the changing landscape of regional trade agreements: 2006

TRANSCRIPT

DISCUSSION PAPER NO 12

The Changing Landscape of Regional Trade Agreements: 2006 Update

by

Roberto V. Fiorentino, Luis Verdeja and Christelle Toqueboeuf1

Regional Trade Agreements SectionTrade Policies Review Division

World Trade OrganizationGeneva, Switzerland

Disclaimer and citation guideline

Discussion Papers are presented by the authors in their personal capacity and opinions expressed in these papers should be attributed to the authors. They are not meant to represent the positions or opinions of the WTO Secretariat or of its Members and are without prejudice to Members’ rights and obligations under the WTO. Any errors or omissions are the responsibility of the authors.

Any citation of this paper should ascribe authorship to staff of the WTO Secretariat and not to the WTO.

1 Roberto Fiorentino, Luis Verdeja and Christelle Toqueboeuf are respectively Economic Affairs Officer, Junior Economic Affairs Officer and Administrative Assistant with the Regional Trade Agreements Section of the Trade Policies Review Division of the WTO Secretariat. The views presented in this paper and expressed during this lecture are personal to the authors. They are not meant to represent the positions or opinions of the WTO Secretariat or of its Members and are without prejudice to Members' rights and obligations under the WTO.

This paper is only available in English – Price CHF 20.-

To order, please contact:

WTO PublicationsCentre William Rappard154 rue de LausanneCH-1211 GenevaSwitzerlandTel: (41 22) 739 52 08Fax: (41 22) 739 57 92Website: www.wto.orgE-mail: [email protected]

ISSN 1726-9466ISBN: 978-92-870-3417-5Printed by the WTO SecretariatIII-2007

Keywords: custom union (CU), economic integration agreement (EIA), free trade agreement (FTA), regional trade agreements (RTAs).

© World Trade Organization, 2007. Reproduction of material contained in this document may be made only with written permission of the WTO Publications Manager.

With written permission of the WTO Publications Manager, reproduction and use of the material contained in this document for non-commercial educational and training purposes is encouraged.

ACKNOWLEDGEMENTS

The authors are indebted to Clemens Boonekamp, María del Carmen Pont-Vieira, Jo-Ann Crawford and colleagues in the Regional Trade Agreements Section of the Trade Policies Review Division, for their helpful comments and suggestions on a previous draft.

ABSTRACT

Regional Trade Agreements (RTAs) are a prominent feature of the multilateral trading system (MTS) and have become an important trade policy tool for virtually all WTO Members. The number of RTAs as well as the world share of trade covered under them has been steadily increasing over the last ten years and this trend will be further strengthened by the many RTAs being proposed and those currently under negotiation; the impasse in the Doha Round exacerbates the gap between the preferential and the MFN paths to trade liberalization. The proliferation of RTAs presents WTO Members with challenges and opportunities; the promotion of free trade through preferential agreements can foster trade liberalization and benefit economic development by integrating developing countries into the world economy; yet the development of complex networks of non-MFN trade relations will increase discrimination and may well undermine transparency and predictability in international trade relations; it is therefore of systemic importance for the MTS that the WTO addresses this dichotomy and ensures that RTAs are designed and implemented so to complement and not undermine the multilateral process. This paper sets out the scene for such discussion by providing an update of recent developments, trends and future directions of the so called "Changing Landscape of RTAs". Two broad themes are explored: "RTAs' kaleidoscope" maps the global landscape of RTAs and looks at main trends and characteristics of "RTA proliferation" through quantitative and qualitative categorizations of RTAs. The second section of this paper focuses on the WTO-RTA relationship and its systemic implications for the MTS; it identifies some of the current and potential tensions arising from the coexistence of the two systems and it provides an insight into multilateral efforts being pursued to address the existing unbalances.

TABLE OF CONTENTS

I. INTRODUCTORY REMARKS ............................................................................................................................................................................................1

II. RTAS' KALEIDOSCOPE ............................................................................................................................................................................................................2

(i) Reassessing RTAs' main trends and characteristics ...........................................................................................................................2

(ii) Quantifying and qualifying the proliferation of RTAs ....................................................................................................................2

(iii) The Global Landscape of RTAs: state of play and future developments ................................................................ 13

III. RTAS AND THE WTO: A TROUBLESOME RELATIONSHIP ........................................................................................ 26

IV. LIST OF ACRONYMS OF NOTIFIED RTAS .............................................................................................................................................. 36

LIST OF BOXES, TABLES AND CHARTS

CHART 1 ALL RTAS NOTIFIED TO THE GATT/WTO (1948-2006), BY YEAR OF ENTRY INTO FORCE ........................................................................................................................................................................ 3

CHART 2 RTAS NOTIFIED TO THE GATT/WTO (1948-2006), CURRENTLY IN FORCE, BY YEAR OF ENTRY INTO FORCE .......................................................................................................... 4

CHART 3 RTAS NOTIFIED TO THE GATT (PRE 1995) AND WTO (POST 1995) ......................................... 5

CHART 4 NOTIFIED RTAS IN FORCE, AS OF DECEMBER 2006, BY TYPE OF AGREEMENT ............................................................................................................................................................................................ 6

CHART 5 RTAS SIGNED, UNDER NEGOTIATION AND PROPOSED, AS OF DECEMBER 2006, BY TYPE OF AGREEMENT.................................................................................................... 6

CHART 6 RTAS' CONFIGURATION, AS OF DECEMBER 2006 ....................................................................................... 8

CHART 7 CROSS-REGIONAL RTAS, AS PERCENTAGE OF TOTAL RTAS AS OF DECEMBER 2006 .................................................................................................................................................................................. 9

CHART 8 NOTIFIED RTAS IN GOODS BY TYPE OF PARTNER, AS OF DECEMBER 2006 ............................................................................................................................................................................... 11

CHART 9 NOTIFIED RTAS IN SERVICES BY TYPE OF PARTNER, AS OF DECEMBER 2006 ............................................................................................................................................................................... 11

CHART 10 NOTIFIED NORTH-SOUTH RTAS IN GOODS BY DEVELOPED COUNTRY PARTNER,AS OF DECEMBER 2006 .............................................................................................................................. 12

CHART 11 NOTIFIED NORTH-SOUTH RTAS IN GOODS BY DEVELOPING COUNTRY PARTNER,AS OF DECEMBER 2006 .............................................................................................................................. 12

MAP 1 EUROPEAN INTRA AND CROSS-REGIONAL RTA NETWORK ..................................................... 16

MAP 2 WESTERN HEMISPHERE INTRA-REGIONAL RTA NETWORK .................................................... 17

MAP 3 WESTERN HEMISPHERE CROSS-REGIONAL RTA NETWORK ................................................... 18

MAP 4 ASIA-PACIFIC INTRA-REGIONAL RTA NETWORK .................................................................................. 21

MAP 5 ASIA-PACIFIC CROSS-REGIONAL RTA NETWORK ................................................................................. 22

MAP 6 AFRICAN INTRA-REGIONAL RTA NETWORK ............................................................................................... 24

MAP 7 AFRICAN CROSS-REGIONAL RTA NETWORK .............................................................................................. 25

MAP A PARTICIPATION IN RTAS AS OF DECEMBER 2006 (GOODS) ........................................................ 30

MAP B PROJECTED PARTICIPATION IN RTAS (GOODS) ......................................................................................... 31

MAP C PARTICIPATION IN RTAS AS OF DECEMBER 2006 (SERVICES) ................................................. 32

MAP D PROJECTED PARTICIPATION IN RTAS (SERVICES) ................................................................................. 33

MAP E CROSS REGIONAL RTAS AS OF DECEMBER 2006 .................................................................................... 34

MAP F ESTABLISHMENT OF REGIONAL TRADING BLOCKS ......................................................................... 35

TABLE 1 NOTIFIED RTAS IN GOODS AND SERVICES BY DATE OF ENTRY INTO FORCE AND TYPE OF PARTNER AS OF DECEMBER 2006 ......................... 10

1

I. INTRODUCTORY REMARKS2

Regional Trade Agreements (RTAs) have become in recent years a very prominent feature of the Multilateral Trading System (MTS). Between January 2005 and December 2006 a further 55 RTAs have been notified to the WTO raising the total number of RTAs notified nd in force to 214.3 In addition to these, many more agreements are currently being negotiated and being considered. The impasse in the Doha Development Agenda (DDA) negotiations is further strengthening Members' resolve to conclude such agreements and indeed a flurry of new RTA initiatives has emerged in recent months whose effects will be felt in the years to come.

The significance of the phenomenon should not be overlooked since it will ultimately influence the nature of international trade relations and the policy choices and behaviour of the operating actors. Developments in recent years suggest that RTAs have become an important trade policy instrument for WTO Members. RTAs' scope and configuration is respectively far reaching and innovative in terms of design and choice of RTA partners. Besides their own dynamics, the appeal for RTAs carries systemic implications for the MTS, noticeably by increasing discrimination and complexity in trade relations and by undermining the transparency and predictability of the System and by extension the standing of the WTO with regards to these principles. The challenge for the latter will be to ensure the effectiveness of its RTA surveillance mechanism as an interface between preferential and MFN trade relations.

The objective of this paper is not to assess the pros and cons of RTAs; our intent is rather to raise awareness of the magnitude of the RTA phenomenon with a view to further existing and future research on those questions. Besides

2 This document has been prepared under the authors' own responsibility and without prejudice to the positions of WTO Members and to their rights and obligations under the WTO Agreement. Colours and boundaries of maps included in this document do not imply any judgement on the part of the WTO as to the legal status or frontier of any territory.

3 This number totals notifications made under GATT Article XXIV, GATS Article V, and the Enabling Clause as well as accessions to existing RTAs; for a complete list of RTAs notified to the GATT/WTO see http://www.wto.org/english/tratop_e/region_e/region_e.htm

mapping the global landscape of RTAs, we attempt to draw the main trends and characteristics of this proliferation and to include quantitative and qualitative indicators. In this respect, the paper builds upon a previous survey and aims at updating the numbers and verifying the trends observed at that time.4 The final section of this paper looks at the state of play of the DDA negotiations on WTO rules applying to RTAs.

Unless otherwise stated, the statistics presented in this paper take account of all bilateral, regional, and plurilateral trade agreements of a preferential reciprocal nature that have been notified to the GATT/WTO.5 The primary focus is on free-trade areas (FTAs) and CUss (CUs) in the area of trade in goods and economic integration agreements (EIAs) in the area of trade in services; details on partial scope arrangements have been included, where possible.6

4 Crawford J. and Fiorentino R. (2005), 'The Changing Landscape of Regional Trade Agreements', WTO Discussion Paper No. 8.

