the deloitte cfo survey...q4 2015 january 2016 the deloitte cfo survey authors ian stewart chief...

TRANSCRIPT

Q4 2015

January 2016

The Deloitte CFO SurveyAuthorsIan StewartChief Economist020 7007 [email protected]

Debapratim DeSenior Economic Analyst020 7303 [email protected]

Alex ColeEconomic Analyst020 7007 [email protected]

ContactsIan StewartChief Economist020 7007 [email protected]

Richard MuschampCFO Programme Leader020 7007 [email protected]

For current and past copies of the survey, historical data and coverage of the survey in the media and elsewhere, please visit:

www.deloitte.co.uk/cfosurvey

The year ahead: A cautious start to 2016

Chart 1. CFO attitudes to EU membership% of CFOs who gave the following responses when asked whether it is in the interests ofUK businesses for the UK to remain a member of the EU

0%

10%

20%

30%

40%

50%

60%

70%

80%

Don't know,no strong opinion,prefer not to say

Too early to say:Depends on results

of renegotiation

NoYes

2015 Q2 2015 Q4

74%

62%

2% 6%

23%28%

1% 4%

Support among the Chief Financial Officers of the UK’s largest corporates for staying in the EU has narrowed, mirroring a drift towards greater scepticism on the part of the UK public in the second half of 2015. A clear majority of CFOs continue to favour remaining in the EU, but those expressing unqualified support for membership fell from 74% in the second quarter to 62% in the fourth quarter. Just 6% of CFOs favour leaving. But 4% did not express an opinion, and a sizeable minority, 28%, say their decision will depend on the results of the Prime Minister’s renegotiation of the UK’s membership of the EU. The outcome of these discussions is likely to emerge following the European Council meeting in February. With almost a third, or 32%, of CFOs undecided or undeclared, an eventual deal could significantly affect business attitudes to EU membership.

UK CFOs are downbeat about the outlook for growth in the euro area in 2016 despite a stronger than expected acceleration in activity seen in the region in 2015. Indeed, CFOs are more pessimistic about prospects for the euro area this year than for emerging market economies. CFO sentiment is most positive on the US and the UK economies. Nonetheless, doubts about the pace and sustainability of the global recovery are weighing on business sentiment. CFO confidence fell through 2015 and ended the year at its lowest level since the second quarter of 2012, when the euro area was in recession.

Corporate risk appetite often reflects trends in financial markets. Thus the decline in the FTSE100 UK equity index since last summer has been accompanied by a softening in corporate risk appetite.

The proportion of CFOs who think now is a good time to take risk dropped to 37% in the fourth quarter, down from 47% in the third quarter and a peak of 72% in late 2014.

Such large moves in risk appetite feed through to the way in which companies run their finances. CFOs’ balance sheet strategies have become more defensive, with a sharper focus on cost control which now tops CFOs’ list of priorities. Meanwhile CFOs are placing less weight on growth through acquisitions and on capital spending.

In recent months uncertainties, especially in emerging markets, have prompted the Bank of England to push back the timing of UK interest rate rises. The consensus in financial markets in mid-December was that the Bank will start raising interest rates in the second half of 2016. The pace of tightening is expected to be gentle, with three-month interest rates rising by a total of about 100bp, from a current 0.6% to 1.6% at the end of 2018. The corporate sector seems well positioned to cope with this sort of trajectory with 64% of CFOs reporting that a 100bp rate rise would have no effect, or a positive effect, on their plans for investment or employment.

The surge in CFO confidence and risk appetite that started in late 2012 went into reverse in 2015. CFOs are upbeat about prospects for the US and UK economies, but see more risks elsewhere, especially in emerging markets and the euro area. CFOs have reacted by cutting back on risk-taking and sharpening their focus on cost control. This more defensive stance by the corporate sector points to slower growth in corporate hiring and capital expenditure in coming months.

Europe

Public support for the UK’s membership of the EU fell in the second half of 2015.

Between the end of May and the beginning of July four major opinion polls gave the ‘In’ camp an average lead of 18 percentage points. In the fourth quarter the same four polls showed the lead had been reduced to six percentage points.

This decline in public support for the EU has coincided with a narrowing in support among CFOs.

