the creation of a market : the western european markets experience maria ivanova / andrea s....

TRANSCRIPT

The Creation of a Market : the Western European markets experience

Maria Ivanova / Andrea S. TranquilliniPresentation to the 2nd AECSD ConferenceMoscow, 5 October 2005

Page 2Maria Ivanova / Andrea S. TranquilliniPresentation to the 2nd AECSD Conference

Moscow, 5 October 2005

Summary

Our Company

Conditions for an efficient market infrastructure

The scenario

Suggestions and Conclusions

Page 3Maria Ivanova / Andrea S. TranquilliniPresentation to the 2nd AECSD Conference

Moscow, 5 October 2005

Clearstream Banking S.A. LuxembourgCBL

(ICSD)

Clearstream Banking AG Frankfurt CBF (CSD)

Organisational Structure

Page 4Maria Ivanova / Andrea S. TranquilliniPresentation to the 2nd AECSD Conference

Moscow, 5 October 2005

Our company Global market coverage 41 markets

USA

Canada South Korea

China

Japan

Singapore

Malaysia

Hong Kong

Indonesia

Thailand

AustraliaNew Zealand

South Africa

Argentina

Mexico

Uruguay

European coverage

- Austria- Belgium- Czech Republic- Denmark- Estonia- Finland- France- Germany

- Greece- Hungary - Iceland - Ireland- Italy- Luxembourg- Netherlands- Norway-Russia (Jan.2006)

- Poland- Portugal- Slovak Republic- Spain- Sweden- Switzerland- Turkey- United Kingdom

Page 5Maria Ivanova / Andrea S. TranquilliniPresentation to the 2nd AECSD Conference

Moscow, 5 October 2005

Our company The size of our core activities

Clearstream:

Offers Settlement and Custody services to more than 2,500 customers world-wide (only regulated financial institutions, including 28 Central Banks), covering over 200,000 domestic and internationally-traded bonds and equities

Has securities on deposit worth EUR 8.3 trillion as at 30 June 2005

Settles transactions involving securities that are traded within Germany and internationally via a total of 17 platforms*

Settles more than 160,000 transactions daily across 41 domestic markets

Has been top rated as the industry provider for Tripartite Repo business

Reached sales revenues of EUR 578,8 Mio in 2004

* Including Xetra, floor trading at FWB, regional German stock exchanges, US BrokerTec and MTS Group

Page 6Maria Ivanova / Andrea S. TranquilliniPresentation to the 2nd AECSD Conference

Moscow, 5 October 2005

Our Company Our Objectives

Our objective is to improve the efficiency of securities services for global markets.

We deliver integrated securities services for financial institutions worldwide by creating competitive and innovative solutions to:

Remove market inefficiencies of today

Build business opportunities for market players

Deliver cost-efficiencies to the securities industry

We are committed to reducing costs for Market Participants

Page 7Maria Ivanova / Andrea S. TranquilliniPresentation to the 2nd AECSD Conference