5 Some of the maps included in this paper also account for RTAs in force but which have not yet been notified.

6 The information gathered in this study is based on notifications to the WTO, RTA documentation submitted to the Committee on Regional Trade Agreements (CRTA), WTO accession documents, Trade Policy Reports, and other public sources. In this sense the information may not be exhaustive since while it is possible to account accurately for all notified RTAs, for the non-notified RTAs, agreements under negotiation and those being proposed, information is often scarce or inconclusive.

2

II. RTAS' KALEIDOSCOPE

“Proliferation” of RTAs has become a common term, in the press and relevant literature, to account for the increasing number of RTAs being recorded in recent years. While this term draws attention to an important development in the global trading system, its quantitative connotation presents limitations as to its capacity to accurately portray the scale and significance of the phenomenon and single out the differences between “this” proliferation and former waves of so-called “regionalism”. In other words, while the increasing number of RTAs is a significant variable, especially when looked at over time, it does not in itself tell us much about the dynamics characterizing this phenomenon, its significance in global trade and its systemic implications vis-à-vis the MTS. In this paper, while we often refer to “RTA proliferation”, we have sought to qualify the term by complementing the focus on numbers with some qualitative categorizations of RTAs.

(i) RTAs' main trends and characteristics

Mapping RTA proliferation and discerning its trends and characteristics in the global trading system presents several difficulties due to the fast pace and random nature of this proliferation. In the previous study four main trends had been identified. First, for most countries RTAs have become the centrepiece of their commercial policy implying in many cases a shift of resources from multilateral trade objectives to the pursuance of preferential agreements. Second, RTAs show an increasing level of sophistication; many of the new ones include liberalization of trade in services; their regulatory regimes extend to trade policy areas not regulated multilaterally; and their outreach in terms of partners is becoming both innovative and not geographically bound. Third, the geopolitics of RTAs indicates an increase in North-South RTAs and their gradual replacement of long established non-reciprocal systems of preferences; while this shift is in some cases driven by compatibility requirements with WTO rules, in others, it is the developing countries themselves that are opting to forego unilateral preferences in favour of more secure reciprocal arrangements. Also significant is the increasing number of South-South RTAs, a development that appears to be tied to the emergence of several major RTA hubs in the developing world. The fourth trend that has been identified points to

a process of expansion and consolidation of regional integration schemes characterised by the consolidation of an increasing number of intra-regional RTAs into continent-wide regional trading blocks.

RTA developments up to December 2006 appear to validate and further strengthen these trends, albeit only partially the last one. Indeed while the number of intra-regional RTAs has expanded in all regions, particularly in Latin America and Asia-Pacific, their consolidation into region-wide RTAs has made modest progress in the best of cases and stalled altogether in others. Paradoxically, besides political differences and technical difficulties, slow progress may be partly attributed to the proliferation of RTAs itself and in particular of extra and cross-regional RTAs. The latter represent the most distinctive feature of the current “proliferation”; indeed these RTAs connote a shift from the traditional concept of “regional integration” among neighbouring countries, a core element of previous RTAs waves, to preferential partnerships driven by strategic political and economic considerations that are unrelated to regional dynamics. As we argue below, these RTAs may be actually weakening regional integration processes themselves.

(ii) Quantifying and qualifying the proliferation of RTAs Reassessing

Quantifying RTAs accurately is a methodological challenge. WTO statistics tend to exaggerate the total number of RTAs since they are based on notification requirements that do not reflect the physical number of RTAs.7 On the other hand to focus on the “actual” number of agreements confronts us with non exhaustive and inaccurate figures since it is practically impossible to verify the data for the many RTAs that have either not yet been notified or are at different phases of implementation. Yet, irrespective of the methodology we choose to employ, a time-based consideration of RTAs leaves us with no doubt as to the unprecedented pace of RTA proliferation

7 RTA notif ications to the WTO include those made under GATT Article XXIV, GATS Article V, the Enabling Clause, as well as accessions to existing RTAs; it should be noted that the notif ication requirements contained in WTO provisions require that RTAs covering trade in goods and services be notified separately.

3

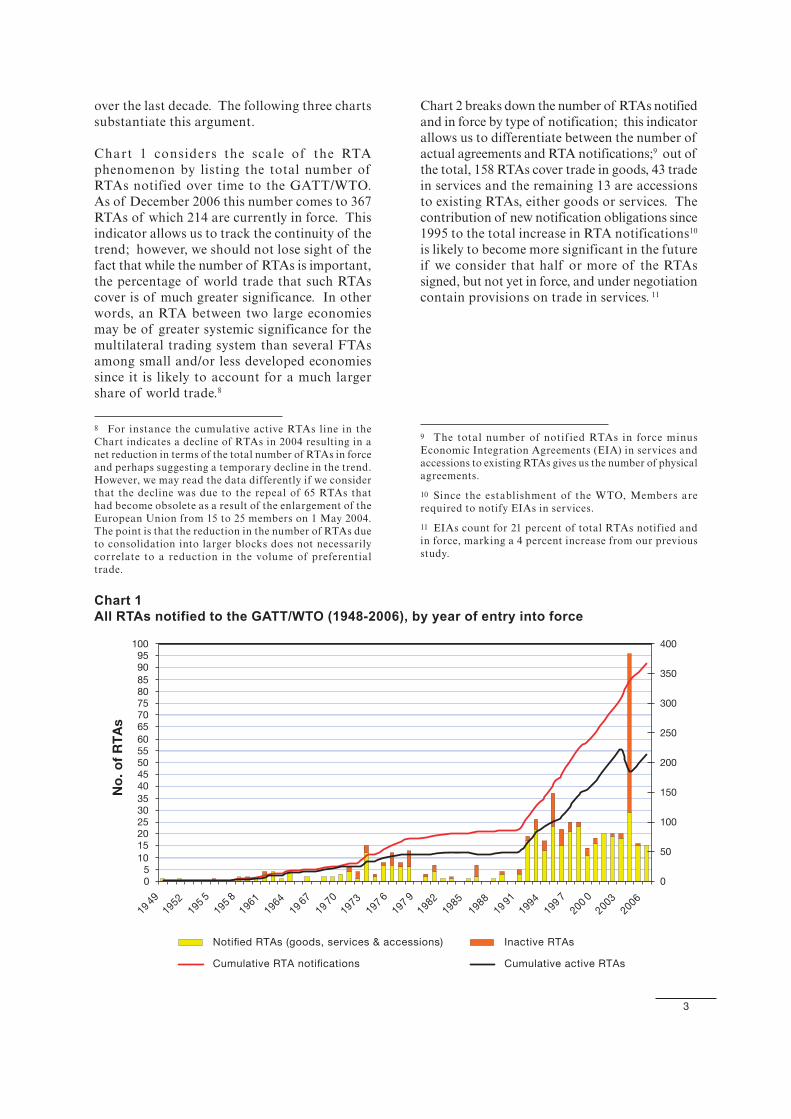

over the last decade. The following three charts substantiate this argument.

Chart 1 considers the scale of the RTA phenomenon by listing the total number of RTAs notified over time to the GATT/WTO. As of December 2006 this number comes to 367 RTAs of which 214 are currently in force. This indicator allows us to track the continuity of the trend; however, we should not lose sight of the fact that while the number of RTAs is important, the percentage of world trade that such RTAs cover is of much greater significance. In other words, an RTA between two large economies may be of greater systemic significance for the multilateral trading system than several FTAs among small and/or less developed economies since it is likely to account for a much larger share of world trade.8

8 For instance the cumulative active RTAs line in the Chart indicates a decline of RTAs in 2004 resulting in a net reduction in terms of the total number of RTAs in force and perhaps suggesting a temporary decline in the trend. However, we may read the data differently if we consider that the decline was due to the repeal of 65 RTAs that had become obsolete as a result of the enlargement of the European Union from 15 to 25 members on 1 May 2004. The point is that the reduction in the number of RTAs due to consolidation into larger blocks does not necessarily correlate to a reduction in the volume of preferential trade.

Chart 2 breaks down the number of RTAs notified and in force by type of notification; this indicator allows us to differentiate between the number of actual agreements and RTA notifications;9 out of the total, 158 RTAs cover trade in goods, 43 trade in services and the remaining 13 are accessions to existing RTAs, either goods or services. The contribution of new notification obligations since 1995 to the total increase in RTA notifications10 is likely to become more significant in the future if we consider that half or more of the RTAs signed, but not yet in force, and under negotiation contain provisions on trade in services. 11

9 The total number of notif ied RTAs in force minus Economic Integration Agreements (EIA) in services and accessions to existing RTAs gives us the number of physical agreements.

10 Since the establishment of the WTO, Members are required to notify EIAs in services.

11 EIAs count for 21 percent of total RTAs notified and in force, marking a 4 percent increase from our previous study.

Chart 1All RTAs notified to the GATT/WTO (1948-2006), by year of entry into force

05

101520253035404550556065707580859095

100

1949

1952195

5

1958

1961

196419

67

1970

1973197

6

1979

1982

19851988

1991

1994199

7

2000

2003

2006

No

. of

RT

As

0

50

100

150

200

250

300

350

400

Notified RTAs (goods, services & accessions) Inactive RTAs

Cumulative RTA notifications Cumulative active RTAs

4

Chart 2RTAs notified to the GATT/WTO (1948-2006), currently in force, by year of entry into force

0

2

4

6

8

10

12

14

16

18

20

22

24

26

28

30

32

1959

1961

1963

1965

1967

196919

71

197319

7519

77

1979

1981

198319

85

198719

89

199119

93

1995

1997

1999

200120

03

2005

No

. of

RT

As

0

50

100

150

200

250

Goods Services Accessions Cumulative

Chart 3 considers RTA proliferation on a chronological basis by differentiating between two time periods, the GATT and the WTO years; the latter is the period we tend to associate with the current wave of RTAs. Notably the chart shows that of the total number of RTAs notified to the GATT/WTO up to December 2006, 124 were notified during the GATT years and 243 during the WTO years; this amounts to an annual average RTA notification of 20 for the WTO years

compared to less than three during the four and half decades of the GATT. Also significant, is the fact that of the GATT notified RTAs only 36 remain in force today, reflecting in most cases the evolution over time of the agreements themselves, as they were superseded by new ones between the same signatories (most often going deeper in integration), or by their consolidation into wider groupings.

