the current prospects for risk-sharing sukuk - tkbb · the current prospects for risk-sharing sukuk...

TRANSCRIPT

The Current Prospects for Risk-Sharing Sukuk

Date : 11 September 2013

Presented by : Rafe Haneef, CEO of HSBC Amanah Malaysia Berhad

I. The Sukuk Market

3

Evolution of the International Sukuk Market Stellar growth however all landmarks achieved so far involve risk-transfer

Size of Global Sukuk Market*

(USD bn) 61.9 4.6 10.7 134.6 212.6 107.9 225.8

2002 Government of

Malaysia

USD 600mn 5 year Sukuk

1st global sovereign Sukuk

2006 Khazanah Nasional

USD 750mn 5 year Exchangeable Sukuk

1st exchangeable Sukuk

2012 Government of

Dubai

USD 600mn / 650mn 5 / 10 year Dual-tranche Sukuk

1st unrated 10-year Sukuk

2013 Saudi Electricity

Company

USD 2bn / 2bn 10 / 30 year Dual-

tranche Sukuk

1st international 30 year Sukuk

2003 State of Qatar

USD 700mn 7 year Sukuk

1st GCC Sukuk

1st subordinated bank capital Sukuk

2012 Abu Dhabi Islamic

Bank

USD 1bnTier 1 Perpetual Sukuk

1st perpetual Sukuk

2010 Nomura

USD 100mn 2 year Sukuk

1st Sukuk by Japanese issuer

2009 International

Finance Corp.

USD 100mn 5 year Sukuk

1st Sukuk by non-Islamic Supranational

2004 State of Saxony-

Anhalt

EUR 100mn 5 year Sukuk

2009 GE Capital

USD 500mn 5 year Sukuk

2007 Maybank

USD 300mn 10 year Subordinated Sukuk

1st Sukuk by US issuer

1st European Sukuk

*Source: Dealogic 10th June 2013

4

Global Sukuk Market Update Some signs of risk-sharing emerging but 98% of sukuk remain risk-transfer

Source: HSBC, Dealogic 3rd September 2013

Historical Sukuk Issuance Volume Since 2008

Total Sukuk volume issued globally since 2008 has surpassed USD 160 bn

· The last USD issuance in the Sukuk market was the USD 1bn 1.535% 5 year Sukuk by the Islamic Development Bank, the only Supranational issuer to issue in Islamic format. This however is a risk transfer sukuk.

· The landmark transaction this year has been the dual-trache 10 & 30-year Sukuk for Saudi Electricity Company (SEC). This marked the first ever issuance of a 30-year Sukuk in the international debt capital markets. No risk-sharing feature though.

· Hybrid capital continues to be an important theme in the Sukuk market, with Dubai Islamic Bank issuing a US$1bn Tier-1 Sukuk in March and Bank Asya issuing a US$250m LT II Sukuk in April. This deal featured elements of risk sharing.

· Since 2010, project finance sukuk have become popular in Malaysia. Notable Sukuk deals include:

- TTM (Trans-Thai Malaysia) Sukuk Bhd (2010) – MYR 600m Sukuk with a maximum tenor of 15 years;

- Tanjung Bin Energy Issuer Bhd (2012) – MYR 3.29 billion Sukuk with a maximum tenor of 20 years;

- Kimanis Power Sdn Bhd (2012) – MYR 860 million Sukuk with a maximum tenor of 16 years; and

- TNB Northern Energy Bhd (2013) – MYR 1.625 billion Sukuk with a maximum tenor 23 years.

· These recent issues demonstrate that some elements of risk-sharing are beginning to emerge.

