the changing landscape of rewards, performance, … · 2.50% 2.75% 3.00% 3.25% 3.50% 3.75% 4.00%...

TRANSCRIPT

THE CHANGING LANDSCAPE OF REWARDS, PERFORMANCE, AND TALENT

September 23, 2014

About Ward Group

• Ward Group is a consulting and analytical firm specializing in the insurance industry and the leading provider of industry benchmarking and best practices services. Our services include:

– Expense, staffing & performance analysis for all functions

– Compensation and pay practices surveys

– Executive compensation consulting

– Distribution management

• Annual evaluation of the financial performance of industry

Jeff Rieder, CPA, CPCUPartnerHead of Ward [email protected](513) 746-2400 (direct)

2 |

About The Jacobson Group

• The Jacobson Group is the leading global provider of insurance talent. For more than 40 years, we have been connecting organizations with insurance professionals through a variety of solutions including the following:

– Executive search

– Professional recruiting

– Emerging talent

– Recruitment process outsourcing

– Temporary staffing

– Subject matter experts

– Onsite and work-at-home operations support

Greg JacobsonCEOThe Jacobson [email protected](312) 884-0407 (direct)

3 |

Objectives

• Analyze current labor trends and future staffing expectations

• Provide an overview of compensation trends and performance

4 |

Key Industry Trends

5 |

Industry Challenges and Initiatives

6 |

CHALLENGES FACING THE INDUSTRY

– Keeping up with technology and managing the associated costs.

– Finding growth in “less hard” market

– Keeping pace with the evolution of data analysis and predictive analytics.

– Prospect of diminishing returns after strong 2013

– Personal Auto product and pricing strategy – Telematics/UBI.

TOP INITIATIVES

– Strategic planning around distribution strategy – evaluating alternate distributions, strengthening key agency relationships, and renewed focus on terminating unprofitable agencies.

– Enhancing the customer experience is a focus of carriers encompassing all touch points in the lifetime of the relationship.

– Core system replacement and legacy retirement.

– Predictive analytics projects continue in underwriting, but now span the rest of the company including claims, agency management, marketing, telematics, and premium audit.

– Aligning company structure to future strategy.

Eight Important External Trends for Insurers

1. Auto Safety

Declining Frequency

7 |

Sources: Aon Benfield Analytics

2. Urbanization

Increasing Aggregations - Severity

3. Lower Interest Rates

Challenging Retirement /Lower Cost Catastrophe Reinsurance

4. Pace of Technology

Lifestyle Changing Technology/Expectations

Eight Important External Trends for Insurers

5. Segmentation

Less Privacy / But Individualization

8 |

Sources: Aon Benfield Analytics

6. Expanding Gov’t Safety Net

Increasing Needs / Increasing Problems

7. Longevity

Everyday is the new 30

8. Chronic Illness

Living Longer May Not be Comfortable

How is the Industry Performing?

Mixed

Needs Work

Improving…

• Return to underwriting profitability

• Capitalize on improving economy/push growth

• Distribution channel management

• Leverage technology investments

• Data analytics for informed business decisions

• Enhancing customer experience

9 |

Mixed

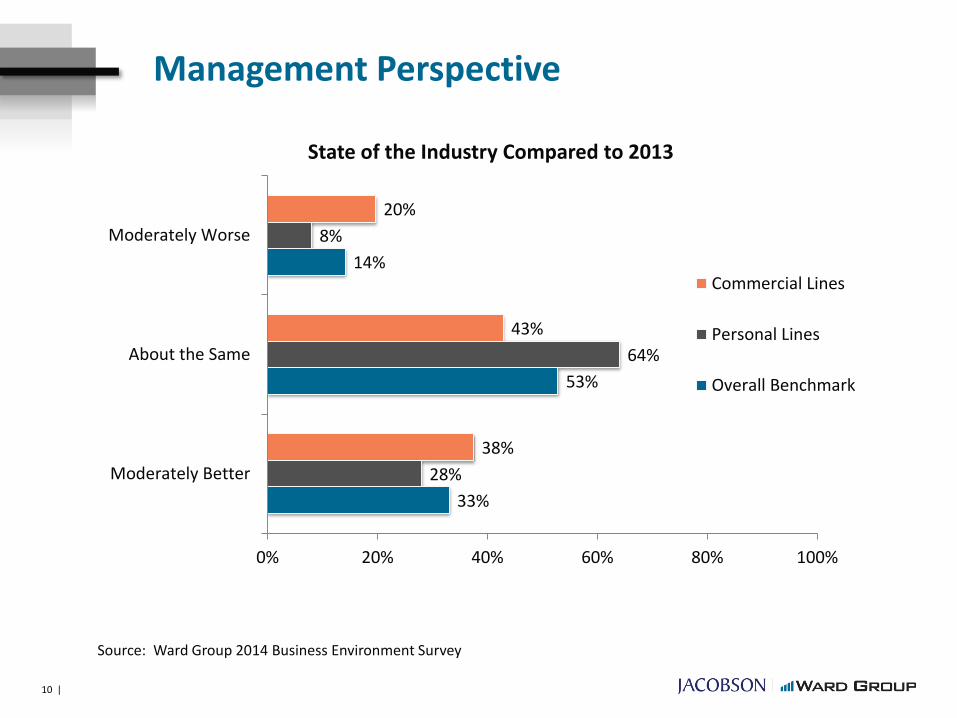

Management Perspective

10 |

33%

53%

14%

28%

64%

8%

38%

43%

20%

0% 20% 40% 60% 80% 100%

Moderately Better

About the Same

Moderately Worse

State of the Industry Compared to 2013

Commercial Lines

Personal Lines

Overall Benchmark

Source: Ward Group 2014 Business Environment Survey

Key Performance Measures

11

97.0%

76.3%

40.6%

30%

50%

70%

90%

110%

130%

150%

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

Combined Ratio Net Premium Written to Surplus Total Expenses

• Combined ratio is prior to effect of policyholder dividends• Expenses include Underwriting, Loss Adjusting and Investment

Avg. 39.9%

Avg. 104.1%

1990 – 2013

Worse

Better

11 |

Avg. 104.6%

2.50%

2.75%

3.00%

3.25%

3.50%

3.75%

4.00%

4.25%

1970 1975 1980 1985 1990 1995 2000 2005 2010

Macro Premium TrendsNet Written Premium to GDP Ratio

Sources: A.M. Best’s Aggregates and Averages, IMF World Economic Outlook Database (www.imf.org), Aon Benfield Analytics

Historical ratio of NPW to GDP provides a macro-level summary of

the underwriting cycle of hard and soft markets

0.6

%

3 years

1.1

%

3 years

0.5

%

4 years

0.6

%

7 years

1.1

%

13 years

>0

.7%

9+ years

3%

12 |

Modest Expense Improvement

13

* Expenses include Underwriting, Loss Adjusting and Investment Expenses

13 |

36.9%

40.6%

32%

34%

36%

38%

40%

42%

44%

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

Total Expenses as % of Net Premiums Written

Ward's 50 Total Industry

2014 Spending Changes - By Function

14 |

0% 20% 40% 60% 80% 100%

Rent/Occupancy

General Counsel

Billing and Collections

Finance

Other Sales Expense

Investment Mgmt

Commissions

Agency/Broker Mgmt

Audit

Human Resources

Personal UW/Processing

Product Development

Claims Administration

Marketing

Actuarial

Commercial UW/Processing

Information Technology

Spend Levels Compared to 2013

Significantly Less (-15% or less)Moderately Less (-3% to -15%)About the Same (-3% to 3%)Moderately More (3% to 15%)Significantly More (15% or more)

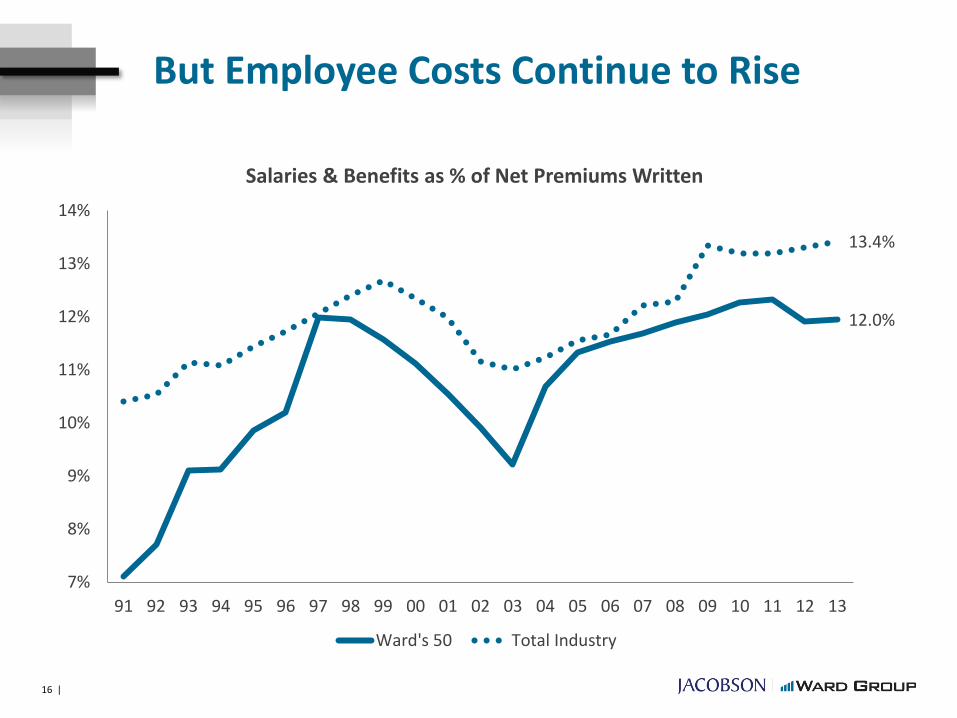

But Employee Costs Continue to Rise

1616 |

12.0%

13.4%

7%

8%

9%

10%

11%

12%

13%

14%

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

Salaries & Benefits as % of Net Premiums Written

Ward's 50 Total Industry

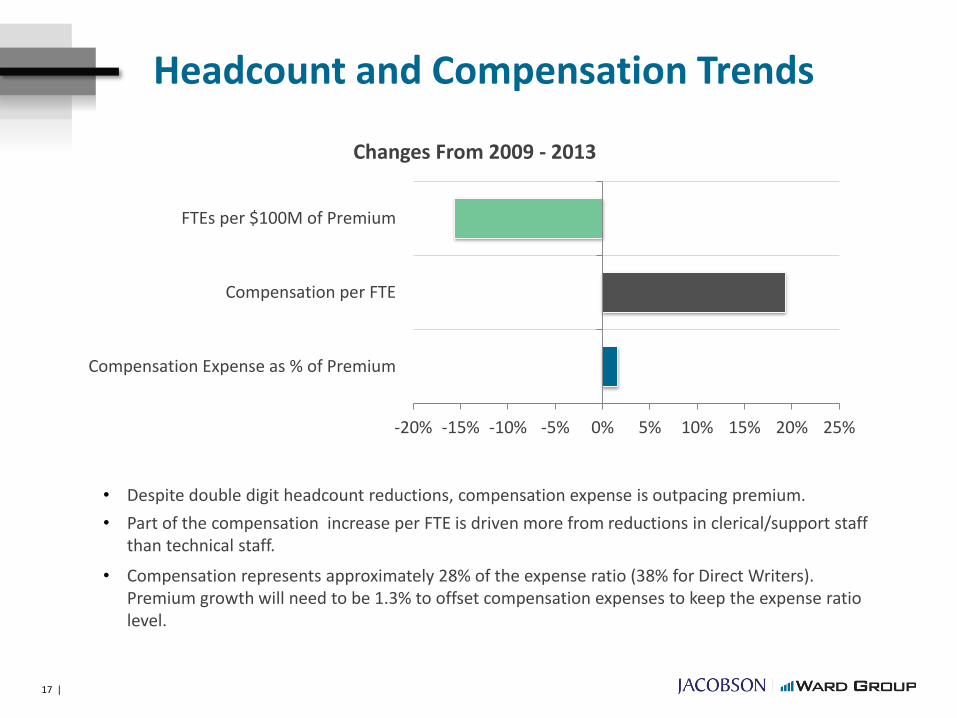

Headcount and Compensation Trends

-20% -15% -10% -5% 0% 5% 10% 15% 20% 25%

Compensation Expense as % of Premium

Compensation per FTE

FTEs per $100M of Premium

Changes From 2009 - 2013

• Despite double digit headcount reductions, compensation expense is outpacing premium.