Moscow, 5 October 2005

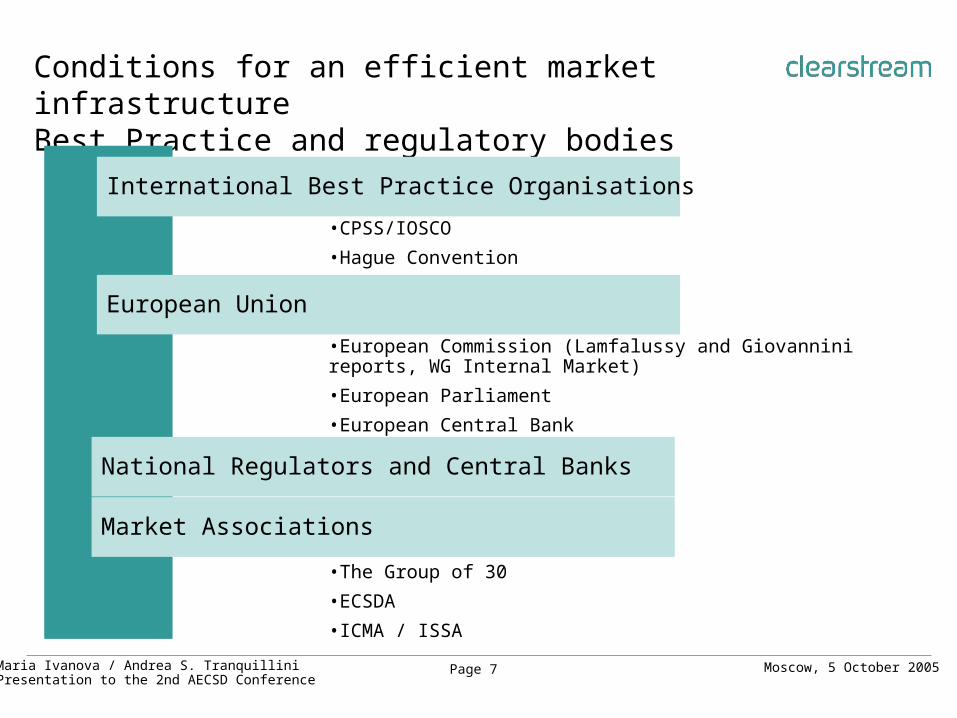

Conditions for an efficient market infrastructure Best Practice and regulatory bodies

•The Group of 30

•ECSDA

•ICMA / ISSA

International Best Practice Organisations

European Union

National Regulators and Central Banks

Market Associations

•European Commission (Lamfalussy and Giovannini reports, WG Internal Market)

•European Parliament

•European Central Bank

•CPSS/IOSCO

•Hague Convention

Page 8Maria Ivanova / Andrea S. TranquilliniPresentation to the 2nd AECSD Conference

Moscow, 5 October 2005

Conditions for an efficient market infrastructureThe drivers - 11) CPSS IOSCO – Hague Convention Formulates broad supervisory standards, gives guidelines, recommends

statements of best practice Hague Convention promotes harmonisation of financial market’s legislation

2) European Union – Lamfalussy Report - Giovannini Committee Focus on harmonization of cross-border post-trade practises. The reports have

identified the existing barriers prevent the efficient delivery of C&S services. Consensus that the EU post-trade landscape could be significantly improved.

Convergence initiatives The removal of barriers related to taxation and legal certainty is clearly the

responsibility of the public sector. European Commission Aims to propose legislation for the financial sector (FSAP,

etc)

3) ECSDA Represents the interest of its CSD and ICSD members and represents them at

international level on technical, financial, legal & regulatory discussion. Streamlines initiatives among its members to achieve harmonisation, increase

efficiency and reduce risk in post-trade across Europe for the benefit of issuers, investors and market participants.

Page 9Maria Ivanova / Andrea S. TranquilliniPresentation to the 2nd AECSD Conference

Moscow, 5 October 2005

Conditions for an efficient market infrastructureThe drivers - 24) “G30 Group” 20 Recommendations Interoperability Focus on creation of a single Financial market by creating cross

border market links for both securities and cash, CCPs, Securities Lending, reference data, messaging and communications.

Risk management Business Continuity and Disaster Recovery plans to avoid large-scale market disruption and minimize Operational risk.

Governance Need of experienced and appropriate Board membership. Development of remote membership. Need of clear regulatory framework in each country.

5) ISSA – International Securities Services Association Need of collecting and disseminating information on the developments in the

rapidly changing international securities markets, Need to offer securities operations professionals a forum to exchange ideas and

issues of common interest. 100 member institutions world-wide and 2000 subscribers to its publications all

over the world. Out of the 44 Asian countries only 7 are members of the ISSA (Pakistan, China-HK,

Japan, Korea, Malaysia,Taiwan, Thailand)

Page 10Maria Ivanova / Andrea S. TranquilliniPresentation to the 2nd AECSD Conference

Moscow, 5 October 2005

1) CPSS IOSCO

(IOSCO) - International Organization of Securities Commissions has developed in 1998 the Objectives and Principles of Securities Regulation

(CPSS) - Committee on Payment and Settlement Systems of the Central Banks of the Group of Ten Countries has produced in 2001 the final version of the Core Principles for Systemically Important Payment Systems.

Building on the previous work, the CPSS and IOSCO have worked to contribute further to this process by jointly developing recommendations for securities settlement systems, to improve the safety and efficiency of these systems.

