the effect of corporate social responsibility(csr

TRANSCRIPT

1

THE EFFECT OF CORPORATE SOCIAL RESPONSIBILITY(CSR) ON

PROFITABILITY OF MULTINATIONAL COMPANIES. A CASE STUDY OF NESTLE

GHANA LIMITED

By

Emmanuel Ocran

PG3079509

A Thesis submitted to the Institute of Distance Learning, Kwame Nkrumah University of

Science and Technology in partial fulfillment of the requirements for the degree of

EXECUTIVE MASTERS OF BUSINESS ADMINISTRATION

OCTOBER 2011

2

DECLARATION

I hereby declare that this submission is my own work towards the Commonwealth Executive

Masters of Business Administration (CEMBA) and that, to the best of my knowledge, it contains

no materials previously published by another person nor materials which has been accepted for the

award of any other degree of the university, except where due acknowledgement has been made in

the text.

Emmanuel Ocran ……………………… ..……………………….

PG3079509 Signature Date

Certified By:

Mr Samuel Kwesi Enninful ………….……………… ………………………..

(Supervisor) Signature Date

Professor I. K. Dontwi ………….……………… ………………………..

(Dean – KNUST - IDL) Signature Date

3

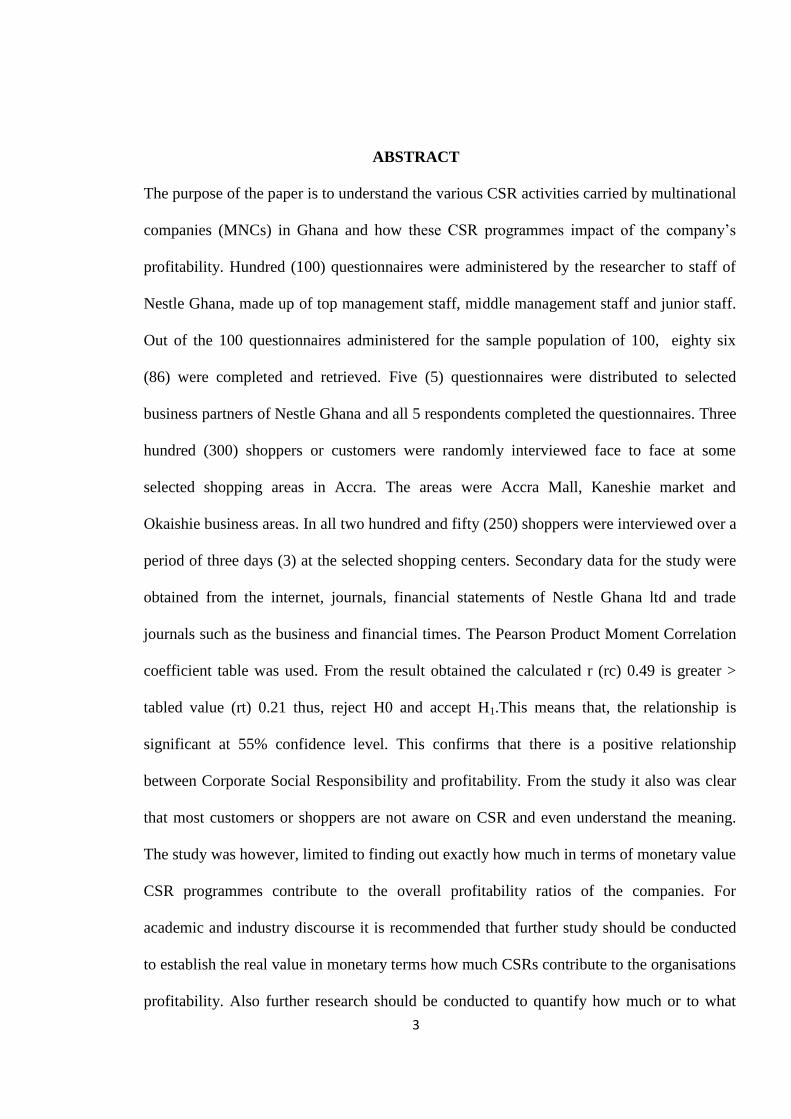

ABSTRACT

The purpose of the paper is to understand the various CSR activities carried by multinational

companies (MNCs) in Ghana and how these CSR programmes impact of the company‘s

profitability. Hundred (100) questionnaires were administered by the researcher to staff of

Nestle Ghana, made up of top management staff, middle management staff and junior staff.

Out of the 100 questionnaires administered for the sample population of 100, eighty six

(86) were completed and retrieved. Five (5) questionnaires were distributed to selected

business partners of Nestle Ghana and all 5 respondents completed the questionnaires. Three

hundred (300) shoppers or customers were randomly interviewed face to face at some

selected shopping areas in Accra. The areas were Accra Mall, Kaneshie market and

Okaishie business areas. In all two hundred and fifty (250) shoppers were interviewed over a

period of three days (3) at the selected shopping centers. Secondary data for the study were

obtained from the internet, journals, financial statements of Nestle Ghana ltd and trade

journals such as the business and financial times. The Pearson Product Moment Correlation

coefficient table was used. From the result obtained the calculated r (rc) 0.49 is greater >

tabled value (rt) 0.21 thus, reject H0 and accept H1.This means that, the relationship is

significant at 55% confidence level. This confirms that there is a positive relationship

between Corporate Social Responsibility and profitability. From the study it also was clear

that most customers or shoppers are not aware on CSR and even understand the meaning.

The study was however, limited to finding out exactly how much in terms of monetary value

CSR programmes contribute to the overall profitability ratios of the companies. For

academic and industry discourse it is recommended that further study should be conducted

to establish the real value in monetary terms how much CSRs contribute to the organisations

profitability. Also further research should be conducted to quantify how much or to what

4

degree these CSR programmes have impacted on the society and its corresponding value

generation for the company.

5

DEDICATION

This work is dedicated to my loving family for their support and encouragement to the successful

completion of my course.

6

ACKNOWLEDGEMENTS

I would like to give praise and thanks to the Almighty God for His guidance and protection

throughout my life and also seeing me through my studies.

I wish to express my gratitude to my supervisor Mr Samuel Kwesi Enninful who took time to read

and made the necessary criticisms, suggestions and corrections in the course of writing this thesis.

I am extremely grateful to Mr & Mrs John Serbe Marfo and the Achimota Study Group for their

support. Thank you very much and may God reward you abundantly.

Again my gratitude goes to my study mates namely, Hannah Tinkorang, Akosua Okrah and Ophelia

Osei.

Finally to Mr Desmond Quaye of Nestle Ghana Ltd and Nestle business partners like Fio Enterprise

who participated in the study, I am very grateful.

7

Table of Contents

Cover Page

Certification Page……………………………………………………………………………….i

Abstract…………………………………………………………………………………………ii

Dedication………………………………………………………………………………………iv

Acknowledgement……………………………………………………………………………….v

Table of Contents……………………………………………………………………………….vi

List of Tables……………………………………………………………………………………ix

CHAPTER ONE - INTRODUCTION

1.1 Background Information………………………………………………………1

1.2 Statement of Research Problem………………………………………………..5

1.3 Research Objectives…………………………………………………………...6

1.4 Research Questions……………………………………………………………6

1.5 Justification for Study…………………………………………………………6

1.6 Scope and Limitation of Study ………………………………………………..6

1.7 Brief Methodology of Study…………………………………………………..7

1.8 Organisation of the Work……………………………………………………...7

CHAPTER TWO - LITERATURE REVIEW

2.1 Introduction………………………………………..…………………………..8

2.1 From Philanthropy to Corporate Responsibility………………………………10

2.2 Multinational Corporation…………………………………………………….12

2.3 Small and Medium-Sized Enterprises………………………………………....13

2.4 Size of organisation…………………………………………………………....14

2.5 CSR Practices………………………………………………………………….15

2.5.1 Government-linked corporations……………………………………………....15

2.5.2 Multinational corporations……………………………………………………..15

8

2.5.3 Local Ghanaian Corporation…………………………………………………..16

2.6 Size of organisation and CSR practices……………………………………….16

2.7 Empirical Studies of CSR and Financial Performance…………………….….17

2.8 Measures of Corporate Social Responsibility………………………………....18

2.8.1 Measures of Financial Performance…………………………………………...19

2.9 Conclusions and Implications…………………………………………………19

2.10 Future Research…………………………………………………………….…20

2.11 Corporate Social Responsibility in Nestle Ghana……………………………..21

2.8 The Impact of Corporate Social Responsibility……………………………….23

CHAPTER THREE - RESEARCH METHODOLOGY

3.1 Introduction…………………………………………………………………….25

3.2 Research Design………………………………………………………………...25

3.3 Population and Sample Size…………………………………………………....25

3.4 Research Instrument…………………………………………………………….26

3.5 Validity of Research Instrument………………………………………………...26

3.6 Data Analysis Technique………………………………………………………..27

CHAPTER FOUR - DATA PRESENTATION, ANALYSIS AND INTERPRETATION

4.1 Introduction……………………………………………………………………..29

4.2. Data Presentation and Analysis………………………………………………….29

4.2 Questionnaire to Staff…………………………………………………………...29

4.2.1 Descriptive Statistics……………………………………………..…………….….29

4.2.2. Presentation and Analysis of research questions…………………………………37

4.3 Questionnaire to External

Stakeholders……………………………………………...46

4.4 Test of Hypothesis……………………………………………………………………56

9

CHAPTER FIVE - SUMMARY, RECOMMENDATION AND CONCLUSION

5.0 Introduction……………………………………………………………………..61

5.1 Summary of Findings……………………………………………………………61

5.1.1 Findings – Profitability…………………………………………………………..61

5.1.2 CSR in the Community…………………………………………………………..62

5.1.3 Nestlé‘s Financial Commitment to CSR...............................................................62

5.1.4 Value Creation.......................................................................................................62