• Part of the compensation increase per FTE is driven more from reductions in clerical/support staff than technical staff.

• Compensation represents approximately 28% of the expense ratio (38% for Direct Writers). Premium growth will need to be 1.3% to offset compensation expenses to keep the expense ratio level.

17 |

Functional Productivity Improvement

0% 5% 10% 15% 20%

Billing

Personal Processing

Commercial Processing

Claims

Commercial UW

Personal UW

Productivity Improvement per Policy or Reported Claim from 2008 - 2012

• Only Personal Processing realized a decrease in the expense ratio.

• Claims improvement driven by new claims systems and centralization /consolidation of headcount.

• Commercial and Personal Underwriting improvements in automation and predictive analytics. Also benefit from higher retentions with high percentage of automated renewals.

• Commercial and Personal Policy Processing realizing benefits of automation, particularly through streamlining agency interface and more automated renewal processing (both eliminating duplicate entry)

• Billing and collections on-line payment systems and automated payment processing contributing to the billing productivity gains.

18 |

Hiring and Employment Trends

19 |

Unemployment Rates

Source: U.S. Bureau of Labor Statistics

2.4%

6.1%

0%

2%

4%

6%

8%

10%

12%

Insurance & Related Overall 6 per. Mov. Avg. (Insurance & Related)

20 |

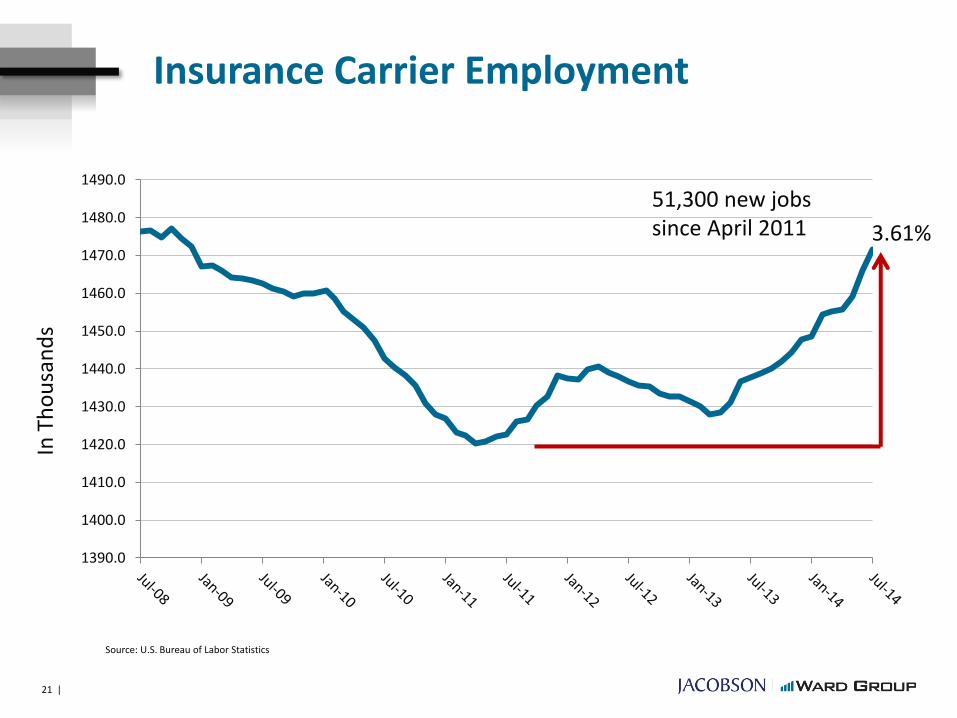

Insurance Carrier Employment

1390.0

1400.0

1410.0

1420.0

1430.0

1440.0

1450.0

1460.0

1470.0

1480.0

1490.0

In T

ho

usa

nd

s

3.61%

51,300 new jobs since April 2011

21 |

Source: U.S. Bureau of Labor Statistics

2014 Revenue and Staffing Expectations

Source: Ward/Jacobson Labor Outlook Survey

Increase Revenue

84%

Flat Growth

13%

Decrease Revenue

3%

12 Month Revenue Plan

Increase Staff58%

Maintain Staff33%

Decrease Staff9%

12-Month Staffing Plan

22 |

12-Month Staffing Plans Increase versus Expected Revenue Growth

56%

66% 65% 66%

75%69%

77%

86%81%

87% 85%

35%

44%39%

44% 44%51%

54% 56% 54%

62%58%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Expected Revenue Growth Increase Employees

July 2009 – July 2014

• 87% of P&C companies expect an increase in revenue growth while 80% of Life/Health companies responded the same.

• Less than 3% of all surveyed companies expect a decrease in revenue during the next 12 months. 10% of Life/Health companies expect a decrease.

• Both Life/Health and P&C companies responded that the primary driver for expected revenue changes will be market share rather than pricing or expansion/contraction.

• 77% of national/multi-national companies expect market share to drive revenue changes compared to 53% of regional carriers.

23 |

Job Openings in Finance and Insurance

120

178163

185

213221

0

50

100

150

200

250

In T

ho

usa

nd

s

Source: U.S. Bureau of Labor Statistics24 |

Yearly Averages

12-Month Staffing Plans

67%

31%

2%

50%

44%

6%

48%

30%

22%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Increase FTE Maintain current size Decrease FTE

Small (Under 300) Medium (300-1000) Large (Over 1000)

By Employee Size

• 54% of small companies are expecting growth in revenue/premium at greater than 10%. This compares to 23% for large companies and 27% for medium-sized companies.

• 79% of large companies responded that revenue growth will be driven by market share compared to 62% of small and 47% of medium-sized companies.

25 |

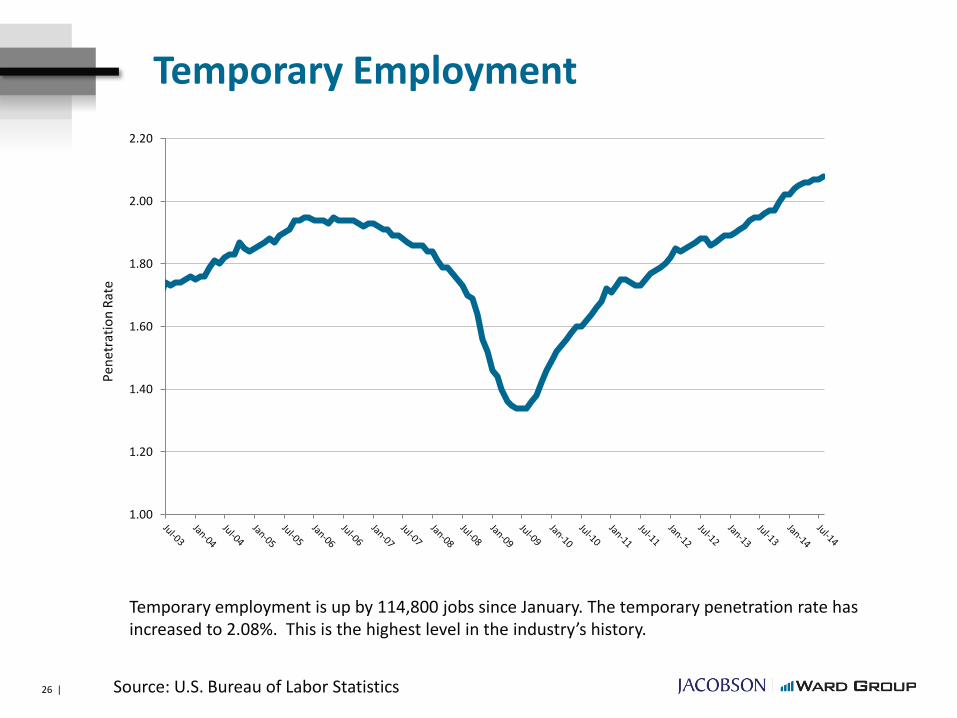

Temporary Employment

Source: U.S. Bureau of Labor Statistics

Temporary employment is up by 114,800 jobs since January. The temporary penetration rate has increased to 2.08%. This is the highest level in the industry’s history.