57% 21%

14%

8%

MalaysiaMiddle East (Excl. Saudi Arabia)Saudia ArabiaRest of the World

Volume by Region 2008-2013YTD

Volume by Currency 2008-2013YTD

55% 28%

10% 7%

MYR USD SAR Other

Volume by Tenor 2008-2013YTD

46%

10%

22%

22%

0-5 5.1-7 7.1-10 >10.1

19.5

25.8 25.5

34.0

44.9

22.2

-

10

20

30

40

50

2008 2009 2010 2011 2012 2013 YTD

USD

Bill

ions

Malaysia UAE Saudi Indonesia Qatar Turkey Others

II. Types of Sukuk

6

· Sukuk is a plural of the word sakk which means certificate, legal instrument, deed or cheque.

· Sakk may sound unfamiliar to many, but it is actually a forerunner of the word “cheque”

· It is a well-documented fact that many commercial practices and customs of the Muslim world were transmitted to medieval Europe through Islamic Spain.

· Types or classifications of Sukuk:

- Senior Unsecured Sukuk – in a winding-up, ranked junior to secured creditors but senior to equity holders

- Subordinated Sukuk – in a winding-up, ranked junior to unsecured creditors but senior to equity holders

- Secured Sukuk or asset-backed Sukuk – in winding-up, ranked senior to all creditors and equity holders

· Examples of risk sharing sukuk include:

- Project finance Sukuk

- Hybrid perpetual Sukuk

Definition and Classifications of Sukuk

Risk Transfer

Risk Transfer

Risk Sharing

III. Project Finance Sukuk

8

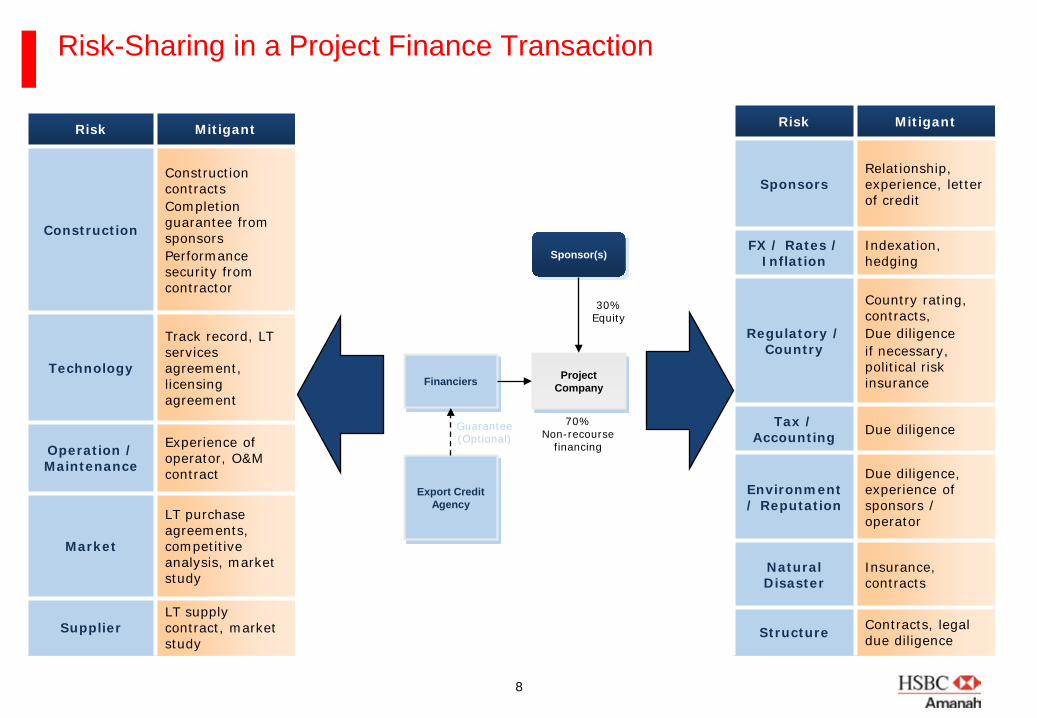

Risk-Sharing in a Project Finance Transaction

Risk Mitigant

Construction

Construction contracts Completion guarantee from sponsors Performance security from contractor