5.1.5 Customer Ignorance of CSR programmes……………………………………….62

5.2 CONCLUSION………………………………………………………………….63

5.3 RECOMMENDATION…………………………………………………………64

REFERENCES…………………………………………………………………………..66

APPENDIX I……………………………………………………………………………..69

APP ENDIX II……………………………………………………………………………71

10

List of Tables

Table 4.1.1.1: Sex Distribution of Respondents……………………………………29

Table 4.1.1.2: Marital Status of Respondents………………………………………31

Table 4.1.1.3: Age Distribution of Respondents…………………………………….32

Table 4.1.1.4: Respondents‘ Job Levels……………………………………………..33

Table 4.1.1.5: Work Experience Distribution of Respondents………………………35

Table 4.1.1.6: Education Qualification Distribution of Respondents………………..35

Table 4.1.1.7: Professional Qualification Distribution of Respondents……………..37

Table 4.2.1.1: Respondents awareness on Nestle Ghana embarking on CSR………37

Table 4.2.1.2: Respondent responds to impact of the CSR projects/programme on the

community……………………………………………………………………………39

Table 4.2.1.3: Respondent responds about other benefits Nestle Ghana stands to gain

apart from profitability………………………………………………………………..39

Table 4.2.1.4: Respondent response to question 11…………………………………..41

Table 4.2.1.5: Respondent response to question 12…………………………………..42

Table 4.2.1.6 Respondent response to question 13……………………………………44

Table 4.2.1.7: Respondent response to question 14…………………………………...44

Table 4.2.1.8: Respondent response to question 15…………………………………...45

Table 4.3.1.1 Sex Distribution of Respondents……………………………………… 46

Table 4.3.1.2 Marital Status Distribution of Respondents…………………………… 46

Table 4.3.1.3 Age Distribution of Respondents……………………………………….47

Table 4.3.1.4: Corporate Relationship…………………………………………………47

Table 4.3.1.5 Level Of Transactions with Nestle Ghana………………………………48

Table 4.3.1.6: Respondents response to question 6…………………………………….48

Table 4.3.1.7: Respondents response to question 7…………………………………….49

Table 4.3.1.8: Respondent responds to Question 8 ……………………………………49

Table 4.3.1.9: Respondents response to question 9…………………………………….50

11

Table 4.3.1.10: Respondents response to question 10……………………………….…51

Table 4.3.1.11: Respondents response to question 11………………………………….51

Table 4.3.1.12: Respondents response to question 12………………………………....52

Table 4.3.1.13: Respondents response to question 13………………………………….53

Table 4.4.1.1: Sex Distribution of Respondents……………………………………….53

Table 4.4.1.2 Customers responds on benefits of CSR………………………………...54

12

13

CHAPTER ONE

INTRODUCTION

1.1 BACKGROUND INFORMATION

Corporate Social Responsibility (CSR) as a concept entails the practice whereby

corporate entities voluntarily integrate both social and environment upliftment in their

business philosophy and operations. A business enterprise is primarily established to

create value by producing goods and services which society demands. The present-day

conception of corporate social responsibility (CSR) implies that companies voluntarily

integrate social and environmental concerns in their operations and interaction with

stakeholders. The notion of CSR is one of ethical and moral issues surrounding corporate

decision making and behaviour, thus if a company should undertake certain activities or

refrain from doing so because they are beneficial or harmful to society is a central

question. Social issues deserve moral consideration of their own and should lead

managers to consider the social impacts of corporate activities in decision making.

Today, managers of Multinational Companies(MNCs) have found a need that the

environment in which they operate should be provided for because their intermediate and

macro environments have a direct impact on the attainment of the corporate goals,

objectives and mission statement. The purpose of all Profit-making organizations, and

even the non-profit making organizations, is to maximize profit and in turn minimize

cost, through optimal utilization of available resources to achieve the best results they are

capable of. Profitability is an important factor to all MNCs, because it is one of the major

purpose for which the MNCs are established.

CSR involves a business identifying its stakeholder groups and incorporating their needs

and values within the strategic and day-to-day decision-making process, thus a means of

analyzing the inter-dependent relationships that exist between businesses, the economic

systems and the communities within which they are operating. CSR is a means of

14

discussing the extent of obligations a business has to its immediate society; a way of

proposing policy ideas on how those obligations can be met; as well as a tool by which

the benefits to a business for meeting those obligations can be identified (CSR Guide).

CSR is also referred to as ‗corporate‘ or ‗business responsibility‘, ‗corporate‘ or ‗business

citizenship‘, ‗community relations‘, ‗social responsibility‘. It involves the way

organisations make business decisions, the products and services they offer, their efforts

to achieve an open and honest culture, the way they manage the social, environmental

and economic impacts of business activities and their relationships with their employees,

customers and other key stakeholders having interest in the Business and its operations.

The motivations to engage in CSR are varied – response to market forces, globalization,

consumer and civil society pressures, corporate objectives, etc. The activities of these

firms are therefore visible because of their global reach. As such, there is a higher

incentive to protect their brands and investments through CSR. The CSR activities in this

sector are mainly focused on remedy the effects of their business activities on the local

communities. So, the firms operating in this sector have often provided pipe-borne

waters, hospitals, schools, etc.

The MNCs seek to conduct CSR so that they meet their financial, social and

environmental responsibilities in an aligned way. At its core, it is simply about having a

set of values and behaviours that underpin its everyday activities, its transparency, its

desire for fair dealings, its treatment of people, its attitudes towards and treatment of its

customers and its links into the Community. As a result, the environmental aspect of CSR

is seen as the duty to cover the environmental implications of the company‘s operations,

products and facilities; eliminate waste and emissions; maximize the efficiency and

productivity of its resources; reward for externalities and minimize unethical practices

that might adversely affect the enjoyment of the country‘s resources by future

generations. In the emerging global economy, where the internet, the news media and the

15

information revolution shed light on business practices around the world, companies are

more frequently judged on the basis of their environmental stewardship (CIBN). Partners

in business and consumers want to know what is inside a company. This transparency of

business practices means that for MNCs, CSR is no longer a luxury but a requirement.

Mazurkiewicz (2004) recognized the concept has been developing since the early 1970s;

there is no single, commonly accepted definition of ―Corporate Social Responsibility‖

(CSR). There are different perceptions of the concept among the private sector,

governments and civil society organizations. Depending on the perspective, CSR may

cover:

a) A company running its business responsibly in relation to internal stakeholders

(shareholders, employees, customers and suppliers);

b) The role of business in relationship to the state and nationally, as well as to global

institutions or standards; and

c) Business performance as a responsible member of the society in which it operates and

the global community.

The first perspective includes ensuring good corporate governance, product

responsibility, employment conditions, workers rights, training and education. The

second includes corporate compliance with relevant legislation, and the company‘s

responsibility as a taxpayer, ensuring that the state can function effectively.

The third perspective is multi-layered and may involve the company‘s relations with the

people and environment in the communities in which it operates, and those to which it

transact business. Too often, attaining CSR is understood from the perspective of

business generosity to community projects and charitable donations, but this fails to

capture the most valuable contributions that a company has to make (Reyes 2002).

CSR is seen by leadership companies as more than a collection of discrete practices or

occasional gestures, or initiatives motivated by marketing, public relations or other

16

business benefits. Rather, it is viewed as a comprehensive set of policies, practices and

programs that are integrated throughout business operations, and decision-making

processes that are supported and rewarded by top management‖.

Simply, many companies have found that CSR has often had a positive impact on

corporate profits. Of all the topics related to corporate social responsibility, it is

environmental initiatives that have produced, so far, the greatest amount of quantifiable

data linking proactive companies with positive financial results. Corporate Social

Responsibility in fast moving consumer goods(FMCG) sector would be aimed towards

addressing the peculiarity of the socio-economic development challenges of the country

(e.g. poverty alleviation, health care provision, infrastructure development, education,

etc) and would be informed by socio-cultural influences (e.g. communalism and charity).

They might not necessarily reflect the popular western standard or expectations of CSR

(e.g. consumer protection, fair practice, green marketing, climate change concerns, social

responsible investments, etc) as a result of the effect of the global economic meltdown.

Companies are assumed to be socially responsible because they anticipate a benefit from

these actions. Examples of such benefits might include reputation enhancement, the

ability to charge a premium price for its output, or the use of CSR to recruit and retain

high quality workers. These benefits are presumed to offset the higher costs associated

with CSR, since resources must be allocated to allow the firm to achieve CSR status,

while a key indicator to determine the true worth and value of modern organizations is

their ability to give back to the society part of their income through some mutually

beneficial initiatives (Nkanbra and Okorite, 2007). There is no doubt that CSR is

becoming indispensable, though involuntary, in the contemporary business world as

societal needs are making it imperative for the corporate organisations to be sensitive to

happenings in their environment, which ensure more understanding and good relationship

17

between the organisation and the society they exist, since CSR contributes to the

wellbeing of the citizenry (Osho 2008).

1.2 STATEMENT OF RESEARCH PROBLEM

With the new ―competent and competitive players,‖ the Ghanaian FMCG system is now

driven by advanced competition brought about by globalization, deregulation of financial

services, recent replacement of some MNCs‘ Chief Executives, astronomical

development in Information and Communication Technology (ICT), among others, to

render services according to cost-benefit criteria. This has affected MNCs customers'

habits as well, while the increasing demands for clear and hard facts about the social and

environmental performance of MNCs by an increasingly well-informed breed of

stakeholders have made corporate social responsibility (CSR).

MNCs in Ghana perceive and practice Corporate Social Responsibility as a corporate

philanthropy aimed at addressing socio-economic development challenges. But then what

impact does this have on the profitability of the organisation?

It is against this background that, there is the need to find out how CSR impact on the

profitability of the MNCs especially, Nestle Ghana Ltd.

1.3 RESEARCH OBJECTIVES

The general objective of this study is to examine the effect of Corporate Social

Responsibility of Nestle Ghana on its profitability. But specifically, the study sought to

achieve the following objectives:

1. To find out how Nestle Ghana carry its CSR as a major partner in the fast moving

consumer goods(FMCG) industry.

2. To find out the challenges of Nestle in practicing of its CSR programmes.

3. To investigate whether Corporate Social Responsibility guarantee customers‘

confidence and security of depositor‘s fund.

18

1.4 Research Questions

1. How does Nestle Ghana embark on Corporate Social Responsibility?

2. What challenges does Corporate Social Responsibility impose on Nestle Ghana?

3. Does Nestle Ghana‘s Corporate Social Responsibility guarantee the customers‘

confidence level in the organisation?

1.5 JUSTIFICATION FOR THE STUDY

The study is expected to make contribution to knowledge in the following areas:

Provide information about CSR in relation to corporate institution especially the FMCG

sector. It is also to be a fundamental material for scholarly discourse in management

science relating to Corporate Social Responsibility. The study will provide information

on the impact of CSR on the profitability of MNCs operations in Ghana. Finally, the

research work will provide information on the challenges of CSR in the fast moving

consumer good(FMCG) sectors with recommendations.

1.6 SCOPE AND LIMITATION OF THE STUDY

The study is focused on the headquarters of Nestle Ghana. It critically examines what

impact Corporate Social Responsibility has on the profitability of Nestle Ghana for the

period 2008-2010. However the study is limited to finding out how much in monetary

terms Nestle commits to towards corporate social responsibility programmes yearly.

1.7 BRIEF METHODOLOGY OF THE STUDY

Primary data was used through the administering of questionnaires to respondents at Nestle

Ghana Limited, Customers, Nestle Business partners and shoppers in general.

The study population is very large, so 100 respondents were selected from the top level

management, middle level management and the supervisors which is a good representation

of the population based on stratified sampling. This cuts across the various departments in

19

the organisation such as corporate affair department, customer services department, retail

department, marketing department and others. Again 300 shoppers/customers were selected

through random sampling. Finally, 5 business partners of Nestle were also interviewed

through administering of simple structured questionnaires for their response in relation to

the study.

1.8 ORGANISATION OF THE WORK

This work is organized and presented in five chapters. Chapter one covered the background

information to the study, objectives of the study, the research questions, significance of the

study as well as the limitations of the study. Chapter two looked at the review of literature

on the subject. This is a review of books, papers, publications of earlier writers on the topic

or similar to that. Chapter three did an appraisal of Nestle Ghana and their operations, it

discussed the methods of collecting the data into details. Chapter four analyzed and

discussed the data collected for the study. Finally, chapter five discussed the findings,

conclusions and recommendations for addressing the problems identified in the study.