5

Chart 3RTAs notified to the GATT (pre 1995) and WTO (post 1995)

0

20

40

60

80

100

120

140

160

180

200

No

. of

no

tifi

ed R

TA

s

In force Inactive

Enabling Clause

Article V

Article XXIV

1947-1995 1995-2006

WTO

In force Inactive

The Charts above indicate a large increase in RTA activity over the last 10 years. In part, the increase in notifications is a reflection of increased WTO membership and new notification obligations. But, this apart, it is obvious that the rate of growth of RTAs is continuing unabated. The magnitude of the phenomenon is even more significant if we consider the number of RTAs in force but not notified (approximately 70), those ones signed but not yet in force (approximately 30), the RTAs currently being negotiated (approximately 65), and those at a proposal stage (approximately 30).12 If all of these agreements are implemented by 2010 we will be looking at a global landscape of RTAs of close to 400 agreements.13 (See Maps I to IV

12 By “proposed” it is meant an interest or commitment to enter negotiations on a given RTA which is supported by an official declaration, feasibility studies, or exploratory talks by the parties' official authorities.

13 Not every RTA under negotiation will automatically increase the number of RTAs in force, given the fact that some will supersede or expand existing RTAs. It should be noted that the conclusion of these agreements may actually result in a net reduction in terms of the total number of RTAs in force due to the consolidation effect that some of these agreements may have. Besides the case of the EC enlargement mentioned earlier, the same pattern may also be observed in Latin America where FTAs currently under negotiation should replace and consolidate a myriad of bilateral partial scope agreements.

in the Annex for actual and projected countries participation in RTAs).

Typology of RTAs

The typology of RTAs reveals other interesting aspects of this proliferation. Chart 4 categorizes RTAs notified and in force according to whether they intend to be FTAs, CUs or partial scope agreements; Chart 5 exhibits the same categorization for RTAs signed, under negotiation and proposed. The data shows that FTAs account for 84 per cent of all RTAs notified and in force; partial scope agreements and CUs agreements each account for 8 per cent. Of the projected RTAs, 92 per cent are intended to be FTAs, 7 per cent partial scope agreements and only 1 per cent CUs. These figures suggest that among the options available to countries today, the FTA is the one that best reflects their trade policy needs and objectives; CUs on the other hand appear to have become less popular and perhaps out of tune with today's trading climate; as for partial scope agreements, figures reveal a slight increase in the number of such agreements compared to our previous study, however, several of these aim to become FTAs over time.

6

Chart 4Notified RTAs in force, as of December 2006, by type of agreement

84%

8%8%

FTA

Customs Union

Partial Scope

Chart 5RTAs signed, under negotiation and proposed, as of December 2006, by type of agreement

92%

1%7%

FTA

Customs Union

Partial Scope

The preference for FTAs is a reflection of the defining characteristics of the current RTA race; the key attributes of this race appear to be speed, flexibility and selectivity and the FTA is, in most cases, the configuration that best meets these needs. Although negotiation of an FTA may take years to conclude,14 evidence suggests that the timing from the launching of the negotiations to their conclusion has been shrinking in recent years, especially for agreements among like-minded countries.15 FTAs afford their parties ample flexibility in terms of the desired trade policy scope and choice of partners; the latter

14 An example of protracted negotiations is the FTA between the EU and Mercosur which after 10 years has not yet been concluded. It should also be noted that these are complex negotiations involving two CUs.

15 A case in point is the FTA between the EFTA States and the Republic of Korea which took one year to negotiate after only four rounds of negotiations.

consideration appears to be particularly relevant to the current wave of cross-regional FTAs where the focus is often on strategic market access or strategic political alliances, unbound by geographical considerations. Most significantly, FTAs allow for ambitious preferential regimes while safeguarding a country's sovereignty over its commercial policy since each FTA party maintains its own trade policy vis-à-vis third parties.

CUs share the FTAs objective of comprehensive trade liberalization among the parties; however, their formation is driven by policy objectives that together with their configuration requirements severely limit their flexibility as a trade policy instrument compared to FTAs. A CUs reflects the traditional objective of regional integration among geographically contiguous countries.16

16 All notified CUs and, to the knowledge of the authors, those ones in the making are among geographically contiguous countries.

7

Besides this, CUs are often flanked, and in most cases driven, by considerations that reach beyond the realm of trade (i.e. political integration, economic and monetary unions, supranational institutions etc.) On the technical side, a CUs requires the establishment of a common external tariff and harmonization of external trade policies; this implies a much higher degree of policy coordination among the parties compared to FTAs and, unquestionably, loss of autonomy over the parties' national commercial policies. As a result CUs entail longer and more complex negotiations and implementation periods.17 Furthermore, while the parties to an FTA have, in principle, full flexibility with regards to their individual choice of future FTA partners,18 participation in CUs, if played by the rules, limits the individual parties' choice for future RTA memberships since a proper functioning of the union requires that any agreement with

17 The predominance of FTAs over CUs is in fact an historical paradox worth mentioning. A perusal of the drafting history of Article XXIV of the GATT (which contains the legal provisions for the conclusion of FTAs, CUs and interim agreements leading to the formation of FTAs or CUs) reveals that it was not until the Havana Charter that provisions for the formation of FTAs were included in what became GATT Article XXIV. The previous charters only spoke of CUs and interim agreements leading to the formation of CUs. This suggests that the perception of regional economic integration and the means to achieve it that the drafting fathers of Article XXIV had in mind were not likely to be along the lines of the proliferation of cross-regional FTAs that we are witnessing today. It is also interesting to speculate how different the current landscape of RTAs would be if the provisions of GATT Article XXIV only applied to CUs with no related provision for the formation of FTAs.

18 Some limitations may apply in the form of an MFN clause whereby parties to the agreement commit to extend to each other any more favourable treatment that they may grant to a third party in a future agreement. Some geographically bound FTAs also show a propensity to negotiate agreements with common parties. Examples would include the EFTA states, Australia and New Zealand and ASEAN members among others. However, we should be careful in making any generalizations since other cases, such as NAFTA, disprove any such rule.

a third party includes the CUs as a whole.19 In the current trading climate of flexible and speedy RTAs, the preference of FTAs over CUs seems obvious.

As for membership in partial scope agreements, their limited trade coverage, poor implementation record, scarce visibility, and limitations with respect to the choice of partners due to WTO rules,20 makes them less attractive to those countries, including developing ones, that are committed to comprehensive trade liberalization. Nevertheless, the projection in Chart 5 shows a 3 per cent increase in this category of RTAs compared to our previous study. While this development is generally due to a more active participation of developing countries in RTAs, it appears to be specifically tied to a novel approach by several of the large developing countries to South-South agreements. Several of these agreements are based on a staged approach to trade liberalization whereby a framework agreement is signed that includes as a first step the conclusion of a partial scope agreement, often accompanied by an “early harvest programme”, and as a second step a commitment to future FTA negotiations.21

19 The requirement in a CU of a common external tariff and harmonization of the parties' commercial policies does not allow in principle a “go alone” policy whereby one party alone negotiates a preferential agreement with a third party. Such a situation would disrupt the functioning of the CU since products from the third party could enter the union at a preferential rate through the bilateral RTA, implying a loss of tariff revenues for the other members to the union. Examples of such a situation include SACU (FTA between the EU and South Africa) and the GCC (FTA between the United States and Bahrain).

20 Under the WTO, the only legal provision applicable to a North-South RTA covering trade in goods is Article XXIV of the GATT 1994. This provision provides among other requirements a comprehensive trade liberalization schedule based on tariff elimination. Partial scope agreements providing for reduction and/or elimination of duties on a limited number of products are unlikely to be found compatible with such provision. Partial scope agreements are allowed under paragraph 2(c) of the Enabling Clause; however, the recourse to such a provision is only available to developing country Members.

21 Example of such agreements include the recently notified China-ASEAN and many of the RTAs being negotiated by India.

8

Confi guration of RTAs

A significant aspect of this proliferation is the evolving configuration of RTAs. Charts 6 and 7 indicate a decreasing propensity for plurilateral RTAs and a net increase in the number of bilateral and cross-regional RTAs. With a few exceptions, the bulk of RTAs in the making are based on bilateral RTA configurations rather than the more burdensome plurilateral RTAs. Bilateral agreements account for 80 per cent of all RTAs notified and in force; 94 per cent of those signed and under negotiation; and 100 per cent of those at a proposal stage.22

The disproportionate number of bilateral configurations is due to several reasons. From a geopolitical perspective, the opportunities for region-wide plurilateral RTAs are fewer since many of these agreements have already been established during past waves of regionalism. New initiatives are either a revamping of existing regional schemes (i.e. SAPTA to SAFTA) or consolidation of such schemes into broader and in some cases continent-wide integration arrangements (See Map V in the Annex). The political dimension of these initiatives combined with the technical complexity of negotiations involving several countries, many of which are already bound in existing RTAs, clearly limits the number of such RTAs.

22 Bilateral agreements may include more than two countries when one of them is an RTA itself (e.g. EC (25) – Turkey (1) is a two party RTA comprising 26 countries). A plurilateral agreement refers to an RTA in which the constituent parties exceed two countries (e.g., EFTA, MERCOSUR, AFTA, SADC, etc.).

Other reasons include the apparent paradigm shift from using RTAs as instruments for regional integration to vehicles for strategic market access; this further strengthens the drive for bilateral RTAs, especially in the case of cross-regional RTAs.23

Another significant aspect of this proliferation is the emergence of atypical RTAs configurations. The simple bilateral (i.e. two countries) and plurilateral configurations are being supplemented by agreements in which one of the parties is itself an RTA; such agreements have been in the making for some time and their number is increasing. An emerging configuration is bilateral RTAs where each party is a distinct RTA. The advent of such agreements points to a consolidation of established trading relationships but also supports the argument raised earlier with regards to the policy choices of plurilateral RTAs and in particular CUs. The fact that several such agreements have been under negotiation for numerous years and that none, thus far, has entered into force underscores the complexity of such negotiations.24

23 The bulk of cross-regional RTAs are bilateral agreements, i.e. two parties (see footnote 20). One exception is the Trans-Pacific Strategic Economic Partnership (SEP-4) between Brunei, Chile, New Zealand and Singapore.

24 Examples include EC-MERCOSUR, EC-GCC, among others. Prospective ones may include EU-ASEAN and EU-CAN. One such agreement between EFTA and SACU has actually been signed between late June and early July 2006 but according to the information available is not yet in force. Another such agreement is the one between SACU and MERCOSUR that was signed in December 2004, however, the limited scope of the agreement prompted a reopening of the negotiations which are currently underway.

