the competitive strength of the danish milk production from a global and eu perspective

TRANSCRIPT

EDF Congress 2006, Denmark

The competitive strength ofthe Danish milk production

from a Global and EU perspective

Preben MikkelsenDanish Cattle Federation

EDF Congress 2006, Denmark

1. Danish Cattle Federation2. The Global milk production structure3. The political framework in EU4. The future of milk quota in EU5. Future challenges and possibilities6. Competitive strength of Danish milk

production7. Concluding remarks

EDF Congress 2006, Denmark

1. Danish Cattle Federation

EDF Congress 2006, Denmark

The Danish Cattle Federation

The Danish Cattle Federation is a unifyingbody working to improve specific conditions ofcattle farming and being the spokesman ofcattle farmersand we work to

Ensure the best possible earnings for cattle farmers

Optimise the industry by a plough to plate approach and viewing the industry as a whole

Organise service, advising and control assignments

EDF Congress 2006, Denmark

The Danish Cattle Federation – stands on three legs

• Cattle and industrial policy• Primary production and advising• Veterinary conditions and primary

product quality

EDF Congress 2006, Denmark

Danish Cattle Federation

Danish Cattle Federation is formed by:

Danish Agriculture (the national farmers’ organisation)

A.I. Centre Dansire

Danish Dairy Board

Danish Meat Board

Objective: Being the most competitive European cattleindustry as regards economy, sustainability and quality

EDF Congress 2006, Denmark

2. The Global milk productionstructure

EDF Congress 2006, Denmark

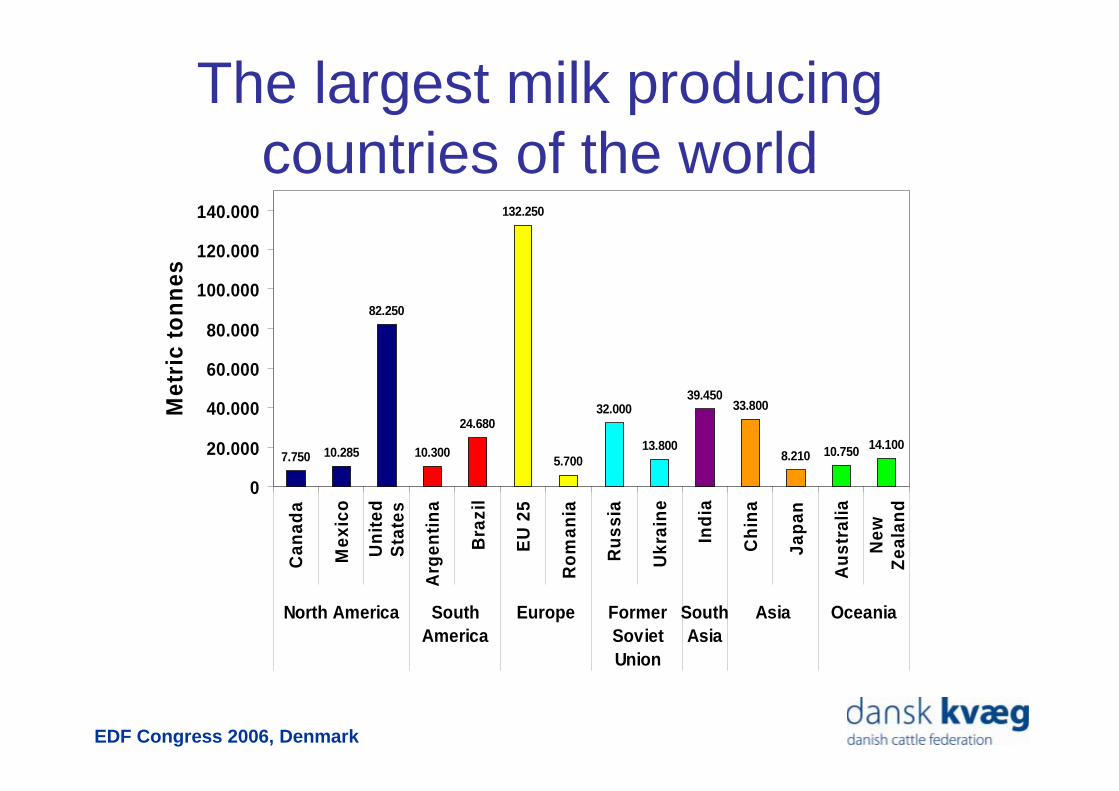

The largest milk producing countries of the world

7.750 10.285

82.250

10.300

24.680

132.250

5.700

32.000

13.800

39.45033.800

8.210 10.750 14.100

0

20.000

40.000

60.000

80.000

100.000

120.000

140.000

Can

ada

Mex

ico

Un

ited

Sta

tes

Arg

enti

na

Bra

zil

EU

25

Ro

man

ia

Ru

ssia

Ukr

ain

e

Ind

ia

Ch

ina

Jap

an

Au

stra

lia

New

Zea

lan

d

North America SouthAmerica

Europe FormerSovietUnion

SouthAsia

Asia Oceania

Met

ric

ton

nes

EDF Congress 2006, Denmark

The biggest players on the world market

EU is loosing market shares to Oceania!