20

CHAPTER TWO

LITERATURE REVIEW

2.0 INTRODUCTION

CSR as defined by European Commission (2001) is ―a concept whereby companies

integrate social and environmental concerns in their business operations and in their

interaction with their stakeholders on a voluntary basis‖ following increasingly aware that

responsible behaviour leads to sustainable business success. CSR is about managing change

at company level in a socially responsible manner which can be viewed in two different

dimensions:

a) Internal – socially responsible practices that mainly deal with employees and related to

issues such as investing in human capital, health and safety and management change, while

environmentally responsible practices related mainly to the management of natural

resources and its usage in production.

b) External – CSR beyond the company into the local community and involves a wide

range of stakeholders such as business partners, suppliers, customers, public authorities and

NGOs that representing local communities as well as environment. A company should

focus on areas such as economic, environmental and social when developing sustainability

strategy (Szekely & Knirsch 2005). Sustainability strategy development can be based on

legitimacy, economic and social theories. These theories explain social disclosures pattern

by organisations (Haniffa & Cooke 2005). Thus, CSR practices can be based on the these

three strategies.

Legitimacy theory is whereby corporate social disclosures were motivated by the corporate

need to legitimise activities (Hogner 1982). This is where corporate management will react

to community expectations (Guthrie & Parker, 1989). Thus, companies are expected to

carry out activities that are acceptable by the community. Legitimacy also implies that

companies will take cautious to ensure their activities and performance acceptable to the

21

community given a growth in community awareness (Wilmshurst & Frost 2000). Corporate

social disclosure can be used to appease some of the concerns of the relevant publics and

also as a proactive legitimation strategy to obtain continued inflows of capital and to please

ethical investors (Haniffa & Cooke 2005).

Economic theory reflects the degree of association of CSR and financial performance by

taking consideration of cost-related advantages, market advantages and reputation

advantages (Chamhuri & Wan Noramelia 2004). In the business, CSR is concerned with

employment, lifelong learning, consultation and participation of workers, equal

opportunities and integration of people towards restructuring and industrial change.

Basically, the formation of policies is influenced by the authority employment strategies,

the initiative on social responsible restructuring, the initiatives to promote quality and

diversity in the workplace and health and safety strategy.

The social issues include the benefits offered in terms of training related to safety, health

and environment, donations, education scheme, medical benefits and others. (Chamhuri &

Wan Noramelia 2004). Environmental issues emphasize on preserving and conserving

natural resources such as conducting recycling activities, noise reduction action plan to

pursue noise improvement initiatives, water and process treatment and compliance with

authority regulations and requirements. Many enterprises recognized the importance of

their responsibilities towards the environment and take them seriously by setting targets for

continually improving their performance. CSR social activities may include charitable

contributions to local and national organisations such as fundraising, donations and gifts in

areas where it trades and others like regeneration of deprived communities, reclamation of

derelict land and creation of new regeneration jobs. Development of strategies and

programmes on social and environmental issues enabled firms to gain close relationship

with community. Firms could take initiatives by conducting campaigns, seminars,

workshops and giving donation to the society. This way enables a company to meet its CSR

22

commitment and indirectly acts as a marketing and promotional strategy. As the result,

higher market share can be obtained, which lead to higher revenues from larger sales. The

CSR‘s policy implementation in business can also be influenced by fair commercial

practices such as advertising, aggressive marketing and after-sales services between

businesses and customers.

Policies, strategies and programmes that are associated with social activities can be used to

indicate the level of CSR‘s commitment of an organisation. Organisations too, need to meet

the customer‘s demand and expectations. Today, buying behaviour is changing whereby

consumers have increasingly required information and reassurance interests on the

environmental and social concerns. As to maintain good relationship and attract more

customers, enterprises are taking initiatives to fulfill the demand of providing such

information. For instance, eco-labelling is a way of communicating organization‘s social

responsibility to public. Besides, CSR is also concerned with employment, lifelong

learning, consultation and participation of workers, equal opportunities and integration of

people towards restructuring and industrial change. Employees who feel protected and

appreciated will increase their productivity in production and thus, achieving economies of

scale.

2.1 From Philanthropy to Corporate Responsibility

The practices of philanthropy has been evolved from the day business existed in this world

until today. The main reason for a company to exist is to create profit. Making profits are

nothing wrong but the way used to derive such profits are of concerned. Before 1970,

basically, corporate share its profit with the community through philanthropic activity. In

other word, CSR is after-profit obligation. If let say, companies are not profitable they do

not have to behave responsibly. This impact is even worse during severe economic

depression or when an organisation is managed by unethical, short-term thinking managers

that would lead to societies having no choice and accepting discrimination, child labour,

23

pollution and dangerous working conditions. Another debate arises in this approach is if

companies are just being good and donating a lot of money to social initiatives then they

will be wasting shareholders' money. That is not sustainable in the long-run, and

shareholders will quickly lose interest. Thus, during 1970 to 1990, organisation had shifted

from sharing profits with the community as a soft approach of philanthropy to the hard

approach by using philanthropy for the purpose of profit-making. CSR is perceived as a

public relation tool in improving an organisation image and performance. CSR is also

performed for mitigating adverse impacts of an organisation onto environment and society

such as those in the oil and gas industry. While philanthropy does little or nothing to help

companies make profits, CSR activities are linked to improving a company's bottom line.

Therefore, during 1990 to 2001 period, embedding socially responsible principles in

corporate management has become a corporate obligation. CSR is increasingly being

embedded into the corporate mission, strategy and actions of organisations.

For a long term survival, CSR has been adopted as a corporate routine. Strategic CR is

whereby an organisation achieves sustainabilility in such a way that its CSR actions have

become part and parcel of the way in which a company carries out its business. Its links to

the bottom line of a company has been laid out clearly simply because, if it does not

contribute to the bottom line, it will eventually be rejected by other stakeholders of the

organisation.

A government linked corporation (GLC) is a corporate entity that may be a private or

public listed on a stock exchange in which an existing government owns a stake using a

holding company. There are two main definitions of GLCs, which are dependent on the

proportion of the corporate entity a government owns. One definition suggests that a

company is classified as a GLC if a government owns an effective controlling interest or

more than 50%, while the second definition suggests that any corporate entity that has a

government as a shareholder is a GLC (Wikipedia 2005). GLC is different from

24

government-owned corporation in terms of holding power by the government.

Government-owned corporation is a legal entity created by a government to exercise some

of the government‘s powers. It may resemble a not-for-profit corporation as it has no need

or goal of satisfying the shareholders with return on their investment through price increase

or dividends (Wikipedia 2005). Though the practice of CSR is still in the early stage the

concept has been much appreciated by most of the government-linked corporations. The

practice has been increasingly important as a strategy towards sustainable business

development. In general, the aim of government-linked corporation is to improve the living

of Ghanaian and contributes towards nation development. They uphold the principle of

giving back to community. The profits they earned are not only for the companies‘ benefits,

but also for the nation as a whole. The strategies and programmes undertaken vary

accordingly but with one goal that is to improve and enhance the quality of life in terms of

safety, health and environment.

2.2 Multinational Corporation

Multinational corporations are companies or enterprises that operate in a number of

countries and have production or service facilities outside the country of its origin. While

still maintaining a domestic identity and a central office in a particular country, the aim is

to maximize profits on a worldwide basis. As world is encouraging on international

business, therefore, multinational corporations are among the major participants in business

activities.

Most multinational companies that were established in Ghana have interesting business

philosophies on CSR. They started with business philosophy as a principal and guideline

towards CSR‘s implementation. Though companies came from various nature of

businesses, their aimed are similar which is to recognize the need of making business

decisions that demonstrate economic, social and environmental responsibilities for the

stakeholders which consist of employees, community, business partners, suppliers,

25

customers, government and shareholders. These companies bring benefits to society

through wealth generation, employment, skill development and transfer and community

initiatives. The words they committed are evident by the policies, strategies and innovative

programme with further establishment and improvement on the social, economic and

environmental issues. There are various policies, strategies and programmes which have

been implemented by multinational companies that can be shared and useful as an

acknowledgement of CSR‘s practices in the business and thus, continuously contributing to

the sustainable development. Among the best practice of CSR can be reflected by the

strategies, which differs by environmental and social scopes.

2.3 Small and Medium-Sized Enterprises

Small and medium-sized enterprises (SME) play an important role in Ghanaian Economy.

The term SME is also synonymous to small and medium-sized industries (SMI). SMEs are

the engine of economic growth which also representing the key source of endogenous

growth. SMEs are also the impetus for the country‘s broad based economic development.

The Ghanaian government has given a priority on development of SMEs. In Ghana, SME is

usually in the form of private limited company, partnership and sole-proprietorship. There

is no standard definition of SMEs in Ghana. However, the Association of Ghana

Industries(AGI) define SME based on the number of employees, amount of capital, total

assets and sales turnover. SMEs can be categorized into three broad sectors namely

manufacturing, agriculture and services. SMEs in Ghana are defined in terms of annual

sales turnover or its number of full-time employees. Since SMEs are a part of business

entities populations in Ghana, therefore, their contributions towards society should be taken

into considerations. Limited capacity, money and other resources may hinder SMEs from

adopting CSR into their business operations. SMEs might have adopted CSR at some level

of implementation, but this is however, need to be verified in the study. Social

26

responsibility is usually done in an informal way and sometimes unconsciously by SMEs. It

could be the terminology or definition of CSR itself that could hinder SMEs from truly

understands and engages in CSR (Jenkins 2005). CSR tools such as codes of conduct and

supply chain standards are usually excluding SMEs in developing countries (Fox 2005).

Therefore, there should be new ways in making CSR to be more relevant for SMEs. Jenkins

(2004) found that SMEs feel most pressure and influence on CSR matters from customers

and employees and barriers to CSR are time and money. Time, resources and delivery

pressures are often preventing SMEs in getting involved in what they see as new activities

(smekey.org). A recent study on social responsibility among SMEs in Ghana as

commissioned by the ACCA concluded that ―SMEs are more concerned with profitability

and less concerned with the impact of their operations on the community, customers and

employees.‖ (Tay 2006).

The commonly perceived barriers for SMEs in getting involved with CSR are:

1. Lack of time

2. Lack of motivation

3. Insufficient resources and capabilities

4. Not knowing how to encourage in social responsibility or inability to see suitable

Opportunity.

5. Not feeling in touch with local needs

6. Perception that community involvement is not related to business

Studies about SME practices in CSR are still inconclusive and limited.

2.4 Size of organisation

Haniffa & Cooke (2005) found that size of organisation influences the level of corporate

disclosure in the annual report. Large organisations undertake more activities and have

greater impact on society. Besides, larger organisations are susceptible to scrutiny by

27

various groups in society and thus, face greater pressure to disclose their social activities in

order to be legal and socially responsible (Cowen et al. 1987). In their study, Haniffa &

Cooke (2005) used total assets as proxy for size of organisation. Besides, size of

organisation can also be defined based on SMIDEC‘s (2006) definitions which use number

of full-time employees besides of annual sales turnover to differentiate between SMEs scale

and their nature of business. The discussion revealed the findings behind the results of

study.

2.5 CSR practices

The extent of CSR practices is compared among different organizational listing status.

These include government-linked corporations (GLC), multinational corporations (MNC),

local Ghanaian corporations (GC) and small and medium-sized enterprises (SME).

2.5.1 Government-linked corporations

Study found that GLC has a significant high policy adopted for workplace. Being

increasingly important as a strategy towards sustainable business development, CSR

practices by GLC are aimed to improve Ghanaian living and to ensure national

development. CSR is held as the principle of giving back to the society by contributing

profits generated for nation enhancement. Therefore, it can be seen that the motives for

GLC doing CSR is not far apart from its philanthropy reason.

