the credit liquidity trap - six swiss · pdf fileproduced by the royal bank of scotland plc....

TRANSCRIPT

BUILDING TOMORROW™

rbs.com/mib

Produced by The Royal Bank of Scotland plc.In the UK, the Royal Bank of Scotland plc is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority.

The Credit Liquidity TrapMacro Credit Research

SSX and SBC, 26 November 2014Alberto Gallo, CFA

Head of European Macro Credit Research+44 (0) 20 7085 5736

Lee Tyrrell-HendryMacro Credit Analyst

+44 (0) 20 7085 [email protected]

Tao PanMacro Credit Analyst

+44 (0) 20 7678 [email protected]

Mateja PopovicMacro Credit Analyst

+44 (0) 20 7085 [email protected]

Rajarshi MalaviyaGaurav Chhapia

Chanchal Beriwal

2

The Credit Liquidity Trap

“There is always a temptation for the central bank to speak in a whisper, because anything that gets said reverberates so loudly in markets. But the softer it talks, the more the market leans in to hear better and, thus, the more the whisper gets amplified. So efforts to overly manage the market volatility associated with our communications may ultimately be self-defeating.” Jeremy C. Stein, Federal Reserve Governor, May 6, 2014

The persistence of current benign market conditions largely hinges on three key factors. First, continued strong investor confidence centres on a fragile euro area recovery with significant downside risks. In view of this, low levels of corporate default and volatility could be tested by a normalisation of global liquidity conditions. Second, strong risk appetite among global investors could be threatened by rising geopolitical tensions, growing vulnerabilities in emerging markets or an unexpected increase in global benchmark rates, which remain at historical lows. Any such unravelling of recent search-for-yield behaviour could prompt a sharp repricing of risk, which could be amplified by low market liquidity in key segments. ECB Financial Stability Review, April 2014

“The whole system relies on liquidity illusion: We know we can’t all buy or all sell all our assets the same day. If you don’t have a contingency plan if liquidity goes away, then you’re up the creek without a paddle” Peter Fisher, Blackrock Investment Institute, June 2014

Some broad combination of these pockets of evolving vulnerabilities—set against a backdrop of a rise in short-term interest rates or an unwinding of currently compressed risk and term premia—could prove disruptive. In particular, a tail risk where there was a precipitous attempt by investors to exit certain markets—perhaps exacerbated by outflows from ETFs and mutual funds as well as near-term market illiquidity—could trigger an abrupt and self-reinforcing re-pricing of a range of financial assets. IMF Article IV Consultation on the United States, June 2014

3

Corporate bond markets have grown and changed since the crisisFund and household holdings of corporate bonds (% of US corp. bond market)

Source: RBS Credit Strategy, Federal Reserve

0%

5%

10%

15%

20%

25%

30%

35%

1945 1951 1957 1963 1969 1975 1981 1987 1993 1999 2005 2011

Household ownership share Fund ownership share

4Source: RBS Credit Strategy, FRED

Asset managers face pressure as yield decline, fees stay the sameSome respond with lower fees, most hunt for more yield

0%

2%

4%

6%

8%

10%

12%

1956 1964 1972 1980 1988 1996 2004 2012

10y Bund yield

Asset Manager fees

5Source: RBS Credit Strategy, FRED

Asset Manager fees as a % of 10-year Bund yield

0%

5%

10%

15%

20%

25%

30%

35%

1956 1964 1972 1980 1988 1996 2004 2012

6

The beta trade: this time is different vs 2004-2007

Source: RBS Credit Strategy

Stylised efficient frontier. From “rating arbitrage” (pre-crisis) to search for high beta, nominal yield

0%

2%

4%

6%

8%

10%

12%

14%

0% 5% 10% 15% 20% 25% 30%

Volat ility

Expected return

QE effect

Today: inves tors buy unlevered, high risk assets (e.g. HY, cocos)

Pre-crisis: leveraged high-rated port folios (e.g. synthetic

CDOs, CPDOs)

“There are three ways to make a living in this business: be first, be smarter, or cheat” John Tuld, Margin Call (2011)

7

Compression in risk premia

Source: RBS Credit Strategy, FRED, Bloomberg. Date range: from 1999 to today (except EM HY where data is only available from Dec 2003 onwards).