Others17%

Australia10%

New Zealand

33%

Argentina3%

EU35%

USA2%

Australia7%

New Zealand

23%

Others24%

EU40%

USA6%

1990 2004

EDF Congress 2006, Denmark

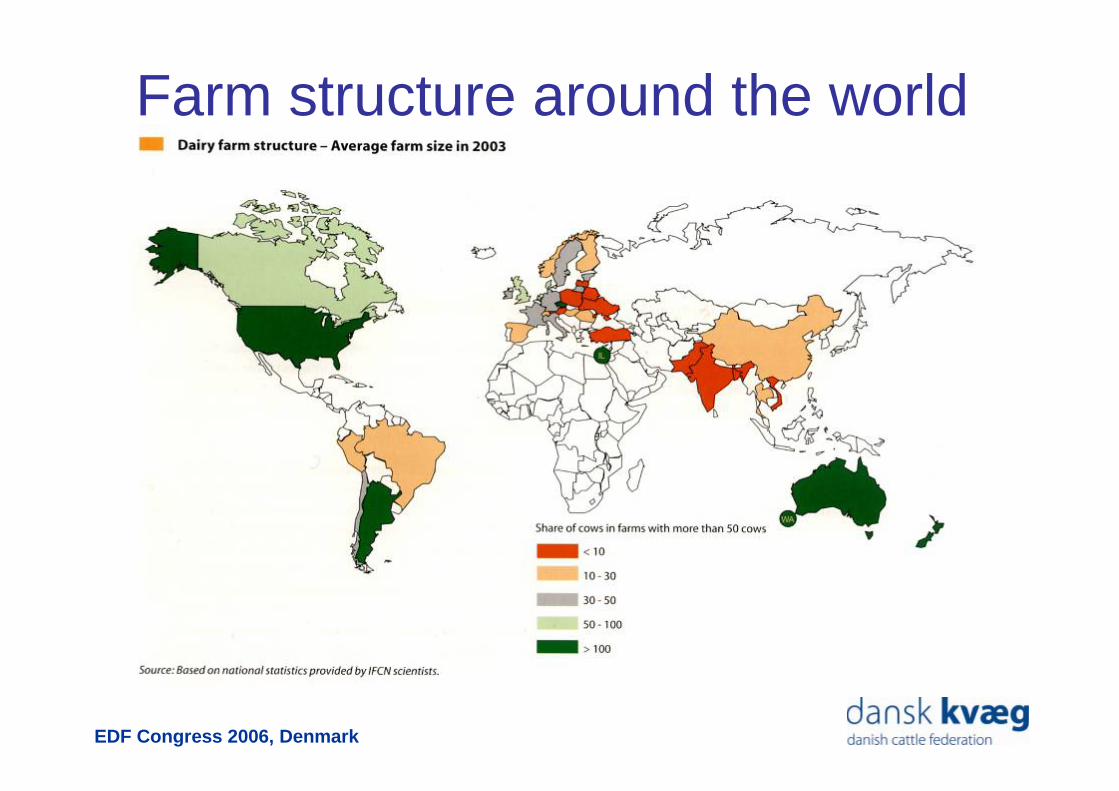

Farm structure around the world

EDF Congress 2006, Denmark

Milk price around the world (2004)

Source: IFCN Dairy Report 2005, national statistics, estimations

30-40> 40

20-25< 20

Milk price in US-$ / 100 kg milk

25-30

32

22

EDF Congress 2006, Denmark

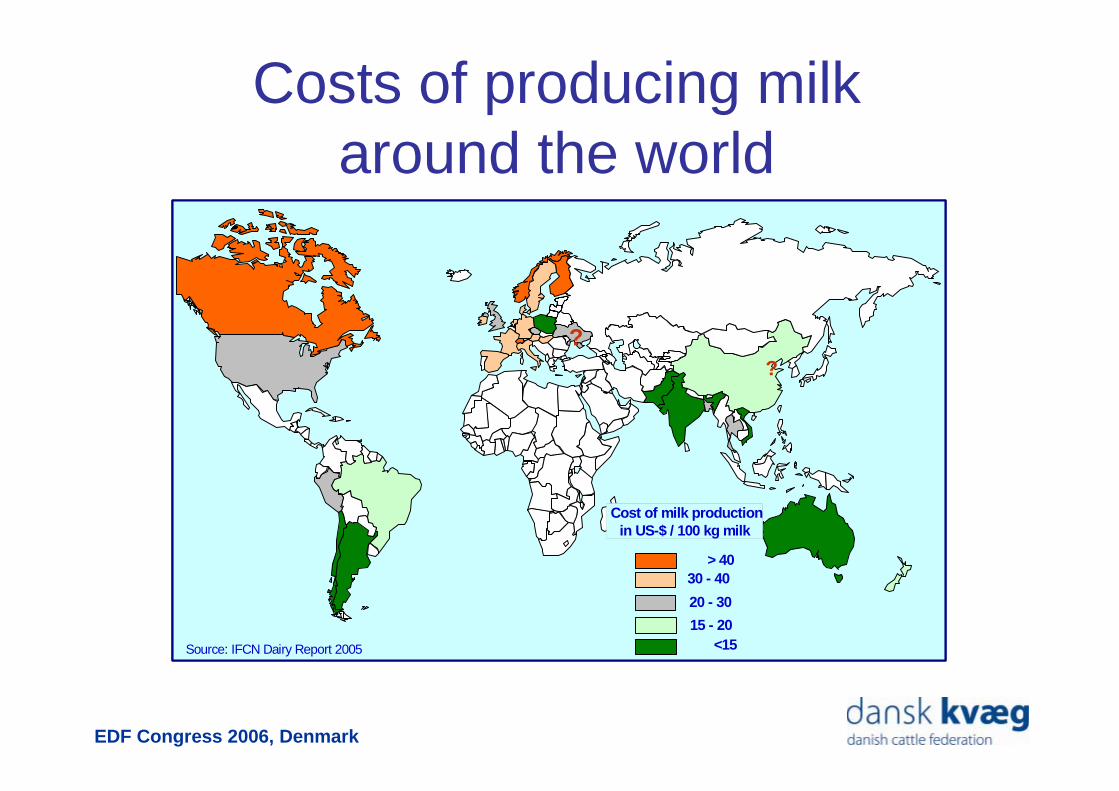

Costs of producing milk around the world

30 - 40> 40

15 - 20<15

20 - 30

Cost of milk productionin US-$ / 100 kg milk

Source: IFCN Dairy Report 2005

??