2.5.2 Multinational corporations

MNC started with business philosophy as a principal and guideline towards CSR

implementation and would like to demonstrate economic, social and environmental

responsibilities that benefiting its stakeholders.

28

By operating in more than one country, MNC imposes greater impact and faces massive

pressures from more stakeholders. Countries whereby its people are highly socially

responsible may demand more CSR practices by MNC. Therefore, best CSR practices

initiated in countries in which CSR is an obligation and subjected to legal actions for non-

conformance might be adapted into the operation of MNC in other countries. This may

suggest the reason of high commitment exhibited by MNC as compared to other

organizational listing status in Ghana. In environmental policy, MNC leads other

organisations for almost the same reason for its highest commitment reported. Facing

pressures from environmental groups and government in some other countries, MNC

prefers the safe side by ensuring its operations has a minimal impact to the environment.

These practices are adopted as part of its environmental and safety practices in other

regional counterparts. Overall, it can be concluded that apart from philanthropic means,

MNC seems to avoid legal actions for non-conformance in CSR. Having good image is

posed as a motive by MNC by appeal pleasingly to various interest groups. Therefore,

MNC is found to be an excellent CSR performer.

2.5.3 Local Ghanaian Corporation

Currently, there are not many studies done on measuring the extent of CSR practices

among local companies.

2.6 Size of organisation and CSR practices

The extent of CSR practices varies among different size of industry. Larger organisations

tend to demonstrate more CSR activities rather than smaller organisation and is in

agreement with related findings by other researchers (Cohen et al. 1987; Haniffa & Cooke

2005). The reason behind this is larger organisations face greater pressure from society to

behave socially responsible and have greater impact on society. Besides, larger

29

organisations usually have better financial positions and thus, enable a considerable

numbers of CSR activities. Therefore, it can be concluded that larger organisation is usually

undertaking more CSR activities in order to remain responsible and sustainable.

2.7 EMPIRICAL STUDIES OF CSR AND FINANCIAL PERFORMANCE

According to Margolis and Walsh (2002), one hundred twenty-two published studies

between 1971 and 2001 empirically examined the relationship between corporate social

responsibility and financial performance. The first study was published by Narver in 1971.

Empirical studies of the relationship between CSR and financial performance comprise

essentially two types. The first uses the event study methodology to assess the short-run

financial impact (abnormal returns) when firms engage in either socially responsible or

irresponsible acts. The results of these studies have been mixed. Wright and Ferris (1997)

discovered a negative relationship; Posnikoff (1997) reported a positive relationship, while

Welch and Wazzan (1999) found no relationship between CSR and financial performance.

Other studies, discussed in McWilliams and Siegel (1997), are similarly inconsistent

concerning the relationship between CSR and short run financial returns.

The second type of study examines the relationship between some measure of corporate

social performance (CSP) and measures of long term financial performance, by using

accounting or financial measures of profitability. The studies that explore the relationship

between social responsibility and accounting-based performance measures have also

produced mixed results. Cochran and Wood (1984) located a positive correlation between

social responsibility and accounting performance after controlling for the age of assets.

Aupperle, Carroll, and Hatfield (1985) detected no significant relation between CSP and a

firm‘s risk adjusted return on assets. In contrast, Waddock and Graves (1997) found

significant positive relationships between an index of CSP and performance measures, such

as ROA in the following year. Studies using measures of return based on the stock market

30

also indicate diverse results. Vance (1975) refutes previous research by Moskowitz by

extending the time period for analysis from 6 months to 3 years, thereby producing results

which contradict Moskowitz and which indicate a negative CSP/CFP relationship.

However, Alexander and Buchholz (1978) improved on Vance‘s analysis by evaluating

stock market performance of an identical group of stocks on a risk adjusted basis, yielding

an inconclusive result.

2.8 Measures of Corporate Social Responsibility

Determining how social and financial performances are connected is further complicated by

the lack of consensus of measurement methodology as it relates to corporate social

performance. In many cases, subjective indicators are used, such as a survey of business

students (Heinze, 1976), or business faculty members (Moskowitz, 1972), or even the

Fortune rankings (McGuire, Sundgren, and T. Schneeweis 1988; Akathaporn and McInnes,

1993; Preston and O‘Bannon, 1997). Significantly, it is unclear exactly what these

indicators measure. In other cases, researchers employ official corporate disclosures—

annual reports to shareholders, CSR reports, or the like. Despite the popularity of these

sources, there is no way to determine empirically whether the social performance data

revealed by corporations are under-reported or over-reported. Few companies have their

SCR reports externally verified. Thus, information about corporate social performance is

open to questions about impression management and subjective bias. Still other studies use

survey instruments (Aupperle, 1991) or behavioral and perceptual measures (Wokutch and

McKinney, 1991). Waddock and Graves (1997) drew upon the Kinder Lydenberg Domini

(KLD) rating system, where each company in the S& P 500 is rated on multiple attributes

considered relevant to CSP. KLD uses a combination of surveys: financial statements,

articles on companies in the popular press, academic journals (especially law journals), and

government reports in order to assess CSP along eleven dimensions1. Based on this

31

information, KLD constructed the Domini 400 Social Index (DSI 400), the functional

equivalent of the Standard and Poors 500 Index, for socially responsible firms.

2.8.1 Measures of Financial Performance

Although measuring financial performance is considered a simpler task, it also has it

specific complications. Here, too, there is little consensus about which measurement

instrument to apply. Many researchers use market measures (Alexander and Buchholz,

1978; Vance, 1975), others put forth accounting measures (Waddock and Graves 1997;

Cochran and Wood 1984) and some adopt both of these (McGuire, Sundgren, Schneeweis,

1988). The two measures, which represent different perspectives of how to evaluate a

firm‘s financial performance, have different theoretical implications (Hillman and Keim,

2001) and each is subject to particular biases (McGuire, Schneeweis, & Hill, 1986). The

use of different measures, needless to say, complicates the comparison of the results of

different studies. In other words, accounting measures capture only historical aspects of

firm performance (McGuire, Schneeweis, & Hill, 1986). They are subject, moreover, to

bias from managerial manipulation and differences in accounting procedures (Branch,

1983; Brilloff, 1972). Market measures are forward looking and focus on market

performance.

2.9 CONCLUSIONS AND IMPLICATIONS

There is an extensive debate concerning the legitimacy and value of being a socially

responsible business. There are different views of the role of a firm in society and

disagreement as to whether wealth maximization should be the sole goal of a corporation.

Most people identify certain benefits for a business being socially responsible, but most of

these benefits are still hard to quantify and measure. Arguments exist that support the view

that firms which have solid financial performance have more resources available to invest

in social performance domains, such as employee relations, environmental concerns, or

community relations. Financially strong companies can afford to invest in ways that have a

32

more long-term strategic impact, such as providing services for the community and their

employees. Those allocations may be strategically linked to a better public image and

improved relationships with the community in addition to an improved ability to attract

more skilled employees. On the other hand, companies with financial problems usually

allocate their resources in projects with a shorter horizon. This theory is known as slack

resources theory (Waddock and Graves, 1997). Other arguments propose that financial

performance also depends on good or socially responsible performance. According to

Waddock and Graves (1997), meeting stakeholder expectations before they become

problematic indicates a proactive attention to issues that otherwise might cause problems or

litigation in the future. Furthermore, socially responsible companies have an enhanced

brand image and a positive reputation among consumers; they also have the ability to

attract more accomplished employees and business partners. Socially responsible

companies also have less risk of negative rare events. Companies that adopt the CSR

principles are more transparent and have less risk of bribery.

2.11 FUTURE RESEARCH

Future research in this area could proceed in a number of directions. First, more extensive

studies are needed to explore the causal mechanisms linking CSR to profitability and to

determine whether or not those relationships hold consistently over time. The source of the

connection between CSR and profitability has rarely been systematically investigated. It is

also important to position the timing in the relationship, since it would be valuable to

investigate and to ascertain how long it takes for the impact of CSR on financial

performance to be revealed. For the above to be realized, more data on CSR should become

available. The reliability of the CSR data is also an important issue, as data from different

sources have significant differences regarding how to evaluate the CSR performance of a

firm.

33

2.12 Corporate Social Responsibility in Nestle Ghana.

Long before such activities became popularly known as Corporate Social Responsibility

(CSR) and long before it became essential for companies to engage in CSR as part of

their brand building agenda, Nestle Ghana have been making regular, substantial

contributions to the wellbeing of grassroots communities and Ghanaians.

Nestle 's CSR strategy reflects their commitment to being socially, economically, and

culturally responsible. With a resolve to provide sustainable solutions to the diverse

developmental challenges that Ghanaians encounter on various fronts, the Organisation

pursues constructive engagements and mutual partnerships with the recipient

stakeholders, through a user-defined needs identification system.

Nestle 's CSR is accentuated by sustained aspiration to lead the industry by example not

just in the provision of the best products, services and developmental assistance for

promoting the individual and common good, but also in maintaining the highest standards

of corporate governance, accountability and responsiveness to their internal and external

stakeholders.

Nestle organization‘s CSR initiatives, have provided targeted support for education and

youth development, grassroots sports development, healthcare, arts and culture,

entrepreneurial and economic development, as well as sustainability of the environment.

Fig 2.1: Nestle in the society

Source: Community.Nestle.com.

34

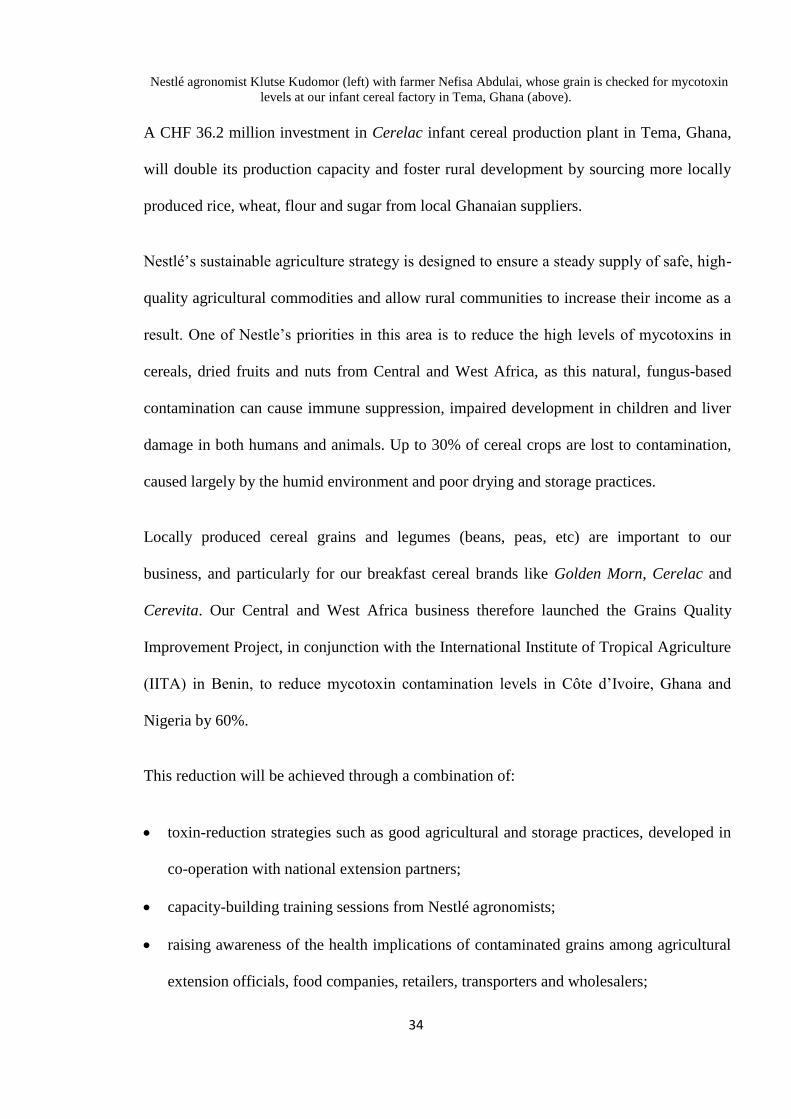

Nestlé agronomist Klutse Kudomor (left) with farmer Nefisa Abdulai, whose grain is checked for mycotoxin

levels at our infant cereal factory in Tema, Ghana (above).

