the china money report-aug2011

TRANSCRIPT

THE CHINA MONEY REPORT

AUGUST 2011

Inside this Issue: China Macro Focus: Internationalization of the Renminbi currency Chinese Reverse merger stock market Chaos Focus on : Spreadtrum Communications

A Tiger Hill Capital Publication

August 2011 THE CHINA MONEY REPORT

A Tiger Hill Capital Publication

Welcome to the China Money Report In this issue we will discuss the internationalization of the Chinese renminbi currency and our own forward projections that it will eventually surpass the U.S. Dollar as the most import global reserve currency in the world. We will then take an overview of the Chinese stock listings in the U.S. and what has been behind the recent Chinese Reverse Merger Fraud. We have personally been shorting this space for almost two years but we are now going long on the survivors. These are real companies which have seen their stock prices decimated and the opportunity now presents itself to swoop in and pick up the real companies which rock bottom prices. Many of these stocks have P/E multiples less than 10 so today provides a great opportunity to pick up beaten down stocks. Lastly , we will review this months stock recommendation, Spreadtrum Communications.

Internationalization of the RENMINBI The global U.S. Dollar standard that the world has lived under since World War 2 is collapsing all around us. At the time of this writing it appears inevitable that at sometime in the near future the USD will lose it’s AAA standard. Once the gold plated AAA standard has been breached it can lead quickly down to further downgrades. We may never again see a AAA rated American in our lifetime. Many people including ourselves believe the USD in reality has not been AAA for many years as the American entitlement society along with massive government deficits have continued to grow. The world is now searching for a new store of value and a new currency in which to transact business and conduct trade. We believe the world will look increasingly to China as it is now the world’s second largest economy, the world’s largest exporter, and the world’s largest creditor nation. The gravitational pull of China on the global economy is immense and growing. Pay close attention to this extract from HSBC Bank in a research report titled “Rise of the Redback”. I was recently in Hong Kong and I was amazed at the push in Hong Kong for the RMB deposit business. There are now 80 banks in Hong Kong dealing with RMB deposits. In Hong Kong you see double decker business and taxi cabs all advertising RMB deposit business for Hong Kong banks. The number of RMB deposits in Hong Kong has grown from only 60 billion RMB in 2009 to over 1 trillion RMB in 2011. Hong Kong is the spearhead in Beijing’s plan to take the renminbi international. This will be a three step process. Which are as follows: Step 1 is to make the RMB a global trade settlement currency Step 2 is to make the RMB an international investment/debt currency Step 3 is to make the RMB an international reserve currency.

(2)