1.00

1.20

1.40

1.60

1.80

2.00

2.20

Pen

etra

tio

n R

ate

26 |

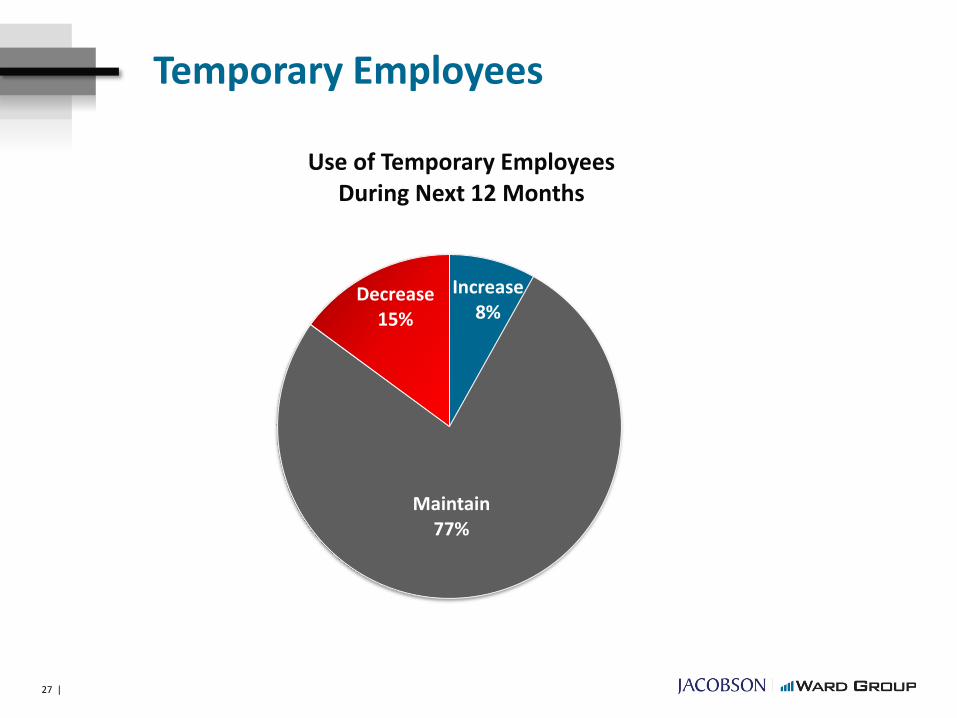

Temporary Employees

Increase8%

Maintain77%

Decrease15%

Use of Temporary Employees During Next 12 Months

27 |

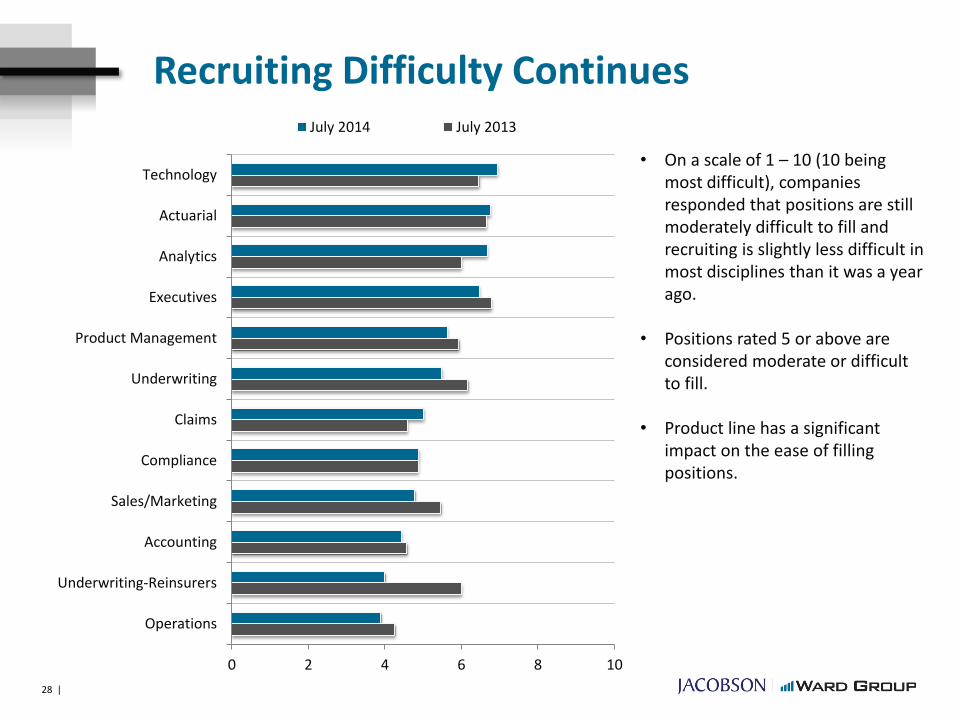

Recruiting Difficulty Continues

• On a scale of 1 – 10 (10 being most difficult), companies responded that positions are still moderately difficult to fill and recruiting is slightly less difficult in most disciplines than it was a year ago.

• Positions rated 5 or above are considered moderate or difficult to fill.

• Product line has a significant impact on the ease of filling positions.

0 2 4 6 8 10

Operations

Underwriting-Reinsurers

Accounting

Sales/Marketing

Compliance

Claims

Underwriting

Product Management

Executives

Analytics

Actuarial

Technology

July 2014 July 2013

28 |

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

P&C Balanced P&C Commercial P&C Personal

Most in Demand

Least in Demand

Least Likely

Likelihood of Increasing Staff By Function

Most Likely

• After Technology, large companies are most likely to increase staff in Analytics, medium-sized companies in Claims and small companies look to Underwriting.

• Commercial lines companies have a higher need for Underwriters in the next 12 months compared to personal lines companies.

• Life/Health companies have the greatest need in the Technology function followed by Sales/Marketing.

• Technology has had the greatest likelihood to increase staff in 10 of the past 11 surveys for P&C companies.

29 |

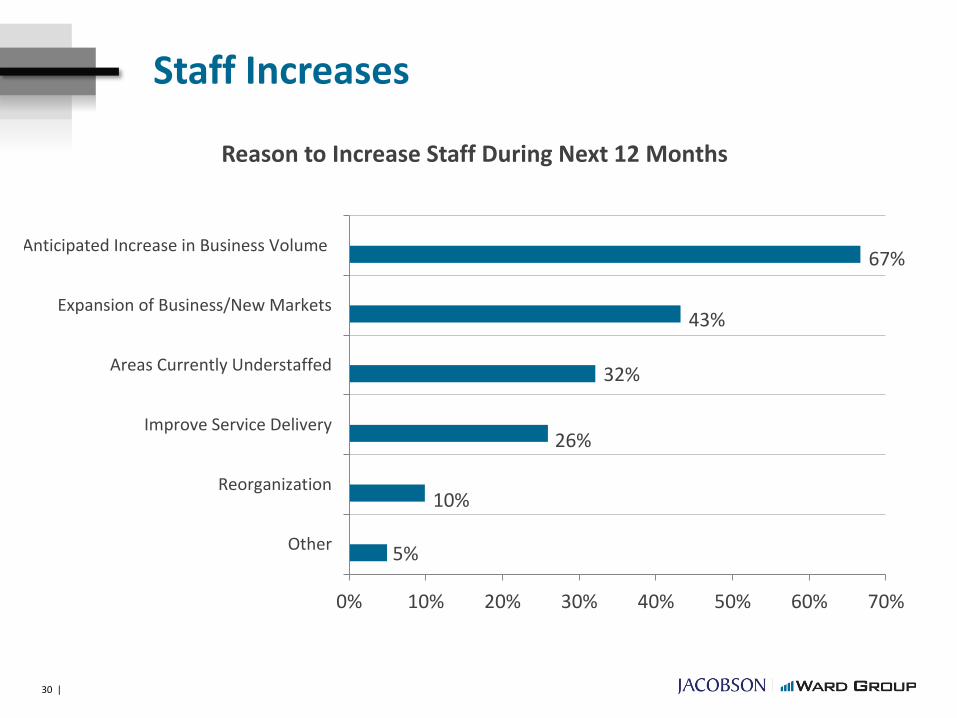

5%

10%

26%

32%

43%

67%

0% 10% 20% 30% 40% 50% 60% 70%

Other

Reorganization

Improve Service Delivery

Areas Currently Understaffed

Expansion of Business/New Markets

Anticipated Increase in Business Volume

Reason to Increase Staff During Next 12 Months

Staff Increases

30 |

Compensation Survey Key Findings

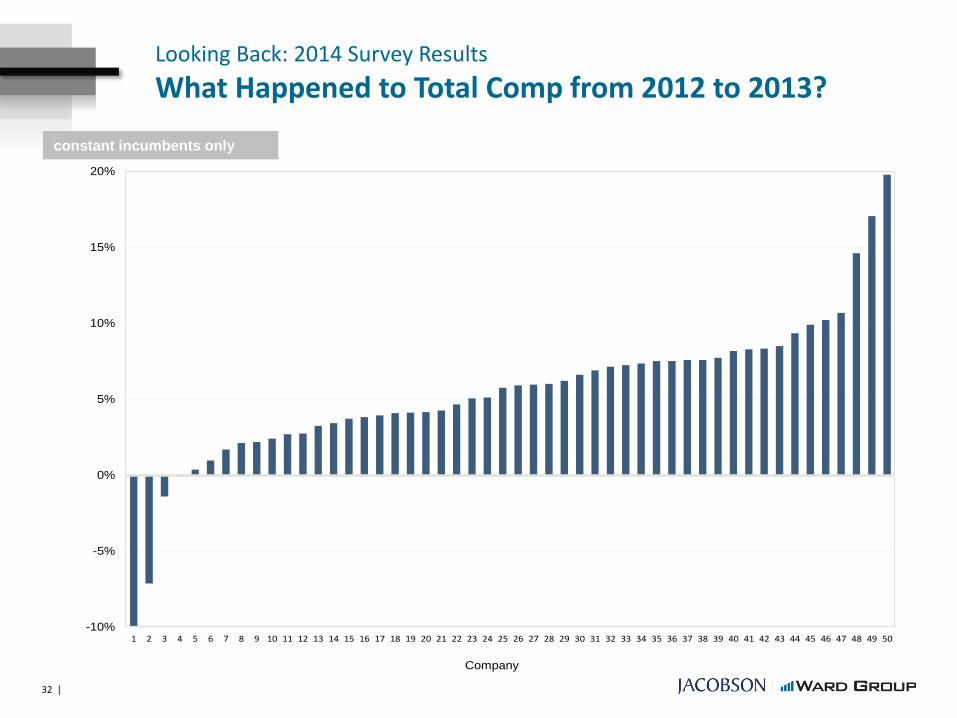

Looking Back: 2014 Survey Results

What Happened to Total Comp from 2012 to 2013?

-10%

-5%

0%

5%

10%

15%

20%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50

Company

constant incumbents only

32 |

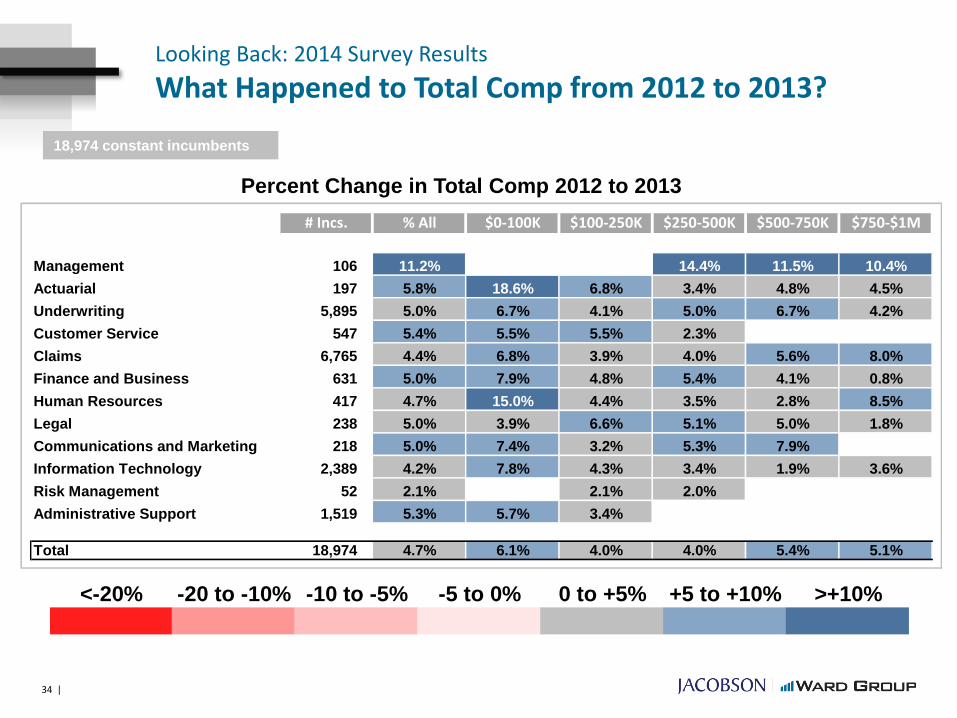

Looking Back: 2014 Survey Results

What Happened to Total Comp from 2012 to 2013?