Chart 6RTAs' configuration, as of December 2006

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

In Force

Signed/Neg

Proposed Bilateral

Plurilateral

9

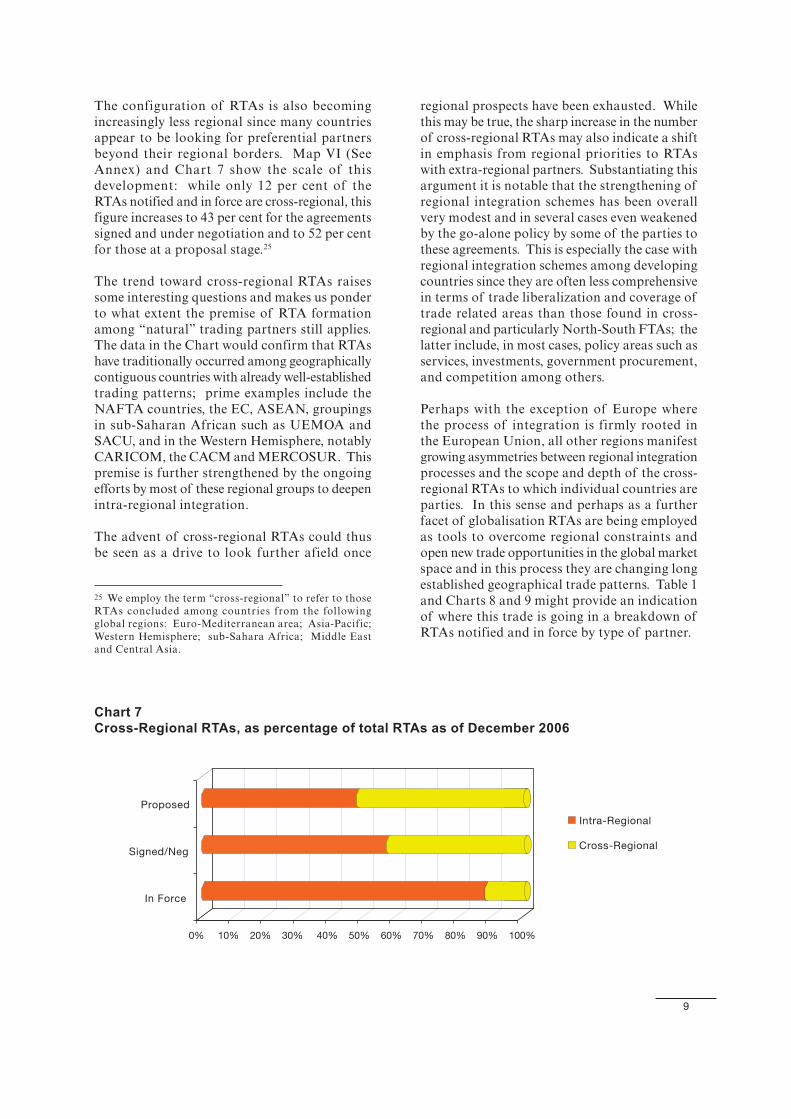

The configuration of RTAs is also becoming increasingly less regional since many countries appear to be looking for preferential partners beyond their regional borders. Map VI (See Annex) and Chart 7 show the scale of this development: while only 12 per cent of the RTAs notified and in force are cross-regional, this figure increases to 43 per cent for the agreements signed and under negotiation and to 52 per cent for those at a proposal stage.25

The trend toward cross-regional RTAs raises some interesting questions and makes us ponder to what extent the premise of RTA formation among “natural” trading partners still applies. The data in the Chart would confirm that RTAs have traditionally occurred among geographically contiguous countries with already well-established trading patterns; prime examples include the NAFTA countries, the EC, ASEAN, groupings in sub-Saharan African such as UEMOA and SACU, and in the Western Hemisphere, notably CARICOM, the CACM and MERCOSUR. This premise is further strengthened by the ongoing efforts by most of these regional groups to deepen intra-regional integration.

The advent of cross-regional RTAs could thus be seen as a drive to look further afield once

25 We employ the term “cross-regional” to refer to those RTAs concluded among countries from the following global regions: Euro-Mediterranean area; Asia-Pacific; Western Hemisphere; sub-Sahara Africa; Middle East and Central Asia.

regional prospects have been exhausted. While this may be true, the sharp increase in the number of cross-regional RTAs may also indicate a shift in emphasis from regional priorities to RTAs with extra-regional partners. Substantiating this argument it is notable that the strengthening of regional integration schemes has been overall very modest and in several cases even weakened by the go-alone policy by some of the parties to these agreements. This is especially the case with regional integration schemes among developing countries since they are often less comprehensive in terms of trade liberalization and coverage of trade related areas than those found in cross-regional and particularly North-South FTAs; the latter include, in most cases, policy areas such as services, investments, government procurement, and competition among others.

Perhaps with the exception of Europe where the process of integration is firmly rooted in the European Union, all other regions manifest growing asymmetries between regional integration processes and the scope and depth of the cross-regional RTAs to which individual countries are parties. In this sense and perhaps as a further facet of globalisation RTAs are being employed as tools to overcome regional constraints and open new trade opportunities in the global market space and in this process they are changing long established geographical trade patterns. Table 1 and Charts 8 and 9 might provide an indication of where this trade is going in a breakdown of RTAs notified and in force by type of partner.

Chart 7Cross-Regional RTAs, as percentage of total RTAs as of December 2006

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

In Force

Signed/Neg

Proposed

Intra-Regional

Cross-Regional

10

Table 1Notified RTAs in goods and services by date of entry into force and type of partner as of December 2006

Developed

only

Developed

Developing

Developed

Transition

Developing

only

Developing

Transition

Transition

onlyTotal

G S G S G S G S G S G S G S

1958-1964 2 1 1 3 1

1965-1969 1 1

1970-1974 5 1 2 8

1975-1979 3 1 4

1980-1984 2 1 1 4

1985-1989 1 1 1 2 4 1

1990-1994 3 2 3 4 6 1 4 21 2

1995-1999 3 1 7 1 2 6 4 2 17 35 8

2000-2002 1 11 5 4 11 5 3 6 35 11

2003-2006 3 1 18 14 1 12 6 2 19 54 22

19 7 45 20 8 3 43 15 8 0 46 0 169 45

Further empirical research is needed to substantiate the claim of changing patterns of trade, however, Table 1 does reveal significant trends. Besides RTAs among transition economies,26 the major clusters of RTAs are North-South followed by South-South RTAs

26 The large number of RTAs among transition economies is due to geopolitical changes following the collapse of the former Soviet Union. Many of these agreements are likely to be repealed due to accession to existing RTAs and consolidation of bilateral RTAs into larger agreements (see Section III – Europe).

accounting for 27 and 25 percent, respectively, of the total number of notified RTAs in goods (see Chart 8) and 44 and 33 percent respectively for EIAs (see Chart 9). Both of these clusters will be considerably expanded given that almost all of the RTAs in the making fall under these two categories.27

27 Out of the 45 North-South RTAs, 36 entered into force during the WTO years (i.e. since 1995); of the latter, 18 date since 2003.

11

Chart 9Notified RTAs in services by type of partner, as of December 2006

16%

44%7%

33%

0%

Developed only

Developed-Developing

Developed-Transition

Developing only

Developing-Transition

Transition only

Chart 8Notified RTAs in goods by type of partner, as of December 2006

5%

25% 5%

27%

11%27%

Developed only

Developed-Developing

Developed-Transition

Developing only

Developing-Transition

Transition only

What is notable in the North-South cluster is that the criteria of reciprocity and comprehensive trade liberalization28 do not appear to be deterring developing countries from forging such agreements and foregoing non-reciprocal systems of preferences under schemes like the Generalized System of Preferences (GSP) and other unilateral initiatives covered by WTO waivers. While for those developing countries benefiting from WTO waivers such as Cotonou this transition is in part driven by compatibility requirements with WTO rules, for others the choice is based on a conscious trade policy strategy underpinned by domestic reforms and trade liberalization at the

28 Given that the legal cover of the Enabling Clause only applies to preferential agreements concluded among developing countries, RTAs involving developed and developing WTO Members may only fall under GATT Article XXIV and therefore are subject to the requirements contained therein.

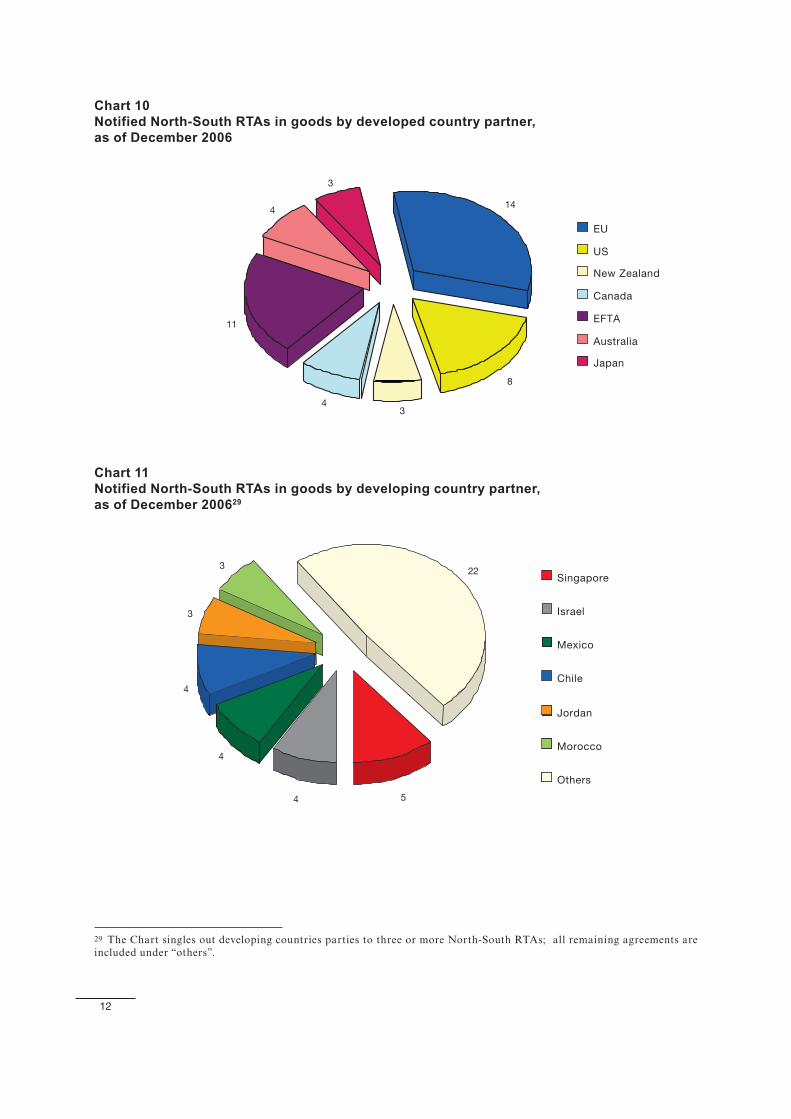

bilateral and multilateral level. Chart 10 shows the breakdown of notified North-South RTAs in goods by developed country partner and Chart 11 does the equivalent for developing countries partners to North-South RTAs.