30 - 40> 40

15 - 20<15

20 - 30

Cost of milk productionin US-$ / 100 kg milk

Source: IFCN Dairy Report 2005

??

EDF Congress 2006, Denmark

Reasons for differences in costs of production

New Zealand

DenmarkBrazil

19,0002,9751,6302,70010,963Land price per ha, $

2010-121,52-310Labor costs per hour, $

5,0004,500*700-800500-6002,800Capital input per cow, $

8,8009,1001,2004,1003,700Milk yield per cow, kg

10010514139291Average herd size, number of cows

DenmarkUSABrazilArgentinaNZ

Argentina USA

* 145 cow farm in Wisconsin. Large farm i.e. >700 cows: 2,500$

Source: IFCN Dairy report 2005

EDF Congress 2006, Denmark

3. The political framework in EU

EDF Congress 2006, Denmark

Reform of the milk policy

Quotas: Extension of the quota system until 2014/153 x 0.5% quota increase in Denmark from 2006/07-2008/09

Prices:Reduction of the intervention price

– butter: 3x7% in 2004, ’05 and ’06 + 4% in 2007– SMP: 3x5% in 2004-2006

Intervention ceiling of 70,000 t for butter in 2004/05 dropping to 30,000 t in 2008/09

Compensation:Partial compensation for the reduction of intervention pricesDecoupling in Denmark in 2005

05.08.2003

EDF Congress 2006, Denmark

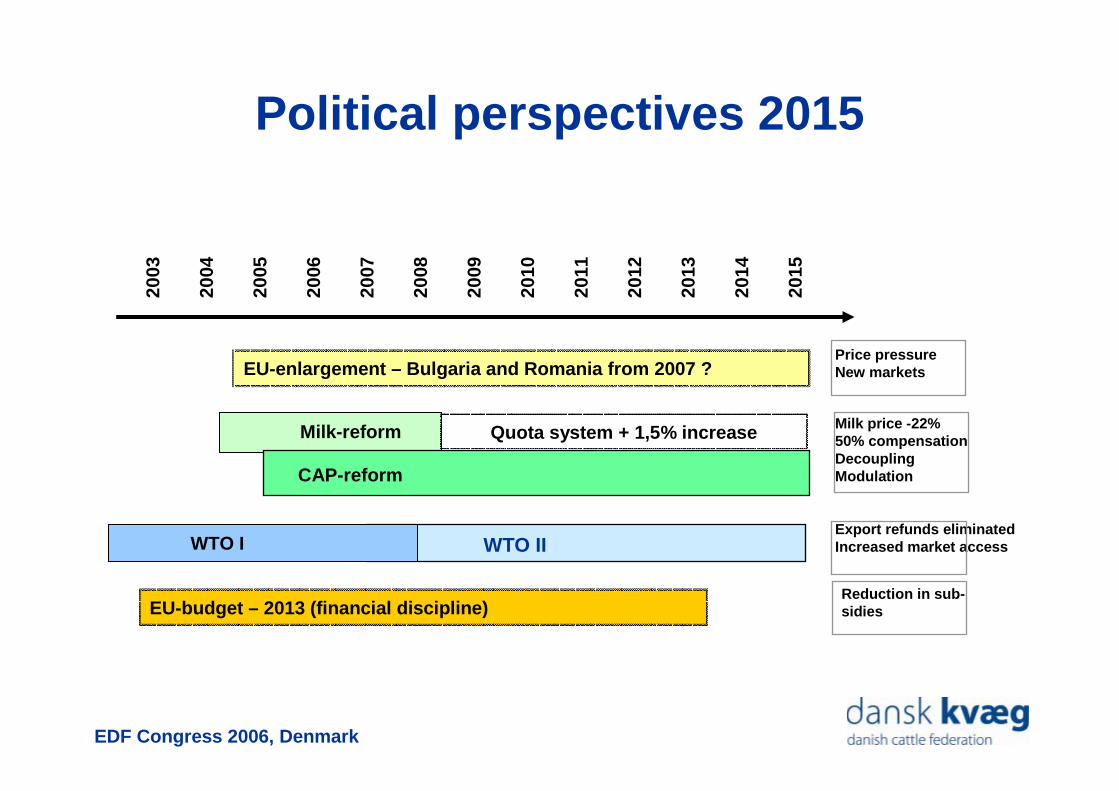

WTO II

Price pressureNew markets

Milk price -22%50% compensationDecouplingModulation

Export refunds eliminatedIncreased market access

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

WTO I

Milk-reform

Political perspectives 2015

EU-enlargement – Bulgaria and Romania from 2007 ?

CAP-reform

EU-budget – 2013 (financial discipline)Reduction in sub-sidies

Quota system + 1,5% increase

EDF Congress 2006, Denmark

4. The future of milk quotas in EU

EDF Congress 2006, Denmark

Market balance in EU28To ensure the good balance

60

70

80

90

100

110

120

130

140

150

160

1998

2000

2002

2004

2006

2008

2010

2012

2014

Mio

. to

ns

60

70

80

90

100

110

120

130

140

150

160

Mio

. to

ns

Exports

Sales EU

Milk deliveries + imports

Milk deliveries

Prognosis 2006-2015:

- Consumption in EU: +1% p.a.

