the cruise market and uk perspective by william gibbons director passenger shipping association...

TRANSCRIPT

The Cruise Market The Cruise Market and UK Perspectiveand UK PerspectiveThe Cruise Market The Cruise Market

and UK Perspectiveand UK PerspectiveByBy

William GibbonsWilliam Gibbons

DirectorDirector

Passenger Shipping AssociationPassenger Shipping Association

Marketing Director Marketing Director

European Cruise CouncilEuropean Cruise Council

ByBy

William GibbonsWilliam Gibbons

DirectorDirector

Passenger Shipping AssociationPassenger Shipping Association

Marketing Director Marketing Director

European Cruise CouncilEuropean Cruise Council

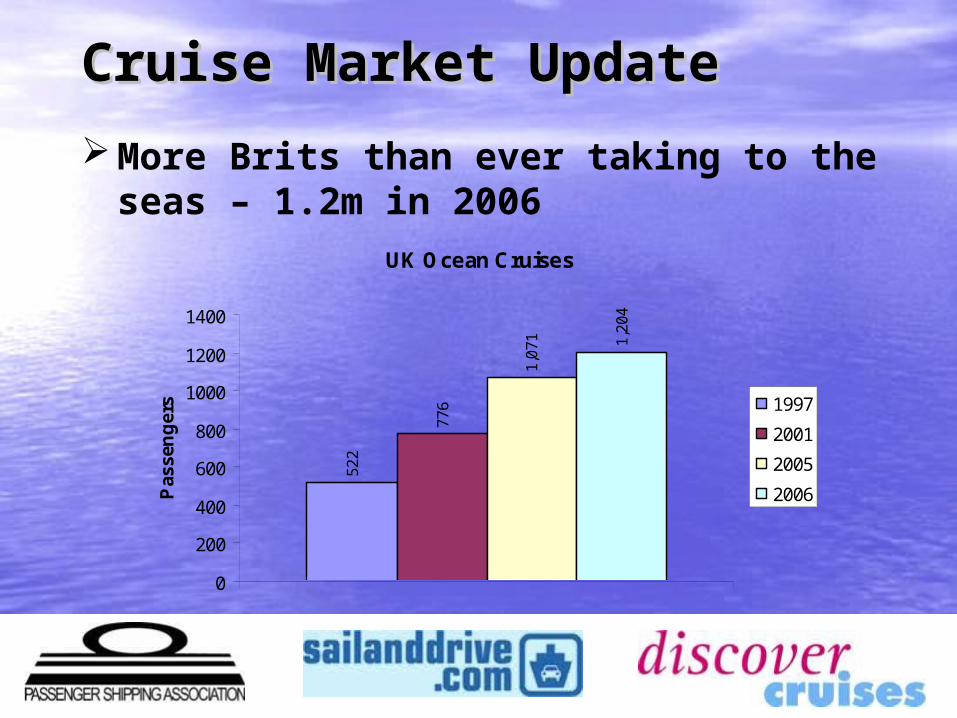

Cruise Market UpdateCruise Market Update

More Brits than ever taking to the seas – 1.2m in 2006

UK Ocean Cruises

522

776

1,07

1 1,20

4

0

200

400

600

800

1000

1200

1400

Pas

sen

ger

s 1997

2001

2005

2006

EX-UK Growth EX-UK Growth

Cruises taken from UK ports up 12% - 450,000

Trend set to continue with increased ex-UK capacity on its way in 2007.2007 – 500,0002008 – 700,000

Fly-CruiseFly-Cruise Fly-cruise market increased

by 13% - to 753,000 Brits

Another trend that looks set to continue with increased capacity:2006 – Island Cruises2007 – Ocean Village

Two, Thomson Calypso

Destinations – EX-UKDestinations – EX-UK

107

67

57

51

50

14

28

18

9

130

88

59

54

51

15

26

18

10

Mediterranean

UK - Western Europe

Norway

Baltic

Altantic Islands

CaribbeanOther areas (Greenland, Iceland,

Arctic, USA, etc.)Line Voyages

Charters

Passengers (in 000s)

2005

2006

Destinations – Fly-Cruise Destinations – Fly-Cruise

263

202

18

46

34

26

18

60

322

195

40

35

35

29

25

72

Mediterranean

Caribbean, inc Bermuda

Indian Ocean, Red Sea, P Gulf

Atlantic Islands

West Coast, Mexico, Hawaii, P Canal

Alaska

Transatlantic - repositioning

Other areas

Passengers (in 000s)

2005

2006

BALTICBALTICEach Passenger visit at a European Port Embarkation and visiting - Expenditure €100.