Technology

Track record, LT services agreement, licensing agreement

Operation / Maintenance

Experience of operator, O&M contract

Market

LT purchase agreements, competitive analysis, market study

Supplier LT supply contract, market study

Risk Mitigant

Sponsors Relationship, experience, letter of credit

FX / Rates / Inflation

Indexation, hedging

Regulatory / Country

Country rating, contracts, Due diligence if necessary, political risk insurance

Tax / Accounting Due diligence

Environment / Reputation

Due diligence, experience of sponsors / operator

Natural Disaster

Insurance, contracts

Structure Contracts, legal due diligence

Sponsor(s)

Project Company Financiers

Export Credit Agency

30% Equity

70% Non-recourse

financing

Guarantee (Optional)

9

Exercise of purchase undertaking

Purchase price

Case Study 1: Project Finance Sukuk Structure MYR 860 million Sukuk Issuance by Kimanis Power Sdn Bhd

Transaction flow

Cash flow

The Kimanis Sukuk structure is based on the combination of Istisna’ and Ijarah concepts

At inception, KImanis sells the project to the Trustee, acting on

behalf of the Sukuk investors, for a spot payment with deferred

delivery terms (upon completion), and the Trustee

leases the to-be project to Kimanis

Kimanis pays to the Trustee forward lease rentals during the

construction and lease rentals post-construction, which are equal to respective periodic

distribution amounts payable to the investors

At maturity, Kimanis purchases the project from the Trustee at

an exercise price pursuant to a purchase undertaking

It is a structure widely adopted for Islamic project finance

globally; however, the Sukuk might not be tradable on the

secondary market during the construction period for

investors wishing to meet global Shariah compliance

requirements

1. At Inception

Structure Breakdown

2. During Construction & Delivery

4. At Maturity

Sukuk Investors

Trustee (Purchaser,

Lessor)

Kimanis (Seller, Lessee)

Sukuk issue (directly from Kimanis)

Sukuk proceeds

Istisna’ purchase of plant (delivery upon completion)

1 2

3

(Forward) lease of plant

Sukuk Investors

Trustee (Lessor)

Kimanis (Lessee)

Periodic distribution amounts Forward lease rentals

5 4

Sukuk Investors

Trustee (Seller)

Kimanis

(Obligor-Purchaser)

Sukuk redemption (directly to Kimanis)

Dissolution distribution amount

11 Sale of plant

9

Delivery of plant

3. During Operation (post-construction)

Sukuk Investors

Trustee (Lessor)

Kimanis (Lessee)

8

Lease rentals

7

6

Periodic distribution amounts

10

Exercise price

10

On 19 July 2012, Kimanis Power Sdn Bhd (“Kimanis”) priced a

highly successful MYR860 million issuance (“Sukuk”)

under their newly established MYR1.16 billion Islamic Sukuk

Programme (“Sukuk Programme”)

This landmark transaction

represents:

üFirst-ever Istisna-Ijara Ringgit-denominated Sukuk üFirst-ever project bond issued by the PETRONAS group in the power sector üHSBC’s second consecutive project bonds financing transaction with the PETRONAS Group, underlining HSBC’s dedication to committed relationships with their clients

HSBC acted as Sole

Coordinating Bank, Joint Lead Arranger, Joint Lead Manager,

Joint Shariah Advisor and Hedge Provider

Issuer Kimanis Power Sdn Bhd (“Kimanis”) Ratings AA-(IS) (MARC) Format Islamic Sukuk Programme (“Sukuk

Programme”) Programme Size MYR1,160 million Programme Tenor 16 years First Issuance under the Programme Issue Size MYR 860 million Pricing / Settlement Date

19 July / 8 August 2012

Tenor Serial tenors of 4 to 16 years Coupon / Profit 4.25% to 5.5% Governing Law Malaysian Law HSBC Role Sole Coordinating Bank, Joint Lead Arranger,

Joint Lead Manager, Joint Shariah Advisor & Hedge Provider

· Kimanis is a 60:40 joint venture between PETRONAS Gas Berhad and Sabah state owned entity NRG Consortium (Sabah) Sdn Bhd (NRG). NRG is an indirect wholly owned subsidiary of Sabah state’s investment arm Yayasan Sabah Group (YSG).