12

Chart 10Notified North-South RTAs in goods by developed country partner,as of December 2006

8

14

3

4

11

43

EU

US

New Zealand

Canada

EFTA

Australia

Japan

Chart 11Notified North-South RTAs in goods by developing country partner,as of December 200629

54

4

4

3

3 22Singapore

Israel

Mexico

Chile

Jordan

Morocco

Others

29 The Chart singles out developing countries parties to three or more North-South RTAs; all remaining agreements are included under “others”.

13

Regardless of the motivations, the point is that through RTAs, the nature of North-South trade relations appears to be evolving to a framework of reciprocity and ambitious trade policy scope. In this respect it is interesting to note that approximately half of the notified North-South RTAs provide for liberalization of trade in services and most of the others foresee the negotiations of a services chapter in the future. In terms of the so-called WTO plus issues, almost all of these RTAs include references to competition, government procurement, intellectual property and investment provisions among others; however, the treatment of these trade policy issues varies from detailed provisions and commitments to frameworks providing for future negotiations.

(iii) The Global Landscape of RTAs: state of play and future developments

In the previous study, the proliferation of RTAs was associated with a combination of geopolitical developments dating back to the late 1980s and early 1990s; the most important included multilateral and regional dynamics as well as individual countries' policy choices. At the multilateral level, the protracted Uruguay Round (1986-1994) had prompted several countries to pursue preferential deals as an insurance against an eventual failure of the multilateral trade negotiations; at the regional level the fragmentation of the former Soviet Union and the disbandment of the Council for Mutual Economic Assistance (COMECON) had generated a new cluster of RTAs between transition economies and the European Union and the EFTA States as well as among transition economies themselves (See table 1); at the country level, the predominance of Europe in RTAs began to be challenged by the RTA policy of countries that had traditionally been agnostic to such preferential agreements. In the 90s we saw the establishment of NAFTA, MERCOSUR and AFTA which had a domino effect on other countries' decisions to pursue RTAs; we also saw the emergence of a policy of “additive regionalism” whereby countries such as Chile, Mexico and Singapore engaged in forging preferential relations with their major trading partners. Albeit sporadic in their manifestation, these combined developments have laid the seeds for the surge in RTAs that we are witnessing today.

More significantly this process of action-reaction whereby the creation of discriminatory arrangements by one country is matched by an equal reaction (often defensive) by other countries seems to have become irreversible almost as if RTA proliferation has reached a critical mass from which there is no turning back. Paradoxically these layers of discriminatory treatment have flourished under a multilateral framework of laws and regulations (GATT and now WTO) that is underpinned by the fundamental principle of non-discrimination in trade relations (MFN). Clearly the MTS is not functioning properly and as the Uruguay Round experience first revealed, the propensity for RTAs is likely to increase at times when the WTO is perceived as failing to deliver to its Members. It is thus not surprising that sluggish progress in the Doha Round is being rivalled by an ever increasing number of notified RTAs with many more in the making. Mapping these developments is the objective of the sections that follow.

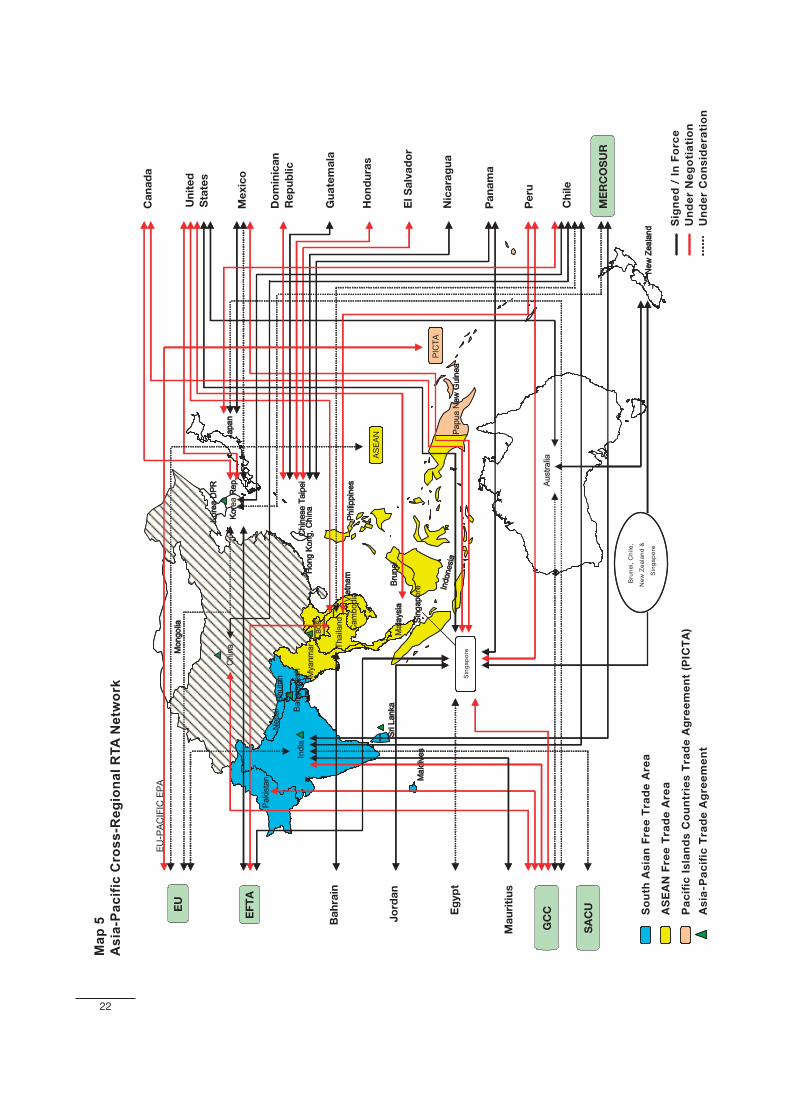

Europe

Europe is the region with the largest number of RTAs, accounting for almost half of the agreements notified to the WTO and in force. The main regional groupings are the European Union (EU) and the EFTA.30 South-Eastern Europe is consolidating into a third trading group under the auspices of the Stability Pact;31 this sub-region achieved in 2005 a matrix of bilateral FTAs and negotiations to replace these agreements with a plurilateral agreement were launched in 2006.32 Existing ties between this sub-region and the EU are being further institutionalized: EU accession negotiations with Croatia were officially

30 Given that the paper contains information up to December 2006, the reference is to EU (25) and it does not account for the accession of Bulgaria and Romania that occurred on 1 January 2007.

31 Albania, Bosnia-Herzegovina, Bulgaria, Croatia, Macedonia, Moldova, Romania, Serbia & Montenegro and UNMIK/Kosovo.

32 The so called CEFTA plus agreement was signed on 19th December 2006. However, it has not been included in this paper due to time constraints. The implications of this agreement will be the repeal of all the bilateral RTAs concluded among the Stability Pact's countries.

14

launched in October 2005 (along with Turkey),33 and a Stability and Association Agreement (SAA) between the EU and Serbia and Montenegro is underway.34 In the Mediterranean basin, the establishment of a Euro-Mediterranean FTA between the EU and its Mediterranean partners made further progress in 2005/06;35 at the 5th Euromed Trade Ministerial Conference in March 2006, Euromed Trade Ministers took stock of progress and officially launched negotiations for the liberalisation of trade in services to boost the existing Association Agreements; they also agreed to deepen agricultural liberalisation and to reinforce the institutional and legal framework. Other developments include the endorsement of the Pan-Euro-Mediterranean Protocol of origin by Morocco, Israel and Egypt.

Beyond its immediate neighbourhood, the EU has focused on furthering already commenced RTA negotiations; these include FTAs with MERCOSUR, the GCC and the six Economic Partnership Agreements (EPAs) with sub-groupings of the African Caribbean and Pacific (ACP) countries.36 In a change of policy stance, the EU has also signalled an interest to launch new FTA negotiations; prospective candidates include Korea, India and the countries parties to the ASEAN, the CACM and the CAN. As for the EFTA States, their FTAs with Tunisia and Korea entered into force in June 2005 and September 2006 respectively while the FTA with Lebanon was notified in December 2006; an FTA with the SACU countries was signed in June 2006. EFTA States have opened FTA negotiations with Thailand in 2005 and with the countries

33 The Former Yugoslav Republic of Macedonia (FYROM) is also a candidate country; however, accession negotiations have not started yet.

34 In the sub-region, the EU has SAAs with Croatia and FYROM, it has signed an SAA with Albania, and it is negociating one with Bosnia-Herzegovina.

35 The Mediterranean partners are Algeria, Egypt, Israel, Jordan, Lebanon, Morocco, Palestinian Authority, Syria, Tunisia and Turkey. A grid of bilateral RTAs in trade in goods is already in place and parallel ones are being established by the EFTA States and Turkey. The EU-Algeria FTA was notified in July 2006.

36 The EC is negotiating with six different groups of countries: ECOWAS plus Mauritania; CEMAC plus DRC and Sao Tomé and Principe; East and Southern Africa (ESA), the CARIFORUM (CARICOM plus Dominican Republic) and the Pacific Islands.

of the GCC in 2006 and they are considering one with India.