Chart 2. UK public opinion polls on EU membership

Mid-year polling (May to July)

In Out Don't Know Lead (In)

ICM 31 May 47% 33% 20% +14

Ipsos Mori 14-16 Jun 66% 22% 12% +44

YouGov 19-24 Jun 44% 38% 18% +6

Survation 29 Jun-6 Jul 45% 37% 18% +8

Average 51% 33% 17% +18

End-year polling (October to December)

Ipsos Mori 17-19 Oct 52% 36% 12% +16

Survation 16-17 Nov 43% 40% 18% +3

YouGov 19-24 Nov 40% 38% 22% +2

ICM 6 Dec 43% 39% 17% +4

Average 45% 38% 17% +6

CFOs are positive about prospects for growth in the US and the UK in 2016.

But CFOs are strikingly downbeat about the euro area. Levels of pessimism about euro area growth in 2016 are greater than for emerging markets’ growth.

Chart 3. Growth prospectsNet % of CFOs who are optimistic about prospects for growth in the following regions in 2016

-40%

-20%

0%

20%

40%

60%

80%

100%

USUKChinaJapanEmergingmarketsincluding

China*

Euro areaEmergingmarkets

excludingChina*

-25%-18%

-27%

-6%

68%82%

-5%

*GDP-weighted estimate based on CFO readings for emerging markets excluding China, and for China

Although CFOs are negative about prospects for the euro area, activity in the region picked up through 2015, and at a rather faster rate than expected.

German business confidence ended 2015 at higher levels than at the beginning of the year. Meanwhile US manufacturing activity dropped to a six-and-a-half year low in November.

Chart 4. German and US business confidenceGerman Ifo Business Climate Index and US ISM Purchasing Managers Index (Manufacturing)

80

85

90

95

100

105

110

115

120

Dec15

Dec14

Dec13

Dec12

Dec11

Dec10

Dec09

Dec08

Dec07

Dec06

Dec05

US ISM (RHS)

German IFO (LHS)

30

35

40

45

50

55

60

65

2 | CFO Survey Q4 2015 The year ahead: A cautious start to 2016

Risk appetite wanes

Other than a brief, post-election bounce, corporate risk appetite has been trending down for over a year. Just 37% of CFOs say that now is a good time to take greater risk onto their balance sheets, down from a peak of 72% in Q3 2014.

Chart 5. Risk appetite% of CFOs who think this is a good time to take greater risk onto their balance sheets

0%

10%

20%

30%

40%

50%

60%

70%

80%

15Q3

15Q1

14Q3

14Q1

13Q3

13Q1

12Q3

12Q1

11Q3

11Q1

10Q3

10Q1

09Q3

09Q1

08Q3

08Q1

2007Q3

The fall in corporate risk appetite has been mirrored by a decline in investor risk appetite.

The second half of 2015 saw a rise in risk aversion among investors, as they moved from riskier assets including equities into safer government bonds.

Chart 6. CFO and investor risk appetites% of CFOs who think this is a good time to take greater risk onto their balance sheets(LHS) and change in UK equities over bonds (RHS)

% CFOs saying now is a good time to take risk (RHS)

Equities vs bonds (LHS)

30

35

40

45

50

55

60

65

70

75

2015201420132012201120102009200820070

10

20

30

40

50

60

70

80

Sentiment among large corporates has declined for the third consecutive quarter. CFO optimism is at its lowest level since the second quarter of 2012, when the euro area was in recession and gripped by concerns that the single currency might break up.

-80%

-60%

-40%

-20%

0%

20%

40%

60%

Mor

e op

tim

isti

cLe

ss o

ptim

isti

c

Chart 7. Business confidenceNet % of CFOs who are more optimistic about financial prospects for their company now than three months ago

15Q4

15Q1

14Q4

14Q1

13Q4

13Q1

12Q4

12Q1

11Q4

11Q1

10Q4

10Q1

09Q4

09Q1

08Q4

08Q1

07Q4

2007Q3

CFO Survey Q4 2015 The year ahead: A cautious start to 2016 | 3

Focus on cost control

For the first time in a year CFOs rate cost reduction as their number one priority for the next 12 months.

CFOs are also placing greater emphasis on other defensive strategies such as increasing cash flow, disposing of assets and reducing leverage.