0

500

1,000

1,500

2,000

2,500

3,000

$ IG € IG EM IG $ HY € H Y EM HY 10yUST

10yBunds

10ySPGBs

10y BTPs

V2X VIX P/E

LT average

CurrentMax

Min

20

40

60

80

100

120

8

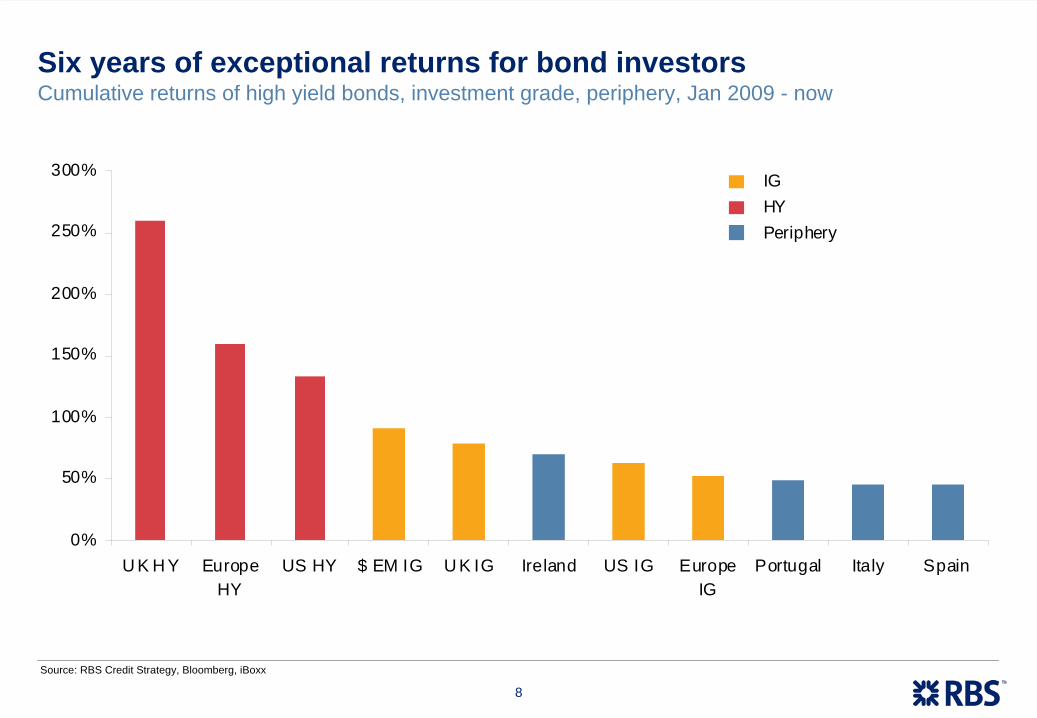

Six years of exceptional returns for bond investors

Source: RBS Credit Strategy, Bloomberg, iBoxx

Cumulative returns of high yield bonds, investment grade, periphery, Jan 2009 - now

0%

50%

100%

150%

200%

250%

300%

U K H Y EuropeHY

US HY $ EM IG U K IG Ireland US IG EuropeIG

Portugal Italy Spain

Periphery

IGHY

9

The end of the beta trade?

Source: RBS Credit Strategy

High-beta credit continues to weaken while Euro IG stays resilient, total returns, 100 = 31 Dec 2013

86

90

94

98

102

106

110

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov

Euro IG US IG

Euro B US CCC

Cocos Corporate H ybrids

US Distressed

10

1. The architecture of the bond market has changed. The corporate bond market has grown in size as well since the crisis (from $6tn to roughly $10tn in the US). Households and especially mutual funds now own a larger share of credit

2. More mutual funds means more market participants in competition to outperform each other. Low yields have put pressure vs fee structures. Some asset managers have reacted by lowering costs – most instead have taken more risk.

3. Unlike pre-crisis, the search for yield since 2009 has manifested itself as a search for beta. This is different than pre-crisis, when investors were mostly leveraging highly rated assets. Today, investors rely less on rating agencies and building exotic/leveraged products is more difficult. The preference is for high nominal yield products, some of which have embedded leverage (e.g. contingent capital)

4. As a result, the last five years have seen strong performance in high beta bonds, including high yield, corporate and financial hybrid bonds, and periphery – this was accompanied by constant inflows into mutual funds

5. But as monetary policy normalises, the market is vulnerable to re-pricing, and the bottleneck of trading liquidity remains tight

11

Exit risk: Policy normalisation and risk repricing“Now, back to Macro. What is your exit strategy? The players won't be in on the scam, so they'll all think it's their lucky night, but you'll never get them out of there with their winnings, they'll gamble it all back. That's Vegas and that's your problem.”

Roman Nagel, Ocean’s Thirteen

12

What is liquidity? Systemic and refinancing liquidity risks are low

EUR 3m Libor-OIS spread, bp

Source: RBS Credit Strategy, Bloomberg

Debt maturity wall for European IG corporates, % of total debt

Source: RBS Credit Strategy, Bloomberg. *Included all non-financial corporates in iTraxx Main

0%

10%

20%

30%

40%

50%

60%

2014 2015 2016 2017 2018 2019 2020onwards

0

20

40

60

80

100

120

140

160

180

200

2006 2007 2008 2009 2010 2011 2012 2013 2014

13

But transactional liquidity is low: RBS liquid-o-meterTrading liquidity in US credit markets continues to decline, but is improving in Treasury markets.

Source: RBS Credit Strategy, Bloomberg, SIFMA, MarketAxess.

0

20

40

60

80

100

120

140

160

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

US T reasuries US corporate bonds100 = D ec 2006

14

Market grows but dealers pull backMarket size ($bn) vs dealer estimated holdings of corporate bonds (% of market size)

Source: RBS Credit Strategy, Bloomberg, SIFMA, MarketAxess, Federal Reserve Bank of New York

0.0%

0.3%

0.6%

0.9%

1.2%

1.5%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 20140

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000Credit market s ize (RHS) Dealers ' est. holdings (LHS)

15

Lower liquidity is partly a symptom of lower dealer inventoriesUS corporate bond dealer inventories, $bn.

Source: RBS Credit Strategy, Federal Reserve Bank of New York, SIFMA, MarketAxess. Note: because corporate bond dealer inventories are not broken down prior to 2013, we have assumed IG and HY inventories are in the same proportion as the average from 2013-present.