<-30% -30 to -20% -20 to -10% -10 to 0% 0 to +10% +10 to +20% >+20%

LEGEND:

Percent Change in Total Comp 2012 to 2013

20,778 constant incumbents

# of Incs 10th 25th 50th 75th 90th

$0 to 50K 6,568 0.5% 2.9% 6.1% 15.5% 22.0%

$50 to 100K 11,220 0.0% 2.0% 4.0% 8.4% 18.3%

$100 to 150K 1,954 -2.0% 1.2% 4.0% 8.9% 16.7%

$150 to 200K 428 -2.6% 1.3% 5.6% 12.8% 24.4%

$200 to 250K 207 -4.5% 0.0% 4.6% 13.1% 28.4%

$250K+ 401 -11.1% -1.9% 5.1% 18.1% 42.9%

Total 20,778 -0.1% 2.0% 4.7% 10.8% 20.6%

33 |

Looking Back: 2014 Survey Results

What Happened to Total Comp from 2012 to 2013?

Percent Change in Total Comp 2012 to 2013

18,974 constant incumbents

<-20% -20 to -10% -10 to -5% -5 to 0% 0 to +5% +5 to +10% >+10%

# Incs. % All $0-100K $100-250K $250-500K $500-750K $750-$1M

Management 106 11.2% 14.4% 11.5% 10.4%

Actuarial 197 5.8% 18.6% 6.8% 3.4% 4.8% 4.5%

Underwriting 5,895 5.0% 6.7% 4.1% 5.0% 6.7% 4.2%

Customer Service 547 5.4% 5.5% 5.5% 2.3%

Claims 6,765 4.4% 6.8% 3.9% 4.0% 5.6% 8.0%

Finance and Business 631 5.0% 7.9% 4.8% 5.4% 4.1% 0.8%

Human Resources 417 4.7% 15.0% 4.4% 3.5% 2.8% 8.5%

Legal 238 5.0% 3.9% 6.6% 5.1% 5.0% 1.8%

Communications and Marketing 218 5.0% 7.4% 3.2% 5.3% 7.9%

Information Technology 2,389 4.2% 7.8% 4.3% 3.4% 1.9% 3.6%

Risk Management 52 2.1% 2.1% 2.0%

Administrative Support 1,519 5.3% 5.7% 3.4%

Total 18,974 4.7% 6.1% 4.0% 4.0% 5.4% 5.1%

34 |

$0

$20

$40

$60

$80

$100

$120

LT/Deferred Awards

Cash Bonus

Salary

Looking Back: 2014 Survey Results

Senior Underwriter PayConstant Incumbents

+5%

+5%

+4%

+4%

Comp Year

LowQ Med HighQ TopD LowQ Med HighQ TopD

Salary $64 $72 $84 $95 $66 $74 $87 $98

Total Cash $66 $76 $90 $104 $69 $79 $93 $108

Total Comp $66 $76 $90 $104 $69 $80 $94 $108

#Firms/Incs

2012 2013

40/1603 40/1603

35 |

$0

$20

$40

$60

$80

$100

$120

LT/Deferred Awards

Cash Bonus

Salary

Looking Back: 2014 Survey Results

Senior Finance & Accounting Staff PayConstant Incumbents

+4%

+6%

+8%

+10%

Comp Year

LowQ Med HighQ TopD LowQ Med HighQ TopD

Salary $64 $70 $80 $88 $67 $72 $83 $92

Total Cash $66 $72 $83 $93 $69 $76 $88 $102

Total Comp $66 $73 $83 $93 $69 $77 $90 $102

#Firms/Incs

2012 2013

29/185 29/185

36 |

20,778 constant incumbents

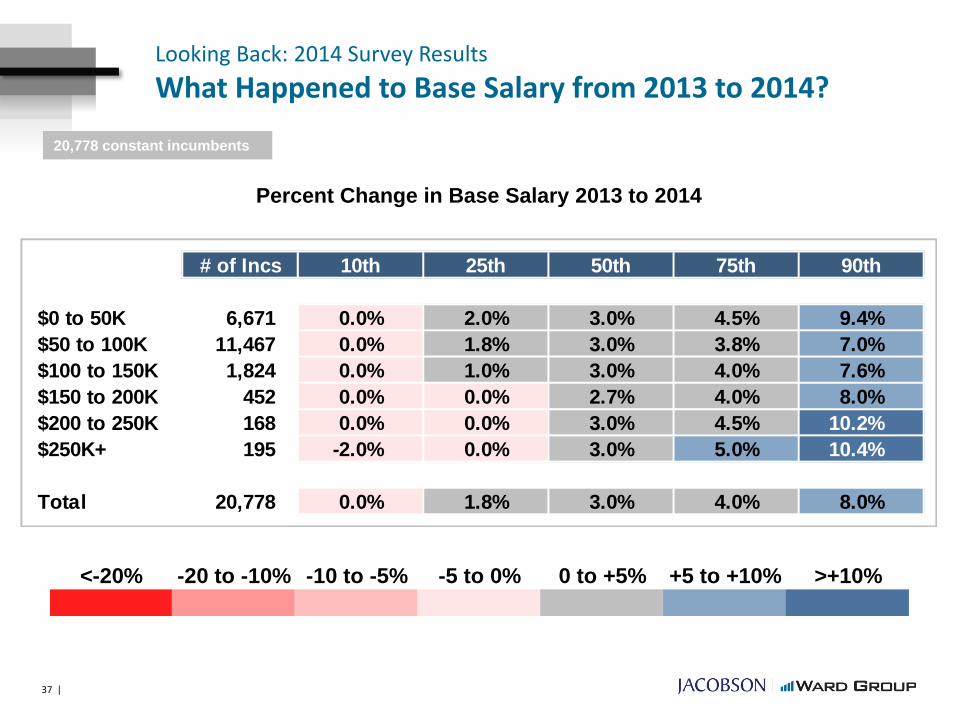

Looking Back: 2014 Survey Results

What Happened to Base Salary from 2013 to 2014?