In contrast, CFOs are placing rather less emphasis on growth strategies such as introducing new products and services, expanding by acquisition and increasing capital expenditure.

0% 10% 20% 30% 40% 50%

Reducing leverage

Disposing of assets

Raising dividends or share buybacks

Increasing capital expenditure

Expanding by acquisition

Increasing cash flow

Introducing new products/services or expanding into new markets

Reducing costs

2015 Q32015 Q4

44%34%

38%39%

37%34%

19%

17%

22%

19%

14%8%

13%9%

12%10%

Chart 8. Corporate priorities in the next 12 months% of CFOs who rated each of the following as a strong priority for their business in the next 12 months

The increased focus on defensive strategies means that CFOs are more defensive than at any time in the last three years.

19%

21%

23%

25%

27%

29%

31%

33%

35%

37%

39%

Chart 9. CFO priorities: Expansionary vs. defensive strategies

Defensivestrategies

Expansionarystrategies

2015Q4

2015Q1

2014Q4

2014Q1

2013Q4

2013Q1

2012Q4

2012Q1

2011Q4

2011Q1

2010Q3

Arithmetic average of the % of CFOs who rated expansionary and defensive strategies as a strong priority for their business in the next 12 months.

Expansionary strategies are introducing new products/services or expanding into new markets, expanding by acquisition and increasing capital expenditure.

Defensive strategies are reducing costs, reducing leverage and increasing cash flow.

4 | CFO Survey Q4 2015 The year ahead: A cautious start to 2016

Inflation and interest rates

CFOs’ expectations for inflation fell between the third and fourth quarters of 2015.

A narrow majority (51%) now expect inflation to remain below 1.5% in two-years’ time.

The fall in CFOs’ expectations for inflation coincided with downgrades to both market and Bank of England forecasts for inflation in 2016.

Chart 10. CFO inflation expectations% of CFOs who expect consumer price inflation in the UK to lie between the following ranges in two-years’ time

0%

10%

20%

30%

40%

50%

60%

Above 2.5%1.6%-2.5%0-1.5%Below zero

2015 Q3 2015 Q4

39%

1%

51%

5% 4%

56%

44%

As inflation forecasts have fallen so, too, have financial market expectations for future interest rates.

Expectations for UK interest rates at the end of 2016, 2017 and 2018 are now lower than they were in the summer of 2015.

0.0

0.5

1.0

1.5

2.0

2.5

Chart 11. Financial market expectations for UK interest ratesUK market rate expectations for end-year three-month interest rates

at Dec ’18 1.6%

at Dec ’17 1.3%

at Dec ’16 0.9%

Now 0.6%

Dec15

Nov15

Oct15

Sep15

Aug15

Jul15

Jun15

The corporate sector seems fairly well positioned to cope with the cumulative 100bp rate rise priced in by financial markets in the next three years.

Almost two-thirds of CFOs say that interest rates would have to rise by more than 100 basis points before their businesses cut planned investment or employment.

Chart 12. Effect of rate rises on corporate spending% of CFOs reporting that the Bank of England’s base rate could rise by the following amountsbefore their business responds by cutting planned investment or employment