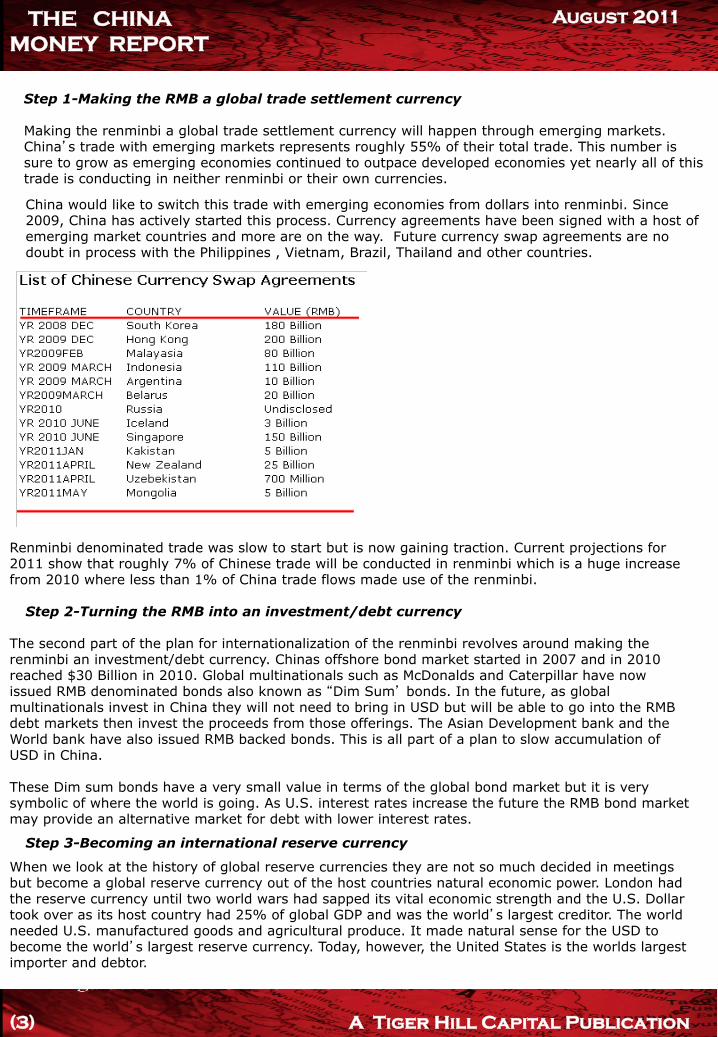

China would like to switch this trade with emerging economies from dollars into renminbi. Since 2009, China has actively started this process. Currency agreements have been signed with a host of emerging market countries and more are on the way. Future currency swap agreements are no doubt in process with the Philippines , Vietnam, Brazil, Thailand and other countries.

THE CHINA MONEY REPORT

August 2011

A Tiger Hill Capital Publication (3)

Renminbi denominated trade was slow to start but is now gaining traction. Current projections for 2011 show that roughly 7% of Chinese trade will be conducted in renminbi which is a huge increase from 2010 where less than 1% of China trade flows made use of the renminbi.

Step 2-Turning the RMB into an investment/debt currency

Step 1-Making the RMB a global trade settlement currency Making the renminbi a global trade settlement currency will happen through emerging markets. China’s trade with emerging markets represents roughly 55% of their total trade. This number is sure to grow as emerging economies continued to outpace developed economies yet nearly all of this trade is conducting in neither renminbi or their own currencies.

The second part of the plan for internationalization of the renminbi revolves around making the renminbi an investment/debt currency. Chinas offshore bond market started in 2007 and in 2010 reached $30 Billion in 2010. Global multinationals such as McDonalds and Caterpillar have now issued RMB denominated bonds also known as “Dim Sum’ bonds. In the future, as global multinationals invest in China they will not need to bring in USD but will be able to go into the RMB debt markets then invest the proceeds from those offerings. The Asian Development bank and the World bank have also issued RMB backed bonds. This is all part of a plan to slow accumulation of USD in China. These Dim sum bonds have a very small value in terms of the global bond market but it is very symbolic of where the world is going. As U.S. interest rates increase the future the RMB bond market may provide an alternative market for debt with lower interest rates.

Step 3-Becoming an international reserve currency

When we look at the history of global reserve currencies they are not so much decided in meetings but become a global reserve currency out of the host countries natural economic power. London had the reserve currency until two world wars had sapped its vital economic strength and the U.S. Dollar took over as its host country had 25% of global GDP and was the world’s largest creditor. The world needed U.S. manufactured goods and agricultural produce. It made natural sense for the USD to become the world’s largest reserve currency. Today, however, the United States is the worlds largest importer and debtor.

(4) A Tiger Hill Capital Publication

The United States is increasingly unable to pay for their imports with massive government and current account deficits. In the normal course of things it may have taken China twenty years to replace the USD as the host of the world’s reserve currency but since the economic crisis and the U.S. reaction to it which is currency debasement may speed the world to moving quicker to a RMB standard. Central Banks around the world are ordering RMB as a reserve currency and China is now encouraging this to take place.

Does Beijing want a world’s reserve currency? Clearly the current status of the renminbi is far underrepresented considering the economic might of China. Indeed the leadership in Beijing now realizes the renminbi is the only currency in the top twenty economies to not be convertible. This is a shame and a loss of face that Beijing intends to correct as soon as possible. There is now open talk in Beijing of the “dollar trap” and a growing consensus in Beijing that they have fallen into the dollar trap by not have a convertible currency. This has led to over $3 Trillion in foreign currency reserves which are being devalued day by day. Watch for this issue to become increasingly political as normal people struggling day to day ask why they have to loan Americans so much money. In summary, as China overtakes the United States as the world’s largest economy it makes complete sense that that worlds largest economy, largest trading nation, and the worlds largest creditor nation (as opposed to the worlds largest debtor nation) would have the most important world reserve currency. In fact, one day we might see the Chinese renminbi replace the U.S Dollar as the defacto AAA standard.