0

50

100

150

200

250

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

IG + HY CP + RMBS + CMBSIG HYCP RMBSCMBS

16

Low volumes and higher transaction costs

Average daily trading volumes, %mkt size

Source: RBS Credit Strategy, SIFMA

Index members’ bid-ask, % CDS spread

Source: RBS Credit Strategy, Bloomberg

0.0%

0.1%

0.2%

0.3%

0.4%

0.5%

0.6%

0.7%

0.8%

05 06 07 08 09 10 11 12 13 140%

5%

10%

15%

20%

25%

30%

35%

2006 2007 2008 2009 2010 2011 2012 2013 2014

CDX HY Xover CDX IG

17

Markets are polarised between few liquid and many illiquid bonds

Distribution of bond by trading frequency in US TRACE

Source: RBS Credit Strategy, Michael A. Goldstein (Babson College)

0

200

400

600

800

1,000

1,200

0 50 100 150 200 250 300Number of bonds

Num

ber o

f tra

des

in 3

0 da

ys

Percent of trading days per quartile

Source: RBS Credit Strategy, IMF GFSR Oct 2014

0

10

20

30

40

50

60

70

80

90

100

0 25 50 75 100

Percent of index const ituentsPe

rcen

t of t

radi

ng d

ays

Corporate EM Bond Index HY

More liquidLess liquid

18

High quality collateral is shrinking

QE effects: repo volume goes down as Fed holdings go up Daily ave. collateral value in tri-party repo vs Fed holdings, $bn

Source: RBS Credit Strategy, SIFMA, Federal Reserve Bank of New York

Collateral velocity is going down Overall collateral volume (blue) vs sources of collateral (green)

Source: RBS Credit Strategy, Singh, M. (IMF, 2012 & 2013)

200

700

1200

1700

2200

2700

2011 2012 2013 2014

OtherTreasury securit iesAgency securitiesFed holdings of Treasury securit iesFed holdings of agency securit ies Central Collateral Desk

$10tn (2007) $5.8tn (2010) $6.1tn (2011) $6tn (2012)

$1.7tn (2007) $1.1tn (2010) $1.1tn (2011) $1.0tn (2012)

Hedge funds

$1.7tn (2007) $1.3tn (2010) $1.3tn (2011) $1.8tn (2012)

Securities lending via custodians

Money market funds

de minimis

Commercial banks

Velocity (overall collateral/sources)

2007: 3.0 2010: 2.4 2011: 2.5 2012: 2.2

“suppliers”“users”

19

Do you get paid for illiquidity? Not much

Deviations of estimated bond liquidity risk premia from historical averages

Source: RBS Credit Strategy, Bank of England

Decomposition of €HY spreads, bp

Source: RBS Credit Strategy, Bloomberg, Moody’s

0

200

400

600

800

1000

1200

1400

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

Volat ility riskD efault riskLiquidity risk

-200

-100

0

100

200

300

400

500

600

2000 2002 2004 2006 2008 2010 2012 2014

USD H YUSD IG (RHS)EUR IG (RHS)GBP IG (RHS)

20

Exiting stimulus can be painful

Source: RBS Credit Strategy, Bloomberg

Total returns during the taper tantrum (22 May – 29 August 2013)

-16%

-12%

-8%

-4%

0%

€ Fi

n T1

€ 1-

3yr

€ H

YS

&P 5

00S

pain

€ 3-

5yr

€ IG

Fin

sH

ealth

Cap

ital G

oods

Con

s N

on-c

ycM

ater

ials

€ IG

Italy

Con

s C

ycIn

dust

rials

Tech

Util

ities

Ene

rgy

BK

LN E

TF€

5-7y

r€

Fin

LT2

Telc

osX

over

JNK

E E

TF

$ H

YC

DX

HY

€ 7-

10yr

UC

00$

IGH

YG E

TFJN

K E

TFC

DX

EMPo

rtuga

lLQ

D E

TF$

EM IG

$ E

M H

Y$

EM

SO

VE

MB

ET

FE

MH

Y E

TFE

MLC

ETF

Gre

ece

IndicesSectorsPeripheryETFs

21

Tantrum 2.0 vs Tantrum 1.0

Source: RBS Credit Strategy, Bloomberg.

Total returns during the taper tantrum (22 May – 29 August 2013) vs 2014 sell off (30 June – 16 October 2014)

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

€ Fi

n T1

€ 1-

3yr

€ H

YS&

P 5

00Sp

ain

sov

€ 3-

5yr

€ IG

Fin

sH

ealth

Cap

ital G

oods

Con

s N

on-c

yc€

IGIta

ly s

ovC

ons

Cyc

Indu

stria

lsTe

chU

tiliti

esEn

ergy

BKLN

ETF

€ 5-

7yr

€ Fi

n LT

2Te

lcos

JNK

E ET

F$

HY

€ 7-

10yr

£ IG

$ IG

HY

G E

TFJN

K E

TFPo

rtuga

l sov

LQD

ETF

$ EM

IG$

EM H

Y$

EM S

ovEM

B E

TFEM

HY

ETF

EMLC

ETF

Gre

ece

sov

Taper tantrum 2014 tantrum

22

Liquidity survey: Are you prepared?

23

Liquidity survey: Are you prepared?

What could make liquidity get worse in the near term?