Hague Convention’s objectives

– Law on cross border securities transfer or cross-border creation of interests iin securities held with an intermediary

– Protection of market participants from legal and systemic risk

– Protection of intl. Capital markets by « harmonisation of « conflict of law ».

– Improvement of efficiency of capital markets

– Cost reduction in cross border securities settlement and collateralisation.

Page 11Maria Ivanova / Andrea S. TranquilliniPresentation to the 2nd AECSD Conference

Moscow, 5 October 2005

2) EUROPEAN UNIONThe Giovannini committee

Identification of inefficiencies in EU financial markets.

Definition of Barriers preventing market integration. Three main groups:

– National differences in technical requirements and market practice;

– National differences in tax procedures;

– Issues relating to legal certainty.

Proposal of practical solutions to improve market integration.

DBAG endorses the results of the two Giovannini reports and, as a top priority, supports a quick and comprehensive removal of the barriers identified.

Despite the non-enforceability of the second report, Deutsche Börse Group has been willing to make sizeable efforts to remove those barriers individually and together with other market participants.

Deutsche Börse Group is actively participating with market associations, such as ECSDA, to develop viable solutions to barriers 4, 7 and 3, and has already implemented and comply with barrier 1 (implementation of ISO15002).

Page 12Maria Ivanova / Andrea S. TranquilliniPresentation to the 2nd AECSD Conference

Moscow, 5 October 2005

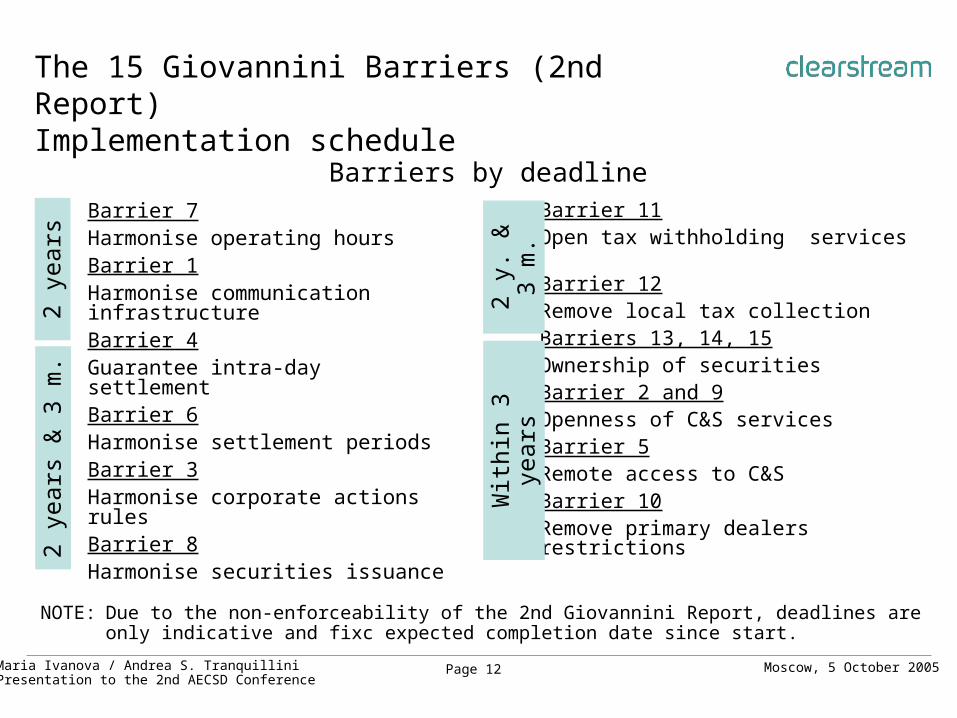

The 15 Giovannini Barriers (2nd Report)Implementation schedule

Barriers by deadlineBarrier 7Harmonise operating hoursBarrier 1Harmonise communication infrastructureBarrier 4Guarantee intra-day settlementBarrier 6Harmonise settlement periodsBarrier 3Harmonise corporate actions rulesBarrier 8Harmonise securities issuance

Barrier 11Open tax withholding servicesBarrier 12Remove local tax collectionBarriers 13, 14, 15Ownership of securitiesBarrier 2 and 9Openness of C&S servicesBarrier 5Remote access to C&SBarrier 10Remove primary dealers restrictions

2 y

ears

2 y

ears

& 3

m.