· The proceeds are to part-finance the development, design and construction of a 285-megawatt (MW) combined-cycle gas turbine power plant in Sabah by Kimanis.

· Under the IMTN Programme, Kimanis plans to issue the sukuk in two series: the first series being the MYR860 million IMTN issuance and the second series being a forward start sukuk of MYR300 million.

· The AA-(IS) (MARC) rated Sukuk Programme reflects a well-structured Power Purchase Agreement, low technology risk, expectation of adequate operating performance, limited fuel supply risk and strong commitment of project sponsors. The stable outlook reflects MARC’s expectations that the construction of the power plant would be compelted on schedule and within budget.

· The project represents the first Independent Power Producer for the PETRONAS group and forms part of PETRONAS’s strategy to develop its power generation business in Malaysia. The project also plays an important role in the Government of Malaysia’s plan to address power requirements in the state of Sabah.

· HSBC secured and executed multiple roles in this transaction despite strong competition, reflecting the close coordination and teamwork across PEF, DCM, Global Markets and Client management functions, allowing HSBC to maximise client value and deal economics.

· This landmark transaction reinforces HSBC’s position as leading provider of project bond and Islamic financing solutions in the Malaysian market. This is our third project bond in Malaysia over the last two years.

Financial Institutions (25%)Funds (21%)Government Agencies (17%)Insurance (37%)

Case Study 1: Kimanis Power Sdn Bhd MYR 860 million Sukuk issuance

Transaction Overview Breakdown by Investor Type

Transaction Highlights

11

On 6 March 2012, Tanjung Bin Energy Issuer Berhad

(“TBEIB”) successfully priced a MYR3,290 million

Islamic Medium Term Notes (“IMTN”) issuance with

tenors ranging from 5 to 20 years.

This ground breaking transaction marks the

commencement of Tanjung Bin’s expansion and serves

to strengthen Malakoff’s position as the leading

independent power producer in Malaysia and the ASEAN

region

HSBC acted as the sole coordinating bank for this

landmark non-recourse project financing for a

greenfield power plant; both for senior and junior facilities

HSBC acted as Joint

Principal Advisor, Joint Lead Arranger and Joint Lead

Manager

Issuer Tanjung Bin Energy Issuer Berhad (“TBEIB”)

Format Islamic Sukuk (Senior) Structure Sukuk Commodity Murabahah Issue Ratings AA3 (RAM) Amount MYR3,290 million Settlement Date 16 March 2012 Tenor 5 to 20 years Coupon / Profit 4.65% to 6.20% Governing Law Malaysian Law HSBC Role Joint Principal Advisor, Joint Lead Arranger &

Joint Lead Manager

· Tanjung Bin Energy issuer Berhad, a wholly owned subsidiary of Tanjung Bin Energy Sdn Bhd, who in turn is wholly owned by Malakoff Corporation Berhad, was structured as a special purpose vehicle to issue Islamic bonds for the development of the new 1,000 MegaWatt super-critical coal fired power plant.

· The Sukuk was part of a financing package which includes a senior facility of USD400 million term loan and a MYR700 million term loan and a junior facility comprising equity loans of MYR1.3 billion.

· The MYR Sukuk transaction was successfully executed through an accelerated 2 hour bookbuilding process and attracted over MYR16.9 billion in bids from a wide group of investors to arrive at an oversubscription rate of more than 5.13x over the issue size of MYR3.29 billion.

· The transaction had a balanced distribution as follows: Funds (18.7%), Insurance Companies (13.2%), Financial Institutions (39.9%0 and Government Agencies (5.0%).