THE CHINA MONEY REPORT

August 2011

Chinese Reverse Merger Chaos At the time of this writing, Chinese stocks listed in the U.S. have been decimated. Their have been many high profile Chinese companies listed in the U.S. that have been reporting fraudulent information. We have personally been short this space for almost 2 years. The China money report recommends not buying any China based companies listed in the U.S. unless you see them recommended here. Fraud and corruption are rife in China and many U.S. retail investors have been taking for a ride. Chinese companies have sold a bill of goods to U.S. based investors. The story usually involves “China + something else”. For example, “China + environmental clean up or “China + raw materials”. These “fraud-caps” have listed in the U.S. as it is there that investors are the most naive and regulations are lax. These companies would not dare try this in mainland China or even Hong Kong. Most of these companies are reverse merger companies or so called “reverse take-over” companies. The good news is, with good due diligence work in China you can find the winners and now pick up the real companies at a substantial discount. We will be profiling some of these companies in upcoming editions of the China Money Report. What is a Chinese Reverse Merger? A Chinese reverse merger is when a Chinese company buys a shell company in the U.S. that is publicly traded. It changes the company name in the U.S. then has access to the U.S. capital market and seeks fresh capital in the U.S. with the assistance of U.S. firms. These types of listings can be done in as little as 3 months and for well under $1 million in fees. This is an RTO or Reverse Take-over. At it’s peak, the Chinese reverse merger market consisted of over 300 companies with a total market cap of $30 Billion USD.

The exposure of the Chinese reverse merger market started with independent short sellers. One prominent example was a man in Texas named John Bird. He had been tracking a China stock called China Sky One Medical, a manufacturer of medical products. They had listed inventory turns of 7 days which seemed impossible to Bird. (Bird himself was a retired inventory manager) As the stock continued to climb, he was able to find an interlocking web of companies and was able to obtain credit reports from the SAIC (Chinese agency responsible for market supervision, regulation, and enforcement) and was to discover the Sky one had most likely overstated their revenues by a factor of 90 to 1. As allegations of fraud continued into the market, not many people were paying attention. then along came a small firm named Muddy Waters. Muddy Waters is a short seller started by someone with real China experience and has lived in China. He saw the opportunity to short sell these companies and publish research on them. Muddy Waters was able to put the boots on the ground and come up with clear evidence that the companies it targeted were involved in clear cases of overstating their businesses. Muddy Waters first gained prominence last June with a report against Orient Paper Inc (ONP.A), which it called a "fraud" that had overstated its 2009 revenue by about 40 times. Muddy then targeted several other companies including Duoyuan Global Water, RINO, and China Media Express and their influence grew with every successful report. Duoyuan Global Water Inc (DGW.N) slumped 29.3 percent from its close before the April 4 report until April 19, when its shares were halted. They have not traded since. RINO International (RINO.PK) plummeted 96.5 percent, from $15.52 before the report to 55 cents currently, China MediaExpress Holdings (CCME.PK) is down 91.8 percent to $1.28. Both stocks were delisted by the Nasdaq following the charges and currently trade on the pink sheets However, what will most likely become the most famous case of Chinese Reverse Merger Fraud is the recently targeted Sino Forest. It will become famous because who was associated in losing money with the stock. None other than Sub-prime King John Paulson had to close out a position in Sino Forest with a $468 million dollar loss.

THE CHINA MONEY REPORT

August 2011

John Paulson. King of Sub-prime CDS. Burned for $468 million USD loss on Sino-Forest.

The Chinese Reverse Merger Market has since exploded . How many of these companies are frauds? The China Money report is tracking over 90 Chinese RTO companies. The majority have P/E ratios which suggest that the market believes many if not most of these stocks have been providing fraudulent information. Of the 90 Companies we are is tracking, 51 of them have a P/E ratio less than 6 and 32 companies have a PE ratio less than 32. This type of fraud for the most part involves overstating revenues, customer relationships that do not exist, double counting revenues between subsidiaries and parent companies, etc

A Tiger Hill Capital Publication (5)

THE CHINA MONEY REPORT

August 2011

(6) A Tiger Hill Capital Publication

Summary of the chinese reverse merger space . The Chinese reverse merger space has been an absolute train wreck. The opportunity to short these stocks has mostly run its course as most companies have lost between 50-90% of their value.

Why is the fraud happening? There are much more strict penalties for these companies to commit fraud in China. They are not actually committing fraud in China as they are following the rules and have submitted correct documentation to the SAIC. It is the U.S. market where they are overstating their sales and earnings.

In addition, Hong Kong regulators know to look more closely for business fraud than do U.S. regulators and hence these companies have gravitated to the small cap market in the States. U.S. based auditors are checking the books to make sure they align between the U.S. and China. They are set up to find accounting fraud, not business fraud.