Average Revenue Per Passenger - £1,447.

Average Revenue Per Diem - £122.

Norway – (£156.)

Average length of Cruise from UK 12days

Growth of UK PortsGrowth of UK PortsPassengers embarking in the UK grew

15% to 576,000- Non-UK residents accounted for

127,000, a growth of 27%

Ports of call passengers to UK ports grew 22% - to 392,000

Total value of cruise passenger expenditure in the UK – over £197m

Contribution of cruiseContribution of cruise

tourism to the tourism to the economieseconomies

of Europeof Europe

GP Wild/ BREA – Undertook StudyGP Wild/ BREA – Undertook Study

Over 3.1m European residents booked cruises – Over 3.1m European residents booked cruises – 23% of cruise tourists (passengers) worldwide23% of cruise tourists (passengers) worldwide

Over 2.8m cruise tourist embarked in Europe – Over 2.8m cruise tourist embarked in Europe – 90% were European nationals90% were European nationals

Majority visited Mediterranean, Baltic and other Majority visited Mediterranean, Baltic and other European regions generating 13.1m visits in European regions generating 13.1m visits in EuropeEurope

Major Highlights in 2005Major Highlights in 2005

As a result of European cruise operations As a result of European cruise operations and investment in new cruise ships, key and investment in new cruise ships, key economic impacts (direct, indirect, induced) economic impacts (direct, indirect, induced) throughout Europe in 2005 include:throughout Europe in 2005 include:

€€8.3 billion in direct spending by lines 8.3 billion in direct spending by lines and passengersand passengers

€€19.1 billion in total output19.1 billion in total output Over 187,000 jobsOver 187,000 jobs €€6.0 billion employee remuneration6.0 billion employee remuneration

Major Highlights in 2005Major Highlights in 2005

Country Impacts - 2005Country Impacts - 2005

CountryCountry Spending Spending €m€m

Total JobsTotal Jobs Compensation Compensation €m€m

ItalyItaly 2,5012,501 61,44561,445 1,8101,810

UKUK 1,6861,686 37,31937,319 1,4571,457

GermanGermanyy

1,0731,073 19,96919,969 725725

SpainSpain 683683 13,94013,940 422422

FinlandFinland 621621 10,20510,205 371371

FranceFrance 536536 7,2657,265 310310

Top sixTop six 7,1007,100 150,143150,143 5,0955,095

TotalTotal 8,3268,326 187,252187,252 6,0176,017

Cruise Tourism by Destinations Cruise Tourism by Destinations 20052005

CountryCountry Cruise touristsCruise tourists Market Share Market Share (%)(%)

ItalyItaly 3,028,2243,028,224 23.023.0

SpainSpain 2,627,7262,627,726 20.020.0

GreeceGreece 2,069,7672,069,767 15.715.7

FranceFrance 1,034,0921,034,092 7.97.9

NorwayNorway 691,209691,209 5.35.3

PortugalPortugal 498,431498,431 3.83.8

MaltaMalta 336,400336,400 2.62.6

United KingdomUnited Kingdom 322,000322,000 2.42.4

SwedenSweden 301,826301,826 2.32.3

EstoniaEstonia 249,102249,102 1.91.9

Western Europe as a Source Western Europe as a Source Market 2003-06Market 2003-06

Country 2003Group Total

(1,000’s Pax)

2004Group Total

(1,000’s Pax)

2005Group Total

(1,000’s Pax)

2006Group Total

(1,000’s Pax)