0%

5%

10%

15%

20%

25%

30%

A rise ininterest rates

would be goodfor my business

More than300 basis

points

300 basispoints

200 basispoints

100 basispoints

50 basispoints

25 basispoints

8%

2%

26%

21%

10%

24%

10%

36% say rate rises of ≤100bp would affect investment/jobs

64% say rates would have to rise by >100bp

to affect investment/jobs

CFO Survey Q4 2015 The year ahead: A cautious start to 2016 | 5

Weaker margins

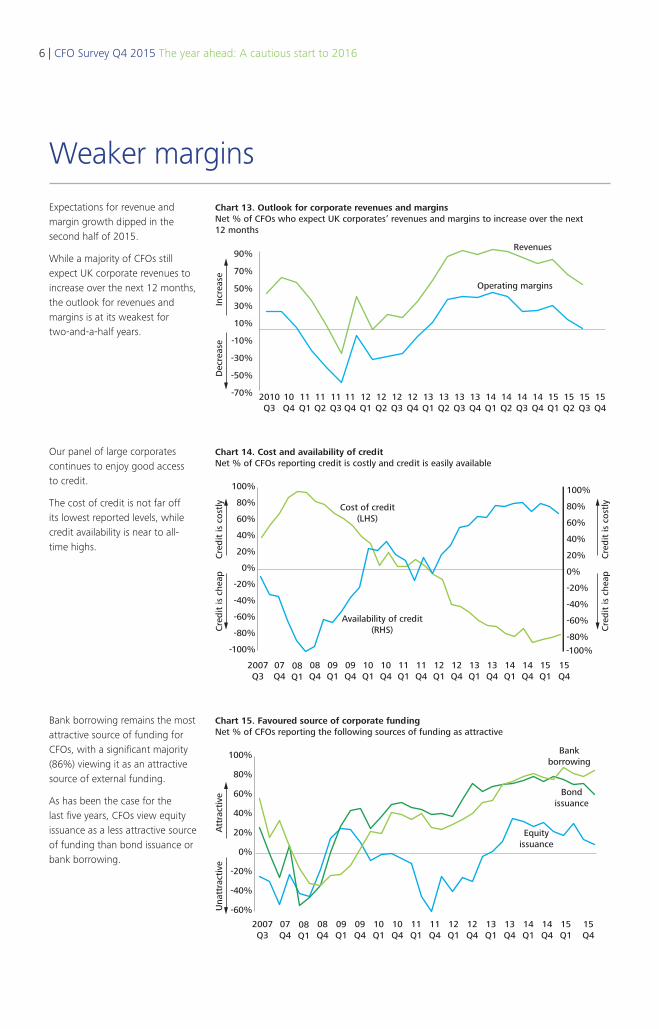

Expectations for revenue and margin growth dipped in the second half of 2015.

While a majority of CFOs still expect UK corporate revenues to increase over the next 12 months, the outlook for revenues and margins is at its weakest for two-and-a-half years.

-70%

-50%

-30%

-10%

10%

30%

50%

70%

90%

15Q4

15Q3

15Q2

15Q1

14Q4

14Q3

14Q2

14Q1

13Q4

13Q3

13Q2

13Q1

12Q4

12Q3

12Q2

12Q1

11Q4

11Q3

11Q2

11Q1

10Q4

2010Q3

Incr

ease

Dec

reas

eChart 13. Outlook for corporate revenues and marginsNet % of CFOs who expect UK corporates’ revenues and margins to increase over the next 12 months

Revenues

Operating margins

Our panel of large corporates continues to enjoy good access to credit.

The cost of credit is not far off its lowest reported levels, while credit availability is near to all-time highs.

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

Cre

dit

is c

ostl

yC

red

it is

che

ap

Cre

dit

is c

ostl

yC

red

it is

che

ap

Chart 14. Cost and availability of creditNet % of CFOs reporting credit is costly and credit is easily available

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

15Q4

15Q1

14Q4

14Q1

13Q4

13Q1

12Q4

12Q1

11Q4

11Q1

10Q4

10Q1

09Q4

09Q1

08Q4

08Q1

07Q4

2007Q3

Cost of credit(LHS)

Availability of credit(RHS)

Bank borrowing remains the most attractive source of funding for CFOs, with a significant majority (86%) viewing it as an attractive source of external funding.

As has been the case for the last five years, CFOs view equity issuance as a less attractive source of funding than bond issuance or bank borrowing.

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

Att

ract

ive

Una

ttra

ctiv

e

Chart 15. Favoured source of corporate fundingNet % of CFOs reporting the following sources of funding as attractive

Bankborrowing

Equityissuance

Bondissuance

15Q4

15Q1

14Q4

14Q1

13Q4

13Q1

12Q4

12Q1

11Q4

11Q1

10Q4

10Q1

09Q4

09Q1

08Q4

08Q1

07Q4

2007Q3

6 | CFO Survey Q4 2015 The year ahead: A cautious start to 2016

CFO Survey: Economic and financial context

The macroeconomic backdrop to the Deloitte CFO Survey Q4 2015The International Monetary Fund cut its forecast for global growth in 2015 and 2016. Activity in emerging markets continued to disappoint, with economists nudging down their forecasts for growth in most emerging economies. Growth in the advanced economies continued and broadened, though indicators of industrial activity have generally softened, partly as a result of weaker export market demand. After a short-lived market rally in October, equities, especially those in emerging markets, lost value towards the end of the year. In early December the oil price fell below $40, to the lowest level in seven years; metals prices also softened. Inflation remained close to zero in the US, the euro area and the UK and inflation forecasts for 2016 continued to decline. The European Central Bank’s announcement of a further round of Quantitative Easing fell short of market expectations, though the ECB’s President subsequently reassured markets that there were “no limits” to the tools the ECB could use to fight deflation. As widely anticipated the US Federal Reserve raised interest rates on 16th December, the first time US interest rates have been increased in almost ten years.