Source: RBS Credit Strategy

How do you address lack of liquidity

Source: RBS Credit Strategy

84% of investors think lack of liquidity is a potential systemic risk for credit markets

0%

10%

20%

30%

40%

50%

60%

70%

Fed getsmore hawk ish

Risinggeopolit ical

risk

Idiosyncraticrisk

Eurozonedef lat ion

Other0%

10%

20%

30%

40%

50%

60%

70%

Mov

e to

mor

eliq

uid

asse

tcl

asse

s

Incr

ease

cas

h

Hol

d to

mat

urity

/laun

chfu

nds

with

targ

et d

ates

Trad

e m

ore

CD

S in

dice

s

Oth

er

Intro

duce

rede

mpt

ion

fees

24

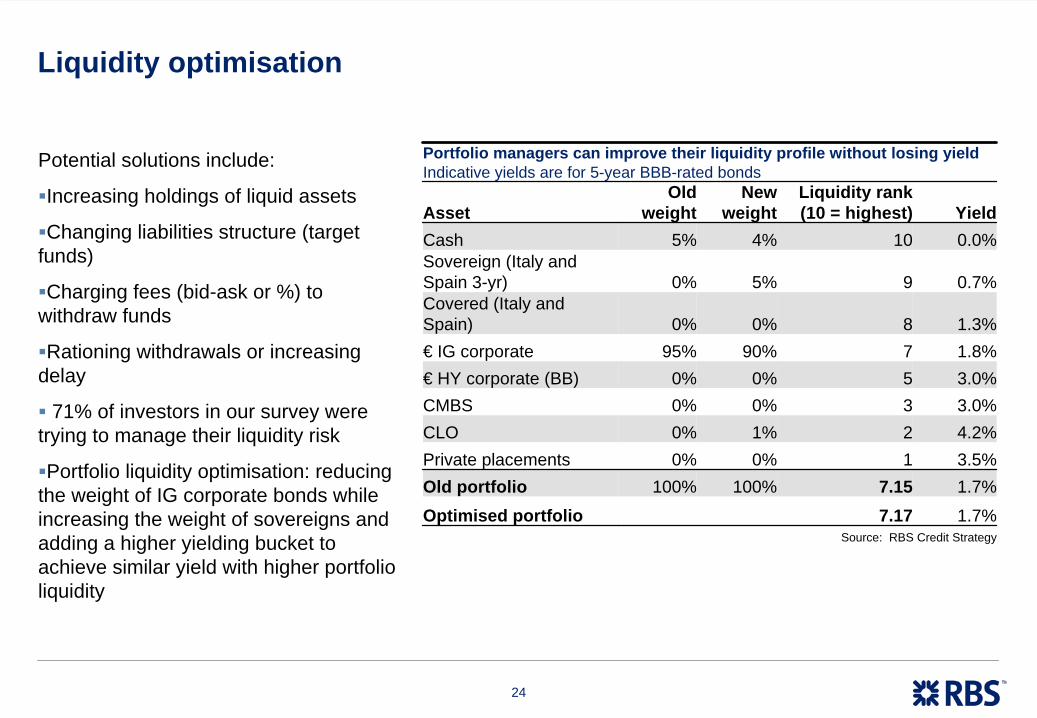

Liquidity optimisation

Portfolio managers can improve their liquidity profile without losing yield Indicative yields are for 5-year BBB-rated bonds

AssetOld

weightNew

weightLiquidity rank (10 = highest) Yield

Cash 5% 4% 10 0.0%Sovereign (Italy and Spain 3-yr) 0% 5% 9 0.7%Covered (Italy and Spain) 0% 0% 8 1.3%€ IG corporate 95% 90% 7 1.8%€ HY corporate (BB) 0% 0% 5 3.0%CMBS 0% 0% 3 3.0%CLO 0% 1% 2 4.2%Private placements 0% 0% 1 3.5%Old portfolio 100% 100% 7.15 1.7%

Optimised portfolio 7.17 1.7%Source: RBS Credit Strategy

Potential solutions include:

Increasing holdings of liquid assets

Changing liabilities structure (target funds)

Charging fees (bid-ask or %) to withdraw funds

Rationing withdrawals or increasing delay

71% of investors in our survey were trying to manage their liquidity risk

Portfolio liquidity optimisation: reducing the weight of IG corporate bonds while increasing the weight of sovereigns and adding a higher yielding bucket to achieve similar yield with higher portfolio liquidity

25Source: RBS Credit Strategy, Markit, Bloomberg. RBS JBI is an indicator of relative value of credit based on valuations, fundamentals, investor/issuer behaviour.

Vulnerable areas: High yield markets

0%

50%

100%

150%

200%

250%

300%

350%

400%

01 02 03 04 05 06 07 08 09 10 11 12 13 14

USEurope

Overvalued

Undervalued

RBS Junk Bubble Indicator (JBI) shows that European HY is no longer cheap

26

Flows of funds: Highest volatility in retail/HY segments

Source: RBS Credit Strategy, AMG US cumulative fund flows

-50

0

50

100

150

200

250

300

350

400

Jun 2010 Dec 2010 Jun 2011 Dec 2011 Jun 2012 D ec 2012 Jun 2013 Dec 2013 Jun 2014-10

0

10

20

30

40

50

60

70

80

Equity

Corp IG

Corp HY (RHS)

Loans (RHS)

Euro debt crisis

Yellen on HY

T aper Tantrum

27

The dangers of deflation: Small firms with high leverage will suffer

There is a weak tail of periphery firms with high leverage Share of listed companies by Net Debt/EBITDA, % total firms

Source: RBS Credit Strategy, Bloomberg

Default rates are low, but bad loans are rising European HY default rates vs average bank NPL%

Source: RBS Credit Strategy, Moody’s, Bloomberg, bank filings

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

U K Ire Fra Ger Ita Esp Gre Por

<0 0-1 1-2 2-3 3-4 4-5 >5

0%

2%

4%

6%

8%

10%

12%

14%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

HY default rates Average bank NPL%

28

Vulnerable areas: Contingent capital instruments

…but do expect a steep drop when a conversion occurs How do you think the market will react to a conversion?

Source: RBS Credit Strategy

Investors are searching for yield Why are you buying cocos?