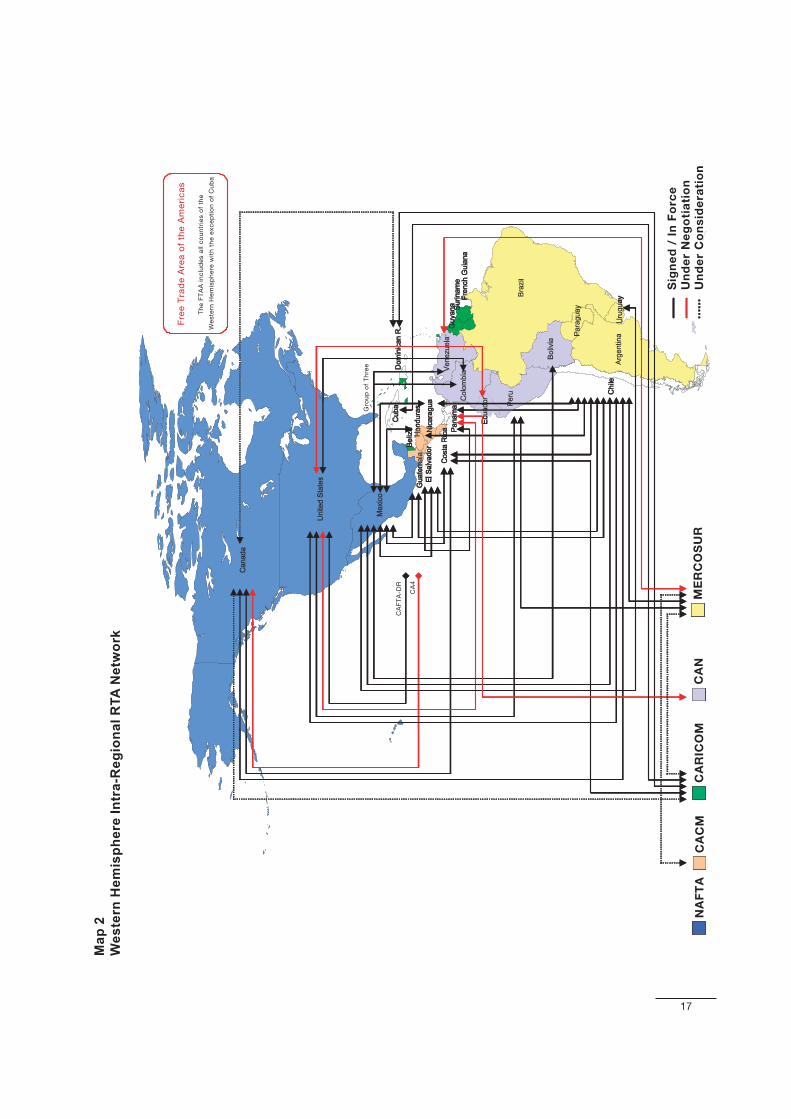

The Americas

The United States has been an active RTA player throughout 2005 and 2006. It has signed FTAs with Colombia, Peru and with five Central American countries and the Dominican Republic (DR-CAFTA)37 and it has further pursued negotiations with Ecuador and Panama. Further afield, it has secured deals with some Northern African and Middle Eastern countries, as part of its Middle East Free Trade Initiative: the FTA with Oman has been signed while the FTAs with Morocco and Bahrain have both entered into force; negotiations have been launched with the United Arab Emirates (other prospective FTAs could include Egypt, Kuwait, Qatar and Tunisia). In Asia-Pacific, the United States has opened FTA negotiations with Korea and Malaysia in an effort to strengthen ties with ASEAN countries.38 The other two NAFTA members have also been active; Canada has opened FTA negotiations with Korea and is considering possible FTAs with CARICOM, MERCOSUR and the Dominican Republic. Mexico is also intent on expanding its RTA network and is considering FTAs with Ecuador, Korea and MERCOSUR;39 its FTA with Japan has entered into force and negotiations are ongoing with Singapore.

Further South in the Americas, Panama has concluded an FTA with Singapore and CARICOM has ratified agreements with Cuba and Costa Rica. The Andean Community members, while working as a group towards an FTA with MERCOSUR, are pursuing several other FTAs on an individual basis: in addition to its FTA with the United States, Peru is engaged in negotiations with Singapore and has concluded

37 The CAFTA-DR was signed on August 5, 2004. The agreement entered into force for El Salvador and the United States on March 1, 2006, for Honduras and Nicaragua on April 1, 2006, and for Guatemala on July 1, 2006. Entry into force for Costa Rica and the Dominican Republic is pending.

38 The United States has an FTA with Singapore and ongoing negotiations with Thailand.

39 Mexico and MERCOSUR signed in 2002 a framework agreement for the creation of an FTA.

15

an early harvest agreement with Thailand in view of a fully-fledged FTA; as for Colombia and Ecuador, they are both engaged in FTAs with the United States;40 Venezuela, for its part, is in the process of acceding to MERCOSUR. Turning to MERCOSUR, it has signed framework agreements aiming at the establishment of FTAs with the GCC, India, Israel, Egypt, Morocco and the SACU, and is undertaking a joint FTA feasibility study with Korea.

40 The Colombia-US FTA has been signed while the Ecuador-US FTA is under negotiation.

Chile too is expanding its FTA network; the Trans-Pacific Strategic Economic Partnership (SEP-4) with New Zealand, Brunei and Singapore, entered into force in November 2006, it has signed an FTA with China, and a framework agreement for a possible FTA with India; it has also opened negotiations with Japan, and has held preliminary FTA talks with Thailand.

16

Ma

p 1

Eu

rop

ea

n I

ntr

a a

nd

Cro

ss

-Re

gio

na

l R

TA

Ne

two

rk

EU

25

EF

TA

Eu

roM

ed

Pa

rtn

ers

Cu

rre

ntl

y u

nd

er

wa

ive

r

Oth

er

RT

A P

art

ne

rs

Ch

ile

Me

xic

o

Sin

ga

po

re

Re

p.

of

Ko

rea

Th

aila

nd

So

uth

A

fric

a

Ca

na

da

EU

EU

-- AC

PA

CP

EP

As

EP

As

Neg

otiatio

ns

Neg

otiatio

ns

ME

RC

OS

UR

GC

C

CE

MA

C +

DR

C +

S

ao

To

mé

&P

rincip

e

EC

OW

AS

+

Maurita

nia

East

and

So

uth

ern

Afr

ica

SA

DC

CA

RIF

OR

UM

PA

CIF

IC

Sig

ne

d /

In

Fo

rce

Un

de

r N

eg

oti

ati

on

Un

de

r C

on

sid

era

tio

n

OC

TA

SE

AN

Ind

ia

EU

EU

-- AC

PA

CP

EP

As

EP

As

Neg

otiatio

ns

Neg

otiatio

ns

ME

RC

OS

UR

SA

CU

EU

GC

C

CE

MA

C +

DR

C +

S

ao

To

mé

&P

rincip

e

EC

OW

AS

+

Maurita

nia

East

and

So

uth

ern

Afr

ica

SA

DC

CA

RIF

OR

UM

PA

CIF

IC

OC

TA

SE

AN

EF

TA

17

Ma

p 2

W

es

tern

He

mis

ph

ere

In

tra

-Re

gio

na

l R

TA

Ne

two

rk

Sig

ne

d /

In

Fo

rce

Un

de

r N

eg

oti

ati

on

Un

de

r C

on

sid

era

tio

n

CA

4

CA

FT

A-D

R

Gro

up

of

Th

ree

NA

FT

AC

AC

MC

AR

ICO

MC

AN

ME

RC

OS

UR

Fre

e T

rad

e A

rea

of

the

Am

eri

ca

s

Th

e F

TA

A i

nc

lud

es a

ll c

ou

ntr

ies o

f th

e

We

ste

rn H

em

isp

he

re w

ith

th

e e

xc

ep

tio

n o

f C

ub

a

18

Ma

p 3

We

ste

rn H

em

isp

he

re C

ros

s-R

eg

ion

al

RT

A N

etw

ork

Ind

ia

Tu

rke

y

Isra

el

Jo

rda

n

Mo

roc

co

Ba

hra

in

Eg

yp

t

Om

an

SA

CU

Sin

ga

po

re

Re

p.

of

Ko

rea

Th

aila

nd

Ja

pa

n

Ch

ina

Au

str

alia

Ch

ine

se

Ta

ipe

i

Ma

laysia

UA

E

Sig

ne

d/

InF

orc

e

Un

de

rN

eg

oti

ati

on

Un

de

rC

on

sid

era

tio

n

Sin

ga

po

re

Ne

wZ

ea

lan

d

Bru

ne

i

EU

-CA

RIC

OM

EP

A

GC

C

NA

FT

AC

AC

MC

AR

ICO

MC

AN

ME

RC

OS

UR

SA

CU

GC

C

EU

EF

TA

19

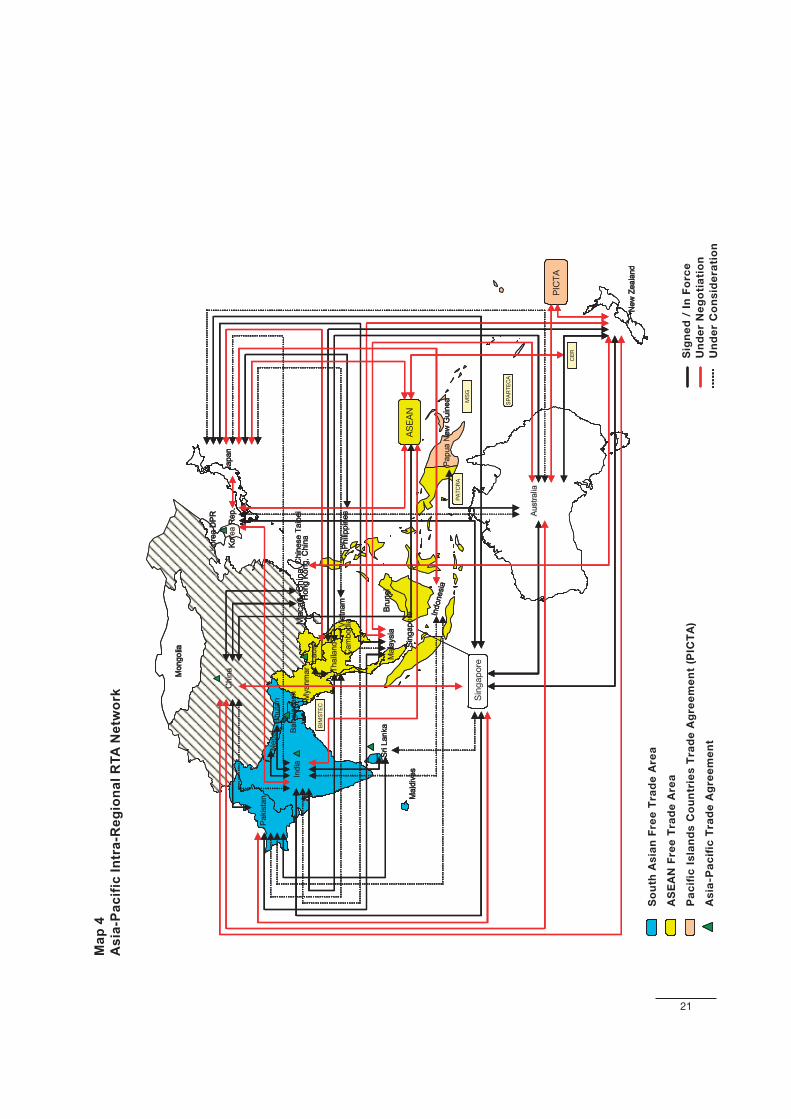

Asia-Pacifi c

Countries in Asia-Pacific are consolidating their drive towards regionalism at an accelerated pace. The apathy towards RTAs is long gone and a network of regional and cross-regional RTAs is clearly in the making. Notwithstanding the existence of sub-regional groupings41 most of the RTAs being created are on a bilateral basis with some instances of collective RTA negotiations (mainly involving the ASEAN group); as a result overlapping memberships are on the increase and so is the complexity in intra-regional trade relations.42 Rationalization of these bilateral relationships into region wide integration schemes is however on the agenda with several initiatives being either pursued (ASEAN + 3)43 or suggested.44

At the country level, Japan appears to have fully jumped on the RTA bandwagon; developments over the last two years suggest that its focus on partnerships with Asian countries has broadened to include cross-regional partners;45 following the entry into force of its FTA with Mexico, Japan has launched negotiations with Chile and the GCC countries, has agreed to open FTA negotiations with Vietnam in early 2007 and it has commenced feasibility studies for FTAs with Australia, India and Switzerland. As for Korea, in addition to

41 In Asia: ASEAN, the Asia-Pacific Trade Agreement (APTA) formerly named the Bangkok Agreement, and the South Asian Association for Regional Cooperation (SAARC). In the Pacific: the CER between Australia and New Zealand and the Pacific Islands Forum.