· The MYR Sukuk was rated by RAM, with HSBC leading the ratings process. TBEIB was awarded a rating of AA3 from RAM reflecting the project’s high reliability and credit worthiness and setting a new benchmark for AA3-rated Malaysian project bonds.

· This ground breaking transaction is a significant milestone for Malakoff as it marks the commencement of Tanjung Bin’s expansion and serves to strengthen Malakoff’s position as the leading independent power producer in Malaysia and within the ASEAN region.

· The transaction also marks the first participation of international lender for a power project financing in Malaysia. · This transaction pioneered the Malaysian infrastructure market as the first combined MYR bond and USD loan project

financing for an IPP in Malaysia

FI (40%)Funds (19%)Insurance (13%)Government Agencies (28%)

Case Study 2: Tanjung Bin Energy Issuer Berhad MYR 3.29 billion Sukuk issuance

Transaction Overview Breakdown by Investor Type

Transaction Highlights

12

On 9 October 2011, Saudi Aramco Total Services

Company successfully issued a SAR

3.75 billion Sukuk Musharakah with a tenor of

14 years

This transaction was first project Sukuk issued in the

Kingdom of Saudi Arabia

The structure is based on an istisna contract for

construction together with a forward lease agreement.

The issuer and the obligor

(SATORP) are partners under the Musharakah agreement

and co-lessors under the forward lease agreement.

SATORP is also the

managing partner under the Musharakah agreement and

the lessee under the forward lease agreement.

Issuer Saudi Aramco Total Services Company

Format Islamic Sukuk (Senior) Structure Sukuk Musharakah Issue Ratings Not Rated Amount SAR 3.75 billion Settlement Date 9 October 2011 Tenor 14 years Coupon / Profit 6 month SAIBOR + 95 basis points Governing Law Laws of Saudi Arabia Joint lead managers and bookrunners

Deutsche Securities Saudi Arabia, Samba Capital & Invsetment Management, Saudi Fransi Capital

· The combined value of the Sukuk issuance was SAR3.75 billion (US$1 billion) and received subscription orders in excess of SAR13 billion (US$3.45 billion).

· The SATORP Sukuk was the first project Sukuk instrument in Saudi Arabia. · Pricing for the Sukuk was exceptionally tight given that the yield for the SAR1.8 billion (US$480 million) Sukuk Mudarabah

issued by Saudi International Petrochemical Company (Sipchem) in June 2010 was SAIBOR plus 1.75% per year. Despite this, the Sukuk was still heavily oversubscribed by 3.5 times.

· The offering received strong interest from financial institutions, mutual funds, insurance companies and pension funds as well as certain high net worth individuals.

· The structure is based on an istisna contract for construction together with a forward lease agreement. The issuer, Saudi Aramco Total Services Company and SATORP are partners under the Musharakah agreement and also co-lessors under the forward lease agreement. SATORP is also the managing partner under the Musharakah agreement and the lessee under the forward lease agreement.

· The proceeds of the Sukuk were used to finance SATORP’s planned crude oil refinery in Jubail. SATORP is 62.5% owned by Saudi Aramco and 37.5% owned by Total. The total cost of the Jubail project is estimated at over US$14 billion.

Case Study 3: Saudi Aramco Total Refining and Petrochemical Company (SATORP) SAR 3.75 billion Sukuk issuance

Transaction Overview

Transaction Highlights

IV. Perpetual Sukuk

14

Perpetual Mudaraba Sukuk Structure Overview

Mudaraba Capital Mudaraba Agreement

SPV (Issuer / Trustee / Rab-al-Maal)

Sukuk Proceeds Sukuk Issue

Investors

1

Obligor (Mudareb)

2

Inception Ongoing & Maturity

Mudaraba Profit (+ shortfall cover, if any) (payable if so elected by

Obligor)

SPV (Issuer / Trustee / Rab-al-Maal)

Dissolution Distribution Amount

Sukuk Redemption

Investors

9

Obligor (Mudareb)