Percent Change in Base Salary 2013 to 2014

<-20% -20 to -10% -10 to -5% -5 to 0% 0 to +5% +5 to +10% >+10%

# of Incs 10th 25th 50th 75th 90th

$0 to 50K 6,671 0.0% 2.0% 3.0% 4.5% 9.4%

$50 to 100K 11,467 0.0% 1.8% 3.0% 3.8% 7.0%

$100 to 150K 1,824 0.0% 1.0% 3.0% 4.0% 7.6%

$150 to 200K 452 0.0% 0.0% 2.7% 4.0% 8.0%

$200 to 250K 168 0.0% 0.0% 3.0% 4.5% 10.2%

$250K+ 195 -2.0% 0.0% 3.0% 5.0% 10.4%

Total 20,778 0.0% 1.8% 3.0% 4.0% 8.0%

37 |

Base Salary Increases

-1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

Average Base Salary Increase

38 |

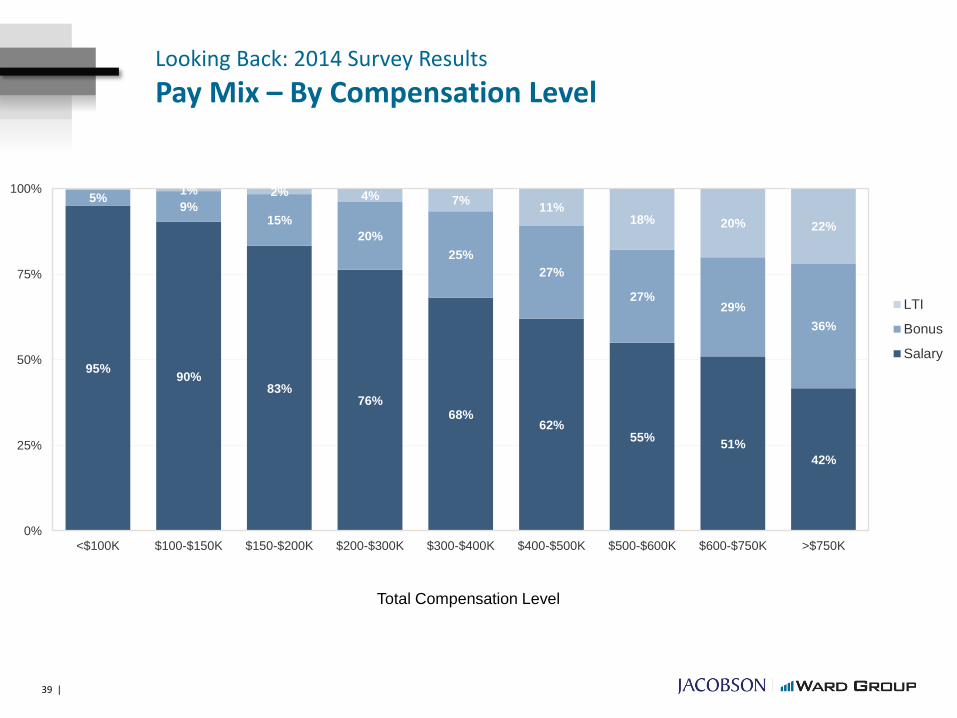

Total Compensation Level

Looking Back: 2014 Survey Results

Pay Mix – By Compensation Level

95%90%

83%76%

68%62%

55%51%

42%

5%9%

15%

20%

25%

27%

27%29%

36%

1% 2% 4% 7%11%

18% 20% 22%

0%

25%

50%

75%

100%

<$100K $100-$150K $150-$200K $200-$300K $300-$400K $400-$500K $500-$600K $600-$750K >$750K

LTI

Bonus

Salary

39 |

Looking Back: 2014 Survey Results

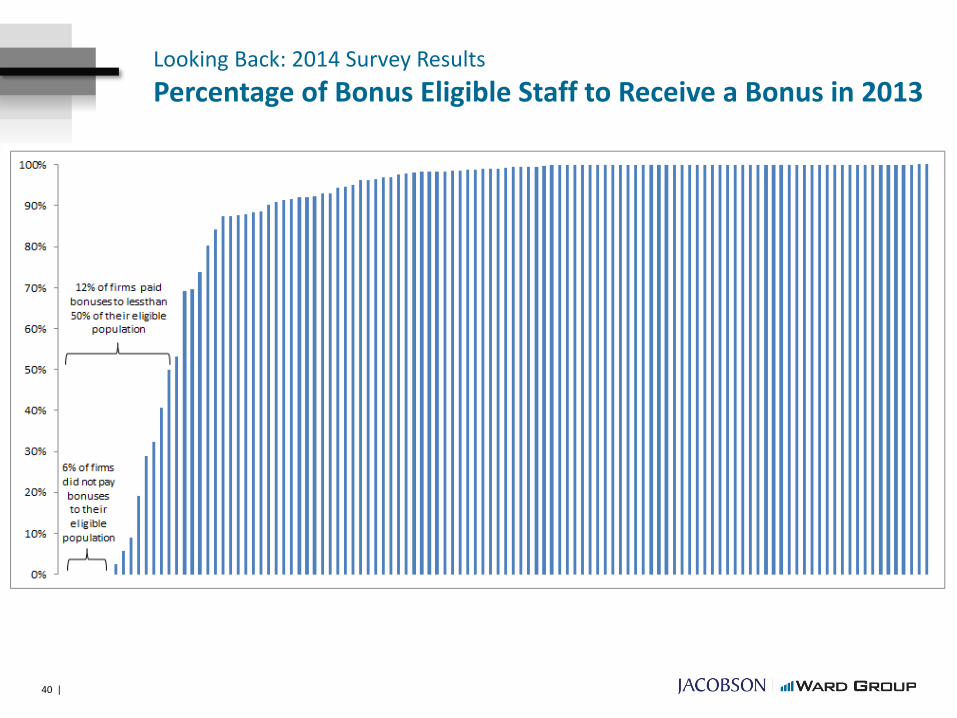

Percentage of Bonus Eligible Staff to Receive a Bonus in 2013

40 |

Looking Back: 2014 Survey Results

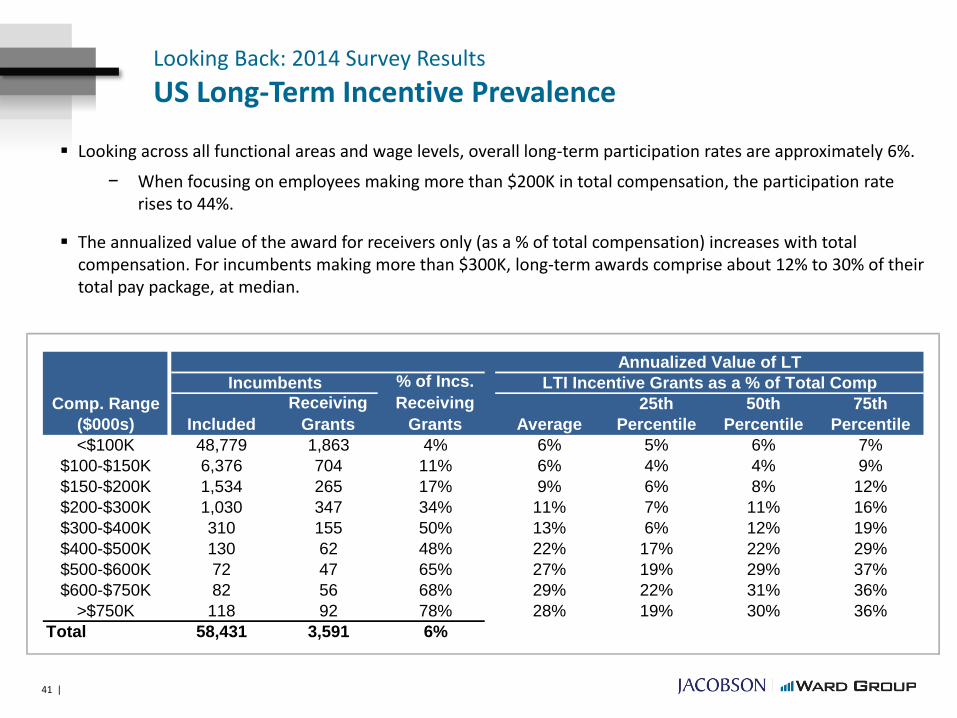

US Long-Term Incentive Prevalence

Looking across all functional areas and wage levels, overall long-term participation rates are approximately 6%.

− When focusing on employees making more than $200K in total compensation, the participation rate rises to 44%.

The annualized value of the award for receivers only (as a % of total compensation) increases with total compensation. For incumbents making more than $300K, long-term awards comprise about 12% to 30% of their total pay package, at median.

25th 50th 75th

($000s) Average Percentile Percentile Percentile

<$100K 48,779 1,863 4% 6% 5% 6% 7%

$100-$150K 6,376 704 11% 6% 4% 4% 9%

$150-$200K 1,534 265 17% 9% 6% 8% 12%

$200-$300K 1,030 347 34% 11% 7% 11% 16%

$300-$400K 310 155 50% 13% 6% 12% 19%

$400-$500K 130 62 48% 22% 17% 22% 29%

$500-$600K 72 47 65% 27% 19% 29% 37%

$600-$750K 82 56 68% 29% 22% 31% 36%

>$750K 118 92 78% 28% 19% 30% 36%

Total 58,431 3,591 6%

Comp. Range

Annualized Value of LT

Incumbents % of Incs.

Receiving

Grants

LTI Incentive Grants as a % of Total Comp

Included

Receiving

Grants

41 |

Long-Term Incentive

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

1 4 7

10

13

16

19

22

25

28

31

34

37

40

43

46

49

52

55

58

61

64

67

70

73

76

79

82

85

88

91

94

97

10

0

10

3

10

6

10

9

11

2

11

5

Long Term Incentive as % of Total Compensation

67% of companies did not provide long term incentives!

42 |

Long-Term Incentive

Notable Job FamiliesLTI as %

Total Comp

Overall 0.6%

Claims 0.5%

Underwriting 0.7%

Information Technology 0.5%

Finance & Business Services 1.0%

Human Resources 0.8%

Actuarial Service 0.8%

Communication & Marketing 1.0%

Product Management and Development 1.4%

Independent Agency/Broker 2.8%

Legal and Compliance 1.0%

Management 5.6%

• Mutual companies averaged only 0.1% LTI compared to 1.1% of Stock companies

• Ward 50 companies averaged 2.3% for LTI as compared to only 0.2% for Non-Ward 50 companies

• Large companies had 0.8% LTI compared to 0.3% for Medium and Small companies.

43 |

How well is pay linked with performance?

Survey Background

To further evaluate the link between performance and rewards, we evaluated the operating performance of 115 of the 132 participants that filed NAIC annual statements.

• We compared participants compensation results against public data along following key metrics:

• Return on Equity

• Return on Revenue

• Combined Ratio

• Expense Ratio

• Surplus Growth

• In addition, separate analysis was done for 30 companies in the Ward Expense Benchmarking Program to evaluate additional employee performance metrics.

45 |

Profile of Deep Dive Participants

564

1,042

504 411

863

41

332

2,105

Overall Ward 50 NonWard 50

Mutual Stock Small Medium Large

Average Net Premiums Written (millions)