A CHF 36.2 million investment in Cerelac infant cereal production plant in Tema, Ghana,

will double its production capacity and foster rural development by sourcing more locally

produced rice, wheat, flour and sugar from local Ghanaian suppliers.

Nestlé‘s sustainable agriculture strategy is designed to ensure a steady supply of safe, high-

quality agricultural commodities and allow rural communities to increase their income as a

result. One of Nestle‘s priorities in this area is to reduce the high levels of mycotoxins in

cereals, dried fruits and nuts from Central and West Africa, as this natural, fungus-based

contamination can cause immune suppression, impaired development in children and liver

damage in both humans and animals. Up to 30% of cereal crops are lost to contamination,

caused largely by the humid environment and poor drying and storage practices.

Locally produced cereal grains and legumes (beans, peas, etc) are important to our

business, and particularly for our breakfast cereal brands like Golden Morn, Cerelac and

Cerevita. Our Central and West Africa business therefore launched the Grains Quality

Improvement Project, in conjunction with the International Institute of Tropical Agriculture

(IITA) in Benin, to reduce mycotoxin contamination levels in Côte d‘Ivoire, Ghana and

Nigeria by 60%.

This reduction will be achieved through a combination of:

toxin-reduction strategies such as good agricultural and storage practices, developed in

co-operation with national extension partners;

capacity-building training sessions from Nestlé agronomists;

raising awareness of the health implications of contaminated grains among agricultural

extension officials, food companies, retailers, transporters and wholesalers;

35

paying price premiums to farmers for mycotoxin-free produce.

In 2008/09, 10 000 trained farmers produced grains with mycotoxin levels within Nestlé

standards (four parts per billion) and in 2010, the number rose to 30 000 farmers. The

management and control of mycotoxins is supported by an awareness campaign and greater

stakeholder dialogue, delivered through leaflets, newsletters and even pictorial guides for

illiterate farmers, which are intended to make food companies, retailers and wholesalers, as

well as farmers, more aware of the health implications of mycotoxin contamination.

The 10 million trees will help to reduce deforestation by replacing 10 000 hectares of old

cocoa trees over a decade, each of which will yield three times more cocoa beans. The

potential of the propagated varieties is between 1.5 and 2.5 tonnes per hectare, and annual

farmers‘ income has the potential to rise from USD 480 per hectare to USD 1800.

Taken together, the potential yield, the technical training of more than 30 000 cocoa

farmers, the premiums paid for good quality and the social projects funded via The Cocoa

Plan will improve the social environment of farmers and increase the supply of better

quality beans to Nestlé‘s factories.

2.13 The Impact of Corporate Social Responsibility.

CSR is a required investment to create sustainable development for the business, because it

offers the companies (MNCs) an opportunity to bridge the ―trust gap‖ among different

stakeholders such as, government, customers, employees, suppliers, investors, and others.

Some of the impact of CSR includes:

To the company:

Ajala (2005) says: ―CSR programmes offer opportunity to build goodwill, affect corporate

image and reputation as a result of company‘s contribution to the welfare of the

36

community, either local or international‖. She added that CSR enhances growth of

investors‘ confidence in the company‘s shares.

A firm that consistently fulfil its social obligations makes itself a welcomed member of the

community and this may attract customer both home and aboard.

– Social and human pressure. These have induced contending demand and requests on

MNCs in the face of financial constraints. Today, the outlook of Ghanaian MNCs is no

more measured by, ―local standards‖, but by international standards. Often, the inability of

MNCs to satisfy these demands have resulted in disappointments and eventually to,

―organisation bashing‖;

– Inadequate information to the public on the modalities and essence of CSR as

– well as the achievements of MNCs in this regard. Many believe that MNCs are not

doing enough to improve the welfare of the public in view of the supposedly ―jumbo

profits‖ they make;

– Inability of MNCs to co-ordinate efforts and collaborate to execute CSR projects,

particularly the capital intensive ones, such as road construction.

37

CHAPTER THREE

RESEARCH METHODOLOGY

3.1 INTRODUCTION

According to Oni (2003), research methodology is used to describe all the methods

involved in the collection of all information required for a study. This chapter contains

research design, population and sampling size, research instrument, validity and reliability

of data, measurement of variable, data analysis technique, limitations of the research

methodology of the study.

3.2 RESEARCH DESIGN

Research design is the structuring of investigation aimed at identifying variables and their

relationship to one another. This is used for the purpose of obtaining data to enable the

researcher test hypothesis or answer research questions. It is an outline or scheme that

serves as a guide to the researcher in his effort to generate data for his study. In this study,

the research design used is the survey design. A survey research design is one in which the

sample subject and variables that are being studied are simply being observed as they are

without any attempt to control or manipulate them (Ojo 2003). The survey research design

is aimed at discovering the inter-relationship between variables. Questionnaires was used as

the instrument of gathering information from knowledgeable respondents and also going

beyond the observation of the correlation between independent and dependent variables.

3.3 POPULATION AND SAMPLE SIZE

The study population is very large, so 100 respondents were selected from the top level

management, middle level management and the supervisors which should be a good

representation of the population based on stratified sampling. This cuts across the various

departments in the organisation such as corporate affair department, customer services

department, retail department, marketing department and others. Again 300 customers were

38

selected from customers through random sampling. Finally five(5) business partners of

Nestle were interviewed on face to face discussions to solicit their views on the subject of

the study. In all 405 respondents were used for the research.

3.4 RESEARCH INSTRUMENT

The instrument used for the collection of data for the purpose of this study were

questionnaires and face to face interviews. The questionnaires contain relevant questions

for the purpose of this study. The data obtained from completed questionnaires were

analyzed and used.

3.5 VALIDITY OF THE RESEARCH INSTRUMENT

To ensure that the study instrument is valid and reliable, as the quality of a research largely

depends on the quality of the instruments used and procedures of collecting the data since

the two essentials of a good research are validity and reliability, the researcher ensured that

the questions designed are based on the following guidelines:

The questions were formed in such a way as to make it easy for respondents to

understand them

The questions asked were as few in number as necessary to produce the information

required..

The questions required answers that were very straight forward and precise in

nature.

The questions are directly related to the information required.

The questions were such that could be answered honestly and without bias.

Since validity is the extent to which the instrument used measures what it was intended to

measure, the accuracy of a research instrument being reliable is whether the data collection

process is consistent and stable.

39

3.6 DATA ANALYSIS TECHNIQUE

The statistical techniques employed in analyzing data collected in this study are:

TABLES

Tables effectively order and summarize the quantitative data. They are used to arrange

facts and figures in columns and rows. These facts and figures can be systematically

examined. (Ojo, 2005)

PERCENTAGES

These are used in translating frequency counts into percentage. These percentages were

used to show the distribution of respondents according to their responses. (Ojo, 2005)

CORRELATIONAL ANALYSIS

The Pearson product-moment correlation coefficient (sometimes referred to as the

PMCC, and typically denoted by r) is a measure of the correlation (linear dependence)

between two variables X and Y, giving a value between +1 and −1 inclusive. It is used as

a measure of the strength of linear dependence between two variables. According to Ojo

(2005) PMCC is used to find out if there is any relationship between two variables. While

doing this, a variable is regressed to another variable.

When increase in variable X leads to an increase in variable Y; we say there is a positive

correlation. If vice versa it is negative. (Ojo, 2005)

Product moment correlation coefficient (r) is given as;

Where: r = Pearson‘s Product Moment correlation.

∑n= Number of pairs of values

X = Independent variable (CSR)

X = Mean of independent variable (CSR)

40

Y = Dependent variable (Profitability)

Y = Mean of dependent variable (Profitability).

Interpretation:

The correlation coefficient ranges from −1 to 1. A value of 1 implies that a linear

equation describes the relationship between X and Y perfectly, with all factors affecting Y

held constant for which Y increases as X increases. A value of −1 implies Y decreases as

X increases. A value of 0 implies that there is no linear correlation between the variables.

41

CHAPTER FOUR

DATA PRESENTATION, ANALYSIS AND INTERPRETATION

4.1 INTRODUCTION

This chapter deals with presentation, analysis and interpretation of the data collected

from the field by means of questionnaire as well as those collected from secondary

sources (annual report) to show the impact of corporate social responsibility of the

profitability on multinational companies in Ghana.

4.2. DATA PRESENTATION AND ANALYSIS

4.2.1 QUESTIONNAIRE TO STAFF:

The table shows the suggested answer and the numbers of respondents with the

percentage of the respondent to each.

DESCRIPTIVE STATISTICS:

Section A

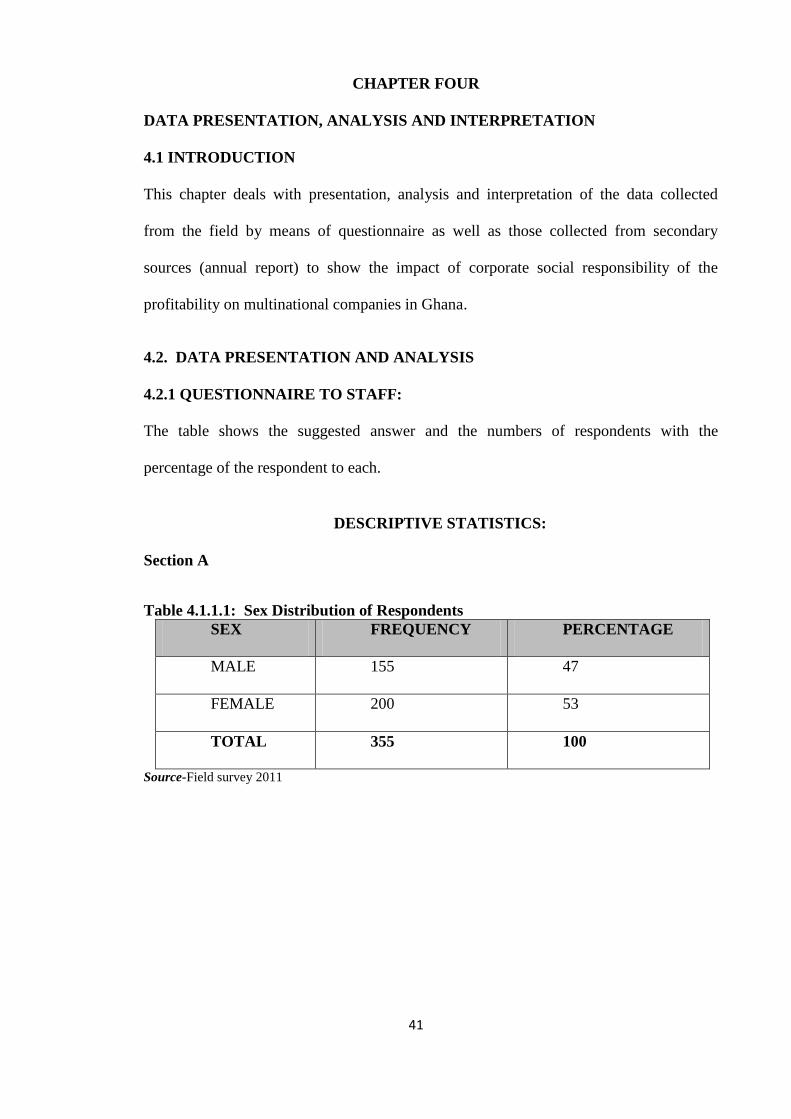

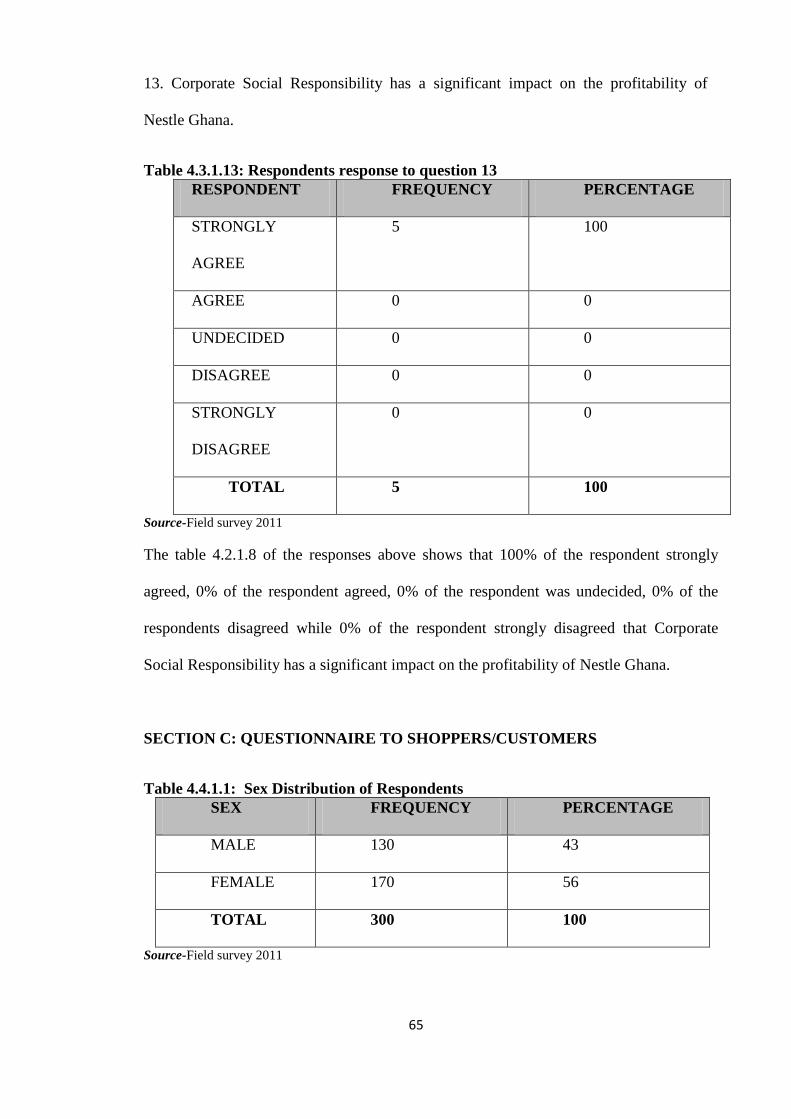

Table 4.1.1.1: Sex Distribution of Respondents

SEX FREQUENCY PERCENTAGE

MALE 155 47

FEMALE 200 53

TOTAL 355 100

Source-Field survey 2011

42

Graphical representation of the Nestle staff respondents

Fig: 4.1 Gender distribution of Nestle Staff (pie chart)

Source-Field survey 2011

Fig: 4..2 Gender distribution of Nestle Staff (bar chart)

Source-Field survey 2011

The table 4.1.1.1 reveals that 40 (47%) of the respondents are male while 46 (53%) are

females, indicating that the organization has a fairly favorable policy towards the

employment of women.

47%

53%

Gender Frequency (%)

male

female

36

38

40

42

44

46

male female

Gender Frequency - %

Frequency

43

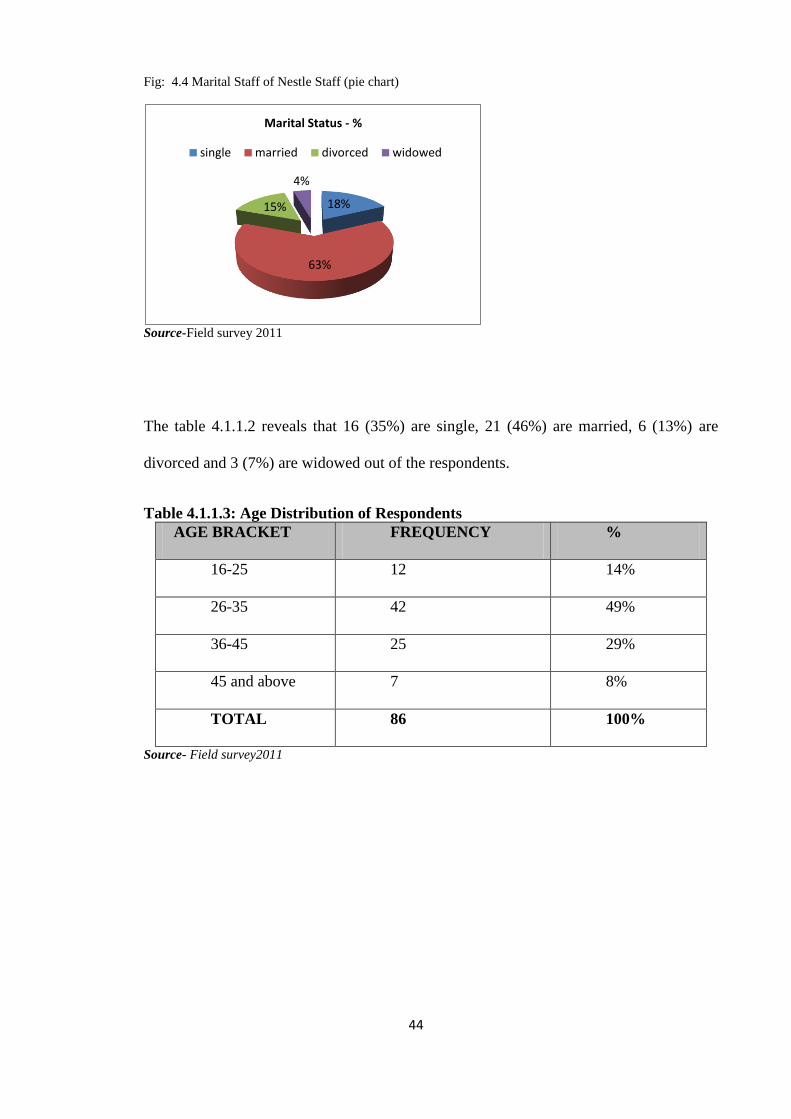

Table 4.1.1.2: Marital Status of Respondents

MARITAL STATUS FREQUENCY %

SINGLE 31 36

MARRIED 42 49

DIVORCED 10 12

WIDOWED 3 3

TOTAL 86 100

Source- Field survey 2011

Fig: 4.3 Marital Status of Nestle Staff (bar chart)

Source-Field survey 2011

0

10

20

30

40

50

Marital Status

Frequency

%

44

Fig: 4.4 Marital Staff of Nestle Staff (pie chart)

Source-Field survey 2011

The table 4.1.1.2 reveals that 16 (35%) are single, 21 (46%) are married, 6 (13%) are

divorced and 3 (7%) are widowed out of the respondents.

Table 4.1.1.3: Age Distribution of Respondents

AGE BRACKET FREQUENCY %

16-25 12 14%

26-35 42 49%

36-45 25 29%

45 and above 7 8%

TOTAL 86 100%

Source- Field survey2011

18%

63%

15%

4%

Marital Status - %

single married divorced widowed

45

Fig: 4.5 Age distribution of Nestle Staff (bar chart)

Source-Field survey 2011

Fig: 4.6 Age distribution of Nestle Staff (pie chart)

Source-Field survey 2011

The table 4.1.1.3 reveals that 12(14%) of the respondent are within the ages of 15-25,

42(49%) are within the ages of 26-35, 25(37%) are within the ages of 36-45 and 7 (8%)

are within the ages of 45 and above..

Table 4.1.1.4: Respondents’ Job Levels

STATUS/POSITION FREQUENCY %

Low level manager 12 14

Middle level manager 67 78

0

10

20

30

40

50

16-25 26 -35 36 -45 above 45

Age Brackets Frequency - %

Frequency

%

14%

49%

29%

8%

Age Distribution Frequency (%)

16-25 26 -35 36 -45 above 45

46

Top level manager 7 8

TOTAL 86 100

Source- Field survey 2011

Fig: 4.7 Position distribution of Nestle Staff (bar chart)

Source- Field survey 2011

Fig: 4.8 Position distribution of Nestle Staff (pie chart)

Source- Field survey 2011

The table 4.1.1.4 reveals that 12 (14%) of the respondents are low level managers, 67

(78%) are middle level managers and 7 (8%) are Top level managers.

0

20

40

60

80

Lower level manager

middle level manager

top level manager

Position Frequency - %

Frequency %

14%

78%

8%

Position Frequency - %

Lower level manager middle level manager

top level manager

47

Table 4.1.1.5: Work Experience Distribution of Respondents

LENGTH OF TIME FREQUENCY %

Less than a decade 57 66

A decade and more 29 34

TOTAL 86 100

Source- Field survey 2011

The table 4.1.1.5 reveals that 57 (66%) respondents have less than a decade work

experience while 29(34%) have a decade and more work experience with Nestle Ghana.