Source: RBS Credit Strategy

Investors are asking for more standardisation. Real money demand could retreat on recent restrictions

Yield is the top reason why people buy cocos, despite heavy losses expected upon trigger event

0%

10%

20%

30%

40%

50%

60%

70%

80%

Yield Conversion isunlikely

Lack ofalternat ives

Cheap vs risks

0

10

20

30

40

50

60

70

0 -2 -4 -6 -8 -10 -12 -14 -16 -18 -20

Avg expected drop: -15%

% answers

But high tail risk

Coco market price drop following a conversion

29

Cocos: Large divergence in conversion/cancellation risks

Source: RBS Credit Strategy; based on model estimates for a 7% conversion trigger and an 8.5% cancellation threshold

Conversion and coupon cancellation probabilities

IntesaBBVA

Barclays

SocGenDB

Nationwide

Credit SuisseCredit Ag Group

UniC redit

UBS

Danske

Lloyds

Santander

NordeaKBCHSBC

0%

5%

10%

15%

0% 1% 2% 3% 4% 5% 6% 7% 8% 9% 10%

Probability of >1 cancellation in 5 years

Probability of conversion in 5 years

High earnings volat ility, weak capital

Low earnings volatility, strong capital High earnings volatility, strong capital

Low earnings volatility, weak capital

30

Vulnerable areas: Credit ETFs

ETFs own a larger share of the credit market now Corporate bond ownership in the US, % total

Source: RBS Credit Strategy, Federal Reserve

Liquidity mismatches are rising Days for the full liquidation of credit mutual funds & ETFs

Source: RBS Credit Strategy, IMF

0

10

20

30

40

50

60

70

2007 2008 2009 2010 2011 2012 2013 2014

U.S. corporate bond total

U.S. high yield7-day lim it for redemption payments

0%

1%

2%

3%

4%

5%

2006 2007 2008 2009 2010 2011 2012 20130%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%Money market funds Closed-end funds

ETFs Mutual funds (RHS)

31

1. Trading liquidity is low in corporate bonds. It has declined by around 70% since the crisis. Liquidity remains good on low-risk government bonds.

2. We measure trading liquidity using a combination of transaction costs, volumes and dealers’ inventories

3. Liquidity is polarised across areas of the bond market: few bonds trade every day, 80-90% do not

4. Are investors compensated for taking liquidity risk? Various indicators suggests they aren’t. Liquidity is a risk, no longer an opportunity

5. Which areas and instruments are most vulnerable? The low-end of the high yield market is fundamentally weak and exposed to deflation. It is also a highly retail- held market. Contingent capital instruments also bear strong negative convexity and lack standardisation, and are not priced according to risks

6. Is liquidity risk overstated? 84% of investors in our survey think lack of liquidity is a potential systemic risk for credit markets

7. The asset management industry can resist shocks, but some products may be vulnerable (e.g. credit ETFs)

32

Eurozone: Why liquidity will get worse

33

Banking systems: Euro area vs US

Source: RBS Credit Strategy, Bank of Italy, ECB, IMF, World Bank, FRED

5,605 - Number of banks - 5,783

3.1x - Bank assets/GDP - 0.8x

37 - Number of branches - 35 per 100,000 adults

22% - Bonds/total debt - 52%

16% - Mkt share of top 5 banks - 33%

€1,041bn - NPLs - $200bn

10.9% - NPLs/GDP - 1.2%

USEuro area

34

Stress test: Many passing banks are still weak

44% of banks failed or passed narrowly % by number and by total EU banking assets

Source: RBS Credit Strategy, ECB

Austria, UK and Germany have more narrow passes Assets as % of total banking system assets in the country

Source: RBS Credit Strategy, ECB

0%

10%

20%

30%40%

50%

60%

70%80%

90%

100%

Gre

ece

Cyp

rus

Aus

tria

UK

Italy

Bel

gium

Slo

veni

aP

ortu

gal

Ger

man

yIre

land

Fran

ceLa

tvia

Spa

inP

olan

dN

ethe

rland

sD

enm

ark

Finl

and

Hun

gary

Luxe

mbo

urg

Mal

taN

orw

aySw

eden

Fail Pass narrowly Pass

Narrow pass24%

(20% by total assets)

Pass56%

(77% by total assets)

Fail20%

(3% by total assets)

25

2969

35

Too big to fail has not gone awayBank asset size / GDP

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

200%

Dan

ske

UBS C

S

ING

Ban

k

San

tand

er

Rab

oban

k

HS

BC

Cre

dit A

g

BNP

Bar

clay

s

SEB

DB

KB

C

Soc

Gen

Uni

cred

it

BES

RZB

JPM

BAC C

iti

GS

MS

Source: RBS Credit Strategy, Bloomberg, company filings

36

0

10

20

30

40

50

60

70

80

Museums High schools Secondaryschools

Primaryschools

Pharmacies Kindergartens Hotels Bankbranches

Costs are still high

Source: RBS Credit Strategy, OECD, Istat

Number of branches per 1,000 people, Italy

37

Interconnectedness: Cross-holdings in Europe’s banking system

Source: RBS Credit Strategy, Bloomberg, company filings. Red = bank, Grey = sovereign, Blue = other