- Quota: +0,5% p.a.*

- Imports: 2.5% of comsumption p.a. in 2006/07 rising to 5% p.a. in 2012-2015

- Exports: 13.5 mio. tons p.a. falling to 10 mio. tons in 2013-2015

* Quota increase not included for B, F, GR, LUX, AUST, FIN, SW and U.K.

EDF Congress 2006, Denmark

The market and the quota

The expected market development leaves room for a gradual, annualquotaenlargement of 0.5-1% with a continued market balance – should beevaluated on an annual basis dependent on the development.

Impact:• Preparation for termination of the quota system• Gives certain possibilities for competitive countries• It is expected that Denmark will utilize the quota increase –an increase will have a minor, calming impact on the quota

price• Countries not utilizing the quota, will have no negative impact

EDF Congress 2006, Denmark

Future of the quota system

Several countries discuss termination of the quota system

It ”simply” calls for a blocking minority (90 seats) to terminate

quotas (Sweden, Denmark, U.K., Italy and Poland)

Requirements up to 2015:

• flexibility

• gradual phasing out / gradual increase of quota

• clear signal in due time

EDF Congress 2006, Denmark

Is it realistic to give up milk quotas?

YES! If the Council of Ministers does not decide otherwise, the milk quota system will be abolished by 2015. An extension requires the EU Commission to put forward a proposal.

A blocking minority may secure that the present quota system is not extended.

90 votes out of 321 form a blocking minority: I.e. Great Britain, Italy, Poland, and Denmark may together block a proposal.

EDF Congress 2006, Denmark

5. Future challenges and possibilities

EDF Congress 2006, Denmark

Challenges and countermovesThe challenges

– Lower milk price– Less economic support– Stricter environmental

regulations– More focus on animal welfare

The countermove of the dairy farmer– Cost minimization– Increase in farm size– Exploitation of new

technological advances and new knowledge

– Focus on strategy, leadership and management

EDF Congress 2006, Denmark

New knowledge and new technologyBetter machinery

Better milking systems

Better housing facilities

Better feeding equipment

EDF Congress 2006, Denmark

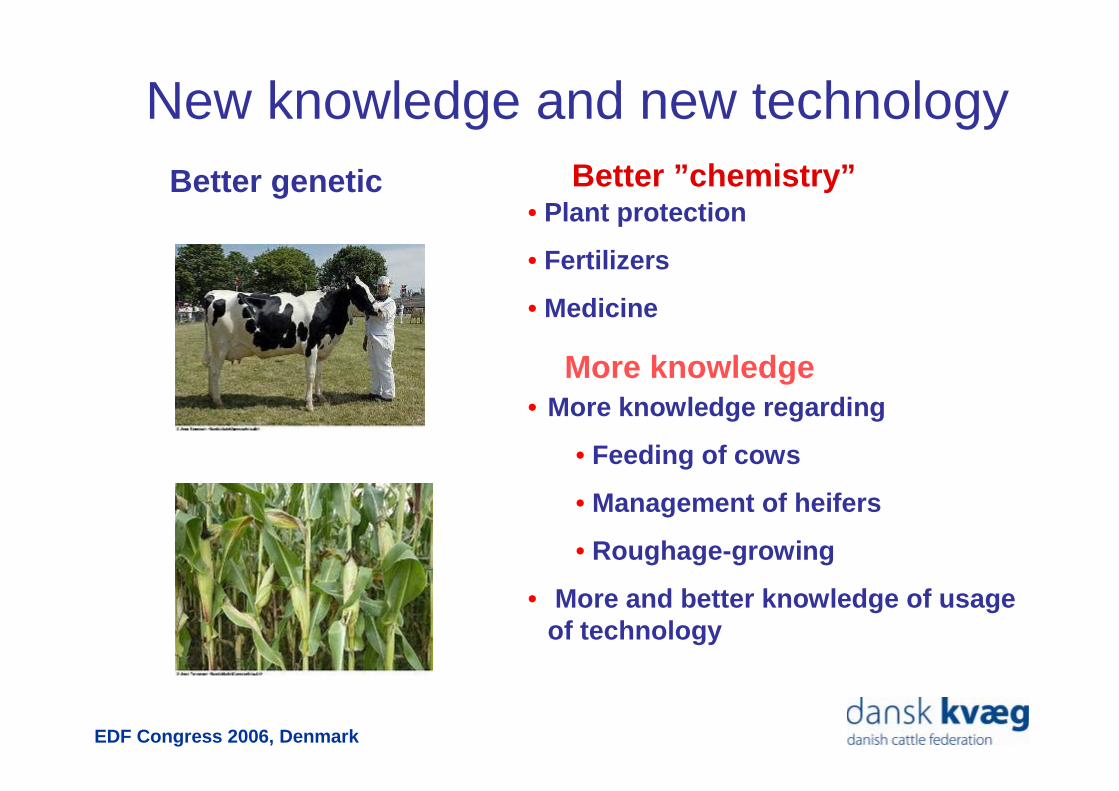

New knowledge and new technologyBetter genetic

• Plant protection

• Fertilizers

• Medicine

Better ”chemistry”

• More knowledge regarding

• Feeding of cows

• Management of heifers

• Roughage-growing

• More and better knowledge of usage of technology

More knowledge

EDF Congress 2006, Denmark

Technology will monitor the herdHealth and reproduction Feed uptake

Health and reproduction

The registrations are converted into useful information

EDF Congress 2006, Denmark

The role of the farmer is changing

From • Doing all the farm work

– Milking– Feeding– Field work– Monitoring the herd

To• Strategy formulation• Management of

production and economy• Management of labor• “Management” of

consultants• Monitoring the herd by use

of technology

Manager and leaderTo

Skilled craftsman

From

EDF Congress 2006, Denmark

Trends for the coming yearsregarding ownership

The family farm

From To

The family farm

The limited company

Thenetwork

Cr.