100.6%

93.2%

101.5%

101.0%

99.7%

100.3%

102.0%

96.3%

Overall

Ward 50

Non Ward 50

Mutual

Stock

Small

Medium

Large

Combined Ratio

45.1%

41.7%

45.5%

44.4%

46.4%

53.5%

42.6%

40.4%

Overall

Ward 50

Non Ward 50

Mutual

Stock

Small

Medium

Large

Expense Ratio

14.9%

11.8%

15.3%

14.5%

15.9%

16.5%

14.7%

13.2%

Overall

Ward 50

Non Ward 50

Mutual

Stock

Small

Medium

Large

Salary and Benefits Expense

Mutual66%

Stock34%

Large17%

Medium56%

Small27%

# cos 115 13 102 76 39 30 65 20

46 |

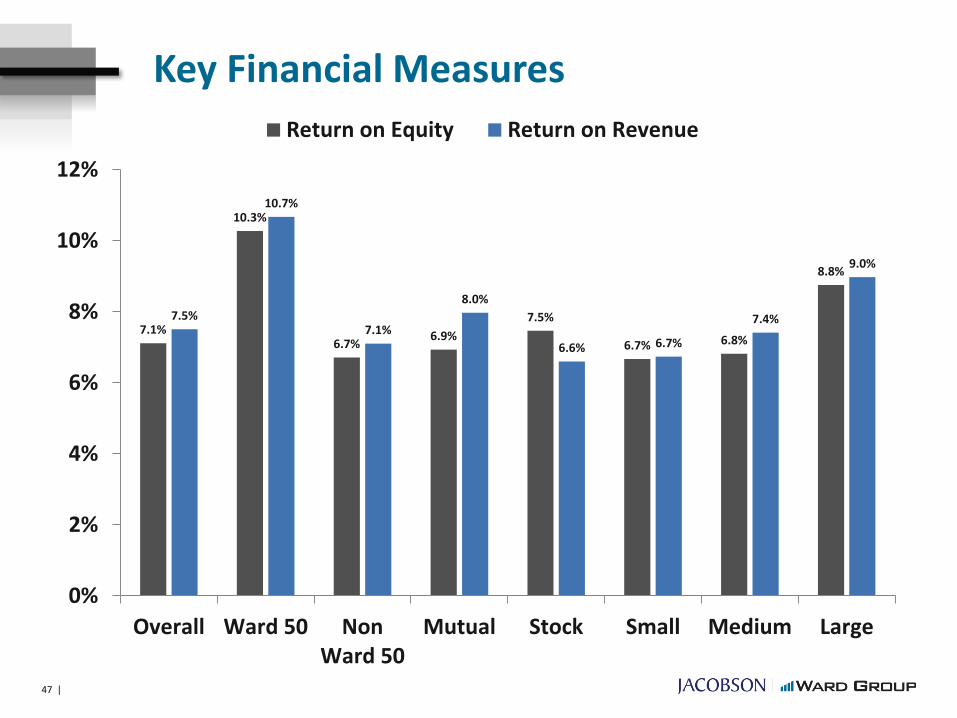

Key Financial Measures

7.1%

10.3%

6.7%6.9%

7.5%

6.7% 6.8%

8.8%

7.5%

10.7%

7.1%

8.0%

6.6% 6.7%

7.4%

9.0%

0%

2%

4%

6%

8%

10%

12%

Overall Ward 50 NonWard 50

Mutual Stock Small Medium Large

Return on Equity Return on Revenue

47 |

Key Financial Measures

9.9%

10.6%

9.8%

11.2%

7.3%

11.9%

9.5%

8.2%

10.0%

12.1%

9.7%10.2%

9.6%

11.1%10.6%

6.2%

0%

2%

4%

6%

8%

10%

12%

14%

Overall Ward 50 NonWard 50

Mutual Stock Small Medium Large

Surplus Growth Premium Growth

48 |

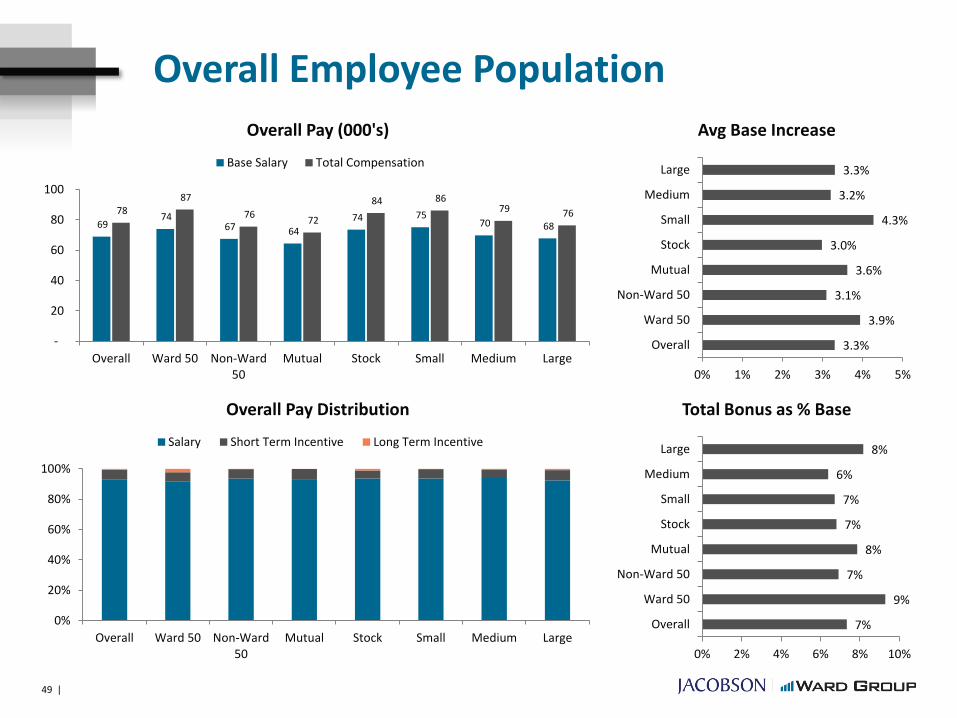

Overall Employee Population

69 74

67 64

74 75 70 68

78 87

76 72

84 86 79 76

-

20

40

60

80

100

Overall Ward 50 Non-Ward50

Mutual Stock Small Medium Large

Overall Pay (000's)

Base Salary Total Compensation

3.3%

3.9%

3.1%

3.6%

3.0%

4.3%

3.2%

3.3%

0% 1% 2% 3% 4% 5%

Overall

Ward 50

Non-Ward 50

Mutual

Stock

Small

Medium

Large

Avg Base Increase

0%

20%

40%

60%

80%

100%

Overall Ward 50 Non-Ward50

Mutual Stock Small Medium Large

Overall Pay Distribution

Salary Short Term Incentive Long Term Incentive

7%

9%

7%

8%

7%

7%

6%

8%

0% 2% 4% 6% 8% 10%

Overall

Ward 50

Non-Ward 50

Mutual

Stock

Small

Medium

Large

Total Bonus as % Base

49 |

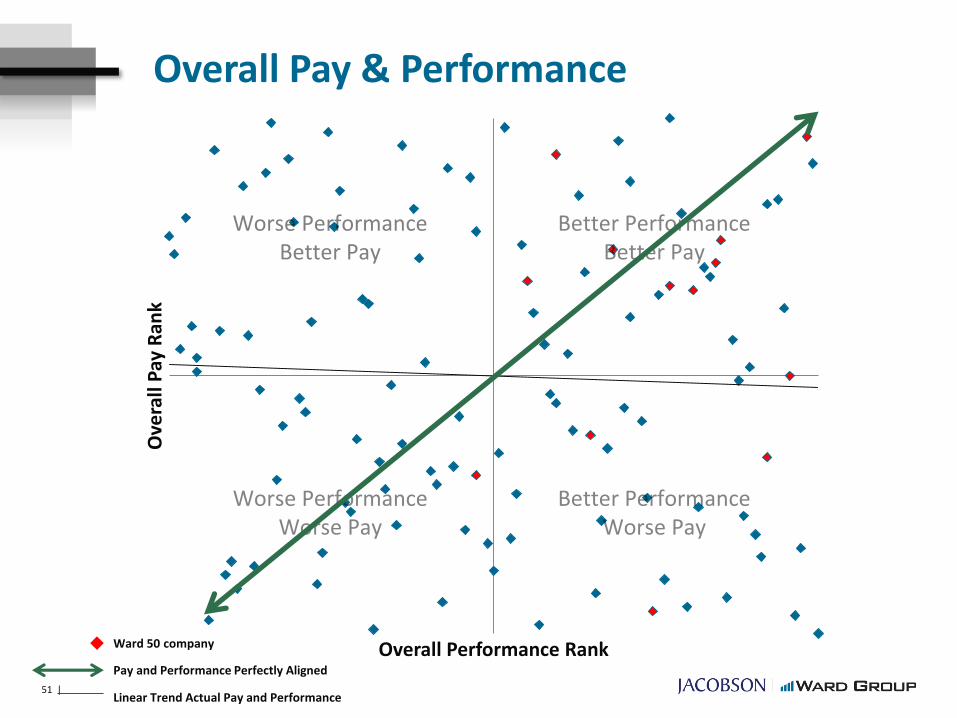

Overall Pay & Performance

• While the Ward 50 companies were more aligned between pay and performance, overall pay is generally not aligned with performance

• Many of the companies with the worst performance paid employees near the highest, perhaps indicating they are more likely to pay “at market” rather than based on organizational performance.

0%

20%

40%

60%

80%

100%

Surplus Growth Pay Percentile

0%

20%

40%

60%

80%

100%

Return on Equity Pay Percentile

0%

20%

40%

60%

80%

100%

Combined Ratio Pay Percentile

50 |

Overall Pay & Performance

Ward 50 company

Ove

rall

Pay

Ran

k

Overall Performance Rank

51 |

Pay and Performance Perfectly Aligned

Linear Trend Actual Pay and Performance

CEO/President

426 438 515

380

533

237

471

653 780

1,240

916

589

1,217

285

879

1,458

-

200

400

600

800

1,000

1,200

1,400

1,600

Overall Ward 50 Non-Ward50

Mutual Stock Small Medium Large

CEO/President - Property & Casualty Pay (000's)

Base Salary Total Compensation

5.8%

6.5%

5.5%

5.4%

6.5%

6.0%

5.8%

4.9%

0% 2% 4% 6% 8%

Overall

Ward 50

Non-Ward 50

Mutual

Stock

Small

Medium

Large

Avg Base Increase

0%

20%

40%

60%

80%

100%

Overall Ward 50 Non-Ward50

Mutual Stock Small Medium Large

CEO/President - Property & Casualty Pay Distribution

Salary Short Term Incentive Long Term Incentive

41%

97%

48%

31%

73%

16%

49%

94%

0% 50% 100% 150%

Overall

Ward 50

Non-Ward 50

Mutual

Stock

Small

Medium

Large

Total Bonus as % Base

52 |

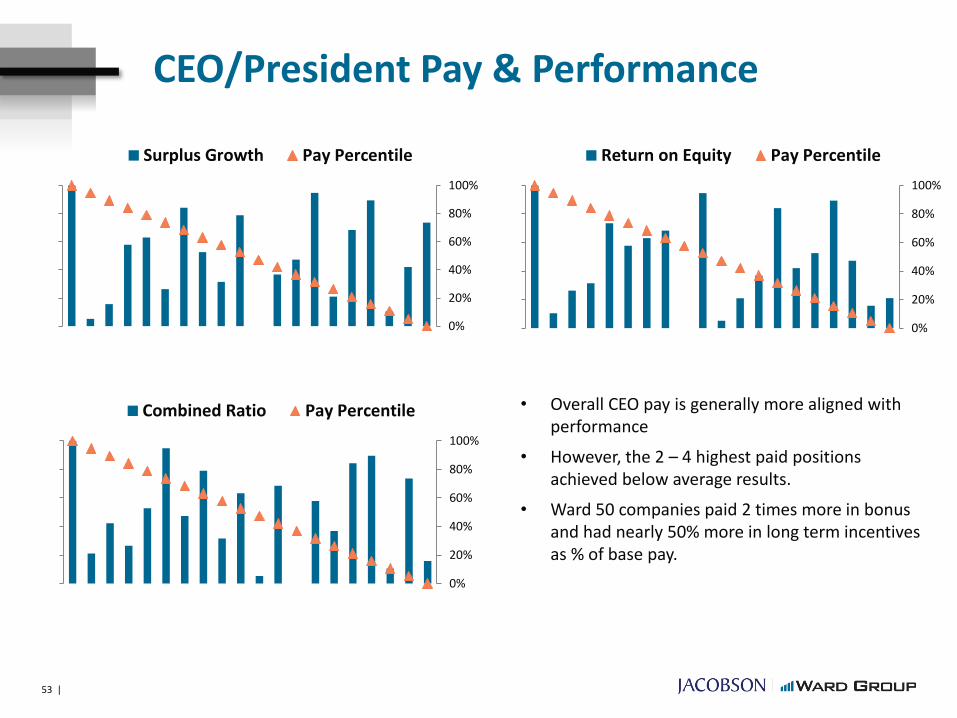

CEO/President Pay & Performance

• Overall CEO pay is generally more aligned with performance

• However, the 2 – 4 highest paid positions achieved below average results.

• Ward 50 companies paid 2 times more in bonus and had nearly 50% more in long term incentives as % of base pay.

0%

20%

40%

60%

80%

100%

Surplus Growth Pay Percentile

0%

20%

40%

60%

80%

100%

Return on Equity Pay Percentile

0%

20%

40%

60%

80%

100%

Combined Ratio Pay Percentile

53 |

CEO/President Pay & Performance

CEO

Pay

Ran

k

CEO Total Performance RankWard 50 company

54 |

Pay and Performance Perfectly Aligned

Linear Trend Actual Pay and Performance

Underwriting

67 73

65 59

77 81

69 65

76 85

72 65

89 96

78 73

-

20

40

60

80

100

120

Overall Ward 50 Non-Ward50

Mutual Stock Small Medium Large

Underwriting Pay (000's)