3.15%

Mediobanca8.7% UniCredit

Generali

12.2%

IntesaMonte

Groupama4.9%

Mediolanum

3.4%Credit AgricoleSocGen

0.52%

Natixis AM

AXA 0.52%

BNP

0.1%0.34%

Toro

1.4%1.3%

100%

0.10%

0.6%

2.45%

4.5%

Libya

2.6%

SantanderCredit Suisse

3.65%

France 2.51%

Deutsche Bank1.21%

0.01%

Commerzbank

0.19%

Allianz

Germany

Italy

17%

2.27%

2.28%

Bankinter

0.15%

2.8%UBS

Singapore

6.4%

Norway

3.26%

BBVA

0.22%

6.43%

Abu Dhabi

POP

State Street

0.14%

Caixa Geral4.92%

Portugal Telecom

0.16%

Telefonica

RepsolCaixabank

2.81%

11.6%

5.6%

5.75%CRH

4%

Veolia

5%

IberdrolaQatar9.42%

Gas Natural

Caixa Holdings34.6%

1.7%

BlackRock6.44%

0.07%

1.18%

9.88%

Fondo Strategico

77.7%

2.57%

38

Current leverage ratio requirements are too low

Bank losses in previous crises Losses as % of loans and assets

Source: RBS Credit Strategy, Bloomberg, Company filings

European banks are generally between 3-4% capital Leverage ratio, Q4 2013

Source: RBS Credit Strategy, Company filings. Using our estimates for Intesa and UniCredit

We estimate that banks need to reach a leverage ratio of 5.8% to insulate sovereigns from the cost of a crisis

Bail-in is only useful for idiosyncratic losses. 3% leverage ratio is insufficient

0%

5%

10%

15%

20%

AIB

Ang

lo

NB

G

Bank

ia

Amag

Mon

te

HB

OS ML

BoI

WaM

u

B&

B

Wac

h

Nro

ck

SN

S

UB

S

Dex

ia

Losses as % initial loans Losses as % initial assets

0%

1%

2%

3%

4%

5%

6%

BBV

A

Inte

sa

San

tand

er

Rab

oban

k

Uni

cred

it

KBC

Nor

dea

ING

Ban

k

Cre

dit A

g G

roup

BN

P

Soc

Gen

AB

N

Lloy

ds

UB

S

CM

ZB

Dan

ske

DB

Bar

clay

s

CS

Leverage ratio

39

Bank capital is near a 200-year low. More capital = less liquidity…

Source: RBS Credit Strategy, FDIC, Historical Statistics of America

0%

10%

20%

30%

40%

50%

60%

70%

1834 1844 1854 1864 1874 1884 1894 1904 1914 1924 1934 1944 1954 1964 1974 1984 1994 2004

Book value of equity / total assets for US banks

40

Capitalism without capital: The RWA optimisation arbitrage

Source: RBS Credit Strategy, Bloomberg

Large banks have optimised risk weights, but absolute capital levels remain low

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0 200 400 600 800 1,000 1,200 1,400 1,600 1,800 2,000

Credit Ag

HSBC

BNP

DB

Barclays

Soc Gen

Santander

BPCELloyds

UBSNordeaCS

UniCredit

ING

BBVA

Intesa

Rabo

Natixis

DanskeABN

SHSEB

PohjolaNwideDeka

LBBWDZ

Balance sheet size, EUR bn

RWA % total

41

Is more stimulus a solution?

Source: RBS Credit Strategy, Bloomberg, Federal Reserve, ECB, Bank of Japan, Bank of England

Central bank assets, $tn

0

2

4

6

8

10

12

14

16

18

2007 2008 2009 2010 2011 2012 2013 Now 2015E

BoE

BoJ

EC B

Fed

PBoC

42

The QE infinity trap: Further easing expectations can delay investment

Tighter fiscal policy than when the US and Japan did QE Government deficit, % GDP

Source: RBS Credit Strategy, IMF

Drops in interest rate do not seem to boost investment Change in US corporate investment after certain events, %

Source: RBS Credit Strategy, S.P. Kothari, J. Lewellen, J. Warner, the Economist (data from 1952 onwards)

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

1 2 3 4 5 6Quarters after event

1 ppt decrease in interes t rates

10% increase in profits10% increase in return to shareholders

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%

2000 2002 2004 2006 2008 2010 2012 2014

Euro area USJapan

IMF forecas ts

Start of Fed QE

Start of ECB QE?

Start of BoJ QE

BoJ QE expansion

(Abenomics)

BoJ QE expans ion

43

The credit supercycle

Source: RBS Credit Strategy, ECB, FRED, Bloomberg

?

0

10

20

30

40

50

60

70

52 54 56 58 60 62 64 66 68 70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 14

US GDPUS credit market debtEuropean credit m arket debt

Com petition & credit control introduced / Bretton Woods breaks down

Big Bang (UK) Glass-Steagall Act repealedFinancial crisisQuantitative eas ing

$tn

You are here

Asset bubbles

Deflation

44

Source: Google images

Conclusions: Learn to live with low liquidity

1. The size and shape of bond market has changed. There are more bonds, less trading liquidity and more leveraged products

2. Bond markets are vulnerable to policy normalisation in the US and UK, and investors are not paid for liquidity risk. Standardising bond markets will take time

3. European banks are still weak and will remain focused on strengthening capital, and liquidity will remain scarce for now

4. Investors should learn to live with low liquidity, adjusting their asset mix and liabilities structure

45

Source: Google images

BibliographyBank of England | Financial Stability Report, June 2014

BlackRock | Setting New Standards: The Liquidity Challenge II, May 2013

International Monetary Fund | 2014 Article IV Consultation with the United States of America, Concluding Statement of the IMF Mission, June 2014

M&G Bond Vigilantes | Corporate bond market liquidity – flush or flushed?, 4 December 2012