S

C

EDF Congress 2006, Denmark

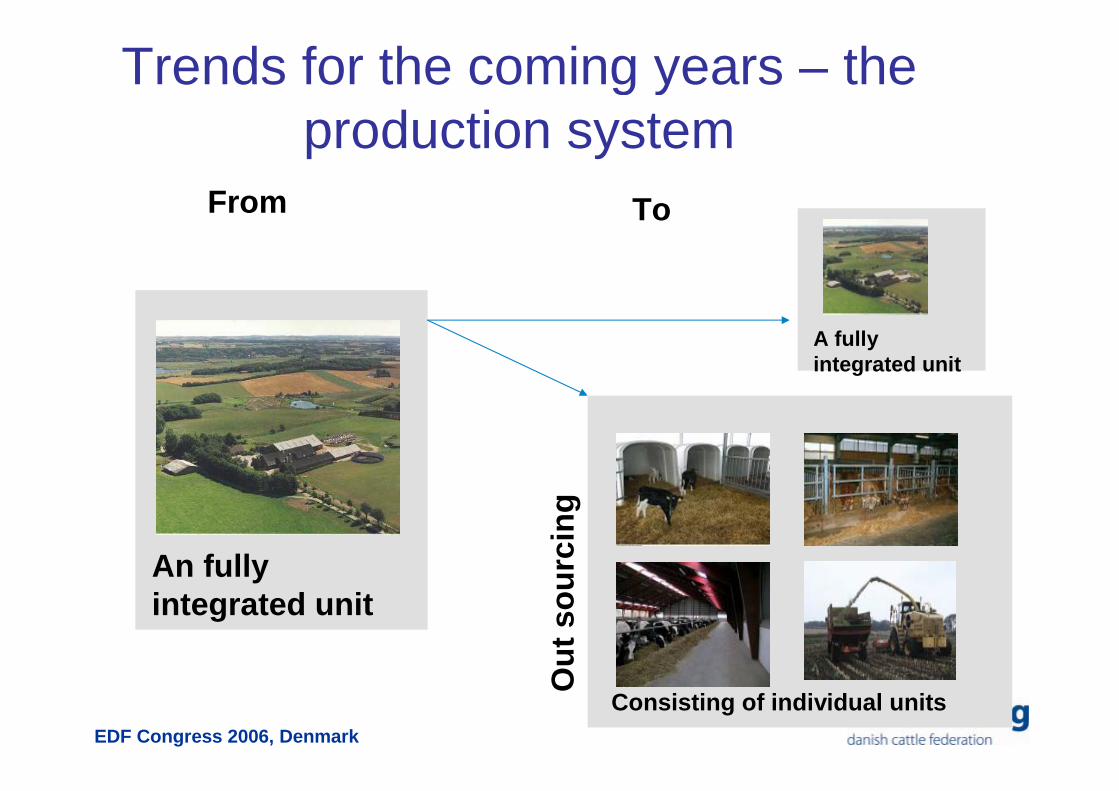

Trends for the coming years – the production system

From

An fully integrated unit

To

A fully integrated unit

Consisting of individual units

Ou

t so

urc

ing

EDF Congress 2006, Denmark

The role of the advisor is changing

The traditional role• Specialist on specific subjects

such as: Feeding, animal health, economy etc.

• Treatment of sick animals• The recipient of the advice is the

dairy farmer• Little communication between

the different advisors• Little focus on the farm as a

whole• Knowledge and advisory tools

are very

The new role• Technology takes over much of the

registration on the farm• Due to technology diseases can be

identified at an earlier stage• Prevention of diseases• Specialist and discussion partner • The recipient of the advice could

be several people on the farm• More focus on the farm as a whole• The advisor acts in a team of

advisors• Knowledge and advisory tools are

important but so are collaboration and communication skills

• Sharing knowledge

EDF Congress 2006, Denmark

6. Competitive strength of theDanish milk production

EDF Congress 2006, Denmark

Net capital and liabilities

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Denmark

Sweden

Norway

Finland

Netherlands

Germany

France

Spain

U.K.