Base Salary Total Compensation

3.6%

4.2%

3.3%

3.7%

3.4%

4.7%

3.6%

3.4%

0% 1% 2% 3% 4% 5%

Overall

Ward 50

Non-Ward 50

Mutual

Stock

Small

Medium

Large

Avg Base Increase

0%

20%

40%

60%

80%

100%

Overall Ward 50 Non-Ward50

Mutual Stock Small Medium Large

Underwriting Pay Distribution

Salary Short Term Incentive Long Term Incentive

9%

10%

8%

8%

9%

7%

8%

10%

0% 5% 10% 15%

Overall

Ward 50

Non-Ward 50

Mutual

Stock

Small

Medium

Large

Total Bonus as % Base

55 |

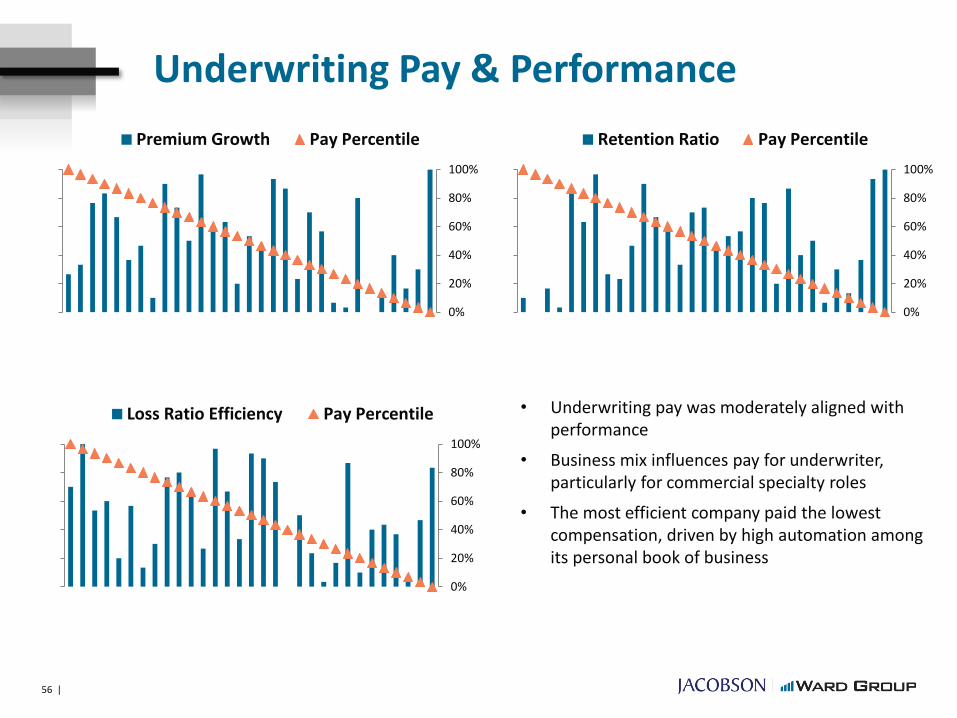

Underwriting Pay & Performance

• Underwriting pay was moderately aligned with performance

• Business mix influences pay for underwriter, particularly for commercial specialty roles

• The most efficient company paid the lowest compensation, driven by high automation among its personal book of business

0%

20%

40%

60%

80%

100%

Premium Growth Pay Percentile

0%

20%

40%

60%

80%

100%

Retention Ratio Pay Percentile

0%

20%

40%

60%

80%

100%

Loss Ratio Efficiency Pay Percentile

56 |

Underwriting Pay & Performance

Un

de

rwri

tin

g P

ay R

ank

Underwriting Performance RankWard 50 company

57 |

Pay and Performance Perfectly Aligned

Linear Trend Actual Pay and Performance

Claims

66 72

65 64 68 69 67 65

71

80

69 69 73 75 71 71

-

10

20

30

40

50

60

70

80

90

Overall Ward 50 Non-Ward50

Mutual Stock Small Medium Large

Claims Pay (000's)

Base Salary Total Compensation

3.1%

3.5%

3.0%

3.6%

2.7%

4.2%

3.0%

3.1%

0% 1% 2% 3% 4% 5%

Overall

Ward 50

Non-Ward 50

Mutual

Stock

Small

Medium

Large

Avg Base Increase

0%

20%

40%

60%

80%

100%

Overall Ward 50 Non-Ward50

Mutual Stock Small Medium Large

Claims Pay Distribution

Salary Short Term Incentive Long Term Incentive

6%

9%

5%

7%

5%

5%

5%

7%

0% 2% 4% 6% 8% 10%

Overall

Ward 50

Non-Ward 50

Mutual

Stock

Small

Medium

Large

Total Bonus as % Base

58 |

Claims Pay & Performance

0%

20%

40%

60%

80%

100%

Expense Efficiency Pay Percentile

0%

20%

40%

60%

80%

100%

Staff Efficiency Pay Percentile

0%

20%

40%

60%

80%

100%

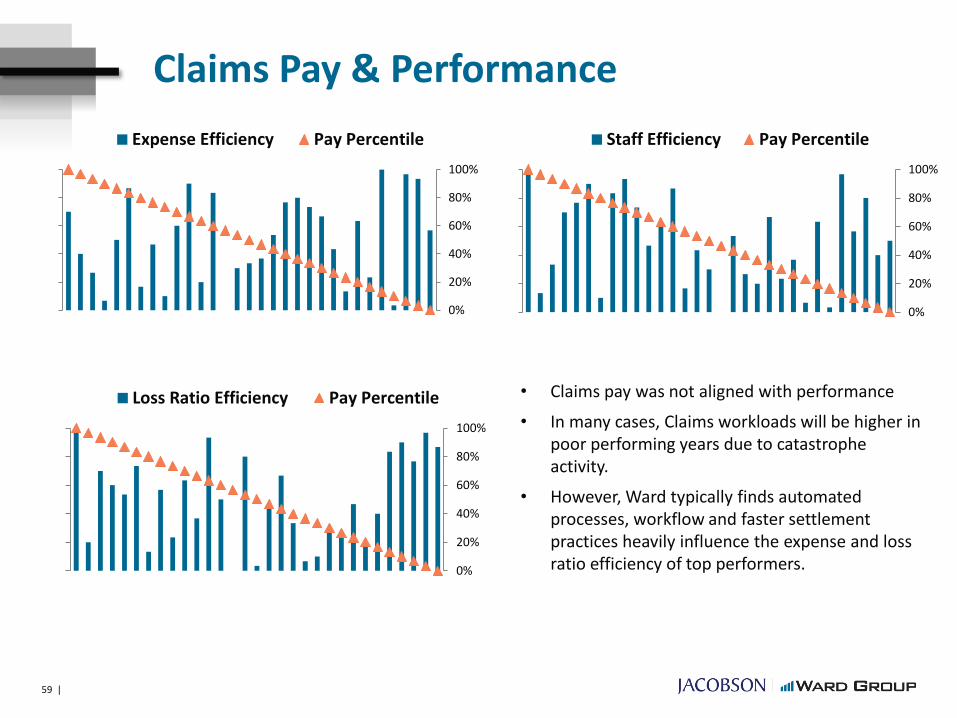

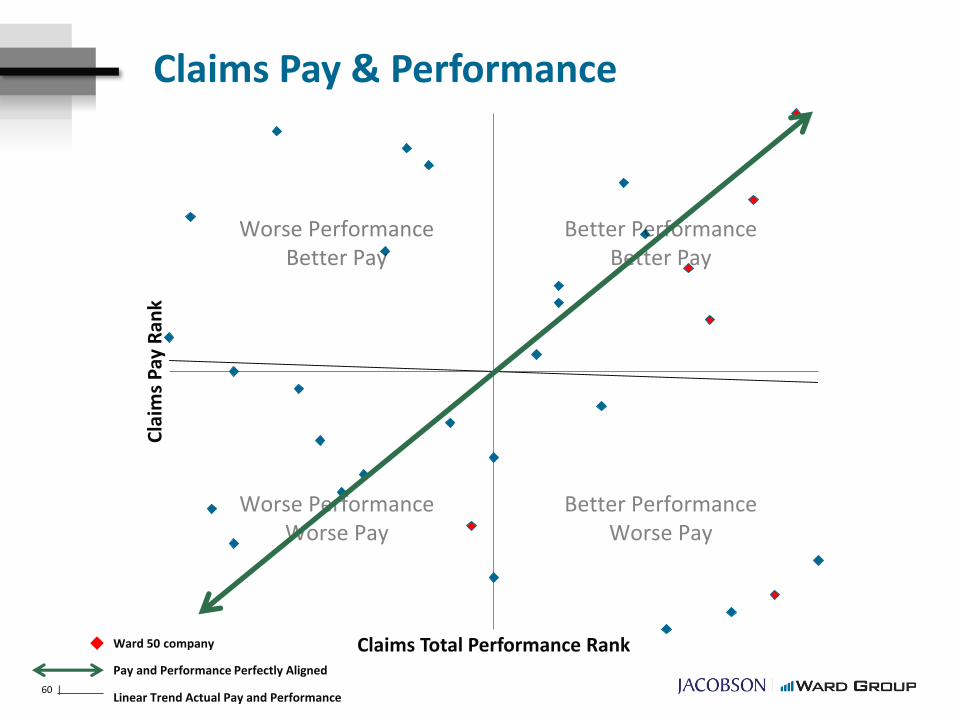

Loss Ratio Efficiency Pay Percentile • Claims pay was not aligned with performance

• In many cases, Claims workloads will be higher in poor performing years due to catastrophe activity.

• However, Ward typically finds automated processes, workflow and faster settlement practices heavily influence the expense and loss ratio efficiency of top performers.

59 |

Claims Pay & Performance

Cla

ims

Pay

Ran

k

Claims Total Performance RankWard 50 company

60 |

Pay and Performance Perfectly Aligned

Linear Trend Actual Pay and Performance

Information Technology

83 83 83 79

87

76 80

85 89 90 90 86

92

80 86

92

-

20

40

60

80

100

Overall Ward 50 Non-Ward50

Mutual Stock Small Medium Large

Information Technology Pay (000's)