Wit

hin

3 y

ears

2 y

. &

3

m.

NOTE: Due to the non-enforceability of the 2nd Giovannini Report, deadlines are only indicative and fixc expected completion date since start.

Page 13Maria Ivanova / Andrea S. TranquilliniPresentation to the 2nd AECSD Conference

Moscow, 5 October 2005

3) ECSDA Working Groups

Barrier 7 Harmonisation of Operating Hours and Settlement Deadlines

Barrier 4 Intra-day settlement finality

Action: Addressed by ECSDA Working Group 5 through development of an inventory and a set of 10 harmonisation standards agreed that all 17 member CSDs have committed to acheive by April 2005.

Status: Targets reached at 75%. Considerable change expected over the next 6 month.

Barrier 3 Corporate Actions harmonisation

Action: Also assigned to ECSDA’s Working Group 5, which is currently finalising a solution for cash distribution suitable to all 17 member CSDs and in close collaboration with the European Banking Federation (EBF) and the the European Securities Forum /ESF)

Page 14Maria Ivanova / Andrea S. TranquilliniPresentation to the 2nd AECSD Conference

Moscow, 5 October 2005

4) G30 Recommendations on C&SRecommendation Monitoring organisation

1 Eliminate paper and automate communication, data capture and enrichment

North American committee, European Monitor Committee, Asia/Pacific Regional Committee

2 Harmonise messaging standards and communication protocolsISSA, SWIFT

3 Develop and implement reference data standards (ISIN numbering)

4 Synchronise timing between C&S systems and payment FX systems North American committee, European Monitor Committee, Asia/Pacific Regional

CommitteeAssociation Global Custodians

5 Automate ans standardsize institutional trade matching

6 Expand the use of Central counterparts

ISSA7 Permit securities lending and borrowing to expedite settlement

8 Automate and standardise assets servicing processes, inclusing CA, Tax relief and restriction to foreign ownership

9 Ensure financial integrity of providers of C&S servicesPriceWaterhouseCoopers

10

Reinforce risk mgmt practices of users of C&S services

11

Ensure final simultaneous transfer and availability of assets. North American committee, European Monitor Committee,

Asia/Pacific Regional CommitteeAssociation Global Custodians1

2Ensure effective business continuity and disaster recovery planning

13

Address the possible failure of a systematically important institution

14

Stengthen assessment of the enforceability of contracts Legal Subcommittee – ISDA, EFMLG, CPSS/IOSCO

15

Advance letgal certainty over rights to securities, cash, or collateral Legal Subcommittee, UNIDROIT, Hague Conference, CPSS/IOSCO, ISDA, EUPFL

16

Recognise and support improved valuation and closeout netting arrangements

Legal Subcommittee, ISDA, EFMLG, EUPFL

17

Ensure appointment of appropriately experienced and senior board members

Regional co-chairs18

Promote fair access to securities C&S networks

19

Ensure equitable and effective attantion to stakeholders interests

20

Encourage consistent regulation and oversight of C&S service providers

Page 15Maria Ivanova / Andrea S. TranquilliniPresentation to the 2nd AECSD Conference

Moscow, 5 October 2005

5) ISSA (International Securities Services Association) Barriers 6,7,8 Expand the use of Central counterparts, Facilitate Securities lending and borrowing, Automate and standardize assets servicing processes, including CA, Tax relief and restriction to foreign ownership.

Action: Within the framework of the Group of 30 recommendations, ISSA has received a mandate to assist with finding solutions for recommendations 6, 7, 8. ISSA has requested its members to join in a new project to address the subjects covered in these recommendations, by trying to assemble a useful source of information that is globally consolidated, yet provides details on an individual market level.

Status: Questionnaire to members in progress

Barrier 2,3 Harmonize messaging standards and communication protocols, develop and implement reference data standards (ISIN numbering).

Action: ISSA is supporting SWIFT presently in charge of the Barrier’s removal.