Ireland

Poland

Hungary

USA

Brasil

Kina

Australia

New Zealand

Net capital Liabilities

EDF Congress 2006, Denmark

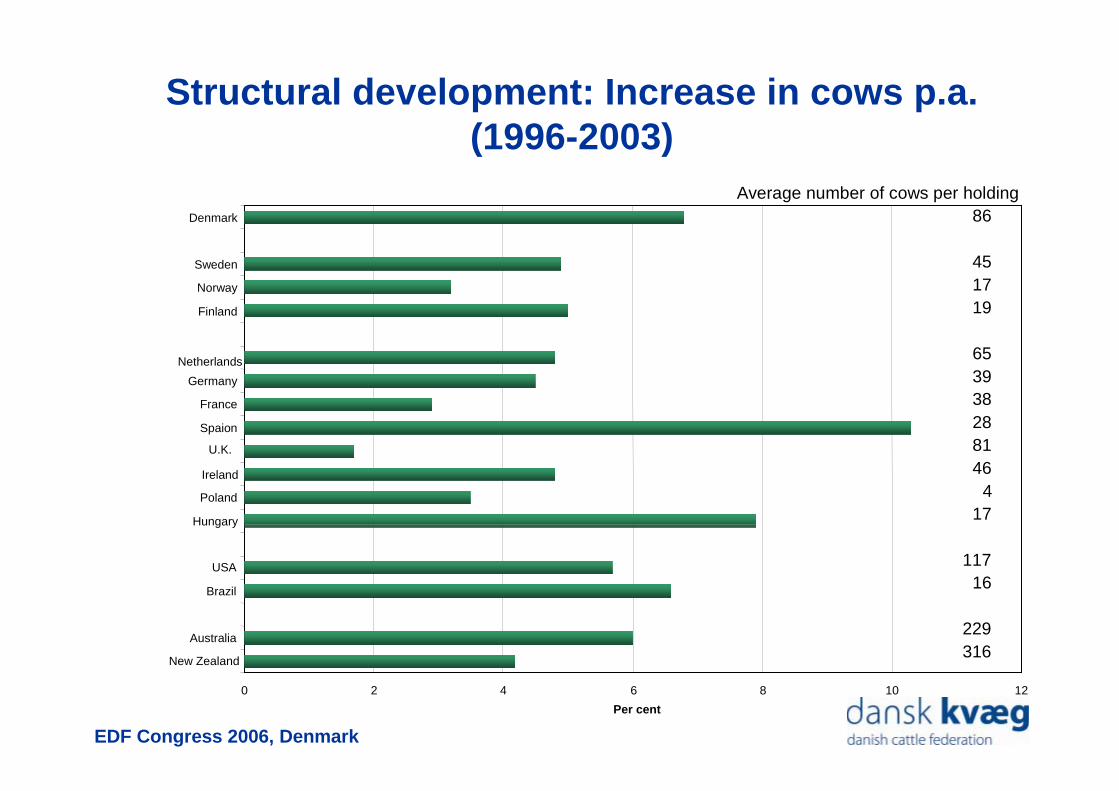

Structural development: Increase in cows p.a. (1996-2003)

0 2 4 6 8 10 12

Denmark

Sweden

Norway

Finland

Netherlands

Germany

France

Spaion

U.K.

Ireland

Poland

Hungary

USA

Brazil

Australia

New Zealand

Per cent

Average number of cows per holding86

451719

653938288146

417

11716

229316

EDF Congress 2006, Denmark

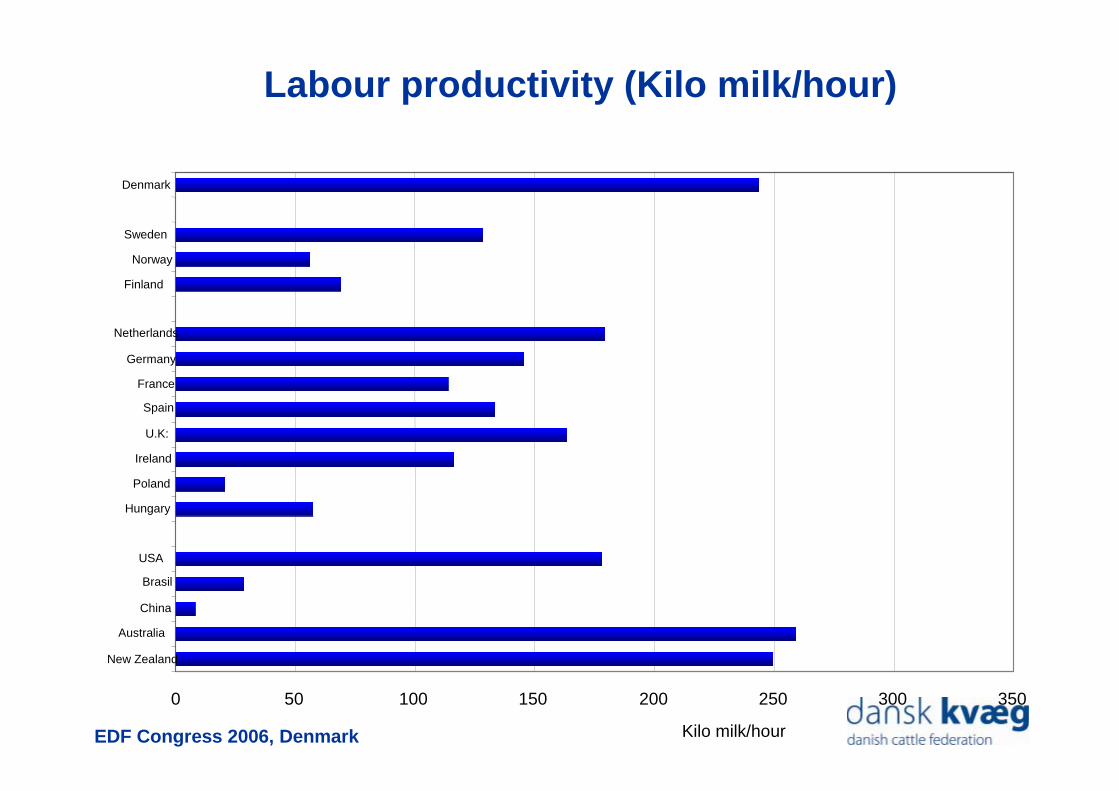

Labour productivity (Kilo milk/hour)

0 50 100 150 200 250 300 350

Denmark

Sweden

Norway

Finland

Netherlands

Germany

France

Spain

U.K:

Ireland

Poland

Hungary

USA

Brasil

China

Australia

New Zealand

Kilo milk/hour

EDF Congress 2006, Denmark

Danish milk productionInternational competitiveness

Structure: 6.8% annual increase in farm sizes

Working productivity: Only exceeded by NZ and Australia. High wages, but well-educated, efficient and ready for readjustments

Debt ratio: 75% = top achievement, but resultis a high investment level = geared for international competition