Base Salary Total Compensation

3.5%

3.9%

3.3%

3.8%

3.2%

4.0%

3.4%

3.5%

0% 1% 2% 3% 4% 5%

Overall

Ward 50

Non-Ward 50

Mutual

Stock

Small

Medium

Large

Avg Base Increase

0%

20%

40%

60%

80%

100%

Overall Ward 50 Non-Ward50

Mutual Stock Small Medium Large

Information Technology Pay Distribution

Salary Short Term Incentive Long Term Incentive

6.1%

6.3%

6.1%

7.7%

4.5%

4.5%

5.3%

6.8%

0% 2% 4% 6% 8% 10%

Overall

Ward 50

Non-Ward 50

Mutual

Stock

Small

Medium

Large

Total Bonus %

61 |

Information Technology Pay & Performance

0%

20%

40%

60%

80%

100%

Expense Efficiency Pay Percentile

0%

20%

40%

60%

80%

100%

Staff Efficiency Pay Percentile

0%

20%

40%

60%

80%

100%

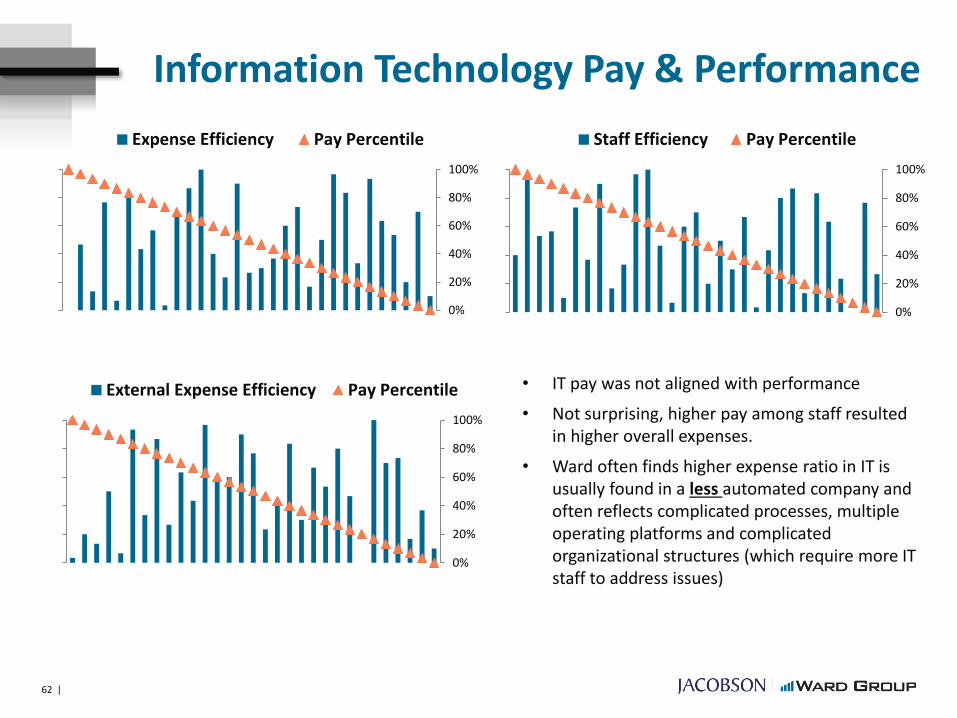

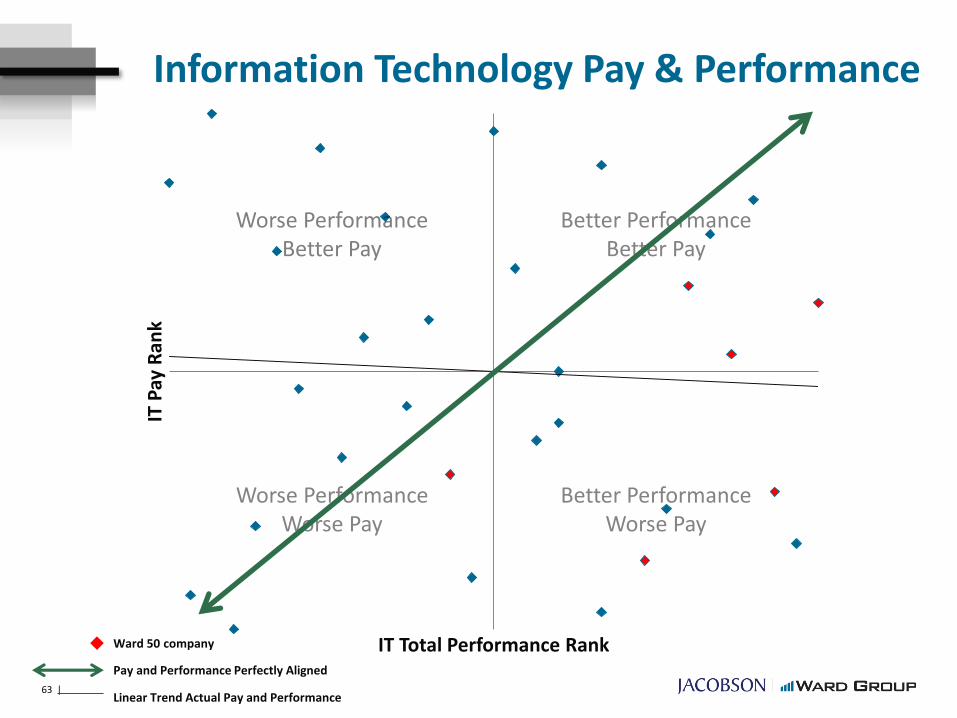

External Expense Efficiency Pay Percentile • IT pay was not aligned with performance

• Not surprising, higher pay among staff resulted in higher overall expenses.

• Ward often finds higher expense ratio in IT is usually found in a less automated company and often reflects complicated processes, multiple operating platforms and complicated organizational structures (which require more IT staff to address issues)

62 |

Information Technology Pay & Performance

IT P

ay R

ank

IT Total Performance RankWard 50 company

63 |

Pay and Performance Perfectly Aligned

Linear Trend Actual Pay and Performance

Leveraging Talent

Current Talent Trends

65 |

Sources: BLS, SunTrust

Aging Workforce

Turnover RateAnnual Quits

Workers aged 45 and older make up 48% of the industry workforce, while only 26.67% of insurance professionals are under the age of 35.

The number of insurance employees aged 55 and older is nearly 30% higher than the rest of the economy and has increased by 74% throughout the past 10 years.

Currently, 20% of the insurance workforce is approaching retirement—a number that will increase to 25% by 2018.

9

11

13

15

17

19

21

2009 2010 2011 2012 2013

Insurance U.S.

13.5%

20.4%

Talent WarUnemployment for college graduates is 3.1%. The practical unemployment rate is currently

between 1.9% and 2.5%.

Current Talent Trends

66 |

Sources: BLS, U.S. Census Bureau

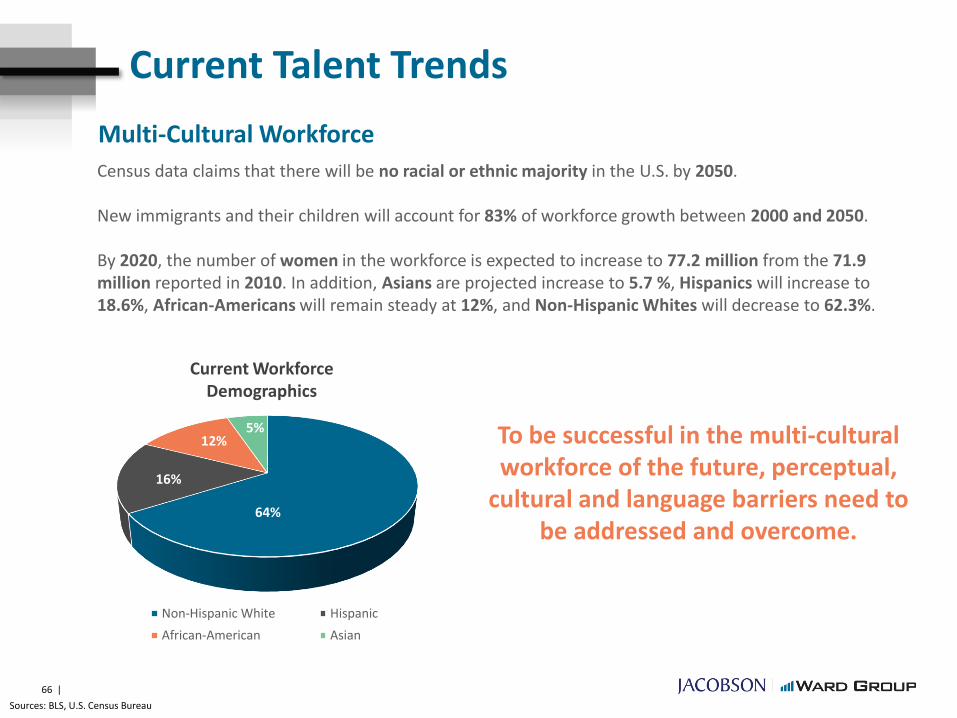

Multi-Cultural Workforce

Census data claims that there will be no racial or ethnic majority in the U.S. by 2050.

New immigrants and their children will account for 83% of workforce growth between 2000 and 2050.

By 2020, the number of women in the workforce is expected to increase to 77.2 million from the 71.9 million reported in 2010. In addition, Asians are projected increase to 5.7 %, Hispanics will increase to 18.6%, African-Americans will remain steady at 12%, and Non-Hispanic Whites will decrease to 62.3%.

Non-Hispanic White Hispanic

African-American Asian

64%

16%

5%12%

Current Workforce Demographics

To be successful in the multi-cultural workforce of the future, perceptual,

cultural and language barriers need to be addressed and overcome.

Current Talent Trends

67 |

Sources: BLS, U.S. Census Bureau, Society for Human Resource Management, Pew Research Center

Multi-Generational Workforce Workplace Generational Breakdown

Traditionalists (1900-1945) Baby Boomers (1946-1964)

Generation X (1965-1976) Millennials (1977 - 1995)

30%

28%13%

26%

Primary Millennial considerations in selecting a job are competitive salary, benefits, and work/life balance.

Unfortunately, only 5% of Millennials know what careers are available in the industry.

Organizations are balancing a generation gap of more than 50 years between the oldest and youngest employees.

Currently, 25% of HR professionals report generational conflict in their workplaces.

Looking forward, the prime labor force, aged 25-54, is expected to decline from 66.9% in 2010 to 63.7% in 2020. In contrast, workers aged 55 and older are expected to increase from 19.5% in 2010 to 25.2% in 2020.

Current Talent Trends

68 |

New Skills Required

CommunicationLost art

64%

16%

5%12%

TechnologyAdaptive to new tools

AnalyticsNot just within analytics department

Critical ThinkingDecision making and problem solving

Social Media SavvyAware of new trends

Key Leadership Qualities

69 |

Engaging

Motivates on a personal level

EmpoweringAbility to assess and lead change

Ask to step up … will step up

Key Leadership Qualities

Adaptive (not weak)

• Able to admit mistakes

• Able to change approach

• Able to approach others differently

70 |

Ability to accurately and quickly size up a situation

• Markets move fast• Buyer needs

change fast• Loyalties change

fast

Focus on succession planning

Develops People

Recruiting Talent

71 |

Selling is key!

Culture

Relationships

Financial Benefits

Opportunity

First and foremost … do they like the environment?

Millennials are social and want to work in teams.

Can they envision challenge, growth, financial rewards in the near future?

Reward = Impact

Recruiting Talent

72 |

Most efficient way to train and assess new talent

Reduce ramp up time and expense!

Current tenure in insurance is 4.9 years.

60% of Millennials will leave their employers within the first 3 years.

Internships

Sources: BLS

Talent Retention

Competitive CompensationTotal expected compensation is what counts.

Realistic incentives act as hand-cuffs.

73 |

Aligned Compensation

Must compete with stock companies

Long-Term Incentives

Talent Retention

74 |

Enterprise involvement

Continued Growth Opportunities

1. Work from home

2. Other priorities

3. Other interests

Work/Life Balance

Top Takeaways and Closing Thoughts

• The future will look much different (both in insurance and externally)

- We need to expand viewpoint

- External changes having bigger influence

• Things are generally looking good for the industry

- But operational changes are significant

- Managing change will be difficult

• Big difference between financial strength and operational efficiency

• Data, Data, DATA

- But most don’t even know how to use it

- Early adopters are likely to gain the most

• Technology is making meaningful improvements in operations

- Need to have courage to allow it to work

75 |

• Companies still struggle with managing compensation

– It is clear proper design drives results

– Mutuals trail stock companies in use of LTI

• You get what you measure

– People want to be measured

– Creates predictable behaviors

• There are ways to objectively measure almost everything

– But value is how it is communicated

– Clear line of sight is needed

– Helps eliminate emotion in decisions

• Despite the demand for technology, underwriting and claims staff, many companies are not aligning pay plans to retain key staff

76 |

Top Takeaways and Closing Thoughts

Questions and Discussion

77 |