed below may not be associated persons of CSSU and therefore may not be subject to the NASD Rule 2711 and NYSE Rule 472 restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account.

Credit Suisse Securities Johannesburg (PTY) Ltd ................................................................................................. Pieter Vorster ; Rishay Dhanraj

IDEAS ENGINE 17

South African Apparel Retail

Important Credit Suisse HOLT Disclosures

With respect to the analysis in this report based on the Credit Suisse HOLT methodology, Credit Suisse certifies that (1) the views expressed in this report accurately reflect the Credit Suisse HOLT methodology and (2) no part of the Firm’s compensation was, is, or will be directly related to the specific views disclosed in this report.

The Credit Suisse HOLT methodology does not assign ratings to a security. It is an analytical tool that involves use of a set of proprietary quantitative algorithms and warranted value calculations, collectively called the Credit Suisse HOLT valuation model, that are consistently applied to all the companies included in its database. Third-party data (including consensus earnings estimates) are systematically translated into a number of default algorithms available in the Credit Suisse HOLT valuation model. The source financial statement, pricing, and earnings data provided by outside data vendors are subject to quality control and may also be adjusted to more closely measure the underlying economics of firm performance. The adjustments provide consistency when analyzing a single company across time, or analyzing multiple companies across industries or national borders. The default scenario that is produced by the Credit Suisse HOLT valuation model establishes the baseline valuation for a security, and a user then may adjust the default variables to produce alternative scenarios, any of which could occur.

Additional information about the Credit Suisse HOLT methodology is available on request.

The Credit Suisse HOLT methodology does not assign a price target to a security. The default scenario that is produced by the Credit Suisse HOLT valuation model establishes a warranted price for a security, and as the third-party data are updated, the warranted price may also change. The default variable may also be adjusted to produce alternative warranted prices, any of which could occur.

CFROI®, HOLT, HOLTfolio, ValueSearch, AggreGator, Signal Flag and “Powered by HOLT” are trademarks or service marks or registered trademarks or registered service marks of Credit Suisse or its affiliates in the United States and other countries. HOLT is a corporate performance and valuation advisory service of Credit Suisse.

For Credit Suisse disclosure information on other companies mentioned in this report, please visit the website at https://rave.credit-suisse.com/disclosures or call +1 (877) 291-2683.

IDEAS ENGINE 21

South African Apparel Retail