EDF Congress 2006, Denmark

Investments on dairy farms

0

1000

2000

3000

4000

5000

6000

7000

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

Inve

stm

ents

, DK

K p

er c

ow

Quota exchangeintroduced

EDF Congress 2006, Denmark

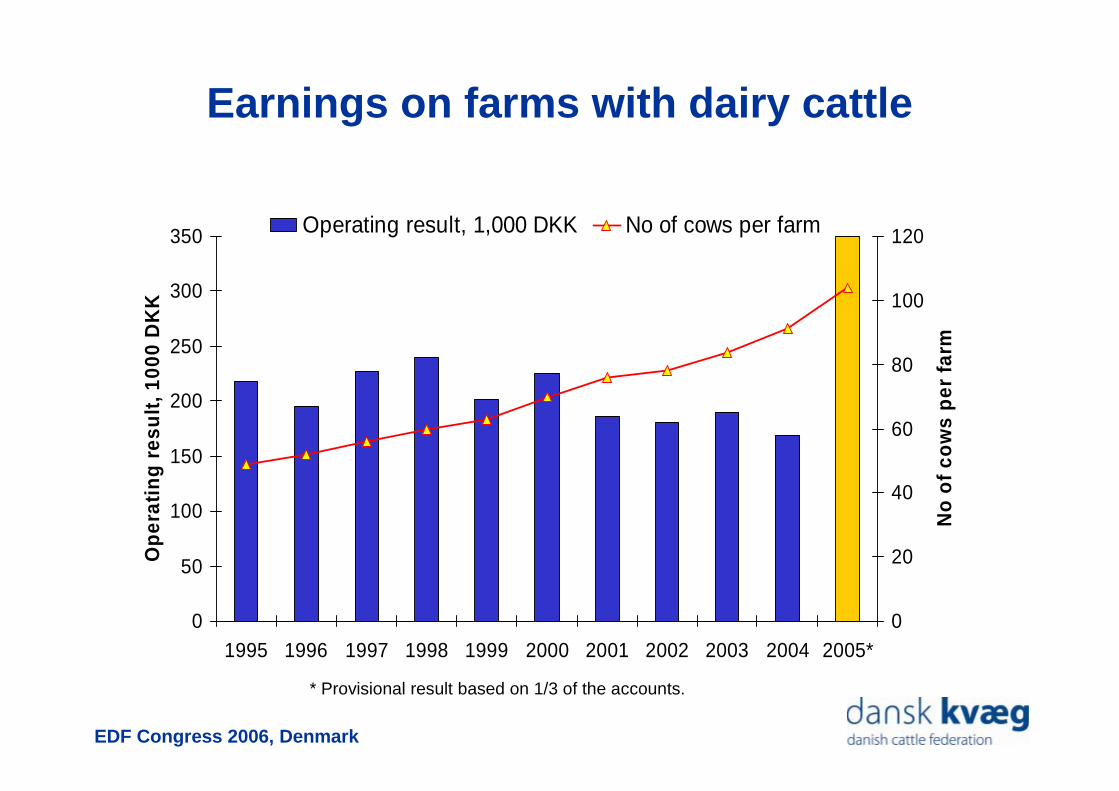

Earnings on farms with dairy cattle

0

50

100

150

200

250

300

350

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005*

Op

erat

ing

res

ult

, 100

0 D

KK

0

20

40

60

80

100

120

No

of

cow

s p

er f

arm

Operating result, 1,000 DKK No of cows per farm

* Provisional result based on 1/3 of the accounts.