5.1 8

Obligor’s General Pool of Assets

5.2

6 Periodic Distribution Amounts (payable if Mudaraba Profit is paid)

5.3 Excess Allocated

Reserve Account

Excess Profit

Mudaraba Assets

3 Mudaraba Capital (invested into Obligor’s Assets according to Investment Plan)

Obligor’s General Pool of Assets Mudaraba Assets

4 Muradaba Profit

7

Dissolution Mudaraba Capital (+ shortfall indemnity, if any)

Transaction Fund flow

7

~ Steps at inception ~ Steps during ongoing ~ Steps at maturity

1 4

9

3 6

Dissolution Mudaraba Capital

The first ever Tier 1 Sukuk in the international markets is based on a

Mudaraba Agreement entered into by the SPV (as Rab-al-Maal) and the Obligor (as

Mudareb), according to which the Obligor invests the Mudaraba capital (=

Sukuk proceeds) into the Obligor’s assets

The Obligor may elects not to pay a

Mudaraba profit to the SPV at its sole discretion (as long as it is not required to

make such payment due to certain conditions such as dividend pusher and stopper), in which case such Mudaraba profit is credited to a Mudaraba reserve

account

The profit sharing ratio is stipulated in the Mudaraba Agreement. If a Mudaraba

profit for the SPV is not sufficient for expected return (= periodic distribution amount), the Obligor utilise the reserve balance to cover the shortfall or, if the

reserve is not sufficient, may cover the shortfall from its own account

The Obligor may liquidate the Mudaraba

at its option If the Obligot exercises its option and the capital to be returned to

the SPV is less than the SPV’s initial capital contribution, the Obligor is

required to continue investing such capital in the Mudaraba. There is

accordingly no actual liquidation occurs. Alternatively, the Obligor may indemnify

the SPV with respect to the capital shortfall in order to liquidate the

Mudaraba

15

Perpetual Mudaraba Sukuk Cash Flow Illustration - USD100 million, 4% annual profit rate

$100 mn Mudaraba Capital Mudaraba Agreement

$100 mn Sukuk Proceeds Sukuk Issue

Investors

1

2

Inception Ongoing & Maturity

$4 mn pa if Obligor elects to pay

Mudaraba Profit (+ shortfall cover, if any)

$100 mn Dissolution Distribution Amount

Sukuk Redemption

Investors

9

5.1 8

Obligor’s General Pool of Assets

$[80] mn Dissolution Mudaraba Capital

5.2

6

5.3 Excess Allocated

Reserve Account

Excess Profit

Mudaraba Assets

3 $100 mn Mudaraba Capital (invested into Obligor’s Assets according to Investment Plan)

Obligor’s General Pool of Assets Mudaraba Assets

4 $4 mn pa Muradaba

Profit 7

$100 mn Dissolution Mudaraba Capital (+ shortfall indemnity, if any) (= $[80] mn + $[20] mn)

$4 mn pa if Obligor elects to pay

Periodic Distribution Amounts

Transaction Fund flow

7

~ Steps at inception ~ Steps during ongoing ~ Steps at maturity

1 4

9

3 6

SPV (Issuer / Trustee / Rab-al-Maal)

Obligor (Mudareb)

SPV (Issuer / Trustee / Rab-al-Maal)

Obligor (Mudareb)

The cash flow illustration is set out on the opposite

Assumptions:

- The SPV’s initial Mudaraba capital is $100 mn

- The dissolution Mdaraba capital is

$80 mn

- The Obligor elects to liquidate the Mudaraba at a certain time by

indemnifying the SPV with the shortfall cover of $20 mn

16

Breakdown by Geography

Perpetual Mudaraba Sukuk Case Study 1: ADIB’s USD 1 billion Tier 1 Perpetual Sukuk

Breakdown by Investor Type · The transaction, which is designed to comply with the Basel III guidelines and is expected to be eligible

as Tier 1 Capital by the UAE Central Bank, was well received by both regional and international investors, culminating in an orderbook in excess of USD15 billion (representing a 15x oversubscription and the largest oversubscription witnessed in any Sukuk offering globally).