Status: SWIFT has established a Independent Advisory Group to solve Giovannini Barrier 1

Page 16Maria Ivanova / Andrea S. TranquilliniPresentation to the 2nd AECSD Conference

Moscow, 5 October 2005

Conditions for an efficient market infrastructurePreliminary steps Central Securities Registry (alternative: the German option)

Certainty of ownership. Official entitlement compensation rules, Record date, Ex date, Pay date. Legal enforcment

Centralised source of Corporate Action information

CSD

Third party account recognition (Nominee, Omnibus)

Single numbering Agency

Real Time settlement (both cash and securities)

Primary market / New issues regulation (eg. IPOs)

Page 17Maria Ivanova / Andrea S. TranquilliniPresentation to the 2nd AECSD Conference

Moscow, 5 October 2005

The « G8 » markets experience compared to Russia

Russia USA Germany FranceUnited

Kingdom Japan Canada Italy

Official Ent.Comp. rules NO YES YES YES YES YES YES YES

Record date YES YES YES YES YES YES YES YES

Ex date NO YES YES YES YES YES YES YES

Pay Date NO YES YES YES YES YES YES YES

Legal enforcment NO YES YES YES YES YES YES YES

Central Securities registry NO YES YES YES YES YES YES YES

Centralised source for CA NO YES YES YES YES YES YES YES

Central Securities Depository 0 2 1 1 1 2 1 1

Nominee account NO YES YES YES YES YES YES YES

omnibus-third party account NO YES YES YES YES YES YES YES

Single numbering Agency NO YES YES YES YES YES YES YES

New Issues regulation NO YES YES YES YES YES YES YES

Page 18Maria Ivanova / Andrea S. TranquilliniPresentation to the 2nd AECSD Conference

Moscow, 5 October 2005

Deutsche Börse AGStock Exchanges Stock Exchanges Stock Exchanges Stock

Exchanges

Stock Exchanges Stock Exchanges Stock Exchanges Stock Exchanges

Stock Exchanges Stock Exchanges Stock Exchanges Stock Exchanges

The example of the German Market

Clearstream Banking Frankfurt (CBF)

HannoverHamburg MunichStuttgartEUWAX

BremenBerlinDüssel-

dorfFrank-

furt Xetra Eurex

BAFIN

Bundesbank

Ministry of Finance

Registrars

CBF as a router and intermediary of market info towards the Registrars.No Central Securities Registry

WM

National Numbering AgencyCentralised source of CA information

Page 19Maria Ivanova / Andrea S. TranquilliniPresentation to the 2nd AECSD Conference

Moscow, 5 October 2005

MICEX GroupStock Exchanges Stock Exchanges Stock Exchanges Stock Exchanges

Stock Exchanges Stock Exchanges Stock Exchanges Stock Exchanges

Stock Exchanges Stock Exchanges Stock Exchanges Stock Exchanges

…and of the Russian Market (2007?)

National Depository & Clearing Centre

The Rostov Currency and Stock Exchange

The Siberian Interbank Currency Exchange

MICEXStock

Exchange

MICEX Settlement

House

National Mercantile Exchange

FSFM

Central Bank of Russian Federation

Ministry of Finance

Registrars

CSD as a router and intermediary of market info towards the Registrars.No Central Securities Registry

?

National Numbering AgencyCentralised source of CA information

The Nizhny Novgorod Stock and Currency Exchange

The Asian Pacific

Interbank Currency Exchange

The Samara Currency Interbank Exchange

Russian Trading System

The St. Petersburg

Stock Exchange

The Ural Regional Currency Exchange

Page 20Maria Ivanova / Andrea S. TranquilliniPresentation to the 2nd AECSD Conference

Moscow, 5 October 2005

Our approach and Conclusion

We seek efficiency through existing models.

We target market growth within a regulated environment (infrastructure and legislation).

We participate to international forums, associations, committees.

Clearstream and Deutsche Börse Group are supportive for the creation of new securities market infrastructure and

available to provide the necessary knowledge.

Page 21Maria Ivanova / Andrea S. TranquilliniPresentation to the 2nd AECSD Conference

Moscow, 5 October 2005

Contacts

Maria Ivanova Andrea S. Tranquillini Customer Relations Management Network Relationship ManagementNorthern and Eastern Europe Central and Eastern European CountriesE-mail:[email protected] E-mail:[email protected]: +352.243.36381 Tel: +352.243.32477Fax: +352.243.636381 Fax: +352.243.632477Mobile: +352.021.295239 Mobile: +352.021.214619