EDF Congress 2006, Denmark

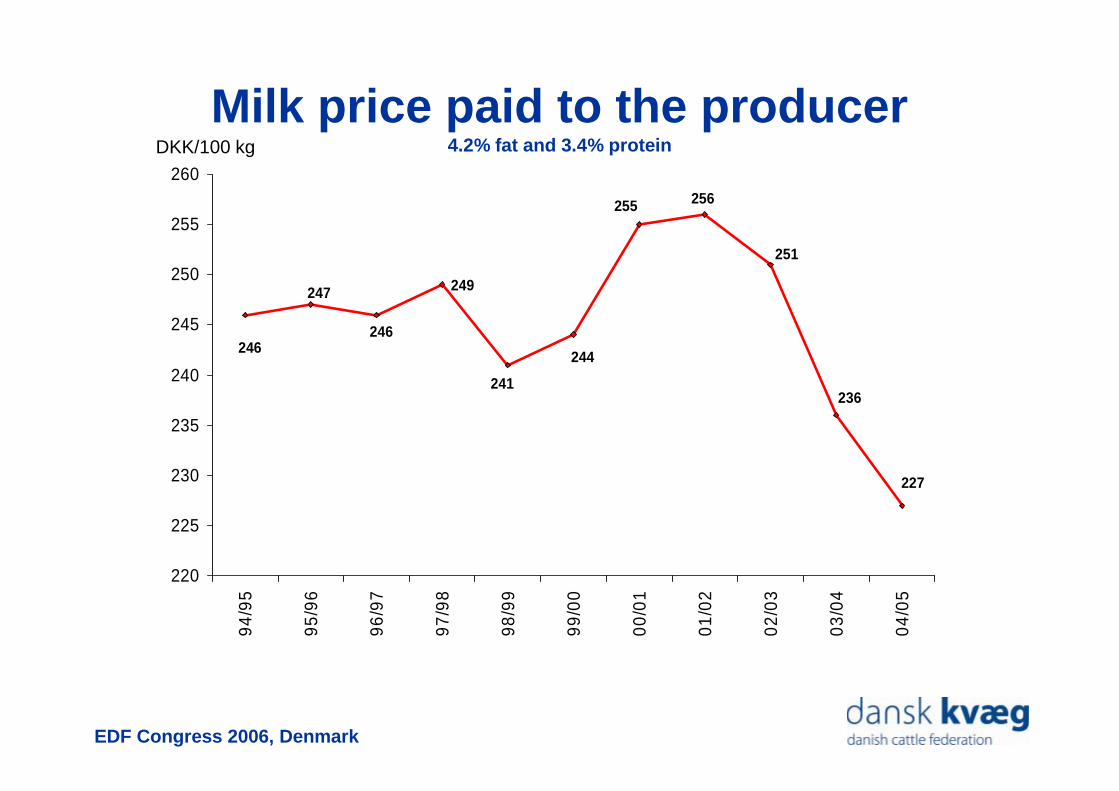

249

227

244

241

246

236

251

255 256

247

246

220

225

230

235

240

245

250

255

260

94/9

5

95/9

6

96/9

7

97/9

8

98/9

9

99/0

0

00/0

1

01/

02

02/

03

03/

04

04/

05

DKK/100 kg

Milk price paid to the producer4.2% fat and 3.4% protein

EDF Congress 2006, Denmark

Milk price paid to the producer in other countries DKK per 100 kg (4.2% fat and 3.4% protein)

1402901662562332552412632552001

1352251502182062242222602362004

133*2101782162042212162562272005

1161881302221982302302662512003

-1%-7%+18%-1%-1%-2%-3%-2%-4%in DKK

-5%-6%+5%-1%-1%-2%-3%-2%-4%in nat’lcurrency

1202181472332062412332662562002

Change in 2005 compared to 2004, percentage

NZUSPLDEUKNLFRFINDK1

Year

Note: 1) The Danish prices are October year prices* Estimated prices

EDF Congress 2006, Denmark

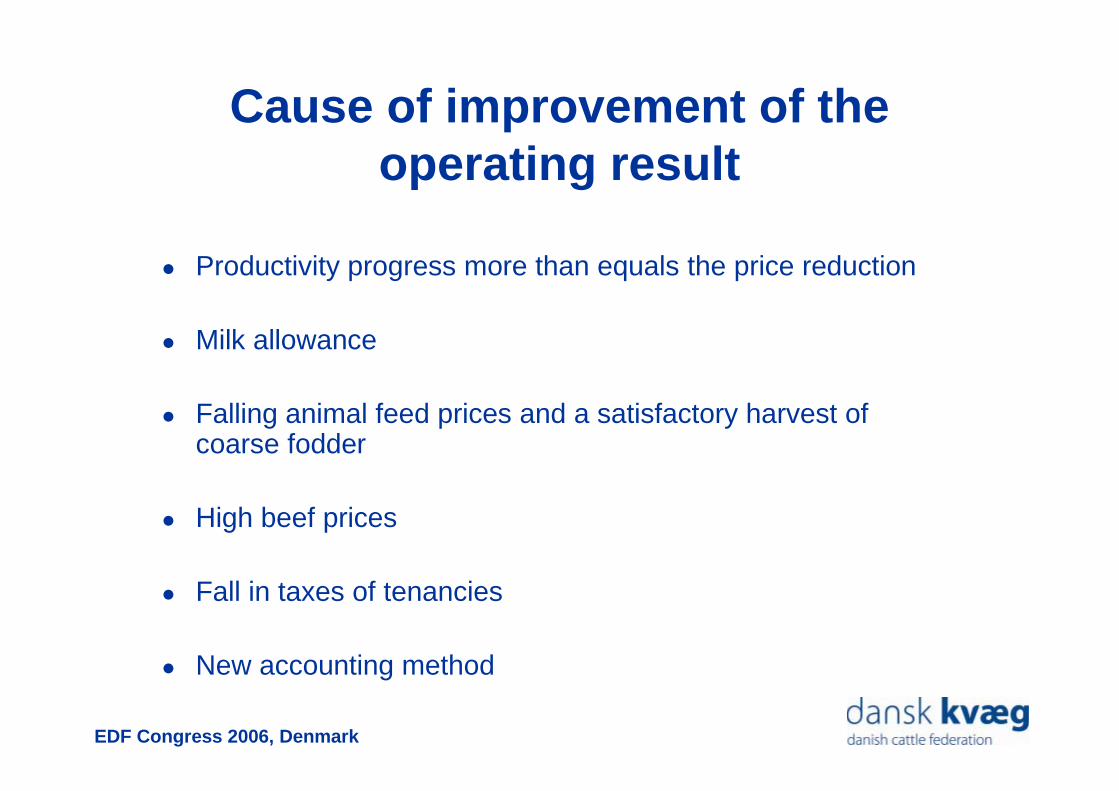

Cause of improvement of theoperating result

Productivity progress more than equals the price reduction

Milk allowance

Falling animal feed prices and a satisfactory harvest ofcoarse fodder

High beef prices

Fall in taxes of tenancies

New accounting method

EDF Congress 2006, Denmark

7. Concluding remarks

EDF Congress 2006, Denmark

Some concluding remarks

• The surrounding environment of the dairy farms in the EU is changing

– Milk price is decreasing and the income of the farms is under pressure

– Economic support to farmers is likely to decrease

– Decoupling of support from production changes the competitiveness of the dairy farms

EDF Congress 2006, Denmark

Some concluding remarks• The likely

countermove of the dairy farmers

– Lowering the cost of production

– Structural development and larger farms

– Investment in technology

– A change from craftsman to manager/leader

EDF Congress 2006, Denmark

If you prepare and change focusfrom support to the market –

there will be a bright future for the European milk producer.