42 Examples include APTA (Bangladesh, China, India, Republic of Korea, Laos and Sri Lanka) and the BIMSTEC (Bangladesh, Bhutan, India, Myanmar, Nepal, Sri Lanka and Thailand) both of which include countries that are members of ASEAN and SAFTA.

43 The ASEAN + China, Korea and Japan process was institutionalized in 1999 at the ASEAN+3 Summit held in Manila. The Process aims at strengthening and deepening East Asia cooperation and foresees the establishment of a region wide FTA; in this regard ASEAN has concluded an FTA with China, is negotiating one with Japan and the one with Korea is under consideration.

44 Japan has proposed a Comprehensive Economic Partnership for East Asia (CEPEA) which adds India, Australia and New Zealand to ASEAN+3; a similar proposal has been made by India under the name of “Pan-Asia Free Trade Area”.

45 Japan has FTAs with Singapore and Malaysia; one signed with the Philippines; and it is negotiating with Indonesia, Korea, Thailand as well as ASEAN.

its FTAs with Chile and the EFTA States, it has signed an FTA with Singapore; it has launched negotiations with ASEAN, Canada, the United States, India and Japan, and it is considering FTAs with Australia, MERCOSUR, Mexico and the EU. The regional giant, China, is not lagging behind; it has signed an FTA with Chile and Pakistan, launched negotiations with the GCC, Singapore, Australia and New Zealand, and is considering an eventual agreement with India, in what would be the world's largest FTA in terms of population. Chinese Taipei is also seeking to conclude RTAs agreements; in addition to its FTA with Panama, it has signed FTAs with Guatemala and Nicaragua and is negotiating others with the Dominican Republic, El Salvador and Honduras.

The ASEAN group is negotiating with India, Japan, Australia and New Zealand, as well as considering an FTA with Korea and possibly the EU. At the same time, some ASEAN countries (Singapore, Thailand and Malaysia) are negotiating individual agreements. Singapore's FTAs with Jordan, India, Korea and Panama have entered into force and so has the SEP-4; it has ongoing FTA negotiations with Canada, China, Mexico, Pakistan, Peru and it is considering further FTAs with Egypt and Sri Lanka; as for its ongoing FTA negotiations with Bahrain, Kuwait, Qatar and the UAE, a decision was taken in November 2006 to include these under a Singapore-GCC FTA whose negotiations are scheduled to start in 2007. Thailand has also become an active RTA player in recent years: its FTAs with Australia and New Zealand have entered into force; it has concluded a framework agreement with India46 and signed FTAs with Bahrain; it has FTA negotiations with the EFTA States, Japan, Peru and the United States; and it is considering FTAs with Chile and Pakistan. Malaysia has signed an FTA with Japan and a partial scope agreement with Pakistan;47 it has launched negotiations with Australia New Zealand and the United States and it is considering an FTA with India.

46 The framework agreement provides for an “early harvest” and for FTA negotiations.

47 Malaysia and Pakistan are also negotiations an FTA to replace the partial scope agreement.

20

Turning to South Asia, SAARC members48 are busy implementing the South Asian Free Trade Area (SAFTA). Beside regional initiatives, India and Pakistan appear to be very keen not to be left behind in the RTA race and to conclude their own preferential deals. In addition to its FTA with Singapore, India has signed an FTA with Mauritius; partial scope agreements with Chile, MERCOSUR, SACU and Thailand; it has FTA negotiations with ASEAN, the GCC countries and Korea; and more RTAs are under consideration with China, Japan, Indonesia and Malaysia and the EU. As for Pakistan, it has concluded an FTA with Sri Lanka, a partial scope agreement with Malaysia and it has signed an FTA with China; it is negotiating FTAs with the GCC and Singapore; and it is considering an FTA with Indonesia.

In the Pacific, in addition to what has already been noted earlier, Australia is considering an FTA with the GCC countries. As for the Pacific Islands Forum, the Pacific Island Countries Trade Agreement (PICTA)49 among them has entered into force and they are negotiating an EPA with the EU.

Central Asia

Integration initiatives in Central Asia have been mainly directed at re-establishing the economic links that existed before the fall of the communist block. However, most early attempts to reproduce those links through plurilateral initiatives, i.e the CIS FTA, have not materialized and although the CIS institutional framework is still present, preferential liberalization has been achieved through an overlapping network of bilateral agreements and other plurilateral initiatives; the latter include the Single Economic Space between Kazakhstan, Russia, Belarus and Ukraine; the EurAsian Economic Community between Russia, Belarus, Kazakhstan, Kyrgyzstan and Tajikistan;50 and the Central Asian Cooperation Organization,

48 Same members as SAPTA (see list of acronyms in Annex).

49 As of June 2005, ten countries had already ratified PICTA, while six signatories were needed for it becoming effective.

50 The EAEC emerged from a CU between Russia, Belarus and Kazakhstan with the later accession of Kyrgyzstan and Tajikistan. Ukraine and Moldova have been granted the status of observers.

whose members are Kazakhstan, Kyrgyzstan, Tajikistan, Uzbekistan and Russia.51 Other regional organizations include the ECO52 whose members, among other initiatives, have signed in 2003 the ECO trade agreement (ECOTA) providing for tariff reductions and have agreed in 2005 on the common objective of forming an FTA in the future.53

51 CACO replaces the Central Asia Economic Union, which was composed by Kazakhstan, Kyrgyzstan and Uzbekistan. When Tajikistan joined in 1998, it was renamed Central Asian Economic Cooperation. Its f inal name, CACO, was adopted in 2002 and then Russia joined the group in 2004.

52 ECO, which was founded originally in 1985 by Iran, Turkey and Pakistan, was later joined by Afghanistan, Azerbaijan, Kazakhstan, Kyrg yzstan, Tajik istan, Turkmenistan, and Uzbekistan.

53 ECO Vision 2015

21

Ma

p 4

A

sia

-Pa

cif

ic I

ntr

a-R

eg

ion

al

RT

A N

etw

ork

AS

EA

N

Sin

gap

ore

Macao

,C

hin

a

PIC

TA

PA

TC

RA

BIM

ST

EC

MS

G

SP

AR

TE

CA

CE

R

AS

EA

N

Macao

,C

hin

a

PIC

TA

PA

TC

RA

BIM

ST

EC

MS

G

SP

AR

TE

CA

CE

R

AS

EA

N

Macao

,C

hin

a

PIC

TA

PA

TC

RA

BIM

ST

EC

MS

G

SP

AR

TE

CA

CE

R

So

uth

As

ian

Fre

e T

rad

e A

rea

AS

EA

N F

ree

Tra

de

Are

a

Pa

cifi

c I

sla

nd

s C

ou

ntr

ies

Tra

de

Ag

ree

me

nt

(PIC

TA

)