· The issuance followed a series of investor meetings in Asia, the Middle East and Europe. In light of the unique nature of the transaction, the investor meetings commenced in the UAE with the objective of providing investors with sufficient time to understand the combination of Shariah and hybrid capital structuring elements.

· The initial momentum in the orderbook allowed ADIB to release initial price thoughts of “7% area” on 7 November, during the Asia morning. The announcement met with an overwhelming positive response, allowing the orderbook to grow to USD13 billion by the end of the day. As a result, official price guidance was released at “6.50% area (+/- 12.5bps)”, before being tightened again on the back of strong demand. The transaction eventually priced on Thursday afternoon during London hours at the tight end of the guidance at 6.375%, representing one of the lowest coupons for USD Tier 1 issuances in the international markets.

Issuer ADIB Capital Invest Ltd Mudarib Abu Dhabi Islamic Bank PJSC Mudarib Senior Ratings: A2(Moody’s)/ A+(Fitch) – both stable outlook (the Tier 1 issue is not rated) Currency / Format USD / Fixed Rate Regulation S Structure Sukuk Mudaraba Amount USD 1 billion Pricing / Settlement Date 08 November 2012 / 19 November 2012 Optional Call Date 16 October 2018, and on each profit distribution date thereafter Reset Date 16 October 2018. and ever 6 years thereafter to a new fixed rate based on the then prevailing 6yr US Mid Swap Rate + The Initial Credit Margin Periodic Distribution 6.375% p.a., semi-annual payments Issue Price/ Re-offer Spread 100/ 6 year USD MS+539.3bps Listing London Stock Exchange Governing Law English Law (except Mudaraba Agreement which is under Abu Dhabi and UAE Law) HSBC’s Role Structuring Adviser and Joint Bookrunner

Transaction Overview HSBC acted as a Structuring Adviser and Joint Bookrunner

on a market defining Tier 1 transaction for Abu Dhabi

Islamic Bank PJSC (“ADIB”)

ADIB is one of the flagship Islamic banks in the UAE and

the fourth largest Islamic bank globally by assets.

The USD1 billion 6.375% RegS

Tier 1 issue represents the first ever Shariah-compliant Tier 1

issue executed in the international markets and the

first ever Tier 1 instrument issued by a Middle East bank

in the capital markets

HSBC has successfully lead managed all four public USD issues executed by ADIB to

date. This repeat appointment demonstrates HSBC’s strong

position in the Sukuk and FI space. The transaction further reinforces HSBC's position as a market leader in structuring and executing innovative and

customized hybrid capital transactions for financial

institutions clients

Transaction Highlights

Asia (38%)Middle East (32%)Europe (26%)US Offshore (4%)

Private Banks (60%)Fund Managers (26%)Banks (11%)Others (3%)

17

Transaction Overview

On 13 March, HSBC acted as a Structuring Adviser and Joint

Bookrunner on a highly successful USD1 billion

6.250% RegS Tier 1 transaction

The issue represents the second Tier 1 Sukuk executed

in the international markets and the first ever public Tier 1 instrument issued by a Dubai-

based bank in the capital markets.

HSBC has acted as structuring

adviser and bookrunner on both of the international Tier 1

issues from the UAE to date demonstrating HSBC’s strong

position in the Sukuk and FI space

The transaction further

reinforces HSBC's position as a market leader in structuring and executing innovative and

customized hybrid capital transactions for financial

institutions clients globally

· The issuance followed a series of investor meetings in Asia, the Middle East and Europe. In light of the recent ADIB Tier 1 Sukuk transaction, investors immediately understood the combination of Shariah and hybrid capital structuring elements in the offering, allowing the issuer to focus its message on the bank’s credit strengths