-7%

-5%

-3%

-1%

1%

3%

5%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

UK GDP growth: Actual and forecast (%)

Quarter-on-quarter growth

Year-on-yeargrowth

Source: ONS, consensus forecasts from The Economist and Deloitte calculations

Forecasts

Source: Thomson Reuters Datastream

3000

3500

4000

4500

5000

5500

6000

6500

7000

2008 2009 2010 2011 2012 2013 2014 2015

FTSE 100 price index

Public

Source: Thomson Reuters Datastream

Private

-400

-300

-200

-100

0

100

200

300

400

500

600

Q22015

Q32014

Q42013

Q42012

Q42011

Q42010

Q42009

Q42008

Q42007

Q12007

UK private and public sector job growth (thousands)

Source: Thomson Reuters Datastream

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

-1

0

1

2

3

4

5

6

7

8

9

UK annual CPI inflation (%)

CFO Survey Q4 2015 The year ahead: A cautious start to 2016 | 7

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), a UK private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.co.uk/about for a detailed description of the legal structure of DTTL and its member firms.

Deloitte LLP is the United Kingdom member firm of DTTL.

This publication has been written in general terms and therefore cannot be relied on to cover specific situations; application of the principles set out will depend upon the particular circumstances involved and we recommend that you obtain professional advice before acting or refraining from acting on any of the contents of this publication. Deloitte LLP would be pleased to advise readers on how to apply the principles set out in this publication to their specific circumstances. Deloitte LLP accepts no duty of care or liability for any loss occasioned to any person acting or refraining from action as a result of any material in this publication.

© 2016 Deloitte LLP. All rights reserved.

Deloitte LLP is a limited liability partnership registered in England and Wales with registered number OC303675 and its registered office at 2 New Street Square, London EC4A 3BZ, United Kingdom. Tel: +44 (0) 20 7936 3000 Fax: +44 (0) 20 7583 1198.

Designed and produced by The Creative Studio at Deloitte, London. J3512

Two-chart summary of key survey messages

About the surveyThis is the 34th quarterly survey of Chief Financial Officers and Group Finance Directors of major companies in the UK. The 2015 fourth quarter survey took place between 11th November and 2nd December. 137 CFOs participated, including the CFOs of 24 FTSE 100 and 62 FTSE 250 companies. The rest were CFOs of other UK-listed companies, large private companies and UK subsidiaries of major companies listed overseas. The combined market value of the 99 UK-listed companies surveyed is £374 billion, or approximately 18% of the UK quoted equity market.

The Deloitte CFO Survey is the only survey of major corporate users of capital that gauges attitudes to valuations, risk and financing. To join our panel of CFO respondents and for additional copies of this report, please contact Anthea Neagle on 020 7303 0116 or email [email protected].

19%

21%

23%

25%

27%

29%

31%

33%

35%

37%

39%

CFO priorities: Expansionary vs. defensive strategies

Defensivestrategies

Expansionarystrategies

2015Q4

2015Q1

2014Q4

2014Q1

2013Q4

2013Q1

2012Q4

2012Q1

2011Q4

2011Q1

2010Q3

CFO attitudes to EU membership% of CFOs who gave the following responses when asked whether it is in the interests of UK businesses for the UK to remain a member of the EU

0%

10%

20%

30%

40%

50%

60%

70%

80%

Don't know,no strongopinion,

prefer notto say

Too earlyto say:

Depends onresults of

renegotiation

NoYes

2015 Q2 2015 Q4

74%

62%

2%6%

23%28%

1% 4%

8 | CFO Survey Q4 2015 The year ahead: A cautious start to 2016