ESMA | Transparency of corporate bond, structure finance product and credit derivatives markets, 10 July 2009

SEC Fixed Income Roundtable | Michael A. Goldstein: Corporate Bonds

Biais, B.; Declerck, F. (2013), Liquidity, Competition & Price Discovery in the European Corporate Bond Market, Toulouse School of Economics

Chen, G.; Cui, R.; He, Z.; Konstantin, M. (2013), Quantifying Liquidity and Default Risks of Corporate Bonds over the Business Cycle, Chicago Booth

Dick-Nielsen, J. (2013), Dealer Inventory and the Cost of Immediacy, Copenhagen Business School

Dick-Nielsen, J.; Feldhütter, P.; Lando, D. (2012), Corporate bond liquidity before and after the onset of the subprime crisis, Journal of Financial Economics 103

Ejsing, J. W.; Sihvonen, J. (2009), Liquidity premia in German government bonds, Swiss National Bank

Fisher, R. W. (2014); Monetary Policy and the Maginot Line, Federal Reserve Bank of Dallas

Gallo, A. (2014); Fed has grown complacent on credit market risk, Financial Times

Scott-Quinn, B.; Cano, D., European Corporate Bond Trading – the role of the buy-side in pricing and liquidity provision

Schultz, P. (1998), Corporate Bond Trading Costs and Practices: A Peek Behind the Curtain, University of Notre Dame

Singh, M. (2013), Collateral and Monetary Policy, IMF Working Paper

Carroll, C.D.; Slacalek, J. and Tokuoka, K. (2014), The distribution of wealth and the MPC: Implications of new European data, ECB Working Paper Series No 1648

Gallo, A. (2014), Regulators must act on coco bond risks, Financial Times

Gallo, A. (2014), A QE Boost for business lending, WSJ

46

© Copyright 2014 The Royal Bank of Scotland plc and affiliated companies ("RBS"). All rights reserved.

This Material was prepared by the legal entity named on the cover or inside cover page. It is provided for informational purposes only and does not constitute an offer to sell or a solicitation to buy any security or other financial instrument. While based on information believed to be reliable, no guarantee is given that it is accurate or complete. While we endeavour to update on a reasonable basis the information and opinions contained herein, there may be regulatory, compliance or other reasons that prevent us from doing so. The opinions, forecasts, assumptions, estimates, derived valuations and target price(s) contained in this Material are as of the date indicated and are subject to change at any time without prior notice. The investments referred to may not be suitable for the specific investment objectives, financial situation or individual needs of recipients and should not be relied upon in substitution for the exercise of independent judgement. The stated price of any securities mentioned herein is as of the date indicated and is not a representation that any transaction can be effected at this price. Neither RBS nor other persons shall be liable for any direct, indirect, special, incidental, consequential, punitive or exemplary damages, including lost profits arising in any way from the information contained in this Material. This Material is for the use of intended recipients only and the contents may not be reproduced, redistributed, or copied in whole or in part for any purpose without RBS' prior express consent. In any jurisdiction in which distribution to private/retail customers would require registration or licensing of the distributor which the distributor does not currently have, this Material is intended solely for distribution to professional and institutional investors. RBS usually makes a market in fixed income and equity securities of issuers discussed in this report and usually deal as a principal in these securities.

THIS MATERIAL IS CLASSIFIED AS INVESTMENT RESEARCH AS DEFINED BY THE FINANCIAL CONDUCT AUTHORITY.

Analyst Certification: The research analyst or analysts responsible for the content of this research report certify that: (1) the views expressed and attributed to the research analyst or analysts in the research report accurately reflect their personal opinion(s) about the subject securities and issuers and/or other subject matter as appropriate; and, (2) no part of his or her compensation was, is or will be directly or indirectly related to the specific recommendations or views contained in this research report. On a general basis, the efficacy of recommendations is a factor in the performance appraisals of analysts. RBS policy prohibits its analysts, professionals reporting to analysts and members of their households from owning securities and from serving as an officer, director, advisory board member or employee of any company in the analyst's area of coverage.