In this months issue we will not be profiling any of these reverse merger companies. The first stock we will bring you in Spreadtrum communications which went through a standard IPO process in the U.S. stock market.

SPREADTRUM COMMUNICATIONS (NASDAQ: SPRD)

Founded in 2001 with operations in the U.S., Spreadtrum is a Caymen’s based holding company. They are for the most part operationally based in Shanghai. They are listed on Nasdaq. (Nasdaq: SPRD)

A leading fabless semiconductor company that designs, develops and markets baseband processor And RF transceiver for the wireless communications and mobile television market. They combine semiconductor design expertise in parallel with software development capabilities to deliver highly integrated baseband processors with rich multimedia functionality and power management. Product solutions based proprietary as well as an open development platform, enabling their customers to develop customized wireless products that are feature-rich and meet their cost and time-to-market requirements. Products: Core chipsets for 2G/3G/3.5G mobile phones Radio frequency (RF) transceivers for 2G/3G/3.5G mobile phones Mocor software platform Total wireless solution for 2G/3G/3.5G Digital audio/video decoder chipsets for AVS/MEGE2/H.264 applications Chipset and solution supporting MBBMS for CMMB-Based Mobile TV Customers: Samsung, Huawei, Local P.R.C hand set makers Competitors: MediaTek, IMC, ST-Ericsson, MStar, Broadcom MediaTek (2454.TW) had approximately 90% of the mainland China mobile handset chip market in 2009. Mobile handset chips are by far its largest revenue source – currently accounting for more than 70% of revenue.3 Estimates now place MediaTek’s mainland market share at only 70%, with SPRD at 20% (an increase of about 15 percentage points). The latest sales data shows Spreadtrum continuing to grow at the expense of Media Tek.

Revenue in Spreadtrum increased to $346.3 million in 2010. 2011 revenue in Q1 is up 163% from the previous year. To date, most revenue has been derived from the sale of products that support 2G and 2.5G wireless standards such as GSM and GPRS although revenue from 3G products is increasing as China expands its 3G product offerings and services.

THE CHINA MONEY REPORT

August 2011

A Tiger Hill Capital Publication (7)

NOTES OWNERSHIP As of February 28, 2011, directors, executive officers, principal shareholders and their affiliated entities owned approximately 44.6% of our outstanding ordinary shares.

In May 201, Silver Lake has made its first investment in a Chinese company, taking a 13% minority stake. Dr Eric Chen, managing director at Silver Lake, said, “We believe Spreadtrum will be a key enabler of China’s home-grown 3G national wireless standard, representing the power of technological innovation in the Chinese economy.” The deal valued the company at $2.75bn, with Silver Lake.

As a fabless semiconductor company, Spreadtrum does not own or operate wafer fabrication or assembly and testing facilities. Instead they develop proprietary designs and provide them to third-party foundries to produce silicon wafers for our semiconductors. By utilizing third-party foundries to produce silicon wafers for our semiconductors and outsourcing our assembly and testing requirements, we are able to focus more of our resources on product design and software development, and eliminate the high cost of building and operating advanced semiconductor fabrication, assembly and testing facilities. All of our current semiconductors are developed and manufactured with 0.18-micron, 0.152-micron, and 40-nanometer CMOS process technologies. We have outsourced all of our wafer production to foundries, most of which has been outsourced to TSMC, the world’s largest foundry and our primary foundry service provider since its inception.

NOTES ON BUSINESS MODEL

Currently rely on Taiwan Semiconductor Manufacturing Company Limited, or TSMC, to manufacture most of our semiconductor products. Significant risks with this business model are a lack of manufacturing capacity, limited control over delivery schedules, quality assurance and control, manufacturing yields and production costs; and the unavailability of, or potential delays in obtaining access to, key process technologies.

RISKS ON BUSINESS MODEL

The worldwide foundry capacity for 8-inch wafers, which are required by most Spreadtrum products, was heavily overbooked in 2010 and is not expected to increase in 2011 as foundries mostly invest capital in leading-edge 12-inch wafer technologies. The assembly and testing service providers are experiencing rising commodity prices such as gold, which is one of the most important input components on packaging assembly. This business model is similar to Qualcomm in the United States. They key advantage is lack of CAPEX spending on fixed assets and overcapacity in economic downturns.