As

ia-P

ac

ific

Tra

de

Ag

ree

me

nt

Sig

ne

d /

In

Fo

rce

Un

de

r N

eg

oti

ati

on

Un

de

r C

on

sid

era

tio

n

22

Ma

p 5

As

ia-P

ac

ific

Cro

ss

-Re

gio

na

l R

TA

Ne

two

rk

So

uth

As

ian

Fre

e T

rad

e A

rea

AS

EA

N F

ree

Tra

de

Are

a

As

ia-P

ac

ific

Tra

de

Ag

ree

me

nt

Pa

cifi

c I

sla

nd

s C

ou

ntr

ies

Tra

de

Ag

ree

me

nt

(PIC

TA

)S

ign

ed

/ I

n F

orc

e

Un

de

r N

eg

oti

ati

on

Un

de

r C

on

sid

era

tio

n

Jo

rda

n

Ba

hra

in

Eg

yp

t

Un

ite

d

Sta

tes

Ch

ile

Me

xic

o

Ca

na

da

Gu

ate

ma

la

Nic

ara

gu

a

Pa

na

ma

GC

C

Ma

uri

tiu

s

SA

CU

Ho

nd

ura

s

El S

alv

ad

or

Pe

ru

ME

RC

OS

UR

PICTA

Bru

ne

i, C

hile

,

Ne

w Z

ea

lan

d &

Sin

ga

po

re

EU

-PA

CIF

ICE

PA

ASEAN

Do

min

ica

n

Re

pu

blic

Sin

ga

po

re

PIC

TA

AS

EA

N

EU

EF

TA

23

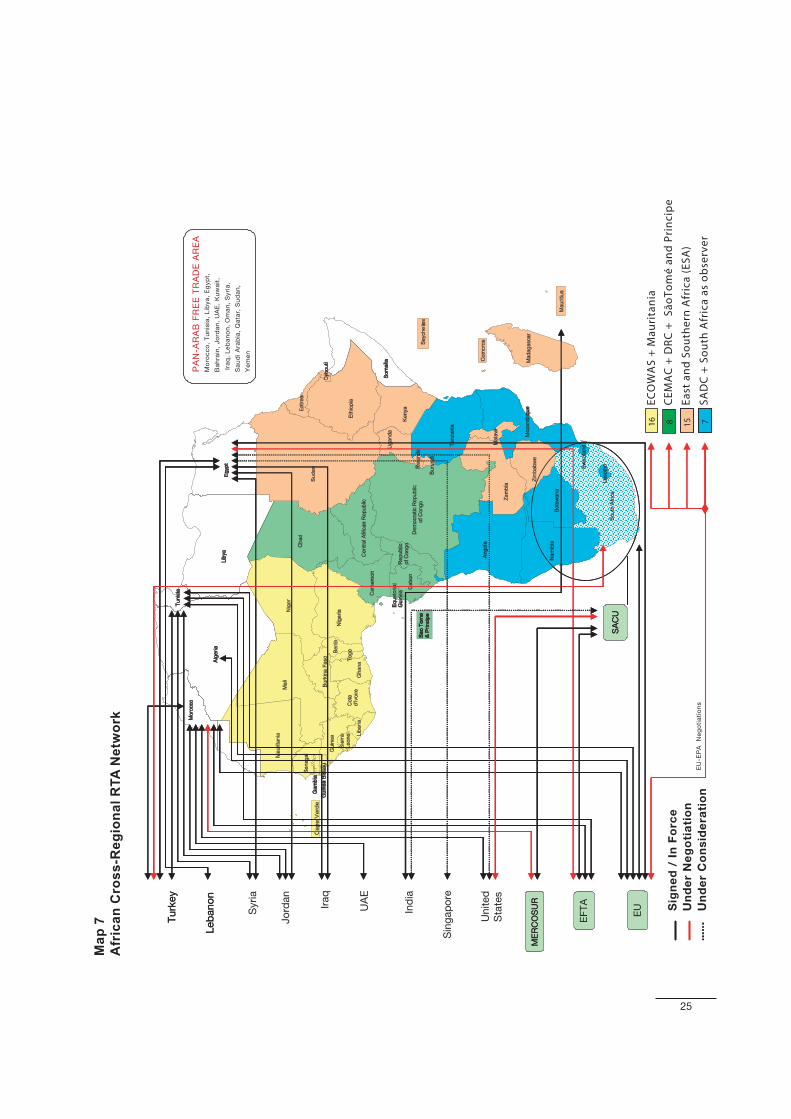

North Africa and Middle East

The most significant initiatives in the regional drive towards closer economic integration include the Agadir Agreement between Jordan, Egypt, Tunisia and Morocco; the agreement was signed in February 2004 and was scheduled to enter into force in January 2006, however, that does not seem to have been the case. The other initiative is the Pan-Arab Free Trade Area54; the agreement has been ratified by its members and is currently in force. As for the Gulf countries, the GCC has established itself as a CU and is engaged in several RTA negotiations both with regional and cross-regional partners. On the cross-regional front, the GCC shares a peculiarity that has been observed also in other CUs whereby while most RTA negotiations are engaged as a group, in others (in this case the United States), GCC members have chosen a “go alone” policy.

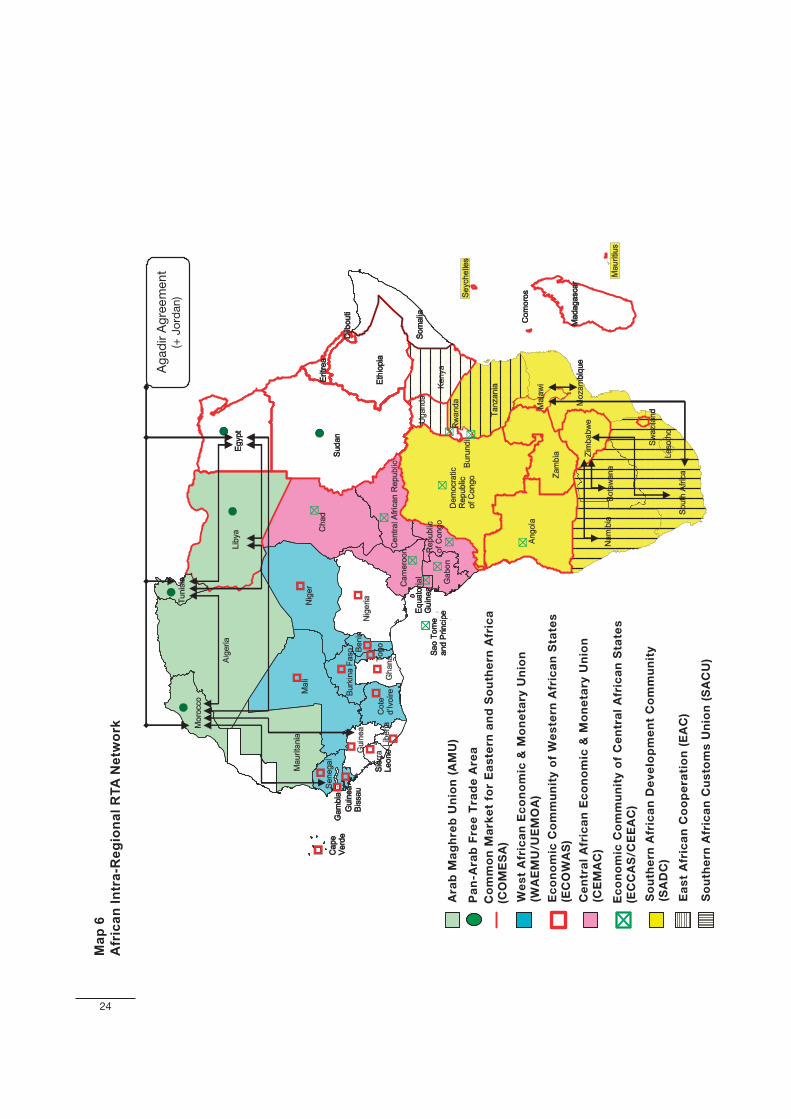

Sub-Sahara Africa

Among all world regions, African RTAs come closest to the traditional concept of regional integration based on the geographical proximity of the RTA partners and political co-operation through economic integration. The ambitious goals of most African RTAs (CU, common markets and economic and monetary unions); their low level of intra regional trade; poor implementation of several agreements; and their overlapping membership, tend to confirm the dominant role played by regional politics in the design of the region's RTAs. Turning to extra-regional preferential trade relations, these have been based, until recently, on non-reciprocal preferences under schemes such as the GSP, the African Growth Opportunity Act (AGOA), and the EU-ACP programmes. Most countries of the continent benefit from such preferential schemes, the exception being countries in North Africa and in Southern Africa that have foregone unilateral preference for reciprocal RTAs with partners in Europe, and more recently in the Western Hemisphere, Asia-Pacific and the Middle East.

54 Pan-Arab FTA members are: the GCC countries plus Egypt, Iraq, Jordan, Lebanon, Libyan Arab Jamahiriya, Morocco, Sudan, Syrian Arab Republic, Tunisia, and Yemen.

The shift to reciprocal preferences will soon extend to most Sub-Saharan countries with the EPAs replacing the long-standing unilateral preferences granted by the EU under its ACP policy. The EPA process has taken centre stage of African RTA developments in recent years and it is likely to significantly affect intra-RTA dynamics given the asymmetry in members' configuration among these agreements and existing integration schemes. The EPA process is supposed to build upon and strengthen existing regional integration arrangements; while this may be the case in Western and Central Africa, where negotiations are taking place with the ECOWAS and CEMAC configurations (with the sole inclusion of Mauritania in ECOWAS and Sao Tomé and Principe and DR Congo in CEMAC),55 it may not be so apparent in Eastern and Southern Africa where the EPA negotiations foresee two configurations (East and Southern Africa (ESA) and SADC minus) with members from four distinct regional integration schemes.56 Considering that each of these RTAs is already (EAC and SACU) a CU, or planning to become one (SADC and COMESA) it is expected that the ESA and SADC EPAs may clash significantly with the integration agendas of the existing RTAs.57

55 The UEMOA has already been a functioning monetary union since 1994; the ECOWAS, comprising all UEMOA members plus other West African countries, decided to merge with UEMOA. On 1 January 2005, ECOWAS launched the CET to become a CU, providing for three years of transition period.

56 The COMESA, the SADC, the EAC and the SACU.

57 Examples of such conf licts are numerous. The most blatant is Tanzania, which is in a CU with Kenya and Uganda, and negotiating with the SADC EPA while Kenya and Uganda have opted for the ESA EPA. Conversely, SADC members Malawi, Mauritius, Zambia and Zimbabwe have chosen to negotiate with ESA while COMESA members Angola and Swaziland (the latter is also a SACU member) have opted for the SADC EPA configuration. A further complicating factor is the standing of South Africa with respect to these negotiations given its membership in SACU and its FTA already in place with the EU.

24

Ma

p 6

Afr

ica

n I

ntr

a-R

eg

ion

al

RT

A N

etw

ork

Ag

ad

irA

gre

em

en

t(+

Jo

rdan)

Ara

b M

ag

hre

b U

nio

n (

AM

U)

Pa

n-A

rab

Fre

e T

rad

e A

rea

Co

mm

on

Ma

rke

t fo

r E

as

tern

an

d S

ou

the

rn A

fric

a

(CO

ME

SA

)

We

st

Afr

ica

n E

co

no

mic

& M

on

eta

ry U

nio

n

(WA

EM

U/U

EM

OA

)

Ec

on

om

ic C

om

mu

nit

y o

f W

es

tern

Afr

ica

n S

tate

s

(EC

OW

AS

)

Ce

ntr

al

Afr

ica

n E

co

no

mic

& M

on

eta

ry U

nio

n

(CE

MA

C)

Ec

on

om

ic C

om

mu

nit

y o

f C

en

tra

l A

fric

an

Sta

tes

(E

CC

AS

/CE

EA

C)

So

uth

ern

Afr

ica

n D

ev

elo

pm

en

t C

om

mu

nit

y

(SA

DC

)

Ea

st

Afr

ica

n C

oo

pe

rati

on

(E

AC

)

So

uth

ern

Afr

ica

n C

us

tom

s U

nio

n (

SA

CU

)

25

Ma

p 7

A

fric

an

Cro

ss

-Re

gio

na

l R

TA

Ne

two

rk

ECO

WA

S +

Mau

rita

nia

CEM

AC

+ D

RC

+ S

ãoTo

mé

an

d P

rin

cip

e

East

an

d S

ou

the

rn A

fric

a (E

SA)

SAD

C +

So

uth

Afr

ica

as o

bse

rve

r

Sin

gap

ore

Tu

rkey

ME

RC

OS

UR

Leb

an

on

Sig

ne

d /

In

Fo

rce

Un

de

r N

eg

oti

ati

on

Un

de

r C

on

sid

era

tio

nE

U-E

PA

N

eg

oti

ati

on

s

SA

CU

PA

N-A

RA

B F

RE

E T

RA

DE

AR

EA

Mo

roc

co

, T

un

isia

, L

ibya

, E

gyp

t,

Ba

hra

in,

Jo

rda

n,

UA

E,

Ku

wa

it,

Ira

q,

Le

ba

no

n,

Om

an

, S

yri

a,

Sa

ud

i A

rab

ia,

Qa

tar,

Su

da

n,

Ye

me

n

16 8 15 7

Jo

rdan

UA

E

Tu

rkey

Ind

ia

Un

ited

Sta

tes

ME

RC

OS

UR

Leb

an

on

Iraq

Syri

a

SA

CU

EU

EF

TA