Australia: This Material is issued in Australia by The Royal Bank of Scotland plc (ABN 30 101 464 528), 88 Phillip Street, Sydney NSW 2000, Australia which is authorised and regulated in Australia by the Australian Securities and Investments Commission (AFS License No. 241114) and the Australian Prudential Regulation Authority. Canada: The securities mentioned in this Material are available only in accordance with applicable securities laws and many not be eligible for sale in all jurisdictions. Persons in Canada requiring further information should contact their own advisors. EEA: This Material constitutes "investment research" for the purposes of the Markets in Financial Instruments Directive and as such contains an objective or independent explanation of the matters contained in the Material. Any recommendations contained in this Material must not be relied upon as investment advice based on the recipient's personal circumstances. In the event that further clarification is required on the words or phrases used in this Material, the recipient is strongly recommended to seek independent legal or financial advice. Denmark: The Royal Bank of Scotland N.V. is authorised and regulated in the Netherlands by De Netherlandsche Bank. In addition, The Royal Bank of Scotland N.V. Danish branch is subject to local supervision by Finanstilsynet, The Danish Financial Supervisory Authority. Hong Kong: To the extent this Material constitutes Type 4 regulated activity (advising on securities) and not within ancillary activities as defined in Part 1, Schedule 5 of the Securities and Futures Ordinance (Cap. 571 of the Laws of Hong Kong), this Material must not be distributed or transmitted into or within Hong Kong Special Administrative Region of the People's Republic of China. India: Shares traded on stock exchanges within the Republic of India may only be purchased by different categories of resident Indian investors, Foreign Institutional Investors registered with The Securities and Exchange Board of India ("SEBI") or individuals of Indian national origin resident outside India called Non Resident Indians ("NRIs"). Any recipient of this Material wanting additional information or to effect any transaction in Indian securities or financial instrument mentioned herein must do so by contacting a representative of RBS Equities (India) Limited. RBS Equities (India) Limited is a subsidiary of The Royal Bank of Scotland N.V.. Italy: Persons receiving this Material in Italy requiring further information should contact The Royal Bank of Scotland N.V. Milan Branch. Japan: This report is being distributed in Japan by RBS Securities Japan Limited to institutional investors only. Malaysia: RBS research, except for economics and FX research, is not for distribution or transmission into Malaysia. Netherlands: the Authority for the Financial Markets ("AFM") is the competent supervisor. Russia: This Material is distributed in the Russian Federation by RBS and "The Royal Bank of Scotland" ZAO (general banking license No. 2594 issued by the Central Bank of the Russian Federation, registered address: building 1, 17 Bolshaya Nikitskaya str., Moscow 125009, the Russian Federation), an affiliate of RBS, for information purposes only and is not an offer to buy or subscribe or otherwise to deal in securities or other financial instruments, or to enter into any legal relations, nor as investment advice or a recommendation with respect to such securities or other financial instruments. This Material does not have regard to the specific investment purposes, financial situation and the particular business needs of any particular recipient. The investments and services contained herein may not be available to persons other than 'qualified investors" as this term is defined in the Federal Law "On the Securities Market". Singapore: This Material is distributed in Singapore by The Royal Bank of Scotland plc, Singapore branch ("RBS plc Singapore"), Level 26, One Raffles Quay, South Tower, Singapore 048583, which is regulated by the Monetary Authority of Singapore. Singapore recipients should contact RBS plc Singapore at +65 6518 8888 for additional information. This Material and the equity securities, investments or other financial instruments referred to herein are not in any way intended for, and will not be available to, investors in Singapore unless they are accredited investors, expert investors and institutional investors (as defined in Section 4A(1) of the Securities and Futures Act (Cap 289) of Singapore (“SFA”). Further, without prejudice to any of the foregoing disclaimers, where this material is distributed to accredited investors or expert investors, RBS plc Singapore is exempted by Regulation 35 of the Financial Advisers Regulations (“FAR”) from the requirements in Section 36 of the Financial Advisers Act (Cap 110) of Singapore (“FAA”) mandating disclosure of any interest in securities referred to in this material, or in their acquisition or disposal. Recipients who are not accredited investors, expert investors or institutional investors should seek the advice of their independent financial advisors prior to making any investment decision based on this document or for any necessary explanation of its contents. South Korea: This Material is being distributed in South Korea by, and is attributable to, RBS Asia Limited (Seoul) Branch which is regulated by the Financial Supervisory Service of South Korea. Thailand: Pursuant to an agreement with Asia Plus Securities Public Company Limited (APS), reports on Thai securities published out of Thailand are prepared by APS but distributed outside Thailand by RBS Bank NV and affiliated companies. Responsibility for the views and accuracy expressed in such documents belongs to APS. Turkey: The Royal Bank of Scotland N.V. is regulated by Banking Regulation and Supervision Authority (BRSA). UAE and Qatar: This Material is produced by The Royal Bank of Scotland N.V and is being distributed to professional and institutional investors only in the United Arab Emirates and Qatar in accordance with the regulatory requirements governing the distribution of investment research in these jurisdictions. Dubai International Financial Centre: This Material has been prepared by The Royal Bank of Scotland N.V. and is directed at "Professional Clients" as defined by the Dubai Financial Services Authority (DFSA). No other person should act upon it. The financial products and services to which the Material relates will only be made available to customers who satisfy the requirements of a "Professional Client". This Material has not been reviewed or approved by the DFSA. Qatar Financial Centre: This Material has been prepared by The Royal Bank of Scotland N.V. and is directed solely at persons who are not "Retail Customer" as defined by the Qatar Financial Centre Regulatory Authority. The financial products and services to which the Material relates will only be made available to customers who satisfy the requirements of a "Business Customer" or "Market Counterparty". United Kingdom: The Royal Bank of Scotland plc is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. United States of America: This Material is intended for distribution only to "major institutional investors" as defined in Rule 15a-6 under the U.S. Exchange Act of 1934 as amended (the "Exchange Act"), and may not be furnished to any other person in the United States. Each U.S. major institutional investor that receives these Materials by its acceptance hereof represents and agrees that it shall not distribute or provide these Materials to any other person. Any U.S. recipient of these Materials that wishes further information regarding, or to effect any transaction in, any of the securities discussed in this Material, should contact and place orders solely through a registered representative of RBS Securities Inc., 600 Washington Boulevard, Stamford, CT, USA. Telephone: +1 203 897 2700. RBS Securities Inc. is an affiliated broker-dealer registered with the U.S. Securities and Exchange Commission under the Exchange Act, and a member of the Securities Investor Protection Corporation (SIPC) and the Financial Industry Regulatory Authority (FINRA).

Material means all research information contained in any form including but not limited to hard copy, electronic form, presentations, e-mail, SMS or WAP.

Disclosures regarding companies covered by us can be found on our research website. Please use https://strategy.rbsm.com/disclosures/default.aspx for Research.

Our policy on managing research conflicts of interest can be found here https://strategy.rbsm.com/Strategy/ConflictsPolicy.aspx.Should you require additional information please contact the relevant research team or the author(s) of this Material.