2005/06% Change

UK 964 1,029 1,071 1,214 13

Germany

537 583 639 700 10

Italy 346 400 514 559 9

Spain 307 300 379 378 0

France 212 222 233 265 14

Other 305 300 291 339 16

Total 2,671 2,835 3,126 3,455 11

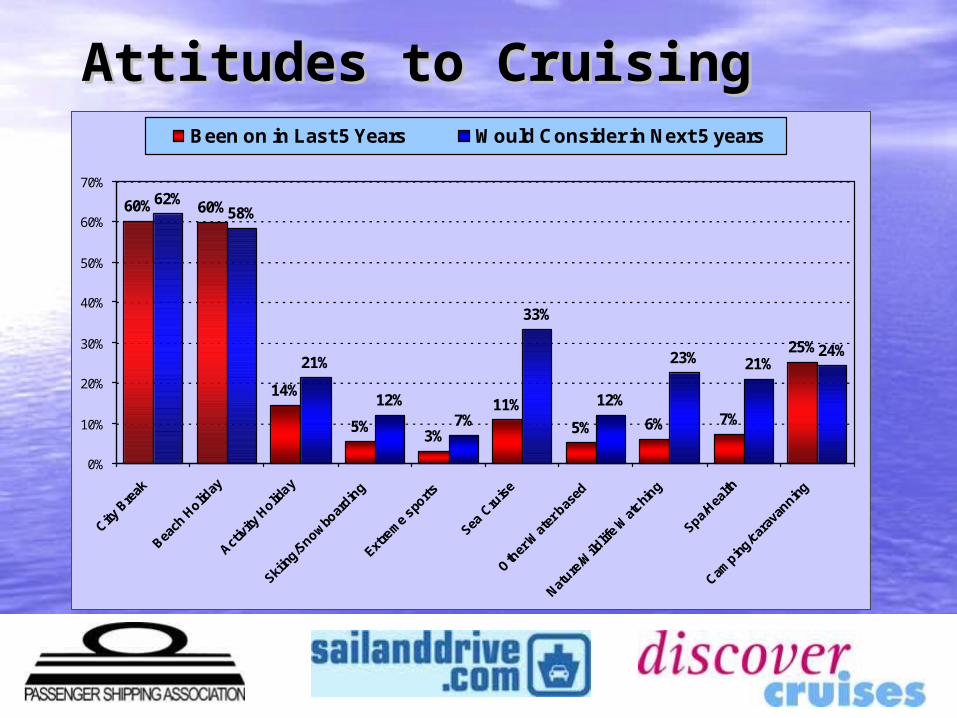

Attitudes to CruisingAttitudes to Cruising

Research into people and their attitudes to cruising

Who would consider a cruise – and if not, why not?

What are the barriers to taking a cruise?

Attitudes to CruisingAttitudes to Cruising

60% 60%

14%

5%11%

5% 6% 7%

25%

62%58%

21%

12%7%

33%

12%

23% 21%24%

3%

0%

10%

20%

30%

40%

50%

60%

70%

City B

reak

Beach

Holid

ay

Activ

ity H

oliday

Skiin

g/Snow

boar

ding

Extre

me

sports

Sea C

ruis

e

Oth

er W

ater

bas

ed

Nature

/Wild

life

Wat

ching

Spa/Hea

lth

Campin

g/car

avan

ning

Been on in Last 5 Years Would Consider in Next 5 years

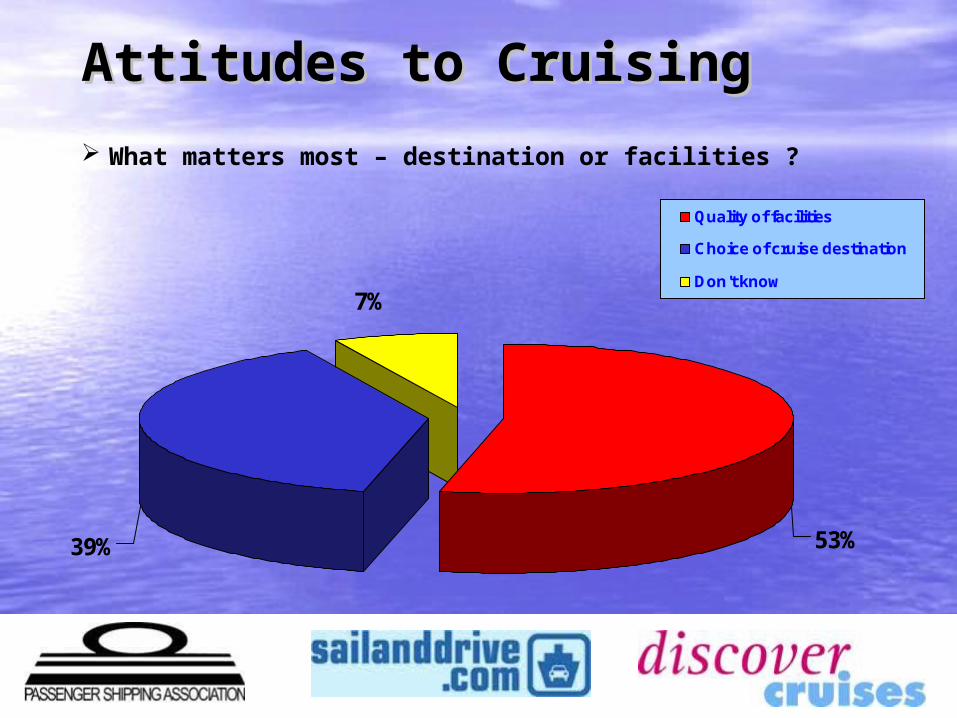

Attitudes to CruisingAttitudes to Cruising

What matters most – destination or facilities ?