The implies that information obtained from the questionnaire were from staff who have

gained sufficient experiences from Nestle Ghana, making the information reliable

Table 4.1.1.6: Education Qualification Distribution of Respondents

QUALIFICATION FREQUENCY %

SSCE 8 9

HND 20 24

B.sc 25 29

BA 12 14

MBA/M.sc 13 15

Others 8 9

TOTAL 86 100%

Source: Field survey 2011

48

Fig: 4.8 Work experience distribution of Nestle Staff (bar chart)

Source- Field survey 2011

Fig: 4.9 Work experience distribution of Nestle Staff (pie chart)

Source- Field survey 2011

0

5

10

15

20

25

30

Staff Qualifications

Frequency

%

10%

23%

29%

14%

15%

9%

Qualifications

SSCE

HND

BSC

BA

MBA/Msc

Others

49

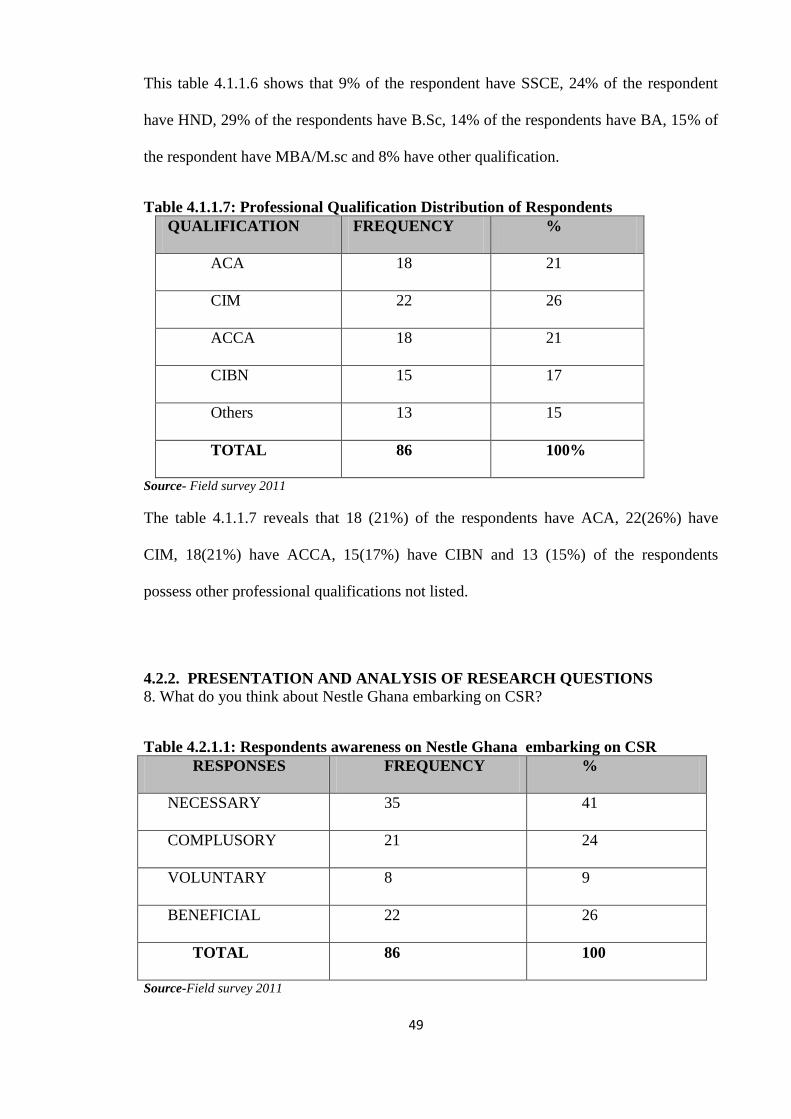

This table 4.1.1.6 shows that 9% of the respondent have SSCE, 24% of the respondent

have HND, 29% of the respondents have B.Sc, 14% of the respondents have BA, 15% of

the respondent have MBA/M.sc and 8% have other qualification.

Table 4.1.1.7: Professional Qualification Distribution of Respondents

QUALIFICATION FREQUENCY %

ACA 18 21

CIM 22 26

ACCA 18 21

CIBN 15 17

Others 13 15

TOTAL 86 100%

Source- Field survey 2011

The table 4.1.1.7 reveals that 18 (21%) of the respondents have ACA, 22(26%) have

CIM, 18(21%) have ACCA, 15(17%) have CIBN and 13 (15%) of the respondents

possess other professional qualifications not listed.

4.2.2. PRESENTATION AND ANALYSIS OF RESEARCH QUESTIONS

8. What do you think about Nestle Ghana embarking on CSR?

Table 4.2.1.1: Respondents awareness on Nestle Ghana embarking on CSR

RESPONSES FREQUENCY %

NECESSARY 35 41

COMPLUSORY 21 24

VOLUNTARY 8 9

BENEFICIAL 22 26

TOTAL 86 100

Source-Field survey 2011

50

Fig: 4.10 View on if Nestle embarks on CSR - Nestle Staff (bar chart)

Source- Field survey 2011

Fig: 4.11 View on if Nestle embarks on CSR - Nestle Staff (pie chart)

Source- Field survey 2011

The table 4.1.2.1 shows that 41% of the respondents feel that Nestle Ghana embarking on

CSR is necessary, 24% feel it is compulsory, 9% feel it is voluntary and 26% felt it is

beneficial.

9. What impact has the project / programme had on the community?

0

10

20

30

40

50

Respondents view on CSR

frequency

%

41%

24%

9%

26%

Respondents view on CSR

necessary compulsory voluntary beneficiary

51

Table 4.2.1.2: Respondent responds to impact of the CSR projects/programme on

the community

RESPONSES FREQUENCY %

Positive 70 81

Negative 0 0

Neutral 16 19

TOTAL 86 100

Source-Field survey 2011

The table 4.1.2.2 above reveals that a high proportion (81%) of the respondents felt the

impact of CSR is positive, none of the respondents felt it is negative and 19% felt it is

neutral.

10. Are there other benefits Nestle Ghana stands to gain aside profitability from the

execution of CSR projects?

Table 4.2.1.3: Respondent responds about other benefits Nestle Ghana stands to

gain apart from profitability

RESPONSES FREQUENCY %

Large Customer

Base

43 50

Customer

Confidence

22 26

Good corporate

Image

15 17

Other Benefits 6 7

TOTAL 86 100%

Source- Field survey 2011

52

Fig: 4.12 Views of the benefits of CSR - Nestle Staff (bar chart)

Source- Field survey 2011

Fig: 4.13 Views of the benefits CSR - Nestle Staff (pie chart)

Source- Field survey 2011

From the table 4.1.2.3 above, 50% of the respondent believes Nestle Ghana also benefit

Large Customer Base, 26% believes it will have Customer Confidence, 17% believes

Good Corporate Image and only 7% believes other benefit could be gained from the

execution of CSR projects apart from Profitability.

11. Profit is increased by the activity of corporate social responsibility of the company?

0

10

20

30

40

50

large customer

base

customer confidence

good corporate

image

other benefits

Respondents view of benefits of CSR

frequency

%

50%

26%

17%

7%

CSR Benefit - Percentage

Large Customer base Customer Confidence

Good Corporate Image Other Benefit

53

Table 4.2.1.4: Respondent response to question 11

RESPONDENT FREQUENCY %

STRONGLY AGREE 23 27

AGREE 37 43

UNDECIDED 15 17

DISAGREE 11 13

STRONGLY

DISAGREE

0 0

TOTAL 86 100

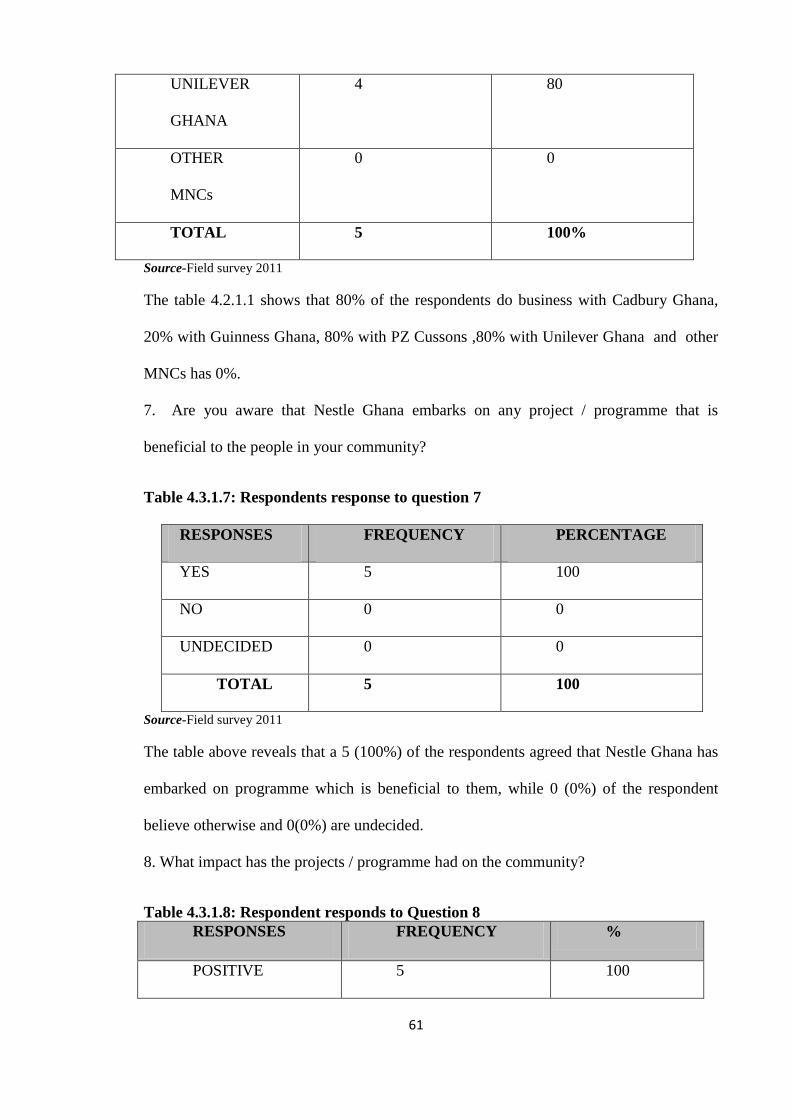

Source- Field survey 2011

Fig: 4.14 Respondents view of how CSR increases the firms profitability.(bar chart)

Source- Field survey 2011

05

1015202530354045

Respondents view of increased profits from CSR

frequency

%

54

Fig: 4.15 Respondents view of how CSR increases the firms profitability. (pie chart)

Source- Field survey 2011

The table 4.1.2.4 above shows that 27% of the respondent strongly agreed, 43% of the

respondent agreed, 17% of the respondent were undecided, 13% of the respondents

disagreed while 0% of the respondent strongly disagreed that Profit is increased by the

activity of corporate social responsibility of the company. Though I couldn‘t gain access

to the records but Nestle Ghana result shows increase in profitability.