· The initial momentum in the orderbook allowed DIB to release initial price thoughts of “7% area” on 12March, during the Asia morning. The announcement met with an overwhelming positive response, allowing the orderbook to grow to USD10 billion by the end of the day. As a result, initial price guidance was released at “6.50% area (+/- 12.5bps)”, before being tightened again on the back of strong demand. The transaction eventually priced on Thursday afternoon during London hours at final guidance at 6.250%, representing the lowest coupon for a USD public Tier 1 issuance in the MENA debt capital markets

· The transaction, which is designed to be eligible as Tier 1 Capital (under both current UAE Central Bank guidelines, as well as prospectively under Basel III), was well received by both regional and international investors, culminating in an orderbook in excess of USD14 billion (representing a 14x oversubscription – second only to the ADIB Tier 1 Sukuk issue executed in November 2012)

· The transaction highlights the strong connectivity between the various relationship, structuring and DCM teams across the UK, UAE and Asia to bring new to market products to HSBC’s clients in the MENA region

Transaction Highlights

Breakdown by Geography

Breakdown by Investor Type

Banks (33%)Private Banks (32%)Fund Managers (29%)Hedge Funds (5%)Others (1%)

Issuer DIB Tier 1 Sukuk Limited Mudareb Dubai Islamic Bank PJSC Currency / Format USD / Fixed Rate Regulation S Status Shariah compliant RegS USD Tier 1 Capital Certificates Issuer Ratings Baa1 (Moodys) / A (Fitch) Amount USD 1 billion Pricing / Settlement Date 13 March 2013 / 20 March 2013 Optional Call Date 20 March 2019, and on each profit distribution thereafter Reset Date 20 March 2019, and every 6 years thereafter to a new rate based on the then prevailing 6 year US Midswap Rate + Initial Credit Margin Maturity Date Perpetual Profit Rate 6.250 per annum Price / Initial Credit Margin 100.00/ MS+495.4bps Listing Irish Listing Governing Law English (except Mudaraba Agreement which is under Dubai and UAE) HSBC’s Role Structure Adviser, Joint Lead Manager, Joint Bookrunner

Perpetual Mudaraba Sukuk Case Study 2: Dubai Islamic Bank’s USD 1 billion Perpetual Sukuk

Middle East (38%)Europe (29%)Asia (29%)US Offshore (4%)

18

Disclaimer

HSBC Amanah Malaysia Berhad (“HSBC”) has prepared this document (the “Document”) for information purposes only. This Document does not constitute a commitment to underwrite or purchase or subscribe for all or any portion of the securities mentioned herein. Any such commitment shall be evidenced only by a fully executed subscription agreement, purchase agreement or similar contractual document. This Document should also not be construed as an offer for sale of or subscription for any investment, nor is it calculated to invite/solicit any offer to purchase or subscribe for any investment. HSBC has based this Document on information obtained from sources it believes to be reliable but which it has not independently verified. HSBC makes no guarantee, representation or warranty and accepts no responsibility or liability for the contents of this Document and/or as to its accuracy or completeness and expressly disclaims any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this Document. HSBC and its affiliates and/or its or their respective officers, directors and employees may have positions in any securities mentioned in this Document (or in any related investment) and may from time to time add to or dispose of any such securities (or investment). HSBC and/or any of its affiliates may act as market maker or have assumed an underwriting commitment in the securities of any companies discussed in this Document (or in related investments), may sell them to or buy them from clients on a principal or discretionary basis and may also perform or seek to perform banking or underwriting services for or relating to those companies. As HSBC is part of a large global financial services organisation, it or one or more of its affiliates may have certain other relationships with the parties relevant to the proposed activities as set out in this Document, and these proposed activities may give rise to a conflict of interest, which the addressee hereby acknowledges. No consideration has been given to the particular investment objectives, financial situation or particular needs of any recipient. This Document, which is not for public circulation, must not be copied, transferred or the content disclosed to any third party and is not intended for use by any person other than the addressee or the addressee's professional advisers for the purposes of advising the addressee hereon.