KEY SUPPORTERS OF SPREADTRUM General Secretary of the Central Committee of the CPC (Communist Party of China), Chinese President and Chairman of Central Military Commission, Jintao Hu paid an inspection visit to Spreadtrum

Board of Directors has authorized a share repurchase program under which the Company may repurchase up to US$100 million of its American Depositary Shares ("ADSs") pursuant to a Rule 10b5-1 repurchase plan. The share repurchase program will be funded with the Company's cash on hand. Members of the Company's management team also intend to purchase the Company's outstanding shares through the open market.

SHARE REPURCHASE- 18JUNE2011

Allegations of Fraud from Muddy Waters: This is an important section and where we make our money. On 28June2011, Muddy Waters who had been so successful previously in identifying Chinese fraud caps issued and open letter to Spreadtrum and announced they were going short the stock. In my opinion, they must have been working with some large funds to drive down the stock before the announcement as the stock had seen unprecedented selling before these open questions from Muddy Waters. On clear examination of these questions however, it was clear this was a real weak case presented by Muddy Waters. In previous cases against Chinese companies they provided pictures of plants and equipment, Chinese tax documents, etc. In the case of Spreadtrum they provided only a few questions. It made no sense to attack a company like Spreadtrum when their were so many more easier targets to attack. Was the attack an attempt to drive down the stock to go to the long side? The stock was down 33% right after the report but rebounded to a loss of only 4% on the day. It then rose another 20% in the following weeks. Spreadtrum took a defense by easily answering their questions the next day. One month later, Muddy Waters has not commented on the case. Spreadtrum has also instituted a share buy-back and dividend policy. I will not bore you with all of the questions and responses from Spreadtrum but I will post an example of a typical question from Muddy Waters and how it was answered by Spreadtrum to give you a fell of the situation. “Questions” from Muddy Waters: (Q1) SPRD’s lack of any cash income tax payment in 2010 is inconsistent with prior years as well as the PRC’s provisional tax payment requirements. The table below shows SPRD’s pre-tax income, income tax provisions, and cash taxes paid for 2008 – 2010 (A1) In 2010, Spreadtrum had a low tax position due to financial loss carryover from previous years With permission of the Chinese government, Spreadtrum made payment of 2010 corporate income tax of approx. $5M on May 27, 2011, which is before the annual tax filing deadline, and with no interest or penalty.

THE CHINA MONEY REPORT

August 2011

SUMMARY: High Tech profitable Chinese company with explicit and implicit backing by the Chinese government. 163% growth rate year over year yet trading at a low PE of just over 8 times earnings. Major insider buying and share repurchase program. We suggest starting long positions for the long term on SPRD.

Next months issue: We will be covering 2 new stocks in the next issue of the China report as well as our usual China macro report. If you are not a subscriber we invite you to join today at www.thechinamoneyreport.com GOOD HUNTING Daniel Collins Editor, The China Money Report

A Tiger Hill Capital Publication (8)

THE CHINA MONEY REPORT

A Tiger Hill Capital Publication

August 2011

(9)

A Tiger Hill Capital Publication (10)

THE CHINA MONEY REPORT

August 2011

THE CHINA MONEY REPORT

August 2011

A Tiger Hill Capital Publication (11)

SHANGHAI 1990

SHANGHAI 2010

PIC OF THE MONTH

DISCLAIMER It should not be assumed that the methods, techniques, or indicators presented in these pages will be profitable or that they will not result in losses. Past results are not necessarily indicative of future results. Examples presented on these pages are for educational purposes only. These set-ups are not solicitations of any order to buy or sell. The authors, the publisher, and all affiliates assume no responsibility for your trading results. There is a high degree of risk in trading. Hypothetical performance results have many inherent limitations, some of which are described below. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. In fact, there are frequently sharp differences between hypothetical performance results and the actual results subsequently achieved by any trading program. One of the limitations of hypothetical performance results is that they are generally prepared with the benefit of hindsight. In addition, hypothetical trading does not involve financial risk of actual trading. For example, the ability to withstand losses or to adhere to a particular trading program in spite of trading losses are material points which can also adversely affect trading results. There are numerous other factors related to the markets in general or to the implementation of any specific trading program which cannot be fully accounted for in the preparation of hypothetical performance results and all which can adversely affect actual trading results. This report is not intended for American investors or American firms.

THE CHINA MONEY REPORT

August 2011

THE CHINA MONEY REPORT

The China Money Report Horizon Towers 21-203 Xinghan Street #188 Suzhou Industrial Park Jiangsu, P.R.C Tel: 86.0512.62768645 [email protected]

Tiger Hill Capital #604, Tower A, New Trade Plaza, 6 On Ping St. Shatin, N.T. Hong Kong

www.thechinamoneyreport.com