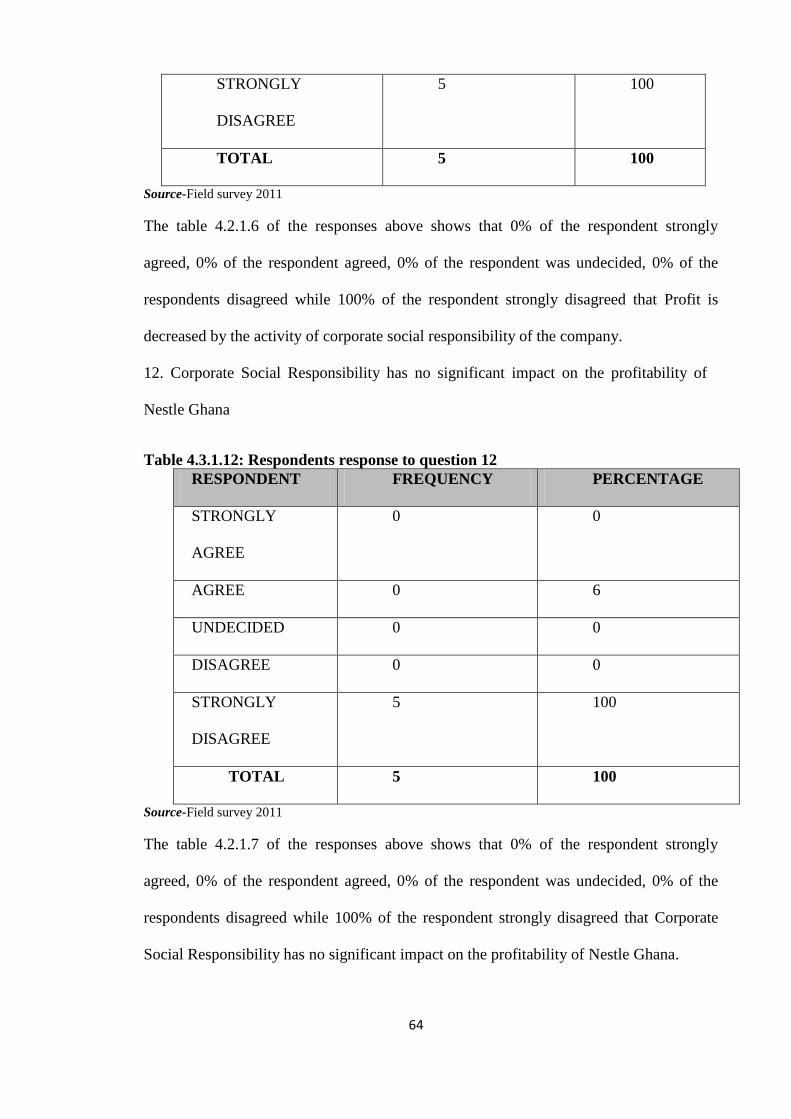

12. Profit is decreased by the activity of corporate social responsibility of the company?

Table 4.2.1.5: Respondent response to question 12

RESPONDENT FREQUENCY %

STRONGLY AGREE 0 0

AGREE 9 10

UNDECIDED 17 20

DISAGREE 47 55

strongly agree27%

agree43%

undecided17%

disagree13%

strongly disagree

0%

Respondents view of increased profits from CSR

55

STRONGLY

DISAGREE

13 15

TOTAL 86 100%

Source- Field survey 2011

Fig: 4.16 Respondents view if CSR decreases the firms profitability. (pie chart)

Source- Field survey 2011

Fig: 4.17 Respondents view if CSR decreases the firms profitability. (bar chart)

Source- Field survey 2011

0

10

20

30

40

50

60

Respondents view if CSR decrease profit

frequency

%

Respondents view if CSR decrease profit

strongly agree

agree

undecided

disagree

strongly disagree

56

The table 4.1.2.5 above shows that 0% of the respondent strongly agreed, 10% of the

respondent agreed, 20% of the respondent were undecided, 55% of the respondents

disagreed while 15% of the respondent strongly disagreed that Profit is decreased by the

activity of corporate social responsibility of the company.

13. Corporate Social Responsibility has no significant impact on the profitability of

Nestle Ghana ?

Table 4.2.1.6 Respondent response to question 13

RESPONDENT FREQUENCY %

STRONGLY

AGREE

0 0

AGREE 9 10

UNDECIDED 11 13

DISAGREE 48 56

STRONGLY

DISAGREE

18 21

TOTAL 86 100

Source-Field survey 2011

The table 4.1.2.6 shows that 0% of the respondent strongly agreed, 10% of the respondent

agreed, 13% of the respondent were undecided, 56% of the respondents disagreed while

21% of the respondent strongly disagreed that Corporate Social Responsibility has no

significant impact on the profitability of Nestle Ghana. This means that majority believe

that CSR has a significant impact on the profitability of Nestle Ghana

14. Corporate Social Responsibility has a significant impact on the profitability of

Nestle Ghana?

57

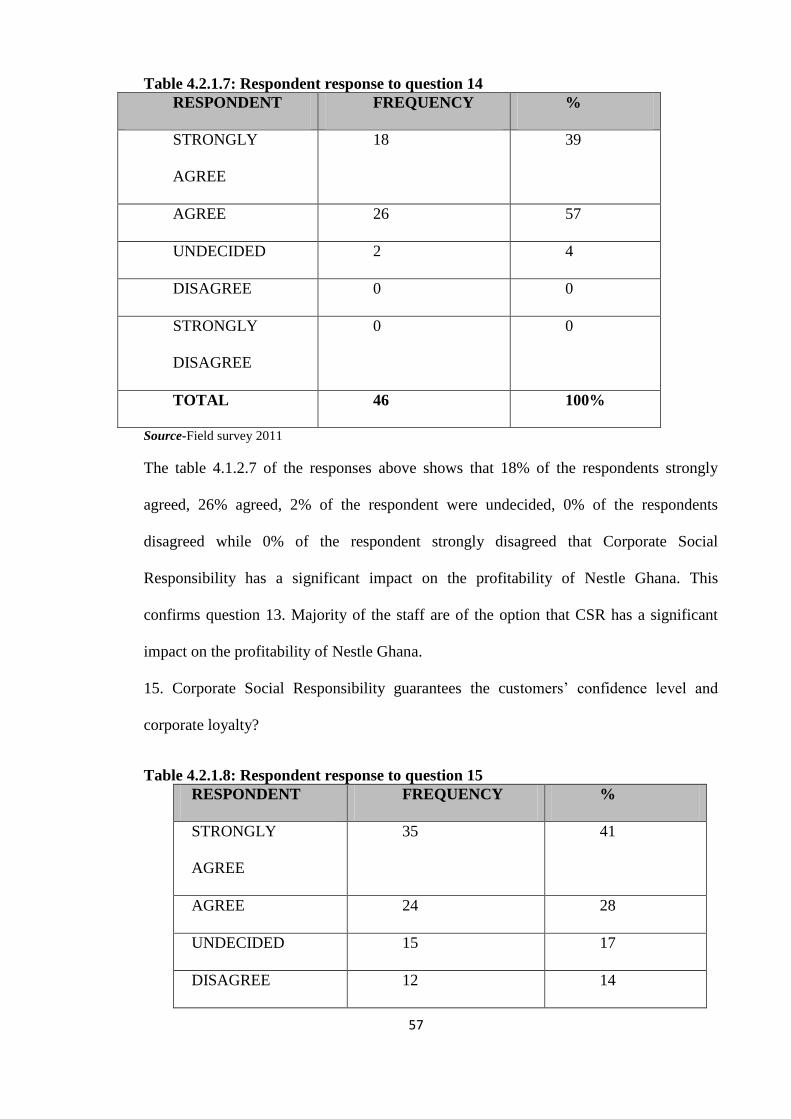

Table 4.2.1.7: Respondent response to question 14

RESPONDENT FREQUENCY %

STRONGLY

AGREE

18 39

AGREE 26 57

UNDECIDED 2 4

DISAGREE 0 0

STRONGLY

DISAGREE

0 0

TOTAL 46 100%

Source-Field survey 2011

The table 4.1.2.7 of the responses above shows that 18% of the respondents strongly

agreed, 26% agreed, 2% of the respondent were undecided, 0% of the respondents

disagreed while 0% of the respondent strongly disagreed that Corporate Social

Responsibility has a significant impact on the profitability of Nestle Ghana. This

confirms question 13. Majority of the staff are of the option that CSR has a significant

impact on the profitability of Nestle Ghana.

15. Corporate Social Responsibility guarantees the customers‘ confidence level and

corporate loyalty?

Table 4.2.1.8: Respondent response to question 15

RESPONDENT FREQUENCY %

STRONGLY

AGREE

35 41

AGREE 24 28

UNDECIDED 15 17

DISAGREE 12 14

58

STRONGLY

DISAGREE

0 0

TOTAL 86 100

Source-Field survey 2011

The table 4.1.2.8 of the responses above shows that 41% of the respondents strongly

agreed, 28% agreed, 17% of the respondent were undecided, 14% of the respondents

disagreed while 0% of the respondent strongly disagreed that Corporate Social

Responsibility guarantees the customers‘ confidence and security of depositors‘ fund.

Section B

4.3 QUESTIONNAIRE TO EXTERNAL STAKEHOLDERS

The table shows the suggested answer and the numbers of respondents with the

percentage of the respondent to each.

DESCRIPTIVE STATISTICS:

Table 4.3.1.1 Sex Distribution of Respondents

SEX FREQUENCY PERCENTAGE

MALE 2 40

FEMALE 3 60

TOTAL 5 100

Source-Field survey 2011

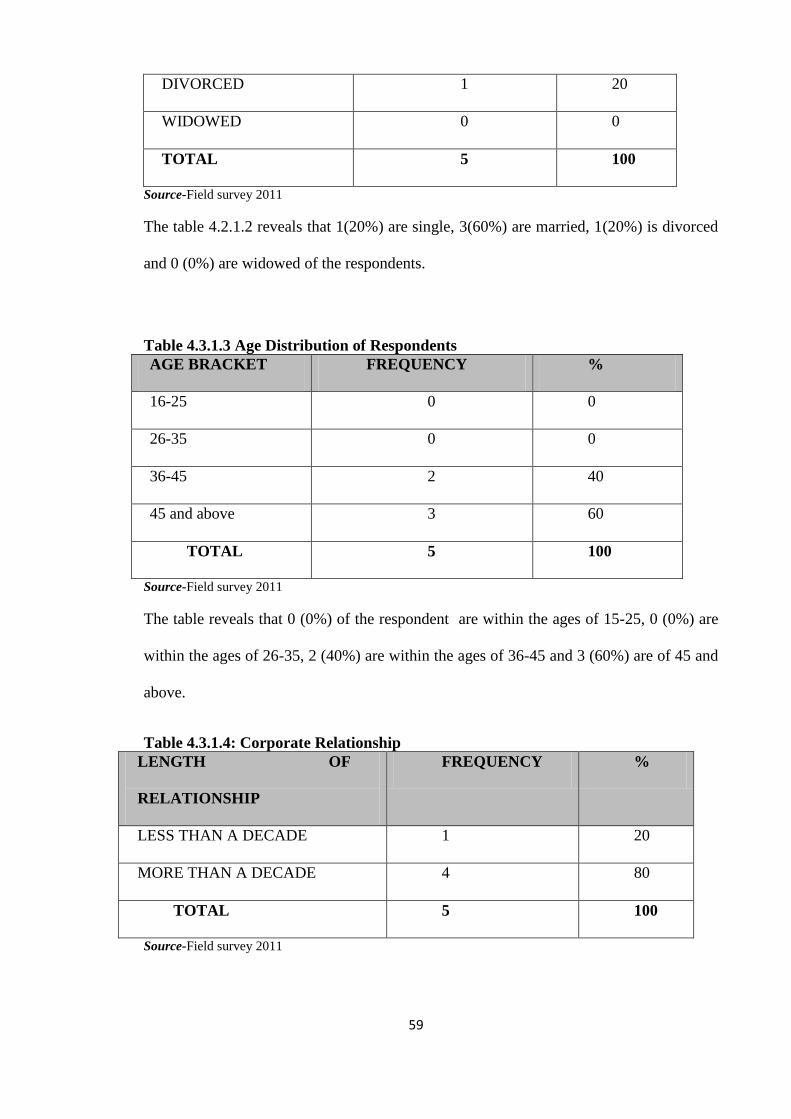

The table 4.2.1.1 reveals that 2 (40%) of the respondent are male while other 3(60%) are

females.

Table 4.3.1.2 Marital Status Distribution of Respondents

MARITAL STATUS FREQUENCY %

SINGLE 1 20

MARRIED 3 60