7%

53%39%

Quality of facilities

Choice of cruise destination

Don't know

Attitudes to CruisingAttitudes to Cruising

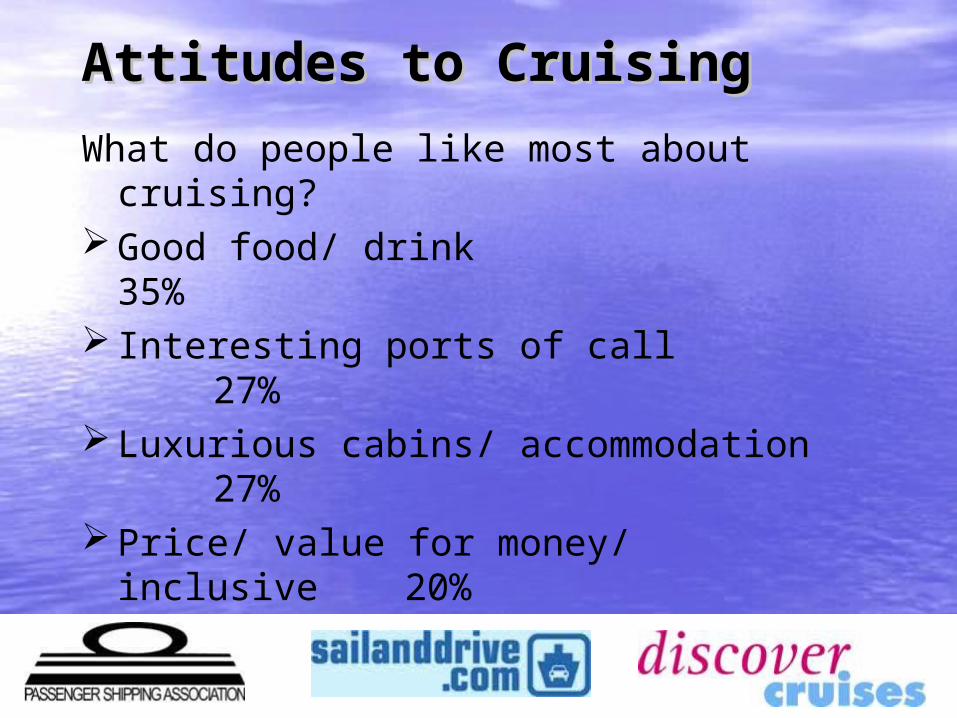

What do people like most about cruising?

Good food/ drink35%

Interesting ports of call27%

Luxurious cabins/ accommodation27%

Price/ value for money/ inclusive20%

Attitudes to CruisingAttitudes to Cruising

What are the barriers to cruising?

Sea sickness/ bad weather 32%Being cooped up/claustrophobic

31%Not liking other passengers 25%

These barriers drop considerably once a person has actually taken a cruise

LUXURY LUXURY CRUISINGCRUISING

The Exclusive Collection – an alliance of nine ships

of excellence

Nearly 20,000 passengers are carried by the ultra

luxury lines – 1.6% of the UK market

Luxury passenger numbers have doubled

since 2002

SPECIALIST SPECIALIST CRUISINGCRUISING

Specialist Cruise Collection – an alliance of

11 cruise lines

Unique itineraries to destinations best

experienced by sea

A 27% growth in 2006

2008 ONWARDS2008 ONWARDS Boom in EX-UK Cruising

Cunard – Victoria

P&O – Ventura

Royal Caribbean Cruise Line – Liberty of the Seas

Fred Olsen – Balmoral

NCL – Jade

MSC – Armonia

(Including 5 Baltic Capital Cruises)

Carnival Cruise Line – Carnival Splendour (5 Cruises)

AND THE FUTURE…AND THE FUTURE…

1.3 million ocean cruise passengers in 2007

1.5 million ocean cruise passengers by 2008

Sheer diversity of cruising outperforming land based holidays – ranging from ships carrying up to 4,400 passengers to 49 passengers

39 brands represented by the PSA in the UK – more than any other country

There really is something for everyone!